the new market model in austria – a case study - engerati day 2 harald... · the new market model...

TRANSCRIPT

The New Market Model in Austria – a case study Harald Stindl, Joint Managing Director, Gas Connect Austria

Vienna, 31 January 2013

Gas Connect Austria and the OMV Group

Gas &Power Activities

ITO Gas Connect = MAM

ITO BOG 51%

ISO TAG GmbH 11%

Storage nat. + internat. International Logistics

Hub, Gas and Power trading

31 January 2013 European Gas Conference 2

Group Strategy Growth guided by E&P equity gas availability – supported by portfolio optimization Infrastructure investment supports group integration and enables equity gas monetization in short: integrated equity gas marketer

OMV Group Activities: Gas & Power / ExplorationProduction / Refining and Markteting EBIT 2011: EUR Mm 2,500 Employees: 30,500

MAM = Market Area Manager, ITO = Independent Transmission Operator, ISO= = Independent System Operator

Business Model Gas Connect Austria

Corporate Values: Responsibility, Fairness, Long-term view

31 January 2013 European Gas Conference 3

• TSO / DSO / MAM

• Know-how + diversification - Operations & Maintenance Services - Construction Services (Pipeline Know-how for the group)

• Participations

Strategy of the TSO - Increasing Austria‘s role as hub, but

according to market demand - Optimizing of asset portfolio position;

within Austria, there is pipeline competition between TSOs, 3 operational + 3 project companies; Regional / cross-border competition

- In-house staffing of 380 people

- Price cap regulation - Flexibility for TSO pricing missing

Mission

Diversified Know-how provider of Gas Transportation in Austria

TSO = Transmission System Operator DSO = Distribution System Operator

New market model – Benefits / Changes

- Balance group system also for “transit” – in total 69 BGs (status quo: 1.1.2013) with balancing on the transmission system – unbalanced nominations possible – done by MAM - Entry/Exit throughout – no flange trading any more – different price

structure – no 50:50 E/E price relationship - Expectation of higher competition and liquidity on the wholesale

market due to the virtual trading point - Coordinating body for transmission system – MAM (Market Area

Manger) - Coordination across transmission and distribution on the basis of

close cooperation between MAM and DAM (Distribution Area Manager); exit transmission rolled into distribution tariffs - Some changes in the allocation of distribution system cost

31 January 2013 European Gas Conference 4

Responsibility Entry/Exit from January 1st Implementing recent changes in the new Market Model secures…

… a significant improvement of service quality by enhanced services on offer

- Free allocable capacities - FZK - Enhanced product quality: access to

VTP on firm basis - No usage restrictions to other points

in the market area - More than 80% of all GCA capacities

in FZK quality available

- Dynamically allocable capacities - DZK - Enhancement of service quality

compared to P2P transportations via access to VTP on interruptible basis

… a maximum flexibility in structuring contract durations

- Yearly: Starting with 1 October

- Quarterly: Starting with 1 January, 1 April, 1 July, 1 October

- Monthly: Starts at the beginning of each month

- Daily

31 January 2013 European Gas Conference 5

Fairness Entry/Exit from January 1st Successful launch of Entry/Exit Booking for our customers

A snapshot of the market shows a high level of customer satisfaction due to …

… a user friendly booking system (OCB ®) which was transferred with improved functionalities in the new market model

… constant information updates via an information event and dedicated Key Account Management

… smooth transferral of contracts from the P2P System to the E/E System

… carefree Balancing Group Responsible Services

… a swift handling of increased short-term bookings

Since the start of Entry/Exit booking in November, short-term bookings increased by over 600%

European Gas Conference 31 January 2013 6

Fairness Entry/Exit from January 1st Successful launch of Entry/Exit Booking for our customers

Capacity Bookings in Numbers

European Gas Conference 31 January 2013 7

Long Term > 1 Year

Short Term < 1 Year

Oct.12 0 33

Nov.12 0 19

Dec.12 2 72

until 24.Jan.13 0 52

- Since December 2012 capacity bookings increased by ~ 600%*

- Predominantly daily capacity products are booked at Baumgarten Entry, Mosonmagyarovar Exit and Murfeld Exit

0 5 10 15 20 25

Baumgarten Entry

Murfeld Exit

Mosonmagyarovar Exit

Wheeling Überackern

January 2013

December 2012

November 2012

Bookings per Entry/Exit Points

* A comparison between December 2011/2012 and January 2012/2013

Vision Entry/Exit from January 1st Gas Connect Austria continues to innovate…

31 January 2013 European Gas Conference 8

…capacity booking and bundling activities

Gas Connect Austria is a shareholder of the European Auction Platform PRISMA - All products of Gas Connect Austria will be auctioned on the European Platform

with the possibility of cross border product bundling - Gas Connect Austria has kicked off the process of product bundling - Gas Connect Austria is actively involved in designing the new booking system for

customers

Auction Mechanism (according to CAM Network Code) - Ascending Clock (long-term) - Uniform Price (short-term) - Auction mechanism of secondary capacity is under development

Planned Customer Information Event 14 February 2013 @ Vienna

Implementation and first experiences with the new Austrian market model

31 January 2013 European Gas Conference 9

Publication of Data

- Work in Progress: https://mgm.gasconnect.at/gca_mgm/mgm/data.do - Coordination and communication necessary concerning data suppliers - High IT-support and IT-resources necessary

31 January 2013 European Gas Conference 10

Experience so far … first lessons learnt

Market start: well done – good cooperation between customers and gas industry

All parties are in a „learning phase“ – intensive support of our customers

Stable operation due to proper behaviour of all market participants

IT-systems: stable, further development in progress – Use it or lose it

Future changes: all stakeholders need more time for implementation

31 January 2013 European Gas Conference 11

BGR – current overview

- Approved (i)BGRs: 69 on 1 January 2013 - Registrations under progress: 24

31 January 2013 European Gas Conference 12

20

12

24

13

1

4

10

2 2 1 3

1

0

5

10

15

20

25

30

BG = Balancing group BGR = Balancing Group Responsible

Deadlines for 1 January 2013 (1) - PLAN

Request for Energy Identification Code(s)

BGR registration finished (Including registration of balance groups and sub balance accounts)

Agreement with BG-members (Allocation authorization for network users)

Assignment of capacity contracts to BGs/SBAs

Structure of BG/SBA incl. all capacity assignments are finished

Start of data exchange with system operators (Early pre-tests will be arranged by respective system operators)

Deadline for day-ahead nominations (gas day 1.1.2013 6:00) 28.12.2012, 14:00 hr

Pre-matching and matching cycle with all system operators 31.12.2012, 15:25 / 15:45 (first confirmation / first imbalance notice)

Start of physical gas flow in the Market Area East Entry/Exit-System

BGR

BGR

NU

BGR

BGR

BGR

NU

BGR

28.12.2012

20.12.2012

19.12.2012

01.01.2013 – 06:00 hr

done

done

done

done

done

done

done

done

done

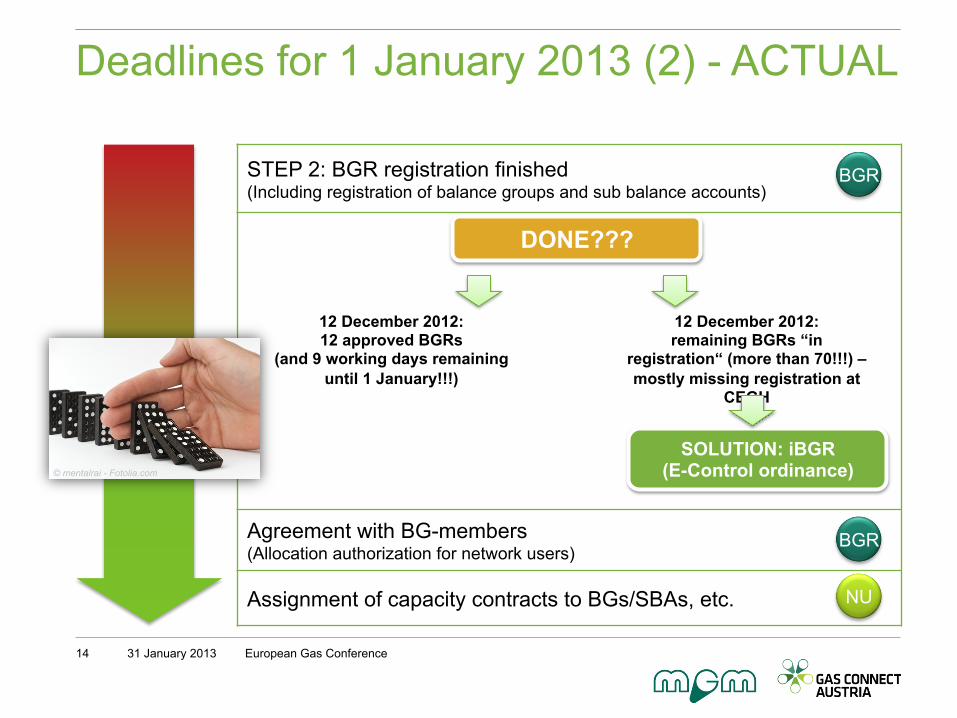

STEP 2: BGR registration finished (Including registration of balance groups and sub balance accounts)

Agreement with BG-members (Allocation authorization for network users)

Assignment of capacity contracts to BGs/SBAs, etc.

Deadlines for 1 January 2013 (2) - ACTUAL

31 January 2013 European Gas Conference 14

BGR

DONE???

NU

BGR

12 December 2012: 12 approved BGRs

(and 9 working days remaining until 1 January!!!)

12 December 2012: remaining BGRs “in

registration“ (more than 70!!!) – mostly missing registration at

CEGH

SOLUTION: iBGR (E-Control ordinance) © mentalrai - Fotolia.com

Deadlines for 1 January 2013 (3) - ACTUAL

31 January 2013 European Gas Conference 15

Agreement with BG-members (Allocation authorization for network users)

Assignment of capacity contracts to BGs/SBAs

Structure of BG/SBA incl. all capacity assignments are finished

Start of data exchange with system operators (Early pre-tests will be arranged by respective system operators)

Deadline for day-ahead nominations (gas day 01.01.2013 06:00): 28.12.2012, 14:00 hrs

Start of physical gas flow in the Market Area East Entry/Exit-System 1.1.2013

Pre-matching and matching cycle with all system operators 31.12.2012, 15:25 / 15:45 (first confirmation / first imbalance notice)

© macgyverhh - Fotolia.com

The First KNEP Experience…

31 January 2013 European Gas Conference 16

… builds the basis…

Stipulated time frame for establishment 16 April 2012 – 30 June 2012

NRA Approval 11 January 2013

Approved projects: - G00.040 Reverse Flow - Prolongation of the Pressure Support Agreement

(PSV) to provide a short-term resolution of the congestion @ Oberkappel

Criticism/Conditions: - Deliver investment steps targeting the capacity

requests @ 7 Fields - Provide a holistic overview of the capacity requests on

all decisive and non-decisive Entry/Exit Points - Develop a feasibility study, and a reasoning for the

respective choices how to resolve the congestion @Oberkappel from the Austrian side.

… for continuous improvement.

- A coordinated process plan for the next KNEP is under development

- A more active coordination through the Market Area Manager of the parties involved (TSOs and Distribution Area Manager, Market Participants)

- Develop a tool for modelling gas flows and analysing scenarios

- Include a more profound analysis of the Austrian Energy Policy Goals

- Consideration of the national Network Development Plans of adjacent TSOs

KNEP = Coordinated Network Development Plan

Outlook for further integration - Early days to assess impact of the new market model for the Austrian

market - Austria`s position in the European network partly dependent on future

projects and on market demand - Integration with adjacent markets will proceed - given sufficient liquidity on

the CEGH this should be attractive for shippers - Austria, Czech Republik, Slovakia Trading Region not first priority but to be

considered alongside other options

31 January 2013 European Gas Conference 17

© 2012 GAS CONNECT AUSTRIA GmbH

floridotower Floridsdorfer Hauptstraße 1 1210 Wien, Vienna, Austria T +43 1 27500-88000

www.gasconnect.at

Thank you for your attention!