storming the cell tower: cable msos move mobile backhaul to the forefront

TRANSCRIPT

© Ciena Confidential and Proprietary

Storming the Cell Tower:

MSOs Move Mobile Backhaul to

the Forefront

2 © Ciena Confidential and Proprietary

Mobile Backhaul: Towering opportunity for N.A. MSOs

North American Mobile Internet Traffic (Peak Period)

Source: Sandvine, October 2010

More mobile data

volume = more mobile

backhaul capacity

Global Mobile Data Traffic Forecast

3 © Ciena Confidential and Proprietary

Backhaul is Booming!

Number of macro cell sites

increasing – 3.8M globally by 2015

More wireless service providers

connecting to same towers

Carriers deploying small cells to

fill coverage gaps

Smartphones

spurring higher

consumption of

multimedia

services

Wireless

carriers

continuing to

upgrade their

networks

4 © Ciena Confidential and Proprietary

Mobile backhaul services revenue (North America) Growth projected to accelerate in 2014

Source: Infonetics

Ethernet will account for >80% of all

backhaul services revenue by 2015

Technology

0

2

4

6

8

10

12

14

2011 2012

2013 2014

2015

Other

Satellite

SONET/SDH

Ethernet

PDH

An

nu

al

Re

ve

nu

e $

B

5 © Ciena Confidential and Proprietary

Mobile backhaul still a small subset of MSO revenue About 7 percent of U.S. cell sites under contract

0

10

20

30

40

50

60

70

80

90

0

1

2

3

4

5

6

7

8

# o

f To

wers

(1000’s

)

Early U.S. MSO Mobile Backhaul Activity

Source: Heavy Reading, June 2011

BH = Bright House Networks

CV-OL = Optimum Lightpath (division of Cablevision)

(Estimates)

MSOs served 18K towers

as of June ‘11, generating

$250M+ in ann. revenue.

An

n. R

ev. ($

M)

6 © Ciena Confidential and Proprietary

But, that’s about to change Combined MSO revenue could approach $1 billion by 2015

Projected Growth of U.S. Cable Mobile Backhaul Business

Source: Heavy Reading, June 2011

0

100

200

300

400

500

600

700

800

900

1000

0

5

10

15

20

25

30

35

40

45

50

2010 2011 2012 2013 2014 2015

# o

f C

ell

To

we

rs (

10

00

’s)

MSO industry will capture as much as15% of the

U.S. mobile backhaul market by 2015

Backh

au

l Rev. ($

M)

7 © Ciena Confidential and Proprietary

Rapid shift to Ethernet in backhaul domain

Contributing Factors:

• Accelerating migration from

TDM to packet technology

• Fiber and packet radios

replacing copper

• Network operators increasingly

adopting Ethernet

• Swift adoption of small-cell

technology (not counted here)

Outcome:

2010 2015

Total cell sites 289,000 345,000

3G/LTE cell sites 163,000 345,000

Total cell sites served by Ethernet backhaul

39,000 327,000

Ethernet-served cell sites – copper 1,200 3,000

Ethernet-served cell sites – microwave

8,000 80,000

Ethernet-served cell sites – fiber 20,000 182,000

Ethernet-served cell sites – HFC 10,000 62,000

Source: Heavy Reading, July 2011

Mobile Backhaul Connections: North America 2010 & 2015

95% of cell sites will be served

by Ethernet by 2015

8 © Ciena Confidential and Proprietary

The Emergence of Small-Cell Technologies Going where macro-cells can’t go

Fifty-eight percent of operators

plan to deploy 3G small cells by the

end of 2011 (Infonetics Research).

• 42 operators intend to deploy LTE

micro/pico cells

• About 40,000 4G small cells will

be deployed in the U.S. by 2015

(Heavy Reading)

• Vendors will ship 4 million base

stations each year by 2015 (ABI

Research)

Why? Small cells can fill coverage

gaps and boost capacity for voice,

data, and video traffic

Trend toward higher cell site density

creates a natural opportunity for MSOs

9 © Ciena Confidential and Proprietary

MSOs face challenges in serving backhaul market But, they aren’t insurmountable

Challenge How MSOs Overcome

Competitive • Incumbent providers remain

formidable players in the

backhaul market

• Better reach (res. footprint)

• Local market knowledge

• Fiber closer to cell towers

Financial • Cable operators must install

even more fiber to meet the

backhaul bandwidth demand

• Reducing cost of bandwidth

• Wider microwave radio adoption

• High-cap transport = lower cost/bit

• Fiber/tower proximity

Technical &

Operational

• Cable providers must meet

mobile carriers' growing

bandwidth, reliability, and

performance demands

• Faster Ethernet adoption

• MEF standards/certifications

• CableLabs collaboration

10 © Ciena Confidential and Proprietary

The Changing Face of Mobile Backhaul Technology Steady migration to packet services

MSC

PDH/SONET/SDH TDM

MSC

PDH/SONET/SDH

Packet Network

HYBRID

MSC

Packet Network PACKET

2011 2007 2015

11 © Ciena Confidential and Proprietary

The Case for Carrier Ethernet Lower TCO for Mobile Backhaul

More efficient any-to-any connectivity

• Fewer protocol layers provisioning, management, restoration

• Lower: equipment cost, people cost, complexity risk, reroute complexity / time

• Smooth migration path from legacy backhaul to LTE

• Compatible with metro transport (e.g. P-OTS)

User-IP

Transport-IP

S-GW

MME eNB

L2 CE/MPLS-TP Backhaul Network

(User IP hidden from backhaul network)

12 © Ciena Confidential and Proprietary

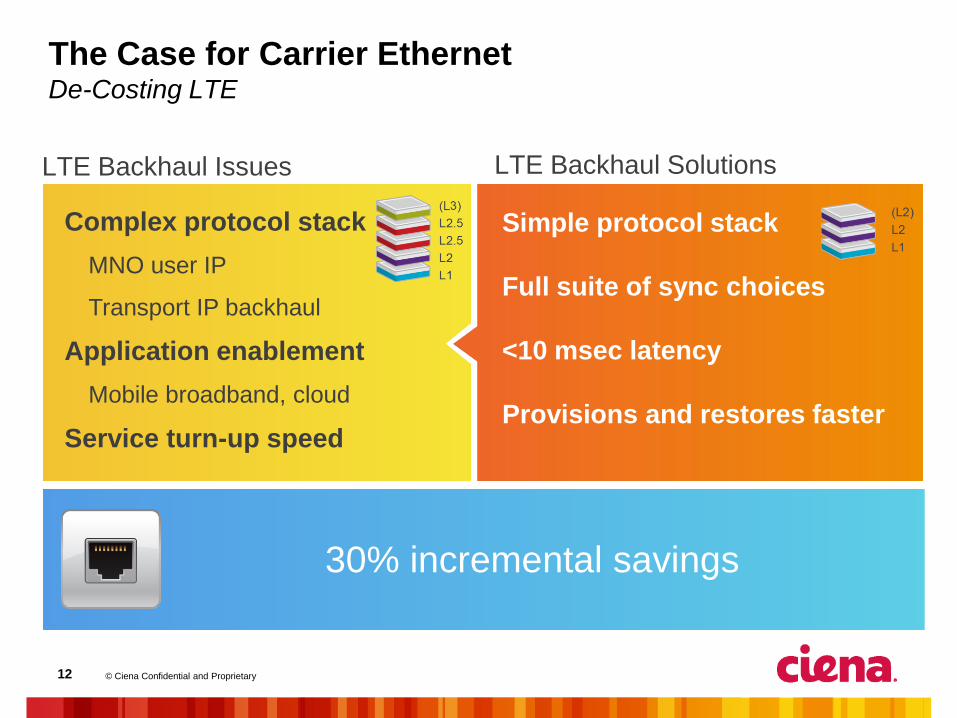

The Case for Carrier Ethernet De-Costing LTE

Complex protocol stack

MNO user IP

Transport IP backhaul

Application enablement

Mobile broadband, cloud

Service turn-up speed

Simple protocol stack

Full suite of sync choices

<10 msec latency

Provisions and restores faster

30% incremental savings

LTE Backhaul Issues LTE Backhaul Solutions

13 © Ciena Confidential and Proprietary

Ethernet OAM* Superior visibility, manageability, and control vs. Layer 3 solutions

Layer 2 solutions enjoy more

sophisticated and field-proven

OAM; more deterministic behavior

Layer 2 OAM standards have been

available longer

Proven Ethernet OAM Tools:

• Turn-up Acceptance and SLA

Conformance Testing

• SLA Monitoring & Metrics

• Service Heartbeats

• Enhanced troubleshooting, rapid

network discovery

FaultDetection

FaultRecovery

FaultNotification

FaultVerification

FaultIsolation

FaultDetection

FaultRecovery

FaultNotification

FaultVerification

FaultIsolation

Packet/Frame Loss Packet/Frame Delay

Packet/Frame Delay Variation

Continuity Check

Link Trace

Loopback

Packet/Frame Sequence

Synchronization

Alarm Indication (AIS)

Remote Configuration

Status Monitoring

Availability Remote Defect Indication (RDI)

Connectivity Verification

Link Error Threshold

Remote Loopback

Remote Failure Indication (dying gasp)

Lock

Test

Link Fault Signaling

*Operations, Administration, and Maintenance

14 © Ciena Confidential and Proprietary

Layer 2 or Layer 3 for Mobile Backhaul? The facts speak for themselves

A Layer 2 Carrier Ethernet

solution – whether based on

fiber or packet radio – permits

strong levels of control and

robust functionality, making it

a truly cost-efficient mobile

backhaul solution.

Scale the network quickly

Achieve lowest cost per bit

Match connectivity with data

demands

Avoid costly network over-

provisioning

• Ciena client

• Standard costs – Ciena solution

• Standard costs – L3 solution*

• Ciena solution: 30% lower TCO

Service Provider Example

• Heavy Reading's Quarterly Market Tracker (August 2010)

• SP deployment plan survey

• 2/3 will use L2 in their 4G backhaul access networks

Market Input

*Provided by client

2/3 will use Layer 2 in their 4G

backhaul access networks

15 © Ciena Confidential and Proprietary

MSO Case Study - U.S. provider of entertainment,

information and communications services

• Mobile backhaul deployment began in 2009

• Approximately 6,000 cell sites connected throughout the U.S.

• Cell sites connected to backhaul network using Ciena's CESD portfolio

Technical Criteria

•QoS supports

differentiated services

•Policy Enforcement

•Line-Rate Throughput

•Integrated enhanced

OAM capabilities

16 © Ciena Confidential and Proprietary

Conclusion

Number of cell sites will continue to increase to keep pace with mobile

voice, data, and video service growth

Wireless service providers will continue upgrading their networks

Cable operators can help wireless providers meet these urgent needs

Mobile backhaul is a strategic entry point into the larger Ethernet

business services market

Leading MSOs rely on Ciena’s True Carrier Ethernet to capitalize on the

growing demand for mobile backhaul and Ethernet Business Services