tax aspects of technology...

TRANSCRIPT

1

TAX ASPECTS OF TECHNOLOGY TRANSACTIONS

Roger RoyseRoyse Law Firm, PC

2600 El Camino Real, Suite 110

Palo Alto, CA [email protected]

www.rroyselaw.comwww.rogerroyse.comSkype: roger.royse

IRS Circular 230 Disclosure: To ensure compliance with the requirements imposed by the IRS, we inform you that any tax advice contained in this communication, including any attachment to this communication, is not intended or written to be used, and cannot be used, by any taxpayer for the purpose of (1) avoiding penalties under the Internal Revenue Code or (2) promoting, marketing or recommending to any other person any transaction or matter addressed herein.

BAYTLFebruary 2,

2011

2

TAX OBJECTIVES

Exploit Rate Differentials

Defer, Defer, Defer (Then Die)

Avoidance (Exemption or Non recognition)

3

OVERVIEW

1. Technology Transfers

2. Entity Formation

2. R&D Partnerships

3. IP Holding Companies

4. Foreign Structures

5. Litigation Recoveries

6. New Developments

4

SALE vs. LICENSE(15% vs. 35%)

Sale:• “All Substantial Rights”

• Capital gains

• No “Personal holding company income”

• Section 197 Amortization

License:• No transfer of “All Substantial Rights”

• Ordinary income

• Ordinary deduction

5

INCORPORATION / FORMATION ISSUES

StartUpCompany

Technology

Services

Cash

6

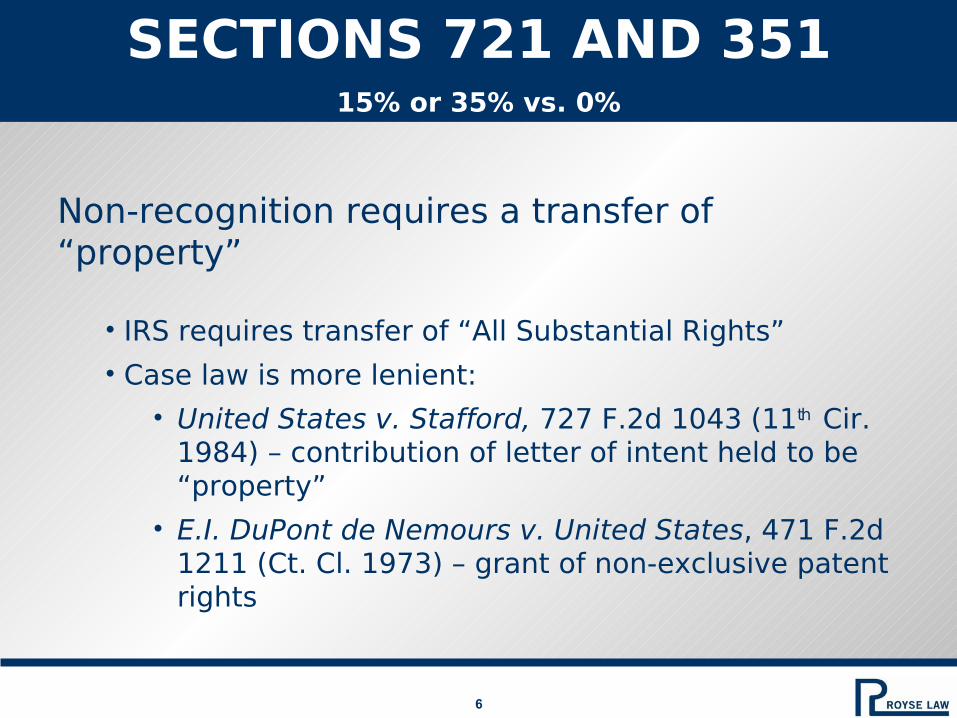

SECTIONS 721 AND 35115% or 35% vs. 0%

Non-recognition requires a transfer of “property”

• IRS requires transfer of “All Substantial Rights”

• Case law is more lenient:

• United States v. Stafford, 727 F.2d 1043 (11th Cir. 1984) – contribution of letter of intent held to be “property”

• E.I. DuPont de Nemours v. United States, 471 F.2d 1211 (Ct. Cl. 1973) – grant of non-exclusive patent rights

7

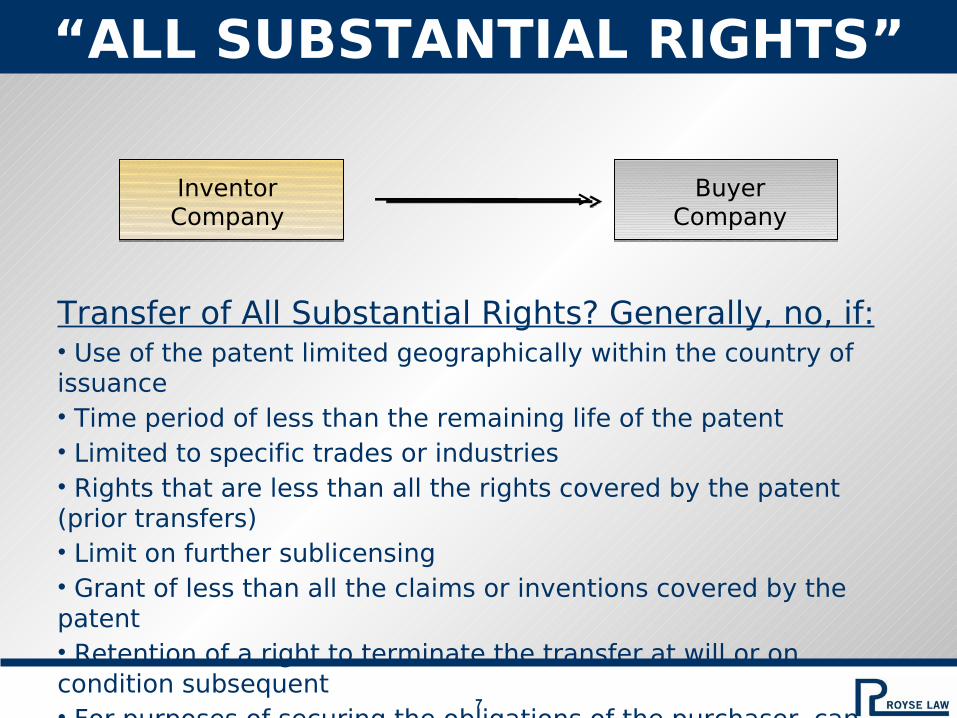

“ALL SUBSTANTIAL RIGHTS”

Transfer of All Substantial Rights? Generally, no, if:• Use of the patent limited geographically within the country of issuance• Time period of less than the remaining life of the patent• Limited to specific trades or industries• Rights that are less than all the rights covered by the patent (prior transfers)• Limit on further sublicensing• Grant of less than all the claims or inventions covered by the patent• Retention of a right to terminate the transfer at will or on condition subsequent• For purposes of securing the obligations of the purchaser, can (1) retain right to use the invention in the event of default and (2) hold the legal title to the patent

Inventor Company

Buyer Company

8

CAPITAL GAIN UNDER SECTION 1235

Allows patent “holder” to obtain long-term capital gains treatment regardless of holding period, the method of payment, and the status of the inventor as a professional; could potentially apply to trade secrets or other patentable know-how

Requirements• Available to “holders” – meaning either the individual who

(1) created the patent or (2) acquired an interest therein prior to reduction to practice; look-through for LLC ownership

• Must transfer “all substantial rights”

• “Patent” means a patent granted under domestic law, or any foreign patent granting rights generally similar to those under a United States patent; not necessary that patent or application be filed

• Not available in (1) transfers to “related parties” (25% threshold) or (2) “hired to invent” scenarios

9

TAX ISSUES – STARTUP, INC.

• Code Section 83– Option Grant– Sale for Partially

Recourse Note– Stock Grant

• Code Sections 351/721– Stock/Capital for

“Property”– License In

10

LLC PROFITS INTEREST

• Under Rev. Proc. 93-27, the receipt of a profits interest is generally not a taxable event for the partner or the partnership.

• A member has a capital interest if he or she has a share of unrealized appreciation in the partnership's assets.

• In Rev. Proc. 2001-43, the IRS stated that it would not tax the employee or the partnership on grant of a non-vested profits interest.

11

PARTNERSHIP EQUITY TRANSFERS FOR SERVICES

Proposed Regulations published May 24, 2005Rev. Proc. 2001-43 and Rev. Proc. 93-27 Will Be ObsoletedSection 83 Applies to Profits InterestSection 83(b) Election Required for Unvested Profits InterestPartnership Deduction in Year of Employee’s Income InclusionPartnership Recognizes No Income on Capital ShiftSafe Harbor ElectionForfeiture Allocations RequiredEffective When Finalized

12

TRADEMARKS

• Acquisition Costs– Expenses to develop

trademark must be capitalized

– No depreciable life– Section 195 (startup

costs) does not apply– Section 197 15 year

amortization– Contingent or periodic

payments deductible

• Income from Disposition– Receipt of amounts

contingent on productivity, use or disposition are non-capital

– Retention of any significant power, right or continuing interest (quality control) results in ordinary income

13

COPYRIGHT

• Costs– Most copyright costs must

be capitalized (no current deduction)

– Subject to depreciation– 195 Startup expenses– Inventory costs– Software may be

depreciated over 36 months

• Revenues– Capital Asset does not

include copyright held by person whose personal efforts created it or to whom it was assigned in a carryover basis transaction

– Personal efforts of corporation?

– Inventory– Software as franchise

14

PATENTS

• Deduction of R&D Expenses under 174

• Section 41 Credits

• Capitalize and Amortize

• 1235 Capital Gains– Available to Holders

• Inventor• Obtained an interest

in the invention before reduction to practice

15

TRADE SECRETS AND KNOW HOW

15

• Section 1235 applies to potentially patentable trade secrets

• Treatment as Property

• Transfer of all substantial rights– No retained rights to use

16

SOFTWARE: PATENT OR COPYRIGHT

• Copyright– Not Capital Asset

in hands of Creator

– One year capital gains holding period

• Patent– Sale by Holder

qualifies for capital gain transaction

– 1235 instant capital gains

17

SOFTWARE

• Right to copy

• Transfer other than right to copy

• Produced for purchaser

• Transfer of copyright right – sale or royalty

• Sale or rent

• Services

18

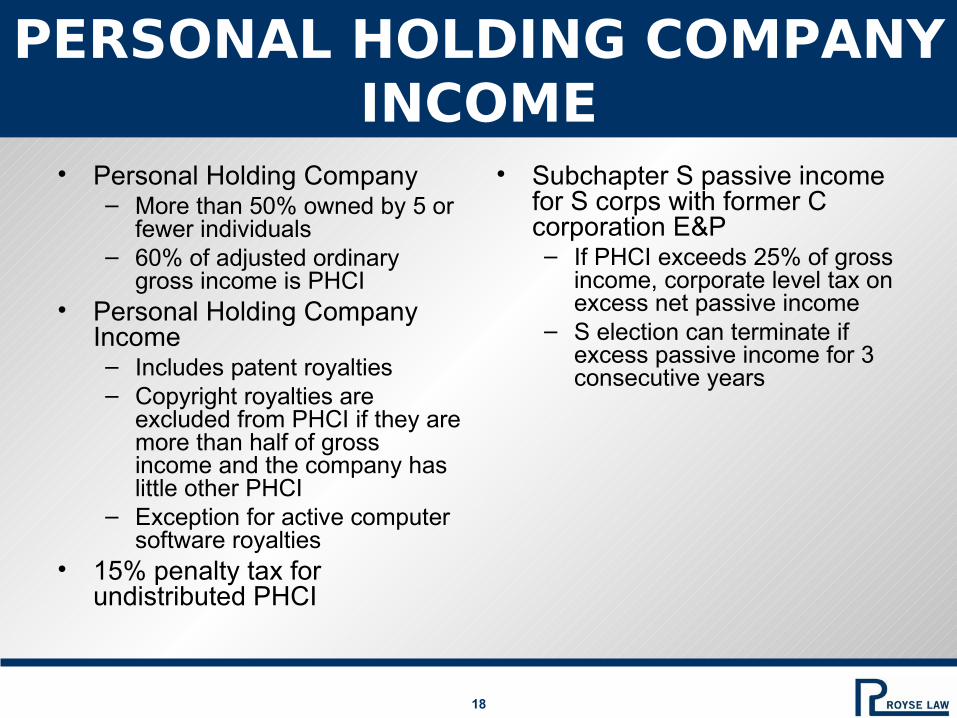

PERSONAL HOLDING COMPANY INCOME

• Personal Holding Company – More than 50% owned by 5 or

fewer individuals– 60% of adjusted ordinary

gross income is PHCI• Personal Holding Company

Income – Includes patent royalties– Copyright royalties are

excluded from PHCI if they are more than half of gross income and the company has little other PHCI

– Exception for active computer software royalties

• 15% penalty tax for undistributed PHCI

• Subchapter S passive income for S corps with former C corporation E&P– If PHCI exceeds 25% of gross

income, corporate level tax on excess net passive income

– S election can terminate if excess passive income for 3 consecutive years

19

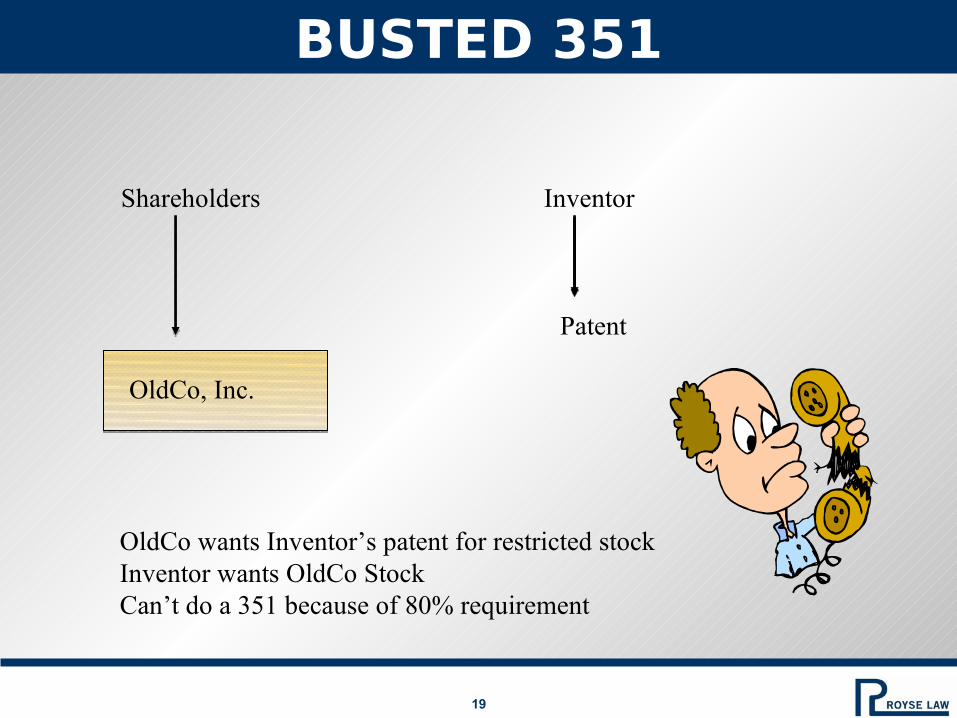

BUSTED 351

Shareholders Inventor

Patent

OldCo wants Inventor’s patent for restricted stockInventor wants OldCo StockCan’t do a 351 because of 80% requirement

OldCo, Inc.

20

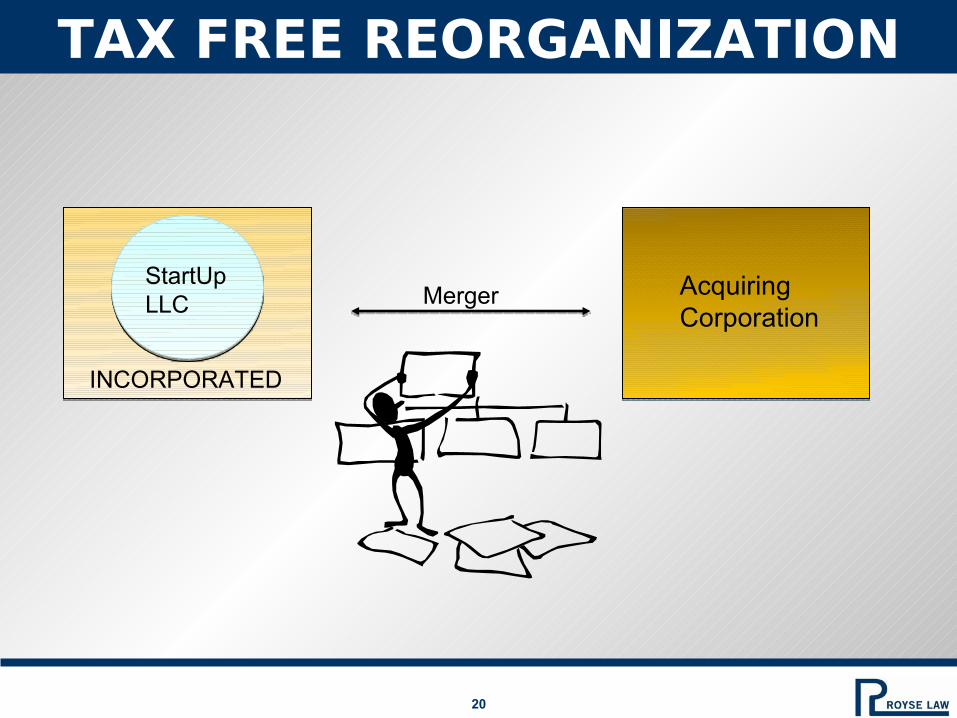

TAX FREE REORGANIZATION

MergerStartUpLLC

INCORPORATED

AcquiringCorporation

21

TAX ISSUES – STARTUP, INC.

Shareholders Inventor

PatentStock

Merger

OldCoStock

Step Transaction - saleContinuity of Business

OldCo, Inc.

NewCo, Inc.

22

WITHHOLDING

• 30% on US Source royalties

• Lower Treaty Rates

• Characterization of payment

• Fees or Royalty

• 1.861-18 Software Regulations

1.861-18 Regulations

• Computer programs

• Sales

• Licenses

• Leases

• Services

• Know-how

23

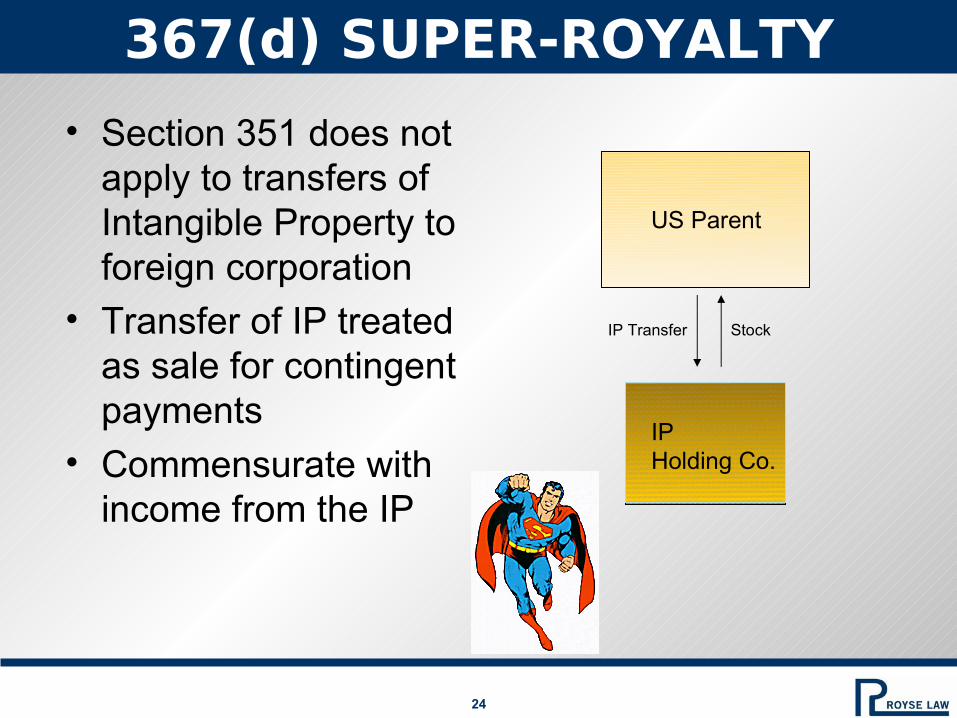

24

367(d) SUPER-ROYALTY

• Section 351 does not apply to transfers of Intangible Property to foreign corporation

• Transfer of IP treated as sale for contingent payments

• Commensurate with income from the IP

IP Transfer Stock

US Parent

IPHolding Co.

25

TRANSFER PRICING

• Under Code section 482, the IRS can re-allocate income among "controlled" entities to properly reflect income.

• The prices charged between related parties (“transfer prices”) are required to be arm's length prices.

• Substantial penalties for understatements of US tax due to transfer pricing adjustments – 20% or 40% of the underpaid taxes, depending on the size of the understatement.

• Penalty may be avoided if taxpayer has adequate documentation supporting its transfer prices (i.e. a transfer price study)

26

COST SHARING

Buy InPayment

OwnershipOf Intangibles

Split ownership ofIntangibles

Share costs and exploitation rights

No Intercompany Royalty

Can migrate intangibles to Low tax country

Current Problems:

NonexclusiveTechnology reverts on termination Capital

TechnologyDistribution Network

Foreign OperationsCompany

USCompany

27

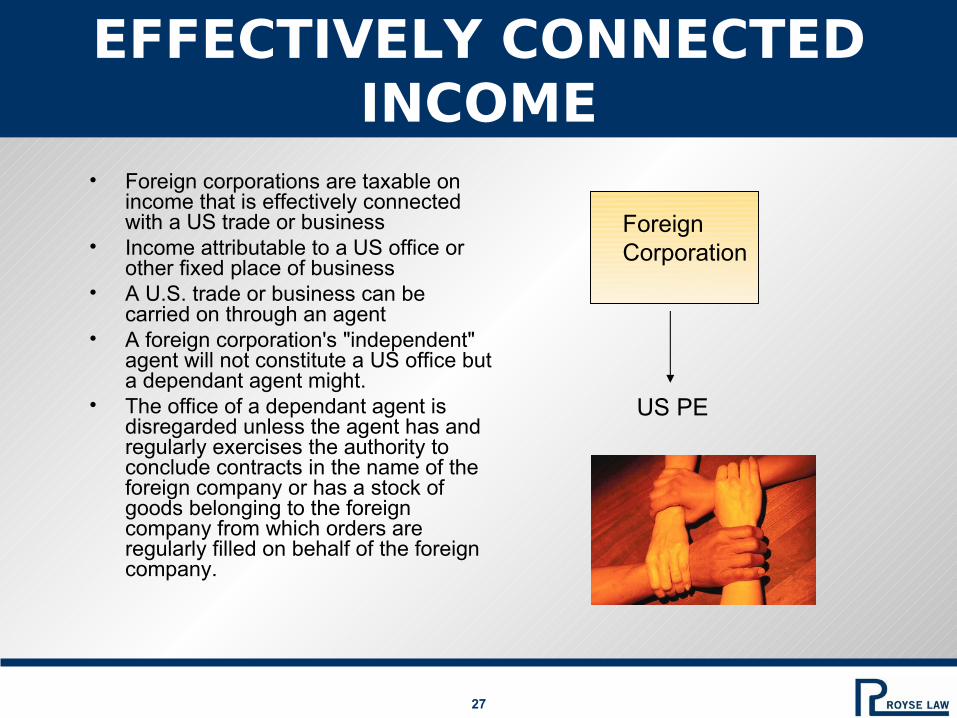

EFFECTIVELY CONNECTED INCOME

• Foreign corporations are taxable on income that is effectively connected with a US trade or business

• Income attributable to a US office or other fixed place of business

• A U.S. trade or business can be carried on through an agent

• A foreign corporation's "independent" agent will not constitute a US office but a dependant agent might.

• The office of a dependant agent is disregarded unless the agent has and regularly exercises the authority to conclude contracts in the name of the foreign company or has a stock of goods belonging to the foreign company from which orders are regularly filled on behalf of the foreign company.

US PE

ForeignCorporation

28

SUBPART F

• US shareholder of CFC is taxed directly on pro rata share of CFC's Subpart F income.

• Foreign corporation is CFC if more than 50% of its stock, by vote or value, is held by U.S. shareholders at any time during the year.

29

PASSIVE FOREIGN INVESTMENT COMPANIES (PFIC)

• Income Test: 75% of gross income is passive• Asset Test: 50% of assets produce passive

income• Interest charge on "excess distributions" from

PFICs • QEF Election

30

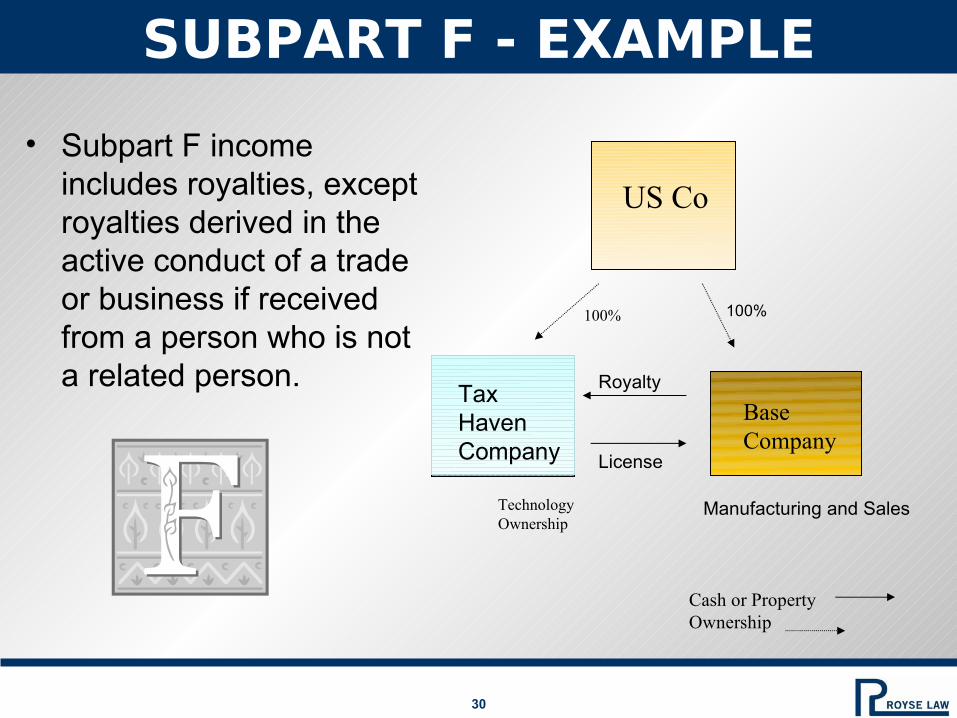

SUBPART F - EXAMPLE

US Co

Base Company

Cash or PropertyOwnership

100%

TechnologyOwnership

TaxHavenCompany

100%

Royalty

License

Manufacturing and Sales

• Subpart F income includes royalties, except royalties derived in the active conduct of a trade or business if received from a person who is not a related person.

31

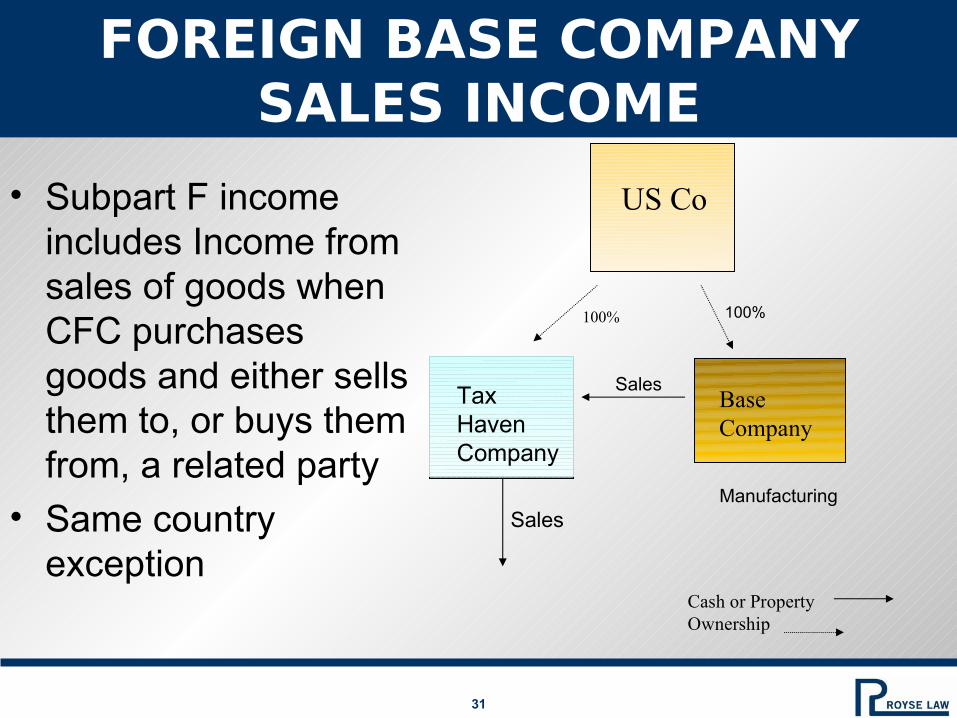

FOREIGN BASE COMPANY SALES INCOME

US Co

Base Company

Cash or PropertyOwnership

100%

TaxHavenCompany

100%

Sales

ManufacturingSales

• Subpart F income includes Income from sales of goods when CFC purchases goods and either sells them to, or buys them from, a related party

• Same country exception

32

BRANCH RULE

• Subpart F Income includes sales income if a related person is the seller or buyer

• Exception for income from sales of goods manufactured or produced by the CFC

• Manufacturing branches treated as separate corporations if located outside the country of incorporation, and the effective rate of tax on non-branch income is less than the lesser of (i) 90% of rate of country of manufacturing, or (ii) a rate 5 percentage points below country of manufacture rate.

US Co

100%

TaxHavenCompany

Manufacturing Branch

Sales Branch

33

CONTRACT MANUFACTURER STRUCTURE

US Co

ContractManufacturing

[PRC]ManufacturerLocal

Distributors

Products

US Sales

Service Fees

Cash or PropertyOwnership

100%Contract R&DService Fees

FounderPreferredShareholder

Optionees

TechnologyOwnership

TaxHavenCompany

Ashland Oil v. CIR

Vetco Inc. v. CIR

Rev. Rul. 97-48

Contract Manufacturer is not a branch

Are activities of contract manufacturer attributed to tax haven company?

34

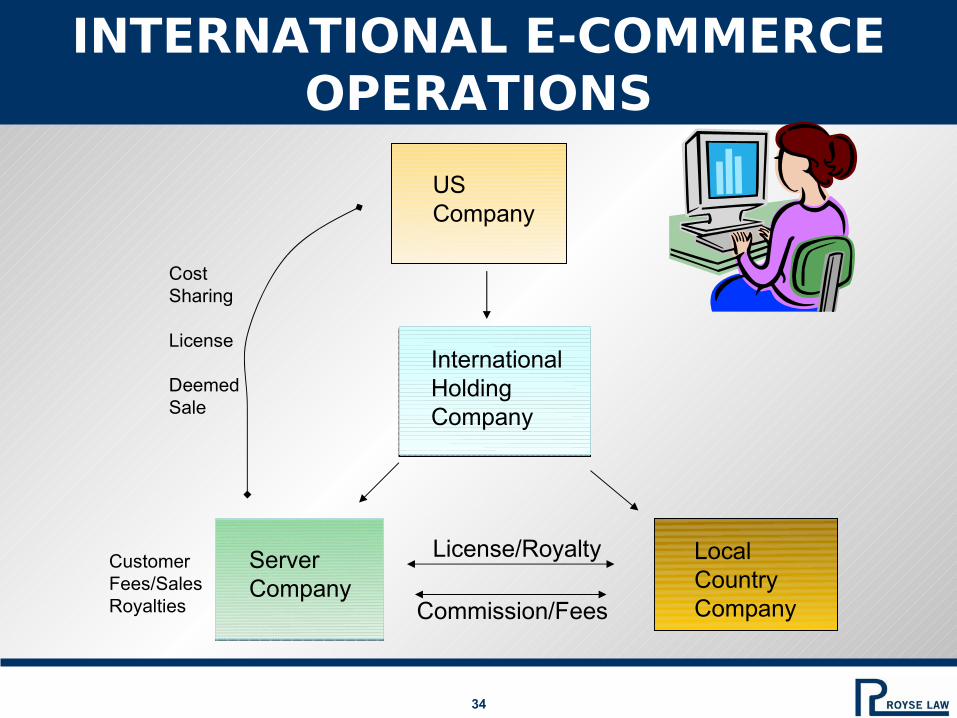

INTERNATIONAL E-COMMERCE OPERATIONS

USCompany

InternationalHoldingCompany

ServerCompany

LocalCountryCompany

License/Royalty

Commission/Fees

CustomerFees/SalesRoyalties

CostSharing

License

DeemedSale

35

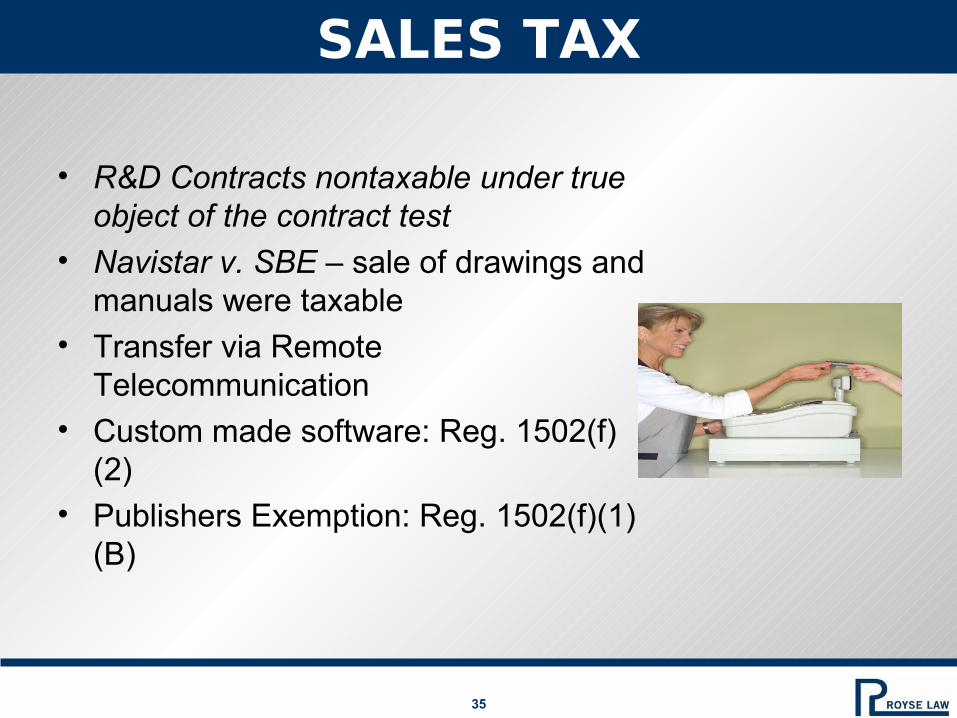

SALES TAX

• R&D Contracts nontaxable under true object of the contract test

• Navistar v. SBE – sale of drawings and manuals were taxable

• Transfer via Remote Telecommunication

• Custom made software: Reg. 1502(f)(2)

• Publishers Exemption: Reg. 1502(f)(1)(B)

36

STATE TAX ISSUES

CaliforniaParent

Nevada IPHolding Co.

IP Transfer LicenseBack

Services Income

EmployeesAdmin, legal and commercialRegistrations, enforcementR&D, commercialization

37

ASSOCIATED PATENTEES CHARACTER CONVERTER

R&D Partnershi

p

“Sale” of Patent

Contingent Payments

Developer Corporatio

n

Associated Patentees, Inc.: current deduction for payments based on patent’s use or production

38

R&D PARTNERSHIPS

• LDL Research & Development II, Ltd.– Partnership had no real prospect of exploiting technology– Developer relied on to conduct technology business– Only possibility that partnership would ever act

• Kantor v. CIR– Partnership must have realistic possibility of entering its own

business– Prospect of entering business must be shown at time of

expenditure– Option to acquire exclusive rights for nominal sum– Lack of Capability to enter business

• Scoggins v. CIR– Developer had significant cost option to acquire IP– Partnership was capable of developing business if developer

did not

39

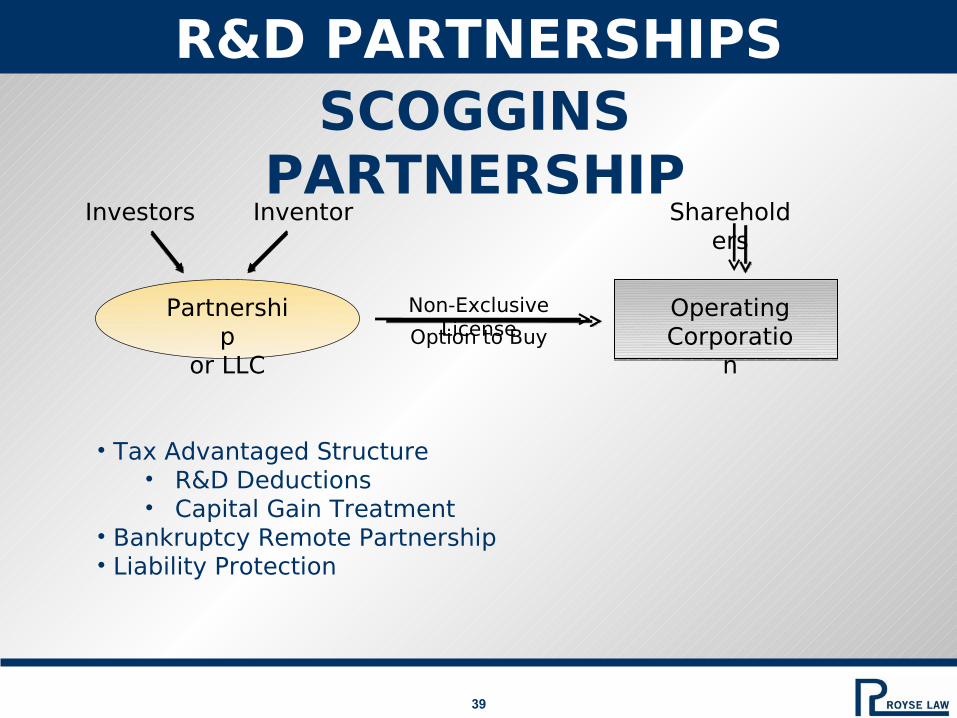

R&D PARTNERSHIPSSCOGGINS

PARTNERSHIP

Partnership

or LLC

Investors Inventor

Option to Buy

Non-Exclusive License

Shareholders

Operating Corporatio

n

• Tax Advantaged Structure • R&D Deductions• Capital Gain Treatment

• Bankruptcy Remote Partnership• Liability Protection

40

IP HOLDING COMPANY STRUCTURES

OptioneesFounder

PreferredShareholder

FOREIGN COMPANY HOLDS IP

US Sales US Compan

y

100% Contract R&DService Fees

LocalDistributors Products

Tax HavenCompany

w/ Technology

Service Fees

ContractManufacturing

[PRC]Manufacturer

41

IP HOLDING COMPANY STRUCTURES

US Sales

US Company

Contract R&DProduct sales

Tax Haven

Technology License

100%

Products

Service Fees

ContractManufacturing(or License)

Manufacturer

100%Local

Distributors

Local Sales

DOMESTIC COMPANY HOLDS IP

42

Litigation Recoveries

Payor – deduction vs. capitalizedRecipient – ordinary vs. cap gains vs. capital recovery

Origin of the Claim Test

State Tax issues related to venue

43

CLIENT PARTNERSHIP WITH ATTORNEY

Inventor

Attorney

Infringement Claims

Legal Services

Patent Infringement

LLC

Litigation Proceeds Defendan

t

• Generally, legal expense deduction limited by (1) 2% floor on AGI, (2) alternative minimum tax and (3) itemized deduction phase out

• Structuring the relationship as a client-attorney partnership may eliminate the client’s tax on the portion paid to the attorney; in a partnership, the client’s gross income will not include legal expenses

• Can be useful in prosecution of patent infringement claims

44

CLIENT PARTNERSHIP WITH ATTORNEY

Partnership Formalities• An Agreement;• Conduct of the parties in execution of its provisions;• Statements of the parties;• Testimony of disinterested persons;• Relationship of the parties;• Respective abilities and capital contributions of the parties;• Actual control of income and purposes for which it is used; and• Other facts showing the true intent of the parties (file partnership

return).

Other Issues• Federal tax law determines existence of partnership (not State)• State rules of professional conduct (conflicts, partnership with

non-attorney)• Control of the case

45

Section 409A Issue

Section 409A Issue• IP transfer distinguished from services agreement -

Boulez v. Comr., 83 T.C. 584 (1984).

• Ownership rights are essential in a transfer of IP.

46

NEW DEVELOPMENTS

2010 Small Business Jobs Act• September 27, 2010, President Obama signed into

law the Small Business Jobs Act of 2010.

• The Act doubled the Section 179 immediate deduction for certain new property placed in service during 2010 and 2011.

• The Act provides for 50% bonus depreciation on new MACRS property with a recovery period of 20 years or less (and certain computer software) placed into service in 2010.

• The Act increased the capital gain exclusion to 100% on the sale of qualified small business stock acquired between Sept. 27 and the end of 2010.

47

NEW DEVELOPMENTS

2010 Tax Extender Bill• December 17, 2010, President Obama signed into

law the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act of 2010

• The Act reduced the Section 179 immediate deduction for certain new property placed in service during 2012 and subsequent years.

• The Act provides for 100% bonus depreciation on new MACRS property with a recovery period of 20 years or less (and certain computer software) placed into service in the end of 2010 and through 2011, which rate goes back down to 50% for 2012.

• The Act extended the capital gain exclusion to 100% on the sale of qualified small business stock acquired during 2011.

• The Act extended the Research Credit through 2011.

• The Act extends many energy related provisions through 2011.

48

NEW DEVELOPMENTS

IRS – Uncertain Tax Positions• December 17, 2010, the IRS released final

regulations (T.D. 9510) that allow the IRS to require that certain taxpayers file a schedule disclosing “uncertain tax positions” with their tax returns.

• The filing requirement will apply to taxpayers based on their asset values, as follows: 2010 – larger taxpayers (assets in excess of $100 M); 2012 – medium taxpayers (assets in excess of $50 MM); 2014 – smaller taxpayers (assets in excess of $10 MM).

• The IRS disclosure requirement is similar to the disclosure requirement under Financial Accounting Standards (FIN 48).

• Disclosures will be detailed, and will contain – (i) ranking of size of uncertain positions, (ii) the Code section(s) implicated, (iii) the years applicable, and (iv) statements about the income, gain, loss, timing, valuation, and basis relevant to the uncertain position.

49

NEW DEVELOPMENTS

Codification of Economic Substance Doctrine

• Codified as a part of the Health Care and Education Reconciliation Act (P.L. 111-152), signed March 30, 2010.

• Immediately effective.

• Clarifies doctrine’s requirements that –

(1) the transaction changes in a meaningful way (apart from Federal income tax effects) the taxpayer's economic position, and

(2) the taxpayer has a substantial purpose (apart from Federal income tax effects) for entering into such transaction.

• Not meant to change circumstances in which doctrine is applied.

• 40% strict liability penalty.

50

www.rroyselaw.com

PALO ALTO2600 El Camino Real Suite 110Palo Alto, CA 94306

SAN JOSE10 Almaden Blvd.Suite 1250San Jose, CA 95113

LOS ANGELES10900 Wilshire Blvd.Suite 300Los Angeles, CA 90024

SAN FRANCISCO155 Sansome StreetSuite 500San Francisco, CA 94104