smeda paper board manufacturing unit

TRANSCRIPT

Pre-Feasibility Study

PPAAPPEERR BBOOAARRDD MMAANNUUFFAACCTTUURRIINNGG UUNNIITT

Small and Medium Enterprise Development AuthorityGovernment of Pakistan

www.smeda.org.pk

HEAD OFFICE

6th & 8th Floor LDA Plaza, Egerton Road, Lahore.Tel: (042) 111-111-456Fax: (042) 6304926-7

REGIONAL OFFICE PUNJAB

REGIONAL OFFICE SINDH

REGIONAL OFFICE NWFP

REGIONAL OFFICE BALOCHISTAN

8th Floor LDA Plaza, Egerton Road, Lahore.Tel: (042) 111-111-456Fax: (042) [email protected]

5TH Floor, BahriaComplex II, M.T. Khan Road,

Karachi.Tel: (021) 111-111-456

Fax: (021) [email protected]

Ground FloorState Life Building

The Mall, Peshawar.Tel: (091) 9213046-47

Fax: (091) [email protected]

Bungalow No. 15-AChaman Housing Scheme

Airport Road, Quetta.Tel: (081) 831623, 831702

Fax: (081) [email protected]

June, 2006

Pre-feasibility Study Paper Board Manufacturing Unit

1

1 PURPOSE OF THE DOCUMENT............................................................................................... 4

2 CRUCIAL FACTORS & STEPS IN DECISION MAKING FOR INVESTMENT..................... 4

2.1 SWOT ANALYSIS ................................................................................................................... 42.1.1 STRENGTH....................................................................................................................... 42.1.2 WEAKNESSES................................................................................................................... 52.1.3 OPPORTUNITIES ............................................................................................................. 52.1.4 THREATS.......................................................................................................................... 5

2.2 KEY SUCCESS FACTORS / PRACTICAL TIPS FOR SUCCESS .......................................................... 6

3 PROJECT PROFILE.................................................................................................................... 7

3.1 OPPORTUNITY RATIONALE ...................................................................................................... 73.2 PROJECT BRIEF ....................................................................................................................... 73.3 MARKET ENTRY TIMING ......................................................................................................... 73.4 PROPOSED BUSINESS LEGAL STATUS ....................................................................................... 73.5 PROJECT CAPACITY AND RATIONALE....................................................................................... 73.6 PROJECT INVESTMENT............................................................................................................. 83.7 PROPOSED LOCATION.............................................................................................................. 8

4 PAPER & PAPER BOARD .......................................................................................................... 9

4.1 PAPER .................................................................................................................................. 94.2 PAPERBOARD ................................................................................................................... 104.3 RECYCLING OF PAPER & PAPER BOARD ...................................................................... 104.4 REGULATIONS TO PAPER & PAPER BOARD ................................................................. 11

4.4.1 Custom Duties and Taxes................................................................................................. 114.4.2 Environmental Technology / Quality Issues ...................................................................... 11

5 RAW MATERIAL ...................................................................................................................... 12

5.1 AVAILABILITY OF RAW MATERIAL.............................................................................. 125.1.1 Wood based material ....................................................................................................... 125.1.2 Agricultural wastes .......................................................................................................... 125.1.3 Other Raw Material ......................................................................................................... 12

5.2 PLUPING CHEMICALS...................................................................................................... 135.3 BOX BOARD MAKING CHEMICALS ............................................................................... 135.4 OTHER CONSUMABLE MATERIALS .............................................................................. 13

6 MARKET INFORMATION ....................................................................................................... 13

6.1 MARKET DEMAND........................................................................................................... 156.2 FACTORS AFFECTING DEMAND AND SUPPLY ............................................................ 15

6.2.1 Demand........................................................................................................................... 156.2.2 Future Demand................................................................................................................ 166.2.3 Supply ............................................................................................................................. 166.2.4 Demand and Supply Scenario........................................................................................... 176.2.5 Imports of Paper and Paper Board Products .................................................................... 186.2.6 Import of Pulp & Paper Board......................................................................................... 186.2.7 Import of Wood Pulp........................................................................................................ 186.2.8 Import of Waste Paper ..................................................................................................... 19

6.3 INTERNATIONAL SCENARIO.......................................................................................... 196.4 PAPER BOARD INSUSTRY AND WTO............................................................................. 19

7 PRODUCTION PROCESS......................................................................................................... 21

7.1 BOX BOARD MANUFACTURING .................................................................................... 217.2 PRODUCTION METHODS AND TECHNOLOGY ............................................................. 21

7.2.1 Recycling Process............................................................................................................ 22

Pre-feasibility Study Paper Board Manufacturing Unit

2

7.2.2 Grades of Recovered Paper & Paper Board..................................................................... 227.3 FLOW CHART FOR BOX BOARD MANUFACTURING ................................................... 247.4 PLANT LAYOUT .................................................................................................................... 257.5 MACHINERY REQUIREMENT .................................................................................................. 267.6 OTHER FIXED ASSETS REQUIREMENT .................................................................................... 27

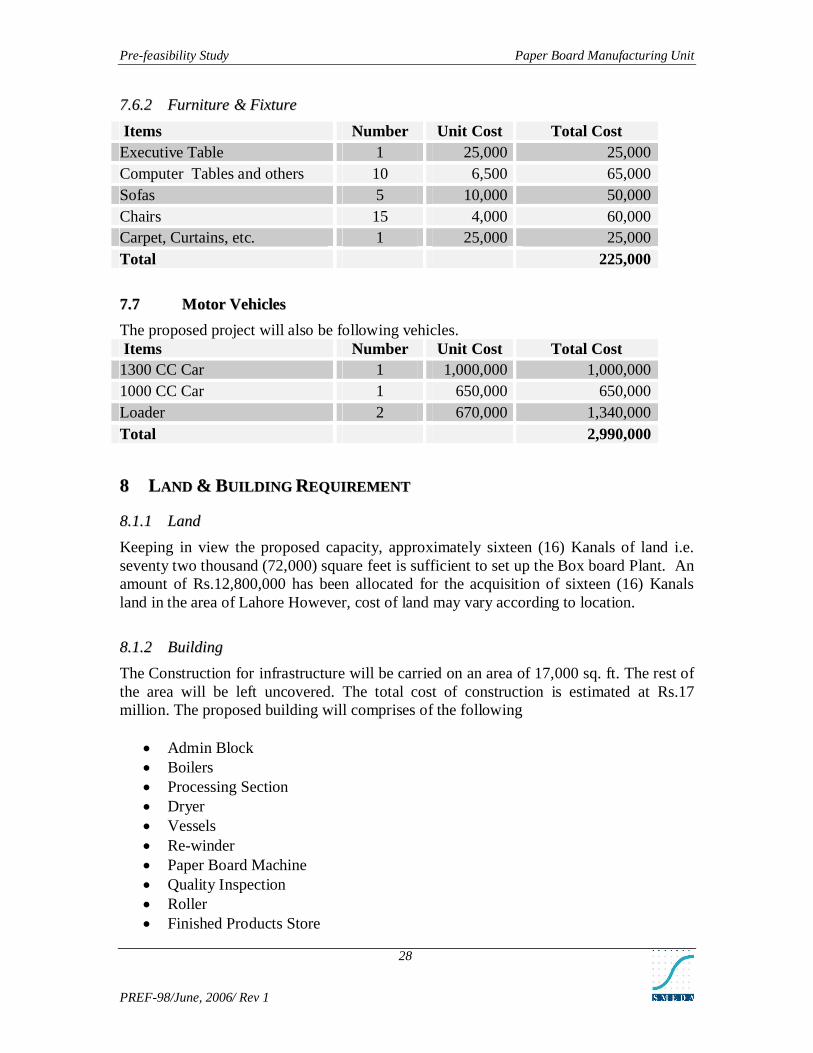

7.6.1 Office Equipment ............................................................................................................. 277.6.2 Furniture & Fixture ......................................................................................................... 28

7.7 MOTOR VEHICLES................................................................................................................. 28

8 LAND & BUILDING REQUIREMENT .................................................................................... 28

8.1.1 Land................................................................................................................................ 288.1.2 Building........................................................................................................................... 28

8.2 UTILITIES REQUIREMENT ...................................................................................................... 29

9 HUMAN RESOURCE REQUIREMENT................................................................................... 29

9.1 HUMAN RESOURCE REQUIREMENTS....................................................................................... 29

10 KEY ASSUMPTIONS................................................................................................................. 30

11 FINANCIAL ANALYSIS............................................................................................................ 31

11.1 PROJECT COST ...................................................................................................................... 3111.2 PROJECTED INCOME STATEMENT........................................................................................... 3211.3 PROJECTED CASH-FLOW STATEMENT..................................................................................... 3311.4 PROJECTED BALANCE SHEET ................................................................................................. 34

12 ANNEXURES.............................................................................................................................. 35

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

3

DISCLAIMER

The purpose and scope of this information memorandum is to introduce the subject

matter and provide a general idea and information on the said area. All the material

included in this document is based on data/information gathered from various sources and

is based on certain assumptions. Although, due care and diligence has been taken to

compile this document, the contained information may vary due to any change in any of

the concerned factors, and the actual results may differ substantially from the presented

information. SMEDA does not assume any liability for any financial or other loss

resulting from this memorandum in consequence of undertaking this activity. The

prospective user of this memorandum is encouraged to carry out additional diligence and

gather any information he/she feels necessary for making an informed decision.

For more information on services offered by SMEDA, please contact our website: www.smeda.org.pk

DOCUMENT CONTROL

Document No. PREF-98

Prepared by SMEDA-Punjab

Issue Date June 2006

Issued by Library Officer

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

4

11 PPUURRPPOOSSEE OOFF TTHHEE DDOOCCUUMMEENNTT

The objective of the pre-feasibility study is primarily to facilitate potential entrepreneurs in project identification for investment. The project pre-feasibility may form the basis of an important investment decision and in order to serve this objective, the document/study covers various aspects of project concept development, start-up, production, marketing, finance and business management. The document also provides sectoral information, brief on government policies and international scenario, which have some bearing on the project itself.

The purpose of this document is to facilitate potential investors in Paper Boardmanufacturing by providing them a macro as well as a micro view of packaging business with the hope that such information as provided herein will aid the potential investors in crucial investment decisions.

The need to come up with pre-feasibility reports for undocumented or minimally documented sectors attains greater imminence as the research that precedes such reports reveal certain thumbs of rules; best practices developed by existing enterprises by trial and error, and certain industrial norms that become a guiding source regarding various aspects of business set-up and it’s successful management.

This particular Pre-feasibility is regarding “Paper Board Manufacturing Unit” which comes under the “Paper” Sector. Before studying the whole document one must consider following critical aspects, which forms basis of any Investment Decision.

22 CCRRUUCCIIAALL FFAACCTTOORRSS && SSTTEEPPSS IINN DDEECCIISSIIOONN MMAAKKIINNGG FFOORR IINNVVEESSTTMMEENNTT

Below are some factors and variables that have a great bearing on setting up Paper BoardManufacturing Unit:

22..11 SSWWOOTT AAnnaallyyssiiss

Before making the decision, whether to invest in the Paper Board Manufacturing or not, one should carefully analyze the associated risk factors. A SWOT analysis can help in analyzing these factors, which can play important role in making the decision.

22..11..11 SSTTRREENNGGTTHH

Availability of raw material i.e. soft wood, which is being extensively used by the match factories available in the locality.

Availability of process water. Plant Effluent disposal. Availability of basic infrastructure facilities like roads, railway, electricity,

fuel and gas. Market of end products. Availability of manpower. Accessible location.

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

5

Suppliers and agents can coordinate as similar business already exists in the area.

Gateway of Central Asian states.

22..11..22 WWEEAAKKNNEESSSSEESS

The major weaknesses in this field of business are:

Poor-availability of suitable processing variety of raw materials at present. Lack of in-house quality control and testing facilities in conformity with the

international standards. Existing technology obsolescence. Poor infrastructure facilities such as irregular power supply, high inland

transportation cost etc. The other major weakness in Pakistan paper board industry is the lack of

coherence and co-operation amongst the processors and exporters due to which the problems can not be effectively addressed and tackled collectively.

Non Availability of properly quality raw material at competitive prices. Tough competition will be faced from the competitors. Its water disposal being closed to residential area may pose pollution to the

residents.

22..11..33 OOPPPPOORRTTUUNNIITTIIEESS

During construction period it has good opportunity of getting cheaper labour force and thus minimizing its cost. So cheaper labour force is also a good opportunity.

Good opportunity exists to manage disposal of product in a short time. Easy coordination can be made with the suppliers and agents who are already

engaged in the area. Huge transaction of some of the raw material is already being executed in the

area.

22..11..44 TTHHRREEAATTSS

The proposed project will be facing the following threat:

Increase in International competition with China, India and Eastern Europe. Imposition of Quality and Environment standards by importing countries. Decline in the average sale price for Pakistani products. Influence of major local and foreign brands operating in the market Unavailability of quality suppliers and distribution channels. If business is looked after in the teething stage and is not well established on

modern and scientific lines, it can create threat for the management.

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

6

Competitors could lower the price of the commodity and can result in low return to the project.

Since good labor has already been engaged by the competitors, therefore efforts will be to make available the experienced staff on handsome salary; otherwise it may be problem for the Mills in the initial stages.

Change in Government regulations WTO challenges and Paper board industry.

22..22 KKeeyy SSuucccceessss FFaaccttoorrss // PPrraaccttiiccaall TTiippss ffoorr SSuucccceessss

Boxboard is used for packaging of consumer items such as cigarettes, cosmetics, garments, detergents, processed foods and spices, matchboxes, bulbs etc. and for making folders, file covers, books and note books, in addition to consumer items industrial consumers are the pharmaceuticals, glass, textile, food products, toiletries, tea, electrical goods, sports and other miscellaneous consumer products. Their consumption is linkedwith the state of business activity in the country.

Food, FMCG will remain the largest market for boxes, comprising over 40 percent of demand. Demand will be fueled in part by popular products such as soft drink beverage carriers etc. Other nondurable goods markets expected to record above-average gains are cosmetics, toiletries and pharmaceuticals, tobacco and textiles etc.

Pakistan can only survive in the present scenario on the strength of technical capabilities, product quality and cost competitiveness, which can be achieved in the following ways:

The plant should be operated by technical staff/technologist to consider the quality standards of ISO, and Environment Protected Agency (EPA).

Should be best located at sites close to a source of bulk supply of fresh water, proximity to effluent disposal facilities,

High quality plan for raw material and ease for availability of fibrous raw material such as grasses, rice husk, sugar cane bagasse and wheat straw.

Keep close interaction with the market demand and producing products in concurrence with the market requirements.

The project employer should employ people who have a complete technical know how of the value added product mix to make project feasible.

Product mix and value added production from by products of paper board industry can be a winning strategy.

Promoting the products in a professional manner etc.

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

7

33 PPRROOJJEECCTT PPRROOFFIILLEE

33..11 OOppppoorrttuunniittyy RRaattiioonnaallee

Boxboard is used for packaging of consumer items such as cigarettes, cosmetics, garments, detergents, processed foods and spices, matchboxes, bulbs etc. and for making folders, file covers, books and note books, in addition to consumer items industrial consumers are the pharmaceuticals, glass, textile, food products, toiletries, tea, electrical goods, sports and other miscellaneous consumer products. Their consumption is linked with the state of business activity in the country.

Food, FMCG will remain the largest market for boxes, comprising over 40 percent of demand. Demand will be fueled in part by popular products such as soft drink beverage carriers etc. Other nondurable goods markets expected to record above-average gains are cosmetics, toiletries and pharmaceuticals, tobacco and textiles etc.

33..22 PPrroojjeecctt BBrriieeff

This particular Pre-feasibility is regarding “Paper Board Manufacturing Unit” which comes under the “Paper” Sector. The objective of the Pre-feasibility study is primarily to provide an overview about the Paper Board Manufacturing business. The proposed Pre-feasibility defines the criteria on which the investment decision is based. This document covers various aspects of Paper Board Manufacturing business concept development, Start-up, Production, Marketing, Finance and Business Management.

33..33 MMaarrkkeett EEnnttrryy TTiimmiinngg

Various Products and Services have high dependence on their commercialization timing and delivery to the Customers but the Paper Board Manufacturing Unit can be started at any time during the year due to the availability of Raw Material throughout the year.

33..44 PPrrooppoosseedd BBuussiinneessss LLeeggaall SSttaattuuss

The said project can be a proprietorship or a partnership and even it can be registered under the Companies Ordinance, 1984 with the Securities & Exchange Commission of Pakistan. The selection totally depends upon the choice of the Entrepreneur. This Pre-feasibility assumes the Legal Status of a Sole Proprietorship.

33..55 PPrroojjeecctt CCaappaacciittyy aanndd RRaattiioonnaallee

The proposed size of the project is capable to produce an average of 39 Ton (Box Board) per day. Considering the local market demand trends, initially the project would be able to receive and entertain such number of orders which are required for the project to be economically viable. The plant has a processing capacity of about 14000 Ton per annum

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

8

with 360 working days basis. Production supported by duplicating the existing box board unit.

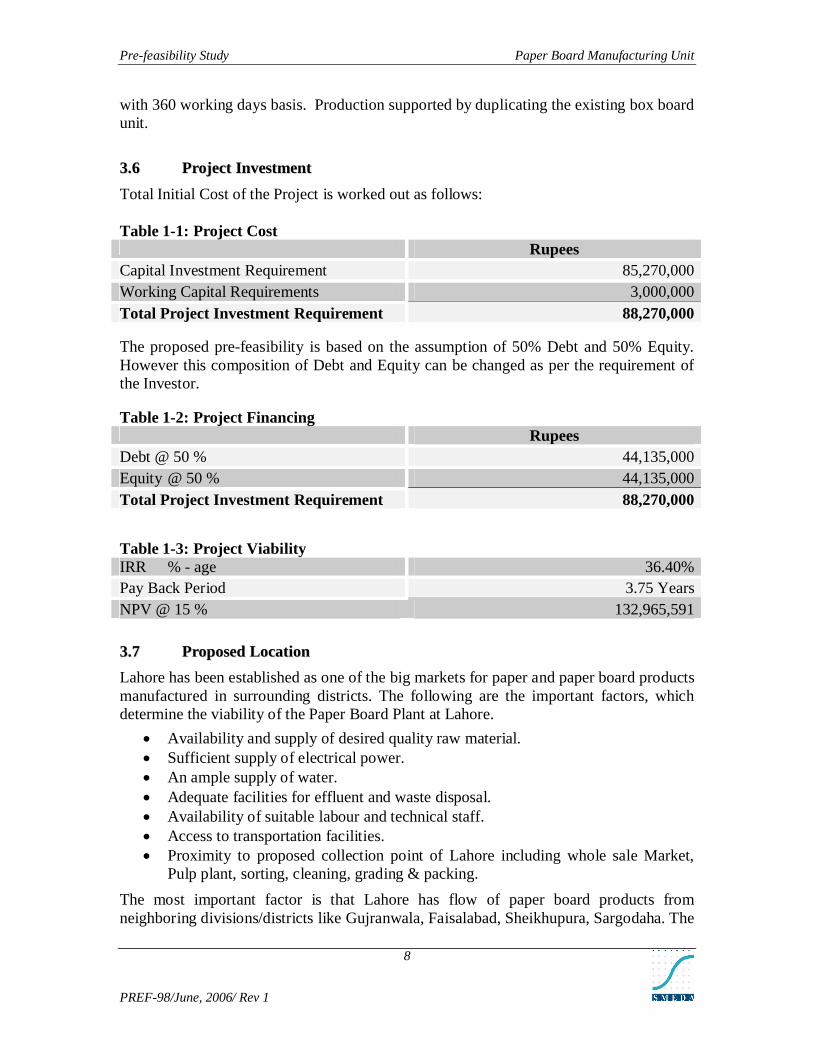

33..66 PPrroojjeecctt IInnvveessttmmeenntt

Total Initial Cost of the Project is worked out as follows:

Table 1-1: Project CostRupees

Capital Investment Requirement 85,270,000Working Capital Requirements 3,000,000Total Project Investment Requirement 88,270,000

The proposed pre-feasibility is based on the assumption of 50% Debt and 50% Equity. However this composition of Debt and Equity can be changed as per the requirement of the Investor.

Table 1-2: Project FinancingRupees

Debt @ 50 % 44,135,000Equity @ 50 % 44,135,000Total Project Investment Requirement 88,270,000

Table 1-3: Project ViabilityIRR % - age 36.40%Pay Back Period 3.75 Years NPV @ 15 % 132,965,591

33..77 PPrrooppoosseedd LLooccaattiioonn

Lahore has been established as one of the big markets for paper and paper board products manufactured in surrounding districts. The following are the important factors, which determine the viability of the Paper Board Plant at Lahore.

Availability and supply of desired quality raw material. Sufficient supply of electrical power. An ample supply of water. Adequate facilities for effluent and waste disposal. Availability of suitable labour and technical staff. Access to transportation facilities. Proximity to proposed collection point of Lahore including whole sale Market,

Pulp plant, sorting, cleaning, grading & packing.

The most important factor is that Lahore has flow of paper board products from neighboring divisions/districts like Gujranwala, Faisalabad, Sheikhupura, Sargodaha. The

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

9

availability of quality raw material is possible and plant will be located near to main market along-with facilities of utilities, fuel, transportation and waste disposal.

Whereas the industrial estate at Sundar which was inaugurate on August 30, 2004. The PIEDMC initially decided to initiate work only on the 500-acre first phase of the project. The Sundar Industrial Estate is ultimately to encompass 1,500 acres. The PIEDMC start the allotment of plots- on September 1 and completed it on September 30, 2004 the development work at Sundar Industrial Estate was at full swing and more than 20 percent of the construction work has already been completed.Keeping in view the locational considerations of the access to raw materials, access to market for finished products, availability of required infrastructure and adequate arrangements for effluent disposal, suitable locations for paper and board industry projects are districts of Sheikhupura, Gujranwala, Gujrat, Kasur, Sialkot, Jacobabad and Khanpur. They are also fast emerging as trade center of country. It is emerging as second Hub for the Pakistan

44 PPAAPPEERR && PPAAPPEERR BBOOAARRDD

There is often an overlapping in the terms used for Paper and Board. Normally, thicker than 0.012 inches or more is called Board, whilst thinner and lighter in weight is called Paper. The weight of paper varies from 10 grams to 125 grams per square meter, whereas the weight of paperboard ranges between 125 and 200 grams per square meter. Board refers to the heavier materials weighing 200 grams and above.

44..11 PPAAPPEERR

Paper is single ply sheet with weights of between 10 and 125 grams per square meter. By varying the fibrous and chemicals materials used and by using different surface treatments, different types and qualities of paper can be produced. Writing and printing papers have a uniform substance, thickness and moisture profile, both along and across the sheet. These are clean, free of holes and flat, have good resistance to aqueous compounds and printability and surface finish.

There are numerous varieties of writing and printing paper distinguished on the basis of substance and finish depending on the requirements of different end-uses. The specialized varieties of paper include poster paper, art paper, bond paper, newsprint etc. These varieties are used for specific purposes and apart from newsprint, have limited market.

The wrapping and packing paper has loser grammage between 40 to 125 grams, and can be produced on paper making machines through change in input mix and chemical treatment. Kraft paper has a higher grammage, greater strength and is mostly used for packing cement.1

1 Market Survey

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

10

44..22 PPAAPPEERRBBOOAARRDD

Paperboard is a multiple sheet with gramage in excess of 125 per square meter. It possesses uniform substance, thickness and moisture profiles, both along and across the sheet. These should have a clean top liner ply, smooth receptive printing surface, good opacity and good creasing quality. The critical physical strength properties are rigidity and good ply adhesion. The main sue of paperboard are for domestic and commercial packaging in the form of printed and un-printed cartons. These are most commonly used in packing of cigarettes, toiletries, detergents, tea, pharmaceuticals, food and other consumer items.

The following are the general categories of Paper and Board.

Paper Board Box Board Newsprint Packing & Wrapping Paper Kraft Paper/Liner Paper Fluting Paper Printing & Writing Paper Specialty Paper

44..33 RREECCYYCCLLIINNGG OOFF PPAAPPEERR && PPAAPPEERR BBOOAARRDD

The paper board industry has recycled used paper and paper board for over 600 years. After using rags for centuries, wood became the main raw material source for papermaking in the 19th century. In recent decades, used paper has become an increasingly important raw material source and, compared to many other materials, is easy to recycle.

Almost any paper can be recycled including used newspapers, cardboard, packaging, stationery, postal mail, magazines, catalogues greeting cards and wrapping paper. The collection of used paper and paper board is the first step in the recycling process. There are different national and regional collection systems for paper. Papermakers usually buy their raw material for recycling from recovered paper merchants. These merchants may be owned by paper and paper board mills and is an integrated part of a mill company, or they may be an independent firm which specializes in particular grades or which perhaps operates in a smaller geographical area.

Until recently, apart from old newspapers and magazines, most recovered paper came from industrial and commercial sources, because it was the easiest, cleanest and most economical to collect. But demand for recovered paper is set to grow substantially, so additional sources like households need to be tapped.

The collecting system in operation must be cost-effective and efficiently organized so that the necessary volumes and qualities of recovered paper can be obtained and appropriately recycled. The paper and paper board mills that depend on recovered paper must have assurance of a regular supply.

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

11

44..44 RREEGGUULLAATTIIOONNSS TTOO PPAAPPEERR && PPAAPPEERR BBOOAARRDD

The current Laws, Regulations and Government Duties on paper and paperboard are as follows:

44..44..11 CCuussttoomm DDuuttiieess aanndd TTaaxxeess

Chapter 48 of Custom Tariff and Trade Controls lists the tariff applicable to paper & paperboard, which is given in annexure 3, page 36.

44..44..22 EEnnvviirroonnmmeennttaall TTeecchhnnoollooggyy // QQuuaalliittyy IIssssuueess

The existing production units require technological up gradation through greater investments for overcoming the environmental hazards arising from their operations. The pulp and paper mills contaminate the environment both as a result of atmospheric pollution through gaseous discharges as well as water pollution through discharge of process and conveying water. The new investment for rover coming pollution is almost equal to the total initial investment in the unit. Local Mills are making progress to control pollution and treat effluent. Mills are also working with EPA and NGOs and other local & foreign institutions to develop home grown and financially viable treatment process.2

Use of large quantity of water for pulp involves disposal of large quantity of waste water. In recent years disposal of waste has assumed importance because of restrictive legislation enacted to prevent pollution of rivers, streams, lakes etc, into which mill’s effluents were discharged. The only impurity involved is suspended fibrous matter and it is both easy and remunerative to recover it from the effluent

An effective and economical method of disposal of mill’s waste is to discharge it into streams with adequate flow throughout the year to furnish dilution, so that the prescribed B.O.D (Biological Oxygen Demand) is maintained and there is no risk to fish and aquatic life or pollution of water used by cattle and human beings for drinking purposes or for washing and irrigation purposes. Another device, applicable only to relatively small alkaline pulp mills, is to segregate the small volume of bad effluents, partly treat it by sedimentation, and discharge it with permission from concerned authorities into local sewerage system, so that it is mixed with domestic sewage of locality and is treated in usual way.

2 Expert Advisory Cell

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

12

55 RRAAWW MMAATTEERRIIAALL

55..11 AAVVAAIILLAABBIILLIITTYY OOFF RRAAWW MMAATTEERRIIAALL

The basic raw material sources for manufacturing of paper and paper board can be broadly classified into three groups:

55..11..11 WWoooodd bbaasseedd mmaatteerriiaall

Among the wood based raw materials, coniferous pine is in short supply in Pakistan. The soft wood forests in the country exist in extreme northern hills of North West Frontier province and Azad Kashmir which are mostly inaccessible due to lack of suitable communication facilities.

Popular and eucalyptus, among the non-coniferous species, are produced mostly on irrigated land. The eucalyptus trees however, more are extensively grown but their plantations are not yet sufficient to meet pulping requirements of the paper industry. Besides, their cost is significantly higher as compared to other local material available for pulping.

55..11..22 AAggrriiccuullttuurraall wwaasstteess

Among the agro-based wastes the following are being extensive used:

StrawsStraws are by-products of cereal crops, the major being wheat and rice. Paper and paper board industry is presently the main user of the marketed supplies of wheat straw. Adequate quantities of wheat straw are available for the industry. Rice straw is generally used as packing material for glass and ceramic products. Its use in paper making is limited as it contains silica and gives some process problems.

BagasseIt is a well established raw material for making almost al grads of paper, from fine quality paper to board.

GrassesThere is a wide range of grasses grown in Pakistan which can be used for making pulp and paper. Kahi grass grows wild along the river banks, some quantity are already being use by paper mills. Other grasses available in Pakistan are Bhabbar, Gauj Gumaz, Rhodes Grass, Chorkha, Pawpi, Chari and Dhawar. The main problems for using grasses relate to their collection and procurement.

55..11..33 OOtthheerr RRaaww MMaatteerriiaall

The group of other raw material used for pulp and paper making include the following:

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

13

Waste PaperThere are two main sources of collection of waste paper. One is waste paper collected at offices and factories such as government offices, business concerns, banks, newspapers and publishing companies, printing and book binding concerns etc. the other source is waste paper purchased by trash dealers from private persons at their homes. It is estimated that adequate quantities of waste paper are available for use in paper board industry. It is also being imported for the paper industry.

Cotton Linters and WasteThese are available from ginning and spinning operations as their by-products and are used for making pulp of high quality for producing superior paper as well as blending with short fibre pulp produced from wheat straw and grasses. Adequate quantities of cotton linters and wastes are available for paper industry while about 10 % of the cotton waste is also exported from Pakistan.

55..22 PPLLUUPPIINNGG CCHHEEMMIICCAALLSS

The quantity of pulping chemicals required depends on the pulping process. In the case of sulphate pulping, a chemical recovery system which regenerates the cooking chemicals is incorporated in the process. The Sulphate pulping process uses sodium sulphate and limestone (calcium Carbonate). The chemicals used in bleaching pulp are chlorine, caustic soda, lime, sodium chlorate and sodium peroxide.

55..33 BBOOXX BBOOAARRDD MMAAKKIINNGG CCHHEEMMIICCAALLSS

Alum, starch, rosin, clay, soap stone, caustic soda and other chemicals are used at product making stage. Stock is treated with starch to improve adhesion of fibres to each other and with rosin to prevent the spread of ink, while clay and various chemicals are used to improve weight, opacity and printing qualities.

Caustic soda, rosin, starch, alum and limestone are available in adequate quantities for the paper and paper board industry from local sources while other chemical are imported.

55..44 OOTTHHEERR CCOONNSSUUMMAABBLLEE MMAATTEERRIIAALLSS

These materials include machine wires, felt, lubricants and all other non-chemical material consumed during the manufacture of pulp and paper board as well as spare parts and tools.

66 MMAARRKKEETT IINNFFOORRMMAATTIIOONN

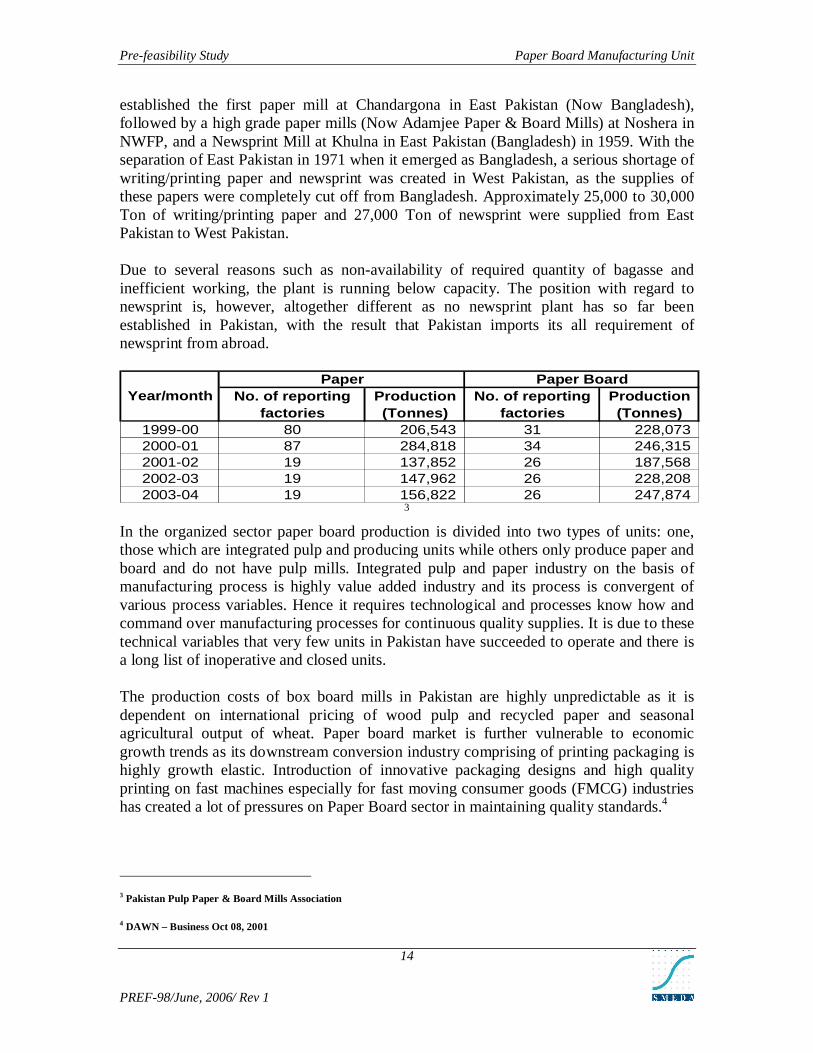

In 1947 when Pakistan came into existence, there was not a single plant to manufacture paper in the country. All the requirements of the paper in the country had to be met through imports. Pakistan Industrial Development Corporation (PIDC) was set up for the establishment of different industries including paper mill in public sector. In 1953, PIDC

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

14

established the first paper mill at Chandargona in East Pakistan (Now Bangladesh), followed by a high grade paper mills (Now Adamjee Paper & Board Mills) at Noshera in NWFP, and a Newsprint Mill at Khulna in East Pakistan (Bangladesh) in 1959. With the separation of East Pakistan in 1971 when it emerged as Bangladesh, a serious shortage of writing/printing paper and newsprint was created in West Pakistan, as the supplies of these papers were completely cut off from Bangladesh. Approximately 25,000 to 30,000 Ton of writing/printing paper and 27,000 Ton of newsprint were supplied from East Pakistan to West Pakistan.

Due to several reasons such as non-availability of required quantity of bagasse and inefficient working, the plant is running below capacity. The position with regard to newsprint is, however, altogether different as no newsprint plant has so far been established in Pakistan, with the result that Pakistan imports its all requirement of newsprint from abroad.

No. of reporting factories

Production (Tonnes)

No. of reporting factories

Production (Tonnes)

1999-00 80 206,543 31 228,073 2000-01 87 284,818 34 246,315 2001-02 19 137,852 26 187,568 2002-03 19 147,962 26 228,208 2003-04 19 156,822 26 247,874

PaperYear/month

Paper Board

3

In the organized sector paper board production is divided into two types of units: one, those which are integrated pulp and producing units while others only produce paper and board and do not have pulp mills. Integrated pulp and paper industry on the basis of manufacturing process is highly value added industry and its process is convergent of various process variables. Hence it requires technological and processes know how and command over manufacturing processes for continuous quality supplies. It is due to these technical variables that very few units in Pakistan have succeeded to operate and there is a long list of inoperative and closed units.

The production costs of box board mills in Pakistan are highly unpredictable as it is dependent on international pricing of wood pulp and recycled paper and seasonal agricultural output of wheat. Paper board market is further vulnerable to economic growth trends as its downstream conversion industry comprising of printing packaging is highly growth elastic. Introduction of innovative packaging designs and high quality printing on fast machines especially for fast moving consumer goods (FMCG) industries has created a lot of pressures on Paper Board sector in maintaining quality standards.4

3 Pakistan Pulp Paper & Board Mills Association

4 DAWN – Business Oct 08, 2001

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

15

Forest area plays an import role in the development of paper and paper board industry as it provides the basic raw material for it. Today forest cover one-fourth of the total land area of the world excluding Antarctica and Greenland. Seven countries – Russia, Brazil, Canada, US, China, Indonesia and the Democratic Republic of Congo (former Zaire) hold over 60 per cent of the world’s forest area.

However, forest area constitutes just 4.8 per cent or 4.2 million hectares in Pakistan which is far below the internationally acceptable ratio of 20-30 per cent necessary for the balanced economy. In addition, actual production from the forest area in Pakistan is even smaller as only one-third of it is productive while the remaining two-third is maintained for environmental protection.5

66..11 MMAARRKKEETT DDEEMMAANNDD

The demand for the various categories of paper and paper board has shown a steady increase over the years and is expected to continue increasing as literacy improves and economic growth takes place. The shortage so far has been met through imports.

66..22 FFAACCTTOORRSS AAFFFFEECCTTIINNGG DDEEMMAANNDD AANNDD SSUUPPPPLLYY

66..22..11 DDeemmaanndd

The major factors affecting the demand for the products of paper, paper board and packaging industry include the following:

The demographic trend and age group The education sector developments and future education policy The economic growth trends and projections of gross national product Trends in industrialization and future projections Development of electronic media

Demographic Trends: In developing countries, increase in population and in the standard of living result in a tremendous demand for paper, packaging and fibre. According to the age-group classification based on 1981 census result, about 40 percent of the total population belongs to the age group of 5-19 years. This is the population segment which is directly related to the education sector and hence has the greatest effect on the demand for paper and paper board.

Education: Education facilities in Pakistan have been expanding overtime but have not kept pace with the requirements of a modernizing society. The literacy rate which is estimated at 53 %, activities associates with the education sector account for almost one half of the paper consumption in the country. The significant development of the

5 Pakistan Economist

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

16

education sector in the next five years, as envisaged in the new education policy would lead to considerable increase in demand for the writing and printing paper.

Economic Growth Trend: The demand for paper, paper board and other packaging materials is directly influenced by the level of economic activity. In Pakistan the annual Gross Domestic Product (GDP) has grown at the rate is 8.4 percent in 2004-05. The increase tempo of economic activity and investment friendly policies of the government are expected to lead to greater demand for paper products.

Development of Electronic Media: It is some times asserted that the demand for paper might be adversely affected due to the phenomenal growth and popularity of electronic information system. It is asserted that we are moving towards the paperless office scenario. The argument however does not have much force. We may use computers but we still like to print out our works, as for electronic information, it works only up to a point.

66..22..22 FFuuttuurree DDeemmaanndd

The demand of paper and paper board is a function of number of parameters. The most important of the parameter is the per capita GNP which is an Index of the income and purchasing power of the people. It has been established by study that the demand for paper is strongly related to per capita GNP. The demand increases rapidly at low levels of per capita GNP and less rapidly at higher levels of per capita GNP.

A second important parameter is the growth of literacy and education in a country. A third parameter is the rate of urbanization. Per capita consumption of paper is higher in urban areas than in the rural sector, at present, the Government checking the urbanization through several rural development programs. Another significant factor is industrialization. Since most industries use paper for packing purposes, the consumption of paper will increase as industrial production increases.

Food, beverages, FMCG will remain the largest market for boxes, comprising over 40 percent of demand. Demand will be fueled in part by popular products such as soft drink beverage carriers etc. Other nondurable goods markets expected to record above-average gains are cosmetics, toiletries and pharmaceuticals, tobacco and textiles etc.

66..22..33 SSuuppppllyy

The domestic paper board industry has currently been facing a number of challenges affecting its supply. The major factors contributing to the present sate of affairs are explained below:

Devaluation of Pak Rupee Increase in input costs Changes in the level of duties

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

17

Devaluation of Pak Rupee: The value of Pak rupee has been persistently declining in terms of foreign currencies through official policies of adjustment of foreign exchange rates. This has resulted in increase in rupee value of imported inputs, especially of long fibre wood pulp needed for mixing with local short fibre pulp for paper making.

Increase in Input Costs: The increase in the rates of local energy and other input charges have also contributed to increase in cost of production. The local producers are thus placed at a comparative disadvantage in competition with imported supplies.

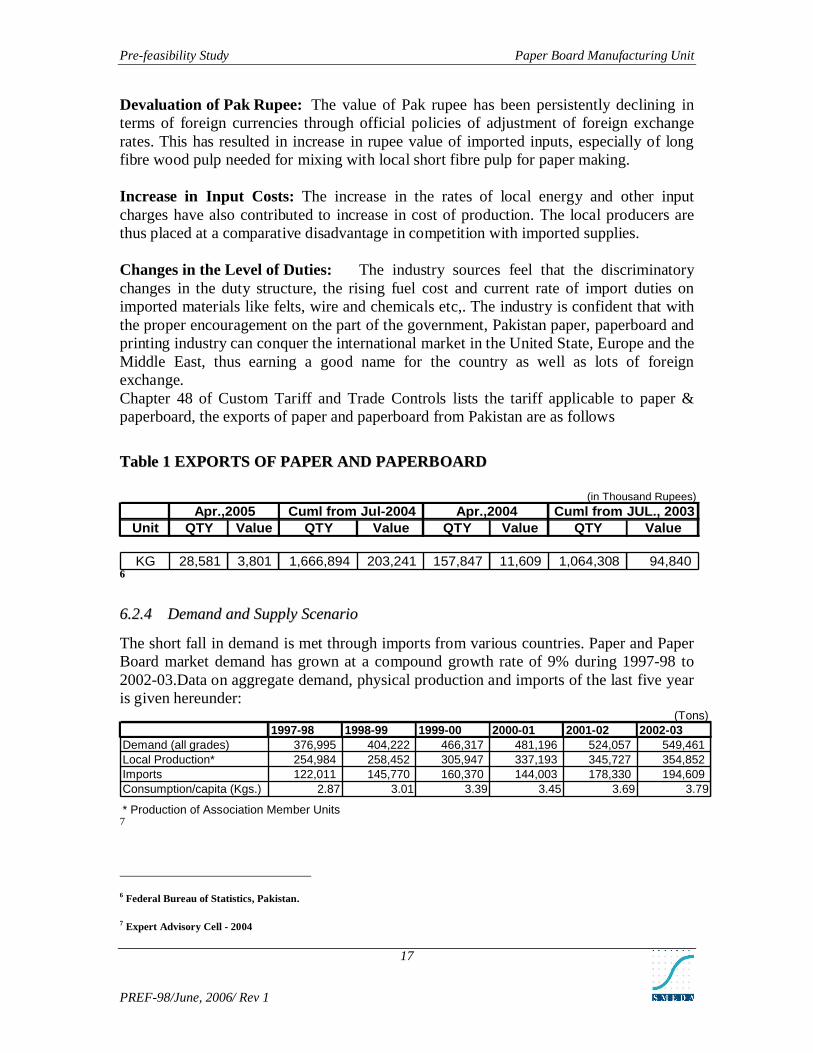

Changes in the Level of Duties: The industry sources feel that the discriminatory changes in the duty structure, the rising fuel cost and current rate of import duties on imported materials like felts, wire and chemicals etc,. The industry is confident that with the proper encouragement on the part of the government, Pakistan paper, paperboard and printing industry can conquer the international market in the United State, Europe and the Middle East, thus earning a good name for the country as well as lots of foreign exchange.Chapter 48 of Custom Tariff and Trade Controls lists the tariff applicable to paper & paperboard, the exports of paper and paperboard from Pakistan are as follows

TTaabbllee 11 EEXXPPOORRTTSS OOFF PPAAPPEERR AANNDD PPAAPPEERRBBOOAARRDD

Unit QTY Value QTY Value QTY Value QTY Value

KG 28,581 3,801 1,666,894 203,241 157,847 11,609 1,064,308 94,840

(in Thousand Rupees)

Apr.,2005 Cuml from Jul-2004 Apr.,2004 Cuml from JUL., 2003

66

66..22..44 DDeemmaanndd aanndd SSuuppppllyy SScceennaarriioo

The short fall in demand is met through imports from various countries. Paper and Paper Board market demand has grown at a compound growth rate of 9% during 1997-98 to 2002-03.Data on aggregate demand, physical production and imports of the last five year is given hereunder:

(Tons)1997-98 1998-99 1999-00 2000-01 2001-02 2002-03

Demand (all grades) 376,995 404,222 466,317 481,196 524,057 549,461 Local Production* 254,984 258,452 305,947 337,193 345,727 354,852 Imports 122,011 145,770 160,370 144,003 178,330 194,609 Consumption/capita (Kgs.) 2.87 3.01 3.39 3.45 3.69 3.79

* Production of Association Member Units7

6 Federal Bureau of Statistics, Pakistan.

7 Expert Advisory Cell - 2004

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

18

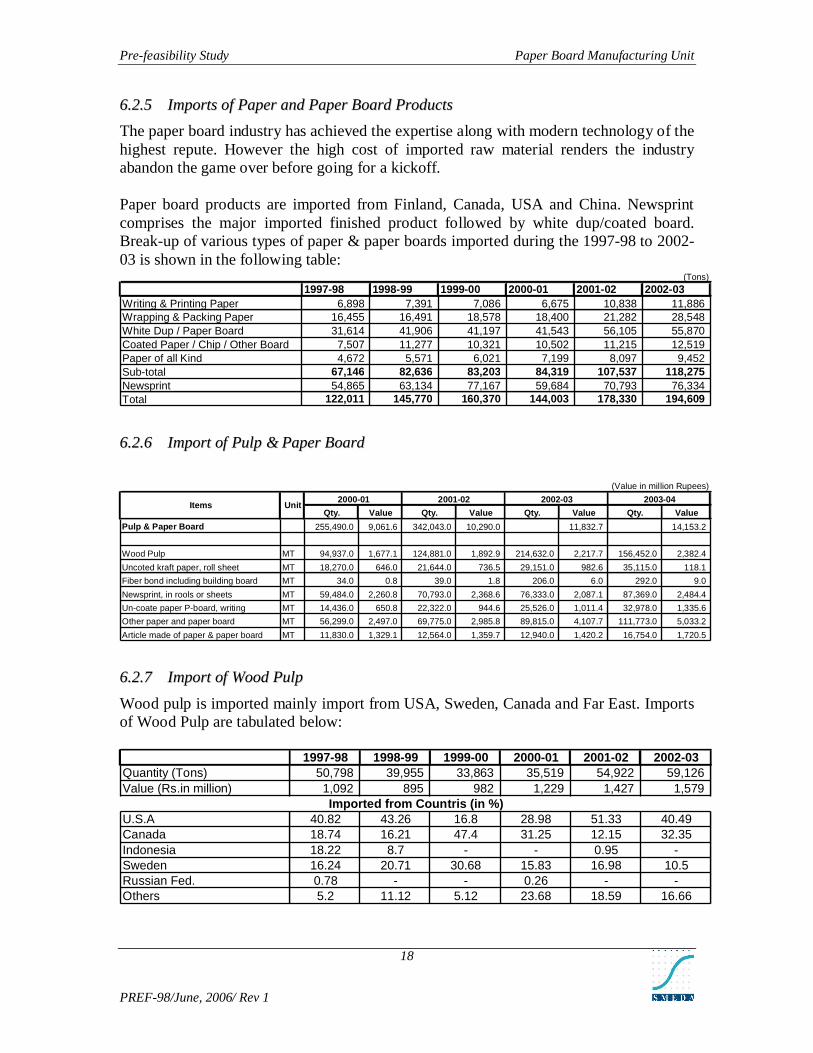

66..22..55 IImmppoorrttss ooff PPaappeerr aanndd PPaappeerr BBooaarrdd PPrroodduuccttss

The paper board industry has achieved the expertise along with modern technology of the highest repute. However the high cost of imported raw material renders the industry abandon the game over before going for a kickoff.

Paper board products are imported from Finland, Canada, USA and China. Newsprint comprises the major imported finished product followed by white dup/coated board. Break-up of various types of paper & paper boards imported during the 1997-98 to 2002-03 is shown in the following table:

(Tons)

1997-98 1998-99 1999-00 2000-01 2001-02 2002-03Writing & Printing Paper 6,898 7,391 7,086 6,675 10,838 11,886 Wrapping & Packing Paper 16,455 16,491 18,578 18,400 21,282 28,548 White Dup / Paper Board 31,614 41,906 41,197 41,543 56,105 55,870 Coated Paper / Chip / Other Board 7,507 11,277 10,321 10,502 11,215 12,519 Paper of all Kind 4,672 5,571 6,021 7,199 8,097 9,452 Sub-total 67,146 82,636 83,203 84,319 107,537 118,275 Newsprint 54,865 63,134 77,167 59,684 70,793 76,334 Total 122,011 145,770 160,370 144,003 178,330 194,609

66..22..66 IImmppoorrtt ooff PPuullpp && PPaappeerr BBooaarrdd

Qty. Value Qty. Value Qty. Value Qty. Value

Pulp & Paper Board 255,490.0 9,061.6 342,043.0 10,290.0 11,832.7 14,153.2

Wood Pulp MT 94,937.0 1,677.1 124,881.0 1,892.9 214,632.0 2,217.7 156,452.0 2,382.4

Uncoted kraft paper, roll sheet MT 18,270.0 646.0 21,644.0 736.5 29,151.0 982.6 35,115.0 118.1

Fiber bond including building board MT 34.0 0.8 39.0 1.8 206.0 6.0 292.0 9.0

Newsprint, in rools or sheets MT 59,484.0 2,260.8 70,793.0 2,368.6 76,333.0 2,087.1 87,369.0 2,484.4

Un-coate paper P-board, writing MT 14,436.0 650.8 22,322.0 944.6 25,526.0 1,011.4 32,978.0 1,335.6

Other paper and paper board MT 56,299.0 2,497.0 69,775.0 2,985.8 89,815.0 4,107.7 111,773.0 5,033.2

Article made of paper & paper board MT 11,830.0 1,329.1 12,564.0 1,359.7 12,940.0 1,420.2 16,754.0 1,720.5

Items Unit

(Value in million Rupees)

2000-01 2001-02 2002-03 2003-04

66..22..77 IImmppoorrtt ooff WWoooodd PPuullpp

Wood pulp is imported mainly import from USA, Sweden, Canada and Far East. Imports of Wood Pulp are tabulated below:

1997-98 1998-99 1999-00 2000-01 2001-02 2002-03Quantity (Tons) 50,798 39,955 33,863 35,519 54,922 59,126 Value (Rs.in million) 1,092 895 982 1,229 1,427 1,579

U.S.A 40.82 43.26 16.8 28.98 51.33 40.49Canada 18.74 16.21 47.4 31.25 12.15 32.35Indonesia 18.22 8.7 - - 0.95 -Sweden 16.24 20.71 30.68 15.83 16.98 10.5Russian Fed. 0.78 - - 0.26 - -Others 5.2 11.12 5.12 23.68 18.59 16.66

Imported from Countris (in %)

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

19

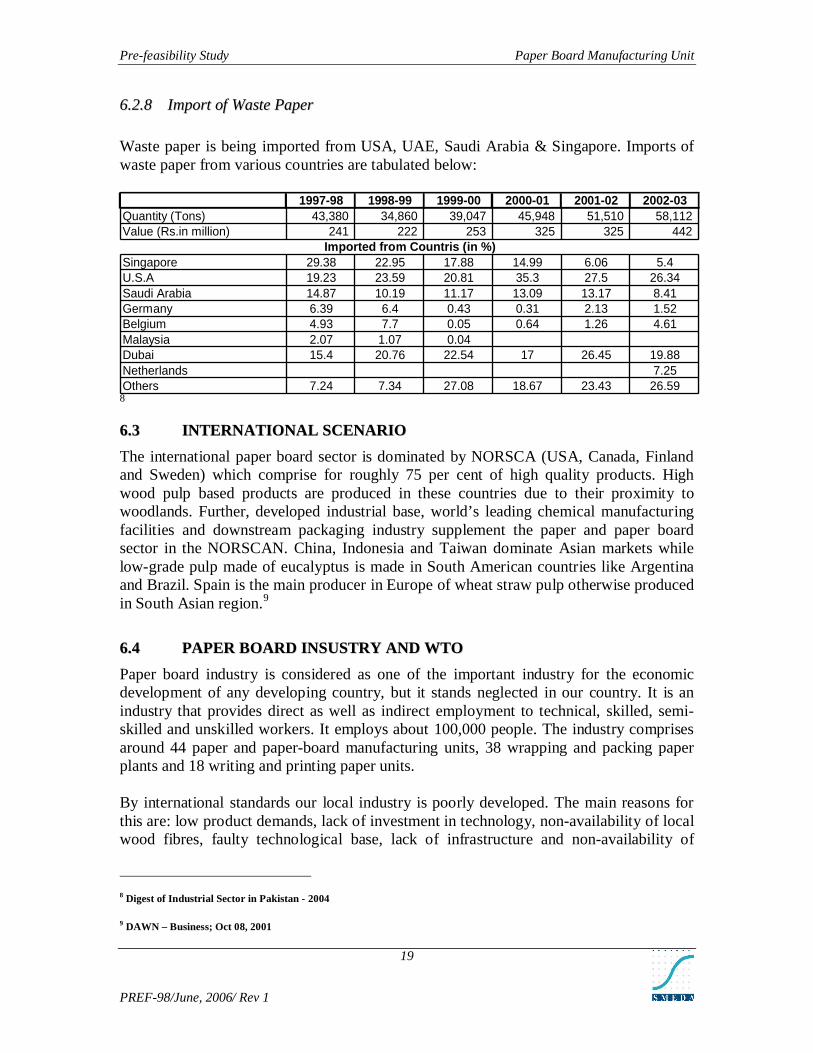

66..22..88 IImmppoorrtt ooff WWaassttee PPaappeerr

Waste paper is being imported from USA, UAE, Saudi Arabia & Singapore. Imports of waste paper from various countries are tabulated below:

1997-98 1998-99 1999-00 2000-01 2001-02 2002-03Quantity (Tons) 43,380 34,860 39,047 45,948 51,510 58,112 Value (Rs.in million) 241 222 253 325 325 442

Singapore 29.38 22.95 17.88 14.99 6.06 5.4U.S.A 19.23 23.59 20.81 35.3 27.5 26.34Saudi Arabia 14.87 10.19 11.17 13.09 13.17 8.41Germany 6.39 6.4 0.43 0.31 2.13 1.52Belgium 4.93 7.7 0.05 0.64 1.26 4.61Malaysia 2.07 1.07 0.04Dubai 15.4 20.76 22.54 17 26.45 19.88Netherlands 7.25Others 7.24 7.34 27.08 18.67 23.43 26.59

Imported from Countris (in %)

8

66..33 IINNTTEERRNNAATTIIOONNAALL SSCCEENNAARRIIOO

The international paper board sector is dominated by NORSCA (USA, Canada, Finland and Sweden) which comprise for roughly 75 per cent of high quality products. High wood pulp based products are produced in these countries due to their proximity to woodlands. Further, developed industrial base, world’s leading chemical manufacturing facilities and downstream packaging industry supplement the paper and paper board sector in the NORSCAN. China, Indonesia and Taiwan dominate Asian markets while low-grade pulp made of eucalyptus is made in South American countries like Argentina and Brazil. Spain is the main producer in Europe of wheat straw pulp otherwise produced in South Asian region.9

66..44 PPAAPPEERR BBOOAARRDD IINNSSUUSSTTRRYY AANNDD WWTTOO

Paper board industry is considered as one of the important industry for the economic development of any developing country, but it stands neglected in our country. It is an industry that provides direct as well as indirect employment to technical, skilled, semi-skilled and unskilled workers. It employs about 100,000 people. The industry comprises around 44 paper and paper-board manufacturing units, 38 wrapping and packing paper plants and 18 writing and printing paper units.

By international standards our local industry is poorly developed. The main reasons for this are: low product demands, lack of investment in technology, non-availability of local wood fibres, faulty technological base, lack of infrastructure and non-availability of

8 Digest of Industrial Sector in Pakistan - 2004

9 DAWN – Business; Oct 08, 2001

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

20

skilled manpower. Despite such problems, the industry saves $300 million in foreign exchange through import substitution.

In the changing global economic scenario the demand for paper and paperboard has risen due to changes in social and economic patterns mainly through urbanization, packaged foods, consumer durables and literacy. However, the domestic industry lags behind and is unable to operate efficiently. Many units have become inoperative. Some are facing acute financial constraints. A few have closed down or are on the verge of doing so. Factory owners say that the main problems facing the industry include the non-availability of wood, wood pulp and other raw materials, low capacity utilization, fiscal anomalies, under invoicing and dumping of cheap paper products.

Due to massive and unchecked deforestation, wood pulp and basic raw material for making paper and paperboard is scarce. Pulp production is based on agriculture waste, such as wheat and rice straw, cotton and lint, waste paper, biogases and kahi grassroots. But these are also in short supply, as their resources have not been fully tapped. Mills are facing difficulties in the procurement and storage of these materials. At the same time, agriculture waste available in Pakistan is used for producing only short-fibre pulp. As a result, the quality of paper produced locally suffers and is inferior to imported paper.

Under the new WTO regime, the domestic industry will face stiff competition from Asian countries like China, India, Indonesia, Thailand and Taiwan that have a proximity to the Pakistani market as well as technological and other advantages. A comparison of tariff and bonded rates of India and Pakistan shows that although bonded rates under the WTO regime are lower in India: 40 per cent versus 50 per cent in Pakistan.

The Pakistani paperboard industry, with a capacity of 0.6 million Ton, will be in direct competition with countries like China, which has a capacity in excess of 50 million Ton, and India, which has a capacity of 5.6 million Ton. These countries enjoy economies of scale, a technological edge, trained and qualified manpower and domestic supplies of major processing inputs, required for paper board production. Moreover, consumables like paper board machines for clothing, chemicals and spare parts are locally produced in these countries at much lower prices. China enjoys cheaper power rates, which constitutes around 15-20 per cent of total cost of production. However, due to opening of market and slashing of customs duties, various products used in the paperboard industry may also become cheaper for Pakistani producers to import, which would reduce production costs. The domestic industry will also need to improve environmental standards to meet buyers’ requirements. The implementation of TRIPS (Trade Related Intellectual Property Rights) and TRIMS (Trade Related Investment Measures) may also have negative impact on the industry.

The government and the industry need to address these problems on a war footing to meet the challenges of the WTO regime, which is due to take effect from January 1,

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

21

2005. The government should give due priority to this industry in the agenda list of the ministry of industries and productions. 10

77 PPRROODDUUCCTTIIOONN PPRROOCCEESSSS

77..11 BBOOXX BBOOAARRDD MMAANNUUFFAACCTTUURRIINNGG

Industries in the paper board manufacturing sub sector make pulp, paper, paper board, liner, fluted, box board etc.) or converted paper products. The manufacturing of these products is grouped together because they constitute a series of vertically connected processes. There are essentially three activities.

The manufacturing of pulp involves separating the cellulose fibers from other impurities in wood or used paper.

The manufacturing of paper board involves matting these fibers into a sheet. Converted paper board products are made from paper and other materials by

various cutting and shaping techniques and include coating and laminating activities.

77..22 PPRROODDUUCCTTIIOONN MMEETTHHOODDSS AANNDD TTEECCHHNNOOLLOOGGYY

Production processes used in the industry depend on the type of desired output and variety of raw materials used for paper board making. The use of soda process is preferred for high grade board from waste paper and paper board, Tori and straw etc.

The following sequence of operations are generally followed to produce quality type paper board (box board), though the ultimate process depends upon the type of output and the variety of raw material used for pulp making.

The different type of waste papers, paperboard etc. after refining are stirred separately.

Waste material is now forward to the pulper for water mixing. These are blended proportions in a stock blending chest where it used to mix with

water. Pumps take this material into dump chest. The pulp passed through the screen for removing all foreign material like nails,

pins twigs and un-dissolved knots. This material passes through to refiner. The pulp after stock preparation and proper dilution is usually sent to the machine

through one or more screens. Pulp from the machine chest is pumped to the head box where it is mixed with

water.

10 Weekly Business Review (www.jang.com.pk)

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

22

The suspension is then spread uniformly across the full width of a moving endless screen.

The screen travels over table rolls and suction boxes where water drums are driven by the effect of gravity and vacuum.

The screen then passes under roll squeezing additional water from mat. The mat sheet then passes over to a woolen or synthetic cloth belt passing between batteries of press rolls. Here water is further squeezed out and the mat gets compacted.

The water content is then further reduced by evaporate drying. This is followed by calendaring and collecting operations.

Quality testing of the nature and susceptibility of the output to physical and chemical properties are carried out at this stage.

The output is then converted into standard marketing size.

77..22..11 RReeccyycclliinngg PPrroocceessss

The final production process for recycling paper is the same as the process used for boxboard made from virgin fibres but, as the recovered paper fibres have already been used, they have to be cleaned.

As a first step, recovered paper is sorted and graded then delivered to a paper board mill. Large non-fibrous contaminants are removed (for example staples, plastic, glass etc.). The fibres are progressively cleaned and then the pulp is filtered and screened through a number of cycles to make it more suitable for paper board making. The fibres have to be de-inked. The pulp is then ready to be made into paper or paper board. Depending on the grade of paper board being produced, quantities of virgin pulp from sustainable sources may be added. Some paper products, such as newsprint and corrugated materials, can be made from 100% recycled paper. Once the paper is used, it can be recycled and the process starts again.

There are paper board products that cannot be either collected or recycled. The portion of such paper board products, which consist, for example, of cigarette papers, wallpaper, tissue papers and archives, is estimated to be about 19% of the total paper board consumption. In addition to non-collectable and non-recyclable paper products, it would not be economically or environmentally sound to collect and recycle everything.

77..22..22 GGrraaddeess ooff RReeccoovveerreedd PPaappeerr && PPaappeerr BBooaarrdd

There are different grades of recovered paper and board to satisfy the needs of different producers, according to strict specifications. For example, it is not possible to take mixed recovered paper consisting of different paper grades (newspapers, cartons, corrugated boxes) to make printing and writing paper. Mixed recovered paper is best used in packaging grades. More than 50 grades of recovered paper and board are defined in the European Standard EN634. They can be described as follow:

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

23

Low grades (mixed papers, old corrugated containers, board etc.) constitute the main part of the recovered paper consumed. These are used to produce packaging papers and boards.

De-inking grades (newspapers and magazine, graphic papers etc.) are usually also considered as low grades. These are for graphic and sanitary papers.

High grades (scraps, sheets, print off-cuts etc.) require little or no cleaning. They can be used for the production of any paper product as pulp substitute.

Modern recycling processes require little energy and the auxiliary materials involved are environmentally compatible. The contraries (the pins, staples, adhesives etc.) removed during the recycling process create a ‘sludge’ which may be burned for energy recovery, put into landfill or used for other industrial purposes; they can be used as raw materials for other industries (for example land construction) or they can be spread on agricultural land.

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

24

77..33 FFLLOOWW CCHHAARRTT FFOORR BBOOXX BBOOAARRDD MMAANNUUFFAACCTTUURRIINNGG

Finished Product

Roller

Dryers

Rewinder

Quality Inspection

Stock Chest

Pump

Color Mixing

Paper Machine

Raw Material

Sorting / Refining

Water Mixing

Screen Flow

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

25

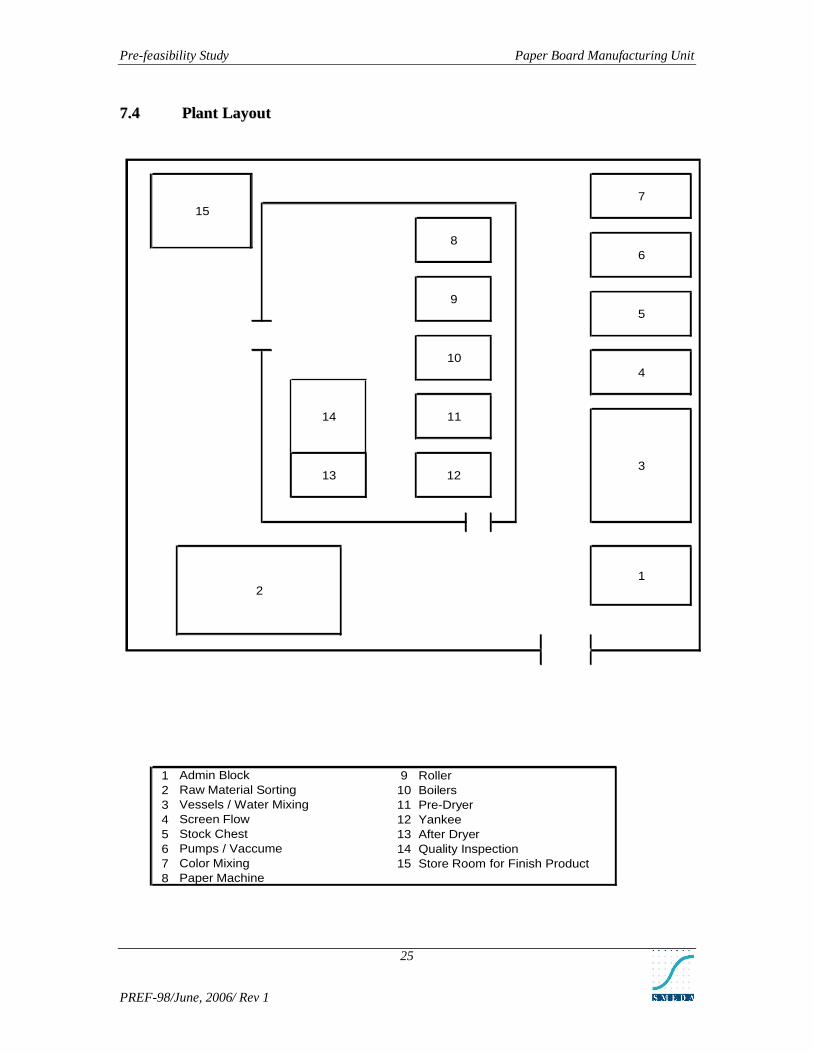

77..44 PPllaanntt LLaayyoouutt

1 9 Roller2 10 Boilers3 11 Pre-Dryer4 12 Yankee5 13 After Dryer6 14 Quality Inspection7 15 Store Room for Finish Product8

104

11

Admin Block

313 12

1

7

86

95

15

14

Raw Material SortingVessels / Water Mixing

Color Mixing

2

Pumps / Vaccume

Paper Machine

Screen FlowStock Chest

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

26

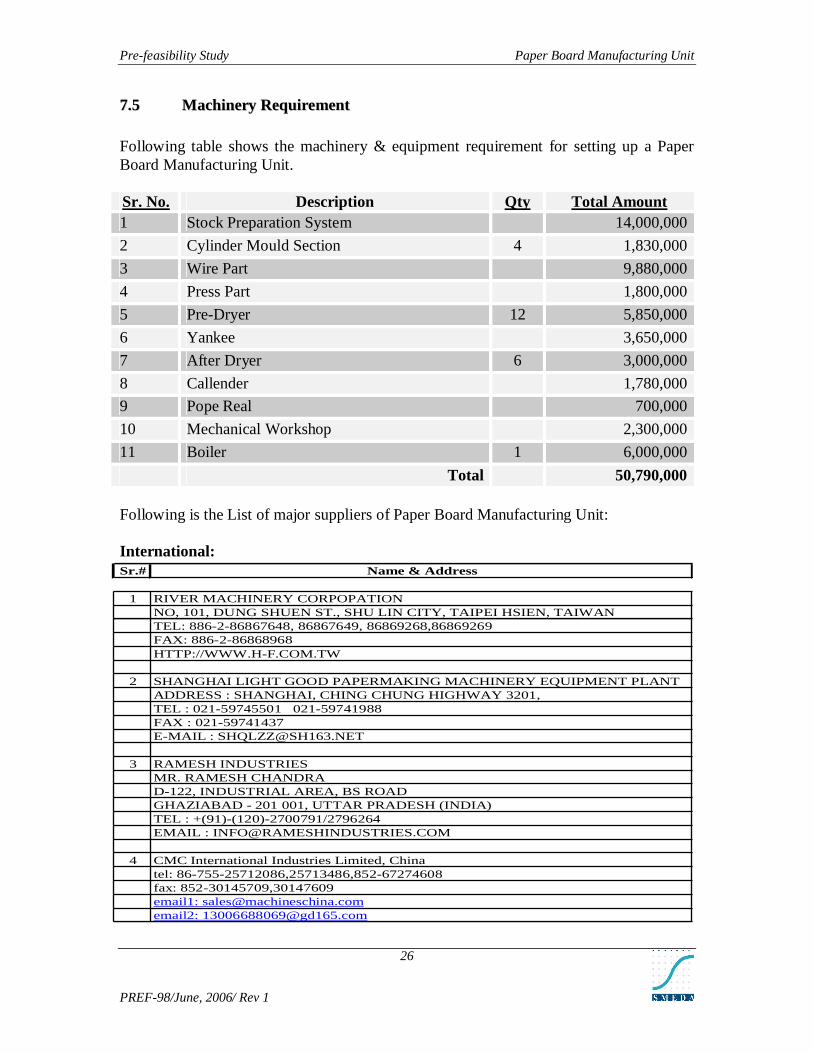

77..55 MMaacchhiinneerryy RReeqquuiirreemmeenntt

Following table shows the machinery & equipment requirement for setting up a Paper Board Manufacturing Unit.

Sr. No. Description Qty Total Amount1 Stock Preparation System 14,000,000

2 Cylinder Mould Section 4 1,830,000

3 Wire Part 9,880,000

4 Press Part 1,800,000

5 Pre-Dryer 12 5,850,000

6 Yankee 3,650,000

7 After Dryer 6 3,000,000

8 Callender 1,780,000

9 Pope Real 700,000

10 Mechanical Workshop 2,300,000

11 Boiler 1 6,000,000

Total 50,790,000

Following is the List of major suppliers of Paper Board Manufacturing Unit:

International:Sr.# Name & Address

1 RIVER MACHINERY CORPOPATIONNO, 101, DUNG SHUEN ST., SHU LIN CITY, TAIPEI HSIEN, TAIWANTEL: 886-2-86867648, 86867649, 86869268,86869269FAX: 886-2-86868968HTTP://WWW.H-F.COM.TW

2 SHANGHAI LIGHT GOOD PAPERMAKING MACHINERY EQUIPMENT PLANTADDRESS : SHANGHAI, CHING CHUNG HIGHWAY 3201,TEL : 021-59745501 021-59741988FAX : 021-59741437E-MAIL : [email protected]

3 RAMESH INDUSTRIESMR. RAMESH CHANDRAD-122, INDUSTRIAL AREA, BS ROADGHAZIABAD - 201 001, UTTAR PRADESH (INDIA)TEL : +(91)-(120)-2700791/2796264EMAIL : [email protected]

4 CMC International Industries Limited, Chinatel: 86-755-25712086,25713486,852-67274608fax: 852-30145709,30147609email1: [email protected]: [email protected]

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

27

Local:

The machinery, equipment and accessories required for Box Board plant at Lahore are fabricated locally. Most advanced technology for drying parameter control, stock preparation system, head box, belt control and belt structure etc., is also used. For this purpose international suppliers are also available to produce finished products confirm to national as well as international standards.

77..66 OOtthheerr FFiixxeedd AAsssseettss RReeqquuiirreemmeenntt

Following additional fixed assets are required for factory and management offices.

77..66..11 OOffffiiccee EEqquuiippmmeenntt

Items Number Unit Cost Total CostFans & Lights 10 3,000 30,000 Air-conditioning 4 25,000 100,000 Computer 5 20,000 100,000 Printer Laser 2 25,000 50,000 Fax 2 25,000 50,000 Networking 1 100,000 100,000 Total 430,000

Sr.# Name & Address

1 Abdul Jabbar & Co88-Railway Road, LahorePh: 042-7661871Fax: 042-7636098

2 H.B sayyed (Pvt.) Ltd.130-D. 1st Flr., Green View Apt., B0Commercial Area, Phase II, Defence, Karachi.Ph: 021-5896021 - 5895790Fax: 021-5895941

3 MAQ Engineering CompanyGondlanwala Road, Near Jinnah Road Chowk,GujranwalaPh; 055-4230498 - 4230497

4 Al-Ahmad Enterprises10-Bangali Street, Shahrah-e-Millat, LahorePh: 042-4121172 - 7121171Fax: 042-712173

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

28

77..66..22 FFuurrnniittuurree && FFiixxttuurree

Items Number Unit Cost Total CostExecutive Table 1 25,000 25,000 Computer Tables and others 10 6,500 65,000 Sofas 5 10,000 50,000 Chairs 15 4,000 60,000 Carpet, Curtains, etc. 1 25,000 25,000 Total 225,000

77..77 MMoottoorr VVeehhiicclleess

The proposed project will also be following vehicles. Items Number Unit Cost Total Cost1300 CC Car 1 1,000,000 1,000,000 1000 CC Car 1 650,000 650,000 Loader 2 670,000 1,340,000 Total 2,990,000

88 LLAANNDD && BBUUIILLDDIINNGG RREEQQUUIIRREEMMEENNTT

88..11..11 LLaanndd

Keeping in view the proposed capacity, approximately sixteen (16) Kanals of land i.e. seventy two thousand (72,000) square feet is sufficient to set up the Box board Plant. An amount of Rs.12,800,000 has been allocated for the acquisition of sixteen (16) Kanals land in the area of Lahore However, cost of land may vary according to location.

88..11..22 BBuuiillddiinngg

The Construction for infrastructure will be carried on an area of 17,000 sq. ft. The rest of the area will be left uncovered. The total cost of construction is estimated at Rs.17 million. The proposed building will comprises of the following

Admin Block Boilers Processing Section Dryer Vessels Re-winder Paper Board Machine Quality Inspection Roller Finished Products Store

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

29

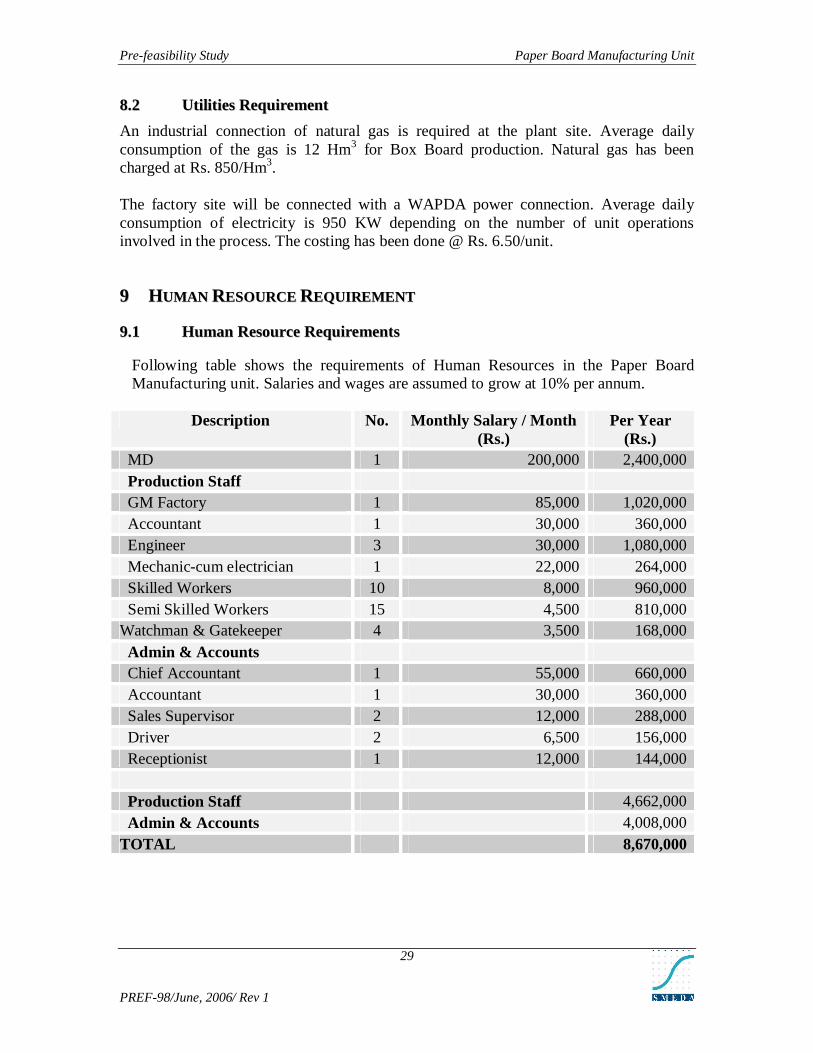

88..22 UUttiilliittiieess RReeqquuiirreemmeenntt

An industrial connection of natural gas is required at the plant site. Average daily consumption of the gas is 12 Hm3 for Box Board production. Natural gas has been charged at Rs. 850/Hm3.

The factory site will be connected with a WAPDA power connection. Average daily consumption of electricity is 950 KW depending on the number of unit operations involved in the process. The costing has been done @ Rs. 6.50/unit.

99 HHUUMMAANN RREESSOOUURRCCEE RREEQQUUIIRREEMMEENNTT

99..11 HHuummaann RReessoouurrccee RReeqquuiirreemmeennttss

Following table shows the requirements of Human Resources in the Paper BoardManufacturing unit. Salaries and wages are assumed to grow at 10% per annum.

Description No. Monthly Salary / Month (Rs.)

Per Year(Rs.)

MD 1 200,000 2,400,000 Production Staff GM Factory 1 85,000 1,020,000 Accountant 1 30,000 360,000 Engineer 3 30,000 1,080,000 Mechanic-cum electrician 1 22,000 264,000 Skilled Workers 10 8,000 960,000 Semi Skilled Workers 15 4,500 810,000 Watchman & Gatekeeper 4 3,500 168,000 Admin & Accounts Chief Accountant 1 55,000 660,000 Accountant 1 30,000 360,000 Sales Supervisor 2 12,000 288,000 Driver 2 6,500 156,000 Receptionist 1 12,000 144,000

Production Staff 4,662,000 Admin & Accounts 4,008,000 TOTAL 8,670,000

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

30

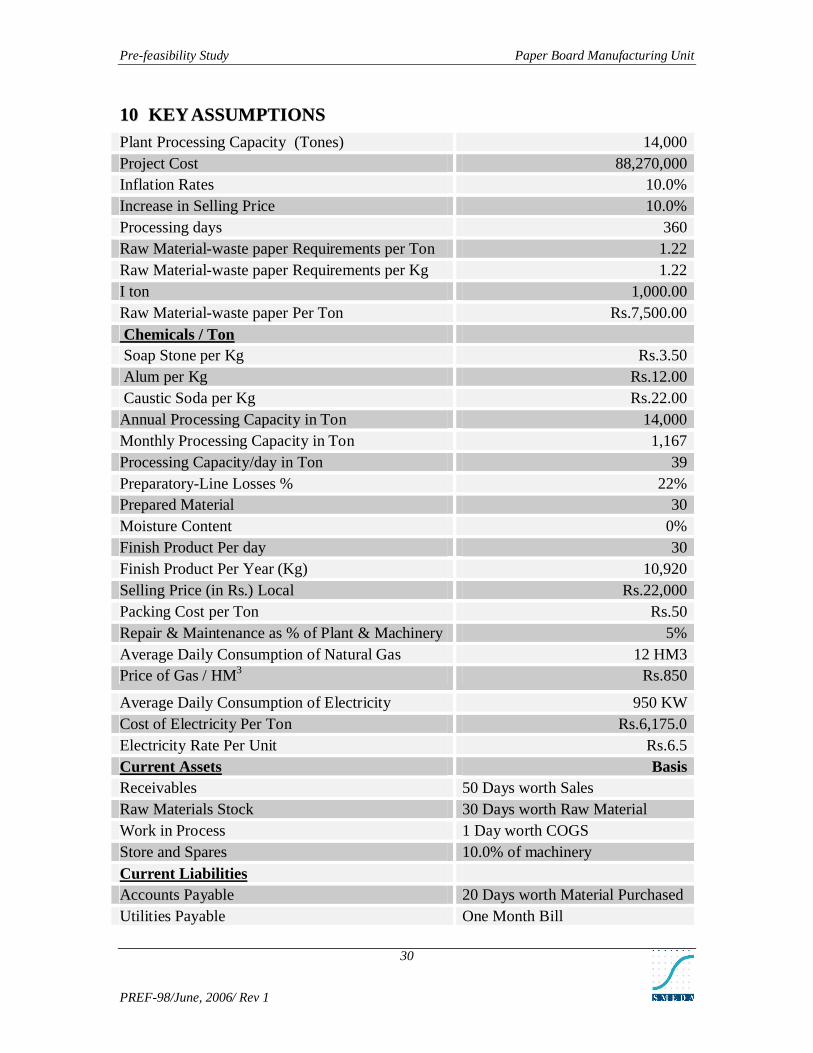

1100 KKEEYY AASSSSUUMMPPTTIIOONNSS

Plant Processing Capacity (Tones) 14,000 Project Cost 88,270,000 Inflation Rates 10.0%Increase in Selling Price 10.0%Processing days 360 Raw Material-waste paper Requirements per Ton 1.22 Raw Material-waste paper Requirements per Kg 1.22 I ton 1,000.00 Raw Material-waste paper Per Ton Rs.7,500.00 Chemicals / Ton Soap Stone per Kg Rs.3.50 Alum per Kg Rs.12.00 Caustic Soda per Kg Rs.22.00Annual Processing Capacity in Ton 14,000 Monthly Processing Capacity in Ton 1,167 Processing Capacity/day in Ton 39 Preparatory-Line Losses % 22%Prepared Material 30 Moisture Content 0%Finish Product Per day 30Finish Product Per Year (Kg) 10,920 Selling Price (in Rs.) Local Rs.22,000Packing Cost per Ton Rs.50Repair & Maintenance as % of Plant & Machinery 5%Average Daily Consumption of Natural Gas 12 HM3Price of Gas / HM3 Rs.850

Average Daily Consumption of Electricity 950 KWCost of Electricity Per Ton Rs.6,175.0Electricity Rate Per Unit Rs.6.5Current Assets BasisReceivables 50 Days worth SalesRaw Materials Stock 30 Days worth Raw MaterialWork in Process 1 Day worth COGSStore and Spares 10.0% of machineryCurrent LiabilitiesAccounts Payable 20 Days worth Material PurchasedUtilities Payable One Month Bill

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

31

1111 FFIINNAANNCCIIAALL AANNAALLYYSSIISS

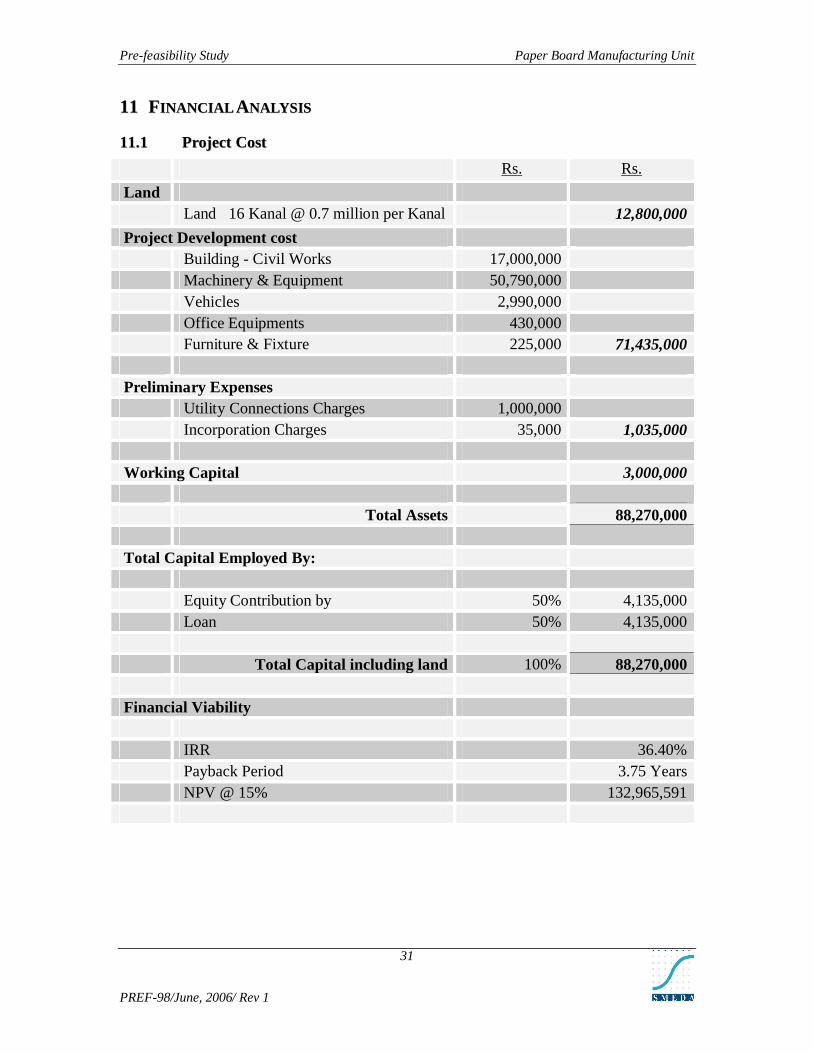

1111..11 PPrroojjeecctt CCoosstt

Rs. Rs.

Land Land 16 Kanal @ 0.7 million per Kanal 12,800,000

Project Development cost Building - Civil Works 17,000,000 Machinery & Equipment 50,790,000 Vehicles 2,990,000 Office Equipments 430,000 Furniture & Fixture 225,000 71,435,000

Preliminary Expenses Utility Connections Charges 1,000,000 Incorporation Charges 35,000 1,035,000

Working Capital 3,000,000

Total Assets 88,270,000

Total Capital Employed By: Equity Contribution by 50% 4,135,000 Loan 50% 4,135,000

Total Capital including land 100% 88,270,000

Financial Viability

IRR 36.40% Payback Period 3.75 Years NPV @ 15% 132,965,591

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

32

1111..22 PPrroojjeecctteedd IInnccoommee SSttaatteemmeenntt

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Sales 108,108,000 118,918,800 145,345,200 159,879,720 193,454,461 232,145,353 276,639,880 304,303,867 360,483,043 396,531,347

Cost of Sales 60,042,399 65,538,739 78,142,640 85,499,794 101,441,159 119,530,669 140,491,078 154,169,927 180,543,195 198,264,281

Gross Profit 48,065,601 53,380,061 67,202,560 74,379,926 92,013,303 112,614,685 136,148,801 150,133,941 179,939,848 198,267,066

Operating Expenses:

Operating Expenses 7,131,834 7,581,017 8,339,119 9,173,031 10,090,334 11,099,368 12,209,304 13,430,235 14,773,258 16,250,584

Depreciation 6,678,500 5,967,550 5,345,270 4,798,185 4,315,338 3,887,732 3,528,609 3,184,139 2,877,841 2,604,704

Amortization 207,000 207,000 207,000 207,000 207,000 - - - - -

14,017,334 13,755,567 13,891,389 14,178,216 14,612,672 14,987,100 15,737,913 16,614,373 17,651,099 18,855,288

Operating Profit 34,048,267 39,624,494 53,311,171 60,201,710 77,400,630 97,627,585 120,410,888 133,519,567 162,288,749 179,411,778

Interest on Loan 2,648,100 4,878,079 4,320,584 3,763,089 3,205,595 2,648,100 2,090,605 1,533,111 975,616 418,121

Interest on Lease - - - - - - - - - -

2,648,100 4,878,079 4,320,584 3,763,089 3,205,595 2,648,100 2,090,605 1,533,111 975,616 418,121

Profit before Tax 31,400,167 34,746,415 48,990,587 56,438,620 74,195,036 94,979,485 118,320,283 131,986,457 161,313,133 178,993,657

Taxation (see working) 1,201,958 13,006,180 17,913,841 20,450,298 26,601,406 33,818,388 41,876,156 46,616,794 56,842,915 62,996,681

Profit after Tax 30,198,209 21,740,235 31,076,746 35,988,322 47,593,629 61,161,097 76,444,127 85,369,662 104,470,218 115,996,976

Balance B/F - 30,198,209 51,938,443 83,015,189 119,003,511 166,597,141 227,758,238 304,202,365 389,572,027 494,042,245

Retained Earnings 30,198,209 51,938,443 83,015,189 119,003,511 166,597,141 227,758,238 304,202,365 389,572,027 494,042,245 610,039,221

Balance C/F 30,198,209 51,938,443 83,015,189 119,003,511 166,597,141 227,758,238 304,202,365 389,572,027 494,042,245 610,039,221

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

33

1111..33 PPrroojjeecctteedd CCaasshh--ffllooww SSttaatteemmeenntt

SOURCES 1 2 3 4 5 6 7 8 9 10

FROM OPERATION

Profit Before Tax 31,400,167 34,746,415 48,990,587 56,438,620 74,195,036 94,979,485 118,320,283 131,986,457 161,313,133 178,993,657

Add: Depreciation 6,678,500 5,967,550 5,345,270 4,798,185 4,315,338 3,887,732 3,528,609 3,184,139 2,877,841 2,604,704

Amortization 207,000 207,000 207,000 207,000 207,000 - - - - - 6,885,500 6,174,550 5,552,270 5,005,185 4,522,338 3,887,732 3,528,609 3,184,139 2,877,841 2,604,704

38,285,667 40,920,965 54,542,857 61,443,805 78,717,374 98,867,217 121,848,892 135,170,595 164,190,974 181,598,361

APPLICATIONCapital Expenditure - - - - - - - - - - Repayments of Loan 2,322,895 4,645,789 4,645,789 4,645,789 4,645,789 4,645,789 4,645,789 4,645,789 4,645,789 4,645,789 Tax Payment 1,201,958 13,006,180 17,913,841 20,450,298 26,601,406 33,818,388 41,876,156 46,616,794 56,842,915 62,996,681

Dividend Paid 3,524,853.19 17,651,969.64 22,559,630.02 25,096,087.30 31,247,196 38,464,178 46,521,945 51,262,584 61,488,705 67,642,471 Surplus / (Deficit) 34,760,814 23,268,995 31,983,227 36,347,718 47,470,178 60,403,040 75,326,946 83,908,011 102,702,270 113,955,891

Increase/(Decrease) In Working Capital

17,841,176 1,431,039 3,888,730 2,116,674 4,944,462 5,713,345 6,561,418 4,045,439 8,289,381 5,276,864

Net Increase/(Decrease)

16,919,638 21,837,956 28,094,497 34,231,044 42,525,716 54,689,695 68,765,528 79,862,573 94,412,889 108,679,027

Opening Bank Balances

3,000,000 19,919,638 41,757,594 69,852,091 104,083,135 146,608,851 201,298,546 270,064,074 349,926,646 444,339,535

Closing Cash Balance 19,919,638 41,757,594 69,852,091 104,083,135 146,608,851 201,298,546 270,064,074 349,926,646 444,339,535 553,018,562

WORKING CAPITAL 17,841,176 19,272,214 23,160,944 25,277,618 30,222,080 35,935,425 42,496,844 46,542,283 54,831,664 60,108,527

Increase (decrease) 17,841,176 1,431,039 3,888,730 2,116,674 4,944,462 5,713,345 6,561,418 4,045,439 8,289,381 5,276,864

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

34

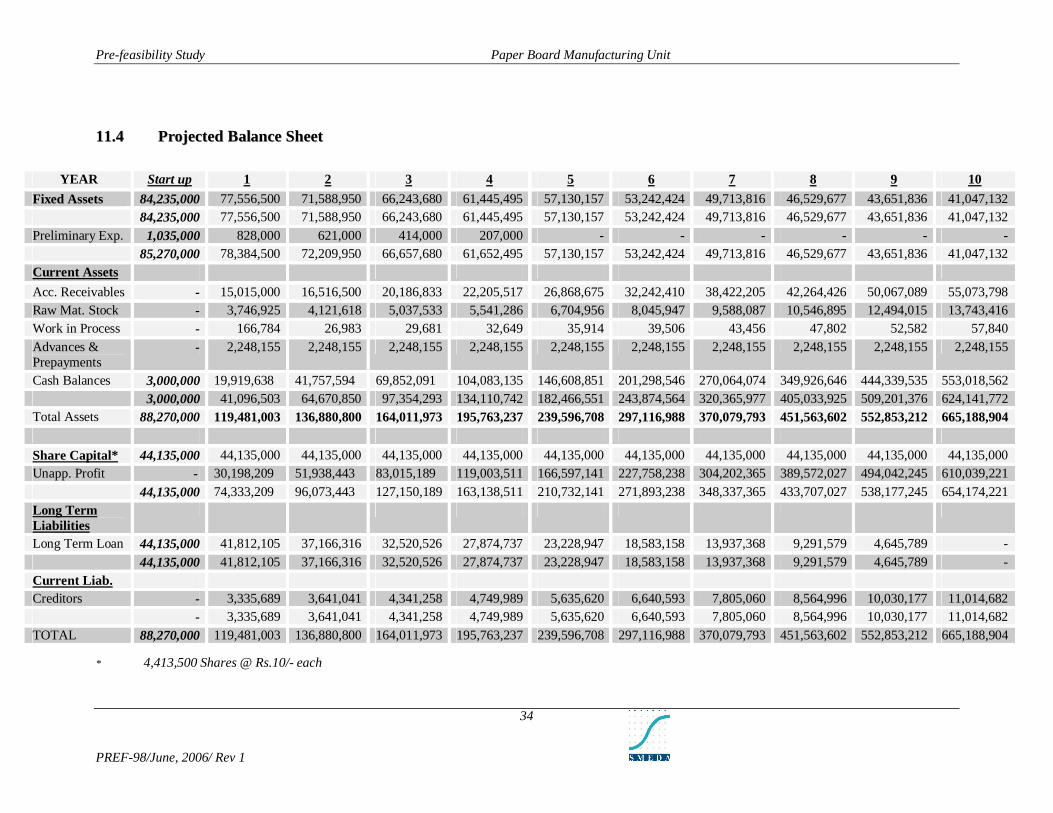

1111..44 PPrroojjeecctteedd BBaallaannccee SShheeeett

YEAR Start up 1 2 3 4 5 6 7 8 9 10

Fixed Assets 84,235,000 77,556,500 71,588,950 66,243,680 61,445,495 57,130,157 53,242,424 49,713,816 46,529,677 43,651,836 41,047,132 84,235,000 77,556,500 71,588,950 66,243,680 61,445,495 57,130,157 53,242,424 49,713,816 46,529,677 43,651,836 41,047,132

Preliminary Exp. 1,035,000 828,000 621,000 414,000 207,000 - - - - - - 85,270,000 78,384,500 72,209,950 66,657,680 61,652,495 57,130,157 53,242,424 49,713,816 46,529,677 43,651,836 41,047,132

Current Assets

Acc. Receivables - 15,015,000 16,516,500 20,186,833 22,205,517 26,868,675 32,242,410 38,422,205 42,264,426 50,067,089 55,073,798 Raw Mat. Stock - 3,746,925 4,121,618 5,037,533 5,541,286 6,704,956 8,045,947 9,588,087 10,546,895 12,494,015 13,743,416 Work in Process - 166,784 26,983 29,681 32,649 35,914 39,506 43,456 47,802 52,582 57,840 Advances & Prepayments

- 2,248,155 2,248,155 2,248,155 2,248,155 2,248,155 2,248,155 2,248,155 2,248,155 2,248,155 2,248,155

Cash Balances 3,000,000 19,919,638 41,757,594 69,852,091 104,083,135 146,608,851 201,298,546 270,064,074 349,926,646 444,339,535 553,018,562 3,000,000 41,096,503 64,670,850 97,354,293 134,110,742 182,466,551 243,874,564 320,365,977 405,033,925 509,201,376 624,141,772

Total Assets 88,270,000 119,481,003 136,880,800 164,011,973 195,763,237 239,596,708 297,116,988 370,079,793 451,563,602 552,853,212 665,188,904

Share Capital* 44,135,000 44,135,000 44,135,000 44,135,000 44,135,000 44,135,000 44,135,000 44,135,000 44,135,000 44,135,000 44,135,000 Unapp. Profit - 30,198,209 51,938,443 83,015,189 119,003,511 166,597,141 227,758,238 304,202,365 389,572,027 494,042,245 610,039,221

44,135,000 74,333,209 96,073,443 127,150,189 163,138,511 210,732,141 271,893,238 348,337,365 433,707,027 538,177,245 654,174,221 Long TermLiabilitiesLong Term Loan 44,135,000 41,812,105 37,166,316 32,520,526 27,874,737 23,228,947 18,583,158 13,937,368 9,291,579 4,645,789 -

44,135,000 41,812,105 37,166,316 32,520,526 27,874,737 23,228,947 18,583,158 13,937,368 9,291,579 4,645,789 - Current Liab.Creditors - 3,335,689 3,641,041 4,341,258 4,749,989 5,635,620 6,640,593 7,805,060 8,564,996 10,030,177 11,014,682

- 3,335,689 3,641,041 4,341,258 4,749,989 5,635,620 6,640,593 7,805,060 8,564,996 10,030,177 11,014,682 TOTAL 88,270,000 119,481,003 136,880,800 164,011,973 195,763,237 239,596,708 297,116,988 370,079,793 451,563,602 552,853,212 665,188,904

* 4,413,500 Shares @ Rs.10/- each

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

35

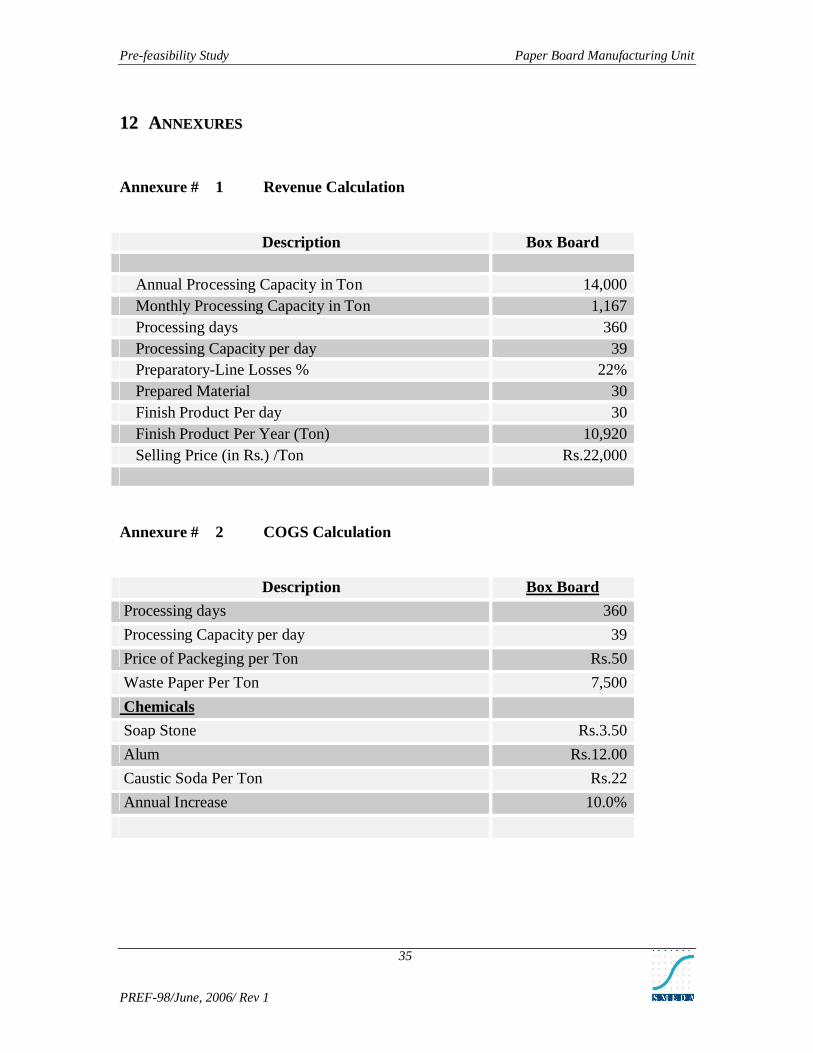

1122 AANNNNEEXXUURREESS

Annexure # 1 Revenue Calculation

Description Box Board

Annual Processing Capacity in Ton 14,000 Monthly Processing Capacity in Ton 1,167 Processing days 360 Processing Capacity per day 39 Preparatory-Line Losses % 22%Prepared Material 30 Finish Product Per day 30Finish Product Per Year (Ton) 10,920 Selling Price (in Rs.) /Ton Rs.22,000

Annexure # 2 COGS Calculation

Description Box Board

Processing days 360

Processing Capacity per day 39

Price of Packeging per Ton Rs.50

Waste Paper Per Ton 7,500

Chemicals

Soap Stone Rs.3.50

Alum Rs.12.00

Caustic Soda Per Ton Rs.22

Annual Increase 10.0%

Pre-feasibility Study Paper Board Manufacturing Unit

PREF-98/June, 2006/ Rev 1

36

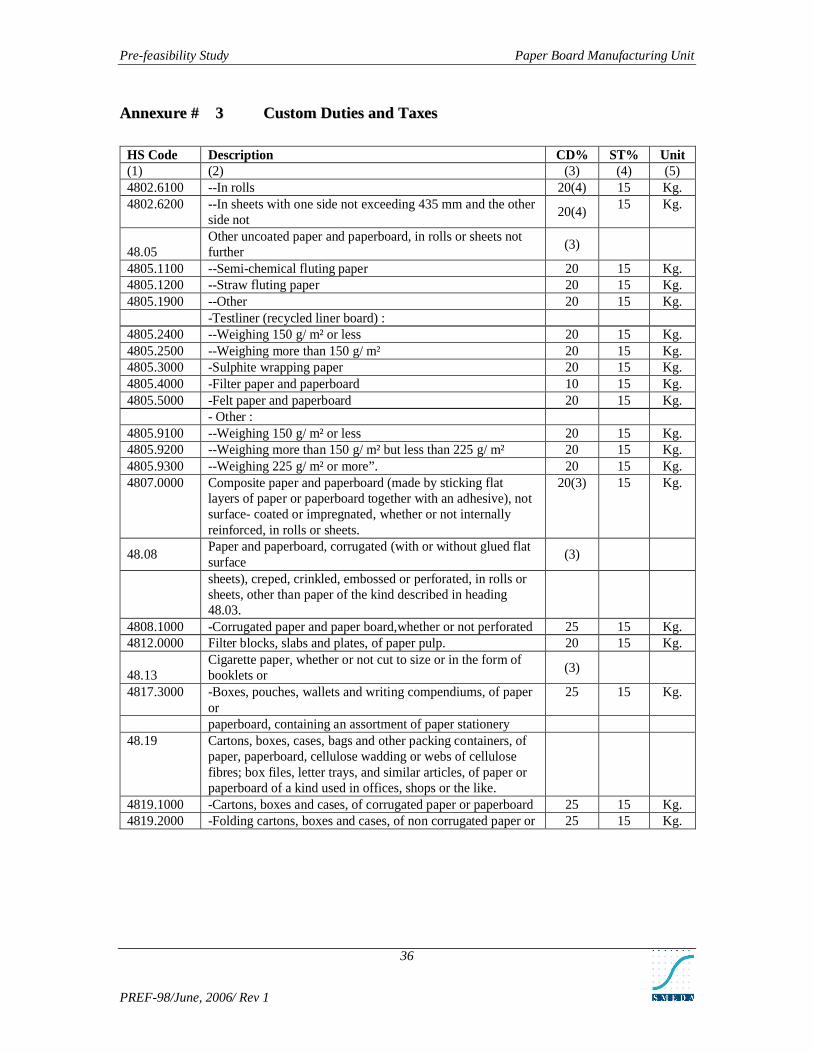

AAnnnneexxuurree ## 33 CCuussttoomm DDuuttiieess aanndd TTaaxxeess

HS Code Description CD% ST% Unit(1) (2) (3) (4) (5)4802.6100 --In rolls 20(4) 15 Kg.4802.6200 --In sheets with one side not exceeding 435 mm and the other

side not 20(4)

15 Kg.

48.05 Other uncoated paper and paperboard, in rolls or sheets not further

(3)

4805.1100 --Semi-chemical fluting paper 20 15 Kg.4805.1200 --Straw fluting paper 20 15 Kg.4805.1900 --Other 20 15 Kg.

-Testliner (recycled liner board) : 4805.2400 --Weighing 150 g/ m² or less 20 15 Kg.4805.2500 --Weighing more than 150 g/ m² 20 15 Kg.4805.3000 -Sulphite wrapping paper 20 15 Kg.4805.4000 -Filter paper and paperboard 10 15 Kg.4805.5000 -Felt paper and paperboard 20 15 Kg.

- Other : 4805.9100 --Weighing 150 g/ m² or less 20 15 Kg.4805.9200 --Weighing more than 150 g/ m² but less than 225 g/ m² 20 15 Kg.4805.9300 --Weighing 225 g/ m² or more”. 20 15 Kg.4807.0000 Composite paper and paperboard (made by sticking flat

layers of paper or paperboard together with an adhesive), not surface- coated or impregnated, whether or not internally reinforced, in rolls or sheets.

20(3) 15 Kg.

48.08 Paper and paperboard, corrugated (with or without glued flat surface

(3)

sheets), creped, crinkled, embossed or perforated, in rolls or sheets, other than paper of the kind described in heading 48.03.

4808.1000 -Corrugated paper and paper board,whether or not perforated 25 15 Kg.4812.0000 Filter blocks, slabs and plates, of paper pulp. 20 15 Kg.

48.13 Cigarette paper, whether or not cut to size or in the form of booklets or

(3)