transfer payments: a federal perspective - fmi*igf · transfer payments: a federal perspective •...

TRANSCRIPT

Transfer Payments:A Federal Perspective

Presentation to FMI – Ontario Chapter

February 15, 2012

RDIMS #1051610

2

Transfer Payments: A Federal Perspective

• Background on federal transfer payments and policy instruments

• Grants and contributions (Gs & Cs) reform– Government of Canada Action Plan and results to date

– Work plan and priorities for Phase 2 of reform (2011‐2013)

– Next steps

• Common Financial Management Business Process Initiative

Background on federal transfer payments and policy instruments

4

Government of Canada budgetary expenditures fiscal year 2009-10

(in Billions $)

Major Transfers *$88.639%

Operating & Capital$67.330%

Debt$27.012%

Other Transfer Payments

(Gs&Cs)$42.119%

Non-Profit Organizations

$10.925%

Persons$7.417%

Provinces / Territories$9.121%

Internat’l Orgs / Foreign Countries

$11.227%

Industry$3.27%

Reallocation of Transfer Pmts

-$0.51%

Other Transfer Payments (Gs&Cs)By Recipient Type

Total Net Expenditures$225.0

Source: Public Accounts of Canada, Volume II* : Includes Major Transfers to provinces/territories, Old Age Security, guaranteed income supplement and Spouse’s allowance, and Children’s benefits

5

Who is involved with Gs & Cs ?

The Minister

Senior Management

Program Managers

Program Officers

RecipientsAnd

Beneficiaries • Finance Officers• Internal Auditors• Program Evaluators• Legal Advisors

• Cabinet• Treasury Board• Parliament

6

PLANNED SUITE OF TB POLICY INSTRUMENTS

The Policy on Transfer Payments supports the Governance and Expenditure Management Framework

Governance and ExpenditureManagementFramework

ServiceFramework

Assets &Acquired Services

Framework

FinancialManagementFramework

PeopleFramework

5POLICIES

2POLICIES

5POLICIES

4POLICIES

9POLICIES

2STANDARDS

3STANDARDS

9 DIRECTIVES7 STANDARDS3 GUIDELINES

6STANDARDS

0DIRECTIVES

4 Policieslinked to

FoundationFramework

Values and Ethics Code for the Public

Service

25DIRECTIVES

12STANDARDS

19 DIRECTIVES

9DIRECTIVES

2 GUIDELINES

0STANDARDS

10GUIDELINES

8DIRECTIVES

GUIDELINES TBD

CompensationFramework

26GUIDELINES

InformationandTechnologyFramework

7POLICIES

11DIRECTIVES

19STANDARDS

22GUIDELINES

OCHRO

0 GUIDELINES

7

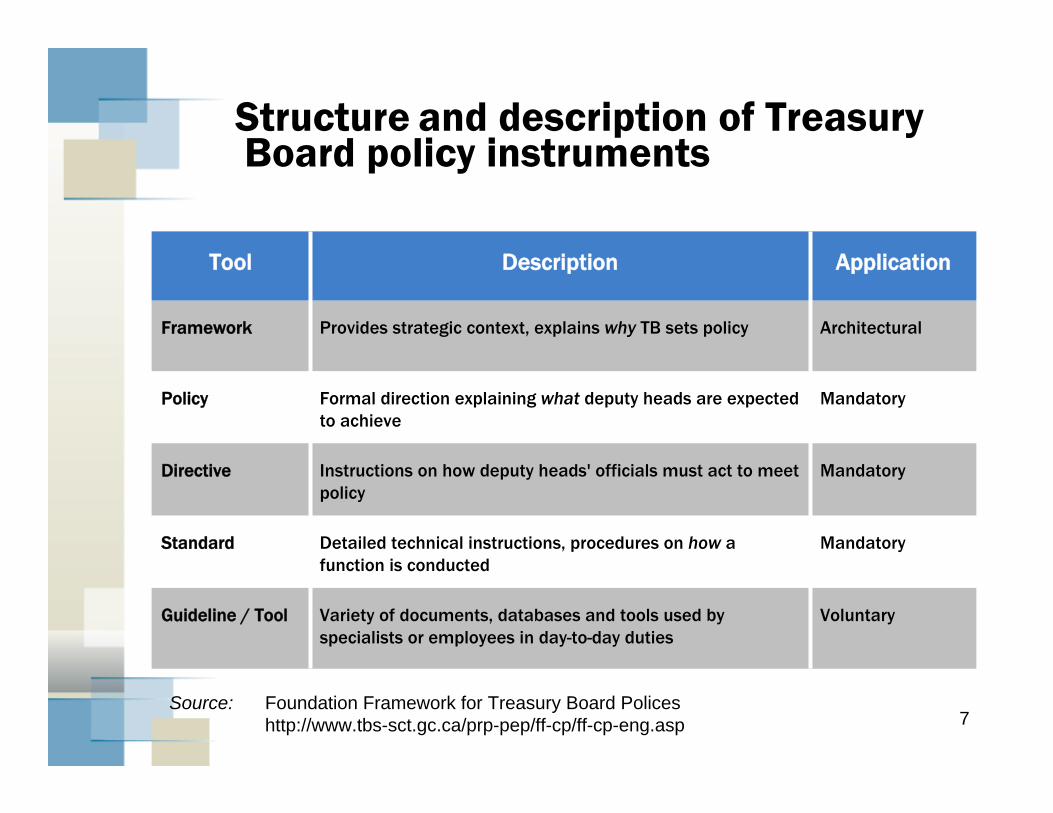

Structure and description of Treasury Board policy instruments

VoluntaryVariety of documents, databases and tools used by specialists or employees in day-to-day duties

Guideline / Tool

MandatoryDetailed technical instructions, procedures on how a function is conducted

Standard

MandatoryInstructions on how deputy heads' officials must act to meet policy

Directive

MandatoryFormal direction explaining what deputy heads are expected to achieve

Policy

ArchitecturalProvides strategic context, explains why TB sets policyFramework

ApplicationDescriptionTool

Source: Foundation Framework for Treasury Board Polices http://www.tbs-sct.gc.ca/prp-pep/ff-cp/ff-cp-eng.asp

8

Types of transfer paymentsDefinitions per Policy on Transfer Payments

• Transfer Payments:– A monetary payment, or a transfer of goods, services or assets to a third party

that does not result in the acquisition by the Government of any goods, services or assets.

• Grant:– Recipient needs to meet prior eligibility requirements– May be required to report on results achieved – not mandatory– Normally not subject to audit

• Contribution:– Payment subject to performance conditions– Must be accounted for– Subject to audit

• Other Transfer Payment:– Other than a grant or contribution– Based on legislation or other arrangements– May be determined by formula– Examples include Major Transfers to Provinces

9

Gs & Cs – TBS Key policy instruments

• Policy on Transfer Payments

• Directive on Transfer Payments

• Directive on the Evaluation Function

• Standard on Evaluation

• Guideline on Recipient Audits Under the Policy on Transfer Payments and the Directive on Transfer Payments

• Accounting Standard 3.2 - Treasury Board - Transfer Payments (Grants and Contributions)

• 3-year integrated plans are integrated into requirements for Departmental Reports on Plans and Priorities

10

Policy on transfer payments

• “The objective of the Policy is to ensure that transfer payment programs are managed with integrity, transparency, and accountability in a manner that is sensitive to risks; are citizen-focused; and are designed and delivered to address government priorities in achieving results for Canadians”

11

Directive on transfer payments

• Objective is to achieve risk-based approaches to the design, management, and delivery of transfer payment programs and to ensure accountability and value for money

• It supports and reinforces key objectives and principles of the Policy on Transfer Payments, including:

– Administrative requirements for recipients tailored to risks– Engagement of applicants and recipients– Increased horizontal harmonization of programs– Increased standardization of procedures, processes and

systems

12

Treasury Board Accounting Standard 3.2 Transfer Payments

• Defines GOC accounting for transfer payments to supplement PSAB

• In process of being revised to incorporate new requirements of PS 3410

• No longer allowed to recognize prepayment

• Include section on Loans Receivable to address unconditionally repayable contributions and concessionary loans

13

Useful Links

Policy on Transfer Paymentshttp://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=13525

Look to right of screen for “Related Instruments” for further links

Directive on Transfer Paymentshttp://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=14208

TBAS 3.2

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=12178

Grants and Contributions (Gs & Cs) Reform

15

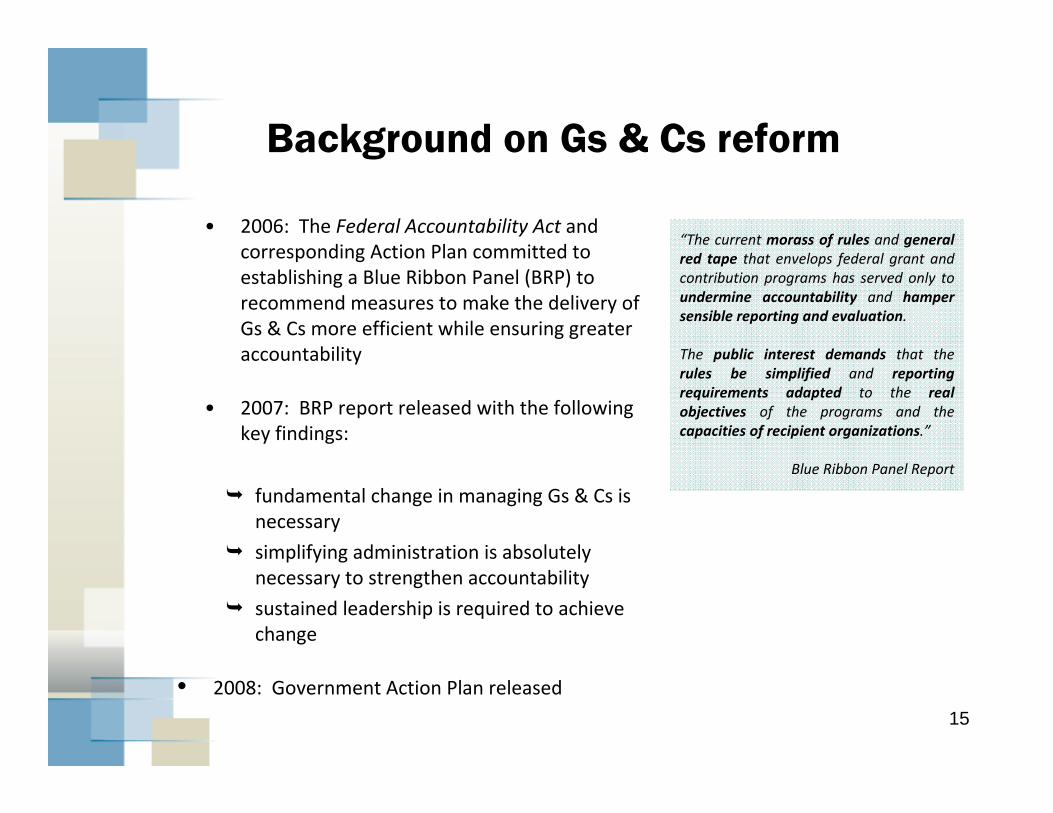

Background on Gs & Cs reform

• 2006: The Federal Accountability Act and corresponding Action Plan committed to establishing a Blue Ribbon Panel (BRP) to recommend measures to make the delivery of Gs & Cs more efficient while ensuring greater accountability

• 2007: BRP report released with the following key findings:

“The current morass of rules and general red tape that envelops federal grant and contribution programs has served only to undermine accountability and hamper sensible reporting and evaluation.

The public interest demands that the rules be simplified and reporting requirements adapted to the real objectives of the programs and the capacities of recipient organizations.”

Blue Ribbon Panel Report

fundamental change in managing Gs & Cs is necessary

simplifying administration is absolutely necessary to strengthen accountability

sustained leadership is required to achieve change

• 2008: Government Action Plan released

16

Government of Canada Action Planto Reform the Administration of Grants and Contributions

In response to the BRP, a plan was developed based on three core elements with the following achievements have been made in Phase 1 (2008‐2011):

1. Policy Reform – revise Treasury Board Transfer Payment Policy suite

New risk‐based policy in effect since October 2008 Provides increased flexibilities

2. Departmental Action Plans ‐ implement opportunities for improved service delivery and increased efficiency

21 federal departments are implementing plans at varying speeds 4 interdepartmental regional‐based pilots are underway

3. Horizontal Enablers – ensure consistency and convergence of efforts for more streamlined approaches and strengthened accountability

TBS Centre of Expertise established Interdepartmental committees are functioning well Standard tools and processes are increasingly being used within departments Best practices are being shared across departments

Despite progress, recipients have not yet felt the impact sufficiently…DMs met on June 29, 2011 & agreed that we need to collectively do more to move beyond embedded practices.

17

Work plan for Phase 2 of reform(2011-2013)

• to develop and test innovative Gs & Cs delivery models through national pilots and focused interdepartmental collaboration

• to identify and tackle specific barriers (i.e. legal, policy, culture change)

• to roll out recommended models from pilots to increasingly streamline and standardize practices across government

To meet recipients’ expectations, TBS and departments are aligning efforts:

See Appendix A for Gs & Cs Reforms at a Glance

See Appendix B for Detailed Phase 1 Achievements

18

Priorities for Phase 2 of reform

(2011-2013)

19

National pilots• Five new national pilots are now being launched to develop

common approaches, instruments and tools for the delivery of Gs & Cs to common recipients:

– First Nations communities and other Aboriginal recipientsAANDC and Health (co-leads), HRSDC and Public Safety

– Non-Aboriginal recipientsCIC (lead) – tbd

ACOA (lead), CED-Q, WED, Fed Dev ON, FedNor and CanNor – regional economic development agency recipients• will develop standard tools and processes for similar recipients

– Federal - Provincial / Territorial GovernmentsTransport (lead), Infrastructure, AAFC, HRSDC

– International organizationsDFAIT (lead) and CIDA• HC participating is also participating in development of World Health

Organization standard funding agreement template

20

Addressing barriers

TBS and interdepartmental efforts on pilots have demonstrated that:

• There is no Treasury Board policy barrier to streamlining administrative requirements or adopting an interdepartmental delivery approach

• The new section 29.2 of the FAA enables departments to provide internal support services to each other to standardize their administrative practices

• Moving away from embedded practices is both complicated and difficult to achieve without sustained leadership at all levels to support innovative risk-based approaches

• To be successful, reform efforts require support from senior management to ensure adequate, dedicated support as well as collaboration between program and finance functions, HQ and regions, and Centers of Expertise across departments

21

IM-IT strategy for Gs & Cs

• TBS is leading the development of an IM-IT strategy to rationalize Gs & Cs application systems across government and to develop a common recipient registry

• An interdepartmental working group is engaged in a project to define common and core business requirements for Gs & Cs across government

• TBS-Chief Information Officer Branch is continuing to advise departments on incremental IT investment decisions in the interim

22

Other reform initiatives

• Facilitating departmental efforts to harmonize programs

– Policy proposal to increase authorities to enable Ministers and Deputy Heads to amend most elements of program terms and conditions

– Sharing expertise and best practices across government e.g. harmonization and standardization

• Increasing implementation of Gs & Cs service standards

– Developing an implementation guide for departments

• Engaging with key recipient organizations to collaborate on initiatives of common interest for reform agenda

23

Appendices

A: Gs & Cs reform at a glanceB: Detailed Phase 1 achievements to date

24

Gs & Cs reform at a glance

Timeline for Reform ActivitiesTimeline for Reform Activities

Phase One20082008--20112011

Current Phase 20112011--20132013

Key OutputsKey Outputs

•• New policy, directive and New policy, directive and guidance guidance

•• TBS CoE established and TBS CoE established and departments increasing their CoE departments increasing their CoE support activitiessupport activities

•• Actions underway as per DAPs: Actions underway as per DAPs: program harmonization, initiating program harmonization, initiating riskrisk--based management based management practices, testing practices, testing interdepartmental delivery via interdepartmental delivery via pilots, sharing tools and best pilots, sharing tools and best practicespractices

Future Phases2013 onward2013 onward

Key OutputsKey Outputs

•• RiskRisk--based approaches for all Gs & based approaches for all Gs & Cs programs are in place to reduce Cs programs are in place to reduce administrative burdenadministrative burden

•• Program harmonization is continuingProgram harmonization is continuing

•• Standard tools promulgated by TBSStandard tools promulgated by TBS

•• Business requirements are defined to Business requirements are defined to support an IM/IT strategy which can support an IM/IT strategy which can leverage and share Gs & Cs systems leverage and share Gs & Cs systems and support the development of a and support the development of a common recipient registrycommon recipient registry

Key OutputsKey Outputs

•• Programs are fully harmonized Programs are fully harmonized and delivered interdepartmentallyand delivered interdepartmentally

•• An IM/IT solution is developed to An IM/IT solution is developed to support a common recipient support a common recipient registryregistry

•• CompetencyCompetency--based training is based training is developed and is being delivered developed and is being delivered to program officials across to program officials across governmentgovernment

•• Departments and TBS explore Departments and TBS explore opportunities to work with opportunities to work with recipient organizations to recipient organizations to implement further reformsimplement further reforms

Reduced administrative burden and improved transparency and

engagement

• Single funding agreements are increasingly being used and reporting and audit requirements are reduced for recipients

• Departments publish and meet service standards

• Departments engage recipients on a regular basis

• An increasing number of departments provide a single window access to departmental Gs & Cs programs

Improved access to federal Gs & Cs programs

• A common registry enables recipient information to be shared across departments to eliminate duplicative reporting for recipients

• Single funding agreements are more commonplace

Cumulative Impacts felt

by recipients

Key Outputs Key Outputs from from

Government Government Action PlanAction Plan

Minimal Impacts for Recipients

Increasing impacts for recipients over timeIncreasing impacts for recipients over time

Appendix A

25

Detailed Phase 1 achievements

Treasury Board Secretariat Departments

Policy Reform

• Policy suite on Transfer Payments (PTP) renewed and new flexibilities communicated to departments

• Guidelines developed and ongoing advice provided on the Directive, Recipient Audits, Performance Measurement Strategies, and Three‐Year Plans

• Communication within departments to increase awareness of PTP requirements

• Implementation of new PTP suite (e.g. renewal and continuation of Ts & Cs, Three‐Year Plans, revised funding agreements, service standards and recipient engagement)

Departmental Action Plans

• Engaged in reporting of government‐wide progress on Gs & Cs reform and increasing departmental participation in development and implementation of Action Plans

• 21 federal organizations have Departmental Action Plans and are actively implementing and reporting on progress

Horizontal Enablers

• On‐going support to interdepartmental pilot projects

• Governance (ADM, D/DG committees) in operation

• Guidance on Gs & Cs risk management and model for internal administrative costing developed

• Best practices shared on consolidated audits, flat recipient overhead rates, harmonization, service standards

• GCPedia site launched to enable sharing of tools and best practices

• Inventory established for training materials and optimal training methods

• Five interdepartmental pilots currently underway

Edmonton Aboriginal Transition Initiative, Northern Communities Wellness Project, Nova Scotia Integrated Service Delivery Project, Pangnirtung “Making Connections for Youth” Project, Quebec Aboriginal Cluster Project (Mashteuiatsh)

Collection of lessons learned to inform next phase of reform efforts

• Increased use of standard tools and processes across programs within departments

Appendix B

Government Action Plan to Reform the Administration of Grants and Contributions

26

2000 Policy Suite 2008 Policy Suite

• Ambiguous roles and responsibilities • One policy mixing mandatory and non‐mandatory

statements

• Clear roles and responsibilities• Increased authorities for Ministers• Separate policy, directive and guidelines

• Detailed, requirements‐based• Led to significant administrative burden

• Flexible, principles‐based• New risk‐based approach: administrative

(management) controls proportionate to the level of risk specific to the program, the materiality of funding, and to the risk profile of applicants and recipients

• Focus was on departmental accountabilities• No reference to recipients needs, capacities or

expertise

• Focus on results and service orientation• Requirement for service standards• Requirement to engage recipients• Tailored requirements for groups of recipients

(e.g. Aboriginals and international organizations)• Silent on horizontal coordination and harmonization• Silo‐ed approach to program management

• Requirements to harmonize programs and standardize administration, where appropriate

• Leadership responsibilities for TB Secretariat• Allowed for inconsistent selection and use of

instruments• Clarified definitions and selection criteria (grants ‐

unconditional; contributions ‐ no longer limited to eligible expenditure reimbursement)

Detailed Phase 1 achievementsAppendix B

Policy Reform: Areas of Significant Change to Policy on Transfer Payments

27

Detailed Phase 1 achievementsDepartmental Participation

• 2008: Six departments emerged to form a vanguard for reform activities

• 50% of total federal Gs & Cs spending

• 2011: Efforts have broadened to now include 23 departments

• 91% of total federal Gs & Cs spending

VanguardsVanguards

AANDC, AANDC, Canadian HeritageCanadian Heritage,,

CEDCED‐‐QQ,, CIDA, Health Canada, CIDA, Health Canada, HRSDC HRSDC

2nd Cohort

Agriculture, ACOA, Canadian Space Agency, Citizenship and Immigration, DFAIT, Environment Canada,

FedNor, Justice Canada, National Research Council,Natural Resources Canada, Industry Canada, Infrastructure Canada,

Public Safety, Status of Women, Transport Canada, Veterans Affairs,

Western Economic Diversification

Appendix B

28

Detailed Phase 1 achievementsDepartmental Action Plans: Examples of Achievements

Single client view – By taking a single client view and harmonizing initiatives, DFAIT and AAFC have dramatically simplified program access and reporting requirements for recipients; AANDC’s suite of Indian Government Support Programs has also adopted a single application, single report approach.

Risk‐based decision making – Increasingly being applied for funding decisions and recipient oversight in all departments.

Reduction of audits – Using a risk management approach, NRC has reduced recipient audits by 75%.

Simplified, transparent approval processes – Through common forms and web technologies, CIDA has reduced by half its response time to recipients for most applications to its Canadian Partnership Branch.

Service standards – ten departments (AAFC, ACOA, CED‐Q, CIC, EC, HRSDC, PCH, TC, VAC, WD) have developed and published standards for Gs & Cs programming.

Consolidated, multi‐year agreements – HC has adopted consolidated multi‐year funding to reduce the number of funding agreements. One agreement covers multiple initiatives over multiple fiscal years. AAFC has also developed a single agreement for AAFC‐wide use with proposal programs.

Recipient Engagement – As an integral component of reform efforts, AAFC, AANDC, ACOA, CED‐Q, CIC, CIDA, DFAIT, DoJ, EC, NRC, NRCan, PCH, PSEP, SWC, TC, and WED have implemented recipient engagement strategies to inform improved program design and delivery practices.

Reduction of audit costs – AAFC has centralized and consolidated the coordination of audits, achieving economies of scale and lowering the average costs for audits by 10%.

Simplified claims process – HRSDC has adopted a portfolio‐wide approach to recipient costs including the use of flat rates, reducing the number of cost categories in funding agreements, and allowing recipients greater latitude to shift funds amongst categories.

Appendix B

* Update as of September, 2011

29

Common Financial Management Business Process (FM-BP) Initiative

Grants and Contributions

30

The Common FM-BP InitiativeGoal:To develop an integrated framework of ‘should be’ common processes that standardize and modernize financial management

Approach:OCG sponsored in collaboration with departments and agencies, financial systems clusters, policy authorities and service providers

Deliverables:• Guidelines which will provide:Standardized process definitions

– System- independent, modular, interoperable – Common to all departments and agencies– Describes roles and responsibilities in detail

“RACI” data analysis includes identification of:– Responsible, Accountable, Consulted, and Informed resources; and– Authoritative data sources

Process Flows– Flow diagrams

31

The Common FM-BP initiative -Scope and governance

Business Processes organized into Domains and Cross functional areas

Governance

Project Operations

32

FM-BP processes

• Processes are described from a financial management point of view.

• Most activities will be financial in nature, however in certain cases, non-financial activities will be included in order to provide a comprehensive description.

• Some of the financial activities described will also be related to controls; however the intent is neither to provide a complete listing of controls, nor to produce a control framework.

• Processes are described at two levels of detail:– Level 2: a one-page business process flow diagram which describes the

whole or part of a functional domain. – Level 3: provides more detail to a level 2 sub-processes through

identification of activities, while remaining common to all departments and system independent.

32

33

Project objectives for Gs & Cs

• The overall project objective, consistent with the Common FM-BP Initiative, is to document the “should be” grants and contributions processes for departments and agencies within existing policies, regulations and legislation for financial management.

The project will define business processes that:

• Are common, department-neutral, system-generic, modular and interoperable;

• Are flexible, can be used immediately in no particular order and as a suite or individually;

• Establish a sound management approach supportive of departmental strategic and operational business plans;

• Reinforce the principles of probity and prudence and contribute to better decision making through standardization; and,

• Protect existing investments and knowledge by leveraging currentsuccesses.

34

Project scope for Gs & Cs

The process scope of the Manage Grants and Contributions (Gs & Cs) starts with the financial due diligence applied at the negotiation, creation and approval stages of the grants and contribution agreements and ends with the payment and/or re-payment (where applicable) and the audit:

1. Arrange (out-of-scope)2. Announce (out-of-scope)3. Apply (out-of-scope)4. Assess (out-of-scope)5. Award6. Administer7. Achieve8. Audit

35

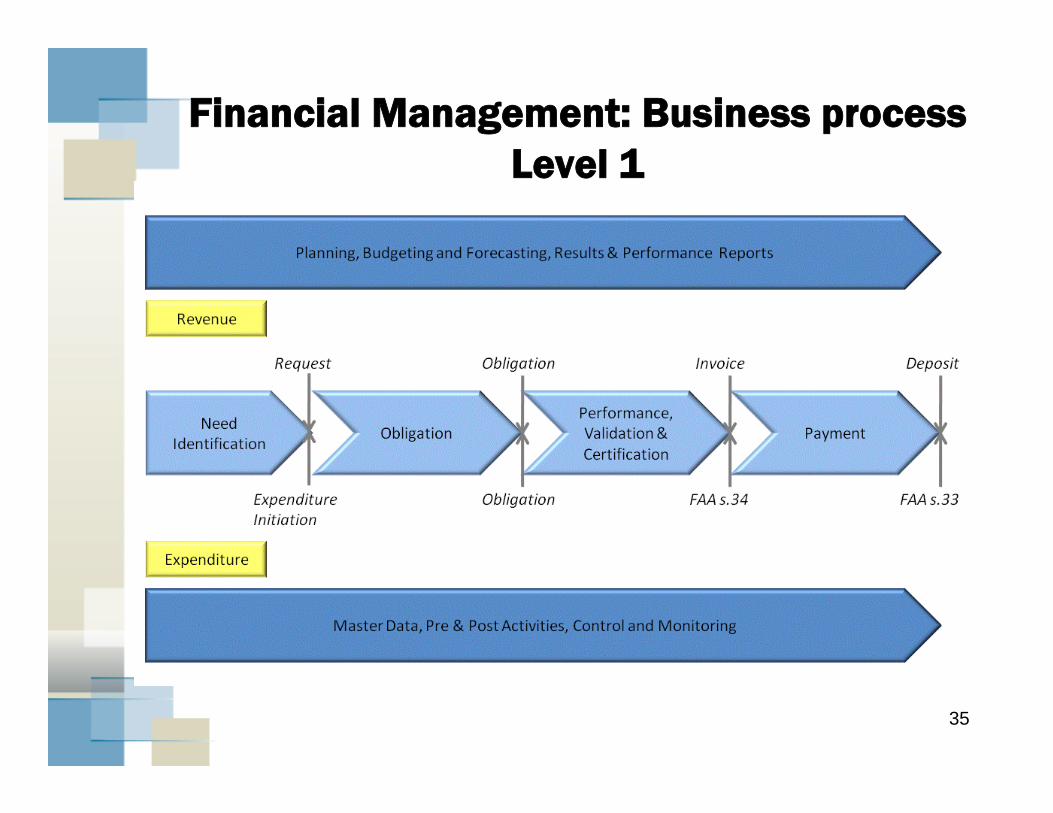

Financial Management: Business process Level 1

36

Level 2 diagram

36

37

Level 3 diagram

6.1.2 Assess (eligibility, proposal, risk)

6.1.4.1 Determine required expenditure

initiation authority6.1.2

YesCan authority be obtained or exercised

End

6.1.4.3 Exercise or obtain authority

6.1.5 Manage funds availability (S.32)

6.1.5

6.1.17 Monitor eligibility/compliance with funding agreement

6.1.17

6.1.4.2 Notify recipient

No

38

RACI Analysis

Explanation of acronyms: CF: Corporate Finance; DFMS: Departmental Financial and Materiel Management System; FIN: Financial Services; and RCM: Responsibility Centre Manager.

Activity Related Data Responsible Accountable Consulted Informed Authoritative Source

6.1.4.1 Determine required expenditure initiation authority

Delegation of authorities instruments

Funding agreement application (if applicable)

RCM RCM CF FIN

- DFMS

6.1.4.2 Notify recipient

Funding agreement application (if applicable)

RCM RCM Recipient DFMS

6.1.4.3 Exercise or obtain authority

Delegation of authorities instruments

Funding agreement application (if applicable)

RCM RCM CF FIN

- DFMS

39

Next Steps

• Has been recommended for approval by directing committee

• TBS Internal Approval process

• March 2012 – departmental review

• October 2012 – target publishing date