stockholders’ equity:paid-in capital

TRANSCRIPT

McGraw-Hill/Irwin Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights reserved.

Stockholders’ Equity:Stockholders’ Equity:Paid-In CapitalPaid-In Capitalotaleem.blogspot.comotaleem.blogspot.comfor more presentation(follow me)for more presentation(follow me)

Chapter 11

11-2

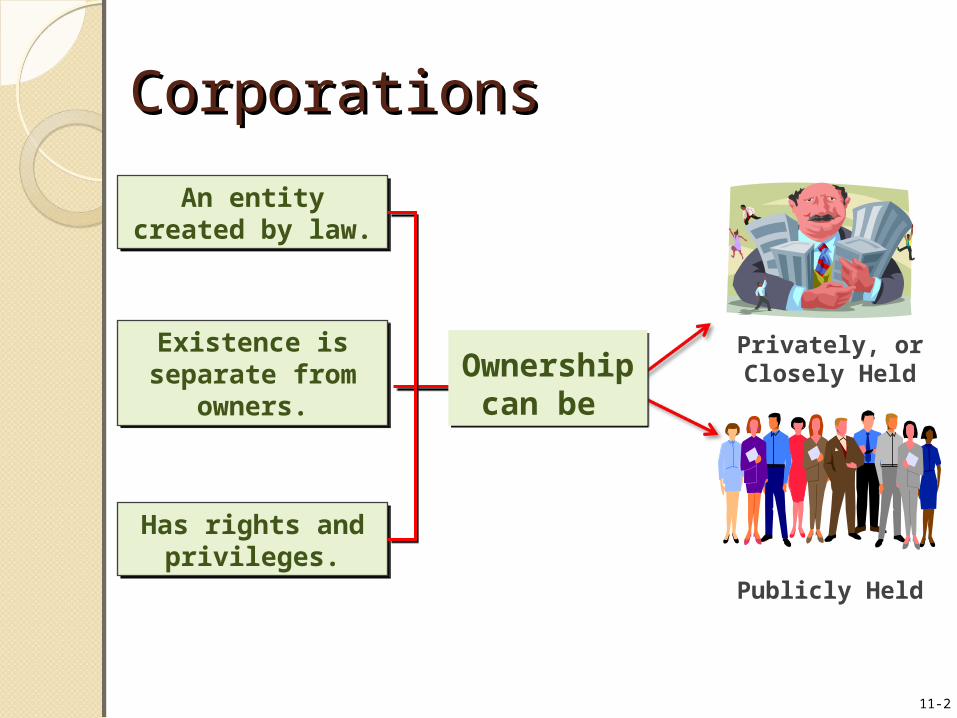

Existence is separate from

owners.

An entity created by law.

Has rights and privileges.

Privately, or Closely Held

Publicly Held

Ownership can be

CorporationsCorporations

11-3

Limited personal liability for

stockholders

Transferability of ownership

Professional management

Continuity of existence

Advantages of Advantages of IncorporationIncorporation

11-4

Heavy taxation

Greater regulation

Cost of formation

Separation of ownership and management

Disadvantages of Disadvantages of IncorporationIncorporation

11-5

The costs associated with incorporation are usually

expensed immediately, but amortized over 5 years for

tax purposes.

Formation of a CorporationFormation of a Corporation

• Each corporation is formed according to the laws of the state where it is located.

• The application for corporate status is called the Articles of Incorporation.

11-6

Stockholders

Rights

Voting (in person or by proxy).

Proportionate distribution of

dividends.Proportionate distribution of

assets in a liquidation.

Rights of StockholdersRights of Stockholders

11-7

Paid-in Capital

Contributions byinvestors in exchange

for capita l stock.

Retained Earnings

Retention of profitsearned by thecorporation.

Stockholders' equity isincreased in tw o w ays.

Stockholders’ Equity of a Stockholders’ Equity of a CorporationCorporation

11-8

Preferred StockPreferred StockA separate class of stock, typically having

priority over common shares in . . . Dividend distributions (rate is usually stated).

Distribution of assets in case of liquidation.

Cumulative dividend rights.

Normally has no voting

rights.

Usually callable by

the company.

Other Features Include:

11-9

Accounting by the issuer.

Accounting by the investor.

Common stock is carried at original issue

price.

Investments in marketable securities are carried at market

value.

Market ValueMarket Value

11-10

Ice Cream Parlor

Stock SplitsNow

Available

Stock SplitsStock Splits Companies use

stock splits to reduce market price.

Outstanding shares increase, but par value is decreased proportionately.

11-11

When stock is reacquired, the corporation records the treasury stock at cost.

Treasury shares are

issued shares that have been reacquired

by the corporation.

Treasury StockTreasury Stock

11-12

Self-testing QuestionSelf-testing QuestionSolve the Demonstration problem

Brief Exercise 11.1, 11.2,11.3, 11.4,11.5Exercise 11.4

11-13

End of Chapter 11End of Chapter 11