subnational debt & fiscal management in asia-pacific outline current stage of subnational...

TRANSCRIPT

Permission to reprint or distribute any content from this presentation

requires the prior written approval of Standard & Poor’s. Copyright © 2015

by Standard & Poor’s Financial Services LLC. All rights reserved.

Subnational Debt &

Fiscal Management in

Asia-Pacific

YeeFarn PHUA

Associate Director

Sovereign & International Public

Finance Ratings

June 4, 2015

Presentation Outline

Current stage of subnational borrowing in Asia: where is Asia on the global map?

Pros and Cons of subnational borrowing

Debt management

• Best practices in managing capital investments and funding sources, debt structure, transparency

• EM Asia: the range of policies and practices

Development of subnational borrowing in Asia – moving forward

Where is Asia on the Global Map?

Subnational ratings – a useful barometer of development

The US remains by far the most developed municipal bond market.

10,000+ rated public-sector entities

$3.63 trillion of municipal debt outstanding (as of end of third quarter 2014)

>50% of funds used for infrastructure projects comes from municipal bond

proceeds

Outside US, S&P rates more than 305 LRGs in 33 countries.

Asia-Pacific LRGs accounts for 13% of all ratings

Number of ratings is a good indicator of the stage of development and depth of

capital markets

Asia Pacific, 13

Mexico & other LatAm, 20

Canada, 16

Europe(& Russia), 51

S&P ratings on LRG globally (ex-US) (%)

Asia public sector borrowing – market overview

Currently 40 Asia-Pacific LG ratings

Many LGs in Asia would like to borrow. Some roadblocks include:

• debt restrictions; off-balance sheet borrowing for some

• lack of debt management capacity, discipline, transparency and credit culture; unsupportive national institutional frameworks

• insufficient size/scale – especially for bond issuance

Most developed: Australia, New Zealand, Japan

Outside the big 3: Some small domestic LGs issuance

Potential: Philippines, India, Indonesia, China, Vietnam, Thailand

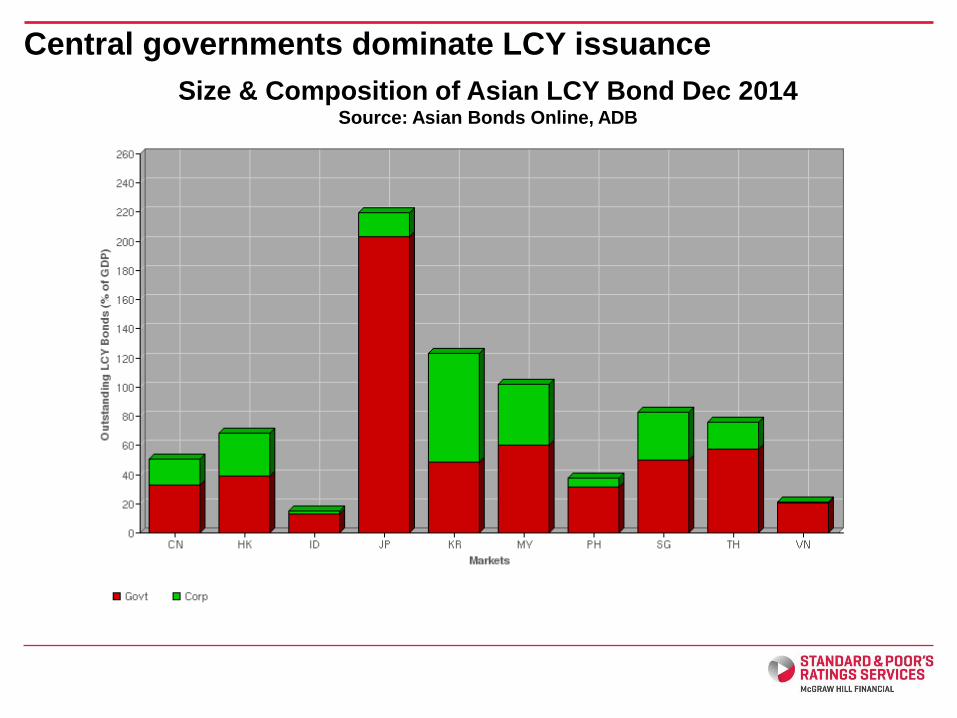

Central governments dominate LCY issuance

Size & Composition of Asian LCY Bond Dec 2014Source: Asian Bonds Online, ADB

Local Government Borrowing restrictions – a snapshot

China

LRGs are generally not allowed to borrow commercially except for the construction of roads. Some

LRGs are allowed to issue bonds through MoF or even by themselves, with size and tenor

approved by MoF, repayment made through MoF, and thus implicitly guaranteed by the central

government. LRGs also borrow extensively via investment companies, though subject to tightened

regulation and restriction since 2010.

India

The states are entitled to borrow, but they need approval from the central government. States

cannot borrow abroad, but can receive external funding indirectly from multilaterals and

development banks via on-lending from the central government.

Indonesia

The government moved to allow LRG bond issuance in 2007, but to date there have been no local

government issues: most LRGs fail to meet the minimum conditions set out by the central

government for doing so.

JapanCurrently 54 LRGs--out of some 1,800 total--are allowed to access capital markets, including

foreign exchange borrowings. The rest either borrow from the central government or from banks.

Malaysia

Peninsular (west) Malaysia states are not allowed to borrow commercially. East Malaysian states

have access to capital markets (including foreign exchange borrowings) albeit requiring federal

government approval.

Philippines

LRGs can borrow in local currency only. For foreign currency they need central bank approval. In

local currency they tend to borrow from government-owned banks. Only a small number/amount of

local bonds has been issued so far, and these are primarily guaranteed by the LGU Guarantee

Corp.

South KoreaLocal governments allowed to access capital market in local currency, but need additional approval

from the Ministry of Finance and Economy (MOFE) to borrow in foreign currency.

TaiwanLRGs can access capital markets for both local currency and foreign exchange. Thus far such

borrowing has only been in local currency.

ThailandLRGs can borrow commercially in local currency, but require central government approval for any

foreign exchange borrowings.

Vietnam

LRGs can borrow commercially in local currency, but require central government approval for any

foreign exchange borrowings. A few large cities have issued domestic bonds. Issuance is subject

to strict monitoring and approval by the central government. Ceiling rates are defined by MoF.

Importance of Local Government Borrowings

Why do local governments borrow?

Borrowing by LGs is important because it:

• Leads to equitable funding of infrastructure

• Provides additional sources of funding – more can be accomplished

• Has a positive effect on public finance management due to scrutiny

• Leads to more transparent funding strategies (i.e. moving off-balance sheet to on-balance sheet)

• Means a more flexible funding strategy

And also:

• Helps deepen domestic bond markets, as it provides assets and benchmarks for investors

Central Governments’ concerns about subnational risks…

Can be addressed by:

• Improved institutional frameworks, including balancing and monitoring mechanisms;

• Differentiation approach to LGs and other subnational entities;

• Building financial management quality and capacity at subnational level

rankings, ratings, risk-to-government products, financial management assessments etc.

technical assistance

Debt Management

Analytical Framework For Rating International LGs

The analytical framework to rate LGs consists of combined quantitative and

qualitative analysis around eight major factors:

Institutional Framework – the only LG rating factor that S&P assess on a

country basis for each level of government.

7 factors are based on the individual characteristics of an LG:

Economy

Financial management

Budgetary flexibility

Budgetary performance

Liquidity

Debt burden

Contingent liabilities

Quality Financial Management is KeyExtended FMA = Extended Financial Management Assessment is a

comprehensive assessment of the financial management sophistication and quality

of Local & Regional Governments.

How can FMA help?

• Increasing focus on building financial management capacity at sub-national levels

• Growing demand for public sector transparency and accountability in emerging

markets

• Continuing public finance reforms across emerging markets

• Growing need for global benchmarking of public finance quality

• Need to enhance information provided by a credit rating/credit report

• Need to assess LGs which are not yet ready for capital markets

S&P’s work with the World Bank;

- Russian Cities 2001-2004, 2006-2008

- Philippines LGUs 2008-2011

- China UDICs 2008-2009

- Indonesian LGs 2009 to 2012

Good practices in Debt Management – what we look for

Link to long-term and annual planning/budgeting

Transparency – timeliness, detail, frequency

Liquidity – linked to debt servicing needs among other demands on

liquidity; overdraft arrangements

Managing SOEs – debt as a contingent liability; guarantees

Management quality at the local level - Asia

Philippines LGUs:

• Weak intergovernmental system; key-man risk factor and lack of institutionalized

policies

• Short-term focused planning framework, weak debt management; But

• Sound to intermediate revenue & cash management

• Moderate financial flexibility

China LGFPs:

• Highly leveraged; liquidity shortages

• Challenging industry environments and/or broad policy mandates with ad hoc

projects;

• Benefited from government fiscal stimulus plans

• Of late, focused on improving financial management practices

• Support from the central government to refinance its existing obligations

Management quality - Indonesian Cities

Indonesian Cities:

• Relatively weak credit culture, mismatch between decentralization of

revenues and expenditures;

• Manual procedures, lack of qualified staff at local level;

• Procurement rules are onerous, capex execution rates remain low;

• Generally weak financial policy framework, no institutionalized debt, liquidity

or risk management practices;

• Management of local SOEs – from basic to adequate. PDAMs – often in

arrears;

• Reporting quality varies – many audits with qualifications.

But also:

• Overall still low direct debt levels and some reserves;

• Ongoing computerization & focus on program-based budgeting, KPIs;

• Fiscal guidelines are better defined now;

• Jakarta DKI and Surabaya City: among the stronger LGs in developing Asia; mix of

basic and sound practices in financial management

Management quality – Indonesian Cities

Moving forwardAt the national level:

• transparent borrowing frameworks for LGs/SOEs;

• educating investors, issuers and developing credit culture at all levels;

• developing credit benchmarks

• municipal funding vehicles for smaller LGs

At the subnational level:

• medium-term fiscal frameworks and visibility beyond political cycles

• improved transparency, financial discipline and debt management capacity

• clear link to capital investments/infrastructure projects

What's next?

• LGs/SOEs will borrow directly in the current environment => develop the

necessary prerequisites

• Later: engage capital markets and increase financial capacity at LG level to

implement more infrastructure projects

Copyright © 2015 by Standard & Poor’s Financial Services LLC. All rights reserved.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof (Content) may be modified,

reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of Standard & Poor’s

Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their

directors, officers, shareholders, employees or agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties

are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or

maintenance of any data input by the user. The Content is provided on an “as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES,

INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS,

SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT’S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE

OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or

consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in

connection with any use of the Content even if advised of the possibility of such damages.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. S&P’s

opinions, analyses and rating acknowledgment decisions (described below) are not recommendations to purchase, hold, or sell any securities or to make any investment decisions,

and do not address the suitability of any security. S&P assumes no obligation to update the Content following publication in any form or format. The Content should not be relied on

and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions.

S&P does not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable, S&P does not

perform an audit and undertakes no duty of due diligence or independent verification of any information it receives.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P reserves

the right to assign, withdraw or suspend such acknowledgement at any time and in its sole discretion. S&P Parties disclaim any duty whatsoever arising out of the assignment,

withdrawal or suspension of an acknowledgment as well as any liability for any damage alleged to have been suffered on account thereof.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain

business units of S&P may have information that is not available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain

non-public information received in connection with each analytical process.

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its

opinions and analyses. S&P's public ratings and analyses are made available on its Web sites, www.standardandpoors.com (free of charge), and www.ratingsdirect.com and

www.globalcreditportal.com (subscription), and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information about our

ratings fees is available at www.standardandpoors.com/usratingsfees.

STANDARD & POOR’S, S&P and RATINGSDIRECT are registered trademarks of Standard & Poor’s Financial Services LLC.