the banca intermobiliare companies · of veneto banca in cal and at the meetings with the top...

TRANSCRIPT

BANCA INTERMOBILIARE DI INVESTIMENTI E GESTIONI S.p.A.Via Gramsci, 7 - 10121 TURINTel. +39 011. 08.28.1 Fax +39 011. 08.28.800Website: www.bancaintermobiliare.com E-mail: [email protected] email: [email protected]

Parent CompanyVENETO BANCA S.p.A. LCA (Compulsory administrative liquidation)

Piazza G.B. Dall’Armi n. 1- 31044 Montebelluna (TV) (Registered office)

Via Feltrina Sud, 250 - 31044 Montebelluna (TV)

(Administrative Headquarters)

The Banca Intermobiliare CompaniesSYMPHONIA SGR S.p.A.10121 Turin – Via A. Gramsci, 7Tel. +39 02.77.7071 - Fax +39 02.77.707350Website: www.symphonia.it E-mail: [email protected] post: [email protected]

BIM FIDUCIARIA S.p.A.10121 Turin - Via Gramsci, 7Tel. +39 011.08.28.270 - Fax +39 011.08.28.852Website: www.bancaintermobiliare.comE-mail: [email protected]

BIM VITA S.p.A.10121 Turin - Via Gramsci, 7Tel. +39 011.08.28,411 - Fax +39 011.08.28,800Website: www.bimvita.it E-mail: [email protected]

BIM INSURANCE BROKERS S.p.A.Lloyd’s Correspondent

10121 Turin - Via Gramsci, 7Tel. +39 011.08.28.416 Fax +39 011.08.28.823Website: www.bimbrokers.it E-mail: [email protected]

BIM IMMOBILIARE S.R.L.10121 Turin - Via A. Gramsci, 7Tel. +39 011. 08.28.1 Fax +39 011. 08.28.800

CONSOLIDATED AND SEPARATE FINANCIAL STATEMENTS AT 31 DECEMBER 2017XXXVI FINANCIAL YEAR

CON

SOLI

DAT

ED A

ND

SEP

ARAT

E FI

NAN

CIAL

STA

TEM

ENTS

AT

31 D

ECEM

BER

201

7 -

XXXV

I FIN

ANCI

AL Y

EAR

Corporate websitewww.bancaintermobiliare.com

Telephone, Banca Intermobiliare:+39 011 - 0828.1

CONSOLIDATED FINANCIAL STATEMENTS AT 31 DECEMBER 2017XXXVI FINANCIAL YEAR

Board of Directors5 April 2018

REGISTERED OFFICE: VIA GRAMSCI, 7 10121 TURIN

SHARE CAPITAL€ 156,209,463 FULLY PAID-UP

BANK CODE NO. 3043.7BANKS REGISTER NO. 5319

TURIN COMPANY REGISTER OFFICE NO. 02751170016

CHAMBER OF COMMERCE OF TURIN REA NO. 600548 TAX ID CODE/ VATNO. 02751170016

REGISTERED IN THE REGISTER OF BANKS WITH NO. 5319

A SUBSCRIBER TO THE NATIONAL COMPENSATION FUND AND TO THE INTERBANK DEPOSIT PROTECTION FUND

PARENT COMPANY OF THE BANKING GROUP

(Registered with the Register of Banking Groups on 3.11.2017 code No. 3043)

BANCA INTERMOBILIARE CONSOLIDATED FINANCIAL STATEMENTS

MANAGEMENT REPORT TO THE CONSOLIDATED FINANCIAL STATEMENTS 5Highlights 6The macroeconomic scenario 12Main Consolidated Banca Intermobiliare data 16Reclassified consolidated financial statements 19Summary of operating results 232017-2021 Business Plan 25Business plan implementation status 27Main post-balance-sheet events 28Going concern 28Business outlook 28Operating figures and consolidated balance sheet data 29Consolidated economic results 53Consolidated comprehensive income 61Results of equity investments 62Market Disclosures 65Development and organisation activities 71Management and auditing activities 76The operating structure and personnel 79Other aspects 81

CONSOLIDATED FINANCIAL STATEMENTS 85Consolidated balance sheet 86Consolidated income statement 88Consolidated statement of comprehensive income 89Consolidated statement of changes in equity 90Consolidated statement of cash flows 92

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 95Part A - Accounting policies 96Part B - Information on the consolidated balance sheet 140Part C - Information on the consolidated income statement 185Part D - Consolidated statement of comprehensive income 202Part E - Information on risks and related hedging policies 203Part F - Information on consolidated equity 258Part G - Business combinations of companies or business units 265Part H - Related-party transactions 266Part I - Share-based payment agreements 271Part L - Segment information 272

ANNEXES TO THE CONSOLIDATED FINANCIAL STATEMENTS 275Annex 1 - Independent auditors’ fees related to the consolidated financial statements 276

REPORTS ON THE CONSOLIDATED FINANCIAL STATEMENTS 277Certification of the consolidated financial statements, in accordance with Article 81-ter of Consob Regulation No. 11971 of 14 May 1999 as amended and supplemented 278Independent Auditors’ report on the consolidated financial statements 279

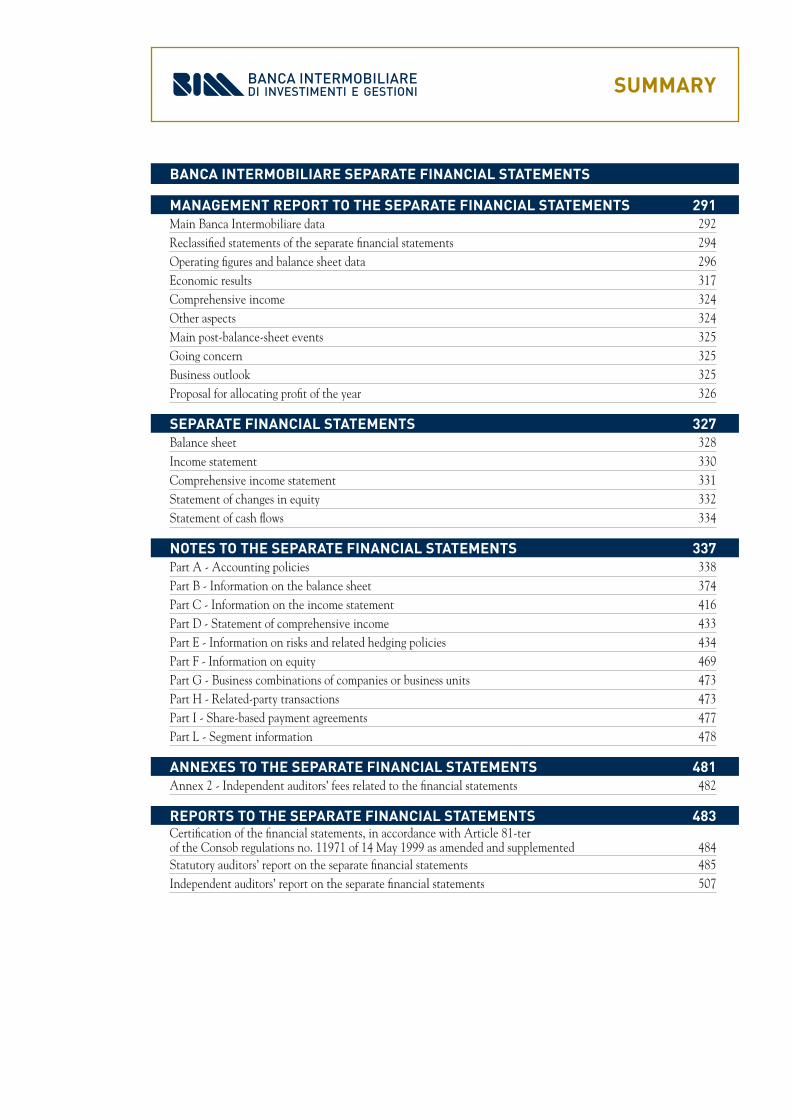

SUMMARY

BANCA INTERMOBILIARE SEPARATE FINANCIAL STATEMENTS

MANAGEMENT REPORT TO THE SEPARATE FINANCIAL STATEMENTS 291Main Banca Intermobiliare data 292Reclassified statements of the separate financial statements 294Operating figures and balance sheet data 296Economic results 317Comprehensive income 324Other aspects 324Main post-balance-sheet events 325Going concern 325Business outlook 325Proposal for allocating profit of the year 326

SEPARATE FINANCIAL STATEMENTS 327Balance sheet 328Income statement 330Comprehensive income statement 331Statement of changes in equity 332Statement of cash flows 334

NOTES TO THE SEPARATE FINANCIAL STATEMENTS 337Part A - Accounting policies 338Part B - Information on the balance sheet 374Part C - Information on the income statement 416Part D - Statement of comprehensive income 433Part E - Information on risks and related hedging policies 434Part F - Information on equity 469Part G - Business combinations of companies or business units 473Part H - Related-party transactions 473Part I - Share-based payment agreements 477Part L - Segment information 478

ANNEXES TO THE SEPARATE FINANCIAL STATEMENTS 481Annex 2 - Independent auditors’ fees related to the financial statements 482

REPORTS TO THE SEPARATE FINANCIAL STATEMENTS 483Certification of the financial statements, in accordance with Article 81-ter of the Consob regulations no. 11971 of 14 May 1999 as amended and supplemented 484Statutory auditors’ report on the separate financial statements 485Independent auditors’ report on the separate financial statements 507

SUMMARY

CONSOLIDATED FINANCIAL STATEMENTS31 DECEMBER 2017

REPORT ON OPERATIONSIN THE CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

6 ■ Management report to the consolidated financial statements

HIGHLIGHTS

ADMINISTRATION AND CONTROL BODIES OF BANCA IMMOBILIARE

BOARD OF DIRECTORS

Chairperson Maurizio LAURI

Director with assignments Giorgio Angelo GIRELLI 1

Directors Paolo CICCARELLISimona HEIDEMPERGHERAlessandro POTESTÀMichele ODELLODaniela TOSCANIAlessandra ZUNINO DE PIGNIER

BOARD OF STATUTORY AUDITORS

Chairperson Luca Maria MANZI

Regular Auditors Elena NEMBRINIEnrico Maria RENIER

Alternate Auditors Alide LUPOMichele PIANA

GENERAL MANAGER Stefano GRASSI

FINANCIAL REPORTING MANAGER Mauro VALESANI

INDEPENDENT AUDITORS PRICEWATERHOUSECOOPERS S.p.A.

1 On 7 March 2018, the Director Giorgio Angelo Girelli informed the Board of Directors of Banca Intermobiliare that he will resign from the position held, on the occasion of the formalisation of the acquisition by Trinity Investments of the shares of Veneto Banca S.p.A. in CAL, envisaged in the coming weeks.

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

Management report to the consolidated financial statements ■ 7

COMPULSORY ADMINISTRATIVE LIQUIDATION OF VENETO BANCA S.P.A.

With Italian Law Decree no. 99 of 25 June 2017, the Ministry of the Economy and Finance, on the proposal ofthe Bank of Italy, made Banca Popolare di Vicenza S.p.A. and Veneto Banca S.p.A. subject to compulsory administrative liquidation. The Bank of Italy appointed as liquidators of Veneto Banca S.p.A., the lawyers Alessandro Leproux, Prof. Giuliana Scognamiglio and Fabrizio Viola, and the Oversight Committee of the same, who, implementing the ministerial indications, are overseeing:i) the continuation, where necessary, of the company’s business or of certain branches of activity for the technical

time necessary to implement the planned sales;ii) the disposal of corporate assets and liabilities in accordance with the binding offer formulated by the transferee

identified as Intesa Sanpaolo S.p.A., which will take over the relationships of the transferor without a break;iii) the sale to Società per la Gestione di Attività S.G.A (in which the public has a stake) of impaired loans and other

assets not disposed of. Banca Intermobiliare, in the context of the said decree, as confirmed on its website by the Bank of Italy with news of 26 June 2017, does not come within the perimeter of Art. 3 among the assets acquired by Intesa Sanpaolo S.p.A., and is continuing its operations in an orderly manner, ensuring the continuity of the existing relationships with its clients. With reference to the sale of corporate assets and liabilities - pursuant to the aforementioned point ii) - Veneto Banca C.A.L. and Intesa Sanpaolo are performing the activities to complete the precise attribution of the various assets.On 28 September 2017 Banca Intermobiliare was ascertained as a less significant bank and brought under the supervision of the Bank of Italy.

VENETO BANCA IN C.A.L. - DISPOSAL OF THE INVESTMENT IN BANCA INTERMOBILIARE

Veneto Banca in CAL by means of a press release on 6 July 2017, informed the market that it had begun, in the context of realisation of its assets, a process aimed at the sale of its controlling equity interest in BIM. During this past July and August, the stages of the procedure that enabled various interested parties to present non-binding offers for purchase of the controlling interest were completed, with consequent performance by the selected bidders of the subsequent due diligence activities. The various stages of the procedure were assisted for the majority shareholder by the financial advisor Lazard & Co S.r.l. and to protect all the stakeholders, the Board of Directors of BIM chose as financial advisor Deutsche Bank AG.The process was carried out through access to the data room specifically established at the request of the advisors of Veneto Banca in CAL and at the meetings with the top management of Banca Intermobiliare. A first selection made by the seller of the expressions of interest was followed by the definition of a short list, then the reduction to two bidders and finally – on 28 September 2017 – the communication of the receivership procedure of an exclusive period granted to Attestor Capital LLP.

SALE OF BANCA INTERMOBILIARE TO TRINITY INVESTMENTS DESIGNATED ACTIVITY COMPANY

On 24 October 2017 Veneto Banca S.p.A. in CAL communicated that on 24 October 2017 it had signed a sale contract in favour of Trinity Investments Designated Activity Company (“Trinity Investments”), an investment firm subject to Irish law and managed by Attestor Capital LLP (“Attestor”), under the terms of which, conditional on the granting of the applicable regulatory authorisations, Trinity Investments undertook to purchase from the CAL 107.483.080 BIM ordinary shares equivalent to a total of 68.807% of the share capital, as well as the remaining equity interest of approximately 2.606% of the BIM share capital which will be sold under the same terms and conditions subsequent to the occurrence of certain events provided for in the Contract within 2 years from that date.The price agreed will be paid as follows: i) initial price of €/Mln 24.1 (€ 0.22411 for each BIM share) at the closing of the sale;ii) any deferred (earn-out) price to be determined on the basis of the profits resulting from the BIM consolidated

financial statements at 31 December 2021, normalised to exclude extraordinary components according to criteria and parameters indicated in the Contract. This “earn out”:- will be payable in 2022;- will be quantified applying a multiplier of 4.0x to the positive difference between the 2021 Normalised Profit and

a fixed amount of €/Mln 20;- will be reduced, if existing, on the basis of: (a) the pro-rata amount (calculated according to criteria indicated

in the Contract) of any BIM provisions on the performing loan portfolio at 30 June 2017 set aside in the BIM

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

8 ■ Management report to the consolidated financial statements

consolidated financial statements for financial years 2017, 2018 and 2019; and (b) any losses deriving from the occurrence of certain risk events related to BIM and its subsidiaries or from compensation payable by the CAL as better provided for in the Contract;

- provides for a total maximum which, in the event of sale of only the controlling interest, will be €/Mln 71.8 (this amount, if appropriate, will be increased in proportion to the further interest purchased by Trinity Investments with respect to the voting capital of BIM).

The Contract contains an interim management clause under the terms of which Veneto Banca CAL, within the limits permitted by law, assumes commitments of “reasonable effort” so that, between the signing date and the closing date, BIM and its investees do not carry out (or conclude agreements regarding) certain extraordinary or significant operations without prior written consent from Trinity Investments (among which, merely by way of example, actions disposing of equity investments held by BIM in investees, acquisitions or disposals, changes to the bylaws, mergers, demergers, winding up, issues of shares or other financial instruments that attribute the right to subscribe or purchase shares, distributions of dividends or reserves, purchase of treasury shares and other significant transactions according to thresholds and parameters specifically indicated in the Contract).

Execution of the sale of Banca Intermobiliare was subject to the condition precedent of obtainment of the following authorisations by 30 April 2018: a) with reference to the direct acquisition in BIM, the ECB’s authorisation required for the purchase of significant

equity investments in banks;b) with reference to the indirect acquisition of the equity investments held by BIM in Symphonia SGR S.p.A., BIM

Fiduciaria S.p.A., and BIM Vita S.p.A., the authorisations of the Bank of Italy and IVASS;c) a measure of the Bank of Italy that authorises the CAL to sell the Controlling Interest pursuant to art. 90,

paragraph 2, of the Consolidated Law on Banking (TUB) or which , in any case, including in the absence of this authorisation, acknowledges the sale with no objections.

With reference to the authorisation of the Antitrust Authority (Autorità Garante per la Concorrenza e il Mercato - AGCM), we can note that the said sale transaction is under the turnover threshold. After examining the documentation made available to it, on 12 December 2017, the AGCM communicated that it acknowledged the data provided without making further requests or objections to the reconstruction proposed.

After the authorisations have been obtained the sale contract will be concluded, and therefore Trinity Investments must launch an obligatory takeover bid on the BIM shares at the same price per BIM share paid to the CAL and, therefore, at a fixed unit price of € 0.22411 which will be paid to the BIM shareholders at the closing of the bid, plus the price per BIM share deriving from the earn-out that will accrue subsequently at the same terms and conditions agreed with the CAL. There may be an increase in the initial price if the Buyer (a) promotes the takeover bid (or increases the price offered) at a higher price than the initial unit price of € 0.22411 (excluding the cases of obligation or right to purchase pursuant to arts 108 and 111 of the TUB), or (b) transfers to third parties BIM shares at a higher price than the initial unit price within the 12 months following the closing of the bid or of any competing offer. For the purposes of obtaining the regulatory authorisations, Trinity Investments has presented a business plan for BIM up to 2021 which, after completion of the takeover bid, provides for a complex reorganisation of BIM which in addition will implement a: a. significant manoeuvre of de-risking BIM’s assets by deconsolidating the bank’s entire portfolio of impaired assets

for a gross value that can be estimated at around €/Mln 633, to be achieved through a so-called self-securitisation transaction and subsequent free assignment of the related “junior notes” to all BIM shareholders that remain such on the outcome of the takeover bid and of the capital strengthening operation pursuant to the next point;

b. an operation to strengthen BIM’s capital in 2018 for a total amount of €/Mln 121.

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

Management report to the consolidated financial statements ■ 9

BANK OF ITALY COMMUNICATION OF 5 APRIL 2018 TO BANCA INTERMOBILIARE - ACQUISITION OF THE CONTROLLING EQUITY INTEREST IN BANCA INTERMOBILIARE BY ATTESTOR CAPITAL

With a communication of 5 April 2018 the Bank of Italy made known to Banca Intermobiliare that the European Central Bank had taken, on the same date, the decision “not to oppose” the acquisition by Trinity Investments Designated Activity Company, Attestor Capital LLP, of the controlling equity interest in the capital of Banca Intermobiliare di Investimenti e Gestioni pursuant to the request made on 4 December 2017.In this regard, in noting the formalities provided for in the current supervisory regulations on the subject of communicating the conclusion of the acquisition operation, the Bank of Italy:i) invited Banca Intermobiliare to prepare suitable monitoring instruments as regards implementation of the business plan connected with the ownership restructuring; ii) requested that the group rescue plan provided for in art. 69-quinquies of the TUB and in the related implementing measures be transmitted within 4 months from conclusion of the acquisition.

ATTESTOR CAPITAL LLP

Attestor Capital LLP is an investment manager based in London that pursues a global investment strategy of the “fundamental value” type with a geographical focus on Europe. Attestor has funds under management for approximately $/Bln 4. The majority of the capital comes from endowments and family offices which agree with the long-term investment philosophy. Attestor has gained skills and a specific track record on the subject of investment in financial institutions thanks to execution of numerous operations in the sector. Attestor’s main focus is the acquisition of assets in which to provide skills and capital, with the aim of making them attractive operating platforms in profitable business segments.

APPEAL TO THE REGIONAL ADMINISTRATIVE COURT (RAC) BY BARENTS AGAINST THE SALE OF THE CONTROLLING STAKE TO ATTESTOR

After the contract was signed for the sale of the equity investment in Banca Intermobiliare held by Veneto Banca in CAL to Attestor, on 24 October 2017, Barents Reinsurance S.A. (“Barents”) presented, to the Regional Administrative Court (RAC), an appeal against:a) the decision on 28 September 2017, regarding the alleged “exclusion” from the competitive bids for the sale

by Veneto Banca S.p.A. in compulsory administrative liquidation of the controlling equity interest in Banca Intermobiliare and rejection of its offer presented on 29 August 2017;

b) and the actions connected with this decision, in particular that concerning (b) the appointment of Lazard S.r.l. as advisor to the liquidators;

c) the choice of Attestor Capital LLP as the buyer of the aforesaid equity interest.

On 4 December 2017 the RAC met in chambers, adjourning its judgement on the appeal. Barents with a plea of additional grounds, notified on 19 January to the Second Section Bis of the Lazio RAC, requested, with reference to the sale of Banca Intermobiliare by the liquidators of Veneto Banca to the Attestor fund, the cancellation of the Bank of Italy authorisation (no. 1330870/17 of 9 November 2017) and of the further actions and orders related to the operation. In particular the RAC judges were to be presented with evidence of further defects and illegitimacies of the procedure, and multiple errors in the assessments of the offers presented by Barents and Attestor.

With judgement no. 1127 of 2018, the Second Section Bis of the Lazio RAC ruled on the appeal lodged by Barents against the rejection of the offer made by the said Barents on 29 August 2017. On the basis of the reconstruction of the events and an in-depth examination of the nature of the actions challenged and the rules applied, the RAC declared that the Administrative Court did not have jurisdiction over the dispute, acknowledging the private-law nature of the procedure for the sale of the controlling stake in BIM, and referring the dispute in question to the jurisdiction of the Ordinary Court.

On 5 February 2018 Barents presented an appeal to the Council of State (general register number 900 of 2018), for the cancellation and/or revision, after precautionary suspension, of the judgement handed down in simplified form no. 1127/2018, issued by the Lazio RAC with which the Court of First Instance declared that the Administrative Court did not have jurisdiction in G.R. no. 10995/2017. The Council of State ruled on 12 February 2018 against a precautionary suspension and on 1 March 2018 rejected the appeal.

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

10 ■ Management report to the consolidated financial statements

REGISTRATION OF BANCA INTERMOBILIARE IN THE REGISTER OF BANKING GROUPS

The placing in compulsory administrative liquidation of Veneto Banca S.p.A. on 25 June 2017, and the ECB’s decision to withdraw Veneto Banca’s banking licence on 19 July 2017 determined the related measures concerning the cancellation of the same from the register of banking groups. On 30 September 2017, Banca Intermobiliare communicated to the Bank of Italy, under the terms of the Supervisory Rules for Banks (Bank of Italy Circular no. 285 of 17 December 2013), the fulfilment of the conditions for assuming the qualification of “Parent Company” and formally requested registration of the same in the register of banking groups providing subsequently, on 26 October 2017, an update on the group’s perimeter, after the sale of BIM Suisse to Banca Zarattini & Co SA.On 3 November 2017, the Bank of Italy communicated the registration of Banca Intermobiliare as Parent Company of the Banca Intermobiliare Banking Group with effects running from 30 September 2017.In particular the perimeter of the banking group includes the subsidiaries Symphonia SGR and Bim Fiduciaria, both subject to the management and coordination activity of Banca Intermobiliare under the terms of Italian Legislative Decree 385/1993 (Consolidated Law on Banking), and the subsidiary Bim Immobiliare, subject to the management and coordination activity of Banca Intermobiliare under the terms of the civil law pursuant to articles 2497 ff. of the Italian Civil Code. The following subsidiaries remain excluded from the banking group: Bim Suisse (sold on 18 October 2017), Bim Vita (held at 50% with UnipolSai and subject to the control of the latter on the basis of contractual commitments), Bim Insurance Brokers (held at 51%), and the non-instrumental property equity investments Immobiliare D, Paomar Terza and Patio Lugano (all held at 100%).

STRUCTURE OF BANCA INTERMOBILIARE

The disclosure on the structure of Banca Intermobiliare is provided below. This has changed with respect to the previous year owing to the operation to sell Banca Intermobiliare di Investimenti e Gestioni (Suisse) SA completed on 18 October 2017 between Banca Zarattini & Co SA and Banca Intermobiliare.

Parent companyThe issuer Banca Intermobiliare S.p.A. is controlled by right by Veneto Banca S.p.A. in L.C.A..

Banca Intermobiliare: subsidiaries and associated companies• Symphonia SGR S.p.A., Bim Fiduciaria S.p.A., Bim Immobiliare S.r.l., Immobiliare D S.r.l., Paomar Terza S.r.l. and

Patio Lugano S.A. (from 18.10.2017) are controlled by right by Banca Intermobiliare S.p.A., which holds directly the entire share capital;

• Bim Vita S.p.A. is equally owned by Banca Intermobiliare (50%) and Fondiaria-Sai (50%) now UnipolSai (UGF Group) and is subject to the control of the latter pursuant to contractual commitments.

• Bim Insurance Brokers S.p.A. is controlled by Banca Intermobiliare S.p.A. which holds 51% of the share capital.

The following diagram represents the shareholdings of Banca Intermobiliare by business area, after the sale of the Swiss investees. The 100% equity investments in Immobiliare D S.r.l. and Paomar Terza S.r.l. (acquired for credit recovery purposes) and the subsidiary Patio Lugano S.A. were presented in “Other Property Companies”:

SYMPHONIA SGR S.p.A.

100%

BIM FIDUCIARIA S.p.A.

100%

BIM INSURANCE BROKER S.p.A.

51%

BIM VITAS.p.A.

50%

BIM IMMOBILIARE S.r.l.

100%

ALTRE IMMOBILIARI

100%

ASSET MANAGEMENT TRUSTEE SERVICES INSURANCE COMPANIES REAL ESTATE COMPANIES

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

Management report to the consolidated financial statements ■ 11

CONSOLIDATION SCOPE

Following the communication of the Bank of Italy on the registration of Banca Intermobiliare as Parent Company of the “Banca Intermobiliare Group” with effect from 30.09.2017 the consolidation scope is presented updated indicating whether or not the investees belong to the banking group.

EQUITY INVESTMENTS BELONGING TO THE BANCA INTERMOBILIARE BANKING GROUPParent Company: • Banca Intermobiliare di Investimenti e Gestioni S.p.A.Wholly-owned subsidiaries (100%), fully consolidated:• Symphonia SGR S.p.A.• Bim Fiduciaria S.p.A.• Bim Immobiliare S.r.l.

EQUITY INVESTMENTS NOT BELONGING TO THE BANCA INTERMOBILIARE BANKING GROUPWholly-owned subsidiaries (100%), fully consolidated: • Immobiliare D S.r.l.• Paomar Terza S.r.l.Subsidiaries at 100%, consolidated according to IFRS 5:• Patio Lugano S.A.Partially-owned subsidiaries (less than 100%), fully consolidated:• Bim Insurance Brokers S.p.A.Associates measured using the equity method: • Bim Vita S.p.A.

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

12 ■ Management report to the consolidated financial statements

THE MACROECONOMIC SCENARIO

The improvement of the profile of economic growth at the global level, which for the first time in the last three years was uniform and synchronised, and maintenance of monetary policies overall still accommodating and expansive, thanks to inflation levels that remain still very low, enabled the financial markets to record very positive results this year, in particular as regards equities. The continuation by the American FED of a gradual normalisation of monetary policy, implemented both by moderately raising interest rates and progressively reducing the dimensions of its budget, determined a rise in yields limited to short-term American bonds but had, surprisingly, a negative effect on the dollar, which fell against the other currencies, with the dollar index down by approximately 10%. The raw material markets took advantage of the improvement in the growth of the industrialised countries and, in the case of oil, of the agreements reached by OPEC for the limitation of production capacity. A further positive element, in particular for the equity markets, came from approval, at the end of the year, of the American fiscal reform which reduced significantly the average tax rate of corporate profits, down from 35% to 21%. The political risk, potentially high in Europe, instead did not materialise given the results of the elections in the Netherlands, France and Germany. During the summer there was then an increase in tension between the United States and North Korea, as a consequence of a series of nuclear experiments conducted by the latter which led also to the launch of a number of missiles that flew over Japan. At the global level economic growth, for 2017, is forecast to have accelerated compared to previous years, coming out at a level currently estimated by the International Monetary Fund (IMF) of 3.7%, sharply up compared to 2016 and 2015 (3.2%). The growth profile in industrialised countries is expected to improve compared to the previous year and should be 2.3% compared to 1.7% in 2016. The highest growth will be recorded in Spain (+3.1%) and in Canada (+3%) while the lowest growth profiles will be recorded in Italy (1.6%) and in Great Britain (1.7%). In the Euro area as a whole, growth is forecast at 2.4% compared to 1.8% the previous year. Also in emerging countries growth in 2017 improved compared to the previous years, coming out at a level estimated by the IMF of 4.7% compared to 4.4% in 2016 and 4.1% in 2015. The highest growth should be recorded in China (+6.8%), while the lowest is expected in Brazil (+1.1%). The level of the inflation rate remained, also in 2017, at figures lower than the average, both in absolute terms and relatively with respect to the targets set by the Central Banks. Despite this, the improvement in the economic growth profile worldwide and the recovery of the prices of a number of raw materials determined a relative increase in inflation, in particular in the industrialised countries. In these latter, the recent IMF forecasts see inflation reaching 1.7% in 2017, up compared to the 2016 levels (0.8%). In emerging countries, however, inflation estimates are expected to be at 4.1%, slightly down compared to 2016 (4.3%). The monetary policies of the main central banks have continued to be divergent, in an environment of sharply-improved growth but low inflation. On the American front, the FED implemented three raises in the level of official interest rates, taking them up from a range of 0.5%-0.75% at the end of 2016 to the current 1.25%-1.5%. In addition, last October the American central bank began the programme of reducing its budget (so-called Quantitative Tightening) for an amount of 10 billion dollars a month up to the end of 2017, of which 6 made up of government securities and 4 of mortgage-backed securities. For 2018, the FED is planning three further interest-rate hikes, motivated by the improving estimates of economic growth, inflation and unemployment and to continue the Quantitative Tightening, taking the monthly reduction ceiling up from the initial 10 billion to a maximum of 50 billion a month, 30 for government securities and 20 billion for securitisations. The handover, this coming February, from the current governor Yellen to the new governor Powell could however determine different orientations with respect to the route followed up to now by the FED, in particular as regards the assessment of the impact on growth of the tax reform approved by the American congress. The ECB, instead, kept official interest rates unchanged (-0.4%), but the Quantitative Easing programme, originally planned to expire in December 2017 was reduced: from 60 billion of monthly purchases it will go down, from January 2018, to 30 billion. The duration of the programme was however prolonged by a further nine months: from the end of 2017 to September 2018 with the possibility, if considered necessary, to continue it. In Great Britain the BOE decided, for the first time for 10 years, to increase by 0.25% the level of official interest rates, taking them up to 0.5%, owing to fears associated with the expected increase in inflation. An analogous raise was decided also by the Canadian central bank which made the cost of money dearer for the first time since 2010, raising by a quarter of a point the level of official rates, from 0.5% to 0.75%. In India instead, the level of interest rates was lowered, taking them from the previous 6.25% to 6%, the lowest level since 2010. As far as sovereign debt is concerned, we can note, in the first half of the year, the lowering of the creditworthiness of Italian public debt by the Canadian agency DBRS, one of the four large global rating agencies, which reduced it, bringing it down from A- to BBB+, with prospects however stable, an adjustment which was besides delayed with respect to the other agencies (Standard & Poor’s, Moody’s and Fitch). Towards the end of the year, instead, the American agency Standard & Poor’s upgraded Italian creditworthiness, raising it to BBB. The reasons for the upgrade included the increase in GDP growth, the improvement in employment and the maintenance of the monetary stimulation by the ECB.

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

Management report to the consolidated financial statements ■ 13

In China we can note the lowering of creditworthiness by Moody’s which, for the first time since ’89, reduced the rating, bringing it down from A1 to Aa3, improving however the outlook from negative to stable. The reasons for the downgrading were expectations of a deterioration in the financial solidity of the country in the next few years, owing to continuously increasing debt and a slowdown of the economy. In the case of Standard & Poor’s instead, the downgrade of the rating was from AA- to A+, the first cut since 1999, and it was motivated by the prolonged period of growth of corporate loans, although the outlook of the debt was instead kept stable. In Venezuela Standard & Poor’s declared the selective default of the government debt owing to the non-payment of an instalment of 200 million dollars of interest on sovereign bonds while two other rating agencies, Fitch and Moody’s, declared in default the state oil company PDVSA for non-payments in October and November. In India we can note the revision of the rating by Moody’s, the first improvement of the creditworthiness of the Asian country for 14 years. The rating changed to Baa2 from Baa3 and was motivated by the positive effect that the economic reforms introduced by the Modi government (demonetisation, introduction of VAT) will have on the stabilisation of the growing levels of public and private debt. In Europe, finally, we can note the agreement reached unanimously by the ministers of the Eurogroup for a third tranche of aid to Greece for €/Bln 8.5, in which the IMF will also take part, for a maximum amount of two billion dollars. Participation of the IMF in this tranche, unlike in the two previous ones in which it took no part, was made possible thanks to the strong stress placed in this programme on growth and on the fact that Greece had observed its commitments and completed the work on the priority actions to be pursued. On the European political front, the numerous electoral appointments of the year did not bring negative surprises: in the Netherlands and in France, the populist candidates hostile to Europe and to the single currency were defeated while, in Germany only after long and extenuating negotiations with the social democrats a new government coalition was formed at the beginning of March 2018. In United Kingdom the outcome of the early general election was disappointing for the Conservative Party which did not obtain an absolute majority of seats. The objective of the early election was therefore not achieved. At this point it is probable that the election result, while not cancelling the decision of last year’s referendum on the United Kingdom leaving the European Union, will weaken the political line of the Conservative party, pushing it towards a softer attitude in relations with Europe. In Japan, instead, the outgoing prime minister came out the winner in the early general election of November. In the USA, finally, the long-awaited tax reform - one of the two economic pillars of Trump’s electoral programme - was approved by congress. The average rate of taxation of corporate profits comes down permanently from the current 35% to 21% while, at the level of individual taxes, the planned reductions will have a ten-year time deadline. To limit the costs of the reform, estimated by the Congressional Budget Office as an increase of a thousand billion in the public account deficit, a fiscal shield was introduced for American multinational companies, which will be able to repatriate profits accumulated abroad at lower rates (8% for non-liquid assets and 15.5 % for liquidity).On the context for listed companies the trend of profit in 2017 was decidedly positive, unlike what happened in the two previous years: for stocks belonging to the American S&P500 index the most recent estimates are for growth in profit of 10.9% on turnover growth of 5.5%. The sectors that showed the best profit trend (up to the third quarter of 2017) were energy and technology, while the weakest results were recorded in the financial and public utilities sectors. There is expected to be a further improvement in profit growth in 2018, currently estimated at 16.9% on turnover growth of 6.4%. Also in Europe in 2017 the profit growth estimates for the Eurostoxx50 index are for a sharp improvement compared to the previous years: +9.4% on a turnover increase of 3.8%. The sectors that show the best profit trend are energy and food, while the weakest results were recorded in the insurance and health sectors. Also in Europe there is expected to be a further improvement in profit growth in 2018, currently estimated at 9.9% on turnover growth of 3.7%. In this framework, the main equity indices achieved on average very positive results in the year, although they were greatly influenced by the currency component. The MSCI World Index closed 2017, in fact, with a positive performance of 16.3% in local currency but only 5.5% in Euro. The US S&P 500 closed the year up 19.4% and the Japanese Topix index analogously rose by 19.7%; the European Eurostoxx50 index closed the year instead up 6.5%. On the domestic front, the FTSE Italia All Share index recorded a rise of 15.6% while the analogous index specialised in small and medium-sized companies, the FTSE Italia Mid Cap, recorded a sharp rise of 35.5%, partly thanks to the introduction of the law on Individual Saving Plans (ISPs) which encouraged significant investment flows on this market segment. In the emerging equity markets, the MSCI Emerging Markets index rose by 27.8% in local currency and 18% in Euro. The market that obtained the best results was Hong Kong with the Hang Seng index up by 36%, while the index that recorded the least brilliant result was the Russian RTS, which was substantially unchanged (0.2%). The best performances by sector worldwide were recorded in the sectors of technology (+35.4%) and raw materials (+19.5%) while the worst results were recorded in the sectors of energy (-1.6%) and telecommunications (-2.2%). As regards raw materials, the overall CRB index rose by 0.7% with the highest increase recorded in the industrial metals sector, up 29.1%, while the largest downside figure was in “soft commodities” (-12.4%). Oil recorded an increase of 12.5% while gold rose by 13%. On the currency markets the Euro surprisingly rose significantly against all the main currencies, with the cross against the American Dollar rising by 13.8%. We can also note the sharp rise of the Euro against the main refuge currencies,up 10% against the Japanese Yen and 9.1% against the Swiss Franc.

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

14 ■ Management report to the consolidated financial statements

The performance of the bond markets continued to be positive, despite the moderate interest rate raise by the American FED and the improvement of economic growth at the global level. The fact that the inflation rate remains at levels always lower than the targets set by the Central Banks makes it possible, in fact, to keep monetary policies still decidedly expansive. In this situation, the index of US government 5 to 10-year securities rose by 2.1% and the US 10-year yield declined slightly from 2.44% at the end of 2016 to 2.41% at the end of 2017. On the European front, the ML EMU index for maturities between 5 and 10 years rose by 0.9% but the German 10-year yield moved from 0.2% at the end of 2016 to 0.4% at the end of 2017. Very positive results were recorded even in riskier segments of the bond market, with the EMU corporate index up by 2.4%, the European High Yield index up by 6.7% and the global index of emerging government issues up by 10.1%.

Il 2018The estimates for global economic growth for 2018, after a sound 2017 (+3.6%), are characterised by a context of global growth which will be positive (+3.7%) and quite widespread at the geographical level, driven by a generalised recovery of investments. In the United States the context is positive owing to the good conditions of the labour and financial markets, even before considering the positive contribution of the tax reform, above all on investments, which in the short term should accelerate growth. In the medium term, however, the effective tax benefits for businesses and individuals are still uncertain. In the Euro Area domestic demand and investments are driving the recovery, increasingly widespread and close to peak acceleration. In Great Britain the economic context remains less weak than the expectations, although the uncertainty on the outcome of Brexit is beginning to be felt on investments and property. Japan is benefiting from the positive global context and from the excellent conditions of the labour market. In China there are some evident signs of slowdown, but this could be slighter than the expectations thanks to the good performance of consumption and the gradual effects of the structural reform. In India recovery is gradual, with the electoral deadline of next year that could lead the government to expansive manoeuvres, bringing short-term benefits to the detriment of the trend in public accounts. In Russia the recovery is quite good, with the possible passing of the baton from investments to consumption as greatest contributor to growth, while the recovery of consumption in Brazil could offset the possible slowdown in investments due to the political uncertainty.As far as corporate profits are concerned, the growth estimates at the global level for 2018 are quite good at 10.5%, although slowing down slightly compared to 2017 (+15.1%), with positive revisions in the last few weeks. The caution of ‘bottom-up’ analysts and the not excessive expectations for growth, in some cases lower than what can be inferred from the early forecasts, could lead to further positive revisions of the estimates, above all if the macroeconomic context does not disappoint.On the inflation front the forecasts for the developed countries are for a recovery of consumer prices, above all in cases where the output gap is closer to zero, as in the USA, where the growth of salaries and the rising oil price could lead to a higher-than-expected rise. In most of the emerging countries, instead, inflation should be down slightly or stable, thanks to higher levels of unused capacity, although in some cases, as in China, increases are being seen.In terms of market interest rates, the current yields on government bonds are not very consistent with the estimated economic scenario so it is possible that they will rise, although the size of the change could be limited owing to the still significant presence of the Central Banks on the secondary market which will boost demand for instruments still capable of offering returns. In the light of the current QE programmes, in fact, the Central Banks will still be net purchasers on the secondary market for the whole of 2018, while they will change to being net sellers in 2019. The gradual reduction of purchases by the Central Banks could however lead to the Term Premium rising again and favour a partial steepening of the interest rate curves. Monetary policies will remain differentiated geographically, with the FED tending to be restrictive in terms of interest rates and budget assets, although with graduality as long as there are no surprises on inflation, while in all the emerging countries they will remain expansive. In Europe the ECB should proceed gradually to reduce securities purchases, while in Japan the latest statements of the governor Kuroda seemed to indicate less conviction on the usefulness of the existing aggressive manoeuvres so surprises in a less expansive direction cannot be excluded a priori.

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

Management report to the consolidated financial statements ■ 15

On the subject of systemic risk the political debate in the USA remains lively despite the approval of the tax reform and, as the mid-term election of next autumn comes closer, it will be possible to see a gradual intensification of political discussions. The geopolitical tensions between the USA and North Korea seem to benefit from a recent relaxation, but the event that will catalyse attention in the first half of the year is the Italian general election on 4 March: the risk of an exit of Italy from the Euro is not high, but it will be difficult for a government coalition in favour of structural reforms to come out of the ballot box.The absolute measurements of the main equity indices are more or less in line with their historical averages, except for some cases where higher figures can be seen, as is the case in the United States, driven by the notable weight of the technological sector. However, observations at the level of indices do not take into account the still significant differences among the various segments and sectors and, in any case, no particular excesses are evident. From a geographical point of view, the European and Japanese markets maintain quite a markdown compared to the other markets, as also some emerging countries, although these differences tend to reflect different levels of profitability. On the equity markets and on the overall economic scenario there is quiet confidence, although at the moment no extreme figures can be seen. On corporate bonds the yields remain positive relative to government bonds in terms of extra yield, although it remains difficult to imagine a further compression of spreads, already towards the bottom of the historical ranges. There remains reasonable value on the segment of subordinated bonds of the financial sector thanks to the gradual improvement of capital ratios achieved up to now and required by the legislation over the next few years. The yields offered by the bonds of emerging countries remain positive, above all on issues in local currencies, also in the light of the gradual improvements of the fundamentals.

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

16 ■ Management report to the consolidated financial statements

MAIN CONSOLIDATED BANCA INTERMOBILIARE DATA

SUMMARY DATA

RECLASSIFIED ECONOMIC VALUES (Thousands of €.)2

31.12.2017 31.12.2016pro-forma

Changeabsolute

Change%

31.12.2016

Net interest income 11,783 21,834 (10,051) -46.0% 21,832

Operating income 86,299 91,948 (5,649) -6.1% 91,215

Operating profit (loss) 1,763 2,255 (492) -21.8% 1,967

Profit (loss) before non-recurring components (44,546) (105,564) 61,018 57.8% (105,852)

Profit (loss) before tax (46,400) (108,321) 61,921 57.2% (108,609)

Consolidated profit (loss) for the period (49,297) (93,371) 44,074 47.2% (93,371)

ASSETS AND OPERATING VALUES (in €/million)31.12.2017 31.12.2016 Change Change

%

Total deposits 7,424 9,372 (1,948) -20.8%

Direct deposits 931 1,450 (519) -35.8%

Indirect deposits 6,493 7,922 (1,429) -18.0%

- of which assets under administration 2,241 2,708 (467) -17.2%

- of which client assets under management 4,101 5,125 (1,024) -20.0%

- of which fiduciary assets deposited externally 150 89 61 68.5%

Loans to clients 632 843 (212) -25.1%

- of which performing loans to clients 344 508 (164) -32.2%

- of which net impaired assets 245 296 (50) -17.0%

Total Assets 1,599 2,599 (1,000) -38.5%

CAPITAL (in €/million) AND CAPITAL RATIOS UNDER BASEL III3

31.12.2017 31.12.2016 Change Change%

Consolidated equity 192.3 237.2 (45.0) -19.0%

Own Funds 121.6 159.8 (38.2) -23.9%

Surplus of Own Funds 35.3 54.1 (18.8) -34.8%

Capital conservation buffer 13.5 8.3 5.2 62.7%

Total RWAs 1,155.9 1,411.7 (255.8) -18.1%

CET1 - Fully Phased 10.22% 11.52% (1.31) N/a

CET1 - Phased in 10.44% 11.13% (0.69) N/a

T1 - Additional Tier 1 Capital 10.44% 11.13% (0.69) N/a

TCR - Total Capital Ratio 10.52% 11.32% (0.80) N/a

Index of capitalisation 1.32 1.41 (0.10) -7.0%

2 The economic figures have been reclassified compared to the income statement required by Bank of Italy Circular no. 262 of 2005 as currently applicable so as to achieve better representation of the results. Please see the notes beneath the table of the reclassified consolidated income statement. The comparative figure at 31.12.2016 was restated in the “pro forma” column in order to take into account the line-by-line recognition of the accounting balances of the subsidiary Bim Insurance Brokers no longer considered a non-current asset held for sale.

3 The CET1 – Fully Phased - was calculated not applying the exceptions deriving from the transitional provisions provided for in Bank of Italy Circular no. 285.

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

Management report to the consolidated financial statements ■ 17

PROFITABILITY INDICES31.12.2017 31.12.2016

pro-formaChange

points %31.12.2016

Net interest income/Net operating income 13.7% 23.7% -10.1 23.9%

Net fees and commissions/Net operating income 67.8% 66.1% 1.7 65.9%

Operating profit (loss)/Net operating income 2.0% 2.5% -0.4 2.2%

Cost/Income ratio (including other operating charges/income) 98.0% 97.5% 0.4 97.8%

Net profit (loss)/Average net equity (ROE) -23.0% -32.7% 9.7 -32.7%

Net profit (loss)/Total Assets (ROA) -2.3% -3.2% 0.9 -3.2%

CREDIT QUALITY RATIOS31.12.2017 31.12.2016 Change

points %

Performing exposures/Loans to clients 54.5% 60.2% (5.7)

Net impaired assets/Loans to clients 38.8% 35.1% 3.7

- of which Net non-performing loans/Loans to clients 23.8% 19.0% 4.8

- of which net probable defaults/Loans to clients 14.7% 15.4% (0.7)

Coverage rate of performing Exposures 0.7% 0.6% 0.1

Coverage rate of impaired Exposures 60.6% 53.1% 7.5

- of which due to non-performing loans 68.7% 64.1% 4.6

- of which due to probable defaults 34.2% 27.0% 7.2

OPERATING STRUCTURE31.12.2017 31.12.2016

pro-formaChange absolute

Change%

Number of employees and collaborators (total) 536 594 (58) -9.8%

- of which Private Bankers 149 164 (15) -9.1%

Number of Banca Intermobiliare branches 28 29 (1) -3.4%

INDICATORI PER DIPENDENTE (Valori espressi in €/Migl.)31.12.2017 31.12.2016

pro-formaChange absolute

Change%

Net Operating Income/Average No. of staff 189 186 3 1.6%

Personnel expenses/Average No. of employees 93 87 5 5.7%

Total assets/Total No. of staff 2,983 4,375 (1,392) -31.8%

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

18 ■ Management report to the consolidated financial statements

31.12.2017 31.12.2016 Absolute change

Change%

No. of outstanding ordinary shares (excluding treasury shares) 149,632,100 149,627,772 4,328 -

Unit equity on shares outstanding 1.29 1.59 (0.30) -18.9%

Price per ordinary share during the year

Minimum 0.45 1.00 (0.55) -55.2%

Average 1.19 1.60 (0.41) -25.7%

Maximum 1.52 2.24 (0.72) -32.1%

Average stock exchange capitalisation 177 239 (62.00) -25.9%

Price/Book Value 0.92 1.01 (0.09) -8.6%

Basic EPS – EUR (0.33) (0.62) 0.29 -47.20%

Diluted EPS – EUR (0.33) (0.62) 0.29 -47.20%

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

Management report to the consolidated financial statements ■ 19

RECLASSIFIED CONSOLIDATED FINANCIAL STATEMENTS

RECLASSIFIED CONSOLIDATED INCOME STATEMENT4

(Thousands of €)

31.12.2017 31.12.2016pro-forma

Absolute Change

Change%

31.12.2016

Interest income and similar items 25,516 42,414 (16,898) -39.8% 42,411

Interest expense and similar items (13,733) (20,580) 6,847 33.3% (20,579)

Net interest income 11,783 21,834 (10,051) -46.0% 21,832

Fee and commission income 78,266 82,044 (3,778) -4.6% 81,050

Fee and commission expenses (19,719) (21,245) 1,526 7.2% (20,982)

Net fee and commission income 58,547 60,799 (2,252) -3.7% 60,068

Dividends 421 1,617 (1,196) -74.0% 1,617

Net gains (losses) on trading instruments 6,207 4,493 1,714 38.1% 4,493

Transactions on AFS securities and financial liabilities 9,377 3,382 5,995 177.3% 3,382

Net gains (losses) on hedging instruments (36) (177) 141 N/a (177)

Net gains (losses) on financial operations 15,969 9,315 6,654 71.4% 9,315

Operating income 86,299 91,948 (5,649) -6.1% 91,215

Personnel expenses (44,364) (44,334) (30) -0.1% (44,008)

Other administrative expenses (40,285) (41,280) 995 2.4% (41,148)

Operating amortisation and depreciation (2,521) (2,689) 168 6.2% (2,676)

Other operating expenses (income) 2,634 (1,390) 4,024 N/a (1,416)

Operating costs (84,536) (89,693) 5,157 5.7% (89,248)

Operating profit (loss) 1,763 2,255 (492) -21.8% 1,967

Write-downs of loans (45,643) (91,619) 45,976 50.2% (91,619)

Net provisions for risks and charges (2,145) (17,680) 15,535 87.9% (17,680)

Profit (Loss) of investee companies measured at equity 1,479 1,480 (1) -0.1% 1,480

Profit (loss) before non-recurring components (44,546) (105,564) 61,018 57.8% (105,852)

Write-downs on financial instruments (1,854) (2,757) 903 32.8% (2,757)

Profit (loss) before tax (46,400) (108,321) 61,921 57.2% (108,609)

Income tax for the period (1,176) 17,402 (18,578) N/a 17,499

Profit of continuing operations after tax (47,576) (90,919) 43,343 47.7% (91,110)

Profit (Loss) of assets held for sale, net of tax (1,651) (2,359) 708 30.0% (2,168)

Consolidated profit (loss) (49,227) (93,278) 44,051 47.2% (93,278)

Profit (Loss) pertaining to non-controlling interests (70) (93) 23 24.7% (93)

Consolidated Profit (Loss) of group (49,297) (93,371) 44,074 47.2% (93,371)

4 In order to provide a clearer representation of the results, the reclassified economic results differ from the Bank of Italy formats with the following reclassifications: the costs relating to the variable component of remuneration of the private bankers who are employees and other minor costs were reclassified from “Personnel expenses” to “Fee and commission expenses” (for €/thou 538 at 31.12.2017 and for €/thou 1,354 at 31.12.2016). The comparative figure at 31.12.2016 was restated in the “pro forma” column in order to take into account the line-by-line recognition of the accounting balances of the subsidiary Bim Insurance Brokers no longer considered a non-current asset held for sale.

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

20 ■ Management report to the consolidated financial statements

RECLASSIFIED CONSOLIDATED BALANCE SHEET5

(Thousands of €)

31.12.2017 31.12.2016pro-forma

Absolute Change

Change%

31.12.2016

Cash 1,689 1,670 19 1.1% 1,669

Loans:

- Receivables from clients for performing loans 344,174 508,194 (164,020) -32.3% 507,719

- Receivables from clients: other 287,406 335,366 (47,960) -14.3% 335,366

- Loans to banks 108,090 371,245 (263,155) -70.9% 371,245

Financial assets:

- Held for trading 44,621 97,374 (52,753) -54.2% 97,374

- Available for sale 414,540 835,237 (420,697) -50.4% 834,780

- Hedging derivatives 1,607 1,327 280 21.1% 1,327

Fixed assets:

- Equity investments 14,365 14,020 345 2.5% 14,020

- Intangible and tangible 95,892 97,809 (1,917) -2.0% 97,779

- Goodwill 49,446 49,446 - - 49,446

Property held for sale 21,900 21,900 - - 21,900

Non-current assets held for sale 21,357 71,902 (50,545) -70.3% 73,480

Other asset items 193,931 193,318 613 0.3% 193,229

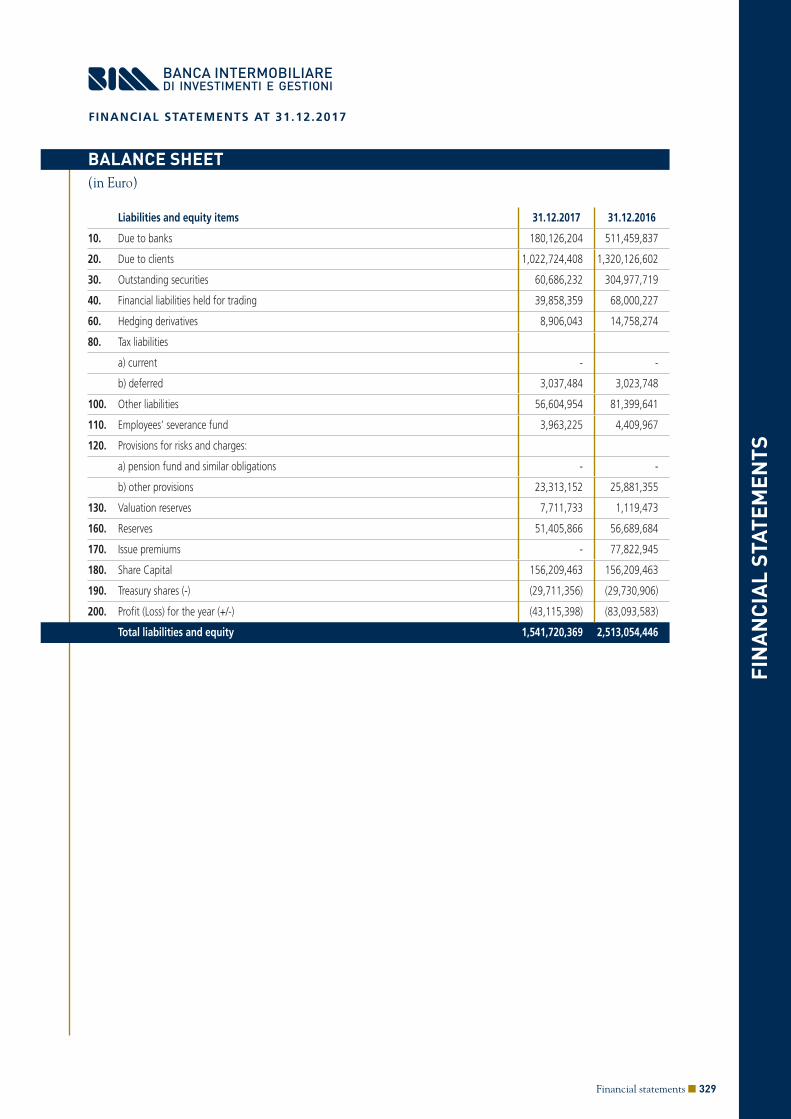

Total Assets 1,599,018 2,598,808 (999,790) -38.5% 2,599,334

Payables:

- Due to banks 183,232 509,294 (326,062) -64.0% 509,294

- Due to clients 985,633 1,285,540 (299,907) -23.3% 1,286,040

Outstanding securities 60,686 304,978 (244,292) -80.1% 304,978

Financial liabilities:

- Held for trading 39,858 67,969 (28,111) -41.4% 67,969

- Hedging derivatives 8,906 14,758 (5,852) -39.7% 14,758

Specific provisions 27,902 30,791 (2,889) -9.4% 30,744

Non-current liabilities held for sale 7,856 38,102 (30,246) -79.4% 38,914

Other liability items 92,641 110,176 (17,535) -15.9% 109,437

Shareholders’ equity 192,304 237,200 (44,896) -18.9% 237,200

Total liabilities 1,599,018 2,598,808 (999,790) -38.5% 2,599,334

5 In order to provide a better representation of operations, the reclassified balance sheet details differ from the Bank of Italy formats for the reclassification of assets arising from recovery claims from item 160 “Other assets” to the item “Property held for sale” (€/thou 21,900 at 31.12.2017 and at 31.12.2016). The comparative figure at 31.12.2016 was restated in the “pro forma” column in order to take into account the line-by-line recognition of the accounting balances of the subsidiary Bim Insurance Brokers no longer considered a non-current asset held for sale.

The entry “Other asset items” includes balance sheet items 130 and 150 of Bank of Italy Circ. no. 262 net of the properties mentioned above. The item “Specific provisions” includes balance sheet items 110 and 120 of Bank of Italy Circ. no. 262. “Other liability items” includes balance sheet items 80 and 100 of Bank of Italy Circ. no. 262.

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

Management report to the consolidated financial statements ■ 21

QUARTERLY CONSOLIDATED/RECLASSIFIED INCOME STATEMENT DATA(Thousands of €)

2017 2016

4Q17 3Q17 2Q17 1Q17 4Q16pro-forma

3Q16pro-forma

2Q16 1Q16

Interest income and similar items 4,543 4,773 6,669 9,531 7,367 11,965 12,886 10,196

Interest expense and similar items (1,867) (1,824) (4,130) (5,912) (2,926) (5,874) (6,980) (4,800)

Net interest income 2,676 2,949 2,539 3,619 4,441 6,091 5,906 5,396

Fee and commission income 23,194 21,592 16,608 16,872 22,813 18,458 19,938 20,835

Fee and commission expenses (5,671) (4,598) (4,863) (4,587) (5,237) (4,672) (5,411) (5,925)

Net fee and commission income 17,523 16,994 11,745 12,285 17,576 13,786 14,527 14,910

Dividends 68 41 294 18 122 814 658 23

Net gains (losses) on trading instruments 706 749 3,025 1,727 1,648 246 1,908 691

Transactions on AFS securitiesand financial liabilities 1,071 (642) 4,698 4,250 697 141 1,723 821

Net gains (losses) on hedging instruments (337) 175 50 76 (37) 265 (190) (215)

Net gains (losses) on financial operations 1,508 323 8,067 6,071 2,430 1,466 4,099 1,320

Operating income 21,707 20,266 22,351 21,975 24,447 21,343 24,532 21,626

Personnel expenses (13,037) (9,559) (11,046) (10,722) (11,052) (9,919) (11,790) (11,573)

Other administrative expenses (9,907) (11,298) (8,841) (10,239) (12,258) (8,970) (10,417) (9,635)

Operating amortisation and depreciation (618) (632) (635) (636) (676) (675) (624) (714)

Other operating expenses (income) 1,213 (92) 1,100 413 (1,665) 414 (451) 312

Operating costs (22,349) (21,581) (19,422) (21,184) (25,651) (19,150) (23,282) (21,610)

Operating profit (loss) (642) (1,315) 2,929 791 (1,204) 2,193 1,250 16

Write-downs of loans (18,301) (3,301) (22,665) (1,376) (64,970) (13,786) (11,022) (1,841)

Net provisions for risks and charges 774 (783) (2,135) (1) (12,713) (1,240) (3,802) 75

Net profit (loss) of subsidiaries carried at equity 385 241 509 344 519 179 457 325

Profit (loss) before non-recurring components (17,784) (5,158) (21,362) (242) (78,368) (12,654) (13,117) (1,425)

Write-downs on financial instruments (249) 73 (473) (1,205) 284 (749) (1,513) (779)

Profit (loss) before tax (18,033) (5,085) (21,835) (1,447) (78,084) (13,403) (14,630) (2,204)

Income tax for the period (495) (888) 94 113 11,601 2,988 2,788 25

Profit (Loss) of current operations after tax (18,528) (5,973) (21,741) (1,334) (66,483) (10,415) (11,842) (2,179)

Profit (Loss) of assets held for sale, net of tax 1,030 (863) (1,097) (721) (799) (889) (529) (142)

Consolidated profit (loss) (17,498) (6,836) (22,838) (2,055) (67,282) (11,304) (12,371) (2,321)

Loss attributable to non-controlling interests (58) (48) 14 22 (77) (47) 14 17

Consolidated Profit (Loss) of group (17,556) (6,884) (22,824) (2,033) (67,359) (11,351) (12,357) (2,304)

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

22 ■ Management report to the consolidated financial statements

QUARTERLY CONSOLIDATED/RECLASSIFIED BALANCE SHEET DATA(Thousands of €)

Financial Year 2017 Financial Year 2016

31.12 30.09 30.06 31.03 31.12 30.09 30.06 31.03

Cash 1,689 1,628 1,624 1,474 1,670 1,618 1,758 1,815

Loans:

- Receivables from clients for performing loans 344,174 371,886 402,613 468,328 508,194 621,374 645,772 708,324

- Receivables from clients: other 287,406 310,774 319,325 325,616 335,366 370,165 404,762 392,078

- Loans to banks 108,090 103,866 144,371 141,738 371,245 184,717 215,491 199,986

Financial assets:

- Held for trading 44,621 103,731 153,428 113,894 97,374 282,577 288,922 287,566

- Available for sale 414,540 456,387 475,827 755,947 835,237 934,531 960,086 977,473

- Hedging derivatives 1,607 1,630 2,044 2,140 1,327 242 248 87

Fixed assets:

- Equity investments 14,365 13,938 13,677 14,294 14,020 13,755 13,491 14,162

- Intangible and tangible 95,892 96,327 96,907 97,373 97,809 98,567 99,027 99,172

- Goodwill 49,446 49,446 49,446 49,446 49,446 49,446 49,446 49,446

Property held for sale 21,900 21,900 21,900 21,900 21,900 21,900 21,900 21,900

Non-current assets held for sale 21,357 67,330 63,621 69,268 71,902 102,988 126,241 108,752

Other asset items 193,931 178,836 190,481 194,757 193,318 183,121 201,661 183,915

Total Assets 1,599,018 1,777,679 1,935,264 2,256,175 2,598,808 2,865,001 3,028,805 3,044,676

Payables:

- Due to banks 183,232 246,036 302,786 331,265 509,294 651,899 760,671 457,943

- Due to clients 985,633 965,387 1,010,264 1,177,809 1,286,040 1,299,171 1,297,321 1,581,840

Outstanding securities 60,686 132,809 174,516 246,675 304,978 336,488 350,235 378,277

Financial liabilities:

- Held for trading 39,858 79,151 78,314 81,298 67,969 118,177 123,089 142,412

- Hedging derivatives 8,906 8,677 7,254 15,807 14,758 16,872 12,119 13,447

Specific provisions 27,902 30,058 32,332 30,527 30,791 20,993 19,786 15,731

Non-current liabilities held for sale 7,856 34,525 28,489 31,536 38,102 42,686 64,128 46,515

Other liability items 92,641 72,355 87,462 109,444 110,176 73,745 86,452 80,804

Shareholders’ equity 192,304 208,681 213,847 231,814 237,200 304,970 314,366 327,707

Total liabilities 1,599,018 1,777,679 1,935,264 2,256,175 2,598,808 2,865,001 3,028,805 3,044,676

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

Management report to the consolidated financial statements ■ 23

SUMMARY OF OPERATING RESULTS

For Banca Intermobiliare financial year 2017 was greatly affected by the situation of the majority shareholder Veneto Banca, which led last June to the process of compulsory administrative liquidation, with a consequent impact on the operating and profit trends. The commitment of the new Board of Directors, of the renewed management and of the entire corporate structure however made it possible to limit the negative effects of this situation, implementing the guidelines of the strategic plan which provides for the relaunch of the Bank. At the same time the authorisation procedure with the Bank of Italy is proceeding for Attestor Capital LLC which on 24 October 2017 signed with Veneto Banca CAL a contract to purchase BIM. Among the documentation provided in the authorisation procedure, the buyer presented a business plan for BIM up to 2021 which, after completion of the takeover bid provides for a complex reorganisation, in 2018, including a further manoeuvre for the de-risking of BIM’s assets through deconsolidation of the entire portfolio of impaired assets and a capital strengthening operation of €/Mln 121. In this context, Banca Intermobiliare carried out a series of managerial actions which made it possible to limit the loss for the period 2017. The loss of €/Mln 49.3, was better than that of 2016 (+€/Mln 93.4), and in line with what was provided for in the 2017-2021 business plan.Client Assets Under Management amounted to €/Bln 7.4 net of duplications and recorded a reduction of 20.8% yoy (-18.4% yoy net of Bim Suisse deposits). Direct deposits amounted to €/Bln 0.9 (-35.8% yoy), while indirect deposits came out at €/Bln 6.5 (-18% yoy), of which invested for €/Bln 4.1 in managed products and €/Bln 2.2 in administered products. As regards receivables, performing loans to clients, of €/Mln 344.2 (€/Mln 508.2 at 31.12.2016), were further reduced by 32.3%, implementing the business plan which provides for gradual disposal of loan exposures to the Corporate segment. The exposure of net impaired assets, of €Mln 245.4, was down 17% compared to 31.12.2016. The coverage rate of “impaired assets” rose to 60.6% (53.1% at 31.12.2016) higher than the average figure for the industry (47.5% referred to the category of “Non-Significant Banks”).As regards consolidated prudential supervision, it is confirmed that there is adequate capital strength in relation to the criteria set out in the Basel III agreement. Consolidated Own Funds are €/Mln 121.6 (€/Mln 159.8 at 31.12.2016), with a surplus of Own Funds on the risk-weighted assets of €/Mln 35.3 (€/Mln 54.1 at 31.12.2016). The Capital conservation buffer of €/Mln 13.5 was up compared to €/Mln 8.3 at the end of 2016. Significant reduction of RWAs (€/Mln 1,156 against €/Mln 1,412 -18.1% yoy) as a consequence of implementation of the de-risking policy resolved by the BoD by means of reducing the non-core loan portfolio, securities recognised in the “banking book” and sale of the equity investment in Bim Suisse. The consolidated regulatory capital ratios at 31.12.2017 (CET1 Phased in 10.44%, T1 10.44% and TCR 10.52%) are higher than the minimum levels required by the Basel III accord. Finally, it should be noted that the Fully Phased as at 31.12.2017, estimated by applying the parameters that will be fully in force from 1 January 2019, stands at 10.22%.Capital resources – adequate for the current technical coordinates - are destined, according to the statements of the Prospective Buyer, to be increased significantly (€/Mln 121), in order to give the Bank what it needs to support a significant relaunch.As regards equity investments, recognised as asset disposal groups, in October 2017, as all the conditions precedent had been fulfilled, the sale of Banca Intermobiliare di Investimenti e Gestioni (Suisse) SA to Banca Zarattini & Co SA was completed at a final price of Chf/Mln 39.4, determining a positive result in the consolidated income statement of €/Mln 0.7. In the context of the above operation, as provided for, Banca Intermobiliare purchased from BIM Suisse the entire share capital of Patio Lugano S.A. for Chf/Mln 15.05.

Regarding the consolidated economic results for the year, the following information is provided.Net interest income amounted to €/Mln 11.8 with a decrease of 46% YOY (€/Mln 21.8 at 31.12.2016), as a result both of the de-risking strategy, which involves a gradual reduction of loan exposures to corporate clients and of the securities portfolio, and of reinvestment in securities with shorter duration. Net fee and commission income of the period amounted to €/Mln 58.5, a decrease of 3.7%, yoy (€/Mln 60.8 at 31.12.2016), despite a drop in AUM of 20.8%. Fees and commissions related to Asset Management grew by 5.1%, as a consequence of the good performance fees, the higher proportion of Asset Management out of total deposits and the improved profitability of the assets, while fees deriving from the Administered segment fell (-34.7%).The result of financial operations came out at €/Mln 16 compared to €/Mln 9.3 recorded in the previous year. The increase was due to the profits made on sales of securities recognised among financial assets available for sale, in the context of the aforementioned “derisking” strategy. Operations on financial instruments recognised in the banking book contributed €/Mln 9.4 (€/Mln 3.4 at 31.12.2016).

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

24 ■ Management report to the consolidated financial statements

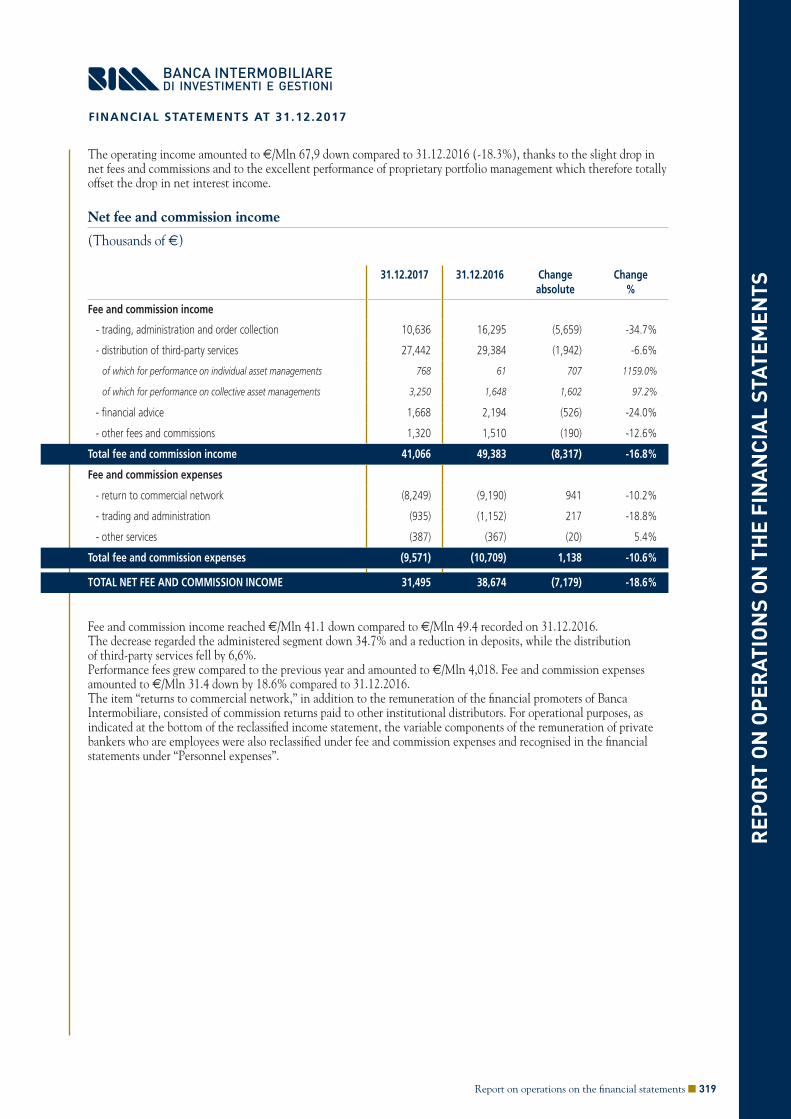

The operating income amounted to €/Mln 86.3, down compared to 31.12.2016 (-6.1% yoy). The excellent performance obtained by management of the proprietary portfolio almost totally offset both the drop in net interest income, and the slight reduction in net fees and commissions.Operating costs amounting to €/Mln 84.5 (€/Mln 89.7 at 31.12.2016) were down by 5.7% yoy.Net of extraordinary expenses of approximately €/Mln 4.4 due to projects for the re-internalisation of outsourced activities, for reorganisation of the Bank and activities that led to signing of the BIM sale contract, operating costs would have recorded a significant reduction of 10.7%. Personnel expenses amounted to €/Mln 44.4 at 31.12.2017, and were in line with 31.12.2016. Other administrative expenses, including the extraordinary expenses mentioned above, amounted to €/Mln 40.3, down by 2.4% compared to 31.12.2016. Net of extraordinary expenses, the yoy comparison shows expenses down 13.1%. The contribution of other operating expenses and income was a positive €/Mln 2.6 (a negative €/Mln 1.4 at 31.12.2016).

The operating profit came out at €/Mln 1.8 (€/Mln 2.3 at 31.12.2016), a decrease of 21.8% compared to 31.12.2016. Net of the above extraordinary expenses, the operating profit would have been €/Mln 6.2, a sharp increase compared to 31.12.2016.Net write-downs on loans amounted to €/Mln 45.6, a decrease of 50.2% compared to the write-downs made at 31.12.2016 (€/Mln 91.6). The provisions set aside during the period were made in keeping with the current policies, which provide for periodic revisions of estimates regarding foreseeable losses, with reference both to the economic and financial situation of clients, and to the evolution of the value of the guarantees received.There was a loss before tax of €/Mln 46.4 (a loss of €/Mln 108.3 at 31.12.2016) after performing value adjustments on loans of €/Mln 45.6 (€/Mln 91.6 at 31.12.2016), allocations to provisions for risks of €/Mln 2.1 (€/Mln 17.7 at 31.12.2016) and impairment on financial instruments of €/Mln 1.9 (€/Mln 2.8 at 31.12.2016). There was a loss on continuing operations after tax at 31.12.2017 of €/Mln 47.6 (loss of €/Mln 90.9 at 31.12.2016). The current and deferred tax burden was a negative €/Mln 1.2 (a positive €/Mln 17.4 at 31.12.2016). The probability test performed on deferred taxation confirmed the recoverability of the deferred tax assets recognised in the previous year, while no deferred tax assets were set aside on the tax losses of financial year 2017.The Group’s consolidated loss, therefore, came out at €/Mln 49.3 (loss of €/Mln 93.4 at 31.12.2016) after determining the losses of assets held for sale, after tax, which were €/Mln 1.7 (result of the sale of Bim Suisse and operating loss of the subsidiary Patio Lugano) and a loss pertaining to non-controlling interests of €/Mln 0.070.

Lastly, if we look closely at the reclassified income statement for each company at the date of 31.12.2017, we can note the results of the consolidating company Banca Intermobiliare and the subsidiary Symphonia SGR.

Banca Intermobiliare S.p.A. recorded a net operating income of €/Mln 67.9 (€/Mln 83.2 at 31.12.2016), an operating loss of €/Mln 4.5 (a positive €/Mln 6 as at 31.12.2016), and a loss for the year of €/Mln 43.1 (loss of €/Mln 83.1 at 31.12.2016). The negative result for the financial year was determined mainly by significant adjustments, in particular from net write-downs on loans of €/Mln 45.5 (€/Mln 91.6 as at 31.12.2016), and allocations to provisions for risks and charges of €/thou 2 (€/Mln 17.9 as at 31.12.2016) and impairment on financial instruments of the “banking book” of €/Mln .9 (€/Mln 2.8 at 31.12.2016). As regards operating income, it was negatively affected by the generalised decline in interest rates which lowered net interest income (-45.2% yoy) and by the decrease in net fees and commissions (-18.6% yoy) owing to the decrease in assets managed (-17.9% yoy), despite the fact that a good profit was recorded on financial operations in the year (+10.6%) and operating costs fell significantly (-6.2% yoy). Symphonia SGR S.p.A. closed 2016 with a profit for the year of €/Mln 9.5 at 31.12.2017, an increase compared to €/Mln 6.8 at 31.12.2016. Net fee and commission income amounted to €/Mln 26 up by 24.2% compared to the previous year (€/Mln 20.9 at 31.12.2016). Operating costs amounted to €/Mln 12.4 at 31.12.2017 (€/Mln 11.3 at 31.12.2016, -10.1% yoy). At 31.12.2017 the assets managed by Symphonia, including those received under delegated management, amounted to €/Bln 2.9, and were down compared to €/Bln 3.8 at 31.12.2016 due to outflows of managed assets of clients in part offset by the positive market effect.

CONSOLIDATED FINANCIAL STATEMENTS AT 31.12.2017

MA

NAG

EMEN

T R

EPO

RT

TO T

HE

CON

SOLI

DAT

ED F

INA

NCI

AL

STAT

EMEN

TS

Management report to the consolidated financial statements ■ 25

2017-2021 BUSINESS PLAN