tax planning for the real estate … planning for re prof - 2013.pdf2013’s list of celebrity tax...

TRANSCRIPT

NOVEMBER 21, 20131

TAX PLANNINGFOR THE

REAL ESTATE PROFESSIONAL

2

INTRODUCTION

THANKS TO

3

INTRODUCTION

TIMOTHY W. NELSON, CPA, CVA, CFEREID H. RIKER, CPA, MAcc

• “Financial Translators”• Accountants with personality

4

INTRODUCTION

DISCLAIMER(the “neighbor” clause)

Much of what we will discuss is generic in nature andintended to be an overview of these issues. While wewill address all questions, some answers are extremelyspecific to your facts and circumstances and may requirethe gathering of additional information or furtherexplanation on our part.

5

INTRODUCTION

Before we start, let’s feel a little bit better about

ourselves…

6

INTRODUCTION

2013’s List of Celebrity Tax Offenders

7

INTRODUCTION

IN THIRD PLACE

Beyonce’s dad Mathew Knowles - $1.2 million in taxes and penalties for failing to pay on

income in 2010 and 2011. Who knew you had to pay taxes on income you made managing

your daughter’s career?

8

INTRODUCTION

IN SECOND PLACE

Singer-Songwriter Mary J. Blige received a tax lien for $3.4 million of taxes and penalties for failing to pay on income in 2009, 2010 and

2011 – this does not include the $900k she owes to New Jersey! Rest assured – she says

her “team” is working on it!

9

INTRODUCTION

IN FIRST PLACE

Beanie Babies founder Ty Warner – assessed a $53 million PENALTY for his Swiss bank account. Oh, by the way, this was for not reporting the account

or the earnings, which were only $3 million!

10

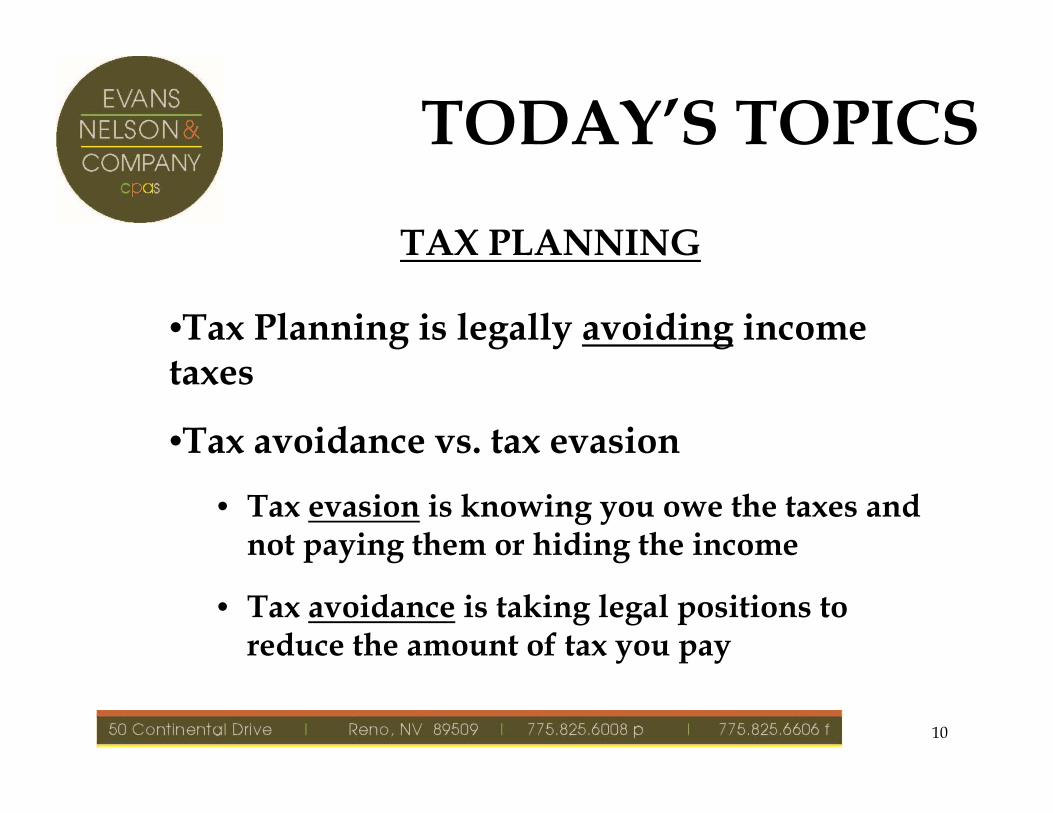

TODAY’S TOPICS

TAX PLANNING

•Tax Planning is legally avoiding income taxes

•Tax avoidance vs. tax evasion

• Tax evasion is knowing you owe the taxes and not paying them or hiding the income

• Tax avoidance is taking legal positions to reduce the amount of tax you pay

11

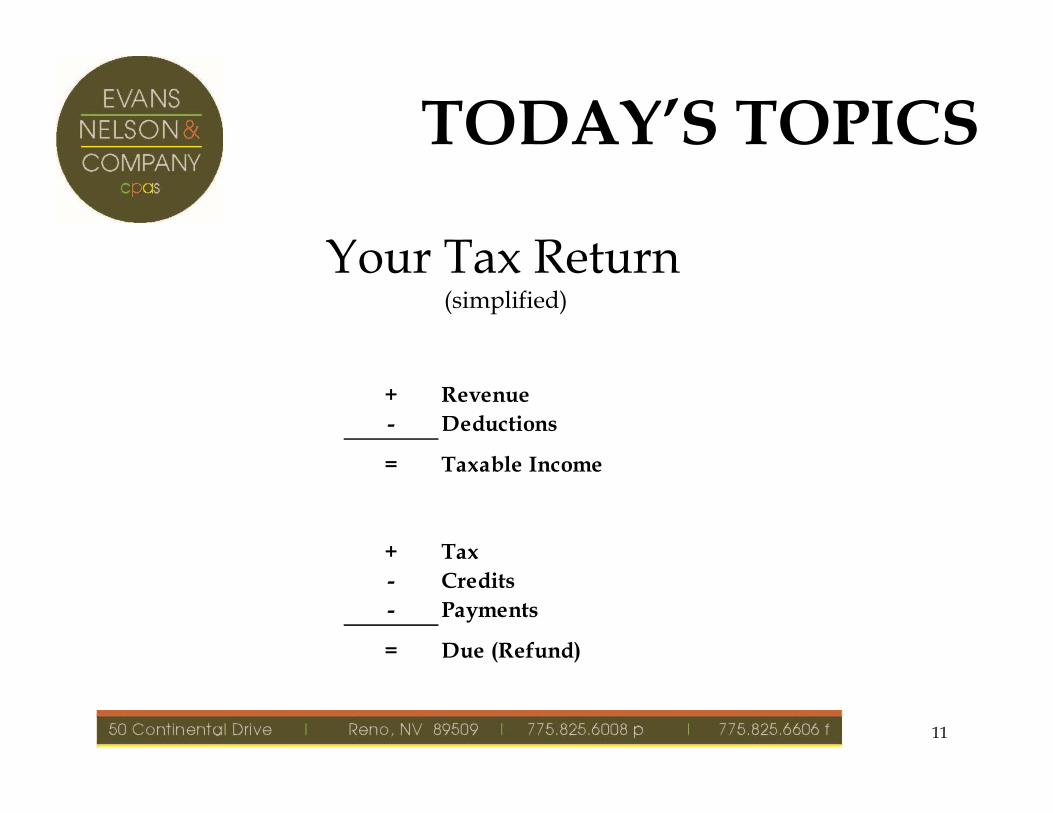

TODAY’S TOPICS

+ Revenue- Deductions

= Taxable Income

+ Tax- Credits- Payments

= Due (Refund)

Your Tax Return(simplified)

12

TODAY’S TOPICS

How to Reduce Taxes?+ Revenue Decrease Revenue

- Deductions Increase Deductions

= Taxable Income

+ Tax Decrease Taxes

- Credits Increase Credits

- Payments

= Due (Refund) Or Pay More!!!!

13

DECREASING REVENUE

14

DECREASING REV

How to Reduce Taxes?+ Revenue Decrease Revenue

- Deductions Increase Deductions

= Taxable Income

+ Tax Decrease Taxes

- Credits Increase Credits

- Payments

= Due (Refund) Or Pay More!!!!

15

DECREASING REV.

Realtors are usually cash basis taxpayers(If you didn’t get it, you don’t pay tax on it)

Presumes a relatively level taxable income from year to year

2013 2014

Receive Dec 31 Receive Jan 2

Pay by April 2014 Pay by April 2015

16

DECREASING REV.

If you are having a great year and want to decrease your taxes, delay receipt of

income/revenue until 2014 (if possible)

17

INCREASING EXPENSES

18

INCREASING EXP.

+ Revenue Decrease Revenue

- Deductions Increase Deductions

= Taxable Income

+ Tax Decrease Taxes

- Credits Increase Credits

- Payments

= Due (Refund) Or Pay More!!!!

19

INCREASING EXP.

Don’t spend a $1.00 to save $0.40!!

Presumes highest individual tax rate. Lower tax rates are even more important!

SpendDon't Spend

Expense ($1.000) $0.000Tax Savings $0.396 ($0.396)

Net Economic Result ($0.604) ($0.396)

If an "unnecessary" expense, you are 20.8 cents better off by NOT spending the $1 and

paying the tax!

20

INCREASING EXP.

GOAL: Find ways to deduct items that you are

already buying, or spend money on productive goods and services

21

WHAT IS DEDUCTIBLE?

Under IRC § 162(a), generally ANY expense can be deducted if it meets certain tests, as follows:

•Incurred in connection with your business

•Ordinary

•Necessary, and

•Reasonable

22

WHAT IS DEDUCTIBLE?

What is an “Ordinary” expense?

•Common and accepted in your business

What is a “Necessary” expense?

•Helpful and appropriate for your business

What is a “Reasonable” amount?

•Determined based on circumstances

23

WHAT IS DEDUCTED?

•Outside Services/Wages

•Auto & Travel

•Rents & Desk Fees

•Retirement Contributions

•Advertising & Promotion

•Dues, Memberships

•Telephone/Internet

•Continuing Education

•Meals & Entertainment

•Gifts & open-house expenses

Major Deductions

24

LOWER YOUR TAXES

25

LOWER TAXES+ Revenue Decrease Revenue

- Deductions Increase Deductions

= Taxable Income

+ Tax Decrease Taxes

- Credits Increase Credits

- Payments

= Due (Refund) Or Pay More!!!!

26

LOWER TAXES

Basic Income Tax Types

• Income Tax• Self-Employment Tax• Medicare Tax (new 3.8%)• Pension “Penalties”

27

LOWER TAXES

Income Tax

• Tax on your income after all available deductions

28

LOWER TAXES

2013 FEDERAL INCOME TAX RATES/BRACKETS

TAXABLE INCOME

Rate Single Married JointHead of

Household

10% 8,925 17,850 12,750 15% 36,250 72,500 48,600 25% 87,850 146,400 125,450 28% 183,250 223,050 203,150 33% 398,350 398,350 398,350 35% 400,000 450,000 425,000

39.6% 400,001+ 450,001+ 425,001+

29

LOWER TAXES

Y1 Y2 Y3 Y4 Y5 Y6 AVGTaxable Income

Joe 200,000 50,000 200,000 50,000 200,000 50,000 125,000 Sally 125,000 125,000 125,000 125,000 125,000 125,000 125,000

Marginal Tax RateJoe 28% 15% 28% 15% 28% 15%

Sally 25% 25% 25% 25% 25% 25%

‐

50,000

100,000

150,000

200,000

250,000

Y1 Y2 Y3 Y4 Y5 Y6

Tax Rate/Effect

30

LOWER TAXES

Self Employment Taxes

• Tax on your self-employment earnings• Basically Social Security and Medicare• Social Security capped ($113,700 in 2013, $117,000 in 2014)

31

LOWER TAXES

ENTITY TYPE

(sole proprietor, LLC, S-Corp)

can have a HUGE impact on Self-Employment Tax

32

LOWER TAXESSELF EMPLOYMENT TAX

BASIC EXAMPLE

Sole Proprietor S-Corp

Total Earnings $200,000 $200,000

Net compensation to proprietor 200,000 N/ASalary paid via W-2 N/A 100,000 Return on investment N/A 100,000

Income Tax (MFJ rates) 42,743 42,743 Payroll / Self-Employment Tax 28,259 14,130

Total Tax Paid $71,002 $56,873

Savings from S-Corp structure $14,130

Assumes MFJ tax rates and no other income or expenses

33

ENTITY CHOICE

Deciding whether to be a sole proprietor, LLC, S/C - Corporation can impact:

•Regular and self-employment taxes paid

•Taking profits out of the business (draws)

•Personal liability

•AUDIT rate

34

LOWER TAXES

3.8% MEDICARE TAX

35

3.8% MEDICARE TAX

• In March 2010, Congress passed the Patient Protections and Affordable Care Act

• It included a new provision for a 3.8% tax on income from interest, dividends, rents & royalties and other “unearned” income excluding active S corporation or partnership income (called the NIIT or net investment income tax)

• It applies to persons making AGI over $200k single or $250k married

• It went into effect on January 1, 2013

36

3.8% MEDICARE TAX

• Only applies on amounts OVER the $200k/$250k

• If this applies, you should have been including in your estimated tax payments for this year

• Your clients should know it applies to their rentals

• VERY important to watch your AGI – keep under the limit if possible

37

3.8% MEDICARE TAXEXAMPLE

NIIT Example

Wages 200,000$ Interest 20,000 Rentals 40,000

AGI 260,000 Threshold (MFJ) (250,000)

Amt subject to NIIT 10,000

NIIT rate 3.80%

Additional tax this year 380$

38

TAX RATE COMPARISON

MAXIMUM TAX RATESYear Over Year Comparison

2012 2013 2014

On income over 388,350 450,000 454,500

Federal 35.0% 39.6% 39.6%NIIT (Medicare) 0.0% 3.8% 3.8%

Total Federal 35.0% 43.4% 43.4%

CA ($1 mm) 10.3% 13.3% 13.3%

Total Income Tax Rate 45.3% 56.7% 56.7%

39

TAX TOPICS AFFECTING REALTORS ®

40

TAX TOPICS

Here are several items affecting Realtors® :

•Nevada Division of Real Estate (NDRE)

TAX PLANNING, DONE PROPERLY, CAN SAVE

THOUSANDS OF $$$

41

QUESTIONS??

42

THANK YOU

43