solvency ii news, from the solvency ii · pdf filesolvency ii association ... mix of bank- and...

TRANSCRIPT

P a g e | 1

___________________ Solvency ii Association

Solvency ii Association 1200 G Street NW Suite 800 Washington, DC 20005-6705 USA

Tel: 202-449-9750 www.solvency-ii-association.com

Solvency 2 News, December 2016

Dear member, The European Insurance and Occupational Pensions Authority (EIOPA) published its December 2016 Financial Stability Report in the (re)insurance and occupational pensions sectors of the European Economic Area. The report presents the evidence that the European macroeconomic environment remains fragile, while insurers and pension funds are challenged by prolonged low interest rates and by a number of geopolitical risks.

European macroeconomic environment remains fragile, further challenged by geopolitical risks

The low interest rate environment continues to be the main challenge for European insurers and Institutions for Occupational Retirement Provision (IORPs)

Advances in technology bring new risks and opportunities challenging existing business models substantially With Solvency II starting in January 2016 insurance undertakings are subject to a risk-based supervisory regime. The low interest rate environment affects both balance sheet figures and business models.

P a g e | 2

___________________ Solvency ii Association

On the latter, there is a trend for the evolution of business models towards unit-linked investments. On the portfolio side, maturing assets have to be reinvested in the current yield environment in order to match the cash flow profiles of outstanding liabilities. In the current environment, insurers are exposed to reinvestment risk. Furthermore, the insurance sector is exposed to risks originating in the European banking sector. As digitalisation becomes more prominent, cyber risks increasingly emerge and challenge companies, but also offer opportunities for insurers to develop new products. In the reinsurance sector, the demand is still subdued, whereas the reinsurance capacity continues to increase. The combination of the continuing capital-inflow into the reinsurance market, benign catastrophe activity and increasingly low investment returns due to the ongoing challenging economic environment increases the profitability pressure in the reinsurance business. The European occupational pensions sector continues to face the challenging macroeconomic environment with low interest rates exerting pressure on IORP liabilities. Total assets significantly increased in 2015. Investment allocation remained broadly unchanged and the average rate of return decreased but remained positive across the sample. The average cover ratios for defined benefit schemes decreased over 2015 compared to 2014 and remain a concern for a number of countries in the European Union. Gabriel Bernardino, Chairman of EIOPA, said: “This year is an important milestone for the European insurance sector. The new regulatory regime increases risk-based awareness. Today, EIOPA is presenting its first Financial Stability Report employing Solvency II data gradually enhancing our analysis of financial stability risks in the European insurance and pensions sector“. This Financial Stability Report includes the following two thematic articles:

P a g e | 3

___________________ Solvency ii Association

The impact of the monetary policy interventions on the insurance industry

A possible approach how the long-term rate should be updated based on regulatory preferences EIOPA’s Financial Stability Report December 2016 is available via EIOPA’s Website: https://goo.gl/EUKmzD

P a g e | 4

___________________ Solvency ii Association

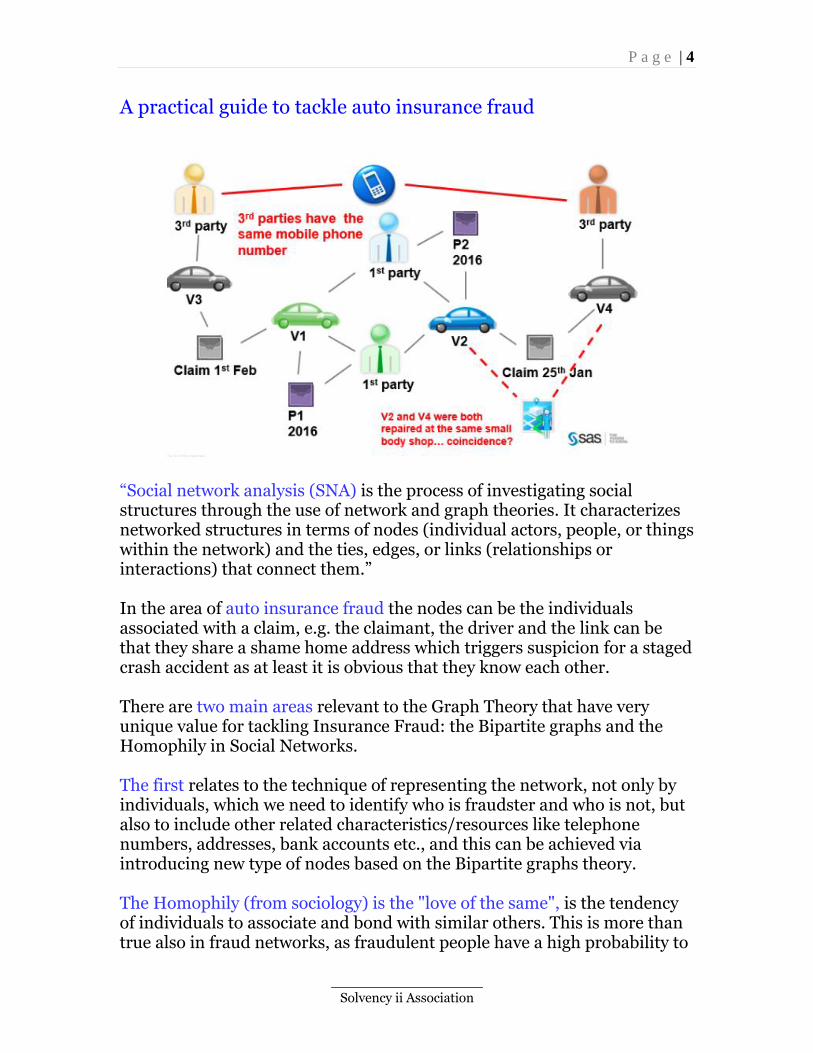

A practical guide to tackle auto insurance fraud

“Social network analysis (SNA) is the process of investigating social structures through the use of network and graph theories. It characterizes networked structures in terms of nodes (individual actors, people, or things within the network) and the ties, edges, or links (relationships or interactions) that connect them.” In the area of auto insurance fraud the nodes can be the individuals associated with a claim, e.g. the claimant, the driver and the link can be that they share a shame home address which triggers suspicion for a staged crash accident as at least it is obvious that they know each other. There are two main areas relevant to the Graph Theory that have very unique value for tackling Insurance Fraud: the Bipartite graphs and the Homophily in Social Networks. The first relates to the technique of representing the network, not only by individuals, which we need to identify who is fraudster and who is not, but also to include other related characteristics/resources like telephone numbers, addresses, bank accounts etc., and this can be achieved via introducing new type of nodes based on the Bipartite graphs theory. The Homophily (from sociology) is the "love of the same", is the tendency of individuals to associate and bond with similar others. This is more than true also in fraud networks, as fraudulent people have a high probability to

P a g e | 5

___________________ Solvency ii Association

be connected to other fraudulent people, and legitimate people have a high probability to connect to legitimate people. To read more: http://blogs.sas.com/content/brightdata/2016/11/21/practical-guide-tackle-auto-insurance-fraud-social-network-analytics/?utm_content=bufferbded5&utm_medium=social&utm_source=twitter.com&utm_campaign=buffer

P a g e | 6

___________________ Solvency ii Association

Macroprudential Policy for Insurers Paper by Vicky Saporta, Chair of the Executive Committee of the International Association of Insurance Supervisors, Association of British Insurers Annual Conference 2016

Introduction 1. Aspects of what we now term microprudential regulation of insurance have existed for well over 100 years in a number of countries. For example, New Hampshire established the first state agency for the supervision of insurance in the United Stated in 1851. In the UK, the first Act of Parliament on Life Assurance in the UK was enacted in 1870. 2. Microprudential insurance regulators have continually adapted their approaches as financial markets and products have become more complex and understanding of risk improves. Risk-based regulation is the latest development in this process of improvement. But even risk-based regulation has now been around for about the last 25 years or so in some jurisdictions. 3. Turning to macroprudential regulation – the concept has been around since the 1970s, with central bank financial stability reports becoming common from mid-1990s onwards. Statutory-based macroprudential regulation, with explicit statutory objectives, policy tools and operational decision making frameworks, however, has largely been a post-crisis development. 4. There is no question in my mind that microprudential regulation to protect companies’ safety and soundness and to protect policyholders is the key foundation of all insurance prudential regulation.

P a g e | 7

___________________ Solvency ii Association

And I know that this is not a controversial statement. What is more controversial is whether macroprudential regulation has a role to play in insurance regulation. 5. In what follows, I will explain why I believe that microprudential regulation – the key plank of prudential regulation in insurance - needs to be complemented with macroprudential overlays to be comprehensive and fully effective.

Macroprudential Regulation 6. Part of the challenge of understanding the implications of macroprudential regulation is setting out what we mean by it. 7. Back in 2003, Claudio Borio, the BIS’s Head of the Monetary and Economic Department and an influential thinker in this area, described the objective of microprudential regulation as limiting the likelihood of distress at an individual institution. In insurance this objective tends to be aligned to an objective about the safety and soundness of regulated firms. By contrast, Borio saw the objective of macroprudential policy as limiting the risk of losses to income in the economy arising through the endogenous behaviour of financial firms and capital markets. 8. According to this view, microprudential regulation is about protecting the firm and its policyholders from external shocks beyond its control (e.g. a longevity shock, a shock from interest rates, or a cyber attack) or from risks in the way it manages itself (e.g. because of its business strategy or governance). Macroprudential regulation is about protecting others from the way a firm or a set of firms contributes to the build-up of risks and to the propagation of amplification of risks. To read more: http://www.bankofengland.co.uk/publications/Documents/speeches/2016/speech941.pdf

P a g e | 8

___________________ Solvency ii Association

Is there a liquidity problem post-crisis? Speech by Mr Stanley Fischer, Vice Chair of the Board of Governors of the Federal Reserve System, at the "Do We Have a Liquidity Problem Post-Crisis?", a conference sponsored by the Initiative on Business and Public Policy at the Brookings Institution, Washington DC Market liquidity is the ability to rapidly execute sizable securities transactions at a low cost and with a limited price impact. The high degree of liquidity in U.S. capital markets historically has contributed to the efficient allocation of capital through lower costs and a mix of bank- and market-based finance that supports the flexibility of these markets. Regulatory changes may have altered financial institutions' incentive to provide liquidity, raising concerns brought into sharp relief by several "flash events" over the past few years. At the same time, any changes in observed liquidity are also likely accompanied by other related changes-such as in technology-and a more complete assessment of these shifts is important when we think about the effects on liquidity of changes in financial regulations that were induced by the global financial crisis. This afternoon, I will first review some of the concerns raised by market participants and others about market liquidity as well as highlight the challenges associated with finding clear evidence that substantiates these concerns. I will then discuss whether potential impairment of liquidity might exacerbate problems related to fire sales and leverage. Finally, I will make the case that any changes in market liquidity resulting from regulatory changes should be analyzed in the broader context of the overall safety of the financial system. This perspective naturally emphasizes potential tradeoffs between the possibly adverse effect regulations may have on market liquidity and their positive effect on the stability of the financial system.

P a g e | 9

___________________ Solvency ii Association

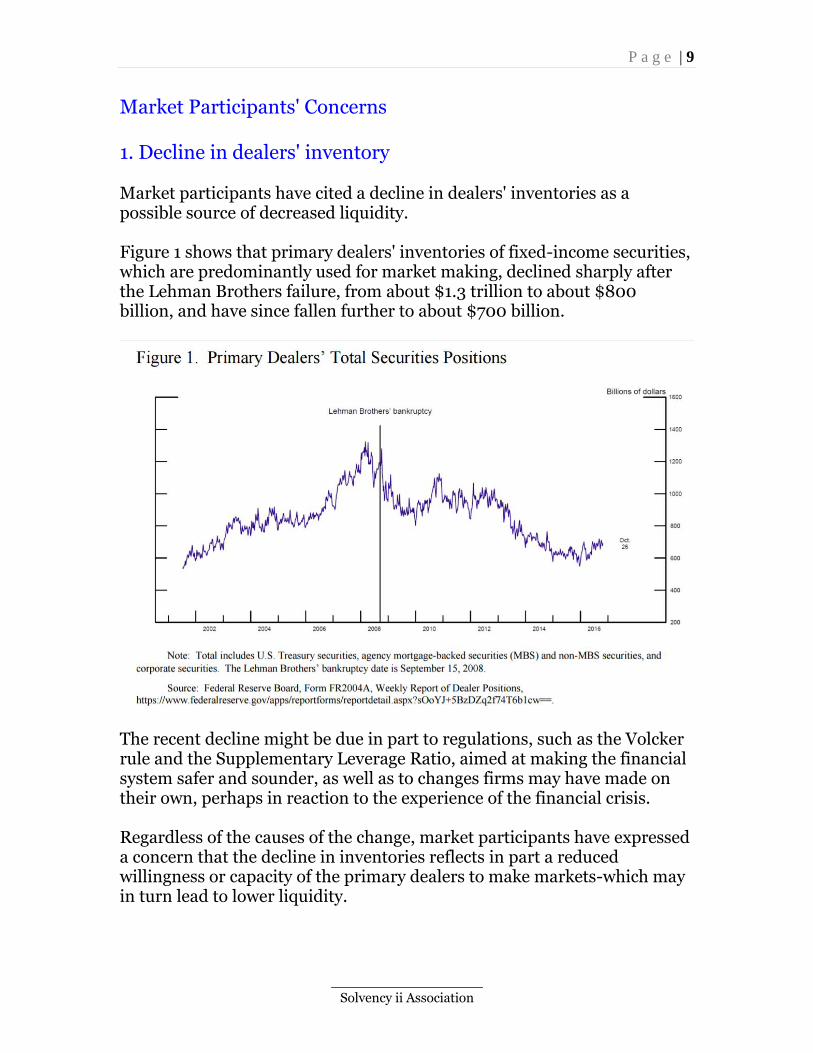

Market Participants' Concerns 1. Decline in dealers' inventory Market participants have cited a decline in dealers' inventories as a possible source of decreased liquidity. Figure 1 shows that primary dealers' inventories of fixed-income securities, which are predominantly used for market making, declined sharply after the Lehman Brothers failure, from about $1.3 trillion to about $800 billion, and have since fallen further to about $700 billion.

The recent decline might be due in part to regulations, such as the Volcker rule and the Supplementary Leverage Ratio, aimed at making the financial system safer and sounder, as well as to changes firms may have made on their own, perhaps in reaction to the experience of the financial crisis. Regardless of the causes of the change, market participants have expressed a concern that the decline in inventories reflects in part a reduced willingness or capacity of the primary dealers to make markets-which may in turn lead to lower liquidity.

P a g e | 10

___________________ Solvency ii Association

However, whether markets are in fact less liquid depends on both the degree to which the decrease in primary dealers' inventories affects their willingness to provide liquidity and the extent to which nonbank firms such as hedge funds and insurance companies fill any lost market-making capacity.

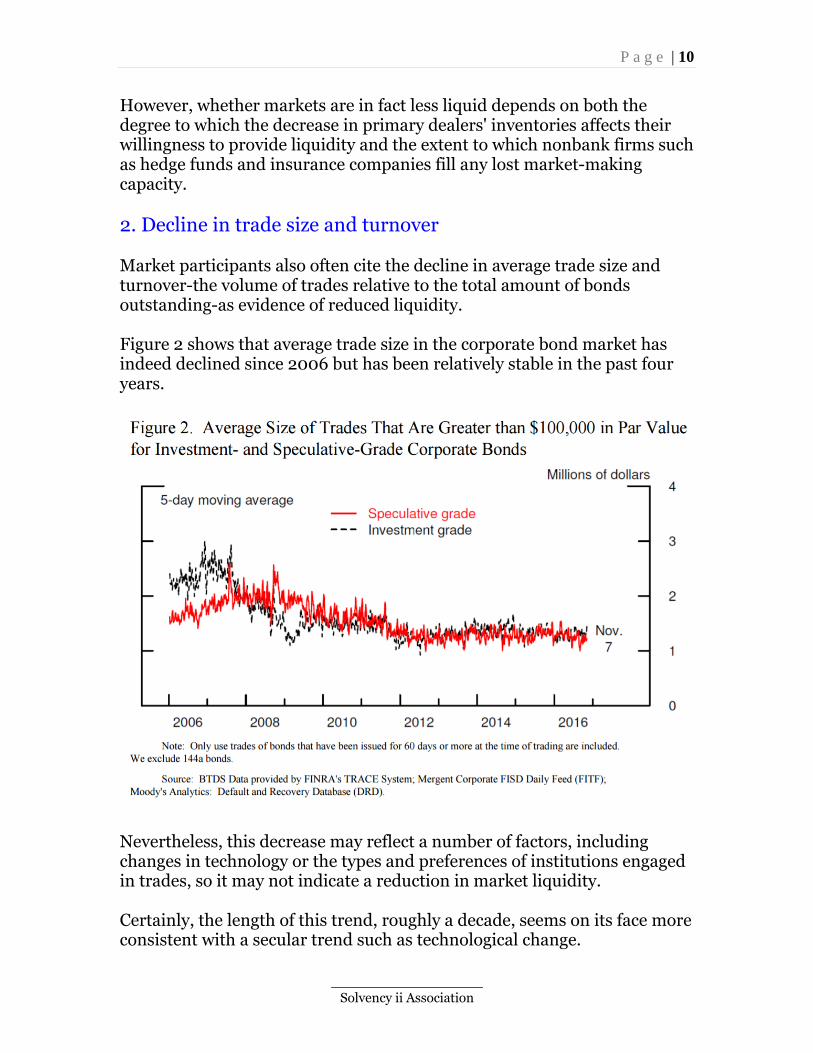

2. Decline in trade size and turnover Market participants also often cite the decline in average trade size and turnover-the volume of trades relative to the total amount of bonds outstanding-as evidence of reduced liquidity. Figure 2 shows that average trade size in the corporate bond market has indeed declined since 2006 but has been relatively stable in the past four years.

Nevertheless, this decrease may reflect a number of factors, including changes in technology or the types and preferences of institutions engaged in trades, so it may not indicate a reduction in market liquidity. Certainly, the length of this trend, roughly a decade, seems on its face more consistent with a secular trend such as technological change.

P a g e | 11

___________________ Solvency ii Association

Turnover in the corporate bond market has declined as well, though this evidence is also not a definitive sign of reduced market liquidity. The decline in turnover is not driven by a reduction in trading volume, but it is the result of a robust growth of the denominator, debt outstanding.

3. Liquidity during times of stress Market participants further express concern about the potential for market liquidity to become less resilient during times of stress, when it is needed the most. However, evidence on this front is difficult to gather. Some argue that market liquidity is resilient because financial markets appear to have functioned fairly well during recent episodes of high market volatility, such as following the Brexit vote or earlier this year, when oil prices were low and stock market volatility was high. Others argue that it is not. According to a recent study, the cost of trading distressed corporate bonds appears to be higher now than in the recent past. Specifically, the authors find that, before the crisis, the cost of a $1 million bond transaction increased about 0.7 percent following a downgrade, but-after the Volcker rule-the cost following a downgrade rose 2.4 percent. This analysis, however, is limited to episodes of distressed borrowers rather than a systemwide stress.

4. Flash events In addition, recent flash events-such as the sharp movement in Treasury prices on October 15, 2014; the rapid rise and decline of the euro-dollar exchange rate on March 18, 2015;6 and the swing in sterling on October 7, 2016-have led some to assert that market liquidity has become less resilient. Researchers at the Federal Reserve Bank of New York have argued that spikes in volatility and sudden declines in liquidity have become more frequent in both Treasury and equity markets.

P a g e | 12

___________________ Solvency ii Association

The Commodity Futures Trading Commission also points out that flash events are more common now. Market participants suggest that the rapid growth in high-frequency trading in equity, foreign exchange, and U.S. Treasury markets, along with broader concerns about less resilient liquidity, potentially explains these flash events. Nevertheless, a report on the October 15, 2014 event by the staff of the Treasury Department, Federal Reserve, and market regulatory agencies found no single factor that caused the sharp swing in prices. To read more: https://www.bis.org/review/r161118d.pdf

P a g e | 13

___________________ Solvency ii Association

10 Steps to Cyber Security Guidance on how organisations can protect themselves in cyberspace, including the 10 steps to cyber security.

This collection comprises: - an introduction to cyber security for executive/board-level staff - a white paper that expains what a common cyber attack looks like, and

how attackers execute them - the 10 technical advice sheets you should consider putting in place.

P a g e | 14

___________________ Solvency ii Association

P a g e | 15

___________________ Solvency ii Association

To learn more: https://www.ncsc.gov.uk/guidance/10-steps-cyber-security

https://www.ncsc.gov.uk/content/files/protected_files/guidance_files/common_cyber_attacks_ncsc.pdf

P a g e | 16

___________________ Solvency ii Association

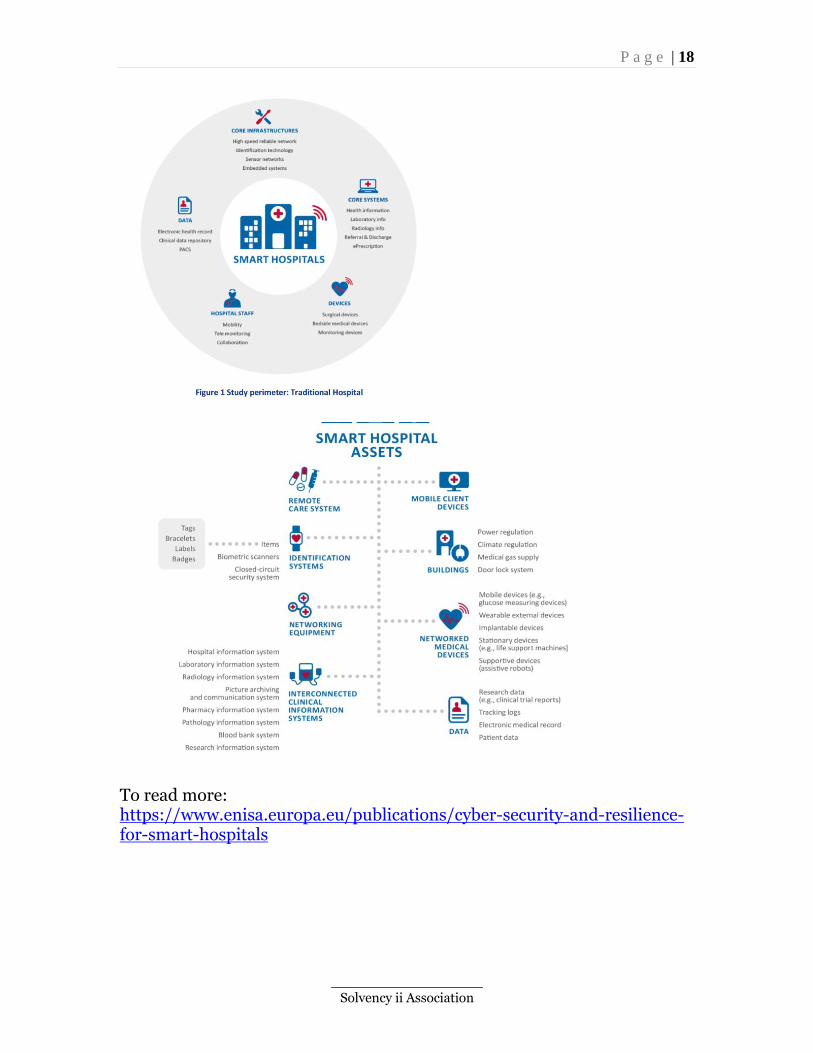

Smart Hospitals Security and Resilience for Smart Health Service and Infrastructures In recent years, many pervasive systems for healthcare have been proposed, discussed and sometimes realised. Pervasive healthcare is highly multifaceted, with many applications focusing on interoperability with the legacy hospital assets, the “traditional hospital”, the security and privacy of sensitive information and the usability of end users. The notion of smart hospitals is introduced when Internet of Things (IoT) components are supporting core functions of a hospital. Collaboration among various stakeholders, numerous interconnected assets and high flexibility requirements do not only lead to complexity and dynamics but also to blurred organisational boundaries. Due to the great number of significant assets at stake (patient life, sensitive personal information and financial resources) information security is a key issue for smart hospitals. Threats to smart hospitals are, however, not limited to malicious actions in terms of their root cause. Human errors and system failures as well as third-party failures also play an important role. The risks that result from these threats and corresponding vulnerabilities are typically mitigated by a combination of organisational and technical security measures taken by smart hospitals which comprise good practices. With respect to organisational measures, compliance with standards, staff training and awareness raising, a sound security organisation, and the use of guidelines and good practices are particularly relevant. Relevant technical measures include network segmentation, asset and configuration management, and network monitoring and intrusion detection.

P a g e | 17

___________________ Solvency ii Association

However, manufacturers of information systems and devices used in smart hospitals have to take certain measures too. Among them are, for instance, building security into products from the outset, adopting secure coding practices and extensive testing. Based on the analysis of documents and empirical data, and the detailed examination of attack scenarios found to be particularly relevant for smart hospitals, the study proposes key recommendations primarily for hospital executives. Namely hospitals should: - Establish effective enterprise governance for cyber security

- Implement state-of-the-art security measures

- Provide specific IT security requirements for IoT components in the hospital

- Invest in NIS products

- Establish an information security sharing mechanism

- Conduct risk assessment and vulnerability assessment

- Perform penetration testing and auditing

- Support multi-stakeholder communication platforms (ISACs) The study also makes recommendations for industry representatives in order to enhance the level of information security in smart hospitals. Namely industry players should: - Incorporate security into existing quality assurance systems

- Involve third parties (healthcare organisations) in testing activities

- Consider applying medical device regulation to critical infrastructure components

- Support the adaptation of information security standards to healthcare

P a g e | 18

___________________ Solvency ii Association

To read more: https://www.enisa.europa.eu/publications/cyber-security-and-resilience-for-smart-hospitals

P a g e | 19

___________________ Solvency ii Association

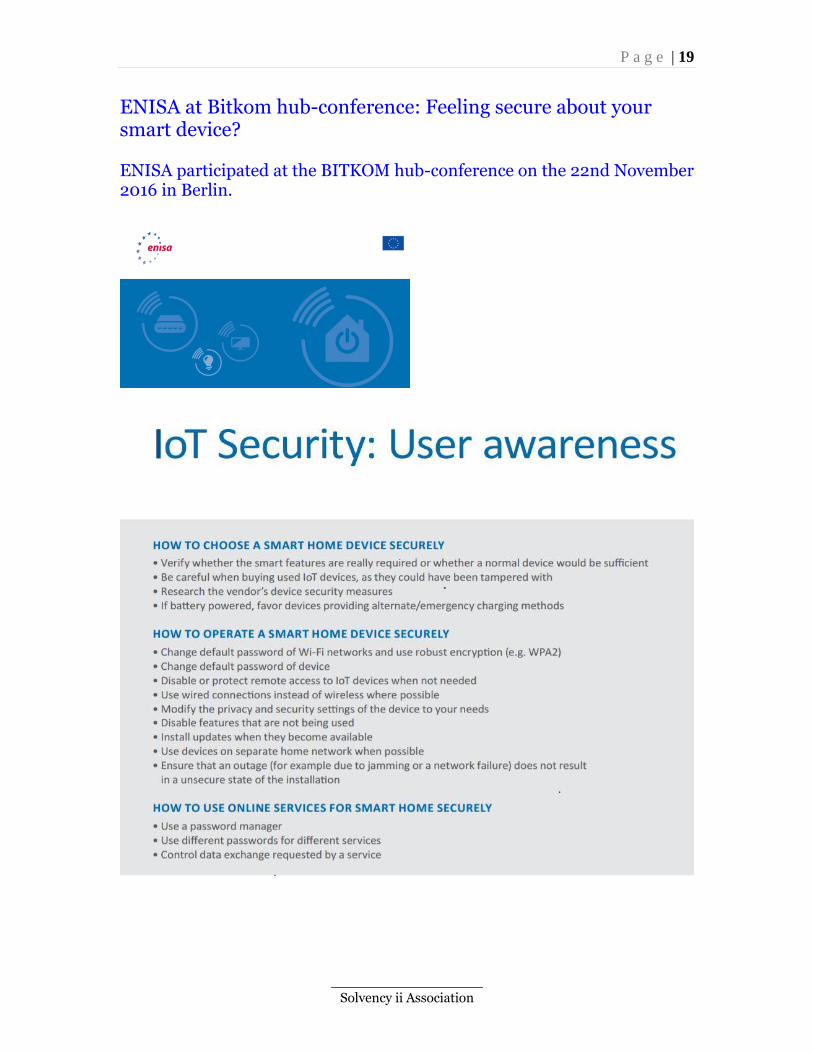

ENISA at Bitkom hub-conference: Feeling secure about your smart device? ENISA participated at the BITKOM hub-conference on the 22nd November 2016 in Berlin.

P a g e | 20

___________________ Solvency ii Association

P a g e | 21

___________________ Solvency ii Association

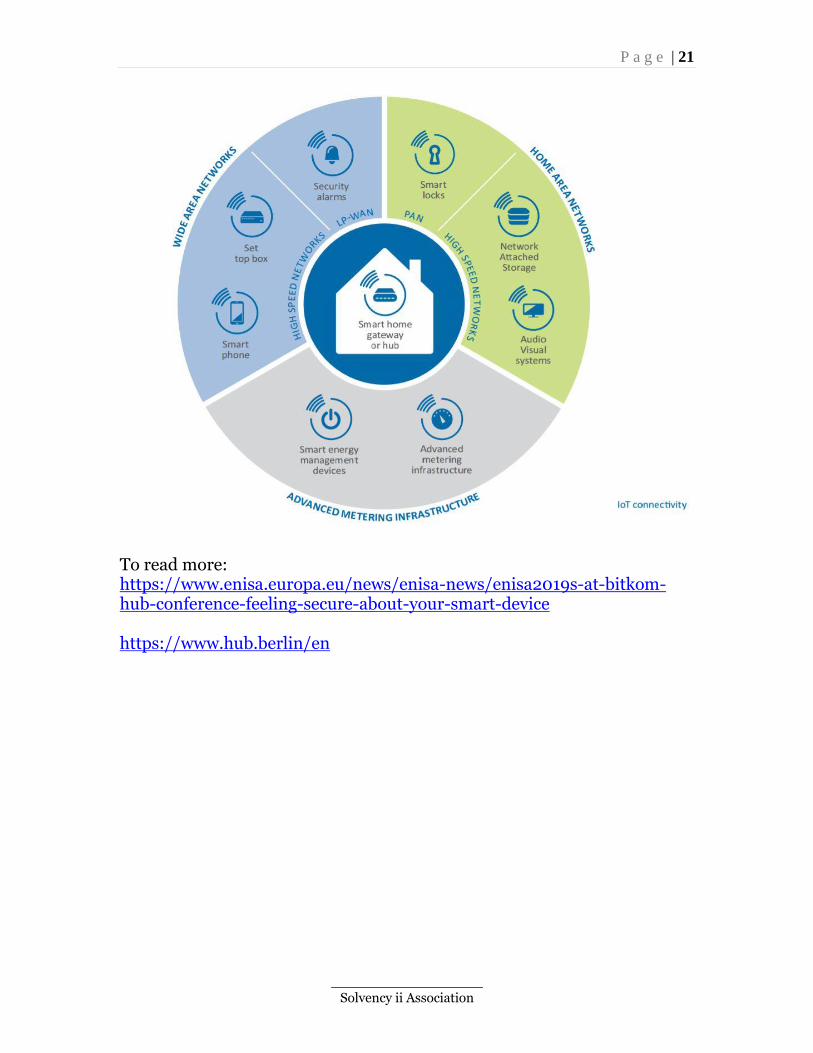

To read more: https://www.enisa.europa.eu/news/enisa-news/enisa2019s-at-bitkom-hub-conference-feeling-secure-about-your-smart-device https://www.hub.berlin/en

P a g e | 22

___________________ Solvency ii Association

The Spectre of Monetarism Mark Carney, Governor of the Bank of England, Roscoe Lecture, Liverpool John Moores University Real incomes falling for a decade. The legacy of a searing financial crisis weighing on confidence and growth. The very nature of work disrupted by a technological revolution. This was the middle of the 19th century. Liverpool was in the midst of a golden age; its Custom House was the national Exchequer’s biggest source of revenue. And Karl Marx was scribbling in the British Library, warning of a spectre haunting Europe, the spectre of communism. We meet today during the first lost decade since the 1860s. In the wake of a global financial crisis. And in the midst of a technological revolution that is once again changing the nature of work. Substitute Northern Rock for Overend Gurney; Uber and machine learning for the Spinning Jenny and the steam engine; and Twitter for the telegraph; and you have dynamics that echo those of 150 years ago. Then the villains were the capitalists. Should they today be the central bankers? Are their flights of fancy promoting stagnation and inequality? Does the spectre of monetarism haunt our economies? These are serious charges, based on real anxieties. They merit sober, objective assessment. This evening I want to discuss the role of monetary policy in this time of great disruption. But first I will focus on the underlying causes and consequences of weak real income growth and inequality across the advanced world.

P a g e | 23

___________________ Solvency ii Association

That’s because any doctor knows that the importance of diagnosing the underlying causes of the patient’s symptoms before administering the cure. Monetary policy has been keeping the patient alive, creating the possibility of a lasting cure through fiscal and structural operations. It has averted depression and helped advanced economies live to fight another day, so that measures to restore vitality can be taken. To read more: https://www.bis.org/review/r161207d.pdf

P a g e | 24

___________________ Solvency ii Association

Disclaimer The Association tries to enhance public access to information about risk and compliance management. Our goal is to keep this information timely and accurate. If errors are brought to our attention, we will try to correct them. This information: - is of a general nature only and is not intended to address the specific circumstances of any particular individual or entity; - should not be relied on in the particular context of enforcement or similar regulatory action; - is not necessarily comprehensive, complete, or up to date; - is sometimes linked to external sites over which the Association has no control and for which the Association assumes no responsibility; - is not professional or legal advice (if you need specific advice, you should always consult a suitably qualified professional); - is in no way constitutive of an interpretative document; - does not prejudge the position that the relevant authorities might decide to take on the same matters if developments, including Court rulings, were to lead it to revise some of the views expressed here; - does not prejudge the interpretation that the Courts might place on the matters at issue. Please note that it cannot be guaranteed that these information and documents exactly reproduce officially adopted texts. It is our goal to minimize disruption caused by technical errors. However some data or information may have been created or structured in files or formats that are not error-free and we cannot guarantee that our service will not be interrupted or otherwise affected by such problems. The Association accepts no responsibility with regard to such problems incurred as a result of using this site or any linked external sites.

P a g e | 25

___________________ Solvency ii Association

Solvency II Association 1. Membership - Become a standard, premium or lifetime member. You may visit: www.solvency-ii-association.com/How_to_become_member.htm 2. Monthly Updates - Subscribe to receive (at no cost) Solvency II related alerts, opportunities, updates and our monthly newsletter:

http://forms.aweber.com/form/70/2081713670.htm 3. Training and Certification – Become a Certified Solvency ii Professional. We are pleased to announce our updated Distance Learning and Online Certification programs: Become a Certified Solvency ii Professional (CSiiP) www.solvency-ii-association.com/CSiiP_Distance_Learning_Online_Certification_Program.htm Become a Certified Solvency ii Equivalence Professional (CSiiEP) www.solvency-ii-association.com/CSiiEP_Distance_Learning_Online_Certification_Program.htm For instructor-led training, you may contact us. We can tailor all programs to your needs. We tailor Solvency II presentations, awareness and training programs for supervisors, boards of directors, service providers and consultants. 4. Solvency II Association Authorized Certified Trainer (SOLV2A-ACT), Certified Solvency ii Professional Trainer (CSiiProT) Program - Become an ACT. This is an additional advantage on your resume, serving as a third-party endorsement to your knowledge and experience. Certificates are important when being considered for a promotion or other career opportunities.

P a g e | 26

___________________ Solvency ii Association

You give the necessary assurance that you have the knowledge and skills to accept more responsibility. To learn more you may visit: www.solvency-ii-association.com/Solvency_II_Association_Authorized_Certified_Trainer.html 5. Approved Training and Certification Centers (SOLV2A-ATCCs) - In response to the increasing demand for Solvency II, the Solvency II Association is developing a world-wide network of Approved Training and Certification Centers (SOLV2A-ATCCs). This will give the opportunity to risk and compliance managers, officers and consultants to have access to instructor-led Solvency II training at convenient locations that meet international standards. ATCCs deliver high quality training courses, using the Solvency II Association’s approved course materials and having access to Authorized Certified Trainers (SOLV2A-ACTs).