solvency and financial condition report 2016 · solvency and financial condition report 2016 5 the...

TRANSCRIPT

SOLVENCY AND FINANCIAL CONDITIONREPORT 2016REPORT OF VIENNA INSURANCE GROUP AGWIENER VERSICHERUNG GRUPPE

(17.05 – J20176540)

3

SUMMARY ____________________________________________________________________________________ 5

DECLARATION BY THE MANAGING BOARD ______________________________________________________________ 6 A BUSINESS ACTIVITIES AND PERFORMANCE ___________________________________________________________ 7

A.1 Business _____________________________________________________________________________________ 8

A.2 Underwriting performance ________________________________________________________________________ 10

A.3 Investment performance _________________________________________________________________________ 11

A.4 Performance of other activities ____________________________________________________________________ 11

A.5 Any other information ___________________________________________________________________________ 11

B SYSTEM OF GOVERNANCE ______________________________________________________________________ 13 B.1 General information on the system of governance _______________________________________________________ 14

B.2 Fit and proper requirements ______________________________________________________________________ 29

B.3 Risk management system, including the own risk and solvency assessment ___________________________________ 30

B.4 Internal Control System _________________________________________________________________________ 37

B.5 Internal audit function ___________________________________________________________________________ 40

B.6 Actuarial function ______________________________________________________________________________ 41

B.7 Outsourcing __________________________________________________________________________________ 41

B.8 Any other information ___________________________________________________________________________ 42

C RISK PROFILE ________________________________________________________________________________ 43 C.1 Underwriting Risk _____________________________________________________________________________ 44

C.2 Market Risk _________________________________________________________________________________ 48

C.3 Credit Risk ___________________________________________________________________________________ 50

C.4 Liquidity Risk _________________________________________________________________________________ 51

C.5 Operational Risk ______________________________________________________________________________ 52

C.6 Other material Risks ____________________________________________________________________________ 54

C.7 Any other Information ___________________________________________________________________________ 56

D VALUATION FOR SOLVENCY PURPOSES _____________________________________________________________ 65 D.1 Assets ______________________________________________________________________________________ 65

D.2 Technical provisions ____________________________________________________________________________ 67

D.3 Other liabilities _______________________________________________________________________________ 70

D.4 Alternative methods for valuation __________________________________________________________________ 72

D.5 Any other information ___________________________________________________________________________ 72

E CAPITAL MANAGEMENT ________________________________________________________________________ 73 E.1 Own funds ___________________________________________________________________________________ 73

E.2 Solvency capital Requirement and Minimum Capital Requirement ___________________________________________ 79

E.3 Use of the duration-based equity risk sub-module in the calculating of Solvency Capital Requirement _________________ 80

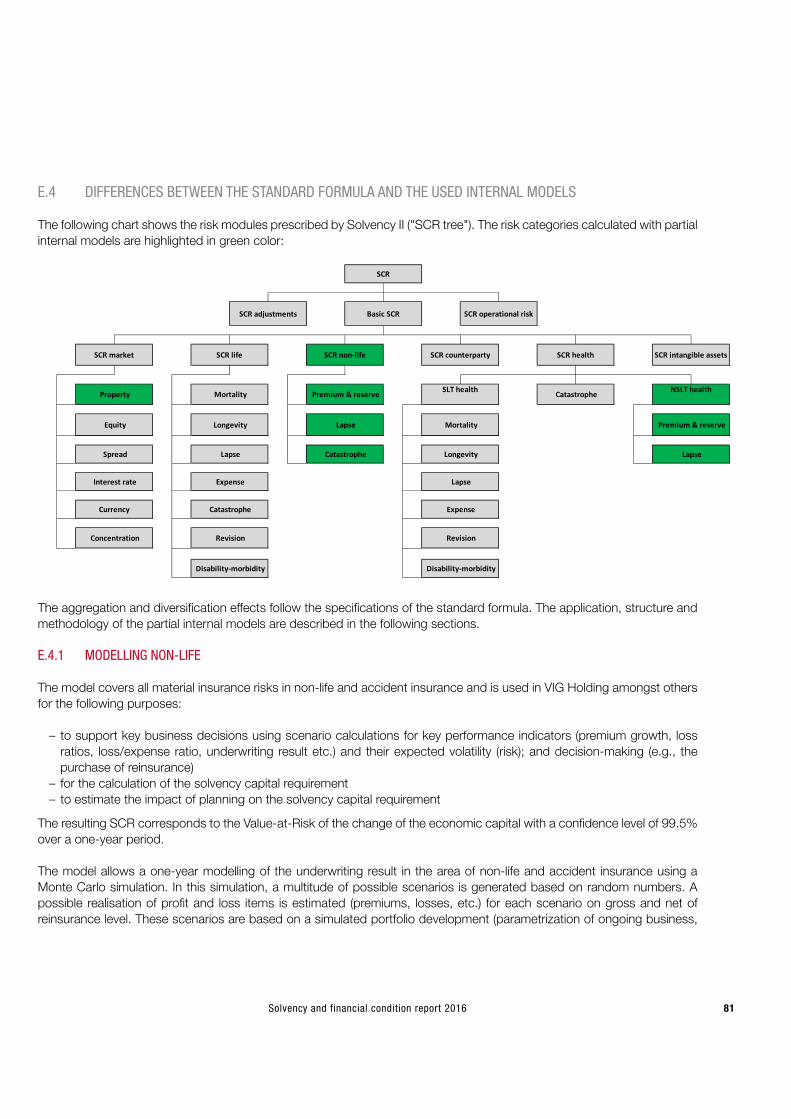

E.4 Differences between the standard formula and any internal model used ______________________________________ 81

E.5 Non-compliance with the Minimum Capital Requirement and non-compliance with the Solvency Capital Requirement _____ 83

E.6 Any other information ___________________________________________________________________________ 83

LIST OF ABBREVIATIONS _________________________________________________________________________ 87

ANNEX ______________________________________________________________________________________ 90

Contents

4 Vienna Insurance Group Holding

Solvency and financial condition report 2016 5

The reporting structure follows the requirements of implementing regulation (EU) 2015/35 and is divided into Sections A to

E with specified sub-sections. The solvency and financial position of VIG Holding as a separate company is reported in the

respective sections in accordance with the legal requirements. The holding company holds the participations in the opera-

tive insurance companies of the Group. For reasons of transparency and materiality in accordance with Article 291 of the

Delegated Regulation, it is therefore useful to address the economic group solvency and financial position separately. The

economic group solvency is assessed under the aspect of a look through of participations and is therefore similar to the

look-through approach, as required under IFRS for full consolidation. This publication has been prepared on a voluntary

basis pursuant to Article 298 of the Delegated Regulation. In this report, VIG Holding represents the individual Company

and VIG Group represents the Group. The statements made in this report are based on market parameters in key areas,

assumptions and estimates. This is particularly the case in areas with high measurement scope and / or complexity.

Section A discusses business activities and performance. VIG Holding is primarily responsible for managerial tasks within

the VIG Group. Corporate business and reinsurance transactions are also performed.

Section B describes the governance system. The term "governance" essentially includes all management processes and

the effective and efficient monitoring of a company or Group. The key elements of the governance system are the Managing

Board, the Supervisory Board, the governance and key functions, the risk management system and the internal control

system (ICS).

This section also deals with the remuneration policy and remuneration practices in addition to the requirements and evalu-

ation process for the professional qualifications and personal reliability of key functions etc.

VIG Holding's risk profile is described in Section C. The risk profile of VIG Holding is sub-categorised into underwriting risk,

market risk, credit risk, liquidity risk, operational risk and other risks and described in Sections C.1 to C.6. The economically

appropriate risk profile of the VIG Group is discussed under C.7 Other information.

Section D describes the valuation of VIG's assets and liabilities for solvency purposes (economic balance sheet). The meth-

ods are mainly defined by Delegated Regulation (EU) 2015/35 of the European Union and by the Austrian Insurance Super-

vision Act (ISA). The valuation is based on the market value principle, and measurement differences compared to prevailing

accounting standards are discussed.

The economic equity capital, minimum capital requirement and solvency capital requirement are shown in Section E, taking

into account the partial internal model approved by the regulatory authorities. At the reporting date 31 December 2016,

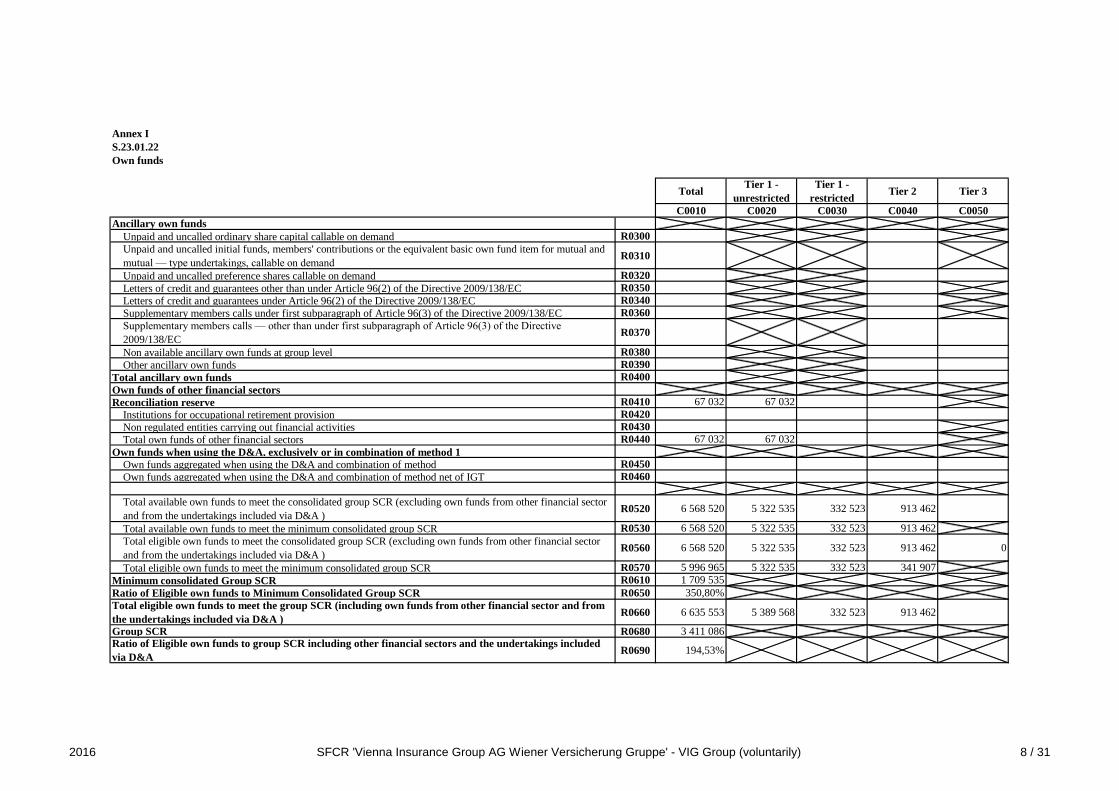

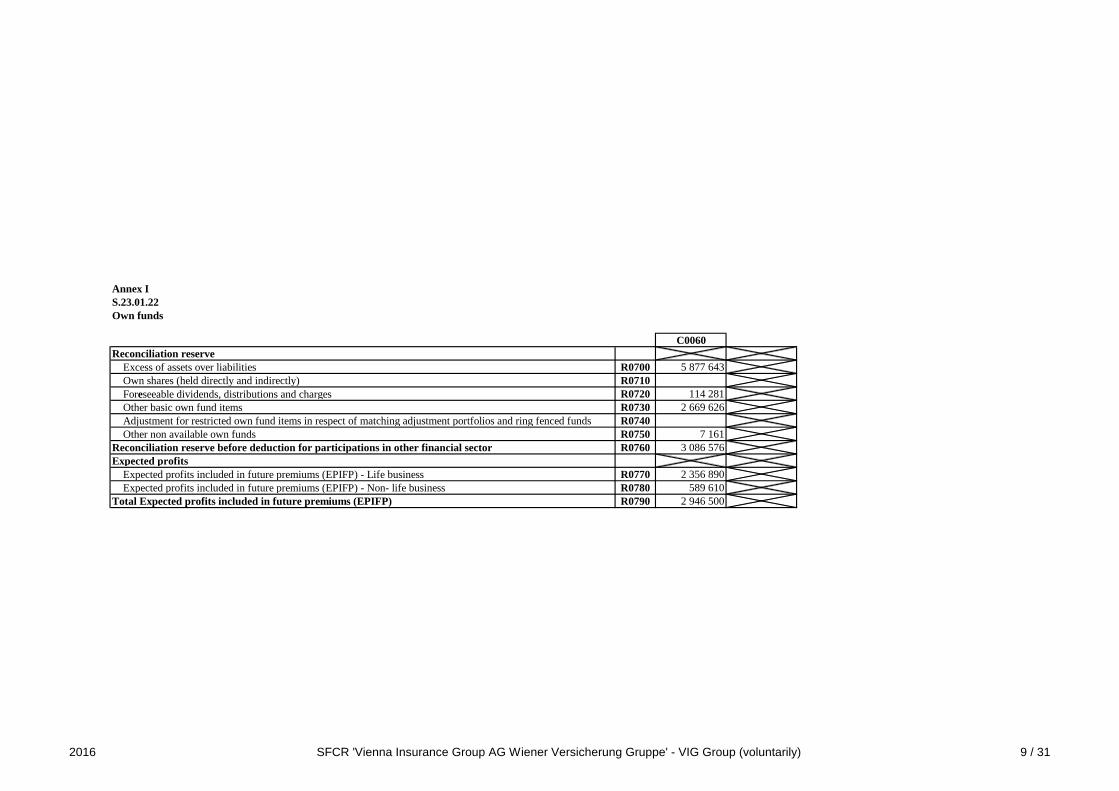

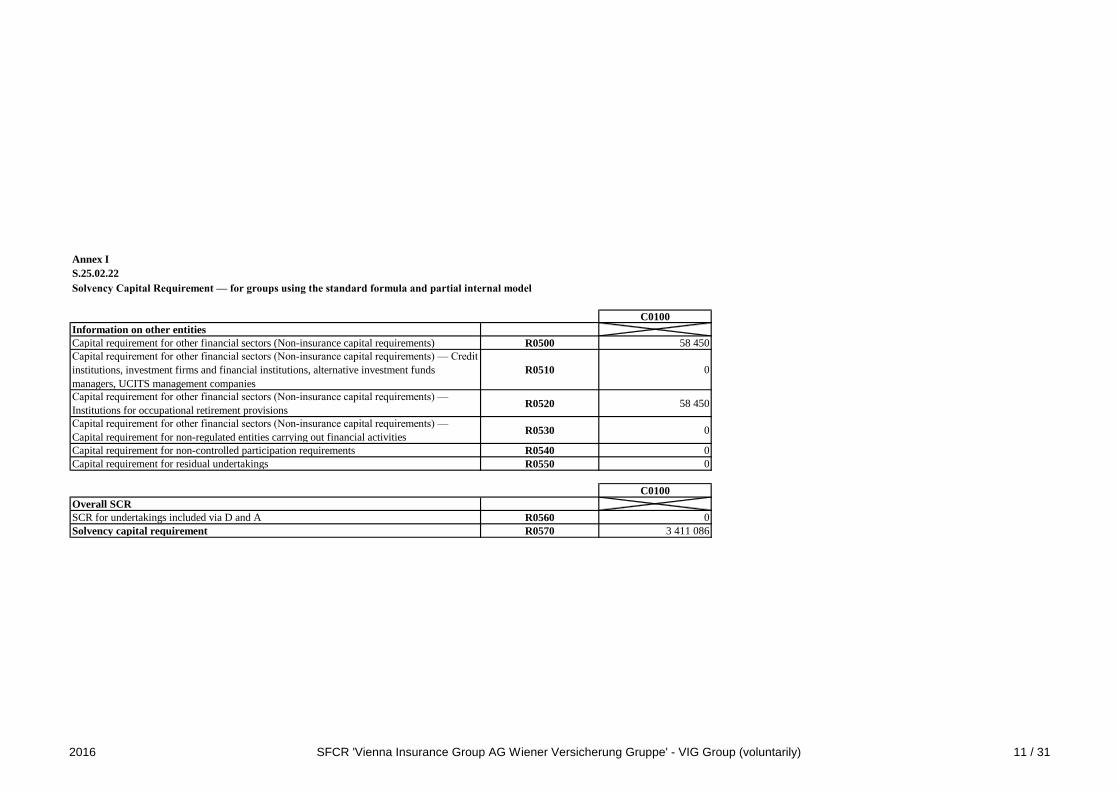

VIG Holding had a solvency ratio of 389.9% as a separate company. An economic solvency ratio of 194.5% was determined

for the VIG Group.

In accordance with Article 2 of implementing regulation (EU) 2015/2452 of the Commission of 2 December 2015, numbers

in this report which reflect an amount of money are specified in thousand euros (TEUR).

Summary

6 Vienna Insurance Group Holding

We confirm to the best of our knowledge that the Solvency and Financial Condition Report of VIENNA INSURANCE GROUP

AG Wiener Versicherung Gruppe, which has been prepared in accordance with the provisions of the Austrian Insurance

Supervision Act and the corresponding directly applicable rules at European level, gives a true picture of the solvency and

financial situation of the Company and that it describes the business development, governance system, risk profile and

assets, liabilities, and equity capital of the solvency balance.

Vienna, 19 April 2017

The Managing Board:

Elisabeth Stadler

General Manager,

Chairwoman of the Managing Board

Franz Fuchs

Member of the Managing Board

Roland Gröll

Member of the Managing Board

Judit Havasi

Member of the Managing Board

Peter Höfinger

Member of the Managing Board

Martin Simhandl

CFO, Member of the Managing Board

DECLARATION BY THE MANAGING BOARD

Solvency and financial condition report 2016 7

This report contains all information required by law regarding the solvency and financial situation of

VIENNA INSURANCE GROUP AG Wiener Versicherung Gruppe

Stock corporation with its registered office in 1010 Vienna, Schottenring 30, registered with the

Vienna Commercial Court under FN 75687f

Tel.: +43 (0) 50 390-22000

www.vig.com

Important information regarding the solvency and financial situation of VIG Holding is communicated to the public to ensure

transparency.

The competent supervisory authority for the Company and the Group to which the Company belongs is the

Austrian Financial Market Authority (FMA)

Otto-Wagner-Platz 5, 1090 Vienna

Tel.: +43 (1) 249 59-0

www.fma.gv.at

The audit of the accuracy of this report and the information contained therein was performed by

KPMG Austria GmbH Wirtschaftsprüfungs- und Steuerberatungsgesellschaft

Porzellangasse 51, 1090 Vienna

Tel.: +43 (0) 1 31332-0

www.kpmg.at

Supplementary notes

In accordance with a letter from the FMA (FMA VU000.110/0003-VPQ/2016) of 17 October 2016, this report contains no

comparison with the information provided in the previous reporting period.

For the sake of readability, the masculine form has been used in this text. Our goal was to make the annual report as quick

and easy to read as possible. It should be understood that the text always refers to women and men equally without

discrimination.

A. Business and Performance

8 Vienna Insurance Group Holding

A.1 BUSINESS

VIG Holding, based in Vienna, is involved in 50 insurance operations in 25 countries employing over 24,000 people. Group-

wide guidelines exist in order to standardise the handling of significant risks throughout the Group, and also provide a tool

for risk monitoring. The requirements set in the investments and reinsurance areas are particularly strict. Local management

is responsible for implementing these guidelines in the individual Group companies.

The following graphic shows a simplified Group structure of the insurance operations.

As early as in 1990, the former Wiener Städtische Versicherung AG created the foundations for a successful expansion into

Central and Eastern Europe (CEE). The reorganisation of the Group holding company VIENNA INSURANCE GROUP AG

Wiener Versicherung Gruppe, based in Vienna, in 2010 was the result of the expansion actively pursued by VIG over the

past two decades. VIG Holding had approximately 230 employees at the end of 2016, who primarily work in the areas of

insurance reinsurance, corporate business and control areas, within the scope of which they take over the management of

risk in the form of, for example, enterprise risk management and asset risk management. They are in contact with the Group

companies so that both the interests of the individual companies and those of the Group are safeguarded. The Group

companies are monitored by the respective Supervisory Boards, in which members of the Managing Board of VIG Holding

are always represented.

Solvency and financial condition report 2016 9

In addition to framework guidelines in all key areas, the central risk management of VIG Holding provides the central mod-

elling tools for the individual companies. Strict requirements are defined, particularly in the field of asset management and

reinsurance, which also apply to VIG Holding as a separate company. The Group also puts great importance on taking own

responsibility of each Group company.

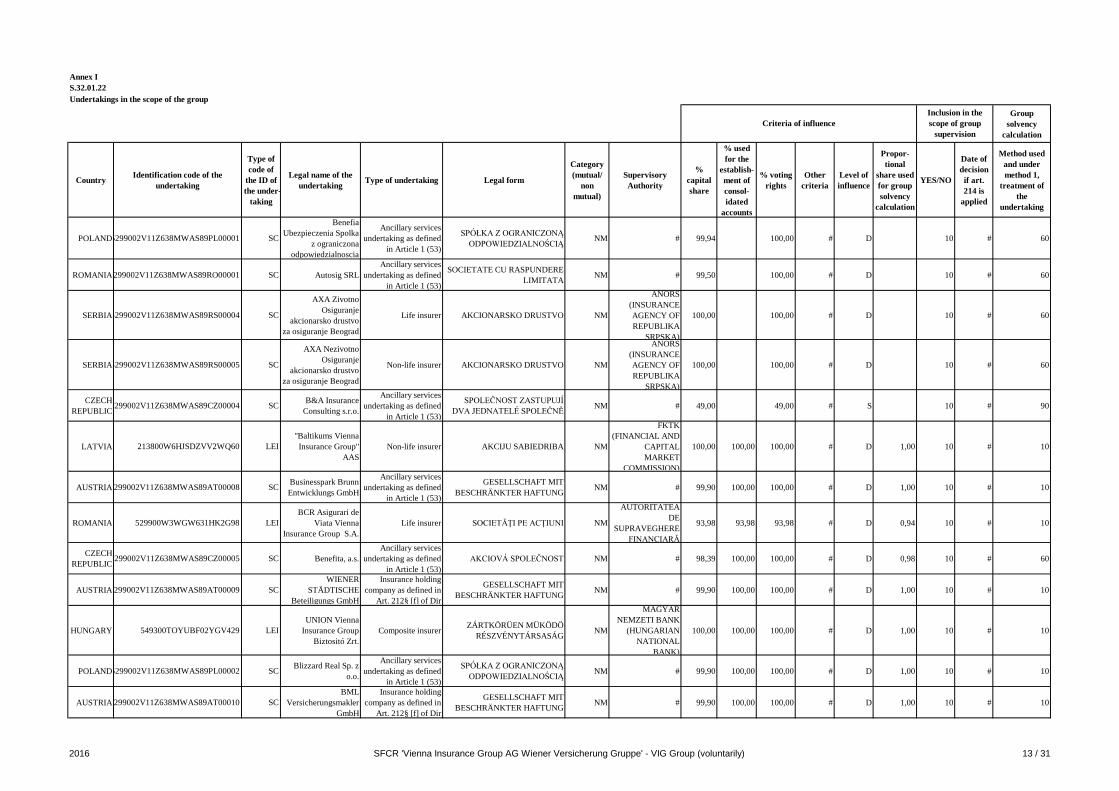

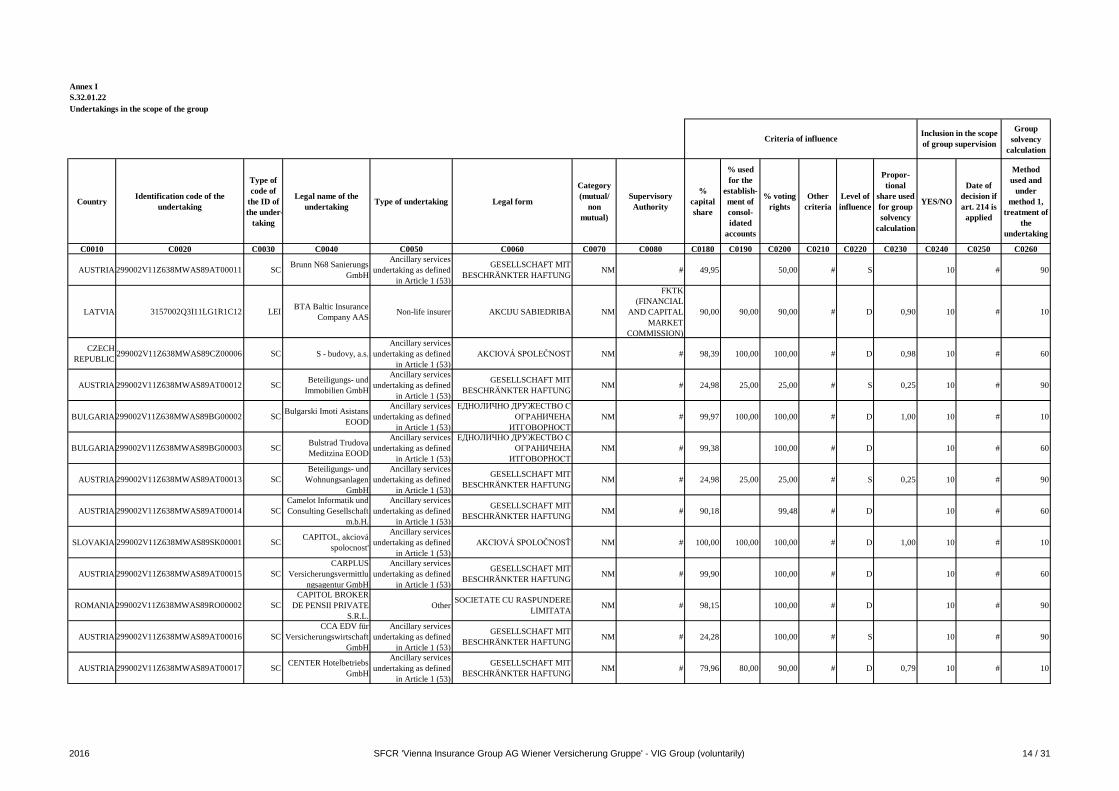

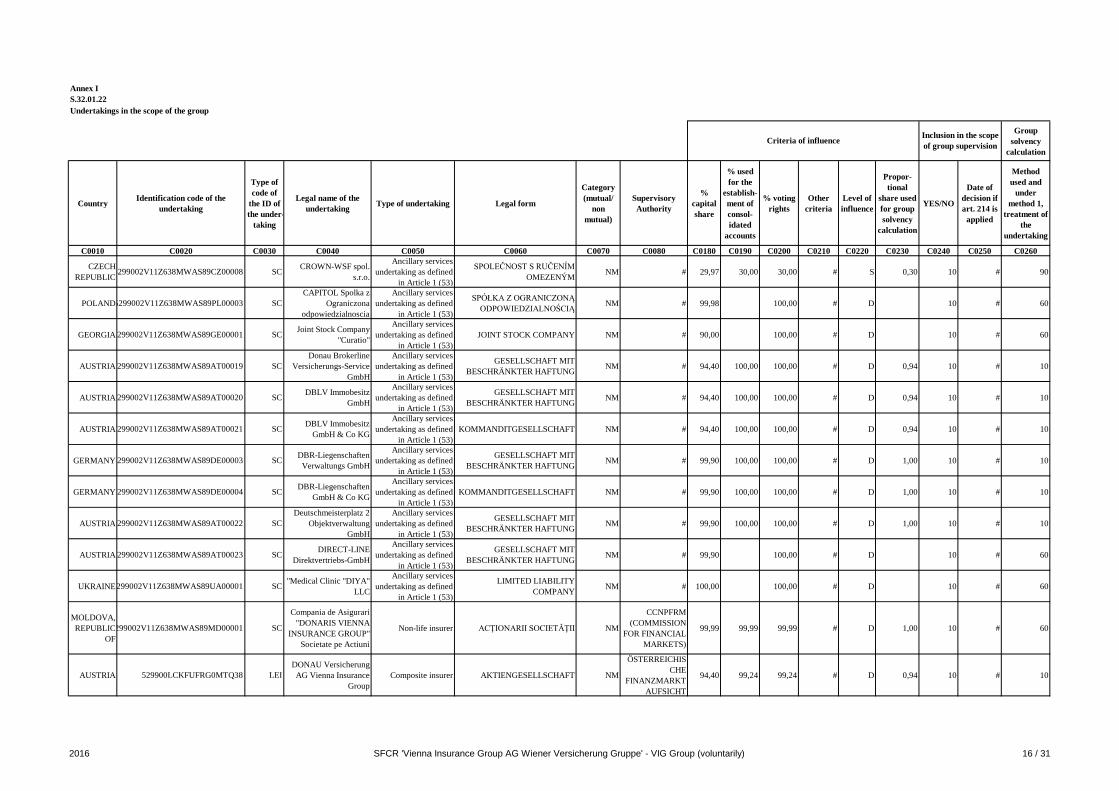

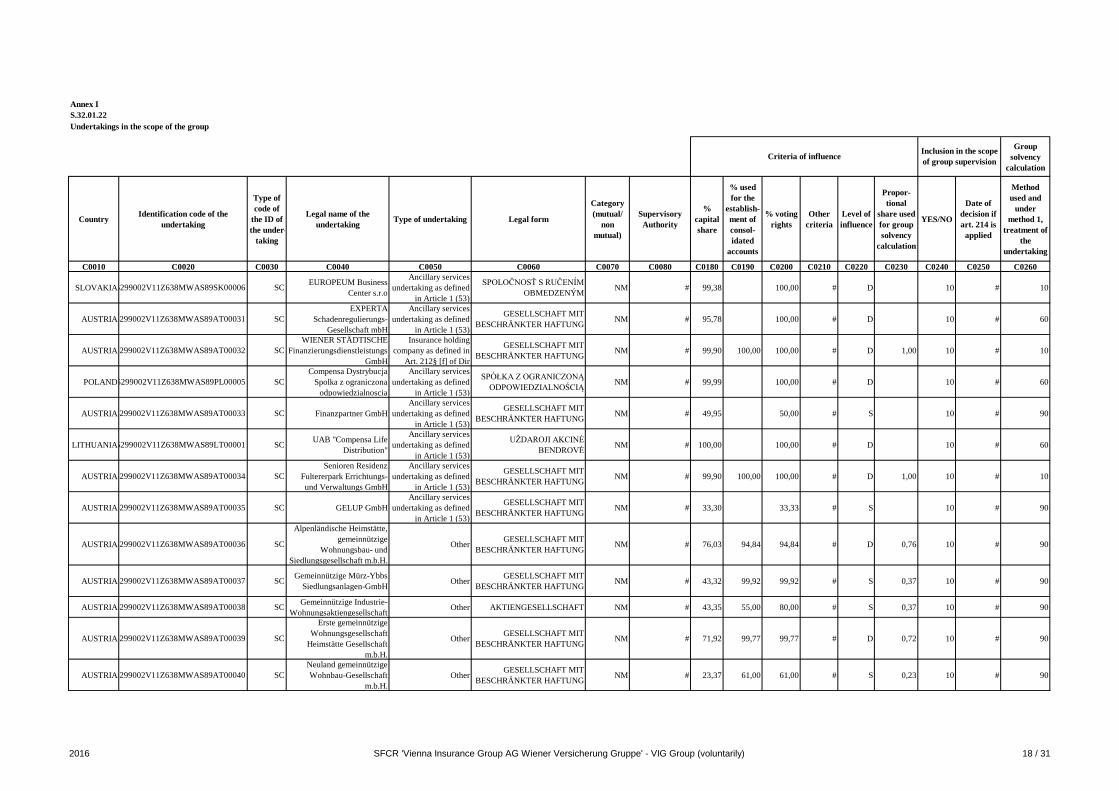

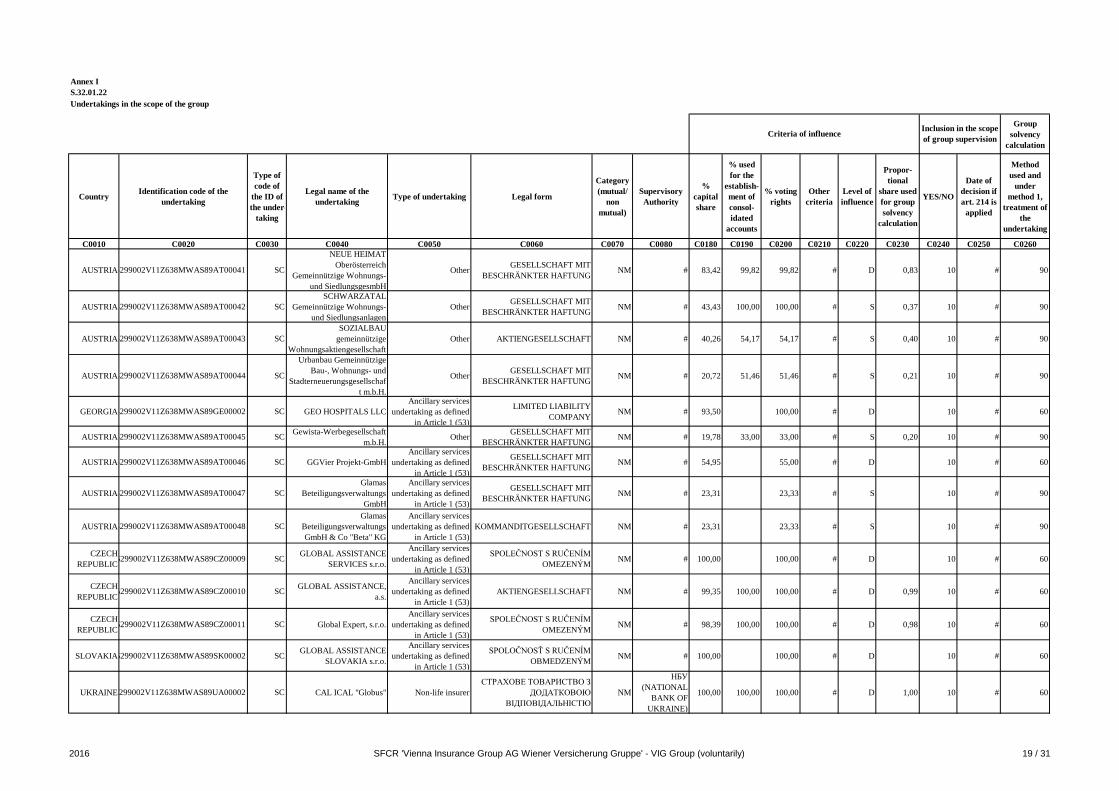

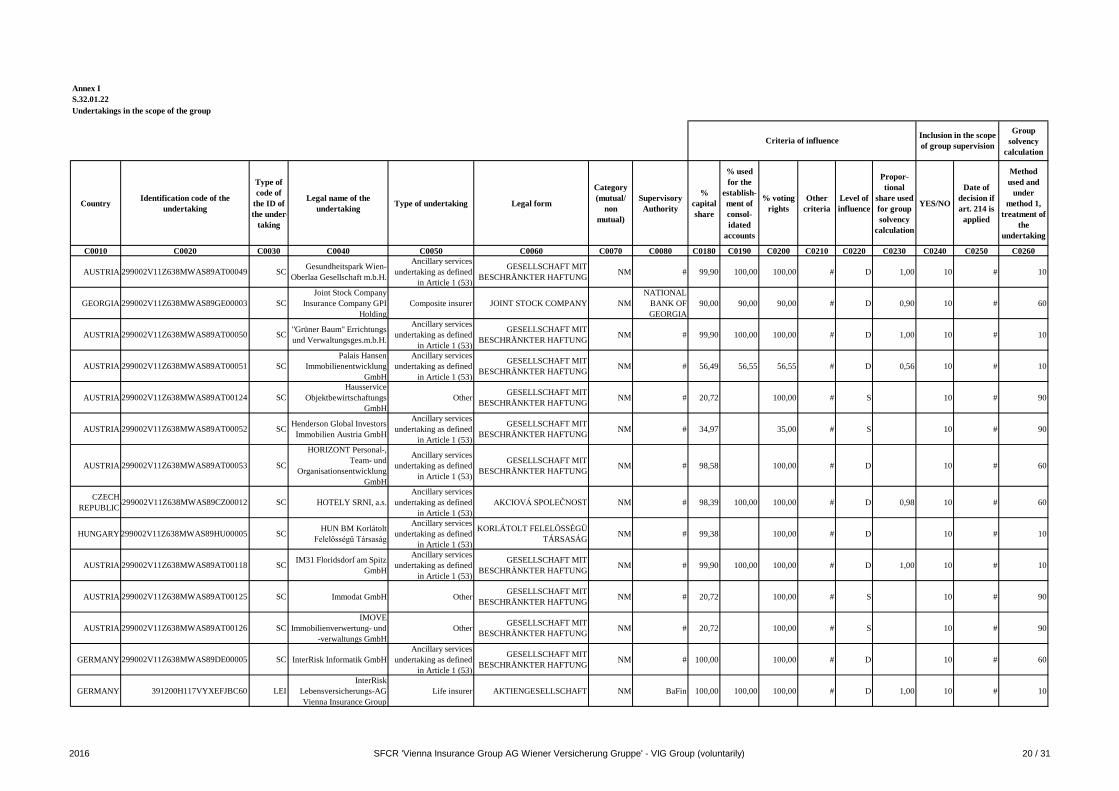

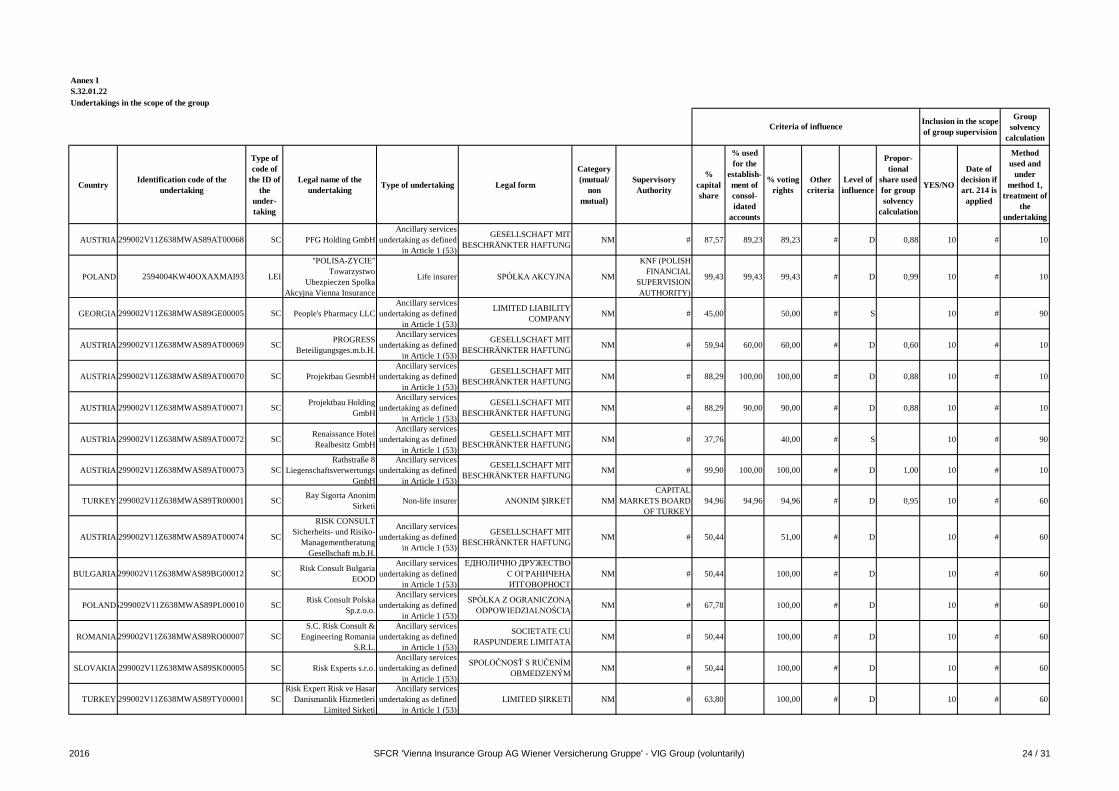

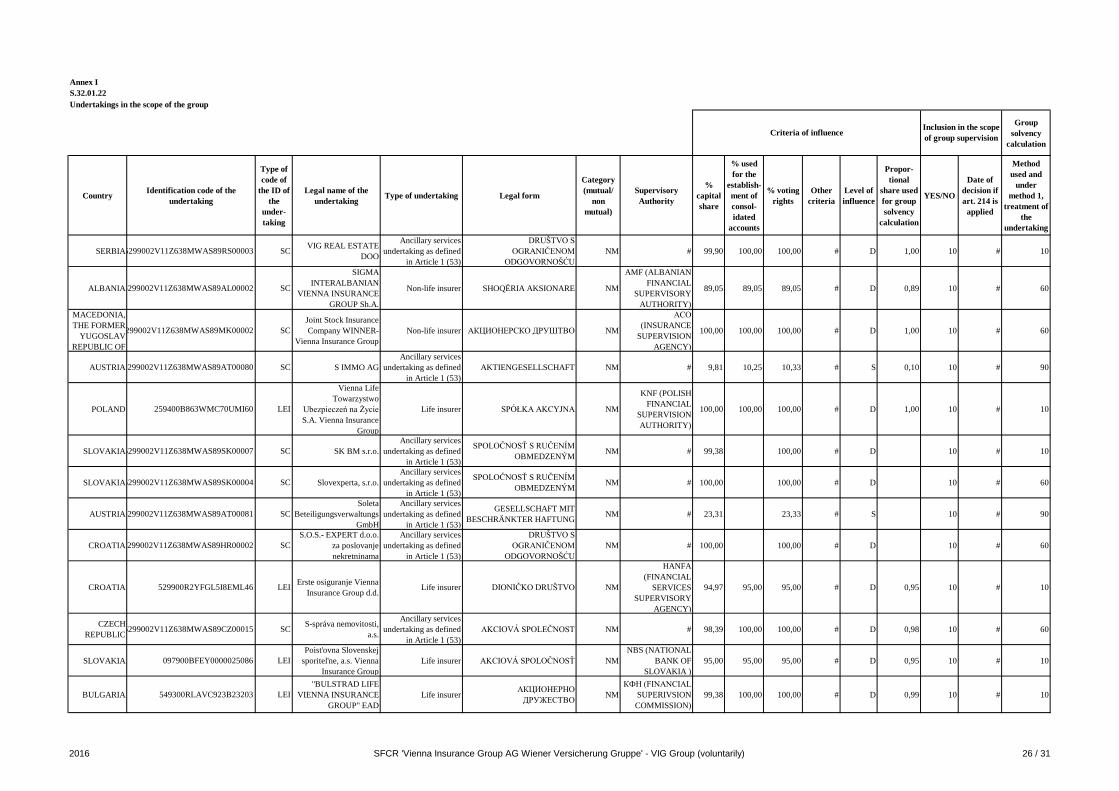

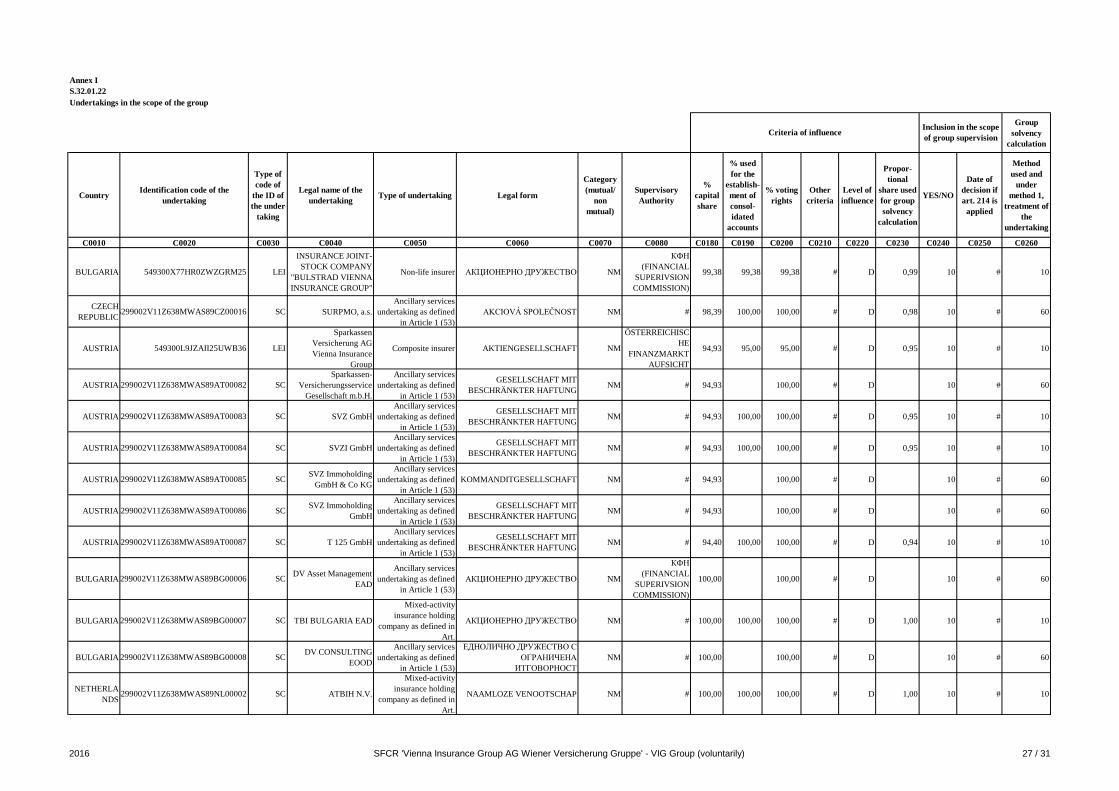

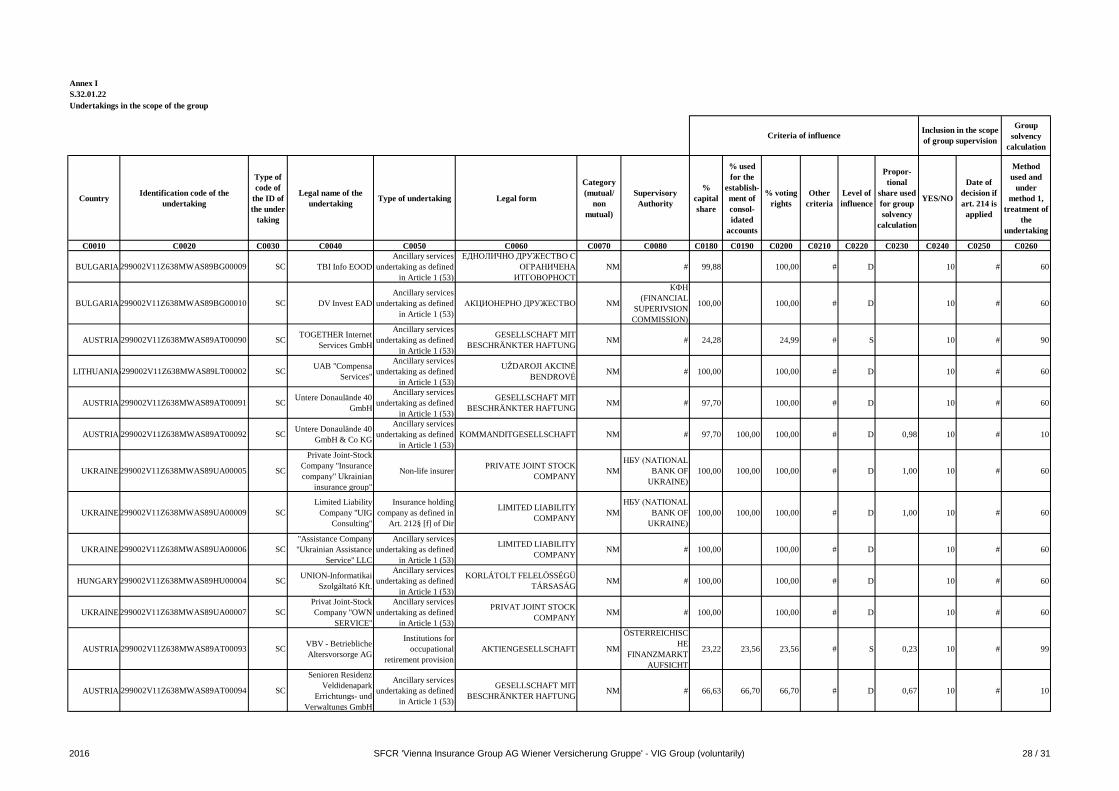

A list of all subsidiaries, affiliated companies and branches of VIG Holding, including their name, legal form and participation

quota, can be found in the Appendix to this report.

VIG Holding's area of operations also includes cross-border companies and international reinsurance transactions.

In the area of reinsurance, VIG Holding controls and supports the Group companies with all reinsurance operations. Pooling

different risks ensures an important balancing of risks at the Group level that in turn ensures optimal external reinsurance

protection for VIG as a whole. The primary goal is to create a safety net. This is intended to provide continuous protection

for all of the companies in the Group against the negative effects of large losses and negative changes in entire insurance

portfolios.

Large customer business beyond the borders of Austria is also bundled and coordinated by VIG Holding. Customised and

professional insurance solutions for international customers are essential, particularly for corporate customer business. To

this end, VIG Holding has set up its own insurance platform, Vienna International Underwriters (VIU), which is specifically

designed for business clients. Its extensive network offers competent and individual cross-border support in this area, which

is provided by experts in Austria and the CEE region.

SIGNIFICANT BUSINESS EVENTS

VIG Holding decided on 5 December 2016 to terminate the two supplementary capital bonds issued on 12 January 2005

with effect until 12 January 2017 and repay them prematurely at their repayment amount of 100% of its nominal amount

plus all interest accrued up to the redemption date.

Ownership structure

The principal shareholder of VIG Holding is Wiener Städtische Wechselseitiger Versicherungsverein, Vermögensverwaltung,

Vienna Insurance Group (a mutual insurance company headquartered at 1010 Vienna, Schottenring 30), which holds

around 70% of the shares (directly and indirectly). The remaining 30% are in free float.

In its capacity as the principle shareholder, Wiener Städtische Versicherungsverein primarily supports VIG in cultural and

social matters. Great emphasis is placed on cross-border cultural exchanges, while the activities of socially active organi-

sations are also supported within the framework of cooperation and initiatives - mainly in Central and Eastern European

countries where the Group operates.

10 Vienna Insurance Group Holding

A.2 UNDERWRITING PERFORMANCE

Underwriting performance in significant lines of business

Overall, VIG Holding generated a gross premium volume of TEUR 967,400 in financial year 2016. The written premium

volume after reinsurance amounts to TEUR 931,035 and TEUR 918,894 following adjustment for unearned premiums.

The predominant share of the premium volume is attributable to the indirect business. Net income from indirect business

amounted to TEUR 25,852. The net earned premiums in indirect business, which amounted to TEUR 875,453, were con-

temporaneously included in the income statement.

The underwriting result in accordance with the local GAAP amounts to TEUR 19,381.

The Combined Ratio is the ratio used in property and casualty insurance to describe the ratio of administrative expenses

and insurance payments to net earned premiums. In 2016, VIG Holding had a ratio of 98.1% (net of reinsurance assets),

which is less than 100%.

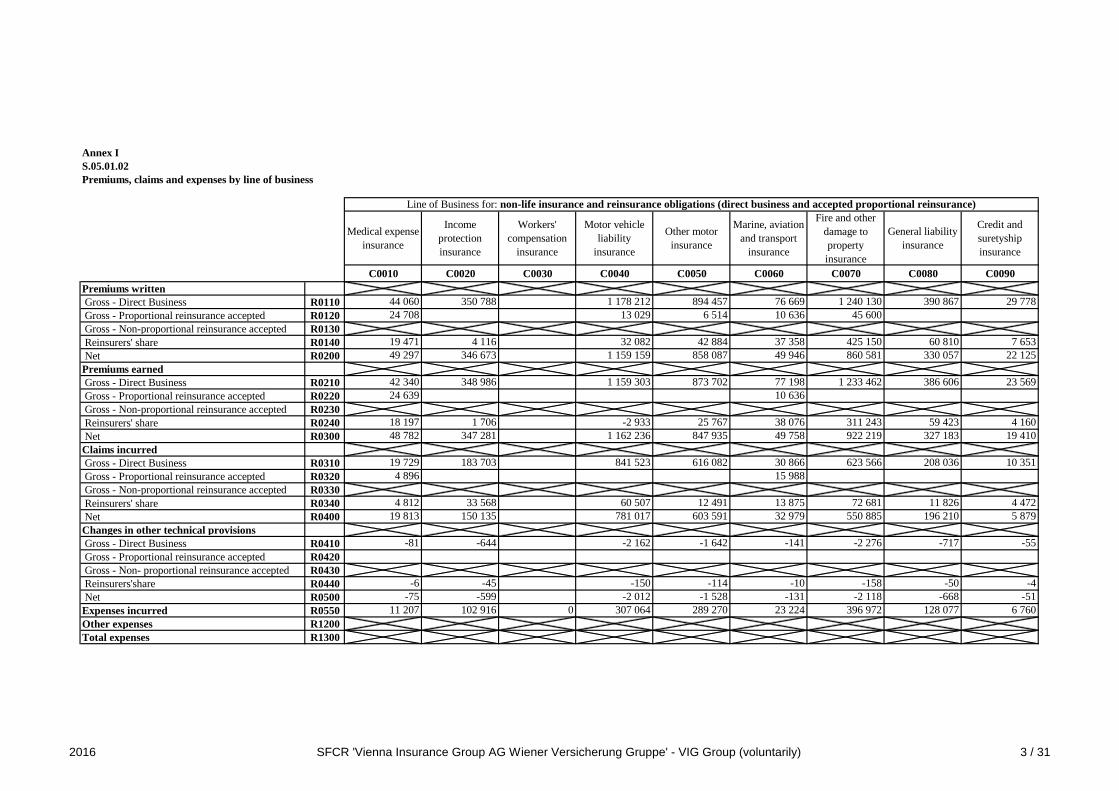

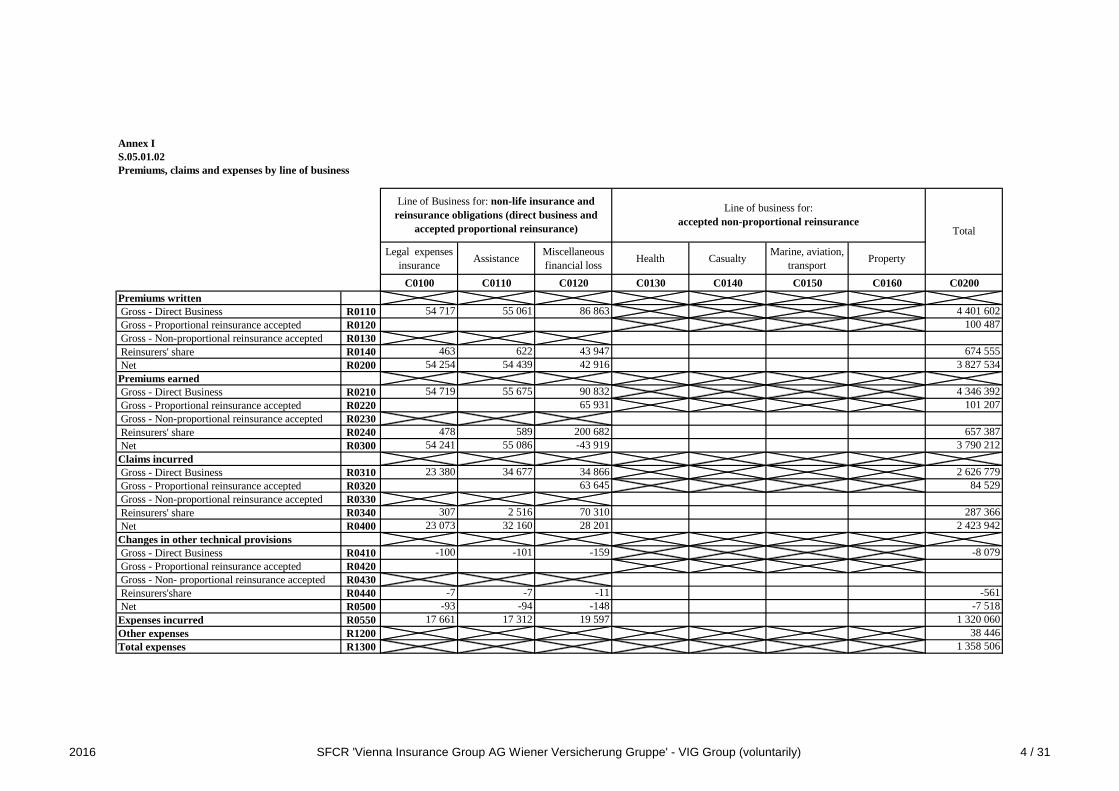

The following table shows the values of the lines of business for non-life insurance after reinsurance (excluding investment

income).

Income compensation

insurance

Motor liability insurance

Other motor insurance

Marine, aviation and

transport insurance

Fire and other property lines

General liability

insurance

Total

in TEUR

Premiums written 269,367 601,312 4,872 1,013 53,086 1,385 931,035

Net earned premiums 267,383 590,643 4,738 1,014 53,814 1,301 918,894

Expenses for claims and insurance benefits -138,426 -443,493 -4,522 -1,001 -38,296 -1,123 -626,860

Changes to other underwriting provisions* 0 0 0 -114 -5,989 -164 -6,267

Other costs -137,104 -192,706 -1,027 -844 -12,824 -328 -344,833

* Exclusive cost items

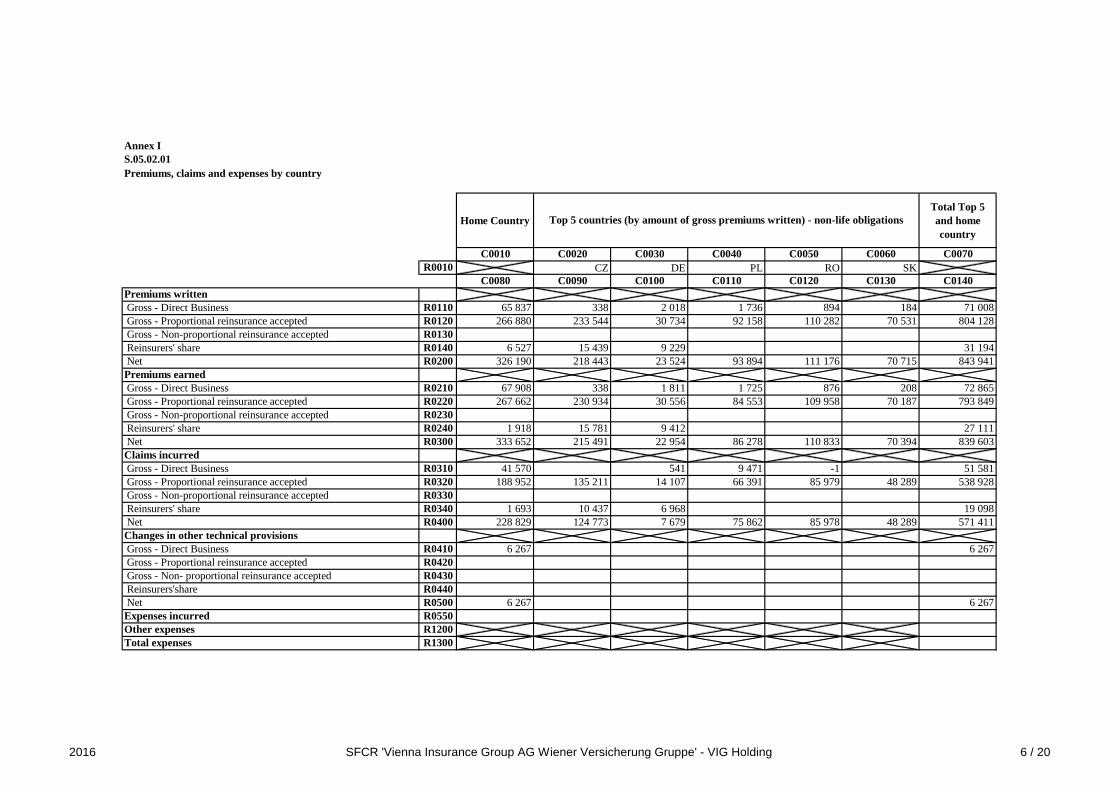

The following table represents the premiums and expenses for claims and insurance benefits of the five most important countries.

Austria Czech Republic Slovakia Poland Romania

in TEUR

Premiums written 326,190 218,443 70,715 93,894 111,176

Net earned premiums 333,652 215,491 70,394 86,278 110,833

Expenses for insurance claims* 228,829 124,773 48,289 75,862 85,978

* Exclusive cost items

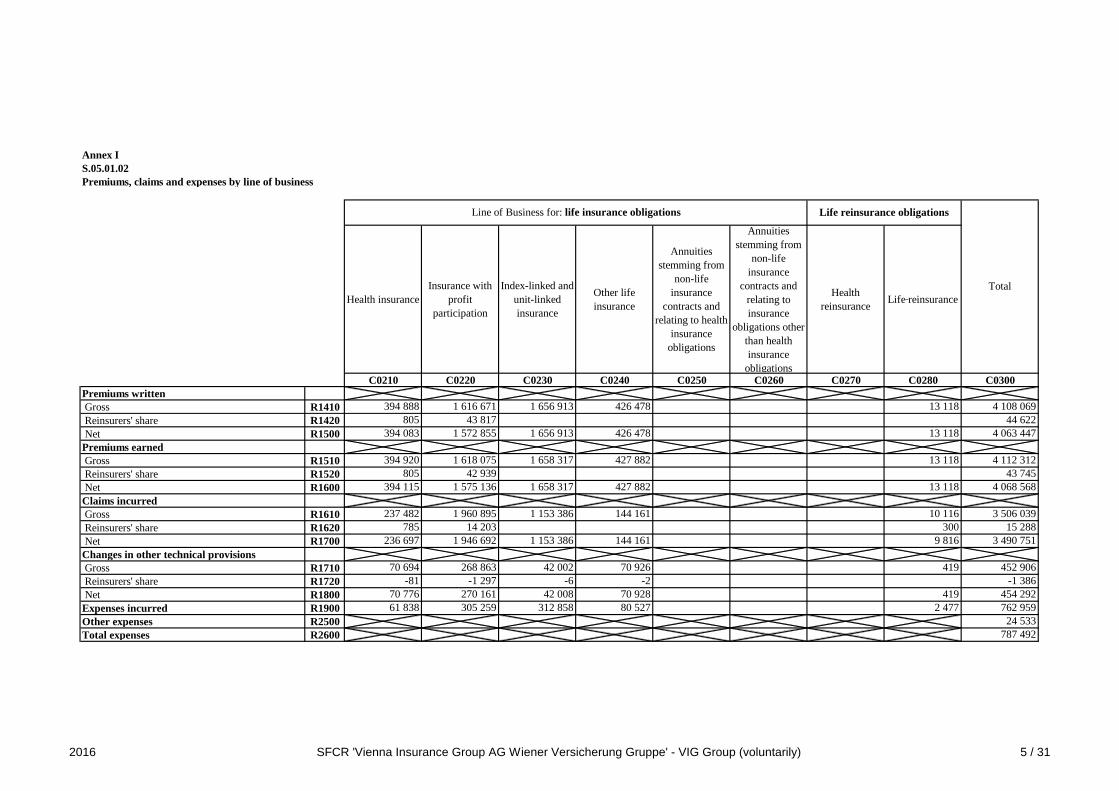

A detailed review of the underwriting performance is presented in the attachment QRT S 05.01.02.

Solvency and financial condition report 2016 11

A.3 INVESTMENT PERFORMANCE

Income and expenses for investment business

The investments of VIG Holding are managed by taking care of the Company´s overall risk situation in fixed income invest-

ments, real estate, participations, loans and shares. When determining volumes and limiting open transactions, the risk

content of intended categories have to be taken into consideration.

In 2016, VIG Holding recorded the income and expenses shown in the following table within the scope of the profit and

loss account.

Dividends Interest Rent Net profit and loss Unrealised gains and losses

in TEUR

Investments 303,702 17,839 14,088 45 45,619

Real estate 0 0 14,088 0 33,180

Shares 296,813 0 0 0 402

Government bonds 0 572 0 1 459

Corporate bonds 0 13,843 0 45 2,525

Loans and mortgages 0 3,277 0 0 -283

Undertakings for collective investment 6,888 0 0 0 9,052

Derivatives 0 0 0 0 283

Cash and cash equivalents 0 146 0 0 0

Extraordinary depreciation amounted to TEUR 140,798 in the financial year.

The income from deposits from indirect business was transferred to the technical account.

There are no securitization exposures within the portfolio of VIG Holding.

As the local GAAP sheet does not know any gains or losses directly recognised in the shareholders' equity, no information

can be provided.

A.4 PERFORMANCE OF OTHER ACTIVITIES

There were no significant other income or expenses in the 2016 financial year.

The following remarks are provided for the non-balance sheet contingencies: There are letters of comfort and undertaking

of liability in the total amount of TEUR 44,103 in connection with borrowing against affiliated companies.

VIG Holding has no significant lease agreements.

A.5 ANY OTHER INFORMATION

VIG Holding primarily focuses on managerial tasks for the Group, which is active in 25 countries. With more than 24,000

employees, the Group is a market leader in its markets in Austria and CEE.

The focus of activities on insurance operations as a clear core business, customer loyalty and proximity to customers in

Austria and Central and Eastern Europe are decisive factors for the success of VIG. Our local employees know the needs

of their customers the best, which is why VIG places its trust in these employees and local management. In order to create

12 Vienna Insurance Group Holding

stability and trust, the Group uses a multi-brand strategy that retains established brands and unites them under the Vienna

Insurance Group umbrella. This also allows a wide variety of distribution channels to be used. The Company’s strategic

orientation is rounded off by a conservative investment and reinsurance policy.

VIG operates with more than one company and brand in most of its markets. The market presence of each company in a

country is also aimed at different target groups. Their product portfolios differ accordingly. Use of this multi-brand strategy

does not mean, however, that potential synergies are not exploited. Structural efficiency and the cost-effective use of re-

sources are examined regularly. Back offices that perform administrative tasks for more than one company are being used

successfully in many countries. Specific country responsibilities also exist at the Managing Board level to ensure uniform

management of each country. Mergers of Group companies are considered if the additional synergies that can be achieved

outweigh the benefits of multiple market presences.

This fundamental approach is also reflected in its continuous sustainable growth and excellent credit rating. The international

rating agency Standard & Poor’s has confirmed VIG’s development with an A+ rating with stable outlook for many years.

VIG continues to have the best rating of all companies in the ATX leading index of the Vienna Stock Exchange.

In total, the Group generated a premium volume (premiums written for direct and indirect business before insurance) of

TEUR 4,878,615 in non-life insurance and TEUR 4,172,353 in health and life insurance in 2016, totalling TEUR 9,050,968.

Of this amount, TEUR 4,502,089 was attributable to non-life insurance and TEUR 4,108,069 to health and life insurance

within the scope of the Solvency II consolidated group, totalling TEUR 8,610,158.

Expenses for claims and insurance benefits, including changes in other underwriting provisions (also before insurance)

amounted to TEUR 3,033,957 in non-life insurance and TEUR 4,051,119 in health and life insurance in 2016, totalling TEUR

7,085,076. Of this amount, TEUR 2,618,700 was attributable to non-life insurance and TEUR 3,958,945 to health and life

insurance within the scope of the Solvency II consolidated group, totalling TEUR 6,577,645.

The Group had a combined ratio (after reinsurance, not including investment income) of 97.3% in 2016. Vienna Insurance

Group was able to continue to keep the combined ratio below the 100% mark as a result of its solid technical result.

Group profit before taxes rose to TEUR 406,734 in 2016. This more than achieved the target of at least doubling the profit

of the previous year, in spite of the negative effects of the low interest rate environment. The financial result includes a one-

time positive effect due to the agreement reached between the Carinthian Compensation Payment Fund and HETA creditors,

which included the VIG Group. Accepting the settlement before the 7 October 2016 deadline meant that the bonds that

had been previously written down could be written up in value by around TEUR 40,000.

Solvency and financial condition report 2016 13

Governance refers to all management processes, in addition to the effective and efficient monitoring of the Company. The

governance system considers not only the internal organisation, structure and mechanisms within the Company, but also

its legal and factual integration into the external (market) environment.

VIG Holding has set up an efficient governance system geared to the Company's needs and requirements, enabling the

sound and cautious management of its insurance operations. In addition to the establishment of governance and other key

functions, all relevant processes are set up to recognise, measure, monitor, manage and report risks, taking their interde-

pendencies into account.

The Company's internal processes ensure that the analyses of the key functions and all results of the risk management

processes are adequately taken into account during the course of business activities.

VIG Holding has a governance system with the following characteristics:

– Functional management of the Company by the Managing Board

– Transparent monitoring by the Supervisory Board

– Orientation of management decisions towards long-term value creation

– Targeted collaboration between company management and monitoring

– Appropriate handling and management of risks through risk management and in the individual organisational units at

the operational level

– Transparency in corporate communications and efficient reporting

– Safeguards for the interests of policyholders, shareholders and employees

The following section describes

– General information about the governance system

– Requirements for professional qualification and personal reliability

– Risk management system, including the Company's risk and solvency assessment

– Internal control system

– Function of the internal audit

– Actuarial function

– Outsourcing

During the reporting period, there were no significant changes to the governance system of VIG Holding.

B System of Governance

14 Vienna Insurance Group Holding

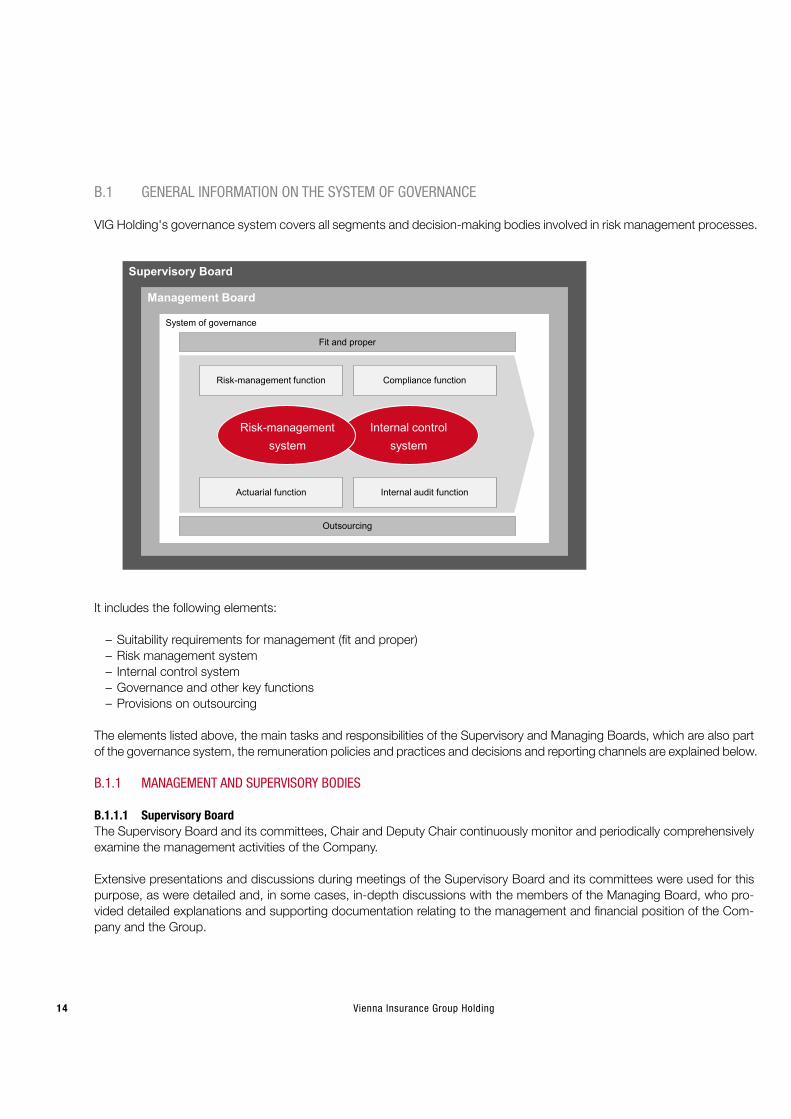

B.1 GENERAL INFORMATION ON THE SYSTEM OF GOVERNANCE

VIG Holding's governance system covers all segments and decision-making bodies involved in risk management processes.

It includes the following elements:

– Suitability requirements for management (fit and proper)

– Risk management system

– Internal control system

– Governance and other key functions

– Provisions on outsourcing

The elements listed above, the main tasks and responsibilities of the Supervisory and Managing Boards, which are also part

of the governance system, the remuneration policies and practices and decisions and reporting channels are explained below.

B.1.1 MANAGEMENT AND SUPERVISORY BODIES

B.1.1.1 Supervisory Board

The Supervisory Board and its committees, Chair and Deputy Chair continuously monitor and periodically comprehensively

examine the management activities of the Company.

Extensive presentations and discussions during meetings of the Supervisory Board and its committees were used for this

purpose, as were detailed and, in some cases, in-depth discussions with the members of the Managing Board, who pro-

vided detailed explanations and supporting documentation relating to the management and financial position of the Com-

pany and the Group.

Supervisory Board

Management Board

System of governance

Risk-management

system

Internal control

system

Risk-management function Compliance function

Internal audit functionActuarial function

Outsourcing

Fit and proper

Solvency and financial condition report 2016 15

Strategy, business development (overall and in individual regions), risk management, the internal control system, internal

audit activities and the IT strategy of the Company were also discussed in the Supervisory Board meetings and discussions

with the Managing Board.

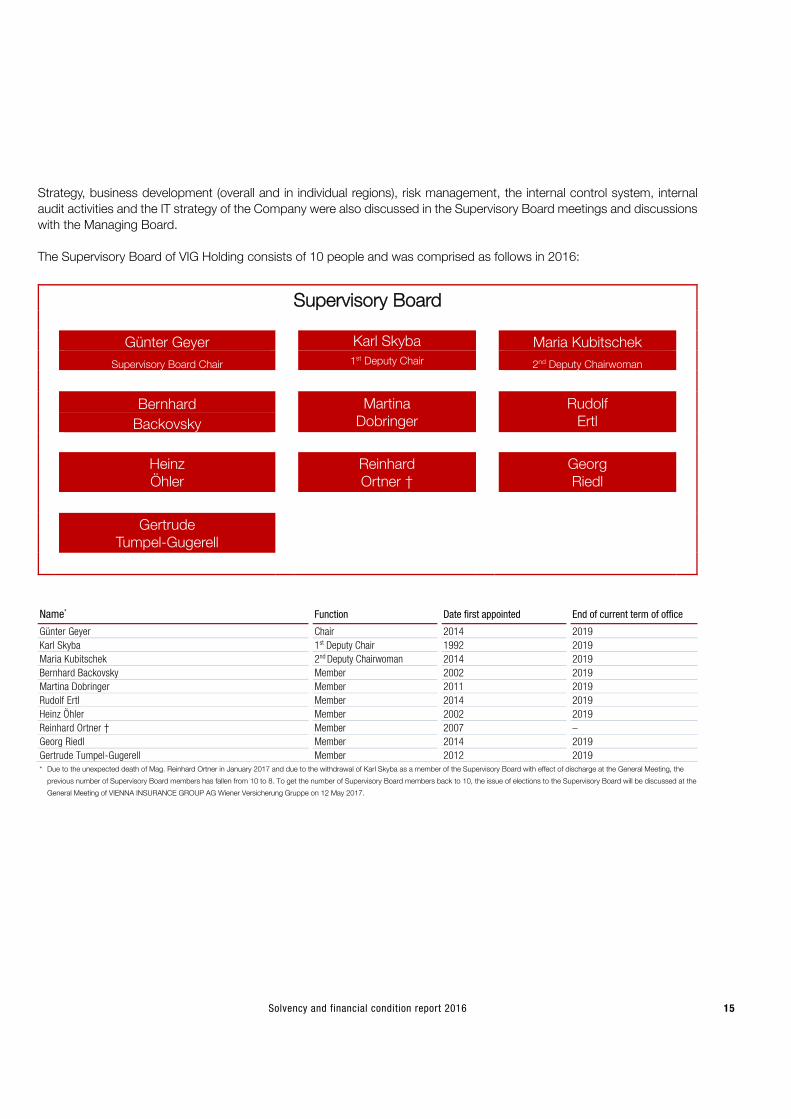

The Supervisory Board of VIG Holding consists of 10 people and was comprised as follows in 2016:

Name* Function Date first appointed End of current term of office

Günter Geyer Chair 2014 2019

Karl Skyba 1st Deputy Chair 1992 2019

Maria Kubitschek 2nd Deputy Chairwoman 2014 2019

Bernhard Backovsky Member 2002 2019

Martina Dobringer Member 2011 2019

Rudolf Ertl Member 2014 2019

Heinz Öhler Member 2002 2019

Reinhard Ortner † Member 2007 –

Georg Riedl Member 2014 2019

Gertrude Tumpel-Gugerell Member 2012 2019 * Due to the unexpected death of Mag. Reinhard Ortner in January 2017 and due to the withdrawal of Karl Skyba as a member of the Supervisory Board with effect of discharge at the General Meeting, the

previous number of Supervisory Board members has fallen from 10 to 8. To get the number of Supervisory Board members back to 10, the issue of elections to the Supervisory Board will be discussed at the

General Meeting of VIENNA INSURANCE GROUP AG Wiener Versicherung Gruppe on 12 May 2017.

Supervisory Board

Günter Geyer Karl Skyba Maria Kubitschek

Supervisory Board Chair 1st Deputy Chair 2nd Deputy Chairwoman

Bernhard Martina Dobringer

Rudolf Ertl

Backovsky

Heinz Öhler

Reinhard Ortner †

Georg Riedl

Gertrude Tumpel-Gugerell

16 Vienna Insurance Group Holding

COMMISSIONS AND COMMITTEES OF THE SUPERVISORY BOARD

The Supervisory Board has formed four committees from among its members in order to meet its obligations under the

statutory provisions and in accordance with the articles of incorporation of VIG Holding:

– Committee for Urgent Matters (Working Committee)

– Audit committee (Accounts Committee),

– Committee for Managing Board Matters (Personnel Committee) and

– Strategy Committee.

Committee for Urgent Matters (Working Committee)

The Committee for Urgent Matters (Working Committee) decides on matters that require an approval of the Supervisory

Board, but cannot be deferred to the next ordinary Supervisory Board meeting because of particular urgency.

Members substitute

Günter Geyer (Chair) 1st substitute: Gertrude Tumpel-Gugerell

2nd substitute: Reinhard Ortner †

Karl Skyba (Deputy Chair) 1st substitute: Georg Riedl

2nd substitute: Reinhard Ortner †

Rudolf Ertl 1st substitute: Martina Dobringer

2nd substitute: Reinhard Ortner †

Audit Committee (Accounts Committee) The Audit Committee (Accounts Committee) is responsible for the duties assigned by Section 92(4a) no. 4 and Section 123(9) of the Austrian Insurance Supervision Act (VAG). All the members of the Audit Committee are experienced financial experts with knowledge and practical experience in finance, accounting and reporting that satisfy the requirements of the Company and of the Group. The Audit Committee (Accounts Committee) is comprised as follows:

Members substitute

Gertrude Tumpel-Gugerell (Chair) 1st substitute: Karl Skyba

2nd substitute: Heinz Öhler

Georg Riedl (Deputy Chair) 1st substitute: Karl Skyba

2nd substitute: Heinz Öhler

Reinhard Ortner † 1st substitute: Maria Kubitschek

2nd substitute: Heinz Öhler

Günter Geyer 1st substitute: Maria Kubitschek

2nd substitute: Heinz Öhler

Rudolf Ertl 1st substitute: Karl Skyba

2nd substitute: Heinz Öhler

Martina Dobringer 1st substitute: Maria Kubitschek

2nd substitute: Heinz Öhler

Solvency and financial condition report 2016 17

Committee for Managing Board Matters (Personnel Committee)

The Committee for Managing Board Matters (Personnel Committee) deals with personnel matters of Managing Board mem-

bers. The Committee for Managing Board Matters therefore decides on terms of employment contracts with members of

the Managing Board and their compensation, and examines remuneration policies at regular intervals.

The Personnel Committee is comprised as follows:

Members

Günter Geyer (Chair)

Karl Skyba (Deputy Chair)

Substitute: Rudolf Ertl

Strategy Committee

The Strategy Committee cooperates with the Managing Board and, when appropriate, with experts that it consults, to

prepare fundamental decisions that must then be decided on by the Supervisory Board as a whole.

The Strategy Committee is comprised as follows:

Members substitute

Günter Geyer (Chair) 1st substitute: Gertrude Tumpel-Gugerell

2nd substitute: Reinhard Ortner †

Karl Skyba (Deputy Chair) 1st substitute: Georg Riedl

2nd substitute: Reinhard Ortner †

Rudolf Ertl 1st substitute: Martina Dobringer

2nd substitute: Reinhard Ortner †

Due to the fundamental importance of strategic issues, these were generally dealt with not in the Committee, but by the

entire Supervisory Board.

B.1.1.2 Managing Board

The Managing Board manages the business of the Company under the leadership of its Chairperson and within the con-

straints of the law, articles of association, rules of procedure for the Managing Board and rules of procedure for the Super-

visory Board. The Managing Board meets when needed (generally each week or every two weeks) to discuss current

business developments, and makes necessary decisions and resolutions during the course of these meetings. The mem-

bers of the Managing Board continuously exchange information with each other and the heads of various departments.

The Managing Board of VIG Holding has been comprised as follows since 1 January 2016:

Substitute members

Divis Lehel

Managing Board

Stadler (CEO) Fuchs Gröll Havasi Höfinger Simhandl (CFO)

18 Vienna Insurance Group Holding

Elisabeth Stadler

General Manager, born in 1961, Actuarial degree

Elisabeth Stadler studied actuarial theory at the Vienna Technical University and began her career in Austrian insurance industry as a Board member and chairwoman. In May 2014, she was awarded the professional title of professor by Federal Minister Gabriele Heinisch-Hosek for her services in the insurance industry. From September 2014 until March 2016, she served as General Manager of Donau Versicherung and has been in charge of VIG since 2016. Areas of responsibility: Management of the VIG Group, strategic issues, European issues, corporate communications and marketing, sponsoring, human resources, Group development and strategy Country responsibilities: Austria, Czech Republic Positions held on the Supervisory Boards of other Austrian and foreign companies outside of the Group: Österreichische Post AG, Bank Austria Real Invest Immobilien Kapitalanlage GmbH (until 6 March 2017), Die Österreichische Hagelversi-cherung, Casinos Austria AG Elisabeth Stadler also has an active role on the Supervisory Boards of material* Vienna Insurance Group companies: Wiener Städtische, Donau Versicherung, s Versicherung, Kooperativa (Czech Republic), ČPP, PČS, InterRisk Franz Fuchs

Board member, born in 1953

Franz Fuchs began his career in the insurance industry as an actuary. He held leading management positions in other international companies as a specialist in the life insurance area and pension funds before joining Vienna Insurance Group. Franz Fuchs was Chair of the Managing Board of Compensa Non-life and Compensa Life from 2003 to the beginning of 2014. He has been Chair of the Managing Board of VIG Polska since 2003. He was first appointed to the Vienna Insurance Group Managing Board on 1 October 2009. Areas of responsibility: Performance management personal and motor insurance, asset risk management Country responsibilities: Baltic states, Moldova, Poland, Ukraine

Positions held on the Supervisory Boards of other Austrian and foreign companies outside of the Group: C-QUADRAT Investment AG Franz Fuchs also has an active role the Supervisory Boards of material* Vienna Insurance Group companies: Kooperativa (Czech Republic), ČPP, PČS, InterRisk, Omniasig.

Solvency and financial condition report 2016 19

Roland Gröll Board member, born in 1965, studied Business Administration Roland Gröll studied at the Vienna University of Economics and Business and joined Wiener Städtische in 1994 in the Finance and Accounting department. He became Deputy Head of the Finance and Accounting department in 2003, and was head of this department from 2008 until the end of 2015. Roland Gröll was also a member of the Managing Board of Donau Versicherung for two years. He has been a member of the Vienna Insurance Group Managing Board since January 2016. Areas of responsibility: Group IT/SAP, international processes and methods Country responsibilities: Bosnia-Herzegovina, Croatia, Macedonia, Romania Roland Gröll also has an active role the Supervisory Board of a material* Vienna Insurance Group company: Omniasig.

Judit Havasi

Member of the Managing Board, born in 1975, Law graduate

Judit Havasi has worked for the Group since 2000. She began as an internal audit employee in UNION Biztosító, and became the head of this company in 2003. Before her appointment to the Managing Board of Wiener Städtische in 2009, Judit Havasi was a substitute member of the Managing Board of Wiener Städtische and a member of the Managing Board of UNION Biztosító in Hungary. Judit Havasi was Deputy General Manager of Wiener Städtische from July 2013 to the end of 2015. She was also a substitute member of the Vienna Insurance Group Managing Board starting in 2011. She has been a member of the Vienna Insurance Group Managing Board since January 2016. Areas of responsibility: Solvency II, planning and controlling, law Country responsibilities: Slovakia Positions held on the Supervisory Boards of other Austrian and foreign companies outside of the Group: Erste&Stei-ermärkische Bank d.d., Die Zweite Wiener Vereins-Sparcasse Judit Havasi also has an active role the Supervisory Boards of material* Vienna Insurance Group companies: Wiener Städ-tische, Donau Versicherung, Kooperativa (Slovakia). Peter Höfinger Member of the Managing Board, born in 1971, Law graduate Peter Höfinger has been a member of the Vienna Insurance Group Managing Board since 1 January 2009. Prior to that, he was director of the Managing Board of Donau. He joined this Company in 2003. Previously, he held management positions outside the Group in Hungary, the Czech Republic and Poland. Areas of responsibility: International corporate and large customer business, Vienna International Underwriters (VIU), rein-surance, Group development and strategy Country responsibilities: Albania (incl. Kosovo), Bulgaria, Montenegro, Serbia, Hungary, Belarus

20 Vienna Insurance Group Holding

Martin Simhandl

Member of the Managing Board, born in 1961, Law graduate

Martin Simhandl began his career with the Group in 1985 in the legal department of Wiener Städtische. In 1995, he became head of the subsidiaries department, and in 2003, he took over coordination of the Group’s investment activities. In 2002 and 2003, Martin Simhandl was also a member of the Managing Boards of InterRisk Non-life and InterRisk Life in Germany, with responsibility for the areas of property insurance, reinsurance and planning/controlling. On 1 November 2004, Martin Simhandl was appointed to the Managing Board of the Company. Areas of responsibility: asset management, subsidiaries department, finance and accounting, treasury/capital markets Country responsibilities: Germany, Georgia, Liechtenstein, Turkey Positions held on the Supervisory Boards of other Austrian and foreign companies outside of the Group: CEESEG Aktieng-esellschaft, Erste Asset Management, Wiener Hafen Management GmbH, Wiener Börse AG. The following two substitute members were also appointed to the Managing Board, and will become members of the

Managing Board if a member of the Managing Board becomes permanently incapable of performing his or her duties:

– Martin Diviš,

– Gábor Lehel

* All companies that contribute at least 2% of written premiums and at least 2% of profit before taxes are considered to be “material”.

The entire Managing Board is responsible for enterprise risk management, general secretariat, (Group) actuarial department,

Group compliance, internal audit and investor relations.

VIG Holding clearly defines its tasks and responsibilities. A well-defined work flow organisation ensures that all employees

of VIG Holding are aware of the responsibilities and reporting paths (primarily always at the higher level). The schedule of

responsibilities and the organisational chart are available to all employees on the intranet.

Commissions and Committees

The Managing Board has formed commissions and committees for the effective management of the Group, which support

it to ensure that it can meet its obligations under the statutory provisions and VIG Holding's articles of incorporation to the

greatest extent possible:

– Risk Committee,

– Reinsurance Security Committee,

– Tactical Investment Committee

– Strategic Investment Committee (Asset Management)

– Asset-Liability Management (ALM) Committee

– Compliance Committee

These are briefly presented in the following sub-sections.

Solvency and financial condition report 2016 21

RISK COMMITTEE

The Risk Committee was established by the Managing Board of VIG Holding to discuss the current risk management

agendas on a regular basis within the organisation and ensure communication about the risk situation between the mem-

bers of the Committee and the Managing Board.

The members of the Committee are appointed by the Managing Board. The Committee is currently composed as follows:

– Holder of the Risk Management Function

– Holder of the Compliance Function

– Holder of the Actuarial Function

– Head of Asset Risk Management

– Head of Reinsurance

– Group IT Security Officer

– optional: Head of Human Resources

Depending on the current risk situation, additional experts may be invited to the meetings as required and may be requested

by the Managing Board or individual members of the Committee. The Risk Committee meetings are held at least once every

quarter and are organised and recorded by the Enterprise Risk Management (ERM) department. The results of the meetings

are presented by the members of the Committee at the next following Managing Board/board meeting.

REINSURANCE SECURITY COMMITTEE

The Reinsurance Security Committee deals with the creditworthiness of reinsurance companies and helps to ensure that a

sufficient degree of diversification is available among the selected re-insurers and that the default risk within the reinsurance

business remains within acceptable limits for the VIG Group.

The Reinsurance Security Committee creates and adapts a quarterly list ("Security List") of re-insurers acceptable to VIG.

The VIG Managing Board sends this list to the members of the Managing Board of the various Group companies responsible

for reinsurance. The security list determines the maximum number of reinsurance assignments which can be issued to re-

insurers (please note: Assignments to re-insurers on the security list are subject to the limits set out in the "Cessions Limi-

tation Table" included in the list).

In the following two cases, the administrator must obtain approval from the Reinsurance Security Committee prior to the

start of the policy period:

– If business (whether facultative or mandatory) is to be given to re-insurers who are not on the VIG security list, an

individual review of the re-insurer and, where appropriate, clearance from the Reinsurance Security Committee is re-

quired.

– If the volume of the planned reinsurance cession to a re-insurer on the security list exceeds the limits stated in the

"Cessions Limitations Table", an individual decision on clearance must be made by the Reinsurance Security Committee.

The Reinsurance Security Committee consists of selected, professionally qualified reinsurance employees and specialist

departments at a number of VIG companies.

22 Vienna Insurance Group Holding

TACTICAL INVESTMENT COMMITTEE

The Tactical Investment Committee (TAA) deals with the risk and earnings situation of the investments. The TAA deals with

issues relating to short-term liquidity requirements and provides advice and makes decisions in this context. The TAA is

firmly anchored in the Company's decision-making and information process.

The members of the TAA are:

– the CFOs,

– the Asset Manager,

– the Asset Risk Manager and

– the Head of Accounting

of the Austrian VIG companies and VIG Holding.

The committee, which usually meets on a weekly basis, can react promptly to the respective risk situation.

STRATEGIC INVESTMENT COMMITTEE (ASSET MANAGEMENT)

The Strategic Investment Committee (Asset Management) deals with the investment portfolios of the Group's five largest

countries (Austria, Czech Republic, Slovakia, Poland and Romania) on a quarterly basis. This meeting is intended to allow

a regular exchange of information on all asset management issues between the key companies. For this purpose, the

portfolio structures are analysed on the basis of different aspects and the major changes or planned measures are dis-

cussed. A report comparing the current status of the financial results to the plan or forecast is also prepared. When estab-

lishing the financial planning figures, the underlying assumptions and results are discussed and the relevant information is

exchanged.

The permanent members are:

– the Group CFO

– the Group-wide Board for Asset Risk Management

– at least one representative Managing Board per country (AT, CZ, SK, PL, RO)

– the Group CIO

– the Head of Asset Risk Management

– local Asset Managers (if required)

If necessary or if requested by individual members, additional experts may be invited to the meetings to discuss current

topics or for other reasons.

ASSET-LIABILITY MANAGEMENT (ALM) COMMITTEE

The Asset Liability Management (ALM) Committee, which meets at least once every quarter, deals with current agendas of

asset liability management with the aim of exchanging information about the risk situation of the Group's five largest coun-

tries (Austria, Czech Republic, Slovakia, Poland and Romania). Topics dealt with by the ALM Committee include the cash

flow situation and the maturity structure of investments versus liabilities of the balance sheet, with a focus on the life and

health business.

The participants of the Strategic Investment Committee are joined by representatives of the Life Insurance. Depending on

current topics, additional experts may be invited to the meetings as required and may be requested by the Managing Board

or individual members of the Committee.

Solvency and financial condition report 2016 23

COMPLIANCE COMMITTEE

As an institutionalised working platform for compliance-relevant topics, the compliance committee of VIG Holding is

set up to provide regular information on current topics relevant to compliance and discuss them in a cross-disciplinary

manner. The members of the committee include individuals with governance functions in VIG Holding, the heads of

selected business units (legal, human resources, asset management, asset risk management, accounting, reinsurance,

corporate and large customer business), the AML officer, the data protection officer and the IT security officer.

During Compliance Committee meetings, the committee members report on compliance issues from their individual busi-

ness units and inform each other about current compliance issues. The meeting minutes are sent to the Managing Board.

B.1.2 GOVERNANCE AND OTHER KEY FUNCTIONS

The entire Managing Board is responsible for monitoring the risk situation within the Company. In doing so, it is supported

by the key functions.

The key functions are the four governance functions provided for in the VAG and the other key functions defined by the

Company. In VIG Holding, key functions guide areas that have a significant influence (directly or indirectly) on the stra-

tegic management and the risk profile of the Company. All key functions directly and regularly report to the Managing

Board. The internal auditing function also regularly reports to the Chair of the Supervisory Board and Audit Committee.

GOVERNANCE FUNCTIONS

The following individuals were entrusted to exercise governance functions within VIG Holding in 2016 by resolution of the

Managing Board:

Governance function Name Division

Compliance function Natalia Cadek Compliance

Internal auditing function Herbert Allram Internal Audit

Risk management function Ronald Laszlo Enterprise Risk Management

Actuarial function Werner Matula Group Actuary

COMPLIANCE FUNCTION

During the fulfilment of its tasks, the compliance function is organisationally assigned to the entire Managing Board and

reports directly to it. Organisationally, the compliance function is separate from the other governance or key functions of

VIG Holding, is independent when exercising its activities and is not entrusted with any operational duties of VIG Holding in

the sense of the core business.

The compliance function exercises its tasks for VIG at an individual Company and Group level. The duties of the compliance

function are stipulated in an internal policy and include, among others, the tasks assigned to the compliance function

according to VAG, in particular:

– Advice and assistance of the Managing Board on compliance with the rules applicable to the Company's operations

as a (re)insurance company – Assessment of the potential impact of changes in the legal environment

– Identification and assessment of compliance risks

– Development of compliance standards and promotion of awareness regarding compliance at VIG, in particular through

training

– Performance of compliance audits and investigation and management of compliance incidents

24 Vienna Insurance Group Holding

An appropriate substitute regulation has been established for the compliance function. When performing its tasks the Group

compliance function is assisted by employees from the Group Compliance department.

INTERNAL AUDIT FUNCTION

During the fulfilment of their tasks, the Internal Audit function is organisationally assigned to the entire Managing Board and

reports directly to it. Organisationally, the Internal Audit function is separate from the other governance or key functions of

VIG Holding, is independent when exercising its activities and is not entrusted with any operational duties of VIG Holding in

the sense of the core business.

The functionary exercises their role for VIG at an individual Company and Group level.

The tasks of the governance function are specified in the function description. These include the auditing requirements according

to the VAG, namely the examination of the legal, regulatory and advisory nature of the (re)insurance company's business, as well

as the adequacy and effectiveness of the internal control system and other elements of the governance system.

This in particular includes:

– Audit planning on the basis of risk-oriented aspects and ensuring comprehensive auditing activities;

– Audit work, including auditing management, particularly with regard to the focus of the test content, scope of the audit

and subsequent coordination of the audit reports;

– Reporting on the areas of the audit and significant audit findings to the members of the Audit Committee and Supervi-

sory Board;

– Ensuring that the implementation of proposed mitigation measures is monitored.

An appropriate substitute regulation has been established for the internal auditing function. The functionary is also assisted

by employees from the Group Internal Auditing department when performing their tasks.

RISK MANAGEMENT FUNCTION

During the fulfilment of their tasks, the risk management function is organisationally assigned to the entire Managing Board

and reports directly to it. Structurally and organisationally, the risk management function acts independently when perform-

ing its activities and has no risk-taking tasks within VIG Holding.

The functions of the governance function are stipulated in the function description and include, among other things, the

requirements placed on the risk management function according to VAG, in particular:

– Regular identification and analysis of risks (risk inventory)

– Determination of the risk profile, implementation of the Own Risk and Solvency Assessment (ORSA)

– Quarterly and annual determination of solvency capital requirements

– Development and maintenance of the partial internal model

– Monitoring the risk bearing ability

– Annual review of the effectiveness of the internal control system (ICS)

– Quarterly and annual reports (QRTs, narrative reporting)

– Preparation and updating of relevant rules and guidelines

– Further development and maintenance of the central computing and reporting platform

An appropriate substitute regulation has been established for the risk management function. The resources necessary for

the above-mentioned tasks are grouped departmentally.

Solvency and financial condition report 2016 25

ACTUARIAL FUNCTION

When fulfilling its tasks, the actuarial function is organisationally assigned to the entire Managing Board and reports directly to it.

The functionary exercises their role for VIG at an individual Company and Group level.

The tasks of the governance function are stipulated in the function description and include, among other things, the re-

quirements placed on the actuarial function according to VAG, in particular:

– Coordination of the calculation of technical provisions;

– Coordination of the consolidation and plausibility checks of the individual companies' technical provisions in accordance

with Solvency II;

– Ensuring the appropriateness of the methods and basic models used and the assumptions made in the calculation of

the technical provisions;

– Assessment of the sufficiency and quality of the data used in the calculation of the technical provisions;

– Comparison of best estimates with experience values (back testing);

– Reporting to the Managing Board on the reliability and appropriateness of the calculation of technical provisions;

– Monitoring the calculation of technical provision;

– Providing an opinion regarding underwriting and the adequacy of reinsurance;

– Contributing to the effective implementation of the risk management system, in particular with a view to creating risk

models based on the calculation of the solvency and minimum capital requirements and the Company's risk and sol-

vency assessment.

An appropriate substitute regulation has been established for the actuarial function of VIG Holding. The functionary is also

assisted by employees from the Group Actuarial department when performing his tasks.

OTHER KEY FUNCTIONS

In addition to the Managing Board and the governance functions, "other key functions" in VIG Holding were defined as

follows in 2016:

An "other key function" has a significant direct or indirect influence on the risk profile of VIG Holding.

A significant direct influence on the risk profile exists if the area directly and operationally assumes risk positions through its

activities and therefore has an influence on central balance sheet items in such a way that the resulting change may jeop-

ardise the solvency of the Company.

A significant indirect influence on the risk profile exists if the area provides data or information that directly serves as the

basis for important strategic decisions that could potentially influence the risk profile in such a way that the solvency of the

Company may be jeopardised.

The following other key functions were identified in VIG Holding in 2016 based on Managing Board resolution: Division Name

Accounting Hartwig Fuhs

VIG Affiliated Companies Department Sonja Raus

26 Vienna Insurance Group Holding

B.1.2.1 Information and reporting channels

Interactive communication is of major importance in VIG Holding. This ensures that all affected individuals have the infor-

mation at their disposal necessary to adequately fulfil the tasks and responsibilities assigned to them. This applies to all

management levels right down to each individual employee. The information and reporting paths are based on a direct line.

In particular, all key functions have set up a direct reporting path to the Managing Board. Important decisions are prepared

in relevant committees or by the departments before being discussed in the regular board meetings and recorded accord-

ingly.

B.1.3. SIGNIFICANT CHANGES TO THE GOVERNANCE SYSTEM

During the reporting period there were no significant changes to the governance system.

B.1.4 REMUNERATION POLICY AND REMUNERATION PRACTICES

B.1.4.1 Remuneration standards for employees

The attractiveness of the VIG Group as an employer is boosted by the fact that the remuneration systems are appropriate

and transparent. The following principles apply to VIG Holding and the VIG Group.

The remuneration policy reflects the risk awareness of VIG Holding. In particular:

– payment structures and elements which could promote risk behaviour which could endanger the Company and/or its

stakeholders (policyholders, employees, owners) are avoided;

– the remuneration of key function holders is arranged with the aim of ensuring that these positions are continuously filled,

in particular the control positions, with appropriately qualified staff;

The remuneration policy supports the focus on sustainable management at all levels of the companies in the VIG Group

and contributes to the Company's current strategy. It aims to promote coherent action and avoid conflicts of interest. It also

supports the compliance requirements with regard to all provisions applicable to the companies of the Group.

VIG Holding observes all relevant statutory requirements when determining and applying the remuneration policy.

The remuneration takes working hours and the required qualifications, responsibilities and duties of the respective position

into account. Care must be taken to ensure that the salary is not below the minimum wage applicable under national law

or existing collective bargaining agreements.

If a variable remuneration component is agreed, the objectives that determine the variable remuneration component must

be transparent and should be updated once a year.

B.1.4.2 Remuneration for key functions and risk takers

The variable portion of the remuneration for key function holders, including members of the Managing Board and risk takers,

is limited and emphasises the need for sustainability. Its full achievement depends on the consideration of the sustainable

development of the Company beyond a single financial year.

Solvency is a central risk indicator which is constantly monitored as part of the risk-bearing capacity. The solvency ratio

must be taken into account when granting variable remuneration components. The allocation of variable remuneration

depends, among other criteria, on the solvency ratio and its management.

Solvency and financial condition report 2016 27

SUPPLEMENTARY PENSIONS AND EARLY RETIREMENT SCHEMES

Depending on the date when an employee joined the Company, individual companies of VIG provide Company pension

payments for key function holders which are based on individual contractual commitments.

B.1.4.3 Compensation plan for members of the Managing Board

Compensation for the Managing Board of VIG Holding takes into account the importance of the Group and the responsibility

that goes with it, the economic situation of the Company, and the market environment.

The variable portion of the compensation emphasises the need for sustainability and achieving it fully depends substantially

on considering the sustainable performance of the Company that extends beyond a single financial year.

The performance-related compensation is limited. The maximum performance-related compensation that members of the Man-

aging Board can receive by overachieving the traditional targets in financial year 2016 is between 60% and 65% of its fixed

salary.

Significant parts of the performance-related compensation are only paid after a delay. The delay for financial year 2016 extends

into the year 2020. The deferred portions are awarded based on sustainable performance of the Group, non-financial factors

are included in the evaluation of target achievement. For example, the performance-related compensation for 2016 is awarded

based on promotion of those aspects of corporate governance that express social responsibility in practice.

In addition extra bonus compensation can be earned for achievement of special targets.

In total, the members of the Managing Board can earn variable compensation equal to a maximum of 81% to 93% of their

fixed compensation in this way.

The Managing Board is not entitled to the performance-related component of compensation if performance fails to meet

certain thresholds.

Even if the targets are fully met in a financial year, because of the focus on sustainability, the full variable compensation is

only awarded if the Company also achieves positive performance in the three following years.

In 2016, the key performance criteria for variable compensation are the combined ratio, premium growth and profit before

taxes, and the key performance criteria for extra bonus compensation are country-specific targets.

Managing Board compensation does not include stock options or similar instruments.

No loans or guarantees were granted to the members of the Managing Board during the reporting period. As of 31 Decem-

ber 2016, there were also no loans or liabilities.

PENSION FUNDS

The standard contract for a member of the Managing Board of the Company includes a pension fund equal to a maximum of

40% of the measurement base if the member remains on the Managing Board until the age of 65 (the measurement base is

equal to the standard fixed salary). A pension is normally received only if a Managing Board member’s position is not extended

and the member is not at fault for the lack of extension, or the Managing Board member retires due to illness or age.

28 Vienna Insurance Group Holding

SEVERANCE PAY

In cases where the provisions of the Austrian Employee and Self-Employment Provisions Act (Mitarbeiter- und Selbstständi-

gen-Vorsorgegesetz) are not applicable by law, the Company’s Managing Board contracts provide for a severance payment

entitlement structured in accordance with the provisions of the Austrian Employee Act (Angestelltengesetz), as before

amended in 2003, in combination with applicable sector-specific provisions. This allows Managing Board members to receive

a severance payment equal to two to twelve months’ compensation, depending on the period of service, with a supplement

of 50% if the member retires or leaves after a long-term illness. A Managing Board member who leaves of his or her own

volition before retirement is possible, or has to leave due to a fault of his or her own, is not entitled to a severance payment.

Members of the Managing Board are provided a company car for both business and personal use.

B.1.4.4 Compensation plan for the members of the Supervisory Board

In accordance with the resolutions adopted by the 21st regular general meeting on 4 May 2012, the members of the

Supervisory Board elected by the general meeting are entitled to receive compensation in the form of a payment remitted

monthly in advance. Members of the Supervisory Board who withdraw from their positions before the end of a month still

receive full compensation for the month in question. In addition to this compensation, Supervisory Board members are

entitled to receive an attendance allowance for participating in Supervisory Board meetings and Supervisory Board com-

mittee meetings (remitted after participation in the meeting).

There are no variable salary components or pension commitments for members of the Supervisory Board.

Supervisory Board compensation does not include stock options or similar instruments.

No loans or guarantees were granted to the members of the Supervisory Board during the reporting period. As of 31

December 2016, there were also no loans or liabilities.

B.1.5 ADEQUACY OF THE GOVERNANCE SYSTEM

The governance system of VIG Holding is well-defined and appropriate with regard to the nature, size and complexity of the

Company.

The roles and responsibilities of the Managing Board at VIG Holding are recorded in the business plan. Direct reporting lines

from the divisional managers to the respective responsible members of the Managing Board ensure that relevant information

is adequately incorporated into the Company's management.

Clearly defined lines of communication between individual companies and the Group and the inclusion of at least one member

of VIG Holding's Managing Board in the subsidiaries' Supervisory Boards continue to contribute to the appropriate manage-

ment of the Group.

As part of the governance system, all legally required governance functions are established at VIG Holding and conflicts of

interest are excluded. A direct subordination of the governance functions to the entire Managing Board guarantees the

appropriate position of the governance functions within the Company.

The internal control system of VIG Holding is based on ICS guidelines which are valid throughout the Group and ensures

that there is always an appropriate control environment for development and process organisation.

Solvency and financial condition report 2016 29

B.2 FIT AND PROPER REQUIREMENTS

When employees are appointed to key functions, particular attention is paid to the fulfilment of the professional and personal

requirements by the candidate.

The professional qualification requirements are defined in the respective function description for each function. In all cases,

the following criteria are considered during recruitment:

1. Education (including studies)

2. Professional experience

3. Other knowledge (e.g. relevant legal knowledge or relevant technical knowledge etc.)

Documentation relevant to the information in the CV is to be provided (certificates, diplomas etc.).

Various measures are used to assess the personal reliability of a person who will perform a key function in the Company:

– At least one objective element (test procedure, standardised conversation, more than one interview partner) is used

during the recruitment process.

– While completing a questionnaire, the candidate must provide information about their financial situation, any involve-

ment in relevant (criminal) proceedings etc. and must also agree to notify the Company of any future changes which

occur during the employment relationship.

A Fit & Proper Framework Directive at the Group level, which provides a uniform framework, has been adopted by the

Managing Board.

It is the responsibility of key functionaries to keep up to date with all essential aspects of their function and, where appro-

priate, to provide relevant information within the Company. This includes both technical, legal and regulatory aspects as

well as, if necessary, internal Company guidelines.

The necessary technical resources, funds and budgets are made available to the key functionaries by the Company.

The individual companies also determine the requirements for the professional qualification of key personnel with regard to

the individuals who effectively manage the Company as well as with regard to the governance functions in the respective

local legislative processes.

Local legal requirements also exist in many areas in terms of personal reliability.

SUPERVISORY BOARD

Since 1 January 2016, the new Austrian Insurance Supervision Act (Versicherungsaufsichtsgesetz) has been applicable.

The new version of the VAG was required as a new supervisory regime due to the European-wide entry into force of Solvency

II. Solvency II uses a three-pillar approach to calculate the risk-based capital requirements (Pillar 1), requirements for the

governance and risk management system (Pillar 2) and disclosure requirements (Pillar 3). For the Supervisory Boards of

insurance companies, this means that they must familiarise themselves with the Solvency II rules within the scope of their

specific duties. The Gesellschaft für Versicherungsfachwissen (Society for Underwriting Expertise) in Vienna offers a

series of seminars with 5 modules ("Practical Governance. Solvency II - Knowledge for Supervisory Boards of Insurance

Companies"), which was specially designed for Supervisory Boards. The aim of this series of seminars is to ensure that the

members of the Supervisory Board acquire sufficient knowledge or deepen their knowledge of the provisions of the

30 Vienna Insurance Group Holding

VAG (Section 123 (1) in conjunction with Section 120 (1)) in order to perform their tasks as well as possible. These events

are tailor-made for Supervisory Board activities and provide a good overview of (legally) relevant knowledge about current

topics in the insurance industry, in particular all essential aspects of Solvency II.

In addition, the members of the Supervisory Board were provided with the "Handbook Insurance Supervision VAG 2016"

from a series by the Austrian Financial Market Authority (FMA). In this hands-on guide, experts from the FMA provide a

good overview of the new supervisory approach. It addresses issues and challenges which are of particular interest in daily

supervisory practice and discusses them from the perspective of what the authority expects from supervisors in terms of

their practical work.

B.3 RISK MANAGEMENT SYSTEM, INCLUDING THE OWN RISK AND SOLVENCY ASSESSMENT

The professional handling of risks is one of the core competencies of the Vienna Insurance Group. VIG Holding uses a

comprehensive risk management system to fully identify, assess, manage and monitor risks to which the company is ex-

posed. One of the central elements of the risk management system is the company's Own Risk and Solvency Assessment.

B.3.1 RISK MANAGEMENT SYSTEM

B.3.1.1 Strategy and objectives

The risk strategy of VIG Holding is based on the following group-wide principles:

UNACCEPTABLE RISKS

– Risks from the insurance business are not accepted if they cannot be adequately assessed. In particular, this includes

risks from third party liability insurance for genetic engineering and nuclear energy.

– As for investments, risks are not accepted if adequate expertise is not available to assess the risks, e.g. weather deriv-

atives and agricultural commodity futures, essentially risks where the potential loss is unlimited.

RISKS ACCEPTED WITH CONSTRAINS

– Operational risks are to be avoided as much as possible, but must be accepted to some extent as they cannot be

completely ruled out or when the costs involved in avoiding the risk exceed the expected loss.

– Investments should be performed in compliance with the principal of commercial prudence.

RISK-MITIGATING MEASURES

– Maintenance and promotion of strong risk awareness in terms of functioning risk governance.

– Reinsurance is a key instrument to hedge against large losses (tail risk), particularly in the area of property and casualty

insurance.

– Limitation of the market risk under the consideration of underwriting obligations.

Solvency and financial condition report 2016 31

B.3.1.2 ORGANISATION OF THE RISK MANAGEMENT SYSTEM

The organisation of risk management is well-integrated into VIG's organisational structure. All departments responsible for

tasks within the risk management system are directly subordinated to the Managing Board (direct responsibility if applicable).

Before the responsibilities and the roles of each department are further discussed, the following chart briefly outlines the

organizational structure of the VIG risk management.

32 Vienna Insurance Group Holding

MANAGING BOARD

The overall responsibility for risk management is borne by the Managing Board. This holistic approach also applies to central

departments in the reporting line, which are in charge of governance functions (risk management, actuarial, internal audit

and compliance) according to Solvency II regulations. The contact person for risk management matters is Judit Havasi.

Furthermore, following risk management tasks are in the responsibility of the Managing Board:

– Development and promotion of risk management

– Definition and communication of the risk strategy including risk tolerance and risk appetite

– Approval of central risk management guidelines

– Consideration of the risk situation in strategic decisions

RISK COMMITTEE

The objective of the Risk Committee is to exchange information and assess risk-related subjects. The Managing Board is

informed about relevant topics discussed in the Risk Committee meetings. Further information about the Risk Committee

can be found in Section B.1.1.2. Risk-related subjects from the Security and Compliance Committee are handled by the

Risk Committee.

ENTERPRISE RISK MANAGEMENT

The Enterprise Risk Management department is subordinated to the Managing Board. The head of the department is

responsible for the risk management function (see Section B.1.2.1). The department head reports to the Managing Board

via the contact person being Judit Havasi.

ASSET RISK MANAGEMENT

The Asset Risk Management department is assigned to the executive board of Franz Fuchs. The primary role of the de-

partment is to analyse, assess and monitor the risks associated with investments, in particular with regard to the solvency

and financial results of the Group. For these purposes, group-wide standards and methods for risk assessment are specified

and a centralised asset inventory system is implemented by the department, while risk budgets are also defined and mon-

itored for the investments of the individual companies. The department is also responsible for the development and mainte-

nance of an internal rating approach for banks.

ASSET MANAGEMENT

The Asset Management department reports directly to the Chief Financial Officer, Martin Simhandl, and steers the invest-

ments. At the level of VIG Holding, the Asset Management department primarily manages the investment portfolio. Following

the group guidelines, the department sets standards and limits and subsequently monitors the strategic asset allocation in

each individual company. The department promotes collaboration across the Group and focuses on providing specialised

investments expertise in order to achieve optimisation of investment processes within the Group.

INTERNATIONAL ACTUARIAL SERVICES

The actuarial department reports directly to entire Managing Board via the contact person Franz Fuchs. In line with Solvency

II regulations, the head of the department is responsible for the actuarial function. The department is therefore especially

responsible for the tasks associated with the actuarial function. Furthermore, the group actuarial department also calculates

the Group Embedded Value and prepares economic analyses and company evaluations. The department supports actuarial

collaboration and professional networking.

Solvency and financial condition report 2016 33

REINSURANCE

The reinsurance department reports directly to the responsible member of the Managing Board Peter Höfinger. Under the

consideration of specified guidelines, the department coordinates and supports all individual companies of the Group and

their reinsurance departments dealing with reinsurance operations in the area of non-life business (property, casualty, and

third party liability insurance). Moreover, the department manages all group-wide reinsurance programmes in the non-life

lines of business. The primary objective is to create a safety net to provide sustainable protection for all companies in the

Group against the adverse effects of catastrophes, events leading to large losses or adverse changes to the insurance

portfolio. The VIG Holding, as a stand-alone company, falls under the group-wide reinsurance protection.

CONTROLLING

Controlling is an important part of the holistic approach to risk management and is assigned to Managing Board member

Judit Havasi. The area coordinates business planning over a three-year horizon. A standardised reporting system comprises

performance indicators and variance analyses for planning, forecasting and assessing the current performance of the VIG

Holding and other companies’ within the Group. Among the regular reports, monthly premium reports, quarterly reports for

each company (aggregated on country and group level) as well as cost reports are prepared.

GROUP IT

The Group IT department reports directly to the responsible member of the Managing Board, Roland Gröll. The department

is responsible for IT-related risk management agendas. Clear guidelines for the IT security and IT governance are defined by

the department for each company of the Group. The compliance with these guidelines is monitored by an IT-Security-Officer.

Identification Risk inventory

Monitoring ICS evaluation Limit monitoring

Control Planning Risk strategy Risk budgeting Asset allocation Reinsurance programme

Evaluation SCR calculation VaR models S&P calculation CAT evaluation Embedded Value

ORSA

34 Vienna Insurance Group Holding