state of the cloud and data centers 2014

TRANSCRIPT

17 September 2014

State of Cloud and the Data CenterWhere we are, and where we’re going

September 16, 2014

Featuring Dave Bartoletti, Forrester Research, Inc.

Introducing today’s presenters:

2

KC MaresProduct Marketing,

Digital Realty@kcmares

Dave BartolettiPrincipal Analyst,

Forrester Research, Inc.@davebartoletti

Q&A Moderator:

3

Michael BohligDirector of Strategic Alliances,

Digital Realty@bohlig

© 2014 Forrester Research, Inc. Reproduction Prohibited 4

Cloud Is Now. The Question Is How?Manage digital disruption or be disrupted

© 2014 Forrester Research, Inc. Reproduction Prohibited 5

Cloud is the engine of digital disruption

• Digital disruption means committing to innovate in both the front and back office

• Cloud services are critical sources of speed and agility, not just cost reduction.

CLOUD IS A TOOL, NOT A COMPETITOR

CLOUD HELPS COMPANIES PROFIT FROM DISRUPTION

© 2014 Forrester Research, Inc. Reproduction Prohibited 6

Cloud disruption affects every industry

› Led by the “unicorns”… › But touching everyone.

“Every business is a software business”

© 2014 Forrester Research, Inc. Reproduction Prohibited 7

Cloud forecast: hypergrowth for both IaaS and PaaS thru 2020

$30B in 2018 =IaaS: $21BPaaS: $9B

$30B in 2018 =IaaS: $21BPaaS: $9B

38% Annual Growth Rate38% Annual Growth Rate

New IaaS+PaaS

Replacement

Source: April 24, 2014, “The Public Cloud Market Is Now In Hypergrowth” Forrester Report

© 2014 Forrester Research, Inc. Reproduction Prohibited 8

“What are your firm’s plans to adopt the following as-a-service technologies?”

Base: 2,200 to 2,444 IT software decision-makers US & EuropeSource: Forrsights Software Survey, Q4 2013

Cloud adoption takes off

*Planning to implement in the next 12 months**Planning to implement in a year or more

50% of companies using IaaS by end of 2014; 61% using at least one SaaS app

50% of companies using IaaS by end of 2014; 61% using at least one SaaS app

© 2014 Forrester Research, Inc. Reproduction Prohibited 9

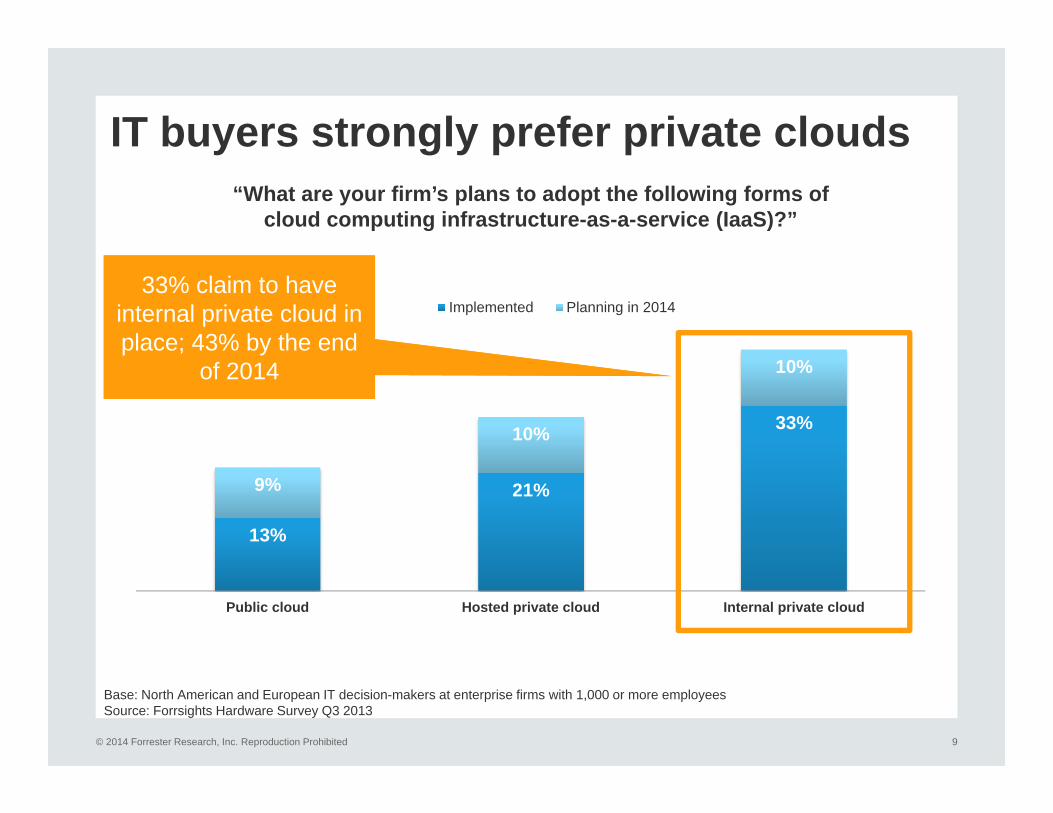

13%

21%

33%

9%

10%

10%

Public cloud Hosted private cloud Internal private cloud

Implemented Planning in 2014

“What are your firm’s plans to adopt the following forms of cloud computing infrastructure-as-a-service (IaaS)?”

Base: North American and European IT decision-makers at enterprise firms with 1,000 or more employeesSource: Forrsights Hardware Survey Q3 2013

IT buyers strongly prefer private clouds

33% claim to have internal private cloud in place; 43% by the end

of 2014

33% claim to have internal private cloud in place; 43% by the end

of 2014

© 2014 Forrester Research, Inc. Reproduction Prohibited

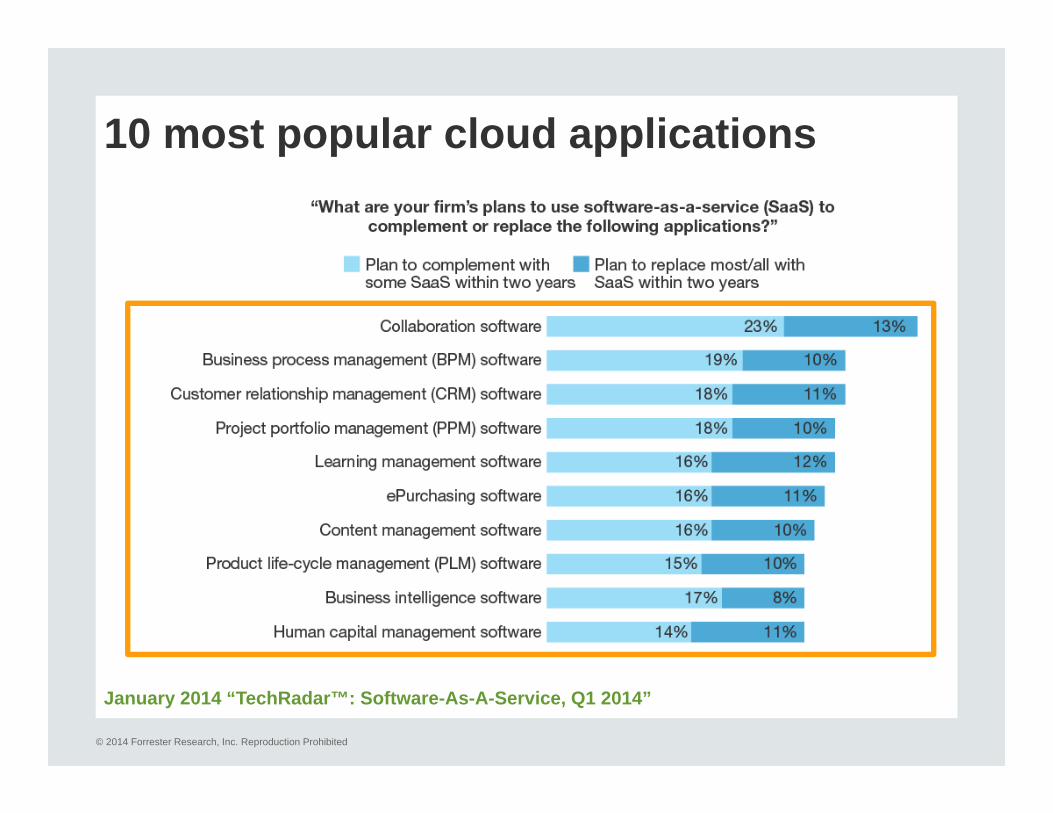

10 most popular cloud applications

January 2014 “TechRadar™: Software-As-A-Service, Q1 2014”

© 2014 Forrester Research, Inc. Reproduction Prohibited

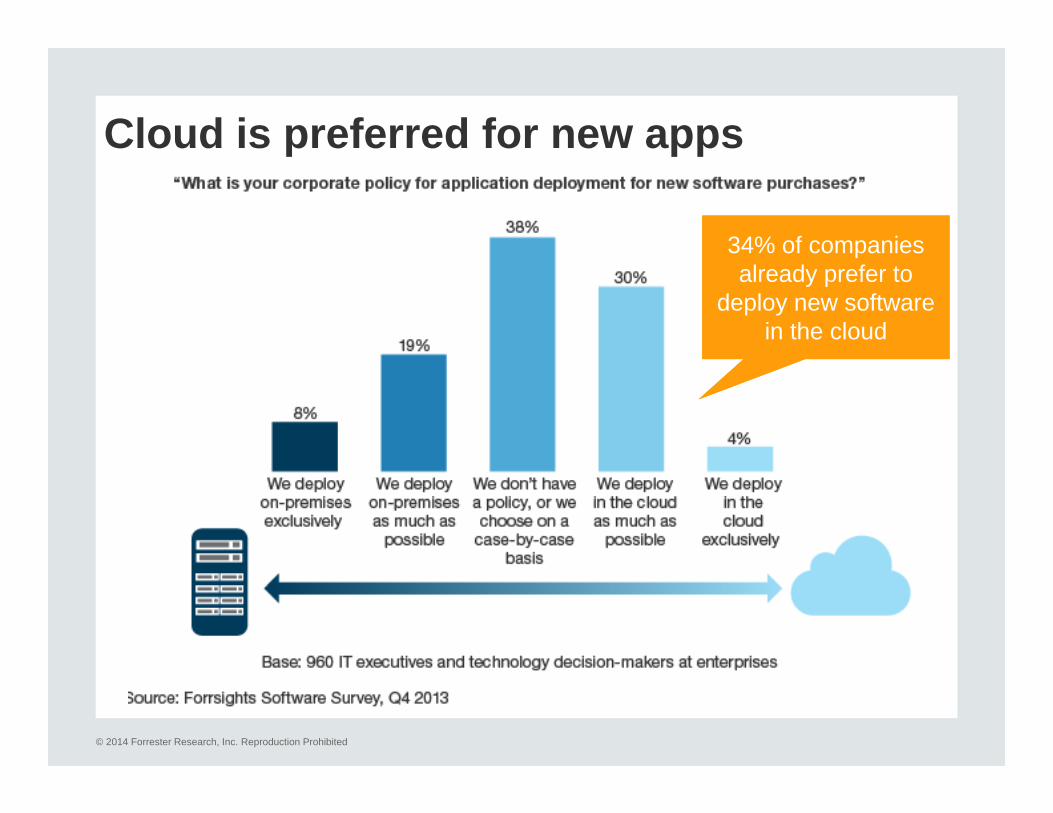

Cloud is preferred for new apps

34% of companies already prefer to

deploy new software in the cloud

34% of companies already prefer to

deploy new software in the cloud

© 2014 Forrester Research, Inc. Reproduction Prohibited 12

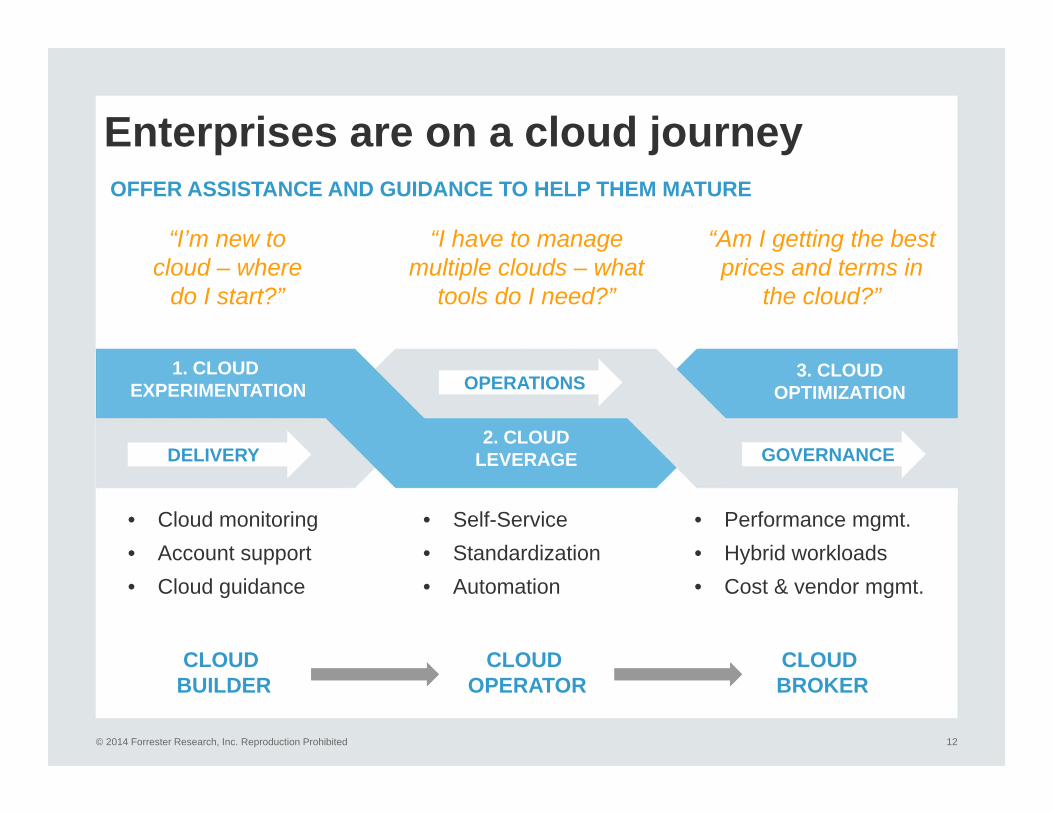

Enterprises are on a cloud journeyOFFER ASSISTANCE AND GUIDANCE TO HELP THEM MATURE

1. CLOUD EXPERIMENTATION

2. CLOUDLEVERAGE

3. CLOUDOPTIMIZATION

“I have to manage multiple clouds – what

tools do I need?”

“I’m new to cloud – where

do I start?”

“Am I getting the best prices and terms in

the cloud?”

• Cloud monitoring• Account support• Cloud guidance

• Self-Service• Standardization• Automation

• Performance mgmt.• Hybrid workloads• Cost & vendor mgmt.

DELIVERY

OPERATIONS

GOVERNANCE

CLOUD BUILDER

CLOUD OPERATOR

CLOUD BROKER

© 2014 Forrester Research, Inc. Reproduction Prohibited 13

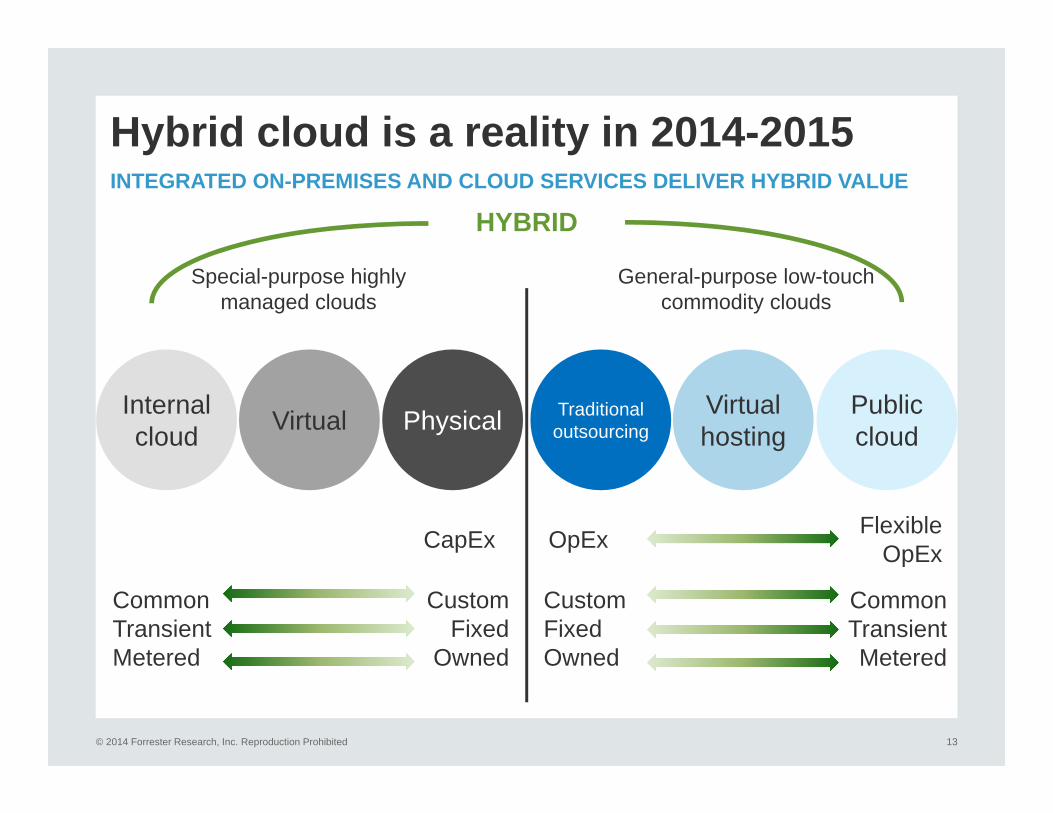

Hybrid cloud is a reality in 2014-2015INTEGRATED ON-PREMISES AND CLOUD SERVICES DELIVER HYBRID VALUE

PhysicalVirtualInternal cloud

Special-purpose highly managed clouds

CommonTransientMetered

CustomFixed

Owned

Public cloud

Virtualhosting

Traditional outsourcing

CommonTransientMetered

CustomFixedOwned

CapEx OpEx Flexible OpEx

General-purpose low-touch commodity clouds

HYBRID

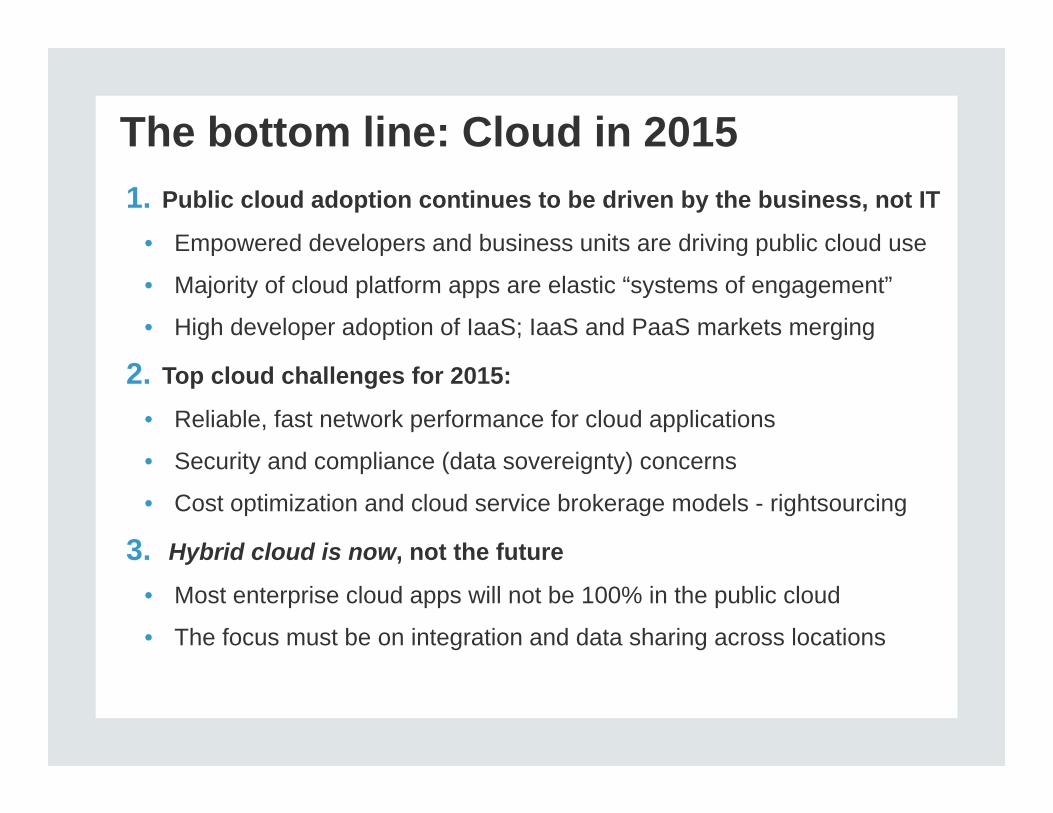

The bottom line: Cloud in 20151. Public cloud adoption continues to be driven by the business, not IT

• Empowered developers and business units are driving public cloud use

• Majority of cloud platform apps are elastic “systems of engagement”

• High developer adoption of IaaS; IaaS and PaaS markets merging

2. Top cloud challenges for 2015:

• Reliable, fast network performance for cloud applications

• Security and compliance (data sovereignty) concerns

• Cost optimization and cloud service brokerage models - rightsourcing

3. Hybrid cloud is now, not the future

• Most enterprise cloud apps will not be 100% in the public cloud

• The focus must be on integration and data sharing across locations

DigitalRealty

Solve for the three C’s with a mixture of Data center solutions

• Capacity– Public cloud solutions can

provide the quickest method to serving short-term and peak-capacity needs.

• Control– Private clouds can provide

high security.• Costs

– A mixture of public and private cloud solutions can meets the business needs at the lowest costs over time.

Public clouds provide

17

• Ability to quickly add capacity• New and alternate back up and disaster recovery options• Scale up to meet peak loads with minimal cost• Packaged apps such as SaaS and Desktop as a Service• Extending your virtual network

Private and internal Clouds provide

18

• Lowest costs for base loads• Most control of security

and privacy• Greatest control over

redundancy and uptime• Customized solutions• Highest management,

responsibility and resources

Hybrid clouds Balance costs and benefits

19

• Netflix grew with a large public cloud than merged into hybrid solutions

• ESPN uses public cloud solutions for extreme peak demands and private solutions to meet everyday customer demands

• Development platforms on public clouds gain the benefits of a larger platform for short-term testing and converted to private for production– Security is a keystone decision between public and

private platforms

Hybrid clouds Provide flexibility

20

• As workloads change, they can move between public and private platforms

• Hybrid solutions can provide the lowest cost across all geographies

• Hybrid solutions often balance lowest cost and flexibility• Hybrid solutions evolve to meet changing data and

privacy laws and security requirements

When deploying clouds

21

• Create a solution for the application and how it will be utilized

• Think about the network and how to achieve it at lowest cost

• Determine how to Integrate all systems– Don’t rely only on SaaS

for your back up solutions

Look for strong SLAs for your Mission-critical applications

• Uptime is critical for these apps– Today, “always up” matters more than even a few

years ago• Evaluate which applications are suitable for the cloud

and protect them with adequate SLAs• Public cloud SLAs are often weak or nonexistent• Create the right architecture and right level of

redundancy• Consider private cloud instead

Plan for the management of all Systems and applications

23

• Set up systems to remotely and centrally manage different infrastructure

• Automate tasks, migrations, back ups and redundancies

• Use same governance, compliance and security tools for internal and external cloud solutions

Security of data and network is critical

• Utilize platforms to minimize security risks and breaches of essential data and operations

• Think about which solution(s) will best prevent and recover from security breaches– Consider on-site data backed up off-site, and off-site

data backed up to an on- and/or another off-site data center

• Utilize solutions to meet country specific data sovereignty requirements

Plan for movement of big data

25

• Moving data into and out of cloud platforms and storing it in cloud platforms can be more costly

• Open-IX enables additional peering and connectivity

• 10 US Internet Exchange points are in DLR data centers. – Global, networked data

centers allow anyone in a DLR data center to connect with nearly any cloud and network provider for lowest cost and latencies

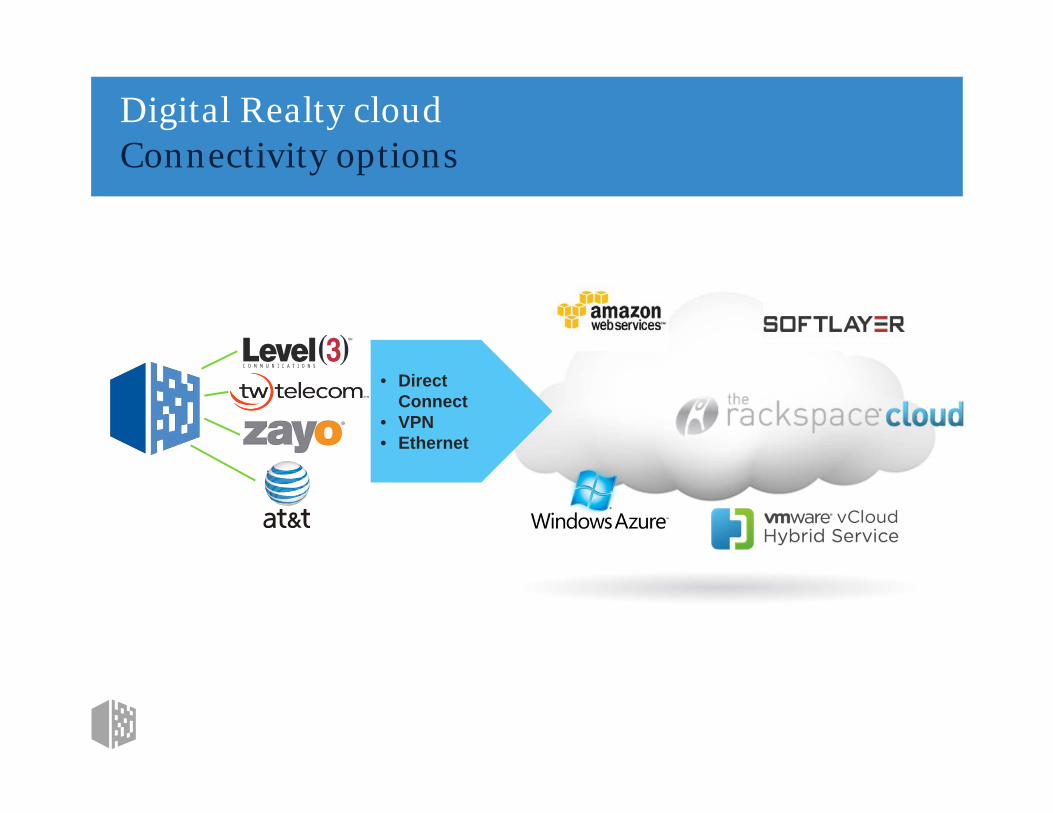

Digital Realty cloud Connectivity options

• Direct Connect

• VPN• Ethernet

Global Alliances

27

• Build faster with less risk

• Scale globally• Boost your skills• Connect

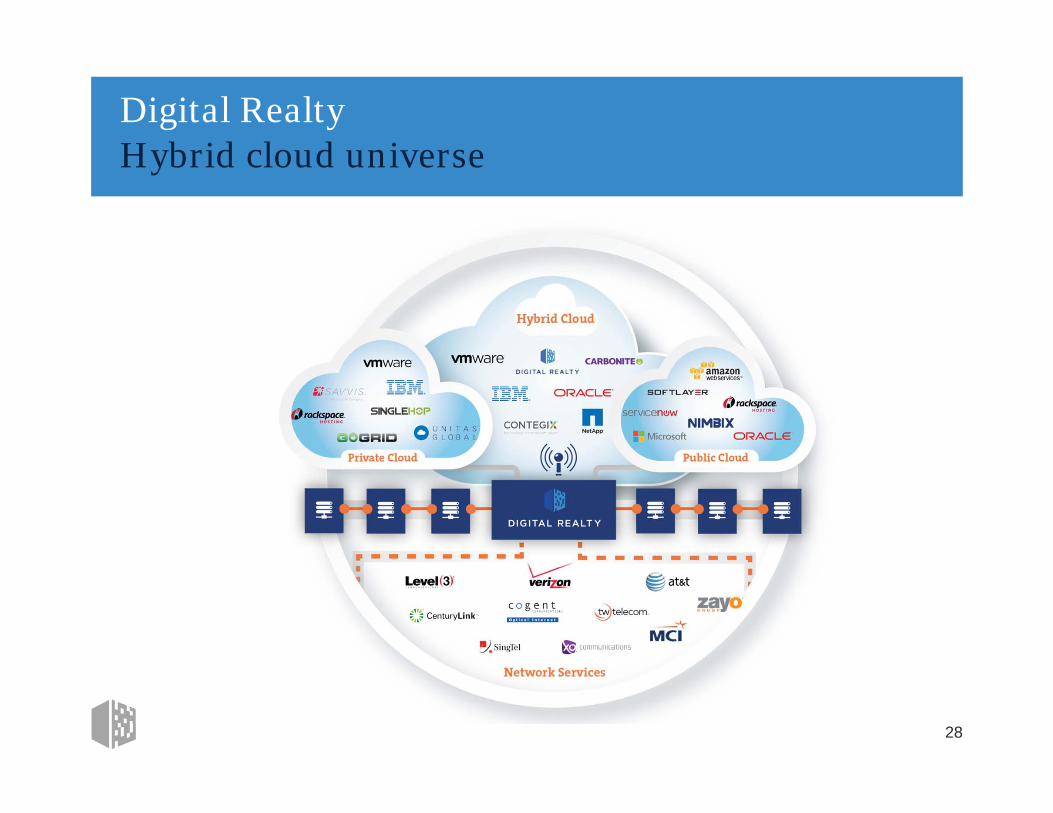

Digital Realty Hybrid cloud universe

28

Summary

• Consider combinations of public and private cloud solutions plus dedicated data centers to create comprehensive solutions that provide:– Scalability and the opportunity for growth– Higher performance and highest availability at the

lowest total cost– More performance yet less complexity and a higher

quality of service

Q&A

30

Presenters: Q&A Moderator:

KC MaresProduct Marketing,

Digital Realty@kcmares

Dave BartolettiPrincipal Analyst,

Forrester Research, Inc.@davebartoletti

Michael BohligDirector of Strategic Alliances,

Digital Realty@bohlig

Thank you for participating in the webinar.

Dave [email protected]@davebartoletti

KC [email protected]@kcmares