spain economic outlook - bbva research · spain economic outlook 2q17 main messages • the world...

TRANSCRIPT

Spain Economic Outlook

2Q17

SPAIN Economic Outlook

2ND QUARTER 2017

Spain Economic Outlook

2Q17

Main messages

• The world economy continues to improve, albeit

within an environment in which risks are still present

• In Spain, current figures confirm the upward bias.

Thus 2017 GDP growth forecast has been revised to

3%, while we have maintained unchanged the 2.7%

for 2018

• There are no major changes in the fundamentals of

growth, nor have there been second-round effects

regarding inflation so far

• Although reforms have had a positive impact, there

are still significant imbalances

Spain Economic Outlook

2Q17

Global Economic

Outlook 2ND QUARTER 2017

Spain Economic Outlook

2Q17

4

The positive dynamic takes hold

The main trends continue… …while uncertainties take shape

Recovery of

industrial activity and

international trade is confirmed

Financial markets stable

amidst growing geopolitical tension

Headline inflation continues to rise,

while core inflation remains stable

A substantial growth stimulus

in the US seems less likely...

…although more protectionist

scenarios too

Central banks move

towards normalisation

Spain Economic Outlook

2Q17

5

The world's economy continues to accelerate in early 2017

Global GDP growth Forecasts based on BBVA-GAIN (% QoQ)

Confidence indicators are at

very high levels, but hard

indicators only partially reflect

that improvement

China and advanced economies

show signs of strength.

However, the emerging

economies are performing more

irregularly

(e): estimated

Source: BBVA Research

0,4

0,6

0,8

1,0

1,2

CI 40%

GDP growth

Average for period

CI 20%

CI 60%

Ma

r 1

4

Ju

n 1

4

Se

p 1

4

De

c 1

4

Ma

r 1

5

Ju

n 1

5

Sep 1

5

De

c 1

5

Ma

r 1

6

Ju

n 1

6

Sep 1

6

De

c 1

6

Ma

r 1

7 (

e)

Ju

n 1

6 (

e)

Spain Economic Outlook

2Q17

(e): estimated

Based on BBVA-Trade Index figures

Source: BBVA Research and CPB

6

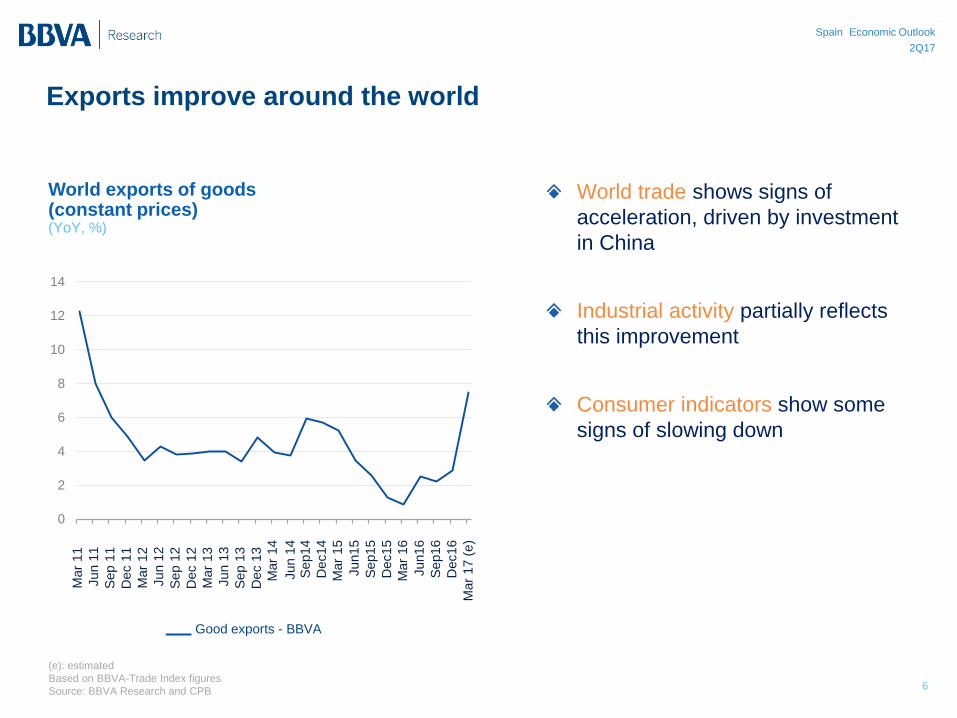

Exports improve around the world

World exports of goods (constant prices) (YoY, %)

World trade shows signs of

acceleration, driven by investment

in China

Industrial activity partially reflects

this improvement

Consumer indicators show some

signs of slowing down

0

2

4

6

8

10

12

14

ma

r-1

1

jun-1

1

sep-1

1

dic

-11

ma

r-1

2

jun-1

2

sep-1

2

dic

-12

ma

r-1

3

jun-1

3

sep-1

3

dic

-13

ma

r-1

4

jun-1

4

sep-1

4

dic

-14

ma

r-1

5

jun-1

5

sep-1

5

dic

-15

ma

r-1

6

jun-1

6

sep-1

6

dic

-16

ma

r-1

7

Exportaciones de bienes - BBVA

Mar

14

Jun 1

4

Sep14

Dec14

Mar

15

Jun15

Sep15

Dec15

Mar

16

Jun16

Sep16

Dec16

Mar

17 (

e)

Mar

11

Jun 1

1

Sep 1

1

Dec 1

1

Mar

12

Jun 1

2

Sep 1

2

Dec 1

2

Mar

13

Jun 1

3

Sep 1

3

Dec 1

3

Good exports - BBVA

Spain Economic Outlook

2Q17

7

Financial tension remains low

BBVA financial tension index (normalised index)

Volatility has shrunk despite

the economic policy

uncertainty

Fiscal and Monetary stimulus

mask substantives concerns

Europe has been the

exception, with sovereign

spreads increasing, due to

forthcoming French elections

and the overall political

scenario

Source: BBVA Research

-2,0

-1,0

0,0

1,0

2,0

4 M

ar-

14

4 S

ep

-14

4 M

ar-

15

4 S

ep

-15

4 M

ar-

16

4 S

ep

-16

4 M

ar-

17

Desarrollados Emergentes Developed Emerging

China1 China2 Brexit

0

Ma

r 1

4

Se

p 1

4

Ma

r 1

5

Sep 1

5

Ma

r 1

6

Sep 1

6

Ma

r 1

7

Trump

Spain Economic Outlook

2Q17

8

Inflation shows no signs of second round effects so far

Headline and core inflation (YoY, %)

The effect of commodity prices on

inflation is reaching its maximum

level

Core inflation remains low, without

apparent second-round effects

As a result, inflation forecasts have

been lowered

Source: BBVA Research and Haver

Core inflation – World

Core inflation – Developed economies

Headline inflation – World

Headline inflation – Developed

economies

0

1

2

3

4

en

e-1

6

feb-1

6

ma

r-1

6

ab

r-1

6

ma

y-1

6

jun-1

6

jul-16

ag

o-1

6

sep-1

6

oct-

16

no

v-1

6

dic

-16

en

e-1

7

feb-1

7

Mar

16

Apr

16

May 1

6

Jun 1

6

Jul 16

Aug 1

6

Sep 1

6

Oct 16

Dec 1

6

Jan 1

7

Fe

b 1

7

Jan 1

6

Feb 1

6

Nov 1

6

Spain Economic Outlook

2Q17

9

FED and ECB interest rates (bp)

Central banks move towards a normalisation of their policies

Source: BBVA Research, FED and

ECB

0,0

0,5

1,0

1,5

2,0

2,5

en

e-1

6

ab

r-1

6

jul-16

oct-

16

en

e-1

7

ab

r-1

7

jul-17

oct-

17

en

e-1

8

ab

r-1

8

jul-18

oct-

18

FED BCE

ECB

Gradual fall in spending

ECB

End of QE. Remains

remains stable

Jan 1

6

Apr

16

Jul 16

Oct 16

Jan 1

7

Apr

17

Jul 17

Oct 17

Jan 1

8

Apr

18

Jul 18

Oct 18

FED ECB

The Federal Reserve continues to raise interest rates,

although it remains cautious about the economic

The ECB is increasingly looking at an exit strategy for

monetary policy

Spain Economic Outlook

2Q17

10 Source: BBVA Research. Latin America comprises: Argentina, Brazil, Chile, Colombia, Mexico, Paraguay, Peru, Uruguay and

Venezuela

Upward revision in China and the eurozone, slightly higher in Latin

America. Unchanged in the US.

USA.

2017

2.3 2018

2.4

LATIN AMERICA

2018

1.8

EURO ZONE

CHINA 2017

1.7

2018

5.8

2018

1.7

2017

1.1

2017

6.3

Downwards

Upwards

Remains

WORLD

2018

3.4 2017

3.3

Spain Economic Outlook

2Q17

11

China: a new impulse from old engines

GDP growth (YoY, %)

We have revised our forecasts for

2017 and 2018 upwards, due to

recent figures that mainly reflect

the fiscal impulse

Nevertheless, mid-term risks

remain considerable:

• The rebalancing process toward

services and consumption has

stagnated

• Economic policy mistakes may lead to

disorderly deleveraging process

Source: BBVA Research and CEIC

3

4

5

6

7

2017 2018

Current forecast Previous forecast

6.3 5.8

Spain Economic Outlook

2Q17

12

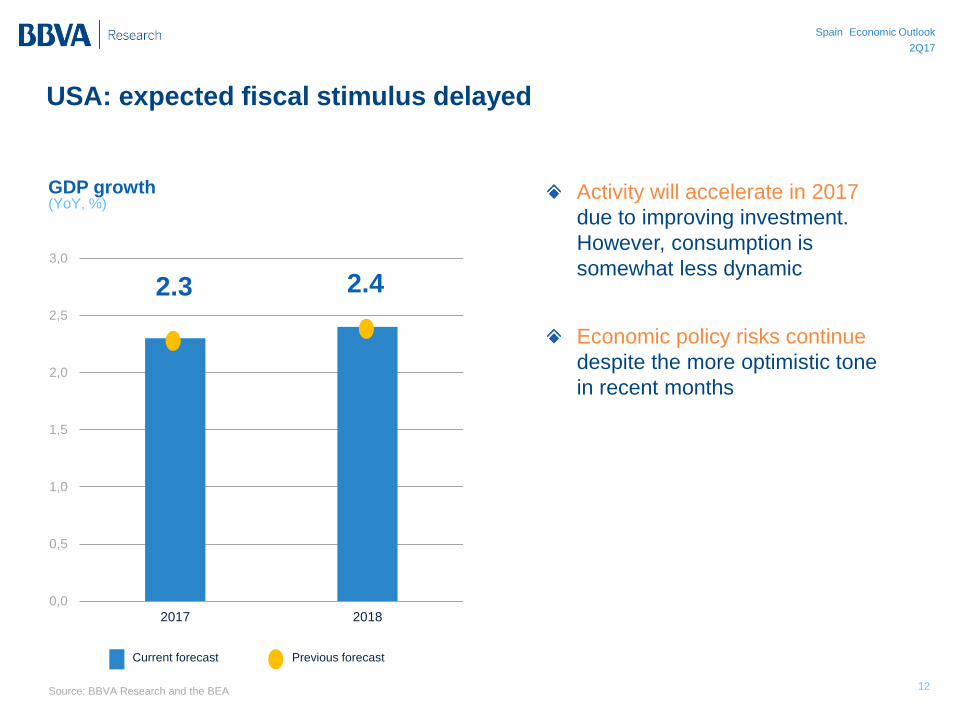

USA: expected fiscal stimulus delayed

Activity will accelerate in 2017

due to improving investment.

However, consumption is

somewhat less dynamic

Economic policy risks continue

despite the more optimistic tone

in recent months

Source: BBVA Research and the BEA

GDP growth (YoY, %)

0,0

0,5

1,0

1,5

2,0

2,5

3,0

2017 2018

Current forecast Previous forecast

2.3 2.4

Spain Economic Outlook

2Q17

13

The eurozone: a more positive panorama, although risks remain

Slight upward growth revision in

2017 and 2018, which may drive

inflation. Exports are behind this

improved scenario

Risks are mainly political in nature,

but there are still many sources of

uncertainty (electoral cycle, hard

Brexit, Greece, the geopolitical

prospect etc.)

Source: BBVA Research and Eurostat

GDP growth (YoY, %)

0,0

0,5

1,0

1,5

2,0

2017 2018

Current forecast Previous forecast

1.7 1.7

Spain Economic Outlook

2Q17

Spain Economic

Outlook 2ND QUARTER 2017

Spain Economic Outlook

2Q17

Recent economic figures (e.g.

employment and exports) point

to a slightly better than expected

short-term outlook

Upward revision of 0.3pp in the

growth forecast, which now

stands at 3% for 2017

Spain: Observed GDP growth and forecasts of the

MICA-BBVA Model* (% QoQ.

(e): estimated

Source: BBVA Research

(*) Camacho, M. and R. Doménech (2010): “MICA-BBVA: A Factor Model of Economic and Financial Indicators

for Short-term GDP Forecasting”, BBVA WP 10/21, available at: http://goo.gl/zeJm7g

Upward bias confirmed

15

0,0

0,5

1,0

1,5

0,0

0,5

1,0

1,5

ma

r.-1

4

jun.-

14

sep.-

14

dic

.-1

4

ma

r.-1

5

jun.-

15

sep.-

15

dic

.-1

5

ma

r.-1

6

jun.-

16

sep.-

16

dic

.-1

6

ma

r-1

7 (

e)

jun-1

7 (

e)

CI (20%) GDP (%, QoQ)

Spain Economic Outlook 1Q17 CI (40%)

CI (60%)

Ma

r 1

4

Ju

n 1

4

Se

p 1

4

Dec 1

4

Ma

r 1

5

Ju

n 1

5

Se

p 1

5

De

c 1

5

Ma

r 1

6

Ju

n 1

6

Se

p 1

6

De

c 1

6

Ma

r 1

7 (

e)

Jun

16

(e)

Spain Economic Outlook

2Q17

16

...despite the slowdown in internal demand

Spain: contributions to YoY GDP growth (%)

We have seen slower

growth in household

consumption, private

investment in machinery

and equipment

Some cyclical stimulus

may have run out (pent-up

demand), while uncertainty

may have seen growth

clipped

(e): estimated

Source: BBVA Research based on INE (National Statistics Institute) figures

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2015 2016 2017 (e)

M&E Investment Consumption GDP

Spain Economic Outlook

2Q17

17

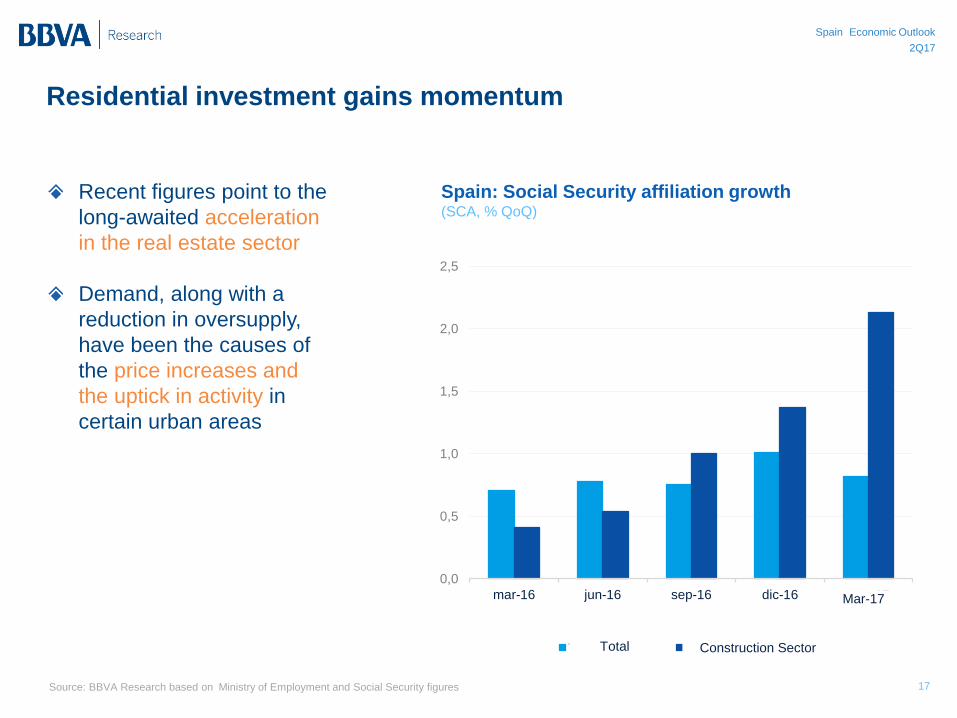

Residential investment gains momentum

Spain: Social Security affiliation growth (SCA, % QoQ)

Recent figures point to the

long-awaited acceleration

in the real estate sector

Demand, along with a

reduction in oversupply,

have been the causes of

the price increases and

the uptick in activity in

certain urban areas

Source: BBVA Research based on Ministry of Employment and Social Security figures

0,0

0,5

1,0

1,5

2,0

2,5

mar-16 jun-16 sep-16 dic-16 mar-17

Total Sector de la construcciónConstruction Sector Total

Mar-17

Spain Economic Outlook

2Q17

18

Exports of goods recover, despite Brexit

The recovery in goods

exports can be explained

partly by improved

performance in emerging

markets

The euro zone continues to

bolster growth in exports,

while lower sales to the

United Kingdom has had a

relatively small impact

Spain: Exports per country (trend, %YoY)

(e): estimated

*Red and green respectively indicate

negative and positive quarterly trend variations

Source: BBVA Research based on INE figures

Se

p-1

5

De

c-1

5

Ma

r-1

6

Ju

n-1

6

Se

p-1

6

De

c-1

6

ma

r-1

7 (

e)

Total

UNIÓN EUROPEA

ZONA DEL EURO

- FRANCIA

- ALEMANÍA

- ITALIA

UE, EXTRA UEM

- REINO UNIDO

RESTO DEL MUNDO

AMERICA

AMÉRICA LATINA

CHINA

min 0 max

Se

p-1

5

De

c-1

5

Ma

r-1

6

Ju

n-1

6

Se

p-1

6

De

c-1

6

ma

r-1

7 (

e)

Total

UNIÓN EUROPEA

ZONA DEL EURO

- FRANCIA

- ALEMANÍA

- ITALIA

UE, EXTRA UEM

- REINO UNIDO

RESTO DEL MUNDO

AMERICA

AMÉRICA LATINA

CHINA

min 0 max

TOTAL

EUROZONE

France

Germany

Italy

EU, NON-EMU

United Kingdom

REST OF THE WORLD

Latin America

China

EUROPEAN UNION

Sep 1

5

Dec 1

5

Mar 1

6

Jun 1

6

Sep 1

6

Dec 1

6

Mar 1

7

Se

p-1

5

De

c-1

5

Ma

r-1

6

Ju

n-1

6

Se

p-1

6

De

c-1

6

ma

r-1

7 (

e)

Total

UNIÓN EUROPEA

ZONA DEL EURO

- FRANCIA

- ALEMANÍA

- ITALIA

UE, EXTRA UEM

- REINO UNIDO

RESTO DEL MUNDO

AMERICA

AMÉRICA LATINA

CHINA

min 0 max

Spain Economic Outlook

2Q17

19

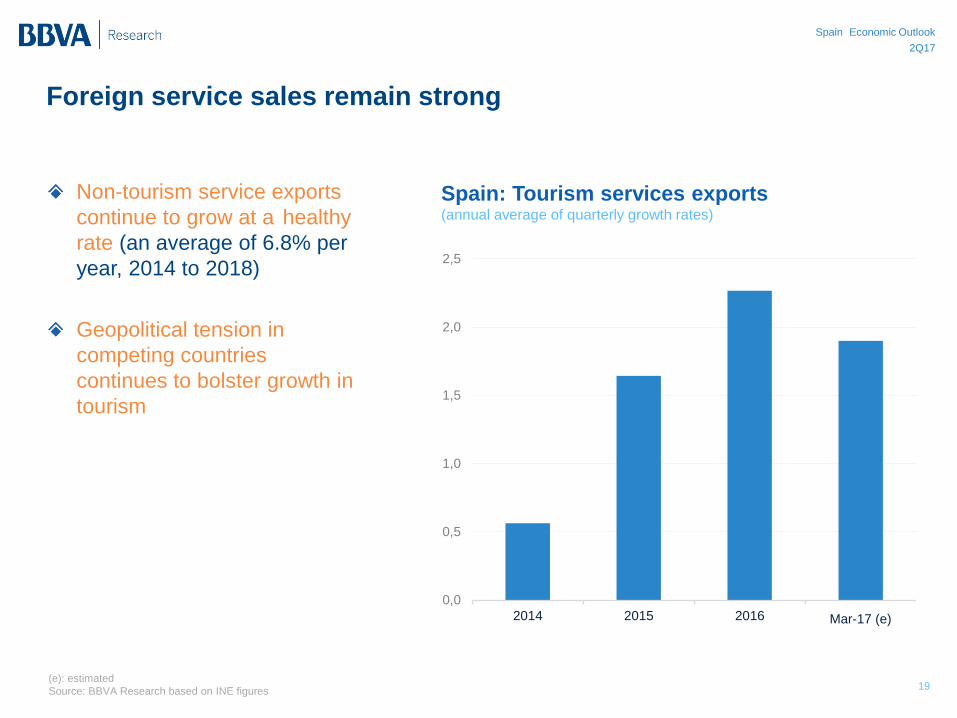

Foreign service sales remain strong

Spain: Tourism services exports (annual average of quarterly growth rates)

Non-tourism service exports

continue to grow at a healthy

rate (an average of 6.8% per

year, 2014 to 2018)

Geopolitical tension in

competing countries

continues to bolster growth in

tourism

(e): estimated

Source: BBVA Research based on INE figures

0,0

0,5

1,0

1,5

2,0

2,5

2014 2015 2016 mar-17 (e)Mar-17 (e)

Spain Economic Outlook

2Q17

20

Source: BBVA Research

We revise our 2017 GDP growth forecast to 3%

2016 2017 2018

3.2% 3.0% 2.7%

Spain Economic Outlook

2Q17

3 2

21

1

Oil price

Despite increases

in recent months,

prices stay 40% below

2014 levels

Euro exchange rate

The euro is still depreciated

against the dollar in 2017, but

with an upward trend for 2018

Risk premium

Still low as a result of the

ECB's Asset Purchase

Programme

Global demand

Positive perspectives,

especially in the euro zone

and in emerging markets,

will drive the exports

Geopolitical tension

Tourism in Spain will continue

to benefit from the perception

of insecurity in competing

destinations

Official Interest rates

At historical lowest levels,

with expectations of

moderate increases in the

short term interest rates in

late 2018

The global context, positive for Spain

5 4

Spain Economic Outlook

2Q17

-1,5 -1,0 -0,5 0,0 0,5 1,0 1,5 2,0

1997-2007

2008-2013

2014-2016

Wages Productivity Margins Taxes Total

Spain: breakdown of the inflation differential with respect to the EMU 12 based on the GDP

deflator (average annual growth)

22

Inflation: gains from competitiveness

During recovery, competitiveness gains have remained stable, thanks to the contribution of both margins and

wages

This distribution has been consistent with the creation of employment, the growth of investment and the increase in

exports. Maintaining this level will be key

Source: BBVA Research based on AMECO figures

Competitiveness gain Competitiveness loss

Spain Economic Outlook

2Q17

23

Fiscal policy in line with targets

(f): forecast.

Source: BBVA Research

Spain: Fiscal adjustment (%, YoY)

The 2016 deficit (in line with

expectations), recovery and

Central Government Budget for

2017 make the stability target

viable

Although there is some

uncertainty regarding expected

revenues, the higher GDP and

prices growth will facilitate a

reduction of the deficit

4,3

1,2 0,0

3,1

1,0 0,0

2,1

0

1

2

3

4

5

Dé

ficit 2

01

6

Política f

isca

l p

asiv

a

Política d

iscre

cio

nal

Dé

ficit 2

01

7

Política f

isca

l p

asiv

a

Política d

iscre

cio

nal

Dé

ficit 2

01

8

2017(p) 2018(p)

Pa

siv

e fis

ca

l p

olic

y

Fis

ca

l e

ffo

rt

De

ficit 2

01

7

Pa

siv

e fis

ca

l p

olic

y

Fis

ca

l e

ffo

rt

De

ficit 2

018

2017(f) 2018(f)

De

ficit 2

01

6

Spain Economic Outlook

2Q17

24

Economic performance highlights structural improvements

Source: BBVA Research based on INE and CF INC

The ongoing upward revision of GDP growth forecasts suggests an underestimation of both structural and

cyclical factors

Deleveraging efforts would appear to have been underestimated, as has reorientation towards external

demand and the impact of reforms

Spain: Potential 2015 GDP growth by forecast date (%)

2015 Forecasted

three years ago

0.5 Current

forecast

1.2

Spain Economic Outlook

2Q17

25

In the medium term, improved productivity will be a key factor

Source: BBVA Research based on Eurostat figures

The gap between Spain and the

EMU in productivity growth has

decreased in recent years

Productivity growth is still low,

although in part this might be the

result of global factors

There are some signs of structural

improvement

0,0

0,2

0,4

0,6

0,8

1,0

1,2

1,4

1,6

1T95-4T07 3T13-4T16

Zona Euro España

Spain

3Q13-4Q16 1Q95-4Q07

Spain: Labour factor productivity (GVA per hour worked % QoQ, annualised average)

EMU

Spain Economic Outlook

2Q17

26

Sectoral composition shows some reasons for optimism

Source: BBVA Research

Productivity performance is

influenced by traditionally

leading sectors, such as ICT

and Manufacturing

Recently, other labour intensive

sectors have increased

productivity, as well as creating

employment

Spain: Labour productivity factor GVA per hour worked (% QoQ, average annualised)

-4

-3

-2

-1

0

1

2

3

4

1Q

95-1

Q08

2Q

08-2

Q13

3Q

13-4

Q16

1Q

95-1

Q08

2Q

08-2

Q13

3Q

13-4

Q16

1Q

95-1

Q08

2Q

08-2

Q13

3Q

13-4

Q16

1Q

95-1

Q08

2Q

08-2

Q13

3Q

13-4

Q16

ICT Manufacturing Professionalactivities

Retail,transport andhotel industry

Spain Economic Outlook

2Q17

90

95

100

105

110

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

PIB per cápita (base 2010=100) Nivel 2007 GDP per capita (2010=100)

27

In any event, there is still much to be done

1.2%

8.2

15.6

Unemployment rate

2007

2018

Spain: GDP per capita (2010=100)

Unemployment rate

Source: BBVA Research based on INE figures

2007 level

Spain Economic Outlook

2Q17

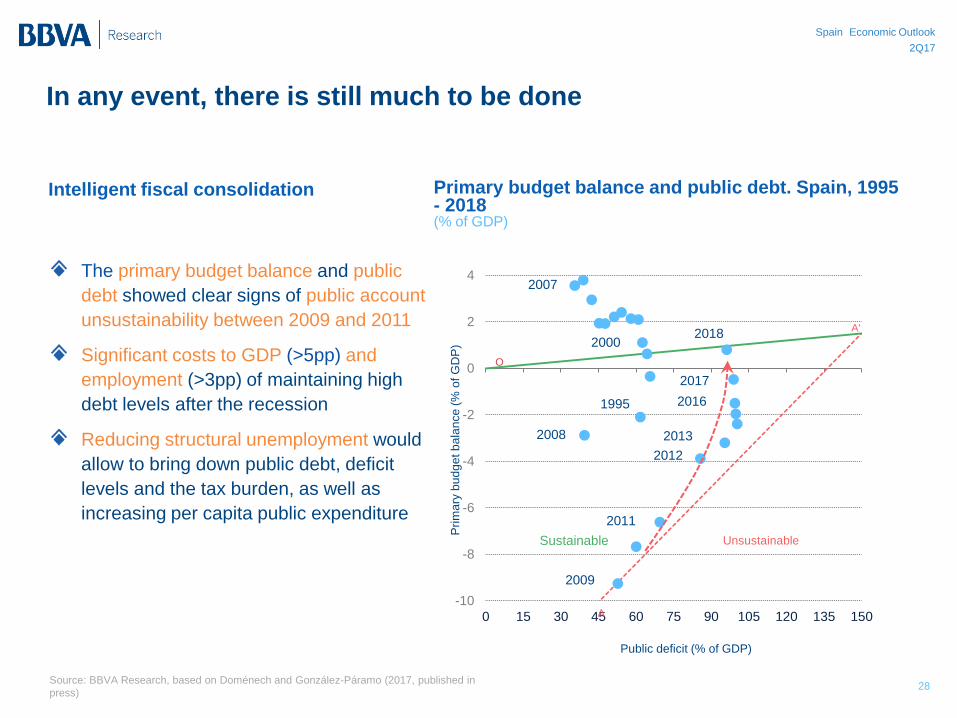

Intelligent fiscal consolidation

The primary budget balance and public

debt showed clear signs of public account

unsustainability between 2009 and 2011

Significant costs to GDP (>5pp) and

employment (>3pp) of maintaining high

debt levels after the recession

Reducing structural unemployment would

allow to bring down public debt, deficit

levels and the tax burden, as well as

increasing per capita public expenditure

Primary budget balance and public debt. Spain, 1995 - 2018 (% of GDP)

Source: BBVA Research, based on Doménech and González-Páramo (2017, published in

press)

Public deficit (% of GDP)

Pri

ma

ry b

ud

ge

t b

ala

nce

(%

of G

DP

)

28

In any event, there is still much to be done

1995

2000

2007

2008

2009

2011

2012

2013

2016

2017

2018

-10

-8

-6

-4

-2

0

2

4

0 15 30 45 60 75 90 105 120 135 150

A'

A

O

Unsustainable Sustainable

Spain Economic Outlook

2Q17

Main messages

• The world economy continues to improve, albeit

within an environment in which risks are still present

• In Spain, current figures confirm the upward bias.

Thus 2017 GDP growth forecast has been revised to

3%, while we have maintained unchanged the 2.7%

for 2018

• There are no major changes in the fundamentals of

growth, nor have there been second-round effects

regarding inflation so far

• Although reforms have had a positive impact, there

are still significant imbalances

Spain Economic Outlook

2Q17

SPAIN Economic Outlook

2ND QUARTER 2017