the 2019 ey homebuilder tax director roundtable methods... · the 2019 ey homebuilder tax director...

TRANSCRIPT

The 2019 EY Homebuilder Tax Director Roundtable

Accounting methods

6 May 2019

The 2019 EY Homebuilder Tax Director Roundtable | 6 May 2019 | Four Seasons Hotel Las Vegas

Disclaimer

Page 2

► EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US.

► This presentation is © 2019 Ernst & Young LLP. All rights reserved. No part of this document may be reproduced, transmitted or otherwise distributed in any form or by any means, electronic or mechanical, including by photocopying, facsimile transmission, recording, rekeying, or using any information storage and retrieval system, without written permission from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material herein is prohibited and is in violation of US and international law. Ernst & Young LLP expressly disclaims any liability in connection with use of this presentation or its contents by any third party.

► Views expressed in this presentation are those of the speakers and do not necessarily represent the views of Ernst & Young LLP.

► This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any taxpayer because it does not take into account any specific taxpayer’s facts and circumstances.

► These slides are for educational purposes only and are not intended, and should not be relied upon, as accounting advice.

► Neither EY nor any member firm thereof shall bear any responsibility whatsoever for the content, accuracy, or security of any third-party websites that are linked (by way of hyperlink or otherwise) in this presentation.

The 2019 EY Homebuilder Tax Director Roundtable | 6 May 2019 | Four Seasons Hotel Las VegasThe 2019 EY Homebuilder Tax Director Roundtable | 6 May 2019 | Four Seasons Hotel Las Vegas

Accounting methods

McRae ThompsonErnst & Young LLP

Susan GraisErnst & Young LLP

Dan PenrithErnst & Young LLP

Page 3

The 2019 EY Homebuilder Tax Director Roundtable | 6 May 2019 | Four Seasons Hotel Las Vegas

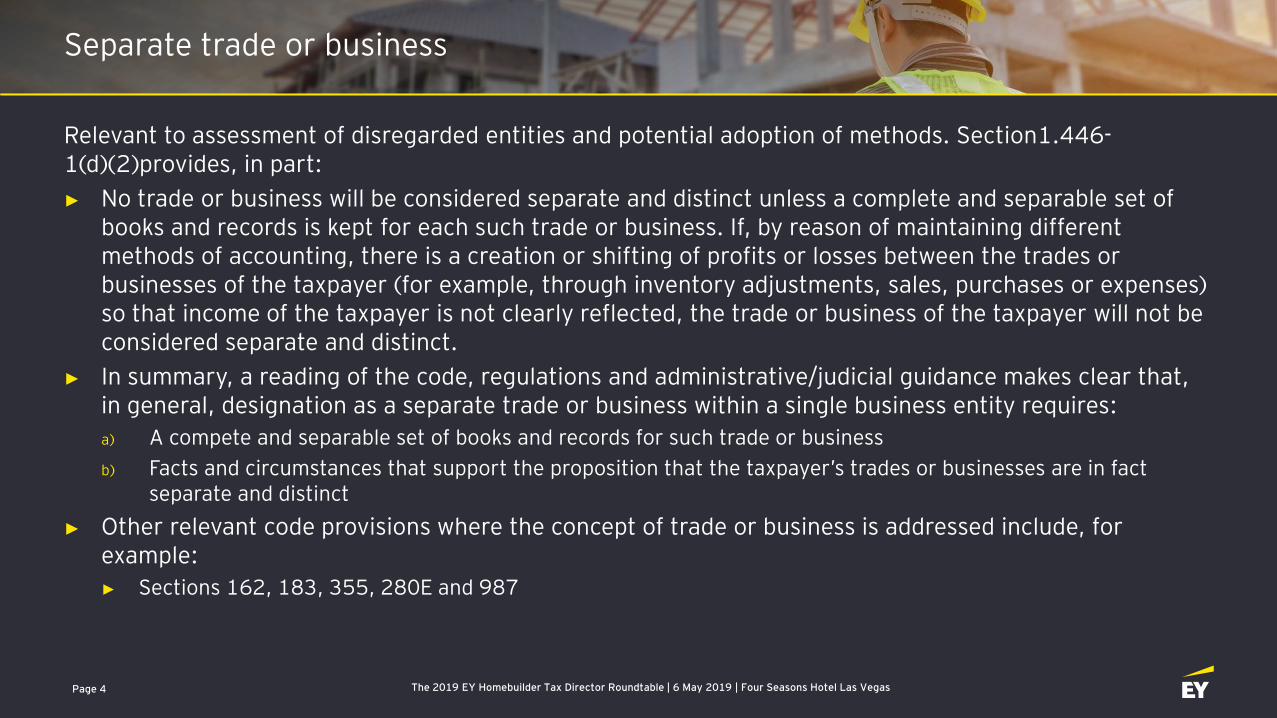

Separate trade or business

Relevant to assessment of disregarded entities and potential adoption of methods. Section1.446-1(d)(2)provides, in part: ► No trade or business will be considered separate and distinct unless a complete and separable set of

books and records is kept for each such trade or business. If, by reason of maintaining different methods of accounting, there is a creation or shifting of profits or losses between the trades or businesses of the taxpayer (for example, through inventory adjustments, sales, purchases or expenses) so that income of the taxpayer is not clearly reflected, the trade or business of the taxpayer will not be considered separate and distinct.

► In summary, a reading of the code, regulations and administrative/judicial guidance makes clear that, in general, designation as a separate trade or business within a single business entity requires:a) A compete and separable set of books and records for such trade or businessb) Facts and circumstances that support the proposition that the taxpayer’s trades or businesses are in fact

separate and distinct► Other relevant code provisions where the concept of trade or business is addressed include, for

example: ► Sections 162, 183, 355, 280E and 987

Page 4

The 2019 EY Homebuilder Tax Director Roundtable | 6 May 2019 | Four Seasons Hotel Las Vegas

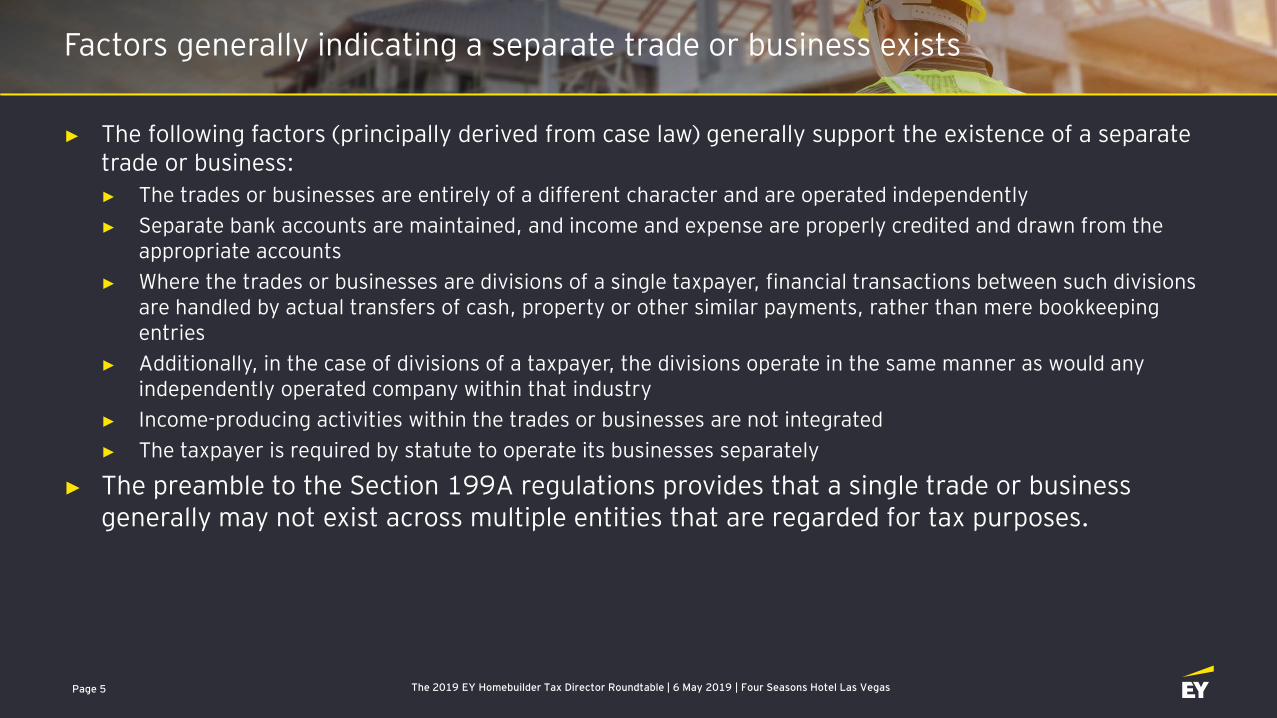

Factors generally indicating a separate trade or business exists

► The following factors (principally derived from case law) generally support the existence of a separate trade or business:► The trades or businesses are entirely of a different character and are operated independently► Separate bank accounts are maintained, and income and expense are properly credited and drawn from the

appropriate accounts► Where the trades or businesses are divisions of a single taxpayer, financial transactions between such divisions

are handled by actual transfers of cash, property or other similar payments, rather than mere bookkeeping entries

► Additionally, in the case of divisions of a taxpayer, the divisions operate in the same manner as would any independently operated company within that industry

► Income-producing activities within the trades or businesses are not integrated► The taxpayer is required by statute to operate its businesses separately

► The preamble to the Section 199A regulations provides that a single trade or business generally may not exist across multiple entities that are regarded for tax purposes.

Page 5

The 2019 EY Homebuilder Tax Director Roundtable | 6 May 2019 | Four Seasons Hotel Las Vegas

Factors generally indicating a separate trade or business exists

► The following factors (based on case law) generally do not support the existence of a separate trade or business:► Use of different accounting methods for each trade or business creates a shifting of profits or losses► A single general ledger is maintained for all the trade or businesses► A single bank account is maintained for all the trades or businesses► Common management and employees► Significant sharing of entity costs among the businesses

And/or► The different lines of business function as a well-integrated department, rather than separate,

autonomous businesses

Page 6

The 2019 EY Homebuilder Tax Director Roundtable | 6 May 2019 | Four Seasons Hotel Las Vegas

IRS update

► Large Business and International (LB&I)► IRS national office

Page 7

The 2019 EY Homebuilder Tax Director Roundtable | 6 May 2019 | Four Seasons Hotel Las Vegas

Final 'negative’ Section 263A regulations and automatic accounting method changes

► The final regulations apply for tax years beginning on or after November 20, 2018 (e.g., calendar year 2019)► For tax years that both begin before and end after November 20, 2018 (e.g., calendar year 2018),

the IRS will not challenge tax positions consistent with the final regulations► New treatment of negative adjustments

► Costs capitalized for book purposes but not permitted or required to be capitalized for tax purposes, such as book/tax differences, Section 174 costs, sales and marketing, distribution, etc.

► New modified simplified production method, which will be favorable for many taxpayers —may want to early adopt for 2018

► New definition of Section 471 costs► Costs capitalized for financial reporting purposes, but must include all direct costs► De minimis rules and safe harbor

► New automatic accounting method changes, including a change to revoke a historic absorption ratio (HAR) election

Page 8

The 2019 EY Homebuilder Tax Director Roundtable | 6 May 2019 | Four Seasons Hotel Las Vegas

Treatment of negative adjustments

► Large taxpayers using simplified production method (SPM) are generally prohibited from classifying negative adjustments as additional Section 263A costs.

► Negative adjustments permitted as additional Section 263A costs only for:► Taxpayers using modified simplified production method (MSPM)► Taxpayers using simplified resale method (SRM)► Small taxpayers using SPM► Certain nondeductible expenses (including bribes, lobbying expenses, and fines and penalties) may

not be treated as negative adjustments, regardless of method.► Examples of common negative adjustments include:

► Section 174 costs and certain distribution costs► Unfavorable book/tax differences related to various production expenses capitalized for book

purposes, such as plant equipment depreciation or bonus expenses for plant employees

Page 9

The 2019 EY Homebuilder Tax Director Roundtable | 6 May 2019 | Four Seasons Hotel Las Vegas

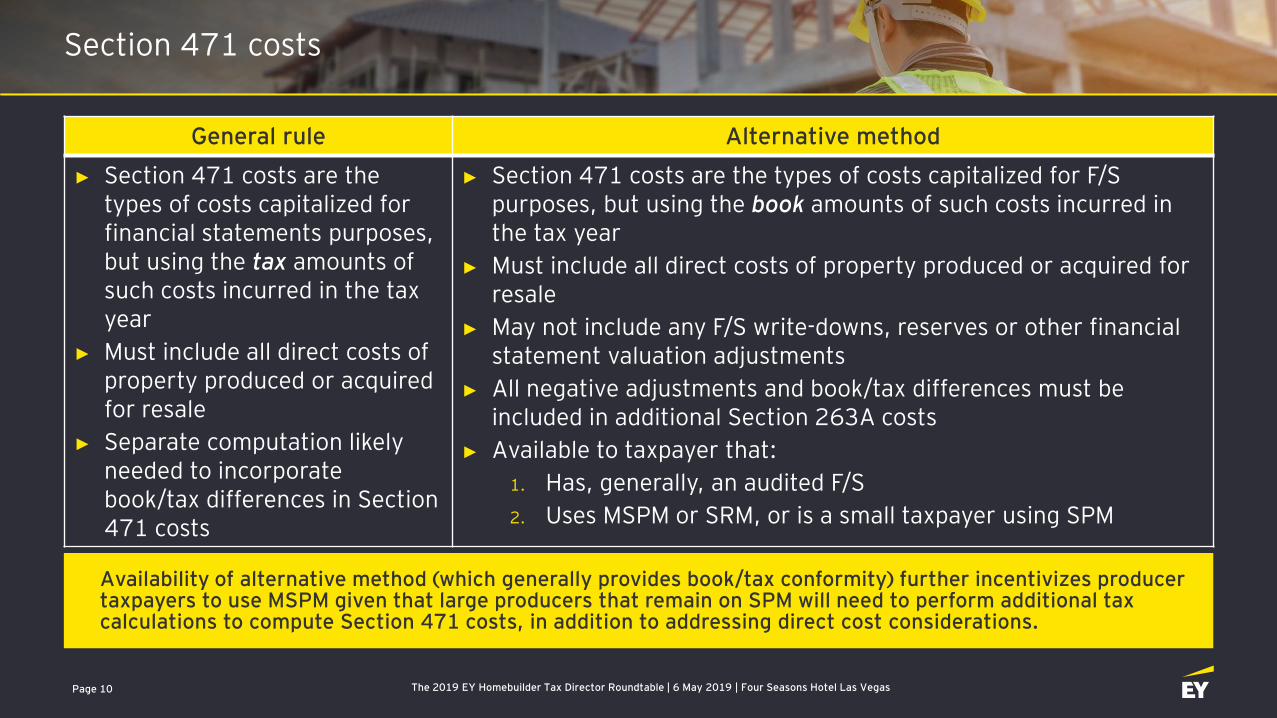

Section 471 costs

Availability of alternative method (which generally provides book/tax conformity) further incentivizes producertaxpayers to use MSPM given that large producers that remain on SPM will need to perform additional tax calculations to compute Section 471 costs, in addition to addressing direct cost considerations.

General rule Alternative method

► Section 471 costs are the types of costs capitalized for financial statements purposes, but using the tax amounts of such costs incurred in the tax year

► Must include all direct costs of property produced or acquired for resale

► Separate computation likely needed to incorporate book/tax differences in Section 471 costs

► Section 471 costs are the types of costs capitalized for F/S purposes, but using the book amounts of such costs incurred in the tax year

► Must include all direct costs of property produced or acquired for resale

► May not include any F/S write-downs, reserves or other financial statement valuation adjustments

► All negative adjustments and book/tax differences must be included in additional Section 263A costs

► Available to taxpayer that:1. Has, generally, an audited F/S 2. Uses MSPM or SRM, or is a small taxpayer using SPM

Page 10

The 2019 EY Homebuilder Tax Director Roundtable | 6 May 2019 | Four Seasons Hotel Las Vegas

Revenue Procedure 2018-56

► Provides the automatic change procedures for complying with the final regulations:► Modifies existing sections 12.01 and 12.02 of Rev. Proc. 2018-31 to include a change to many of

the new methods (e.g., MSPM, alternative method, the direct labor (DL) and direct material (DM) de minimis rules and the safe harbor for variances/certain burdens)

► Adds new automatic changes► Recharacterizing costs between additional Section 263A and Section 471, or vice versa, to comply with the

new rules► Ability to revoke a HAR election automatically for a taxpayer’s first, second or third taxable year ending on

or after November 20, 2018► “Five-year” eligibility rule is waived for a taxpayer’s first, second or third taxable year ending on or

after November 20, 2018► Reduced filing requirements for certain changes

► The procedures allow taxpayers significant flexibility in complying with the regulations:► Can early adopt some or all of the new rules

Page 11

The 2019 EY Homebuilder Tax Director Roundtable | 6 May 2019 | Four Seasons Hotel Las VegasThe 2019 EY Homebuilder Tax Director Roundtable | 6 May 2019 | Four Seasons Hotel Las Vegas

Questions?

Page 12

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. Information about how EY collects and uses personal data and a description of the rights individuals have under data protection legislation are available via ey.com/privacy. For more information about our organization, please visit ey.com.

© 2019 Ernst & Young LLP.All Rights Reserved.

US SCORE no. 06147-191USBSC no. 1901-3011954

ED None

This material has been prepared for general informational purposesonly and is not intended to be relied upon as accounting, tax or otherprofessional advice. Please refer to your advisors for specific advice.

ey.com