usa v harter jurisdictional challenge 101013 doc 89 - 047112581767 ocr

DESCRIPTION

Dr Thomas W Harter challenges the jurisdiction of the US District Court in Florida's Middle District that convicted him of willful failure to fileTRANSCRIPT

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 1 of 65 PageID 961

Case styled:

UNITED STATES DISTRICT COURT MIDDLE DISTRICT OF FLORIDA

OCALA DIVISION

UNITED STATES OF AMERICA

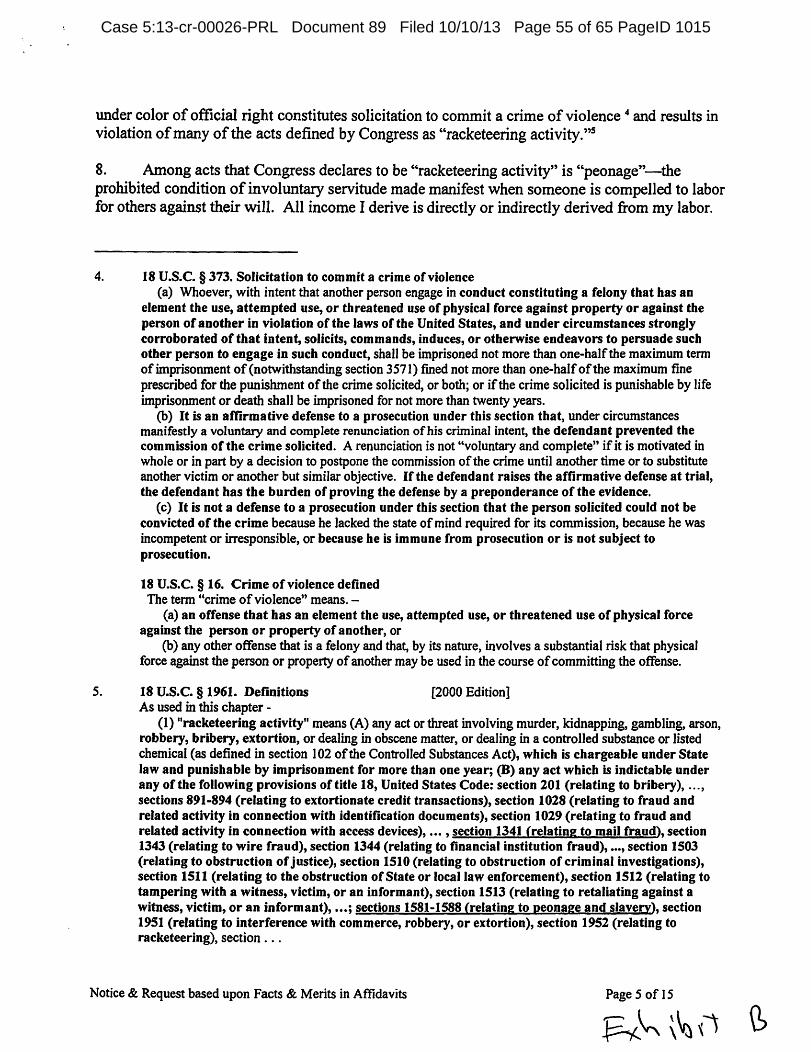

FILED

"q 13 OCT I 0 PM I: 5 i

CASE NO. 5: 13-cr-26-0c-22PRL v.

THOMAS W. HARTER

Harter's JURISDICTIONAL CHALLENGE; REJECTION TO ALLEGED CONVICTION; OFFICIAL MISCONDUCT CHARGE; and

DEMAND IN THE NAME OF JUSTICE

I, Thomas William Harter, asserting my inalienable rights as a sovereign on this great

land known as the United States of America 1 , having discharged Mark Schleben as my

[NOTE: emphasis in quotes added by Harter]

"For when the revolution took place, the people of each state became themselves sovereign; .... subject only to the rights since surrendered by the constitution to the general government." Martin v. Waddell, 41 US 367, 410 (1842)

"Congress can exercise no power by virtue of any supposed inherent sovereignty in the general government. Indeed, it may be doubted whether the power can be correctly said to appertain to sovereignty in any proper sense, as an attribute of an independent political community. The power to commit violence, perpetrate injustice, take private property by force without compensation to the owner, and compel the receipt of promises to pay in place of money, may be exercised, as it often has been, by irresponsible authority, but it cannot be considered as belonging to a government founded upon law. But be that as it may, there is no such thing as a power of inherent sovereignty in the government of the United States. It is a government of delegated powers, supreme within its prescribed sphere, but powerless outside of it. In this country, sovereignty resides in the people, and congress can exercise no power which they have not, by their constitution, intrusted to it; all else is withheld." Juil/ard v. Greenman 'The Legal Tender Cases', 110 U.S. 421, 467 (1884)

"Under our system the people, who are there called subjects, are the sovereign. Their rights, whether collective or individual, are not bound to give way to a sentiment of loyalty to the person of the monarch. The citizen here knows no person, however near to those in power, or however powerful himself, to whom he need yield the rights which the law secures to him when it is well administered. When he, in one of the courts of competent jurisdiction, has established his right to property, [ 106 U.S. I 96, 209] there is no reason why deference to any person, natural or artificial, not even the United States,

Case No: 5:13-cr-00026-PRL-l Page I of32 Harter,s JURISDICTIONAL CHALLENGE; REJECTION TO ALLEGED CONVICTION;

OFFICIAL MISCONDUCT CHARGE; and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 2 of 65 PageID 962

attorney, appear now in propria persona (in my own person) and sui juris (of right) to challenge

jurisdiction 2 (administrative and judicial) and reject the contention that proceedings and alleged

guilty verdict in this Court's Case No. 5:13-cr-26-0c-22PRL (hereinafter this case) have any

foundation in law; and to charge United States (U.S.) Attorney Robert E. O'Neill, Assistant U.S,

Attorney Samuel D. Armstrong, and Criminal Division Deputy Chief Karen L. Gable with

misconduct in office3 ; and to make demands in the name of justice, fair play, and honesty in

government.

1. I, Thomas William Harter, declare under penalties of perjury the personal facts stated

herein are true and correct, and the facts as to law are materially complete, not intended to

mislead anyone, and are true and correct to the best of my knowledge and belief.

2. This is presented in affidavit form for it to stand admissible without any extrinsic

should prevent him from using the means which the law gives him for the protection and enforcement of that right." US v. LEE, 106 U.S. 196. 20 I, 209-210 ( 1882)

"In the United States, sovereignty resides in the people who act through the organs established by the Constitution. Chisholm v. Georgia, 2 Dall. 419, 471; Penhallow v. Doane's Administrators, 3 Dall. 54, 93; McCulloch v. Maryland, 4 Wheat. 316, 404, 405; Yick Wo v. Hopkins, 118 U.S. 356. 370, 6 S.Ct. 1064. The Congress as the instrumentality of sovereignty is endowed with certain powers to be exerted on behalf of the people in the manner and with the effect the Constitution ordains. The Congress cannot invoke the sovereign power of the people to override their will as thus declared. Perry v. United States, 294, U.S. 330, 353 (1935)

2 "Where jurisdiction is challenged, it must be proven. The law required proof of jurisdiction to appear on the proceedings ... Jurisdiction may never be assumed, it must be proven. Hagen v. Lavine, 415 U.S. 528, 533, 39 L.ed 577, 94 S.Ct., (N.Y. March 28, 1974). "Jurisdiction once challenged cannot be assumed and must be decided." State of Maine v. Thiboutot, 448 U.S. I, 100 S.Ct. 2502 (1980). "No sanction can be imposed absent proof of jurisdiction." Standard v. Olsen, 74 S.Ct. 768

3 Misconduct in office. Any unlawful behavior by a public officer in relation to the duties of his office, willful in character. Term embraces acts which the office holder had no right to perform, acts performed improperly, and failure to act in the face of an affirmative duty to act. See also Malfeasance; Misfeasance Black's Law Dictionary, Fifth Edition (1979)

Case No: 5:13-cr-00026-PRL-1 Page 2 of32 Harter's JURISDICTIONAL CHALLENGE: REJECTION TO ALLEGED CONVICTION;

OFFICIAL MISCONDUCT CHARGE; and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 3 of 65 PageID 963\

evidence of authenticity 4 and under the established Common Law maxim that an affidavit is a

presentment which if unrebutted becomes truth in commerce and fact in law.

3. Being a man who has never had any formal schooling in law, I notice this Court of

enunciation of principles as stated in Haines v. Kerner:i. 404 U.S. 519 (1972), wherein that court

directed that those who are unschooled in law making pleadings and/or complaints shall have the

court look to the substance of the writings rather than the form. Based thereon, this Court is

asked to interpret this writing fairly and in light of strict constitutional standards, no matter how

"inartful," and not hold me to the same standard as a practicing attorney. This was restated by

the Supreme Court ten years later in its Boag v. MacDougall, 454 U.S. 364 (1982) ruling. Both

of these rulings have been relied upon in lower court opinions.

STATEMENT AND FACTS OF THE CASE

4. This case was opened based upon the unattested INFORMATION writing over the

signatures of Samuel D. Armstrong and Karen L. Gable, acting on behalf of Robert E. O'Neill

(hereinafter referred to jointly as the U.S. Attorneys). In it they charge defendant THOMAS W.

HARTER with "violation of Title 26, United States Code, Section 7203" (hereinafter IRC or 26

U.S.C) as to years 2006, 2007, 2008, 2009 2010, 2011 (six (6) counts). Having no knowledge

of courtroom process and procedures, I hired an attorney. After the filing of much paperwork

and a few hearings, a proceeding called trial, conducted by Magistrate Judge Philip R. Lammens,

ended on 09/1712013 with a group of people sitting in the jury box declaring me guilty on all

4 Rule 902. Self-authentication Federal Rules of Evidence Extrinsic evidence of authenticity as to condition precedent to admissibility is not required with

respect to the following: (8) Acknowledged documents.-Documents accompanied by a certificate of acknowledgment executed in the manner provided by law by a notary public or other officer authorized by law to take acknowledgments.

Case No: 5:13-cr-00026-PRL-l Page 3 of32 Harter's JURISDICTIONAL CHALLENGE; REJECTION TO ALLEGED CONVICTION;

OFFICIAL MISCONDUCT CHARGE; and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 4 of 65 PageID 964

counts (all of whom are believed to be 1040 form filers and pay what they presume is a lawful

tax on their income; rendering it impossible for them to be impartial).

5. The U.S. Attorneys failed to support their Information charge with a probably cause

statement under oath as required by Rule 9, Federal Rules of Criminal Procedure. The

presentment of a probable cause statement under oath authorizes the Clerk of the Court to issue a

Warrant or Summons for the accused to appear. I have never seen a Summons or probable cause

statement under oath, and have reason to believe none exists since such documents do not appear

on the Court Docket list for this case. This would seem to be a fatal administrative flaw, but

neither this nor any other administrative fault is the premise for my rejecting the validity of this

case and the alleged conviction. What is being presented in this affidavit is authoritative

evidence as to the Constitution, IRC statutes, regulations, and court rulings that prove this case to

be a mistrial ab initio. 5

STATEMENT OF ISSUES & STANDARD OF REVIEW

6. Notwithstanding this case was opened based upon violation of a statute and appears to

have been conducted by an administrative tribunal thus far, the true issue is exertion of

unauthorized administrative power resulting in infringement of my inalienable rights; a matter

cognizable only in an Article III Court.

"When Congress passes an Act empowering administrative agencies to carry on governmental activities, the power of those agencies is circumscribed by the authority granted. This permit the [321 U.S. 288, 31 O] courts to participate in law enforcement entrusted to administrative bodies only to the extent necessary to protect justiciable individual rights against administrative action

5 Mistrial. An erroneous, invalid, or nugatory trial. A trial of an action which cannot stand in law because of want of jurisdiction, or a wrong drawing of jurors, or disregard of some other fundamental requisite before or during trial. Trial which has been terminated prior to its normal conclusion. The judge may declare a mistrial because of some extraordinary event (e.g. death of juror, or attorney), for prejudicial error that cannot be corrected at trial, or because of a deadlocked jury. Black's Law Dictionary, Fifth Edition ( 1979)

Case No: 5:13-cr-00026-PRL-1 Page 4 of32 Harter's JURISDICTIONAL CHALLENGE; REJECTION TO ALLEGED CONVICTION;

OFFICIAL MISCONDUCT CHARGE; and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 5 of 65 PageID 965

fairly beyond the granted powers. The responsibility of determining the limits of statutory grants of authority in such instances is a judicial function entrusted to the courts by Congress by the statutes establishing courts and marking their jurisdiction. Cf. United States v. Morgan, 307 U.S. 183. 190 , 191 S., 59 S.Ct. 795, 799. This is very far from assuming that the courts are charged more than administrators or legislators with the protection of the rights of the people. Congress and the Executive supervise the acts of administrative agents. The powers of departments, boards and administrative agencies are subject to expansion, contraction or abolition at the will of the legislative and executive branches of the government. These branches have the resources and personnel to examine into the working of the various establishments to determine the necessary changes of function or management. But under Article m. Congress established courts to adjudicate cases and controversies as to claims of infringement of individual rights whether by unlawful action of private persons or by the exertion of unauthorized administrative power." Stark v .. Wickard, 321 U.S. 288, 309-310 (1944)

7. The U.S. Supreme Court has ruled: "There are no constructive offenses; and before

one can be punished, it must be shown that his case is plainly within the statute." Fasulo v.

United States, 272 U.S. 620, 629 (1926); brought forward by being quoted in McNally v. United

States., 483 U.S. 350, 360 (1987). There is no ambiguity in this ruling (command). It clearly

states my being duly convicted stands or falls upon me and my estate (real or personal) being

within IRC statutes. Congress identifies precisely who can be duly punished under IRC chapter

75 statutes(§§ 7201-7344) by the definition of"person" for chapter 75.

26 U.S.C. § 7343. Definition of term "person." The term "person" as used in this chapter includes an officer or employee of a corporation, or a

member or employee of a partnership, who as such officer, employee, or member is under a duty to perform the act in respect of which the violation occurs.

This establishes IRC chapter 75 statutes merely prescribe sanctions for violation of a duty to

perform some act stated elsewhere in IRC statutes, and makes clear a charge for violation of IRC

chapter 75 statutes cannot stand as complete without charging the accused as being the IRC §

7343 person and stating the IRC statute(s) that imposes a duty upon the accused "to perform the

act in respect of which the violation occurs."

8. I was allegedly charged and convicted for violation of26 U.S.C. § 7203.

26 U.S.C. § 7203. [in part] Willful failure to file return, supply information, or pay tax.

Case No: 5:13-cr-00026-PRL-1 Page 5of32 Harter's JURISDICTIONAL CHALLENGE; REJECTION TO ALLEGED CONVICTION;

OFFICIAL MISCONDUCT CHARGE; and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 6 of 65 PageID 966

Any person required under this title to pay any estimated tax or tax, or required by this title or by regulations made under authority thereof to make a return, keep any records, or supply any information, who willfully fails to ... at the time or times required by law or regulations, shall, in addition to other penalties provided by law, be guilty of a misdemeanor and, upon conviction thereof, shall be fined ... or imprisoned ... or both ...

Again, this states the duty (requirement) is under some other IRC statute(s). None are stated in

the Information used to initiate this case against me; rendering the entire case and alleged

conviction to be based upon presumptions and personal opinions of officers of this Court and the

twelve people sitting in the jury box; and not due process of law.6

9. I, Thomas William Harter, declare and present proof at law, that IRC statutes are based

upon special legislation (applicable to particular persons and things) that cannot be lawfully

applied upon me or any contract whereby I derive income from labor or otherwise. Support for

this is memorialized in my MEMORANDUM OF LAW (16 page affidavit) executed on

0911012004 (copy attached as Exhibit A) and filed into Marion County, Florida, public records

on 07/28/2005 as #2005132677, at Book 04119, pages 1281-1297. Since it was executed it has

been presented many times to officials of the Department of the Treasury (DOT) and its

enforcement arm, the Internal Revenue Service (IRS); sometimes directly and sometimes

through their agents/employees. I never received a rebuttal thereto, not even when made a part

of my AFFIDAVIT OF FACTS & MERITS (15 page affidavit; copy attached as Exhibit B)

mailed on 05/18/2006 to Mark W. Everson (the then IRS Commissioner), his agents in Ocala,

6 Due process of law. [in part] Law in its regular course of administration through courts of justice. Due process of law in each particular case means such an exercise of the powers of the government as the settled maxims of law permit and sanction, and under such safeguards for the protection of individual rights as those maxims prescribed for the class of cases to which the one in question belongs. A course of legal proceedings according to those rules and principles which have been established in our systems of jurisprudence for the enforcement and protection of private rights. Black's Law Dictionary, Fifth Edition ( 1979)

Case No: 5:13-cr-00026-PRL-l Page 6 of32 Harter's JURISDICTIONAL CHALLENGE: REJECTION TO ALLEGED CONVICTION;

OFFICIAL MISCONDUCT CHARGE: and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 7 of 65 PageID 967

FL, and Ogden, UT, and sent to Senators Bill Nelson and Mel Martinez, and Representative Cliff

Stearns.

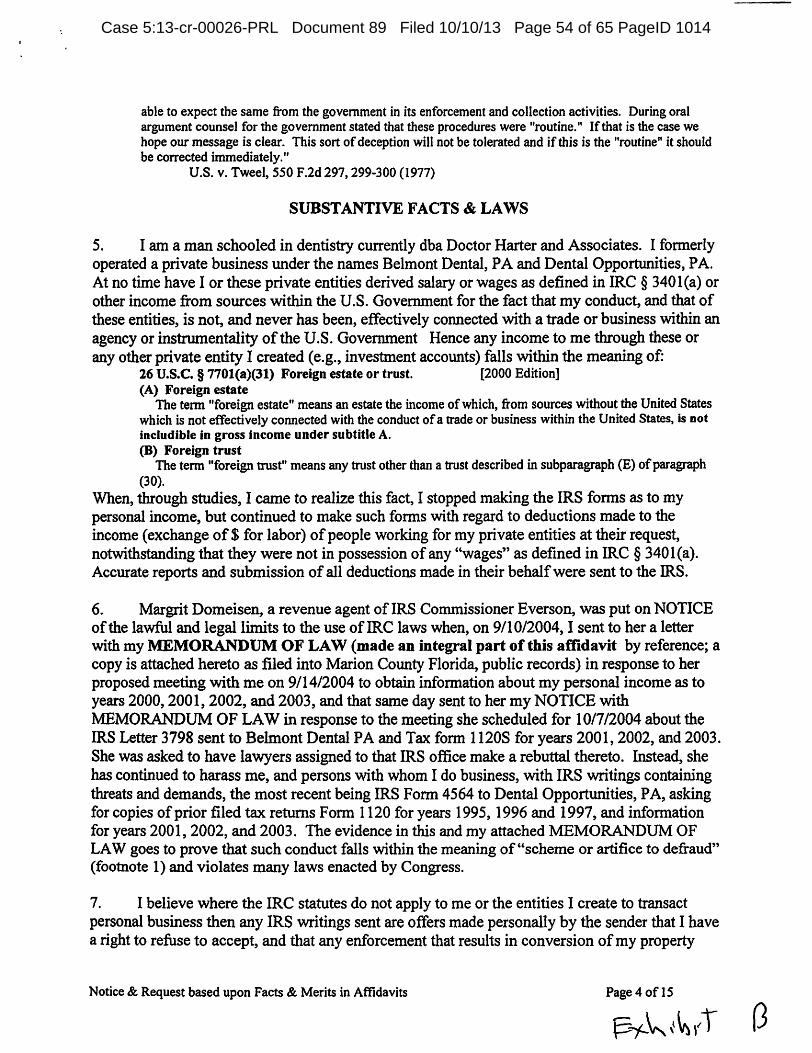

10. Exhibits A and Bare made an integral part of this affidavit as if fully restated. Under

established principles I doctrines, the silence of DOT/IRS officials thereto stands as a tacit

acknowledgement to the veracity of what is stated therein 7 and an admission to the following

(reprinted from the summation in Exhibit B, paragraph 15, omitting references therein to other

parts of that affidavit).

(a) that Congress did not impose a tax upon income; (b) that the IRC subtitle A statutes are part of a bailment for mutual benefit program between the

U.S. Government and human beings employed within an agency or instrumentality of the U.S. Government-Le, the IRC § 770l(a)(30)(A) United States person;

(c) that this bailment program creates an obligation for such United States person to make a return of the U.S. Government's property transferred into their possession that they are not under IRC subtitle A and F law permitted to retain;

( d) that IRC subtitle F statutes provide authority to the IRS for recaption of property possessed by the U.S. Government though in the possession of such United States persons;

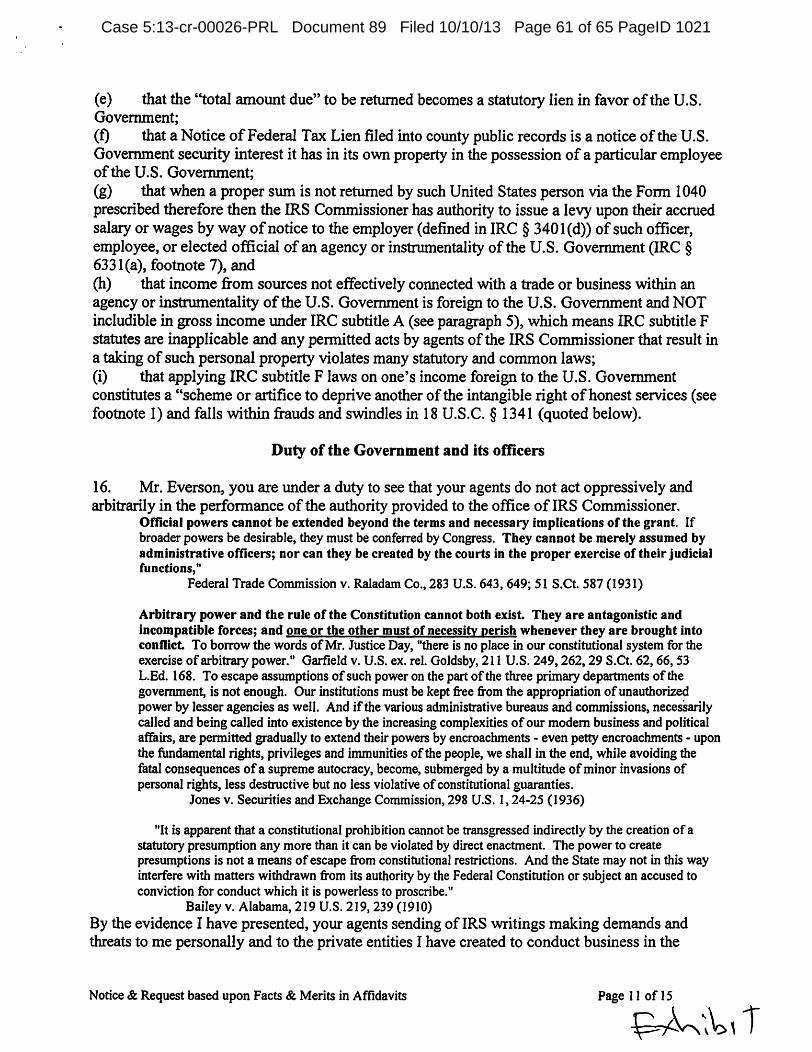

(e) that the "total amount due" to be returned becomes a statutory lien in favor of the U.S. Government;

(f) that a Notice of Federal Tax Lien filed into county public records is a notice of the U.S. Government security interest it has in its own property in the possession of a particular employee of the U.S. Government;

(g) that when a proper sum is not returned by such United States person via the Form 1040 prescribed therefore then the IRS Commissioner has authority to issue a levy upon their accrued salary or wages by way of notice to the employer (defined in IRC § 340l(d)) of such officer, employee, or elected official of an agency or instrumentality of the U.S. Government (IRC § 63 31 (a));

(h) that income from sources not effectively connected with a trade or business within an agency or instrumentality of the U.S. Government is foreign to the U.S. Government and NOT includible in gross income under IRC subtitle A, which means IRC subtitle F statutes are inapplicable and any permitted acts by agents of the IRS Commissioner that result in a taking of such personal property violates many statutory and common laws; and

(i) that applying IRC subtitle Flaws on one's income foreign to the U.S. Government constitutes a "scheme or artifice to deprive another of the intangible right of honest services and falls within frauds and swindles in 18 U .S.C. § 1341.

7 "Silence is a species of conduct, and constitutes an implied representation of the existence of the state of

facts in question, and the estoppel is accordingly a species of estoppel by misrepresentation ..... Even when the statute of frauds has been relied on, the equitable doctrine of estoppel has been enforced to prevent fraud. Goldman v. Brinton, 90 Md. 259, 44. Atl. 1029." Carmine v. Bowen, 104 Md. 198, 64 Ad.Rep. 932, 934 (1906).

Case No: 5:13-cr-00026-PRL-1 Page 7 of32 Harter's JURISDICTIONAL CHALLENGE; REJECTION TO ALLEGED CONVICTION;

OFFICIAL MISCONDUCT CHARGE: and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 8 of 65 PageID 968

11. Being strictly a matter of law, the standard of review is restricted to whether or not I and

my estate (real or personal) fall within IRC statutory authority; wherefore, I declare

administrative process, procedures, and court rules are irrelevant and immaterial; and reject any

use of them as a diversion from the substantive and only issue-i.e., conclusively disproving the

authoritative evidence presented by me that establishes IRC statutes have no lawful force or

effect upon me or my estate.

12. The U.S. Supreme Court has ruled (commanded):"the responsibility of determining the

limits of statutory authority is a judicial function (see, Stark v. Wickland, 321 U.S. 288, 309

(1944)) and the job of the judge is to apply the law, not to bolster the government's case

(see, Beaty v. U.S., 937 F.2d 288, 293 (Sixth Cir. 1991)). Wherefore the onus is placed upon this

district court of the U.S. Government, sitting as a Court oflaw and justice and not as an

administrative tribunal (as it appears to have been thus far), through Magistrate Judge Philip R.

Lammens, to disprove the authoritative evidence in this affidavit and Exhibits A and B, and

bring forth the enactment by the U.S. Congress that compels a human being to pay a tax on their

income via an IRS Form 1040 and upon evidence of willful failure to do so the criminal

sanctions in 26 U.S.C. § 7203 can lawfully be enforced by this Court. I believe, and declare,

justice, fair play, and honesty in government requires the Court to perform the foregoing, OR sua

sponte declare this case a mistrial, and render the verdict void. A showing of good faith in this

matter will be on record if one or the other of these options is on record no later than thirty (30)

days before the sentencing date, currently scheduled for 12110/2013.

DOT/IRS JURISDICTION (AUTHORITY)

13. Like the U.S. Attorneys, the Secretary of the Treasury and the IRS Commissioner are

under a duty to know the /awfu./ limits to the enforcement of IRC statutes and adhere strictly

Case No: 5:13-cr-00026-PRL-1 Page 8 of32 Harter's JURISDICTIONAL CHALLENGE; REJECTION TO ALLEGED CONVICTION;

OFFICIAL MISCONDUCT CHARGE; and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 9 of 65 PageID 969

thereto. They have a correlative duty to properly train their agents/employees to assure strict

adherence to the law. Wherefore, the sending of IRS writings to human beings not subject to

IRC statutes evidences deliberate, arbitrary, operation outside the scope of their office and an

intentional abuse of IRS power, process, and procedures by failing to instruct their

agents/employees that IRC statutes are based upon special law (enactments applicable to

particular persons and things) and identify specifically upon whom and what IRC statutes can

lawfully be applied. In so doing they not only breach their fiduciary to the public 8 but to their

agents/employees.

14. Courts have made it clear that: "With the IRS's broad power must come a

concomitant responsibility to exercise it within the confines of the law." Bothke v. Fluor

Engineers and Constructors, Inc., 713 F.2d 1405 (1983), 9th Cir.; relying upon Butz et al v.

Eonomou et al., 438 U.S. 4 78 at 505-506. These Courts emphasized that no official is above the

law, and that broad powers present broad opportunities for abuse." DOT/IRS officials operate

outside the confines of their office when they permit entries be placed into the DOT/IRS system

of records that have no nexus to IRC statutes, thus such entries constitute false writings (see 18

U.S.C. § 1001) and evidence an abuse of DOT/IRS authority.

15. By promulgation of regulation 26 CFR 601.106(t)(l)~ the DOT Secretary recognizes:

'~An exaction by the U.S. Government, which is not based upon law, statutory or otherwise~ is a

taking of property without due process of law, in violation of the Fifth Amendment.~·

8 "A public official is a fiduciary toward the public" and that fraud "includes the deliberate concealment of material information in a setting of fiduciaD' obligation.~' In addressing schemes to defraud and intangible rights, the McNallv Court stated at page 358: "This is the approach that has been taken by each of the Courts of Appeals that has addressed the issue: schemes to defraud include those designed to deprive individuals, the people, or the government of intangible rights, such as the right to have public officials perform their duties honestly. See, e.g., United States v. Clapps. 732 F.2d 1148, 1152 (CA3 1984); United States v. States, 488 F.2d 761, 764 (CA8 1973)." McNallv v. United States, 483, .S. 350, 372 (1987)

Case No: 5: 13-cr-00026-PRL- I Page 9 of 32 Haner's JURISDICTIONAL CHALLENGE; REJECTION TO ALLEGED CONVICTION;

OFFICIAL MISCONDUCT CHARGE; and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 10 of 65 PageID 970

Substantive due process is the right to be protected from arbitrary and wrongful government

action regardless of the fairness of the procedures government uses to undertake the arbitrary

action. Zinermon v. Burch, 494 U.S. 113 (1990)

LIMITS TO LAWFUL ENFORCEMENT OF IRC STATUTES

16. The authoritative proofs herein and in Exhibits A and B establish IRC statutes have no

lawful application upon me or my estate (real or personal); all of which is derived through

exercise of my right to contract and work in my chosen lawful trade I vocation and thereby

acquire property; a right I liberty long established as inalienable and secured under the

Constitution of the United States of America. 9

9 "The right to follow any of the common occupations of life is an inalienable right. It was fonnulated as such under the phrase 'pursuit of happiness' in the Declaration of Independence." Allgeyer v. State of Louisiana, 165 U.S. 578. 17 S.Ct. 427, 41L.Ed.832 (1897). Hotel, et al. v. Longley, eta/ .. 160 S.W.2d 124, 127 (1942).

"Included in the right of personal liberty and the right of private property -- partaking of the nature of each -- is the right to make contracts for the acquisition of property. Chief among such contracts is that of personal employment, by which labor and other services are exchanged for money or other forms of property." Coppage v. Kansas, 236 U.S. I, 14 (1915).

"The property which every man has in his own labor, as it is the original foundation for all other property. so it is the most sacred and inviolable. The patrimony of the poor man lies in the strength and dexterity of his own hands, and to hinder his employing this strength and dexterity in what manner he thinks proper. without injury to his neighbor, is a plain violation of this most sacred property." Butchers Union Co. v. Crescent City Co., 111 U.S. 764.

"We also think the right to work is one of the most precious liberties that man possesses. Man has as much right to work as he has to live, to be free, to own property, or to join a church of his own choice for without freedom to work the others would soon disappear. It is a fundamental human right which the due process clause of the Fifth Amendment protects from improper infringement by the federal government. To work for a living in the occupations available in a community is the very essence of personal freedom and opportunity that it was one of the purposes of these amendments to make secure. Liberty means more than freedom from servitude. The constitutional guarantees are our assurance that the citizen will be protected in the right to use his powers of mind and body in any lawful calling." Referenced from Smith v. State o/Texas, 233 U.S. 630 (1913) in Hanson v. U.P.RR. Co.~ 71 N.W. 526, 546 (1955).

Case No: 5: 13-cr-00026-PRL-1 Page 10 of32 Harter·s JURISDICTIONAL CHALLENGE; REJECTION TO ALLEGED CONVICTION~

OFFICIAL MISCONDUCT CHARGE: and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 11 of 65 PageID 971

17. IRC subtitle A statutes have been misrepresented and propagandized as imposing a

federal tax on what one derives from their labor and other income. Because of this human beings

living on the land called the United States of America are predisposed to execute and submit

1040 forms to the IRS along with their property 10 though "The Right to receive income or

earnings is a right belonging to every person and realization and receipts of income is therefore

not a ''privilege that can be taxed." (Taxation Key, West 933); thus they perform such act based

upon false belief and custom 11, not law. Ignorance to the truth with regard to this matter is

perpetuated with the aid of Department of Justice (DOJ) attorneys instituting court actions

against people and property not subject to IRC statutes, like me and my property. Judges tend to

permit the government to prevail in such actions notwithstanding the job of a judge is to apply

the law, not to bolster the government's cause. 12 In so doing, it seems to me that

"Constitutional rights would be of little value if they could be ... indirectly denied" Smith v. Al/wright, 321

U.S. 649, 664. " ... or 'manipulated out of existence' "Gomillion v. Lightfoot, 364 U.S. 339. 345.

"It is apparent that a constitutional prohibition cannot be transgressed indirectly by the creation of a statutory presumption any more than it can be violated by direct enactment. The power to create presumptions is not a means of escaping from constitutional restrictions. And the State may not in this way interfere with matters withdrawn from its authority by the Federal Constitution or subject an accused to conviction for conduct which it is powerless to proscribe." Bailey v. Alabama, 219 U.S. 219, 239 (1910)

10 "Because what appears to be a lawful command on the surface, many citizens, because of their respect for the law, are cunningly coerced into waiving their rights, due to ignorance." U.S. v._Minker, 350 U.S. 179. 187(1956)

11 Consuetudo licet sit magnre auctoritatis, nunquam tamen, prrejudicat manifestre veritati. A custom, though it be of great authority, should never prejudice manifest truth. Black's Law Dictionary, Fifth Edition ( 1979) Pg. 286

Consuetudo contra rationem introducta potius usurpatio quam consuetudo appellari debet A custom introduced against reason ought rather to be called a "usurpation" than a "custom." Black's Law Dictionary, Fifth Edition ( 1979) Pg. 285

12 '"A central tenet of our republic-a characteristic that separates us from totalitarian regimes throughout the world-is that the government and private citizens resolve disputes on an equal playing field in the

Case No: 5:13-cr-00026-PRL-l Page 11of32 Harter's JURISDICTIONAL CHALLENGE: REJECTION TO ALLEGED CONVICTION:

OFFICIAL MISCONDUCT CHARGE: and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 12 of 65 PageID 972

Government officials who take office swearing to uphold the Constitution of the United States of

America violate their oath of office and their duty to protect and defend the right of the people to

life~ liberty and property against invasion by enemies, foreign and domestic.

18. It is well established that a tax upon one's estate, whether derived from labor or other

contract, is direct taxation. 13 Constitutional requirement for the imposition of direct taxation is

that it be apportioned. There is no provision for apportionment in the IRC - which can only

mean none of the statutes in the IRC impose a direct tax on anyone or anything. Also, with

Congress having declared ''The labor of a human being is not a commodity or article of

commerce" (15 U.S.C. § 17), what is termed "federal income tax"' cannot represent indirect

taxation upon articles of commerce. Thus the Federal income tax" return program in IRC

subtitle A statutes must be something other than taxation, and so proved by the authoritative

evidence presented in this affidavit and Exhibits A and B.

19. The U.S. Supreme Court conditionally recognized the "federal income tax" return

program as an excise unless and until its enforcement converts it to direct taxation 14 • in which

courts. When citizens face the government in the federal courts, the job of the judge is to apply the law, not to bolster the government's case." Beaty v U.S., 937 F.2d 288, 293 (Sixth Cir. 1991)

l:l Customs & duties -title 19 U.S.C.; regulation - 19 CFR 351.102. Definitions: Direct Tax. "Direct tax" means a tax on wages, profits, interests, rents, royalties, and all other forms of income, a tax on the ownership of real property. or a social welfare charge.

"Ordinarily, an taxes paid primarily by persons who can shift the burden upon someone else, or who are under no legal compulsion to pay them, are considered indirect taxes; but a tax upon property holders in respect of their estates, whether real or personal, or of the income yielded by such estates, and the payment of which cannot be avoided, are direct taxes." Pollock v. Farmers' Loan & Trust Co., 157 U.S. 429, 558 (1895)

"Direct taxes bear immediately upon person, upon possession and the enjoyment of rights." Knowlton v. Moore, 178 U.S. 41, 47 (1900)

14 "Moreover, in addition, the conclusion reached in the Pollock Case did not in any degree involve holding that income taxes generically and necessarily came within the class of direct taxes on property~

Case No: 5: l 3-cr-00026-PRL-1 Page 12 of 32 Harter's JURISDICTIONAL CHALLENGE; REJECTION TO ALLEGED CONVICTION:

OFFICIAL MISCONDUCT CHARGE; and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 13 of 65 PageID 973

instance the Court is required to disregard form (administrative process and procedures., and

court rules) and consider substance alone (substantive issues; e.g., unauthorized taking of

property through wrongful IRC administration 15).

20. The U.S. Supreme Court has ruled: "we think it important to note that the Act's civil and

criminal penalties attach only upon violation of regulations promulgated by the Secretary; if the

Secretary were to do nothing, the Act itself would impose no penalties on anyone" California

Bankers Assn. v. Schultz, 416 U.S. 21, 26 (1974). Congress commanded regulations having

general applicability be published in the Federal Register (see 44 U.S.C. § 1501 et. seq.) and a

list of such regulations be published (44 U.S.C. § 1510). Such list is published in the Table of

Authorities of the Code of Federal Regulations (CFR) Index and Finding Aids; the preface to

which shows exclusion of regulations published pursuant to 5 U.S.C. § 301 16 to conform with

the exception of "those not having general applicability and legal effect or effective only against

Federal agencies or persons in their capacity as officers, agents, or employees thereof' ( 44

U.S.C. § 1505(a)).

but. on the contrary, recognized the fact that taxation on income was in its nature an excise entitled to be enforced as such unless and until it was concluded that to enforce it would amount to accomplishing the result which the requirement as to apportionment of direct taxation was adopted to prevent, in which case the duty would arise to disregard fonn and consider substance alone. and hence subject the tax to the regulation as to apportionment which otherwise as an excise would not apply to it."

Brushaberv. Union Pacific Railroad Co., 240 U.S. I, 16-17 (1915)

15 "A valid law may be wrongfully administered by officers of the state. and so as to make such administration an illegal burden and exaction upon the individual. A tax law, as it leaves the legislative hands, may not be obnoxious to any challenge; and yet the officers charged with the administration of that valid tax law may so act under it, in the matter of assessment or f 154 U.S. 362, 391 ) collection, as to work an illegal trespass upon the property rights of the individual. They may go beyond the powers thereby conferred, and when they do so the fact that they are assuming to act under a valid law will not oust the courts of jurisdiction to restrain their excessive and illegal acts.'' Reagan v. Farmers' Loan & Trust Co., 154 U.S. 362, 391-392 (1894).

16 Title 5 United States Code, Government Organization and Employees, and Appendix.

Case No: 5: 13-cr-00026-PRL-l Page 13 of 32 Harter's JURISDICTIONAL CHALLENGE; REJECTION TO ALLEGED CONVICTION;

OFFICIAL MISCONDUCT CHARGE; and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 14 of 65 PageID 974,.

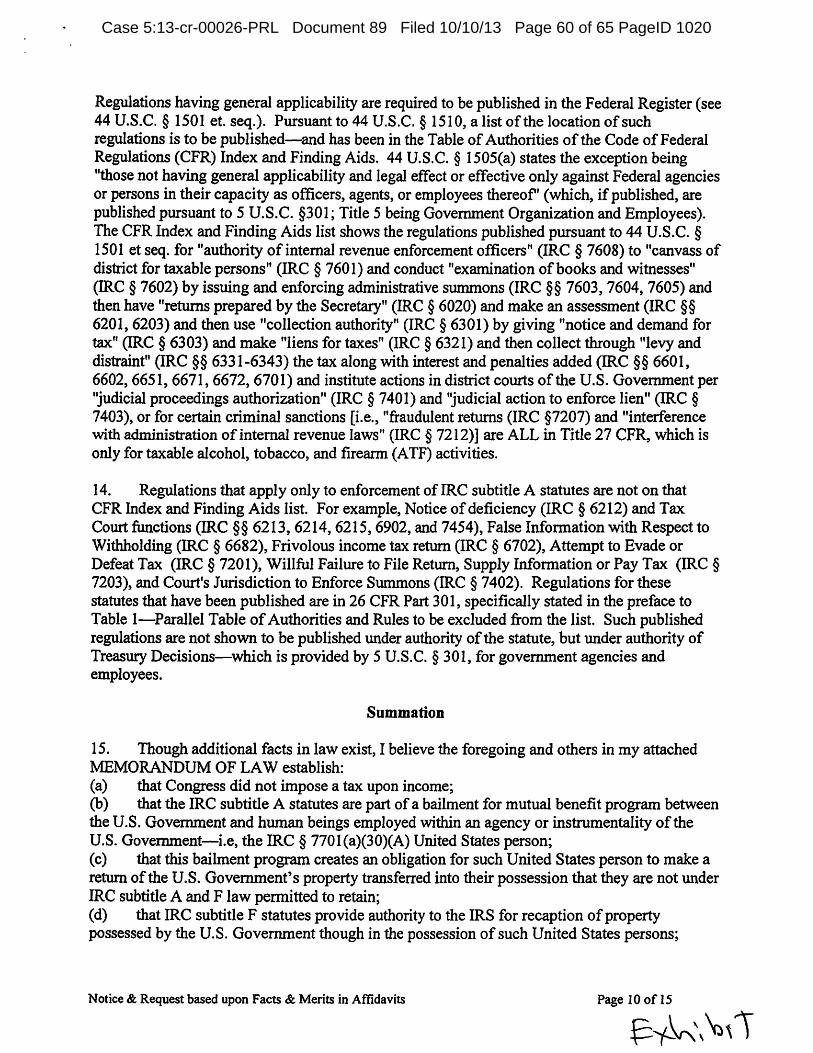

21, The limited enforcement authority provided to the DOT/IRS by IRC subtitle F statutes is

made clear by the CFR Index and Finding Aids Table of Authorities list which shows regulations

published pursuant to 44 U.S.C. § 1501 et seq. for "authority of internal revenue enforcement

officers" (IRC § 7608) to "canvass of district for taxable persons" (IRC § 7601) and conduct

"examination of books and witnesses" (IRC § 7602) by issuing and enforcing administrative

summons (IRC §§ 7603, 7604, 7605) and then have "returns prepared by the Secretary" (IRC §

6020) and make an assessment (IRC §§ 6201, 6203) and then use "collection authority" (IRC §

6301) by giving "notice and demand for tax" (IRC § 6303) and make "liens for taxes" (IRC §

6321) and then collect through "levy and distraint" (IRC §§ 6331-6343) the tax along with

interest and penalties added (IRC §§ 6601. 6602, 6651, 6671, 6672, 6701) and institute actions

in district courts of the U.S. Government per "judicial proceedings authorization" (IRC § 7401)

and "judicial action to enforce lien" (IRC § 7403), or for certain criminal sanctions [i.e ..

"fraudulent returns (IRC § 7207) and "interference with administration of internal revenue laws"

(IRC § 7212)] are ALL IN Title 27 CFR, which is only for taxable alcohol, tobacco, and

firearm (ATF) activities. Those with no regulations published pursuant to 44 U.S.C. § 1501 et

seq. are the Notice of deficiency (IRC § 6212) and Tax Court/unctions (e.g., IRC §§ 6213.

6214, 6215, 6673, 6902, and 7454), False Information with Respect to Withholding (IRC §

6682), Frivolous income tax return (IRC § 6702), Attempt to Evade or Defeat Tax (IRC §

7201), Willful Failure to File Return, Supply Information or Pay Tax (IRC § 7203) .. and

Court's Jurisdiction to Enforce Summons (IRC § 7402); which means these are applicable

only to gross income derived from U.S. Government agencies or instrumentalities by the U.S.

i11dividual (the 26 U.S.C. § 770l(a)(30)(A) U.S. person) and t/1e replevin of the part oftlie

"Federal income tax" (U.S. public/government property) in tlieir possession that is required to

Case No: 5:13-cr-00026-PRL-1 Page 14 of32 Harter's JURISDICTIONAL CHALLENGE: REJECTION TO ALLEGED CONVICTION:

OFFICIAL MISCONDUCT CHARGE; and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 15 of 65 PageID 975" ...

be retumed to the U.S. Treasury. Interestingly, ATF statutes in IRC subtitle E make reference

to the criminal sanctions in IRC chapter 75 being applicable .. whereas no such reference is made

in IRC subtitle A statutes.

22. In brief, IRC statutes are based upon special legislation applicable to particular persons

and things. The authoritative evidence in this affidavit and Exhibits A and B proves the

·"particular persons"' are those associated with IRC subtitle D and E commodities constitutionally

taxable by the U.S. Government, OR those to whom "Federal income tax·' 17 has been transferred

(bailed) as an item of "gross income" with sums paid out of the U.S. Treasury to anyone under

employment contract with U.S. Government agencies or instrumentalities, or an elected or

appointed U.S. Government official. As to the latter, said "gross income" is subject to return to

the U.S. Treasury reduced by deductions and exemptions allowed and reported on particular

DOT/IRS forms by such particular persons (real or artificial); Form 1040 being the instrument

prescribed by regulation for individuals required to make the return required. 18 IRC statutes and

regulations establish the '"particular thing" is property to which the U.S. Government is entitled

either as a tax imposed upon IRC subtitle D and E commodities .. or as a proper return required of

the public's property.

23. The limitations to what is and what is not includible in gross income under IRC subtitle A

to persons in an employment contract within the U.S. Government is confirmed by IRC chapter

24, Collection of income tax at source, IRC § 3401 et. seq. In IRC § 3401(a) Congress defined

17 Logic dictates the term "Federal income tax" is a compound noun for the public's property in the custody and

care of the U.S. Government to be used for legitimate government purposes.

18 26 CFR § 1.6012-1. Individuals required to make returns of income.

(a) Individual citizen or resident --(6) Form of return. Form 1040 is prescribed for general use in making the return required under this paragraph.

Case No: 5: l 3-cr-00026-PRL-1 Page 15 of 32 Harter's JURISDICTIONAL CHALLENGE: REJECTION TO ALLEGED CONVICTION:

OFFICIAL MISCONDUCT CHARGE: and DEMAND IN Tl IE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 16 of 65 PageID 976

. . ~~wages'~ to mean remuneration other than "fees" and specifically excluded remuneration paid for

services for an employer other than the U.S. Government or any of its agencies. 19 Looking to

Black~s Law Dictionary~ Fifth Edition, the word ''fee" is defined as '"A charge fixed by law for

services of public officers or for use of a privilege under control of government."

24. By the fact that I have never been involved in any IRC subtitle D or E taxable activity~

nor employed by any U.S. ~overnment agency or instrumentality (other than being in the Navy

Reserves; 1990-1994), all IRC statutes have no lawful force or effect upon me and my estate

(real and personal); which is foreign to the U.S. Government as defined in 26 U.S.C.

770l(a)(3 l ).20

Authoritative evidence regarding tax "on" income

25. An understanding of the U.S. Government's "~federal income tax" return program and the

U.S. Supreme Court's definition regarding direct and indirect taxation in its Pollock ruling (see

footnotes 13) and the ruling in Brushaber that "taxation on income was in its nature an excise

entitled to be enforced as such unless and until it was concluded that to enforce it would amount

to accomplishing the result which the requirement as to apportionment of direct taxation was

19 26 U.S.C. § 3401. Definitions. [in part] (a) Wages. For purposes of this chapter, the tenn "wages" means all remuneration (other than fees

paid to a public official) for services perfonned by an employee for his employer, including the cash value of all remunerations paid in any medium other than cash; except that such term shall not include remuneration paid-

(8) (A) for services for an employer (other than the United States or any agency thereoO--

20 26 U.S.C. § 770l(a)(31) Foreign estate or trust. [2000 Edition] (A) Foreign estate

The term "foreign estate" means an estate the income of which, from sources without the United States which is not effectively connected with the conduct of a trade or business within the United States, is not includible in gross income under subtitle A. (B) Foreign trust

The term "foreign trust" means any trust other than a trust described in subparagraph (E) of paragraph (30).

Case No: 5: 13-cr-00026-PRL-1 Page 16 of 32 Harter·s JURISDICTIONAL CHALLENGE; REJECTION TO ALLEGED CONVICTION:

OFFICIAL MISCONDUCT CHARGE: and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 17 of 65 PageID 977

adopted to prevent" (see footnote 14) help in understanding the ruling in Kno-wlton v. Moore, 178

US 41, 47 (1900), that: "Direct Taxes bear upon persons, upon possession and the enjoyment of

rights; Indirect Taxes are levied upon the happening of an event." With it recognized and

established that a tax "on" all forms of income (i.e., wages, profits, interests, rents, royalties, and all

other forms of income. a tax on the ownership of real property, or a social welfare charge - see footnote

13) is direct taxation, one must look to what ""happening"' (event) keeps IRC statutes in the classification

of indirect taxation. The event as to IRC subtitle A statutes is the transfer (bailment) of particular

property subject to return to the U.S. Treasury; the event as to IRC subtitle D and E is

involvement with commodities lawfully taxable by the U.S. Government.

26. The above is confirmed by IRC subtitle A statutes only placing a tax upon '"taxable

income" (e.g." see IRC §§ 1and11). Taxable income is defined as '"gain derived from capital,

labor, or both." Eisner v. Macomber, 252 U.S. 189 (1920). However. tax ""on'' capital or labor is

direct taxation and, as so aptly put by the Oregon Supreme Court in Redfield v. Fisher. 292 P

813, pg 819 (1930):

"The individual, unlike the corporation, cannot be taxed for the mere privilege of existing. The corporation is an artificial entity which owes its existence and charter powers to the state: but the individuals' right to live and own property are natural rights for the enjoyment of which an excise cannot be imposed."

With regard to taxing corporations. the U .S, Supreme Court ruled:

"It is therefore well settled by the decisions of this court that when the sovereign authority has exercised the right to tax a legitimate subject of taxation as an exercise of a franchise or privilege, it is no objection that the measure of taxation is found in the income produced in part from property which of itself considered is nontaxable. Applying that doctrine to this case, the measure of taxation being the income of the corporation from all sources, as that is but the measure of a privilege tax within the lawful authority of Congress to impose, it is no valid objection that this measure includes, in part~ at least, property which. as such. could not be directly taxed."

Flint v. Stone Tracy Co., 220 U.S. I 07, 165 (1911)

"As has been repeatedly remarked, the corporation tax act of 1909 was not intended to be and is not, in any proper sense, an income tax law. This court had decided in the Pollock Case that the income tax law of 1894 amounted in effect to a direct tax upon property, and was invalid

Case No: 5: 13-cr-00026-PRL-1 Page 17 of 32 Harter's JURISDICTIONAL CHALLENGE: REJECTION TO ALLEGED CONVICTION:

OFFICIAL MISCONDUCT CHARGE; and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 18 of 65 PageID 978

because not apportioned according to populations, as prescribed by the Constitution. The act of 1909 avoided this difficulty by imposing not an income tax, but an excise tax upon the conduct of business in a corporate capacity, measuring, however, the amount of tax by the income of the corporation, with certain qualification prescribed by the act itself'

Stratton's Independence, LTD. V. Howbert, 231U.S.399, 414-415 (1913)

"'it is obvious that these decisions in principle rule the case at bar if the word 'income' has the same meaning in the Income Tax Act of 1913 that it has in the Corporation Excise Tax Act of 1909, and that it has the same scope of meaning was in effect decided in Southern Pacific v. Lowe ... , where it was assumed for the purpose of decision that there was no difference in its meaning as used in the act of 1909 and in the Income Tax Act of 1913. There can be no doubt that the word must be given the same meaning and content in the Income Tax Acts of 1916 and 1917 that it had in the act of 1913. When we add to this, Eisner v. Macomber ... the definition of "income· which was applied was adopted from Strattons' Independence v. Howbert. supra. arising under the Corporation Excise Tax Act of 1909 ... there would seem to be no room to doubt that the word must be given the same meaning in all the Income Tax Acts of Congress that was given to it in the Corporation Excise Tax Act, and that what that meaning is has now become definitely settled by decisions of this Court."

Merchant's Loan & Trust Co. v. Smietanka, 255 U.S. 509, 519 (1921)

THIS COURT'S DUTY AND OBLIGATIONS ARE MADE CLEAR

27. Without question, this case is a nullity ab initio where subject matter and in personam

jurisdiction is lacking. Keep in mind, I do not contend district courts of the United States do not

have jurisdiction over matters presented with regard to IRC statutes~ but do contend., and have

proved by authoritative evidence, that IRC statutes are based upon special legislation that has no

lawful force or effect upon me or my estate (real or personal). It is self-evident that a claim as to

the court having general subject matter jurisdiction over 26 U.S.C. statutory violations is

irrelevant. immaterial, and frivolous where I and my property are not subject thereto. Ergo., the

Fasulo v. United States, and McNa/ly v U.S., supra. ruling: "There are no constructive

offenses; and before one can be punished, it must be shown that his case is plainly within

the statute."

28. The lack of jurisdiction over me as to the subject matter must be recognized as negating

both in personam and subject matter jurisdiction in this case; without which the alleged

Case No: 5:13-cr-00026-PRL-l Page 18 of32 Harter's JURISDICTIONAL CHALLENGE; REJECTION TO ALLEGED CONVICTION:

OFFICIAL MISCONDUCT CHARGE: and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 19 of 65 PageID 979

conviction and any court ordered imprisonment cannot stand as valid 21 and would evidence use

of a non-existent discretion designed to bolster the government's case and avoid matters of

constitutional violations including, but not limited to, the Thirteenth Amendment.

29. Further, with IRC statutes being lawfully inapplicable to me and my estate (real and

personal). IRC statutes provide no remedy to me or the United States of America (whoever that

may be 22). With violation of my inalienable rights secured by the Constitution of the United

States of America being at issue, remedy is reserved to Article III Courts . Wherefore, this Court

must sit as an Article III Court in this matter, and not as an administration tribunal serving the

DOJ. the DOT, and the IRS in this wrongful administration of IRC statutes (as seems to have

occurred thus far). As put by the U.S. Supreme Court in its Northern Pipeline Const. Co. v.

Marathon Pipe Line Co.~ 458 U.S. 50, 83-84 (1983) ruling:

"Although Crowell and Raddatz do not explicitly distinguish between rights created by Congress and other rights, such a distinction underlies in part Crowell's and Raddatz' recognition of a critical difference between rights created by federal statute and rights recognized by the Constitution. Moreover, such a distinction seems to us to be necessary in light of the delicate

21 "The validity of an order of a federal court depends upon that court's having jurisdiction over both the subject matter and the parties. Stoll v. Gottlieb, 305 U.S. 165, 171-172 (1938); Thompson v. Whitman, 18 Wall. 457, 465 ( 1984). The concepts of subject-matter and personal jurisdiction. however. serve different purposes, and these different purposes affect the legal character of the two requirements.'" Insurance Corp. V. Compagnie Des Bauxites, 456 U.S. 694, 701 (1982)

22 United States of America. A federal republic formed after the War oflndependence and made up of 48 conterminous states .. plus the state of Alaska and the District of Columbia in North America, plus the state of Hawaii in the Pacific. Black's Law Dictionary, Seventh Edition ( 1999) [not in 6'h or prior Black's editions]

Republic. A commonwealth, that form of government in which the administration of affairs is open to all the citizens. In another sense, it signifies the state, independently of its form of government. Black's Law Dictionary, Fifth Edition ( 1959) [Comment: from these definitions. it would appear the United States of America could be all the people on this great land, or it could be the 50 States united in America, or maybe just the "citizens" (people) who make up the U.S. Government. Either way, it seems to me the United States of America is a fictitious plaintiff.]

Fictitious plaintiff. A person appearing in the writ, complaint, or record as the plaintiff in a suit. but who in reality does not exist, or who is ignorant of the suit and of the use of his name in it. It is a contempt of court to sue in the name of a fictitious party. Black's Law Dictionary. Fourth Edition ( J 968)

Case No: 5:13-cr-00026-PRL-1 Page 19of32 Harter's JURISDICTIONAL CHALLENGE: REJECTION TO ALLEGED CONVICTION:

OFFICIAL MISCONDUCT CHARGE: and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 20 of 65 PageID 980•

accommodations required by the principle of separation of powers reflected in Art. Ill. The constitutional system of checks and balances is designed to guard against "encroachment or aggrandizement" by Congress at the expense of the other branches of government. Buckley v. Valeo, 424 U.S .. al 122 . But when Congress creates a statutory right, it clearly has the discretion, in defining that right, to create presumptions, or assign burdens of proof, or orescribe remedies; it may also provide that persons seeking to vindicate that right must do so before particularized tribunals created to perform the specialized adjudicative tasks related to that right. 35 Such provisions do, in a sense, affect the exercise of judicial power, but they are also incidental to Congress' power to define the right that it has created. No f .:t.58 l r.s. 50. 84] comparable justification exists, ~owever, when the right being adjudicated is not of congressional creation. In such a situation, substantial inroads into functions that have traditionally been performed by the Judiciary cannot be characterized merely as incidental extensions of Congress' power to define rights that it has created. Rather, such inroads suggest unwarranted encroachments upon the judicial power of the United States, which our Constitution reserves for Art. Ill courts."

30. The U.S. Supreme stated: "'No higher duty rests upon this court than to exert its full

authority to prevent all violation of the principles of the Constitution." Downes v. Bidwell,

182 U.S. 244, 383 (1901). The same duty falls upon all of the U.S. Government's lower courts;

who also have: "the responsibility of determining the limits of statutory grants of authority

in such instances is a judicial function entrusted to the courts by Congress by the statutes

establishing [Article I, administrative] courts and marking their jurisdiction •.•. But under

Article III, Congress established courts to adjudicate cases and controversies as to claims of

infringement of individual rights whether by unlawful action of private persons or by the

exertion of unauthorized administrative power." Stark v .. Wickard, 321 U.S. 288~ 309-310

(1944).

31. The foregoing having been said, I declare Magistrate Judge Philip R. Lammens'

avoidance to such duties, or any ruling as to sentencing me to prison without a comprehensive

rebuttal to all issues in this affidavit and Exhibits A and B being placed on record in this case~

places the Court and its officers in disrepute and under suspicion of being influenced to

Case No: 5: l 3-cr-00026-PRL-1 Page 20 of 32 Harter's JURISDICTIONAL CHALLENGE~ REJECTION TO ALLEGED CONVICTION;

OFFICIAL MISCONDUCT CHARGE; and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 21 of 65 PageID 981

effectuate rulings favorable to the U.S. Government 23; which not only sullies the integrity of the

U.S. Government and the Court but violates the Judiciary's duty to be independent of the U.S.

Government's Executive Department, 24 the Code of Conduct for U.S. judges 25, their oath of

office, and court Canons.26 "Fraud on the court occurs when the misconduct harms the integrity

23 The Revenue Act of 1918, c. 18. 40 Stat. 1057, Sec. 213 made the pay of U.S.judges includible in ·'gross income'' subject to the "federal income tax return" program. U.S. Court judges successfully fought against this on the basis of the constitutional requirement that their compensation for services not be diminished while in office. It is questionable why they gave up that premise and conceded to be subject thereto by Revenue Act of 1932, c. 209, Sec. 22,, which reads in pertinent part: hln the case of Presidents of the United States and judges of courts of the United States taking office after June 6, 1932, the compensation received as such shall be included in gross income; and all Acts fixing the compensation of such Presidents and judges are hereby amended accordingly." With an understanding of the "'federal income tax return" program, it seems to me the compensation of judges in the same classification (e.g .• supreme court, appellate court, district courts, administrative courts. etc, and various levels within such classifications; e.g., full time, part time, chief judge, etc.) is made variable by their personal family conditions and thus constitutes a denial of equal pay protections. This notwithstanding, it cannot be denied that independence of judges is tainted by being subject to DOT/IRS administrative authority and possible harassment where their rulings are adverse to the revenue enhancement made possible by misrepresentation of this program being applicable to human beings and property not subject to the IRC statutes.

:?.t '"The Judiciary is one of the three great departments of the government. created and established by the Constitution. Its duties and powers are specifically set forth, and are of a character that requires it to be perfectly independent of the two other departments, and in order to place it beyond the reach and above even the suspicion of any such influence, the power to reduce their compensation is expressly withheld from Congress, and excepted from their power of legislation." 0 'Malley v. Woodrough, 307 U.S. 277, 288 ( 1938)

25 Code of Conduct for U.S. Judges reads in part:

Canon I. A Judge Should Uphold the Integrity and Independence of the Judiciary

Canon 2. A Judge Should Avoid Impropriety and the Appearance oflmpropriety in All Activities

Canon 3. A Judge Should Perform the Duties of the Office Impartially and Diligently

16 Court Canon. 8) A judge shall dispose of all judicial matters fairly, promptly, and efficiently. A judge shall manage the courtroom in a manner that provides all litigants the opportunity to have their matters fairly adjudicated in accordance with the law. ADVISORY COMMITTEE COMMENTARY: The obligation of a judge to dispose of matters promptly and efficiently must not take precedence over the judge's obligation to dispose of the matters fairly and with patience. For example, when a litigant is selfrepresented, ajudge has the discretion to take reasonable steps, appropriate under the circumstances and consistent with the law and the canons, to enable the litigant to be heard. A judge should monitor and supervise cases so as to reduce or eliminate dilatory practices, avoidable delays. and

Case No: 5: 13-cr-00026-PRL-I Page 2 I of 32 Harter's JURISDICTIONAL CHALLENGE: REJECTION TO ALLEGED CONVICTION:

OFFlClAL MISCONDUCT CHARGE: and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 22 of 65 PageID 982

of the judicial process, regardless of whether the opposing party is prejudiced." Alexander vs.

Robertson~ 882 F2d 421, 424, (91h Cir. 1989).

32. This Court is also noticed that any order adverse to me without absolute proof on record

that IRC statutes are lawfully applicable to me and my proprietary property is not merely

erroneous, but VOID.27

33. I also respectfully remind this Court that "It is the duty of courts to be watchful for the

constitutional rights of the citizen, and against any stealthy encroachments thereon." Mongahela

Nav. Co. v. U.S., 148 U.S. 312. 325 (1893). and a public officer is bound by oath to faithfully

perform and discharge the duties of his office. Courts of justice are established for such purpose.

28 To do less would appear to be a connivance 29 designed to permit DOT/IRS officials to

unnecessary costs. A judge should encourage and seek to facilitate settlement. but parties should not feel coerced into surrendering the right to have their controversy resolved by the courts.

27 ·'While we agree with the Department's argument that a determination by an administrative board becomes as final as a judgment, we also note that the judgment of a court which has exceeded its jurisdiction is void and can be collaterally attacked at any time. Davidson Chevrolet v. City and County of Denver. 138 Colo. 171, 330 P.2d 1116. It follows that a collateral attack may be made here for "acts or orders [of administrative officers or agencies] which do not come clearly within the oowers granted or which fall beyond the purview of the statute granting the agency or body its powers [such orders] are not merely erroneous, but are void."*** "They [officers or agencies] are without power to act contrary to the provisions of the law or the clear legislative intendment, or to exceed the authority conferred on them by statute." 73 C.J.S. Public Administrative Bodies and Procedure§ 59, pp. 383-384. And see, Liebhardt v. Tasher, 132 Colo. 554, 290 P.2d 1107." Flavell v. Department o/Welfare,CityandCozmtyo/Denver, 355 P.2d 941, 943 (1960)

::?s '" ••• No officer of the law may set that law at defiance with impunity. All the officers of the government, from the highest to the lowest, are creatures of the law and are bound to obey it. It is the only supreme power in our system of government, and every man who by accepting office participates in its functions is only the more strongly bound to submit to that supremacy, and to observe the limitations which it imposes upon the exercise of the authority which it gives.

"Courts of justice are established, not only to decide upon the controverted rights of the citizens as against each other, but also upon rights in controversy between them and the government, and the docket of this court is crowded with controversies of the latter class. Shall it be said, in the face of all this, and of the acknowledged right of the judiciary to decide in proper cases, statutes which have been passed by both branches of congress and approved by the president to be unconstitutional. that the [ I 06 U.S. 196. 2'.21] courts cannot give remedy when the citizen has been deprived of his property by force, his estate seized and converted to the use of the government without any lawful authority,

Case No: 5: 13-cr-00026-PRL- l Page 22 of 32 Harter's JURISDICTIONAL CHALLENGE: REJECTION TO ALLEGED CONVICTION:

OFFICIAL MISCONDUCT CHARGE: and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 23 of 65 PageID 983

perpetuate the wrongful administration of IRC statutes by a scheme or artifice 30 based upon

custom, not law; and evidence a breach of duty 31 placed upon public officials by the

Constitution whereby the people created governments.

STATEMENT OF PERSONAL FACTS

34. With the exception of being in the Navy reserves from 1990 -1994, I. Thomas William

Harter, have never been employed within any agency or instrumentality of the U.S. Government.

35. It is fact that in the past I unwittingly filed IRS 1040 forms based upon my income.

declaring thereon "Amount You Owe.'' The sums so declared on those implied quasi-contracts

were entered on the constructive DOT/IRS account THOMAS W. HARTER. Such entries are

false where IRC subtitle A statutes are lawfully inapplicable to contracts (labor or otherwise)

without any process of law, and without any compensation, because the president has ordered it and his officers are in possession? If such be the law of this country, it sanctions a tyranny which has no existence in the monarchies of Europe, nor in any other government which has a just claim to well-regulated liberty and the protection of personal rights.,, US v Lee, 106 U.S. 196, 220-221, I S.Ct. 240 ( 1882)

29 Connivance. [in part] The secret or indirect consent or permission of one person to the commission of an unlawful or criminal act by another. A winking at; voluntary blindness~ an intentional failure to discover or prevent the wrong; forbearance or passive consent. Pierce v. Crisp. 260 Ky. 519, 86 S. W .2d 293, 296. Black's Law Dictionary. Sixth Edition (1990)

30 Scheme or artifice to defraud. For purposes of fraudulent representation statutes, consists of forming plan or devising some trick to perpetrate fraud upon another. State v. Smith, 121 Ariz. I 06, 588 P.2d 848. Such connotes a plan or pattern of conduct which is intended to or is reasonably calculated to deceive persons of ordinary prudence or comprehension. U.S. v. Washita Const. Co .. C.A.Okl., 789 F.2d 809, 817. ""Scheme to defraud" within meaning of mail fraud statute (18 U.S.C.A. § 1341) is the intentional use of false or fraudulent representation for the purpose of gaining a valuable undue advantage or working some injury to something of value held by another. U.S. v. Mandel, D.C.Md., 415 F.Supp. 997, 1005. See also Artifice; Fraud; Mail fraud. Black's Law Dictionary. Sixth Edition (1990)

.lt Breach. The breaking or violating of a law, right, obligation, engagement, or duty, either by commission or omission. Exists where one party to contract fails to carry out term. promise~ or condition of the contract. Black's Law Dictionary, Fifth Edition (1979)

Case No: 5:13-cr-00026-PRL-1 Page 23 of32 Harter's JURISDICTIONAL CHALLENGE; REJECTION TO ALLEGED CONVICTION:

OFFICIAL MISCONDUCT CHARGE: and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 24 of 65 PageID 984

involving private commercial transactions. The entries on that account as to years 2006-2011

(the years on the bogus Information charge) are based upon writings fabricated by agents of the

DOT/IRS officials without any support (implied or otherwise) by documents bearing my

signature; thus are false writings on their face.

36. All entries in the IRS system of records regarding constructive account titled THOMAS

W. HARTER are based upon my private commercial transactions not subject to IRC statutes.

They are a product of concealment of the true nature of the "federal income tax" return program

being applicable to particular persons and things (i.e., special law). Thus they are materially

false and libelous per se. The filing of IRS false documents into public records, e.g., Notice of

Federal Tax Lien, not only impairs my unalienable right to contract (which is in effect a seizure

32) but is part of a scheme or artifice intended to deprive me of possession of my property-

which constitutes fraud. 33

37 By discontinuing the execution of Form(s) 1040, I performed an act of disaffirmance 34 to

any entries on constructive DOT/IRS account THOMAS W. HARTER resulting from Form(s)

32 " ••• The reason why a government official might ... effectuate a seizure is wholly irrelevant to the

threshold question of whether the [Fourth] Amendment applies. What matters is the intrusion on people's security from governmental intrusion on people's security from governmental interference ... The fourth [amendment] protects two types of expectations, one involving 'searches' and the other 'seizures'. A 'search' occurs when an expectation of privacy that society is prepared to consider reasonable is infringed. A 'seizure' occurs where there is some meaningful interference with an individual's possessory interests in that property." 466 U.S. at 113, 104 S.Ct., at 1656, 1660, Horton v. California, 496 U.S. 128, 133 S.Ct. 2301, 2306, 110 L.Ed2d 347 (1987); Maryland v. Macon, 472 U.S. 463, 469." Soldal et al. v. Cook County. Rlinois. et al., 113 S.Ct. 538, (1992) [from lawyer edition]

33 "Fraud destroys the validity of everything into which it enters," Nudd v. Burrows, 91 U .S 426; "Fraud vitiates the most solemn contracts, documents and even judgments," U.S. v. Throckmorton, 98 U.S. 61 (1878).

34 Disaffirmance. The repudiation of a former transaction. The refusal by one who has the legal power to refuse (as in the case of a voidable contract), to abide by his former acts, or accept the legal

Case No: 5: 13-cr-00026-PRL-1 Page 24 of 32 Harter's JURISDICTIONAL CHALLENGE; REJECTION TO ALLEGED CONVICTION;

OFFICIAL MISCONDUCT CHARGE; and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 25 of 65 PageID 985

1040 made and filed by me due to misrepresentation that it was an act required by law. My

many rejections to subsequent DOT/IRS writings making claim to my property under a

presumption of IRC statutory authority, or official right, is an act of repudiation of all

transactions recorded in the constructive DOT/IRS account THOMAS W. HARTER based upon

false writings manufactured by DOT /IRS agents.

38. Being unfamiliar with court process and procedure, I hired an attorney, Mark Schleben,

believing it to be in my best interest. I shared with him the writings presented to DOT /IRS

officials over the years. While he seemed receptive, I don't believe he truly understood the

matter or was entirely in accord thereto. By the time I realized this it was too late to prevent the

so called trial; the result of which speaks for itself. In order to take back my right to bring truth

and justice to the matter, I discharge him. His notice of discharge was filed October 3, 2013

(Doc. #86).

39. Prior there to, on 09/30/2013) (Doc. #85), Mr. Schleben filed "Defendant's Renewed

Motion for Judgment of Acquittal, Motion to Arrest Judgment, Motion for New Trial, and

Renewed Motion for Kastigar or Jackson-Denno Hearing with Supporting Memorandum of

Law." I understand this was filed on that date because of time constraints in rules. Grounds

used by him are basically: (a) pursuant to two Federal Criminal Procedure rules, "the prosecution

has failed to establish a prima facie case by failing to adduce competent substantial evidence as

to willfulness"; and (b) pursuant to Rules and U.S. Supreme Court and 11th Circuit rulings, he

asks for arrest of judgment or for a new trial ''on the grounds that this Court has failed to: (1)

conduct any kind of Kastigar or Jackson-Denno hearing; (2) suppress all evidence derived from

consequences of them. It may either be "express" (in words) or "implied" from acts inconsistent with a recognition of validity of former transaction. Black's Law Dictionary, Fifth Edition (1979)

Case No: 5:13-cr-00026-PRL-1 Page 25 of32 Harter's JURISDICTIONAL CHALLENGE; REJECTION TO ALLEGED CONVICTION;

OFFICIAL MISCONDUCT CHARGE; and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 26 of 65 PageID 986

the Defendant's compelled and immunized testimonial communications made pursuant to

Section 687.071(6), Florida Statutes (2011); and (3) instruct the jury on the Defendant's good

faith assertion of the Fifth Amendment as justification for not filing tax returns." He goes on to

support this with what appears to be authoritative evidence (not researched by me, as yet). The

problem as I see it is that the filing of these motions is tantamount to my admission that I and my

property are subject to IRC statutes and that I accept being the ''Defendant" in this case when I

believe Defendant THOMAS W. HARTER is the constructive IRS account, not me. To avoid

such false impression while preserving the option to reinstate the Motion for a new trial based

upon the procedural errors enumerated in the Motions in the event officers of this Court place on

record a complete and comprehensive rebuttal to each item in this Jurisdictional Challenge, I am

filing a TEMPORARY I CONDITIONAL WITHDRAWAL OF MOTIONS IN DOCKET #85.

OFFICIAL MISCONDUCT CHARGE

Misconduct in office. Any unlawful behavior by a public officer in relation to the duties of his office, willful in character. Term embraces acts which the office holder had no right to perform, acts performed improperly, and failure to act in the face of an affirmative duty to act. See also Malfeasance; Misfeasance. Black's Law Dictionary, Fifth Edition (1979)

40. I, Thomas William Harter charge official misconduct begins with DOT and IRS officials with

permitting, and perhaps instructing, their agents to operate outside the scope of authority provided by law

to their office. It becomes prosecutorial misconduct when the U.S. Attorney prosecutes IRC civil or

criminal case against a human being, like me, whose person and property are not within IRC statutes.

"The United States Attorney is the representative not of an ordinarv partv to a controversy, but of a sovereignty whose obligation to govern impartially is as compelling as its obligation to govern at all; and whose interest, therefore, in a criminal prosecution is not that it shall win a case, but that justice shall be done. As such, he is in a peculiar and very definite sense the servant of the law, the twofold aim of which is that guilt shall not escape or innocence suffer. He may prosecute with earnestness and vigor-indeed, he should do so. But, while he may strike hard blows, he is not at liberty to strike foul ones. It is as much his duty to refrain from improper methods calculated to produce a wrongful conviction as it is to use everv legitimate means to bring about a just one."

Berger v. U.S., 295 U.S. 78, 88 (1935

Case No: 5:13-cr-00026-PRL-l Page 26 of32 Harter's JURISDICTIONAL CHALLENGE; REJECTION TO ALLEGED CONVICTION;

OFFICIAL MISCONDUCT CHARGE; and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 27 of 65 PageID 987

" ... No officer of the law may set that law at defiance with impunity. All the officers of the government, from the highest to the lowest, are creatures of the law and are bound to obey it. It is the only supreme power in our system of government, and every man who by accepting office participates in its functions is only the more strongly bound to submit to that supremacy, and to observe the limitations which it imposes upon the exercise of the authority which it gives.

US v Lee, 106 U.S. 196, 220-221, 1 S.Ct. 240 (1882)

41. As individuals who routinely prosecute violation of IRC statutes, the U.S. Attorneys have

no excuse for not knowing the precise lawful extent to the enforcement of IRC statutes and

strictly adhere thereto. Wherefore, prosecution of human beings not subject thereto evidences

deliberate, arbitrary, operation outside the scope of their office and an intentional abuse of court

power, process, and procedures-a matter judges are under a duty to prevent.

42. Higher government officials are required to take an oath to uphold the Constitution and

defend the people from enemies, foreign and domestic. It seems they become the enemy when

they aid and abet officials of the DOT /IRS in misapplication of IRC statutory authority with

result to inflict wrongful imprisonment and/or taking of property; and such conduct certainly

falls into the classification of imposing involuntary servitude upon those they wrongfully

prosecute.

"The words involuntary servitude have a 'larger meaning than slavery.' ... The plain intention was to abolish slavery of whatever name and form and all its badges and incidents; to render impossible any state of bondage; to make labor free, by prohibiting that control by which the personal service of one man is disposed of or coerced for another's benefit which is the essence of involuntary servitude."

Bailey v. Alabama, 219 U.S. 219, 241 (1910)

43. I, Thomas William Harter, hereby charge government individuals directly or indirectly

involved in initiating this case with knowingly acting outside the scope of authority provided by

law with purpose to have me unduly imprisoned (a direct violation of the 13th Amendment) and

eventually accomplish a fraudulent taking of my property through the use of false documents and

Case No: 5: 13-cr-00026-PRL-1 Page 27 of 32 Harter's JURISDICTIONAL CHALLENGE; REJECTION TO ALLEGED CONVICTION;

OFFICIAL MISCONDUCT CHARGE; and DEMAND IN THE NAME OF JUSTICE

Case 5:13-cr-00026-PRL Document 89 Filed 10/10/13 Page 28 of 65 PageID 988

representation. In so doing, under color of law or color of official right, they commit a crime of

violence 35 that violates 18 U.S.C. § 242 36 and other statutes in U.S. Code titles 18, 42 and 26.

44. False representation 37 is on record when only facts drawn from the IRS system of

records and witnesses brought in to testify with regard to my personal commercial transactions

was used to convince twelve (12) people sitting in the jury box that I am guilty of violating IRC

§ 7203 (an impossibility as seen by the evidence in this affidavit and Exhibits A and B). It is

impossible to get an unbiased and just verdict from jurors when they are not informed of the true

nature of the "federal income tax" return program and they are selected after presuming they are