union gaming analytics (michael greene)

TRANSCRIPT

Union Gaming Analytics

Financial Suitability – Southeast Kansas Zone

Presentation to the Kansas Lottery Gaming Facility Review Board

June 10, 2015

2

Scope of Work

• Analyze the applicants for the Southeastern Kansas gaming license from a

financial suitability perspective

• Review of the applicants ability to finance the proposed casino development

projects

• Review of the applicants ability to meet their debt obligations and ability to

reinvest in the projects

• Equity and debt commitments, liquidity, cash flow, leverage, and other

metrics

3

Frontenac Development, LLC Camptown Casino

4

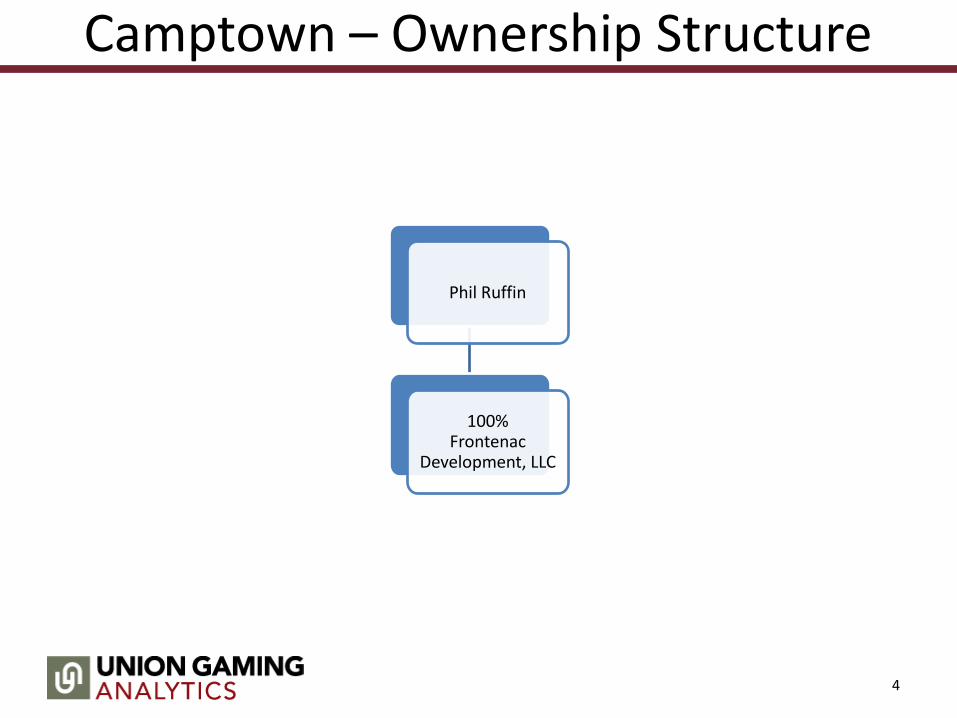

Camptown – Ownership Structure

Phil Ruffin

100% Frontenac

Development, LLC

5

Camptown – Project Budget

Owner Ratio

Frontenac Development, LLC 100%

Project budget: Total

Existing Land & Building 25,000

New Land and Improvements 2,466

New Buildings 15,288

Design, development and construction 799

Furniture, fixture and equipment 26,853

Pre-opening and Contingencies 8,125

License fee 5,500

Funds needed for development 84,031

6

Camptown – Financing Sources

• Frontenac intends to finance Camptown Casino via 100% cash equity

Financing sources Ratio

Cash equity 100.0%

Financing amounts Total

Cash equity 59,031

Total Frontenac 59,031

7

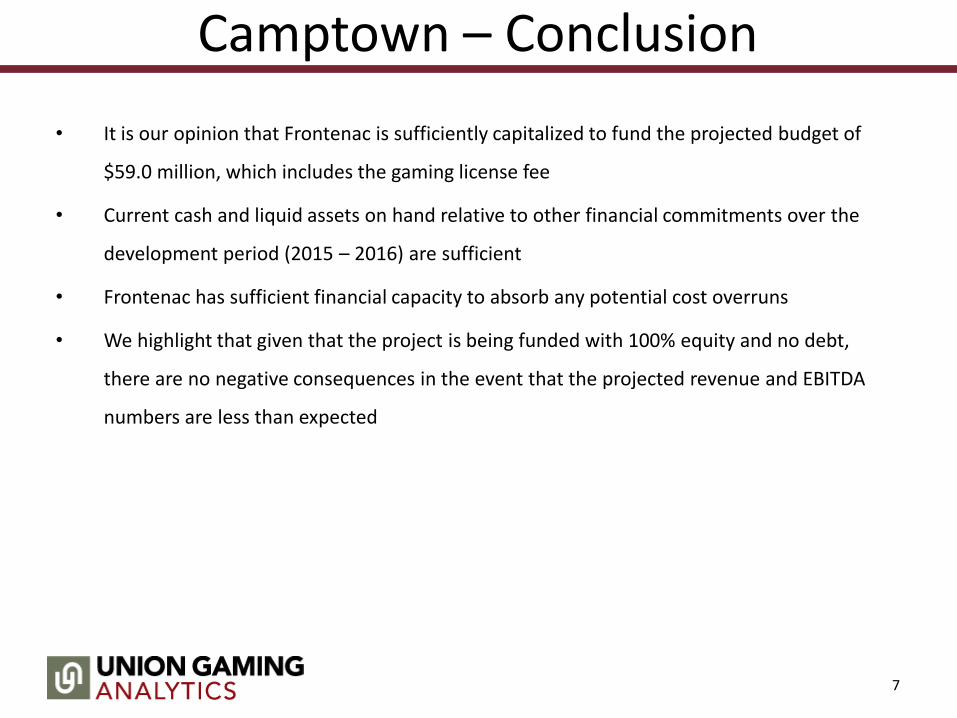

Camptown – Conclusion

• It is our opinion that Frontenac is sufficiently capitalized to fund the projected budget of

$59.0 million, which includes the gaming license fee

• Current cash and liquid assets on hand relative to other financial commitments over the

development period (2015 – 2016) are sufficient

• Frontenac has sufficient financial capacity to absorb any potential cost overruns

• We highlight that given that the project is being funded with 100% equity and no debt,

there are no negative consequences in the event that the projected revenue and EBITDA

numbers are less than expected

8

Castle Rock Casino Resort, LLC Castle Rock Casino Resort

9

Castle Rock – Ownership Structure

Class A Members

29.4%

SK, LLC - 4.90%

JCB, LLC - 4.90%

Michael Steven - 4.90%

Robert Rudd - 2.94%

Crystal River Investments LLC - 1.90%

Jolly Boys Partners LLC - 1.47%

Joplin Holdings LLC - 1.47%

SE Kansas LLC - 1.23%

MOECR LLC - 0.98%

Murfin, Inc. - 0.98%

SEK Investments LLC - 0.74%

Johnny Steven - 0.54%

Rucker Properties LLC - 0.50%

Roll It LLC - 0.49%

Transcontinental Holding Company LLC - 0.49%

David Becker - 0.49%

Gregory Schmidt - 0.49%

Class B Members

Air Capital Gaming LLC

70.2%

Rodney Steven

35.1%

Brandon Steven

35.1%

Class C Members

0.4%

Gregory Ferris

0.4%

American Casino & Entertainment

Properties

10

Castle Rock – Project Budget Owner Ratio

Class A Members 29.4%

Class B Members 70.2%

Class C Members 0.4%

Project budget: Total

Land 30,000

Land & Improvements 5,340

Buildings 32,511

Hotel 29,846

Design, development and construction 11,216

Public Sector Infrastructure 1,450

Financing Costs 3,996

Furniture, fixture and equipment 21,064

Pre-opening and Contingencies 4,076

License fee 5,500

Funds needed for development 144,998

11

Castle Rock – Financing Sources

• CRCR intends to finance Castle Rock Casino via a mix of equity (34.5%) and debt (65.5%)

• Based on the estimated budgets, this implies:

• $50.0mm equity; $95.0mm debt

Financing sources Ratio

Equity 34.5%

Debt 65.5%

Financing amounts

Equity 50,000

Debt 94,998

Total Castle Rock 144,998

12

Castle Rock – Conclusion • It is our opinion CRCR’s equity members have sufficient available liquid assets to fund their

cash equity commitments and absorb cost overruns

• However, we call into question CRCR’s ability to raise the required debt

• Current capital structure includes significant value associated with contributed land

with no independent land appraisal; we were unable to validate the $30.0mm value

• The 65% loan-to-cost ratio is highly correlated to the land value and therefore the

ability to obtain the required debt financing is also dependent on the land value

• No firm debt commitments for the required amount

• Given projected EBITDA, the size of the project budget, the related 65% loan-to-cost ratio,

and high leverage ratio, the project is not feasible because it will not be able to service its

debt

• Based on our projections, the leverage ratio (total debt outstanding divided by

EBITDA) of 10.0x in 2019 is far too high for a stand-alone greenfield casino

development project

13

Kansas Crossing Casino, L.C. Kansas Crossing Casino & Hotel

14

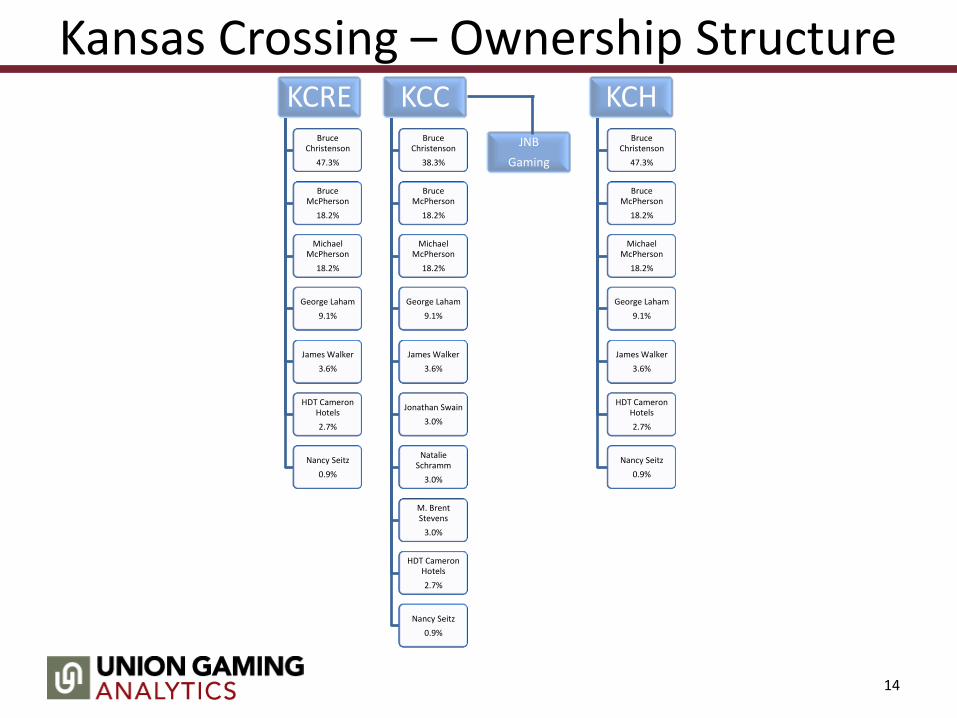

Kansas Crossing – Ownership Structure KCRE

Bruce Christenson

47.3%

Bruce McPherson

18.2%

Michael McPherson

18.2%

George Laham

9.1%

James Walker

3.6%

HDT Cameron Hotels

2.7%

Nancy Seitz

0.9%

KCC Bruce

Christenson

38.3%

Bruce McPherson

18.2%

Michael McPherson

18.2%

George Laham

9.1%

James Walker

3.6%

Jonathan Swain

3.0%

Natalie Schramm

3.0%

M. Brent Stevens

3.0%

HDT Cameron Hotels

2.7%

Nancy Seitz

0.9%

KCH Bruce

Christenson

47.3%

Bruce McPherson

18.2%

Michael McPherson

18.2%

George Laham

9.1%

James Walker

3.6%

HDT Cameron Hotels

2.7%

Nancy Seitz

0.9%

JNB

Gaming

15

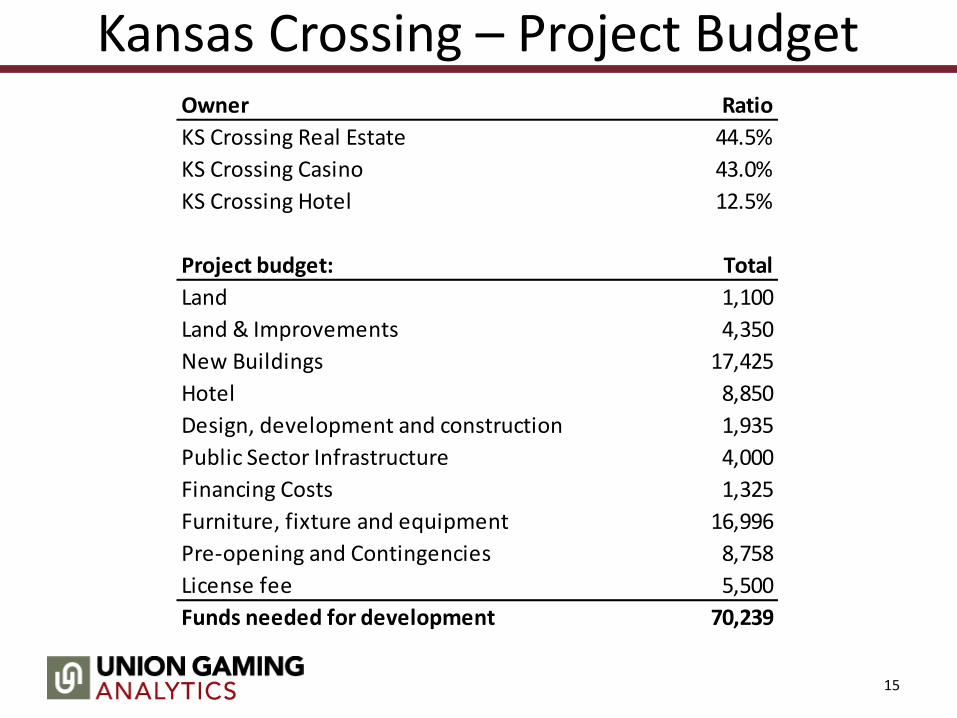

Kansas Crossing – Project Budget Owner Ratio

KS Crossing Real Estate 44.5%

KS Crossing Casino 43.0%

KS Crossing Hotel 12.5%

Project budget: Total

Land 1,100

Land & Improvements 4,350

New Buildings 17,425

Hotel 8,850

Design, development and construction 1,935

Public Sector Infrastructure 4,000

Financing Costs 1,325

Furniture, fixture and equipment 16,996

Pre-opening and Contingencies 8,758

License fee 5,500

Funds needed for development 70,239

16

Kansas Crossing – Financing Sources

• KC intends to finance Kansas Crossing Casino via a mix of cash equity (36.9%) and debt

(63.1%)

• Based on the estimated budgets, this implies:

• $25.9mm cash equity; $44.3mm debt

Financing sources Ratio

Equity 36.9%

Debt 63.1%

Financing amounts

Equity 25,909

Debt 44,330

Total Kansas Crossing 70,239

17

Kansas Crossing – Conclusion

• It is our opinion KC’s equity members have sufficient available liquid assets to fund their

cash equity commitments and absorb cost overruns

• Based on our financial projections, the leverage ratio of 5.2x in 2019 is towards the high end

of the tolerable range for a greenfield casino development project

• However, firm commitment letters with indicative pricing and terms have been

secured for both the KCRE and KCH debt components

• Furthermore, based on our financial projections, there is minimal excess free cash flow

after accounting for the required annual debt service payments (principal and interest), the

preferred return to the equity investors of KCRE and annual maintenance capital

expenditures

• Therefore, it is possible that some of these annual obligations may not be able to be

paid in the event that the projected revenue and EBITDA numbers are less than

expected

www.uniongaminggroup.com