the gabelli equity trust inc.gabelli.com/gab_pdf/qrep/2017q1/-111.pdf · another strong year of...

TRANSCRIPT

Average Annual Returns through March 31, 2017 (a)Since

InceptionQuarter 1 Year 5 Year 10 Year 15 Year 20 Year 25 Year (08/21/86)———— ——— ——— —––—— —––—— —––—— ———–—— ———–——

Gabelli Equity TrustNAV Total Return (b) . . . . . . 6.67% 17.26% 12.27% 7.29% 9.10% 9.82% 10.29% 10.77%Investment Total Return (c) 10.88 22.06 11.95 6.84 7.42 9.76 10.11 10.47

S&P 500 Index . . . . . . . . . . . . . . . 6.07 17.17 13.30 7.51 7.09 7.86 9.62 10.05(d)Dow Jones Industrial Average . . . 4.98 19.56 12.04 8.03 7.31 8.34 10.27 10.95(d)Nasdaq Composite Index . . . . . . . 10.13 22.93 15.38 10.60 9.23 9.16 9.55 9.70(e)

(a) Returns represent past performance and do not guarantee future results. Investment returns and the principal valueof an investment will fluctuate. When shares are sold, they may be worth more or less than their original cost. Currentperformance may be lower or higher than the performance data presented. Visit www.gabelli.com for performanceinformation as of the most recent month end. Performance returns for periods of less than one year are notannualized. Investors should carefully consider the investment objectives, risks, charges, and expenses of the Fundbefore investing. The Dow Jones Industrial Average is an unmanaged index of 30 large capitalization stocks. TheS&P 500 and the Nasdaq Composite Indices are unmanaged indicators of stock market performance. Dividends areconsidered reinvested except for the Nasdaq Composite Index. You cannot invest directly in an index.

(b) Total returns and average annual returns reflect changes in the NAV per share, reinvestment of distributions at NAVon the ex-dividend date, adjustments for rights offerings, spin-offs, and taxes paid on undistributed long term capitalgains and are net of expenses. Since inception return is based on an initial NAV of $9.34.

(c) Total returns and average annual returns reflect changes in closing market values on the NYSE, reinvestment ofdistributions, and adjustments for rights offerings, spin-offs, and taxes paid on undistributed long term capital gains.Since inception return is based on an initial offering price of $10.00.

(d) From August 31, 1986, the date closest to the Fund’s inception for which data is available.(e) From September 30, 1986, the date closest to the Fund’s inception for which data is available.

Comparative Results

To Our Shareholders,

For the quarter ended March 31, 2017, the net asset value (“NAV”) total return of The Gabelli Equity Trust

(the “Fund”) was 6.7%, compared with total returns of 6.1% and 5.0% for the Standard & Poor’s (“S&P”) 500

Index and the Dow Jones Industrial Average, respectively. The total return for the Fund’s publicly traded shares

was 10.9%. The Fund’s NAV per share was $6.08, while the price of the publicly traded shares closed at $5.97

on the New York Stock Exchange (“NYSE”).

The Gabelli Equity Trust Inc.Shareholder Commentary – March 31, 2017

(Y)our Portfolio Management Team

Robert D. Leininger, CFAPortfolio Manager

BA, Amherst CollegeMBA, Wharton School,

University of Pennsylvania

Mario J. Gabelli, CFAChief Investment Officer

Christopher J. MarangiCo-Chief Investment Officer

BA, Williams College MBA, ColumbiaBusiness School

Daniel M. MillerManaging Director,GAMCO Investors

BS, University of Miami

Kevin V. DreyerCo-Chief Investment Officer

BSE, University ofPennsylvania

MBA,ColumbiaBusiness School

2

Premium / Discount Discussion

As a refresher for our shareholders, the price of a closed-end fund is determined in the open market by

willing buyers and sellers. Shares of the Fund trade on the NYSE and may trade at a premium to (higher than)

net asset value (the market value of the Fund’s underlying portfolio and other assets less any liabilities) or a

discount to (lower than) net asset value.

Ideally, the Fund’s market price will generally track the NAV. However, the Fund’s premium or discount to

NAV may vary over time. Over the Fund’s thirty year history, the range fluctuated from a 27% discount in

December 1987 to a 38% premium in June 2002. On March 31, 2017, the market price of the Fund was at a

1.8% discount to its NAV.

The Fund’s long term investment goal is growth of capital, with income as a secondary objective. The

Fund seeks to generate a real rate of return of 10%. We believe that our stock selection process adds to the

investment equation. We have a successful history of investment, providing shareholders average annual

returns of 10.8% since inception.

-40%

’91 ’92 ’93 ’94 ’95 ’96’89’88’87’86 ’90 ’97 ’98 ’99 ’00 ’01

-10%

-20%

0

10%

20%

30%

-30%

40%

PREMIUM/DISCOUNT SINCE INCEPTION

’02 ’03 ’06

8/21/86 3/31/17

’07’05’04

Data points as of each month end.

’08 ’09 ’10

March 31, 2017

Net Asset Value $6.08Market Price $5.97Premium/Discount (1.81)%

’13’12’11 ’14 ’15 ’16

3

First Quarter Commentary

The post-election rally of 2016 continued into the first quarter of 2017, with the U.S. equity market setting

all-time highs. Rising expectations for lower taxes, regulatory reform, and increased fiscal spending have

generated optimism for both businesses and consumers and translated into higher stock prices. Robust hiring,

falling unemployment, and firming wage growth opened the door for the Federal Reserve to raise short term

interest rates for the third time since the financial crisis, increasing the federal funds rate to ¾ to 1 percent in a

widely anticipated move.

Warning bells rang, however, following the failure of the Republican-controlled Congress to repeal and

replace the Affordable Care Act, a key promise of the Trump administration. After a long and extended run,

markets finally took a pause to evaluate the new administration’s ability to deliver on policy and to question the

unity of a Republican party and consider the possibility of more Washington “gridlock.” Failing to dismantle

Obamacare caused markets to reassess the probability of a business friendly agenda, especially tax reform and

a large infrastructure bill, over the next four years. At the same time, the rate increase serves as a reminder that

rising rates often have a negative implication for stock price multiples. Earnings may always rise fast enough in

order to compensate for this effect, but rising earnings are predicated on President Trump enacting at least some

of his agenda – which is why political news continues to take center stage.

Outside the U.S., markets continue to digest the populist upheavals that have occurred not only in America,

but around the globe. Theresa May invoked Article 50 of the Treaty on European Union, formally starting the

process of the withdrawal of the United Kingdom. Presidential elections will be held soon in France, and while

Marine Le Pen is still considered a long shot, political dynamics in 2016 have taught us not to rule her out. A

Le Pen win could ultimately change the relationship EU members have with one another, or even lead to the

dissolution of the group (and the euro) entirely. All this, combined with continued sabre-rattling by North Korea

and the conflict in Syria, show that the world continues to be a tumultuous place. External, unanticipated events

can and will impact the stock market.

With this backdrop, we believe this is a great time to research and pick individual stocks using our Private

Market Value (PMV) with Catalyst™ selection process. The wide variety of policy initiatives of the new

administration is generating catalysts and opportunities for corporate America and will likely stimulate global deal

activity. At the same time, uncertainty may lead to attractive entry points for certain companies.

Deals, Deals & More Deals

Worldwide announced merger and acquisition (M&A ) activity totaled $777.7 billion during the first quarter

of 2017, a 12% increase year over year. U.S. healthcare giant Johnson & Johnson’s $30 billion takeover of

Swiss biotech Actelion Ltd was the largest so far this year, while U.K. household products maker Reckitt

Benckiser agreed to pay $18 billion for U.S. baby formula producer Mead Johnson Nutrition. Other attempted

deals were less successful: Kraft Heinz’s $143 billion “bear hug” bid for Unilever Plc was spurned, while

Netherlands paint manufacturer Akzo Nobel NV rejected a $24 billion bid from Pittsburgh-based PPG Industries.

More deal making could come once there is clarity on tax reform, as well as a better sense for regulatory scrutiny

by the Trump administration.

4

Investment Scorecard

The top contributors to performance in the first quarter included Rollins Inc. (+10%), which delivered yet

another strong year of revenue and earnings per share growth, reaffirming its leading position in the attractive pest

control industry; Honeywell International (+8%), which delivered sizable 2016 earnings growth, driven by margin

expansion and significant FCF generation; Viacom (+27%), which appreciated as investors gained confidence in

new CEO Bob Bakish’s strategy, refocusing the company’s channels around six key brands, and better using those

brands to support the Paramount film slate; Yakult Honsha (+20%), which continues to grow its sales of Yakult

probiotic drinks both in Japan and around the world in local currencies, and whose shares appreciated in U.S. dollar

terms due to the strengthening Japanese yen; and Madison Square Garden (+16%) rose as investors increasingly

appreciate the value and durability of live entertainment, and specifically sports franchises.

Detractors from performance included Macy’s (-16%), which had disappointing sales and earnings amid

the looming threat of online competitors, though the company announced plans to close nearly 100 stores

in order to improve profitability; Inventure Foods (-55%), which sold its Fresh Frozen business, but still has to

take strategic steps in order to reduce its debt; Curtiss-Wright (-7%), which reported declines in sales and

operating income due to lower demand in the energy sector and unfavorable currency translation; Telephone &

Data Systems (-8%), which was impacted by the 14% decline in 83%-owned U.S. Cellular; and Hertz Global

Holdings (-19%), which declined as broader concerns surrounding used car pricing were coupled with soft fourth

quarter results and new CEO Kathy Marinello’s comments that the company’s turnaround could take

considerable investment in service, systems, and fleet.

Let’s Talk Stocks

The following are stock specifics on selected holdings of our Fund. Favorable earnings prospects do not

necessarily translate into higher stock prices, but they do express a positive trend that we believe will develop

over time. Individual securities mentioned are not necessarily representative of the entire portfolio. For the

following holdings, the share prices are listed first in United States dollars (USD) and second in the local

currency, where applicable, and are presented as of March 31, 2017.

Berkshire Hathaway Inc. (BRK/A – $249,850 – NYSE), based in Omaha, Nebraska, is the holding company for

a diverse group of operating subsidiaries, including insurance, freight rail transportation, utilities and energy,

finance, services, and retailing. The subsidiaries operate in an autonomous fashion, while investment and capital

allocation decisions are managed by 86 year-old Warren Buffett in consultation with 92 year-old Charlie Munger.

From 1965 through December 31, 2016, the firm had an annual compounded gain on book value of 19.0%.

Herc Holdings Inc. (HRI – $48.89 – NYSE), based in Bonita Springs, Florida, is the third largest equipment rental

company in the United States, after United Rentals and Sunbelt Rentals (owned by Ashtead). HRI was spun out

of former parent Hertz on June 30, 2016. Underemphasized as part of a significantly larger car rental company,

HRI now has the opportunity to improve profitability to levels more commensurate with peers as a standalone

entity. Ultimately, we view HRI as an attractive acquisition candidate.

5

Honeywell International Inc. (HON – $124.87 – NYSE) operates as a diversified technology company with highly

engineered products, including turbine propulsion engines, auxiliary power units, turbochargers, brake pads,

environmental and combustion controls, sensors, security and life safety products, resins and chemicals, nuclear

services, and process technology for the petrochemical and refining industries. One of the key drivers of HON’s

growth is acquisitions which increase the company’s growth profile globally, creating both organic and inorganic

opportunities. The company recently acquired Elster Industries, a leading provider of thermal gas solutions, smart

meters, software and data analytics for the commercial, industrial, and residential heating market. Elster’s gas

business offers products in high demand among natural gas customers, and brings a strong, global distribution

network and numerous cross-selling opportunities for existing HON technologies to new customers. Elster’s gas,

electric, and water meters are highly valued for their reliability, safety, and accuracy. The company maintains an

installed base of more than 200 million meter modules deployed over the course of the last ten years that

generates significant recurring revenues. We believe acquisitions such as Elster should drive meaningful and

sustained growth for HON, spurred by global energy efficiency initiatives and natural resource management.

Liberty Global plc (LBTYK – $35.04 – NASDAQ), (LBTYA – $35.87 – NASDAQ) is the leading international cable

operator, offering advanced video, telephone, and broadband Internet services. The company operates

broadband communications networks in twelve European countries, under brands that include UPC, Unitymedia

(Germany), Virgin (UK), and Telenet (Belgium). In July 2015 Liberty issued the UK’s first tracker stock, known

as “LiLAC,” to highlight its properties in Chile and Puerto Rico. In May 2016, LiLAC completed the acquisition of

Cable & Wireless, expanding its reach to twenty countries in Latin America and the Caribbean. Management

has stated its intention to fully separate Liberty Global and LiLAC in the future.

Mondelēz International Inc. (MDLZ – $43.08 – NASDAQ), headquartered in Deerfield, Illinois, is the renamed

Kraft Foods Inc. following the tax-free spin-off to shareholders of the North American grocery business on

October 1, 2012. Following the contribution of coffee into a new joint venture, nearly 85% of Mondelēz’s

$26 billion of revenue is derived from snacking, including leading brands such as Oreo, LU and Ritz biscuits,

Trident gum, and Cadbury and Milka chocolates. On July 2, 2015 Mondelēz combined its coffee business with

D.E Master Blenders 1753 to form a new coffee company, Jacobs Douwe Egberts. Subsequently, MDLZ

exchanged part of its stake in this coffee joint venture for 24% ownership in Keurig Green Mountain, which was

acquired by an investor group led by JAB Holding Co. in March 2016. This narrows the company’s product focus,

as only 15% of revenue will be outside snacks — mostly Tang beverages and other products including

Philadelphia cream cheese, which management may look to divest in the future as it executes on its plan to

accelerate growth and improve margins in the faster growing snack business.

Navistar International Corp. (NAV – $24.62 – NYSE), based in Lisle, Illinois, manufactures Class 4-8 trucks,

buses, and defense vehicles, as well as diesel engines and parts for the commercial trucking industry. NFC, a

wholly owned subsidiary, provides financing of products sold by the company’s truck segment. In September,

Navistar and Volkswagen (VW) Truck & Bus announced a long anticipated strategic alliance, in which the two

truck manufacturers would share technology and purchasing efforts in exchange for VW taking a $256 million

stake (16.6%) in Navistar. The deal, which closed on March 1, 2016, confirms our thesis that NAV would

6

eventually be targeted by a larger global capital equipment manufacturer. We believe this initial investment

should lead to an eventual full purchase in the years ahead.

Rollins Inc. (ROL – $37.13 – NYSE) provides pest control services to nearly two million residential and

commercial customers throughout North America primarily under the Orkin and Western Pest brand names. Its

services are critical to homeowners and commercial establishments alike, in both expansionary and

recessionary times. The company has benefited from growth in the commercial service area and mosquito and

bed bug treatments. At the same time, the company has controlled costs through more efficient scheduling and

routing. Rollins has been taking advantage of its strong balance sheet to make tuck-in acquisitions. It has also

begun franchising more operations outside the U.S. Founded in 1901, Rollins is majority owned by members of

the Rollins family.

Viacom Inc. (VIA – $48.75 – NASDAQ) is a pure-play content company that owns a global stable of cable

networks, including MTV, Nickelodeon, Comedy Central, VH1, BET, and the Paramount movie studio. Viacom’s

cable networks generate revenue from advertising sales, fixed monthly subscriber fees, and ancillary revenue

from toy licensing, etc. We believe a low valuation and M&A potential outweigh the secular risks of cord-cutting.

Conclusion

While optimism is on the rise, we anticipate continued volatility in markets due to politics, monetary policy,

or other external factors. We believe our bottom-up process of seeking high quality companies trading at a

discount to Private Market Value – the price an informed industrialist would pay to own an entire business – is

as timely as ever. With M&A activity increasing, we expect industry consolidation to be an important catalyst for

stock performance in coming quarters.

April 13, 2017

Top Ten Holdings

March 31, 2017

Rollins Inc.

Honeywell International Inc.

American Express Co.

MasterCard Inc.

Berkshire Hathaway Inc.

Swedish Match AB

Deere & Co.

Curtis-Wright Corp.

Ametek Inc.

Idex Corp.

7

Note: The views expressed in this Shareholder Commentary reflect those of the Portfolio Managers only through

the end of the period stated in this Shareholder Commentary. The Portfolio Managers’ views are subject to

change at any time based on market and other conditions. The information in this Shareholder Commentary

represents the opinions of the individual Portfolio Managers and is not intended to be a forecast of future events,

a guarantee of future results, or investment advice. Views expressed are those of the Portfolio Managers and

may differ from those of other portfolio managers or of the Firm as a whole. This Shareholder Commentary does

not constitute an offer of any transaction in any securities. Any recommendation contained herein may not be

suitable for all investors. Information contained in this Shareholder Commentary has been obtained from

sources we believe to be reliable, but cannot be guaranteed. Beneficial ownership of shares held in the Fund by

Mr. Gabelli and various entities he is deemed to control are disclosed in the Fund’s annual proxy statement.

10% Distribution Policy for Common Stockholders

The Board of Directors of the Fund (the “Board”) has reaffirmed the continuation of the Fund’s

10% distribution policy. Pursuant to its distribution policy, the Fund paid a $0.15 per share cash distribution on

March 24, 2017 to common stockholders of record on March 17, 2017.

The Fund intends to pay a quarterly distribution of an amount determined each quarter by the Board. Under

the Fund’s current distribution policy, the Fund intends to pay a minimum annual distribution of 10% of the

average net asset value of the Fund within a calendar year or an amount sufficient to satisfy the minimum

distribution requirements of the Internal Revenue Code, whichever is greater. The average net asset value of

the Fund is based on the average net asset values as of the last day of the four preceding calendar quarters.

Each quarter, the Board reviews the amount of any potential distribution from the income, capital gain, or

capital available. The Board will continue to monitor the Fund’s distribution level, taking into consideration the

Fund’s net asset value and the financial market environment. The Fund’s distribution policy is subject to

modification by the Board at any time. The distribution rate should not be considered the dividend yield or total

return on an investment in the Fund.

If the Fund does not generate sufficient earnings (dividends and interest income and realized net capital

gain) equal to or in excess of the aggregate distributions paid by the Fund in a given year, then the amount

distributed in excess of the Fund’s earnings would be deemed a return of capital. Since this would be considered

a return of a portion of a shareholder’s original investment, it is generally not taxable and is treated as a reduction

in the shareholder’s cost basis. Despite the challenges of the extra recordkeeping, a distribution that

incorporates a return of capital serves as a smoothing mechanism resulting in a more stable and consistent cash

flow available to shareholders.

Long term capital gains, qualified dividend income, ordinary income, and paid-in capital, if any, will be

allocated on a pro-rata basis to all distributions to common shareholders for the year. Based on the accounting

records of the Fund currently available, the current distribution paid to common shareholders in 2017 would

include approximately 100% from paid-in capital on a book basis. The estimated components of each distribution

8

are updated and provided to shareholders of record in a notice accompanying the distribution and are available

on our website (www.gabelli.com). The final determination of the sources of all distributions in 2017 will be made

after year end and can vary from the quarterly estimates. All shareholders with taxable accounts will receive

written notification regarding the components and tax treatment for all 2017 distributions in early 2018 via Form

1099-DIV.

Series C and Series E Auction Rate Cumulative Preferred Stock

During the first quarter of 2017, the dividend rates for the Series C and Series E Auction Rate Cumulative

Preferred Stock ranged from 0.963% to 1.593% and 1.085% to 1.593%, respectively. Dividend rates for the

Series C and Series E Preferred Shares may be reset every seven days based on the results of an auction.

Since February 2008, the number of Series C and Series E Preferred Shares subject to bid orders by potential

holders has been less than the number of sell orders. Therefore the weekly auctions have failed, and the

holders have not been able to sell any or all of the Series C and Series E Preferred Shares for which they

submitted sell orders. The dividend rate since then has been the maximum rate. At March 31, 2017, the

maximum rate was 175% of the “AA” Financial Composite Commercial Paper Rate and the Series C

and Series E Preferred Shares are rated “A1” by Moody’s Investors Service and “AA” by Fitch Ratings. The

Series C and Series E Preferred Shares do not trade on an exchange. The Fund was authorized to issue 5,200

Series C Preferred Shares on June 27, 2002 and 2,000 Series E Preferred Shares on October 7, 2003 at

$25,000 per share. As of March 31, 2017, 2,880 and 1,120 Series C and Series E Preferred Shares,

respectively, were outstanding.

5.875% Series D Cumulative Preferred Stock

The Fund’s 5.875% Series D Cumulative Preferred Stock paid a $0.3671875 per share cash distribution

on March 27, 2017 to preferred shareholders of record on March 20, 2017. The Series D Preferred Shares,

which trade on the NYSE under the symbol “GAB Pr D”, are rated “A1” by Moody’s Investors Service and have

an annual dividend rate of $1.46875 per share. The Series D Preferred Shares were issued on October 7, 2003,

at $25.00 per share and pay distributions quarterly. After five years of call protection, the Series D Preferred

Shares became callable at any time at the liquidation value of $25.00 per share plus accrued dividends. The

next distribution is scheduled for June 2017.

The Fund is authorized to purchase its Series D Preferred Shares in the open market from time to

time when such shares are trading at a discount to the liquidation value of $25.00 per share. In total through

March 31, 2017, the Fund has repurchased and retired 156,140 Series D Preferred Shares in the open market

under this share repurchase authorization. The Fund did not repurchase any Series D Preferred Shares during

the first quarter of 2017.

9

Series G Cumulative Preferred Stock

The Fund’s Series G Cumulative Preferred Stock paid a $0.3125 per share cash distribution on

March 27, 2017 to preferred shareholders of record on March 20, 2017. The Series G Preferred Shares, which

trade on the NYSE under the symbol “GAB Pr G”, were issued on August 1, 2012 at $25.00 per share. The

Series G Preferred Shares pay distributions quarterly and for the first twelve months beginning from the date

of issuance (August 1, 2012) had an annual dividend rate of 6.00%, and thereafter an annual dividend rate of

5.00% for all future dividend periods. The Series G Preferred Shares will be callable at any time at the

liquidation value of $25.00 per share plus accrued dividends following the expiration of the five year call

protection on August 1, 2017. The next distribution is scheduled for June 2017.

The Fund is authorized to purchase its Series G Preferred Shares in the open market from time to time

when such shares are trading at a discount to the liquidation value of $25.00 per share. In total through March

31, 2017, the Fund has repurchased and retired 36,728 Series G Preferred Shares in the open market under

this share repurchase authorization, 9,905 of which were repurchased in the first quarter of 2017.

Series H Cumulative Preferred Stock

The Fund’s Series H Cumulative Preferred Stock paid a $0.3125 per share cash distribution on

March 27, 2017 to preferred shareholders of record on March 20, 2017. The Series H Preferred Shares, which

trade on the NYSE under the symbol “GAB Pr H”, are rated “A1” by Moody’s Investors Service and have an

annual dividend rate of $1.25 per share. The Series H Preferred Shares were issued on September 28, 2012,

at $25.00 per share and pay distributions quarterly. The Series H Preferred Shares will be callable at any time

at the liquidation value of $25.00 per share plus accrued dividends following the expiration of the five year call

protection on September 28, 2017. The next distribution is scheduled for June 2017.

The Fund is authorized to purchase its Series H Preferred Shares in the open market from time to

time when such shares are trading at a discount to the liquidation value of $25.00 per share. In total through

March 31, 2017, the Fund has repurchased and retired 27,127 Series H Preferred Shares in the open market

under this share repurchase authorization, 6,900 of which were repurchased in the first quarter of 2017.

5.450% Series J Cumulative Preferred Stock

The Fund’s Series J Cumulative Preferred Stock paid a $0.340625 per share cash distribution on

March 27, 2017, to preferred shareholders of record on March 20, 2017. The Series J Preferred Shares, which

trade on the NYSE under the symbol “GAB Pr J”, are rated “A1” by Moody’s Investors Service and have an

annual dividend rate of $1.3625 per share. The Series J Preferred Shares were issued on March 31, 2016, at

$25.00 per share and pay distributions quarterly. The Series J Preferred Shares will be callable at any time at

the liquidation value of $25.00 per share plus accrued dividends following the expiration of the five year call

protection on March 31, 2021. The next distribution is scheduled for June 2017.

10

The Fund is authorized to purchase its Series J Preferred Shares in the open market from time to time when

such shares are trading at a discount to the liquidation value of $25.00 per share. Through March 31, 2017, the

Fund has not repurchased any Series J Preferred Shares in the open market under this share repurchase

authorization.

The Board shares the view of Gabelli Funds, LLC (the “Investment Adviser”’) that the issuance of the

Preferred Stock is designed to benefit the common shareholders. To the extent that the Fund earns in excess

of the dividend rate on the Preferred Stock, additional value will thereby be created for its common

shareholders. Long term capital gains, qualified dividend income, and ordinary income, if any, will be allocated

on a pro-rata basis to all distributions to preferred shareholders for the year. Based on the accounting records

of the Fund currently available, the current distribution paid to preferred shareholders represents approximately

33% from net investment income, 50% from net capital gains, and 17% from paid-in capital on a book basis.

The estimated components of each distribution are updated and provided to shareholders of record in a notice

accompanying the distribution and are available on our website (www.gabelli.com). The final determination of

the sources of all distributions in 2017 will be made after year end and can vary from the quarterly estimates.

All shareholders with taxable accounts will receive written notification regarding the components and tax

treatment for all 2017 distributions in early 2018 via Form 1099-DIV.

Tax Treatment of Distributions to Common and Preferred Shareholders

All or part of the distributions may be treated as long term capital gain or qualified dividend income (or a

combination of both) for individuals, each subject to the maximum federal income tax rate, which is currently

20% in taxable accounts for individuals. In addition, certain U.S. shareholders who are individuals, estates, or

trusts and whose income exceeds certain thresholds will be required to pay a 3.8% Medicare surcharge on their

“net investment income,” which includes dividends received from the Fund and capital gains from the sale or

other disposition of shares of the Fund.

www.gabelli.com

Please visit us on the Internet. Our homepage at www.gabelli.com contains information about GAMCO

Investors, Inc., the Gabelli/GAMCO Closed-End Funds and Mutual Funds, IRAs, 401(k)s, current and

historical quarterly reports, closing prices, and other current news. We welcome your comments and

questions via e-mail at [email protected].

You may sign up for our e-mail alerts at www.gabelli.com and receive notice of quarterly report availability,

news events, media sightings, and mutual fund prices and performance.

e-delivery

We are pleased to offer electronic delivery of Gabelli fund documents. Shareholders of our closed-end

funds can now elect to receive e-mail announcements regarding available materials, including shareholder

commentaries and Fund reports. For more information or to register for e-delivery, please visit our website at

www.gabelli.com.Tax Treatment of Distributions to Common and Preferred Shareholders.

11

THE GABELLI EQUITY TRUST INC. One Corporate CenterRye, NY 10580-1422

Notice is hereby given in accordance with Section 23(c) of the Investment Company Act of 1940, as amended, that theFund may from time to time purchase shares of its common stock in the open market when the Fund’s shares are tradingat a discount of 10% or more from the net asset value of the shares. The Fund may also from time to time purchase sharesof its preferred stock in the open market when the preferred shares are trading at a discount to the liquidation value.

The Net Asset Value per share appears in the Publicly Traded Funds column, under the heading “General Equity Funds,”in Monday’s The Wall Street Journal. It is also listed in Barron’s Mutual Funds/Closed End Funds section under the heading“General Equity Funds.”

The Net Asset Value per share may be obtained each day by calling (914) 921-5070 or visiting www.gabelli.com.

The Nasdaq symbol for the Net Asset Value per share is “XGABX.”

This report is printed on recycled paper.

Portfolio Management Team Biographies

Mario J. Gabelli, CFA, is Chairman, Chief Executive Officer, and Chief Investment Officer –Value Portfolios ofGAMCO Investors, Inc. that he founded in 1977, and Chief Investment Officer – Value Portfolios of Gabelli Funds,LLC and GAMCO Asset Management Inc. He is also Executive Chairman of the Board of Directors of AssociatedCapital Group, Inc. Mr. Gabelli is a summa cum laude graduate of Fordham University and holds an MBA degreefrom Columbia Business School, and Honorary Doctorates from Fordham University and Roger Williams University.

Christopher J. Marangi joined Gabelli in 2003 as a research analyst. Currently he is a Managing Director and Co-Chief Investment Officer for GAMCO Investors, Inc.’s Value team. In addition, he currently serves as a portfoliomanager of Gabelli Funds, LLC and manages several funds within the Gabelli/GAMCO Funds Complex. Mr. Marangigraduated magna cum laude and Phi Beta Kappa with a BA in Political Economy from Williams College and holdsan MBA with honors from Columbia Business School.

Kevin V. Dreyer joined Gabelli in 2005 as a research analyst covering companies within the consumer sector.Currently he is a Managing Director and Co-Chief Investment Officer for GAMCO Investors, Inc.’s Value team. Inaddition, he currently serves as a portfolio manager of Gabelli Funds, LLC and manages several funds within theGabelli/GAMCO Funds Complex. Mr. Dreyer received a BSE from the University of Pennsylvania and an MBA fromColumbia Business School.

Robert D. Leininger, CFA, joined GAMCO Investors, Inc. in 1993 as an equity analyst. Subsequently, he was apartner and portfolio manager at Rorer Asset Management before rejoining GAMCO in 2010 where he currentlyserves as a portfolio manager of Gabelli Funds, LLC. Mr. Leininger is a magna cum laude graduate of AmherstCollege with a degree in Economics and holds an MBA from the Wharton School at the University of Pennsylvania.

Daniel M. Miller currently serves as a portfolio manager of Gabelli Funds, LLC. He is also a Managing Director ofGAMCO Investors, Inc. Mr. Miller graduated magna cum laude with a degree in finance from the University of Miamiin Coral Gables, Florida.

We have separated the portfolio managers’ commentary from the financial statements and investment portfolio due tocorporate governance regulations stipulated by the Sarbanes-Oxley Act of 2002. We have done this to ensure that thecontent of the portfolio managers’ commentary is unrestricted. Both the commentary and the financial statements,including the portfolio of investments, will be available on our website at www.gabelli.com.

THE GABELLI EQUITY TRUST INC.One Corporate CenterRye, NY 10580-1422

t 800-GABELLI (800-422-3554)f 914-921-5118e [email protected]

GABELL I .COM

DIRECTORS

Mario J. Gabelli, CFAChairman &Chief Executive Officer,GAMCO Investors Inc.Executive Chairman,Associated Capital Group Inc.

Anthony J. ColavitaPresident, Anthony J. Colavita, P.C.

James P. ConnFormer Managing Director &Chief Investment Officer,Financial Security AssuranceHoldings Ltd.

Frank J. Fahrenkopf, Jr.Former President & Chief Executive Officer,American Gaming Association

Michael J. FerrantinoChief Executive Officer,InterEx Inc.

Arthur V. FerraraFormer Chairman & Chief Executive Officer,Guardian Life Insurance Company of America

William F. HeitmannFormer Senior Vice President of Finance,Verizon Communications, Inc.

Salvatore J. ZizzaChairman, Zizza & Associates Corp.

OFFICERS

Bruce N. AlpertPresident

Andrea R. MangoSecretary & Vice President

Agnes MulladyTreasurer & Principal Financial &Accounting Officer

Richard J. WalzChief Compliance Officer

Carter W. AustinVice President

Molly A.F. MarionVice President & Ombudsman

David I. SchachterVice President

INVESTMENT ADVISER

Gabelli Funds, LLCOne Corporate CenterRye, New York 10580-1422

CUSTODIAN

The Bank of New York Mellon

COUNSEL

Willkie Farr & Gallagher LLP

TRANSFER AGENT ANDREGISTRAR

Computershare Trust Company, N.A.

THEGABELL IEQUITYTRUST INC.

Shareholder CommentaryMarch 31, 2017

GAB Mar/2017

GAB

(Y)our Portfolio Management Team

Mario J. Gabelli, CFAChief Investment Officer

Christopher J. MarangiCo-Chief Investment Officer

BA, Williams CollegeMBA, ColumbiaBusiness School

Kevin V. DreyerCo-Chief Investment Officer

BSE, University ofPennsylvania

MBA, ColumbiaBusiness School

Robert D. Leininger, CFAPortfolio Manager

BA, Amherst CollegeMBA, Wharton School,

University of Pennsylvania

Daniel M. MillerManaging Director,GAMCO Investors

BS, University of Miami

To Our Shareholders,For the quarter ended March 31, 2017, the net asset value (“NAV”) total return of The Gabelli Equity Trust Inc. (the

“Fund”) was 6.7%, compared with total returns of 6.1% and 5.0% for the Standard & Poor’s (“S&P”) 500 Index and the DowJones Industrial Average, respectively. The total return for the Fund’s publicly traded shares was 10.9%. The Fund’s NAV pershare was $6.08, while the price of the publicly traded shares closed at $5.97 on the New York Stock Exchange (“NYSE”). Seebelow for additional performance information.

Enclosed is the schedule of investments as of March 31, 2017.

Comparative Results

Average Annual Returns through March 31, 2017 (a) (Unaudited)

Quarter 1 Year 5 Year 10 Year 15 Year 20 Year 25 Year

SinceInception(08/21/86)

Gabelli Equity TrustNAV Total Return (b) . . . . . . . . . . . . . . . . 6.67% 17.26% 12.27% 7.29% 9.10% 9.82% 10.29% 10.77%Investment Total Return (c) . . . . . . . . . . . 10.88 22.06 11.95 6.84 7.42 9.76 10.11 10.47

S&P 500 Index . . . . . . . . . . . . . . . . . . . . . . 6.07 17.17 13.30 7.51 7.09 7.86 9.62 10.05(d)Dow Jones Industrial Average . . . . . . . . . . . 4.98 19.56 12.04 8.03 7.31 8.34 10.27 10.95(d)Nasdaq Composite Index. . . . . . . . . . . . . . . 10.13 22.93 15.38 10.60 9.23 9.16 9.55 9.70(e)(a) Returns represent past performance and do not guarantee future results. Investment returns and the principal value of an investment will fluctuate.

When shares are sold, they may be worth more or less than their original cost. Current performance may be lower or higher than the performancedata presented. Visit www.gabelli.com for performance information as of the most recent month end. Performance returns for periods of less thanone year are not annualized. Investors should carefully consider the investment objectives, risks, charges, and expenses of the Fund beforeinvesting. The Dow Jones Industrial Average is an unmanaged index of 30 large capitalization stocks. The S&P 500 and the Nasdaq CompositeIndices are unmanaged indicators of stock market performance. Dividends are considered reinvested except for the Nasdaq Composite Index. Youcannot invest directly in an index.

(b) Total returns and average annual returns reflect changes in the NAV per share, reinvestment of distributions at NAV on the ex-dividend date,adjustments for rights offerings, spin-offs, and taxes paid on undistributed long term capital gains and are net of expenses. Since inception return isbased on an initial NAV of $9.34.

(c) Total returns and average annual returns reflect changes in closing market values on the NYSE, reinvestment of distributions, and adjustments forrights offerings, spin-offs, and taxes paid on undistributed long term capital gains. Since inception return is based on an initial offering price of$10.00.

(d) From August 31, 1986, the date closest to the Fund’s inception for which data is available.(e) From September 30, 1986, the date closest to the Fund’s inception for which data is available.

The Gabelli Equity Trust Inc.First Quarter Report — March 31, 2017

Shares

Ownership atMarch 31,

2017NET PURCHASESCommon StocksAdvance Auto Parts Inc. . . . . . . . . . . . . . . . 5,000 10,000Akorn Inc. . . . . . . . . . . . . . . . . . . . . . . . . . 21,483 71,098Armstrong Flooring Inc. . . . . . . . . . . . . . . . 120,000 162,500Ascena Retail Group Inc. . . . . . . . . . . . . . . . 130,000 130,000BioScrip Inc.. . . . . . . . . . . . . . . . . . . . . . . . 95,278 2,936,551Bioverativ Inc.(a) . . . . . . . . . . . . . . . . . . . . 3,500 3,500Blackhawk Network Holdings Inc. . . . . . . . . 16,300 32,600Bristol-Myers Squibb Co. . . . . . . . . . . . . . . 20,000 96,300Builders FirstSource Inc. . . . . . . . . . . . . . . . 25,000 25,000Comcast Corp., Cl. A(b). . . . . . . . . . . . . . . . 80,000 160,000Contax Participacoes SA . . . . . . . . . . . . . . . 354 2,004Daseke Inc. . . . . . . . . . . . . . . . . . . . . . . . . 15,000 15,000Donnelley Financial Solutions, Inc. . . . . . . . . 10,000 10,000Edgewell Personal Care Co. . . . . . . . . . . . . . 5,000 196,000Enbridge Inc. . . . . . . . . . . . . . . . . . . . . . . . 98,400 98,400Endo International plc . . . . . . . . . . . . . . . . . 784 55,784Fiesta Restaurant Group Inc. . . . . . . . . . . . . 25,000 25,000Freeport-McMoRan Inc. . . . . . . . . . . . . . . . 30,000 80,000Griffon Corp.(c) . . . . . . . . . . . . . . . . . . . . . 39,105 65,478H&R Block Inc. . . . . . . . . . . . . . . . . . . . . . . 2,000 68,000Hertz Global Holdings Inc. . . . . . . . . . . . . . . 20,000 320,000Hewlett Packard Enterprise Co. . . . . . . . . . . 13,000 35,000Incyte Corp. . . . . . . . . . . . . . . . . . . . . . . . . 3,000 3,000Inventure Foods Inc. . . . . . . . . . . . . . . . . . . 180,492 363,839J.C. Penney Co. Inc. . . . . . . . . . . . . . . . . . . 50,000 100,000Jason Industries Inc.. . . . . . . . . . . . . . . . . . 122,500 365,385Live Nation Entertainment Inc. . . . . . . . . . . . 10,000 10,000Loral Space & Communications Inc. . . . . . . 1,000 22,000Macquarie Infrastructure Corp. . . . . . . . . . . 2,000 25,300MGM Resorts International . . . . . . . . . . . . . 58,425 133,425Marathon Petroleum Corp. . . . . . . . . . . . . . 5,000 22,000Mondelez International Inc., Cl. A. . . . . . . . . 7,000 330,000Mueller Industries Inc. . . . . . . . . . . . . . . . . 159,900 200,000Mueller Water Products Inc., Cl. A . . . . . . . . 6,000 6,000Newell Brands Inc. . . . . . . . . . . . . . . . . . . . 21,500 21,500Nexstar Media Group Inc.(d) . . . . . . . . . . . . 17,376 17,376Och-Ziff Capital Management Group LLC,

Cl. A . . . . . . . . . . . . . . . . . . . . . . . . . . . . 110,000 160,000Pandora Media Inc. . . . . . . . . . . . . . . . . . . . 16,000 36,000Roper Technologies Inc. . . . . . . . . . . . . . . . 2,250 2,250Stericycle Inc.. . . . . . . . . . . . . . . . . . . . . . . 3,000 7,000The Central Europe, Russia, and Turkey

Fund Inc.(e) . . . . . . . . . . . . . . . . . . . . . . 1,333 90,302The Madison Square Garden Co., Cl. A . . . . . 999 103,200The New Germany Fund Inc.(f) . . . . . . . . . . 7,784 143,158Tootsie Roll Industries Inc.(g) . . . . . . . . . . . 3,868 132,809Twitter Inc. . . . . . . . . . . . . . . . . . . . . . . . . . 5,000 55,000Waddell & Reed Financial Inc., Cl. A. . . . . . . 10,000 130,000Welbilt Inc. . . . . . . . . . . . . . . . . . . . . . . . . . 4,000 4,000Zayo Group Holdings Inc. . . . . . . . . . . . . . . 4,000 19,000

Shares

Ownership atMarch 31,

2017RightsMedia General Inc., expire 12/31/17(d). . . . . 139,123 139,123WarrantsDaseke Inc., expire 09/11/20 . . . . . . . . . . . . 15,000 15,000NET SALESCommon StocksAdient plc . . . . . . . . . . . . . . . . . . . . . . . . . . (1) 31,349Alere Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . (25,000) 40,000Allergan plc . . . . . . . . . . . . . . . . . . . . . . . . (4,500) 10,000AMC Networks Inc., Cl. A . . . . . . . . . . . . . . (4,000) 253,600AMETEK Inc. . . . . . . . . . . . . . . . . . . . . . . . (2,000) 418,000Apple Inc.. . . . . . . . . . . . . . . . . . . . . . . . . . (1,000) 10,000Ascent Capital Group Inc., Cl. A . . . . . . . . . . (3,000) 7,000Blucora Inc. . . . . . . . . . . . . . . . . . . . . . . . . (32,500) 32,500Cable One Inc. . . . . . . . . . . . . . . . . . . . . . . (300) 1,300Calamos Asset Management Inc., Cl. A . . . . (10,000) -Canadian Solar Inc. . . . . . . . . . . . . . . . . . . . (40,000) 30,000CBS Corp.,Cl. A. . . . . . . . . . . . . . . . . . . . . . (4,199) 243,300CLARCOR Inc. . . . . . . . . . . . . . . . . . . . . . . (96,900) -Contax Participacoes SA . . . . . . . . . . . . . . . (354) -CST Brands Inc. . . . . . . . . . . . . . . . . . . . . . (10,000) 50,500DigitalGlobe Inc. . . . . . . . . . . . . . . . . . . . . . (4,000) 16,000Dr Pepper Snapple Group Inc. . . . . . . . . . . . (3,000) 82,400EchoStar Corp., Cl. A. . . . . . . . . . . . . . . . . . (19,848) 50,200Energizer Holdings Inc. . . . . . . . . . . . . . . . . (22,000) 146,000Ferro Corp. . . . . . . . . . . . . . . . . . . . . . . . . . (15,000) 442,000General Motors Co. . . . . . . . . . . . . . . . . . . . (4,000) 91,746Gogo Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . (55,000) 135,000Grupo Televisa SAB. . . . . . . . . . . . . . . . . . . (5,000) 533,000H.B. Fuller Co. . . . . . . . . . . . . . . . . . . . . . . (4,000) 35,000Hennessy Capital Acquisition Corp. II . . . . . . (20,000) -Honeywell International Inc. . . . . . . . . . . . . (3,000) 326,000Internap Corp. . . . . . . . . . . . . . . . . . . . . . . (437,500) 562,500Liberty Expedia Holdings Inc., Cl. A . . . . . . . (2,000) 24,642Liberty Media Corp.-Liberty SiriusXM, Cl. A . (2,000) 75,000Marriott International, Inc., Cl. A . . . . . . . . . (8,200) 15,000Media General Inc.(d) . . . . . . . . . . . . . . . . . (139,123) -Meredith Corp. . . . . . . . . . . . . . . . . . . . . . . (14,000) 82,300Methanex Corp. . . . . . . . . . . . . . . . . . . . . . (15,000) 5,000NCR Corp. . . . . . . . . . . . . . . . . . . . . . . . . . (11,000) 21,000Penske Automotive Group Inc.. . . . . . . . . . . (3,000) 12,000Quinpario Acquisition Corp. 2 . . . . . . . . . . . (4,547) 10,453Rolls-Royce Holdings plc, Cl. C . . . . . . . . . . (55,614,000) -Spectra Energy Corp. . . . . . . . . . . . . . . . . . (100,000) -The Boeing Co. . . . . . . . . . . . . . . . . . . . . . . (12,500) 42,500The Interpublic Group of Companies Inc. . . . (4,000) 290,000Time Warner Inc. . . . . . . . . . . . . . . . . . . . . (4,000) 200,800Vivendi SA . . . . . . . . . . . . . . . . . . . . . . . . . (25,000) 245,000Xylem Inc. . . . . . . . . . . . . . . . . . . . . . . . . . (4,000) 270,000

The Gabelli Equity Trust Inc.Portfolio Changes — Quarter Ended March 31, 2017 (Unaudited)

See accompanying notes to schedule of investments.

2

Shares

Ownership atMarch 31,

2017Convertible Corporate BondsGriffon Corp. . . . . . . . . . . . . . . . . . . . . . . . (2,000,000) -

(a) Spin-off - 0.5 shares of Bioverativ Inc. for every 1 share of Biogen Inc. held.1,100 shares were sold after the spin-off.

(b) Stock Split - 2 shares for every 1 share held.(c) Conversion - 19.5528 new common Shares and $1.250 cash for each $1,000

Principal amount of bonds held.(d) Merger - 0.1249 shares of Nexstar Media Group Inc. and 1 Media General

Inc. Right for every 1 share held of Media General Inc. held.(e) Stock dividend - 0.015 Shares for every 1 share held.(f) Stock dividend - 0.0575 shares for every 1 share held.(g) Stock dividend - 0.03 new shares for every 1 share held.

The Gabelli Equity Trust Inc.Portfolio Changes (Continued) — Quarter Ended March 31, 2017 (Unaudited)

See accompanying notes to schedule of investments.

3

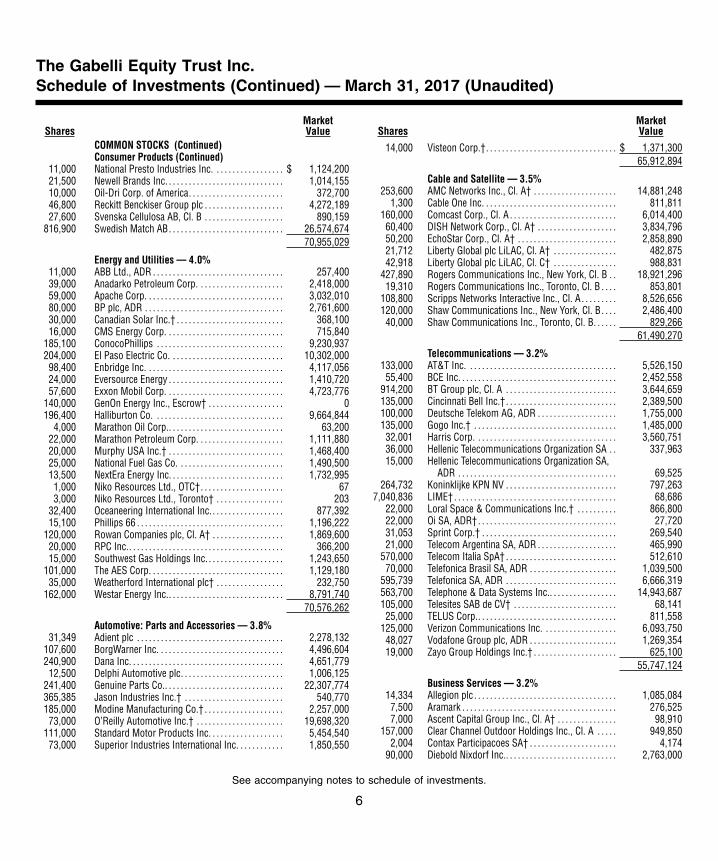

SharesMarketValue

COMMON STOCKS — 98.2%Food and Beverage — 11.8%

3,000 Ajinomoto Co. Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 59,189106,200 Brown-Forman Corp., Cl. A. . . . . . . . . . . . . . . . . . . . . 4,998,83435,950 Brown-Forman Corp., Cl. B. . . . . . . . . . . . . . . . . . . . . 1,660,17163,800 Campbell Soup Co. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,651,91265,000 Chr. Hansen Holding A/S . . . . . . . . . . . . . . . . . . . . . . . 4,172,02015,000 Coca-Cola European Partners plc . . . . . . . . . . . . . . . 565,350

135,000 Conagra Brands Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . 5,445,90030,000 Constellation Brands Inc., Cl. A. . . . . . . . . . . . . . . . . 4,862,10018,000 Crimson Wine Group Ltd.† . . . . . . . . . . . . . . . . . . . . . 180,000

201,500 Danone SA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13,705,904652,800 Davide Campari-Milano SpA. . . . . . . . . . . . . . . . . . . . 7,569,967171,000 Diageo plc, ADR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19,764,18082,400 Dr Pepper Snapple Group Inc.. . . . . . . . . . . . . . . . . . 8,068,60880,000 Flowers Foods Inc.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,552,80076,200 Fomento Economico Mexicano SAB de CV,

ADR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,745,22455,000 General Mills Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,245,550

1,848,400 Grupo Bimbo SAB de CV, Cl. A . . . . . . . . . . . . . . . . . 4,595,76341,300 Heineken NV. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,515,90611,000 Ingredion Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,324,730

363,839 Inventure Foods Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . 1,608,168105,000 ITO EN Ltd. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,833,87227,800 Kellogg Co. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,018,55864,000 Kerry Group plc, Cl. A . . . . . . . . . . . . . . . . . . . . . . . . . . 5,064,67086,666 Lamb Weston Holdings Inc. . . . . . . . . . . . . . . . . . . . . 3,645,1729,700 LVMH Moet Hennessy Louis Vuitton SE . . . . . . . . 2,130,134

45,000 Maple Leaf Foods Inc.. . . . . . . . . . . . . . . . . . . . . . . . . . 1,092,304330,000 Mondelez International Inc., Cl. A. . . . . . . . . . . . . . . 14,216,40070,000 Morinaga Milk Industry Co. Ltd. . . . . . . . . . . . . . . . . 519,35741,000 Nestlé SA. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,145,660

190,000 PepsiCo Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21,253,40039,200 Pernod Ricard SA. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,637,69226,000 Post Holdings Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,275,52040,000 Remy Cointreau SA . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,916,02155,000 The Kraft Heinz Co.. . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,994,550

104,600 The Coca-Cola Co. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,439,22432,000 The Hain Celestial Group Inc.† . . . . . . . . . . . . . . . . . 1,190,4003,000 The J.M. Smucker Co. . . . . . . . . . . . . . . . . . . . . . . . . . 393,240

57,000 The WhiteWave Foods Co.† . . . . . . . . . . . . . . . . . . . . 3,200,550132,809 Tootsie Roll Industries Inc. . . . . . . . . . . . . . . . . . . . . . 4,960,42550,000 Tyson Foods Inc., Cl. A. . . . . . . . . . . . . . . . . . . . . . . . . 3,085,500

341,000 Yakult Honsha Co. Ltd. . . . . . . . . . . . . . . . . . . . . . . . . . 18,929,130206,234,055

Financial Services — 9.6%417,000 American Express Co.(a) . . . . . . . . . . . . . . . . . . . . . . . 32,988,87025,000 American International Group Inc. . . . . . . . . . . . . . . 1,560,75014,520 Argo Group International Holdings Ltd. . . . . . . . . . 984,45672,000 Banco Santander SA, ADR . . . . . . . . . . . . . . . . . . . . . 437,040

116 Berkshire Hathaway Inc., Cl. A† . . . . . . . . . . . . . . . . 28,982,60032,600 Blackhawk Network Holdings Inc.† . . . . . . . . . . . . . 1,323,560

SharesMarketValue

12,800 CIT Group Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 549,50488,000 Citigroup Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5,264,1609,000 Cullen/Frost Bankers Inc.. . . . . . . . . . . . . . . . . . . . . . . 800,730

16,000 Deutsche Bank AG†. . . . . . . . . . . . . . . . . . . . . . . . . . . . 274,5608,000 Financial Engines Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . 348,400

50,000 Fortress Investment Group LLC, Cl. A . . . . . . . . . . 397,50068,000 H&R Block Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,581,00040,000 Interactive Brokers Group Inc., Cl. A . . . . . . . . . . . . 1,388,800

340,100 Janus Capital Group Inc. . . . . . . . . . . . . . . . . . . . . . . . 4,489,32061,400 JPMorgan Chase & Co. . . . . . . . . . . . . . . . . . . . . . . . . 5,393,37629,800 Kinnevik AB, Cl. A. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 888,614

125,000 Legg Mason Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,513,75088,000 Leucadia National Corp. . . . . . . . . . . . . . . . . . . . . . . . . 2,288,00014,000 Loews Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 654,780

125,000 Marsh & McLennan Companies Inc. . . . . . . . . . . . . 9,236,2509,000 Moody’s Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,008,360

160,000 Och-Ziff Capital Management Group LLC, Cl. A. . 361,60020,000 PayPal Holdings Inc.†. . . . . . . . . . . . . . . . . . . . . . . . . . 860,40010,453 Quinpario Acquisition Corp. 2† . . . . . . . . . . . . . . . . . 109,391

105,300 S&P Global Inc.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13,766,922124,100 State Street Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9,879,60117,000 SunTrust Banks Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . 940,100

103,400 T. Rowe Price Group Inc.. . . . . . . . . . . . . . . . . . . . . . . 7,046,710210,500 The Bank of New York Mellon Corp. . . . . . . . . . . . . 9,941,91520,000 The Charles Schwab Corp. . . . . . . . . . . . . . . . . . . . . . 816,20012,300 The Dun & Bradstreet Corp. . . . . . . . . . . . . . . . . . . . . 1,327,66210,000 The PNC Financial Services Group Inc. . . . . . . . . . 1,202,40013,000 W. R. Berkley Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 918,190

130,000 Waddell & Reed Financial Inc., Cl. A . . . . . . . . . . . . 2,210,000235,000 Wells Fargo & Co. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13,080,100

167,815,571

Entertainment — 7.3%30,812 Charter Communications Inc., Cl. A† . . . . . . . . . . . 10,085,38441,600 Discovery Communications Inc., Cl. A† . . . . . . . . . 1,210,144

235,800 Discovery Communications Inc., Cl. C† . . . . . . . . . 6,675,498533,000 Grupo Televisa SAB, ADR . . . . . . . . . . . . . . . . . . . . . . 13,826,02010,700 Liberty Media Corp.-

Liberty Braves, Cl. A†. . . . . . . . . . . . . . . . . . . . . . . . 256,15873,758 Liberty Media Corp.-

Liberty Braves, Cl. C†. . . . . . . . . . . . . . . . . . . . . . . . 1,744,37748,641 Lions Gate Entertainment Corp., Cl. B† . . . . . . . . . 1,185,86710,000 Live Nation Entertainment Inc.† . . . . . . . . . . . . . . . . 303,70024,000 Pinnacle Entertainment Inc.† . . . . . . . . . . . . . . . . . . . 468,480

103,200 The Madison Square Garden Co, Cl. A† . . . . . . . . . 20,610,072200,800 Time Warner Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19,620,16840,000 Tokyo Broadcasting System Holdings Inc. . . . . . . 714,273

560,200 Twenty-First Century Fox Inc., Cl. A. . . . . . . . . . . . . 18,144,878370,000 Twenty-First Century Fox Inc., Cl. B. . . . . . . . . . . . . 11,758,60070,000 Universal Entertainment Corp.. . . . . . . . . . . . . . . . . . 2,238,390

279,521 Viacom Inc., Cl. A. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13,626,649

The Gabelli Equity Trust Inc.Schedule of Investments — March 31, 2017 (Unaudited)

See accompanying notes to schedule of investments.

4

SharesMarketValue

COMMON STOCKS (Continued)Entertainment (Continued)

245,000 Vivendi SA. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 4,763,410127,232,068

Equipment and Supplies — 5.7%418,000 AMETEK Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22,605,440

7,000 Amphenol Corp., Cl. A . . . . . . . . . . . . . . . . . . . . . . . . . 498,19094,000 CIRCOR International Inc. . . . . . . . . . . . . . . . . . . . . . . 5,587,360

337,800 Donaldson Co. Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15,376,656207,000 Flowserve Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10,022,94037,400 Franklin Electric Co. Inc. . . . . . . . . . . . . . . . . . . . . . . . 1,610,070

240,000 IDEX Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22,442,40043,000 Ingersoll-Rand plc . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,496,76040,100 Mueller Industries Inc. . . . . . . . . . . . . . . . . . . . . . . . . . 1,372,6236,000 Mueller Water Products Inc., Cl. A . . . . . . . . . . . . . . 70,920

13,000 Sealed Air Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 566,54045,000 Tenaris SA, ADR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,536,30010,000 The Greenbrier Companies Inc.. . . . . . . . . . . . . . . . . 431,0004,000 The Manitowoc Co. Inc.†. . . . . . . . . . . . . . . . . . . . . . . 22,800

80,000 The Timken Co. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,616,00059,600 The Weir Group plc . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,431,475

125,000 Watts Water Technologies Inc., Cl. A. . . . . . . . . . . . 7,793,7504,000 Welbilt Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78,520

98,559,744

Diversified Industrial — 4.9%500 Acuity Brands Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102,000

160,000 Ampco-Pittsburgh Corp. . . . . . . . . . . . . . . . . . . . . . . . 2,248,000173,100 Crane Co.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12,953,073153,000 General Electric Co. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,559,400132,000 Greif Inc., Cl. A . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7,271,88010,000 Greif Inc., Cl. B . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 653,00065,478 Griffon Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,614,033

326,000 Honeywell International Inc. . . . . . . . . . . . . . . . . . . . . 40,707,620117,000 ITT Inc.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,799,34011,000 Jardine Strategic Holdings Ltd. . . . . . . . . . . . . . . . . . 462,00040,000 Kennametal Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,569,20050,000 Myers Industries Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . 792,50085,000 Park-Ohio Holdings Corp. . . . . . . . . . . . . . . . . . . . . . . 3,055,7509,666 Rayonier Advanced Materials Inc. . . . . . . . . . . . . . . 130,008

30,000 Rexnord Corp.†. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 692,40015,000 ServiceMaster Global Holdings Inc.† . . . . . . . . . . . 626,25015,000 Sulzer AG. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,569,410

100,000 Toray Industries Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . 886,55312,000 Tredegar Corp.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 210,60046,000 Trinity Industries Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . 1,221,300

86,124,317

Health Care — 4.9%6,000 Agilent Technologies Inc.. . . . . . . . . . . . . . . . . . . . . . . 317,220

71,098 Akorn Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,712,04040,000 Alere Inc.†. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,589,200

SharesMarketValue

10,000 Allergan plc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 2,389,20034,000 Amgen Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5,578,38017,000 Baxter International Inc.. . . . . . . . . . . . . . . . . . . . . . . . 881,62010,000 Becton, Dickinson and Co. . . . . . . . . . . . . . . . . . . . . . 1,834,4009,200 Biogen Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,515,464

2,936,551 BioScrip Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,992,1373,500 Bioverativ Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 190,610

270,000 Boston Scientific Corp.† . . . . . . . . . . . . . . . . . . . . . . . 6,714,90096,300 Bristol-Myers Squibb Co. . . . . . . . . . . . . . . . . . . . . . . 5,236,79415,000 DaVita Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,019,55055,784 Endo International plc† . . . . . . . . . . . . . . . . . . . . . . . . 622,54920,000 Express Scripts Holding Co.† . . . . . . . . . . . . . . . . . . 1,318,20017,500 Globus Medical Inc., Cl. A†. . . . . . . . . . . . . . . . . . . . . 518,35028,000 Henry Schein Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,759,1603,000 Incyte Corp.† . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 401,010

46,800 Indivior plc . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 188,86537,000 Johnson & Johnson . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,608,35025,000 Mead Johnson Nutrition Co.. . . . . . . . . . . . . . . . . . . . 2,227,00010,000 Medtronic plc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 805,60095,200 Merck & Co. Inc.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,049,00884,000 Novartis AG, ADR. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,238,6801,500 Shire plc, ADR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 261,345

15,000 Teva Pharmaceutical Industries Ltd., ADR . . . . . . 481,35074,000 UnitedHealth Group Inc.. . . . . . . . . . . . . . . . . . . . . . . . 12,136,7404,000 Waters Corp.† . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 625,240

268,000 William Demant Holding A/S† . . . . . . . . . . . . . . . . . . 5,599,3468,600 Zimmer Biomet Holdings Inc. . . . . . . . . . . . . . . . . . . 1,050,146

35,000 Zoetis Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,867,95084,730,404

Consumer Services — 4.1%20,000 eBay Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 671,40043,000 IAC/InterActiveCorp.† . . . . . . . . . . . . . . . . . . . . . . . . . . 3,169,96024,642 Liberty Expedia Holdings Inc., Cl. A† . . . . . . . . . . . 1,120,718

225,200 Liberty Interactive Corp. QVC Group, Cl. A† . . . . . 4,508,50421,000 Liberty TripAdvisor Holdings Inc., Cl. A† . . . . . . . . 296,10045,398 Liberty Ventures, Cl. A† . . . . . . . . . . . . . . . . . . . . . . . . 2,019,303

1,605,000 Rollins Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59,593,6505,500 TripAdvisor Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 237,380

71,617,015

Consumer Products — 4.1%125,000 Avon Products Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . . 550,00014,100 Christian Dior SE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,276,13128,000 Church & Dwight Co. Inc. . . . . . . . . . . . . . . . . . . . . . . 1,396,36065,600 Coty Inc., Cl. A. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,189,328

196,000 Edgewell Personal Care Co.† . . . . . . . . . . . . . . . . . . . 14,335,440146,000 Energizer Holdings Inc. . . . . . . . . . . . . . . . . . . . . . . . . 8,139,500

2,100 Givaudan SA. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,782,15990,000 Hanesbrands Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,868,40023,800 Harley-Davidson Inc.. . . . . . . . . . . . . . . . . . . . . . . . . . . 1,439,9001,270 Hermes International. . . . . . . . . . . . . . . . . . . . . . . . . . . 601,6845,000 Mattel Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 128,050

The Gabelli Equity Trust Inc.Schedule of Investments (Continued) — March 31, 2017 (Unaudited)

See accompanying notes to schedule of investments.

5

SharesMarketValue

COMMON STOCKS (Continued)Consumer Products (Continued)

11,000 National Presto Industries Inc. . . . . . . . . . . . . . . . . . $ 1,124,20021,500 Newell Brands Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,014,15510,000 Oil-Dri Corp. of America. . . . . . . . . . . . . . . . . . . . . . . . 372,70046,800 Reckitt Benckiser Group plc . . . . . . . . . . . . . . . . . . . . 4,272,18927,600 Svenska Cellulosa AB, Cl. B . . . . . . . . . . . . . . . . . . . . 890,159

816,900 Swedish Match AB. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26,574,67470,955,029

Energy and Utilities — 4.0%11,000 ABB Ltd., ADR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 257,40039,000 Anadarko Petroleum Corp. . . . . . . . . . . . . . . . . . . . . . 2,418,00059,000 Apache Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,032,01080,000 BP plc, ADR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,761,60030,000 Canadian Solar Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . . 368,10016,000 CMS Energy Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 715,840

185,100 ConocoPhillips . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9,230,937204,000 El Paso Electric Co. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10,302,00098,400 Enbridge Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,117,05624,000 Eversource Energy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,410,72057,600 Exxon Mobil Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,723,776

140,000 GenOn Energy Inc., Escrow† . . . . . . . . . . . . . . . . . . . 0196,400 Halliburton Co. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9,664,844

4,000 Marathon Oil Corp.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63,20022,000 Marathon Petroleum Corp. . . . . . . . . . . . . . . . . . . . . . 1,111,88020,000 Murphy USA Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,468,40025,000 National Fuel Gas Co. . . . . . . . . . . . . . . . . . . . . . . . . . . 1,490,50013,500 NextEra Energy Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,732,9951,000 Niko Resources Ltd., OTC†. . . . . . . . . . . . . . . . . . . . . 673,000 Niko Resources Ltd., Toronto† . . . . . . . . . . . . . . . . . 203

32,400 Oceaneering International Inc.. . . . . . . . . . . . . . . . . . 877,39215,100 Phillips 66 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,196,222

120,000 Rowan Companies plc, Cl. A† . . . . . . . . . . . . . . . . . . 1,869,60020,000 RPC Inc.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 366,20015,000 Southwest Gas Holdings Inc. . . . . . . . . . . . . . . . . . . . 1,243,650

101,000 The AES Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,129,18035,000 Weatherford International plc† . . . . . . . . . . . . . . . . . 232,750

162,000 Westar Energy Inc.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8,791,74070,576,262

Automotive: Parts and Accessories — 3.8%31,349 Adient plc . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,278,132

107,600 BorgWarner Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,496,604240,900 Dana Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,651,77912,500 Delphi Automotive plc. . . . . . . . . . . . . . . . . . . . . . . . . . 1,006,125

241,400 Genuine Parts Co.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22,307,774365,385 Jason Industries Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . 540,770185,000 Modine Manufacturing Co.† . . . . . . . . . . . . . . . . . . . . 2,257,00073,000 O’Reilly Automotive Inc.† . . . . . . . . . . . . . . . . . . . . . . 19,698,320

111,000 Standard Motor Products Inc. . . . . . . . . . . . . . . . . . . 5,454,54073,000 Superior Industries International Inc. . . . . . . . . . . . 1,850,550

SharesMarketValue

14,000 Visteon Corp.†. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 1,371,30065,912,894

Cable and Satellite — 3.5%253,600 AMC Networks Inc., Cl. A† . . . . . . . . . . . . . . . . . . . . . 14,881,248

1,300 Cable One Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 811,811160,000 Comcast Corp., Cl. A . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,014,40060,400 DISH Network Corp., Cl. A† . . . . . . . . . . . . . . . . . . . . 3,834,79650,200 EchoStar Corp., Cl. A† . . . . . . . . . . . . . . . . . . . . . . . . . 2,858,89021,712 Liberty Global plc LiLAC, Cl. A† . . . . . . . . . . . . . . . . 482,87542,918 Liberty Global plc LiLAC, Cl. C† . . . . . . . . . . . . . . . . 988,831

427,890 Rogers Communications Inc., New York, Cl. B . . 18,921,29619,310 Rogers Communications Inc., Toronto, Cl. B . . . . 853,801

108,800 Scripps Networks Interactive Inc., Cl. A . . . . . . . . . 8,526,656120,000 Shaw Communications Inc., New York, Cl. B. . . . 2,486,40040,000 Shaw Communications Inc., Toronto, Cl. B. . . . . . 829,266

61,490,270

Telecommunications — 3.2%133,000 AT&T Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5,526,15055,400 BCE Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,452,558

914,200 BT Group plc, Cl. A . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,644,659135,000 Cincinnati Bell Inc.†. . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,389,500100,000 Deutsche Telekom AG, ADR . . . . . . . . . . . . . . . . . . . . 1,755,000135,000 Gogo Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,485,00032,001 Harris Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,560,75136,000 Hellenic Telecommunications Organization SA . . 337,96315,000 Hellenic Telecommunications Organization SA,

ADR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69,525264,732 Koninklijke KPN NV . . . . . . . . . . . . . . . . . . . . . . . . . . . . 797,263

7,040,836 LIME† . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68,68622,000 Loral Space & Communications Inc.† . . . . . . . . . . 866,80022,000 Oi SA, ADR†. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27,72031,053 Sprint Corp.† . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 269,54021,000 Telecom Argentina SA, ADR . . . . . . . . . . . . . . . . . . . . 465,990

570,000 Telecom Italia SpA† . . . . . . . . . . . . . . . . . . . . . . . . . . . . 512,61070,000 Telefonica Brasil SA, ADR . . . . . . . . . . . . . . . . . . . . . . 1,039,500

595,739 Telefonica SA, ADR . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,666,319563,700 Telephone & Data Systems Inc.. . . . . . . . . . . . . . . . . 14,943,687105,000 Telesites SAB de CV† . . . . . . . . . . . . . . . . . . . . . . . . . . 68,14125,000 TELUS Corp.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 811,558

125,000 Verizon Communications Inc. . . . . . . . . . . . . . . . . . . 6,093,75048,027 Vodafone Group plc, ADR . . . . . . . . . . . . . . . . . . . . . . 1,269,35419,000 Zayo Group Holdings Inc.† . . . . . . . . . . . . . . . . . . . . . 625,100

55,747,124

Business Services — 3.2%14,334 Allegion plc . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,085,0847,500 Aramark . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 276,5257,000 Ascent Capital Group Inc., Cl. A† . . . . . . . . . . . . . . . 98,910

157,000 Clear Channel Outdoor Holdings Inc., Cl. A . . . . . 949,8502,004 Contax Participacoes SA† . . . . . . . . . . . . . . . . . . . . . . 4,174

90,000 Diebold Nixdorf Inc.. . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,763,000

The Gabelli Equity Trust Inc.Schedule of Investments (Continued) — March 31, 2017 (Unaudited)

See accompanying notes to schedule of investments.

6

SharesMarketValue

COMMON STOCKS (Continued)Business Services (Continued)

16,000 DigitalGlobe Inc.†. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 524,00010,000 Donnelley Financial Solutions, Inc.† . . . . . . . . . . . . 192,9003,000 Edenred . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70,889

160,000 G4S plc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 610,01116,000 Jardine Matheson Holdings Ltd. . . . . . . . . . . . . . . . . 1,028,00088,000 Landauer Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,290,00025,300 Macquarie Infrastructure Corp. . . . . . . . . . . . . . . . . . 2,038,674

289,000 MasterCard Inc., Cl. A. . . . . . . . . . . . . . . . . . . . . . . . . . 32,503,8307,000 Stericycle Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 580,230

290,000 The Interpublic Group of Companies Inc. . . . . . . . 7,125,30010,000 Vectrus Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 223,50012,800 Visa Inc., Cl. A . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,137,536

55,502,413

Retail — 3.0%10,000 Advance Auto Parts Inc.. . . . . . . . . . . . . . . . . . . . . . . . 1,482,600

130,000 Ascena Retail Group Inc.†. . . . . . . . . . . . . . . . . . . . . . 553,80095,300 AutoNation Inc.†. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,030,23738,000 Costco Wholesale Corp.. . . . . . . . . . . . . . . . . . . . . . . . 6,372,22050,500 CST Brands Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,428,545

118,900 CVS Health Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9,333,6504,000 Denny’s Corp.† . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49,480

25,000 Fiesta Restaurant Group Inc.† . . . . . . . . . . . . . . . . . . 605,000320,000 Hertz Global Holdings Inc.† . . . . . . . . . . . . . . . . . . . . 5,612,80022,100 HSN Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 819,910

100,000 J.C. Penney Co. Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . 616,000326,000 Macy’s Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9,662,64012,000 Penske Automotive Group Inc. . . . . . . . . . . . . . . . . . 561,72033,300 Sally Beauty Holdings Inc.† . . . . . . . . . . . . . . . . . . . . 680,65217,000 The Cheesecake Factory Inc. . . . . . . . . . . . . . . . . . . . 1,077,1203,000 Tiffany & Co. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 285,900

17,000 United Natural Foods Inc.† . . . . . . . . . . . . . . . . . . . . . 734,91052,000 Walgreens Boots Alliance Inc. . . . . . . . . . . . . . . . . . . 4,318,60032,000 Wal-Mart Stores Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,306,56055,000 Whole Foods Market Inc.. . . . . . . . . . . . . . . . . . . . . . . 1,634,600

53,166,944

Broadcasting — 2.6%243,300 CBS Corp., Cl. A, Voting. . . . . . . . . . . . . . . . . . . . . . . . 17,125,887

2,000 Cogeco Inc.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 89,57417,334 Corus Entertainment Inc., OTC, Cl. B . . . . . . . . . . . 169,8736,666 Corus Entertainment Inc., Toronto, Cl. B . . . . . . . . 65,465

16,000 Gray Television Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . . 232,00019,250 Liberty Broadband Corp., Cl. A† . . . . . . . . . . . . . . . . 1,637,98366,192 Liberty Broadband Corp., Cl. C† . . . . . . . . . . . . . . . . 5,718,98919,250 Liberty Media Corp.-

Liberty Formula One, Cl. A†. . . . . . . . . . . . . . . . . . 629,47552,250 Liberty Media Corp.-

Liberty Formula One, Cl. C†. . . . . . . . . . . . . . . . . . 1,784,33775,000 Liberty Media Corp.-

Liberty SiriusXM, Cl. A† . . . . . . . . . . . . . . . . . . . . . 2,919,000

SharesMarketValue

158,000 Liberty Media Corp.-Liberty SiriusXM, Cl. C† . . . . . . . . . . . . . . . . . . . . . $ 6,127,240

292,400 MSG Networks Inc., Cl. A† . . . . . . . . . . . . . . . . . . . . . 6,827,54017,376 Nexstar Media Group Inc. . . . . . . . . . . . . . . . . . . . . . . 1,218,92636,000 Pandora Media Inc.† . . . . . . . . . . . . . . . . . . . . . . . . . . . 425,16085,200 Television Broadcasts Ltd.. . . . . . . . . . . . . . . . . . . . . . 344,242

45,315,691