welspun india limited (wil)• a part of us$ 3 billion welspun group, welspun india ltd. is among...

TRANSCRIPT

Welspun India Limited (WIL) Investor Presentation

……………………………………………..……………………………………………………………………….……..

……………………………………………………………………….……..

May 2015

Agenda

Financial Highlights

Industry Overview:

Advantage India

Welspun India: Global

Leader in Home Textiles WIL – An Overview

Way forward

2

Commitment & Empowerment Global Home Textiles Leader

• A part of US$ 3 billion Welspun Group, Welspun

India Ltd. is among the top three home textile

manufacturers in the world and the largest home

textile company in Asia

• Leading Home Textile exporter to the US for the third

consecutive year

• With a distribution network in more than 50

countries, it is the largest exporter of home fashion

products

• Centered on excellence and transparency, the

company has emerged as a trusted partner to 14 of

Top 30 global retailers like Wal-Mart, JC Penney,

Target and Macy’s among others

• State-of-the-art manufacturing facilities at Anjar and

Vapi (Gujarat)

Creates opportunities for financial inclusion for women in the

geographies they operate in – through initiatives like Spun,

Rags to Rugs and Swasti

Innovation Focus

• Patents (Granted /Pending) : 12

• About 31% of sales comes from innovative products

WIL – An overview

3

5,960 6,438

10,253

13,691

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

FY12 FY13 FY14 FY15

EBITDA in INR Million

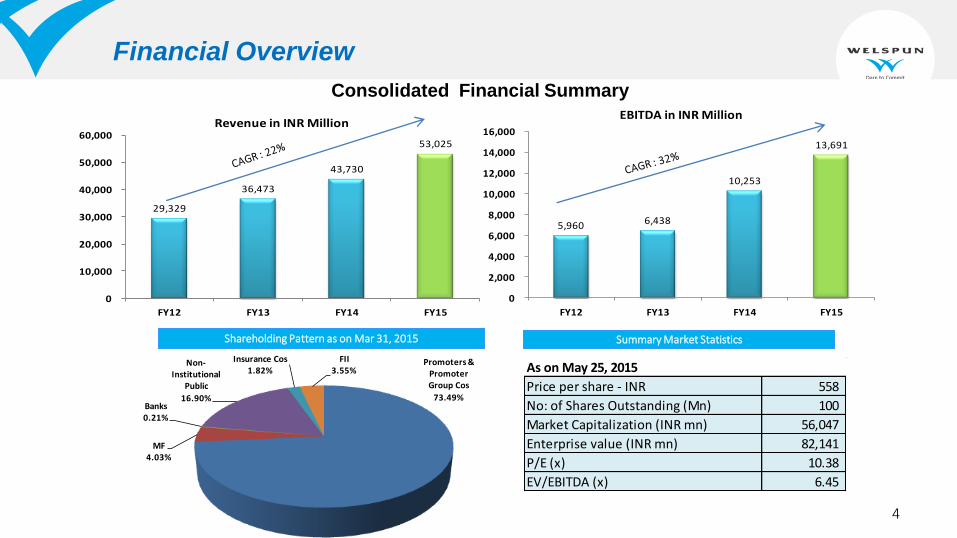

Financial Overview

Shareholding Pattern as on Mar 31, 2015 Summary Market Statistics

Consolidated Financial Summary

As on May 25, 2015

Price per share - INR 558

No: of Shares Outstanding (Mn) 100

Market Capitalization (INR mn) 56,047

Enterprise value (INR mn) 82,141

P/E (x) 10.38

EV/EBITDA (x) 6.45

29,329

36,473

43,730

53,025

0

10,000

20,000

30,000

40,000

50,000

60,000

FY12 FY13 FY14 FY15

Revenue in INR Million

Promoters & Promoter Group Cos

73.49%

MF4.03%

Banks0.21%

Non-Institutional

Public

16.90%

Insurance Cos 1.82%

FII3.55%

4

7 12

16 17

26 28 32

36

44

53

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

WIL – Revenue Milestones

WIL Revenue in Rs. Billion

Textiles business has been growing at a CAGR of 26.2 % since the inception of the Anjar Facility

Sustained growth indicates the potential of Home Textile market in the world

International operations majorly contribute to the revenue

Anjar facility is the largest home textiles facility in Asia

• 1993: Towels facility at Vapi

• 2000: JV for bath robes

Pre-2005

Towels &

Sheets Facility at Anjar

Entry into bath rugs

Entry into Accent Rugs/ Carpets

5

Industry Overview: Advantage India

6

Global Home Textile Scenario

Market Size

Home textile market at US$45 bn

Bath towel and Bed linen constitute ~60%

Key Consumers

US , Europe and Japan are the largest consumers

Global demand almost equally split between US, Europe and Rest of the World

Key Producers

India , Pakistan and China are the largest producers

Account for 85% of cotton home textile trade to US

Global market share: China 35%; India 11%

India’s market share is higher in cotton home textiles

7

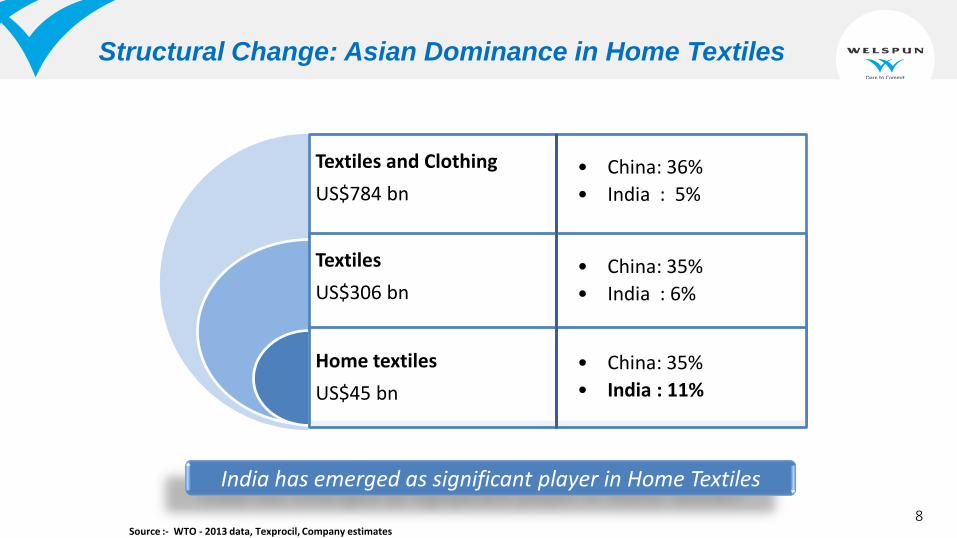

Structural Change: Asian Dominance in Home Textiles

Textiles and Clothing

US$784 bn

Textiles

US$306 bn

Home textiles

US$45 bn

• China: 36%

• India : 5%

• China: 35%

• India : 6%

• China: 35%

• India : 11%

Source :- WTO - 2013 data, Texprocil, Company estimates

India has emerged as significant player in Home Textiles

8

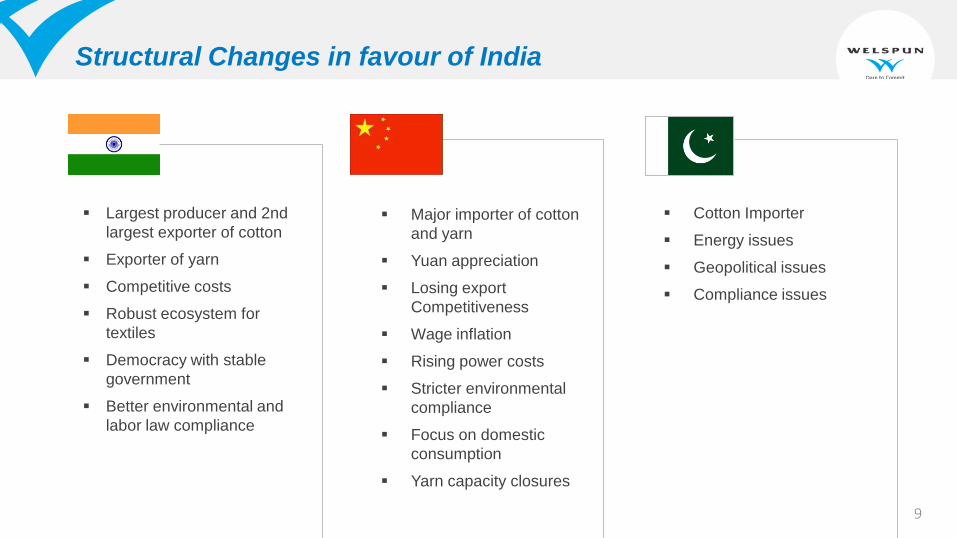

Structural Changes in favour of India

Largest producer and 2nd

largest exporter of cotton

Exporter of yarn

Competitive costs

Robust ecosystem for

textiles

Democracy with stable

government

Better environmental and

labor law compliance

Major importer of cotton

and yarn

Yuan appreciation

Losing export

Competitiveness

Wage inflation

Rising power costs

Stricter environmental

compliance

Focus on domestic

consumption

Yarn capacity closures

Cotton Importer

Energy issues

Geopolitical issues

Compliance issues

9

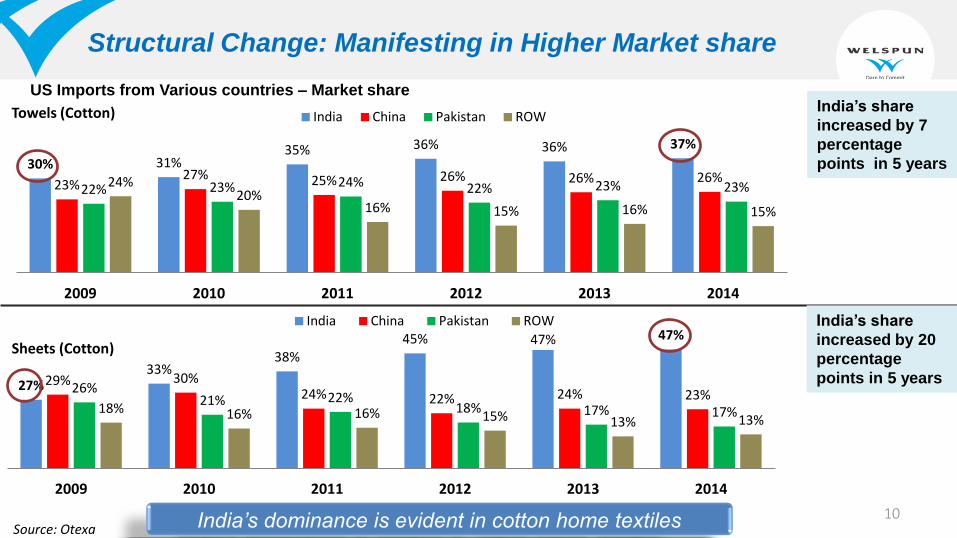

27% 33%

38% 45% 47% 47%

29% 30% 24% 22% 24% 23% 26%

21% 22% 18% 17% 17% 18% 16% 16% 15% 13% 13%

2009 2010 2011 2012 2013 2014

Sheets (Cotton)

India China Pakistan ROW

30% 31% 35% 36% 36% 37%

23% 27% 25% 26% 26% 26%

22% 23% 24% 22% 23% 23% 24% 20%

16% 15% 16% 15%

2009 2010 2011 2012 2013 2014

Towels (Cotton) India China Pakistan ROW

US Imports from Various countries – Market share

Structural Change: Manifesting in Higher Market share

Source: Otexa

India’s share

increased by 7

percentage

points in 5 years

India’s share

increased by 20

percentage

points in 5 years

India’s dominance is evident in cotton home textiles 10

Structural Change: Advantage India

Market Size

US market

European market

Other markets

Home textile market at US$45 bn

Bed towel and Bed Lenin constitute ~60%

Constitutes about one-third of the global market

India best placed among competing countries

Potential to increase penetration in key categories (TOB, carpets, basic bedding etc.)

Constitutes about one-third of the global market

India competitive in spite of duty disadvantage

Proposed India - EU FTA to reduce duties by 5% - 10%

Potential to increase presence in markets like Japan, Korea, Australia

FTA with Japan, Korea to boost trade

Indian domestic market is a huge potential opportunity

Growth opportunities across markets 11

Welspun India

12

Key Developments in FY 15

Home Textile exporter to the US for the third

consecutive year

Commissioned India’s ‘largest spinning facility

under one roof’ at Anjar

Launched a major campaign for ‘Spaces’ in India

Launched Brand ‘Spun” globally Launched ‘Hygro’ branding campaign in the US

Global Ecommerce – Tie-up with major portals in

US, UK and India Gained traction in hospitality business globally

Increased vertical integration for yarn and fabric

to ~70%

Launched ‘Christy’ stores in China

Innovative products accounted for 31% of the

revenue

Gained foothold in LatAm, Central America and

Ireland

13

Global Client Recognitions in 2014-15

Green Manufacturing Excellence Award Green Believers Award 2014

by Frost & Sullivan

Macy’s Global Citizen Award for CSR for 2014.

Golden Peacock : Environment Management Award 2014

World CSR Congress - Global CSR Excellence & Leadership

Best Corporate Social Responsibility Practices 2013

Target Partner Award of Excellence

for performance in 2014

Macy’s 5 Star Vendor Award for

performance in 2014

Sheridan – Best Supplier Award for

performance in 2014

ASDA Self Testing Certification,

April 2015

Kohl’s Self Testing Certification

JCPenney –Innovation Award for

year 2013

Texprocil : Highest Global

Exports – Special Gold 2013-14

ECGC D&B - Best Trader

Exporter, Indian Exporter

Award’14

ASDA George Home

Best Product Quality award for

Egyptian Nanospun Towel

14

A differentiated End-to-end Solutions Provider in Home Textiles

Widest product range in the Home Textiles segment

Uniquely positioned for cross-selling due to Customer reach, Competitive manufacturing and Global delivery model empowering higher wallet share

Strong track record of customer satisfaction and repeat business from them; 80% revenue from replenishment

Bath Bedding Flooring

Towels Sheets Carpets

Bath robes TOB Rugs

Basic and Fashion Bedding

Wide product range in Home textiles

Leadership: Focus and Excellence

15

Leadership: Trusted Partner to Global Retail Giants

• Wal Mart • Bed Bath & Beyond • Macy’s • J C Penney • Target • Kohl’s • K Mart- Sears ….. and many more

• Ikea • Carrefour • JYSK • El Corte Ingles • Vincenzo Zucchi S.p.A … and many more

• ASDA • Tesco • Marks & Spencer • Debenhams • House of Frazer • Christy ….. and many more

• Spaces- Home & Beyond • Welhome

Partner to Marquee clients across geographies 16

Leadership: Global Reach & Delivery Model

Delivery & Reach in over 50 countries 17

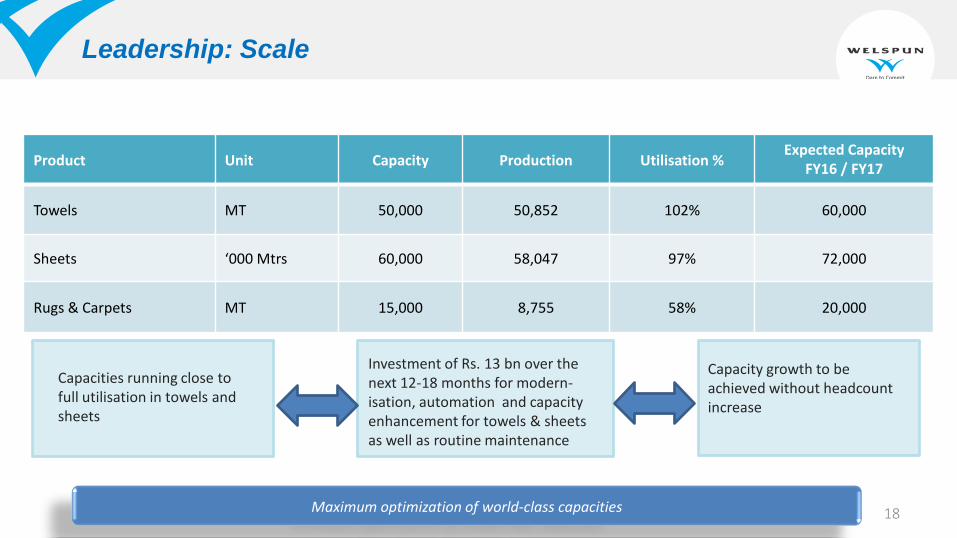

Leadership: Scale

Maximum optimization of world-class capacities

Product Unit Capacity Production Utilisation % Expected Capacity

FY16 / FY17

Towels MT 50,000 50,852 102% 60,000

Sheets ‘000 Mtrs 60,000 58,047 97% 72,000

Rugs & Carpets MT 15,000 8,755 58% 20,000

Capacities running close to full utilisation in towels and sheets

Investment of Rs. 13 bn over the next 12-18 months for modern-isation, automation and capacity enhancement for towels & sheets as well as routine maintenance

Capacity growth to be achieved without headcount increase

18

Leadership: FMCG Approach – Consumer-Driven Innovation

End Consumer

Product Promotion & Communicat

ion

Consumer Research & Developme

nt

Partnership with

Retailers

Integrated Manufactur

ing

Distribution

Unmatched Interactive experience

Superlative Products

Valuable partnerships

Quality, cost control

Robust SCM

19

Today’s Welspun: “FAST”

Fast Affordable Tech-

oriented Sustainable

Quick

response

time

(Speed to

Market)

Best cost

structures for

different price

levels

Technology

leveraged

across

Products,

Processes

and Supply

Chain

Caring for the

environment

and the

community

20

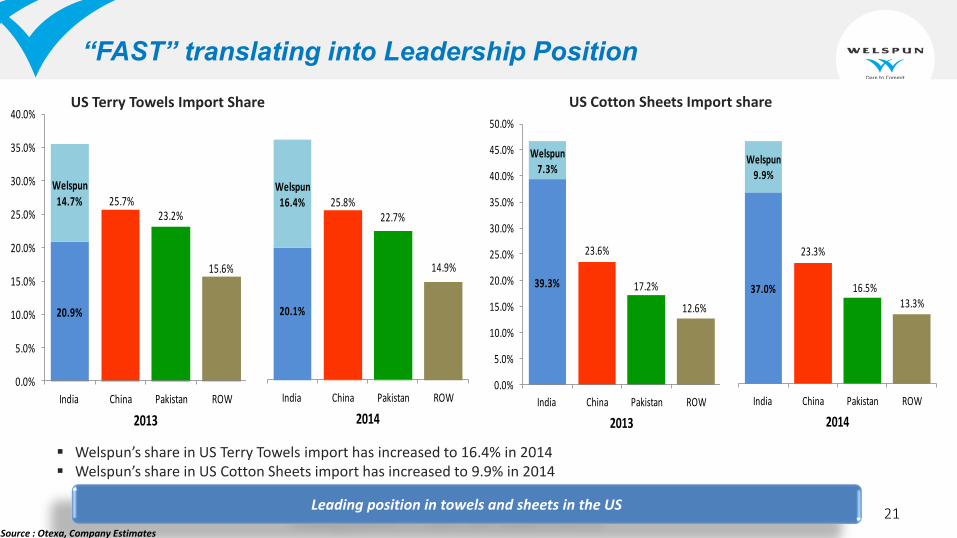

20.9%

25.7%23.2%

15.6%

Welspun 14.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

India China Pakistan ROW

2013

20.1%

25.8%22.7%

14.9%

Welspun 16.4%

India China Pakistan ROW

2014

39.3%

23.6%

17.2%

12.6%

Welspun 7.3%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

India China Pakistan ROW

2013

37.0%

23.3%

16.5%13.3%

Welspun 9.9%

India China Pakistan ROW

2014

“FAST” translating into Leadership Position

Source : Otexa, Company Estimates

Welspun’s share in US Terry Towels import has increased to 16.4% in 2014 Welspun’s share in US Cotton Sheets import has increased to 9.9% in 2014

US Terry Towels Import Share US Cotton Sheets Import share

Leading position in towels and sheets in the US 21

Value through Brands

Mass premium brand with presence in India and Middle East

Footprint of over 200 shop-in-shop outlets and distribution

BR

AN

DS

Mass brand presence via mass retailers; also growing via

distributor network

Largest terry towel brand in the UK with growing presence in China

and the Middle East

Present in over 40 retailers within UK

Also present in USA and seeing aggressive growth in e-commerce

Mass brand in the UK with a focus on bedding

Growing aggressively in affordable fashion

22

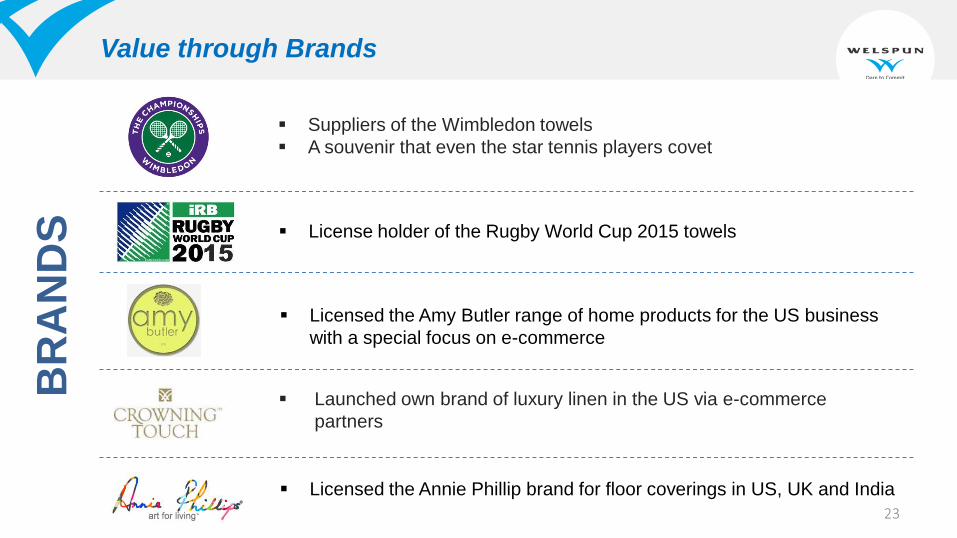

Value through Brands

Suppliers of the Wimbledon towels

A souvenir that even the star tennis players covet

BR

AN

DS

License holder of the Rugby World Cup 2015 towels

Licensed the Amy Butler range of home products for the US business

with a special focus on e-commerce

Launched own brand of luxury linen in the US via e-commerce

partners

Licensed the Annie Phillip brand for floor coverings in US, UK and India

23

Spaces Campaign

24

Branding our Innovation

• Launching nation-wide campaign in the US to introduce patented Hygrocotton®

technology to consumers

• First ever such campaign in textiles in the past 15 years

25

Value through Brands

Strong growth expected in the branded category, especially in India

Expansion of Christy into geographies such as USA, China and Middle East

Increased penetration of Spaces and Welhome through shop-in-shop and e-commerce

Very low capex and risk

India – Growth of branded products at ~40% CAGR over a period of 2 years

Global – Growth of branded products currently at ~11% of consolidated sales

Rising Share of Branded Products

8.0%

8.5%

9.0%

9.5%

10.0%

10.5%

11.0%

11.5%

FY13 FY14 FY15

Branded sales as % of Total

26 26

First model village, Versamedi, Anjar

SUSTAINABLE :

Corporate Social Value (CSV) - Vision

27

CSV – Through 3E’s

Empowerment

28

SPUN : Our Corporate Social Value initiative to Empower Women and Revive

the crafts of our country

CSV – Through 3E’s – Launched Campaign for “SPUN”

29

Welspun Group | Welspun Corp Ltd

PLANTATIONS: 565

fruit and vegetable

plantations done at 3

villages of Anjar

MOBILE HEALTH VANS at

Anjar & Mumbai: Provide

basic health facilities,

awareness sessions in the

underprivileged communities

20 Villages in Anjar, 9

communities in Mumbai

SANITATION PROJECT:

1160 toilets constructed in

8 villages of Anjar

HEALTH CAMPS: 10 camps

on blood group detection,

general health check up,

diabetes detection, dental

camps, etc. were conducted in

10 villages of Anjar

Environment

& Health

Education

ADULT LITERACY

PROGRAMME: 3

classes were

conducted consisting

of a total of 75

women at Versamedi

and Ajapar villages

since August 2014

QUALITY EDUCATION

PROGRAMME WITH 20

GOVT SCHOOLS IN

ANJAR : We recruited 26

Para –teachers. 51%

average increase in scores

of students

RO DRINKING WATER

initiative at Vapi (2

nos) and Anjar (3 nos)

CSV – Through 3E’s

30

Financial Highlights

31

Key financial highlights of FY15

Achieved highest annual

sales and profitability in

the Company’s history

Long Term Credit Rating

improved two notches to

AA- by FITCH

Net Debt to Equity

at 1.8x vs. 2.4x

Net debt to Operational

EBITDA at 2.0x vs. 2.9x

Positive free cash flows

after meeting capex

requirements

Tighter working capital

control reduces cash

conversion cycle to 59 days

from 67 days

Crossed Rs. 50 bn

milestone for revenue

and Rs. 5 bn milestone

for PAT

Operating EBITDA

margin at 24.0%;

PAT margin at 10.2%

32

Income Statement – Strong improvement

(Rs. Million)

Consistent improvement in financial performance

Note: 1) Cash Profit = PBDT – Current Tax 2) FY14 PAT and EPS are adjusted for one-time additional depreciation net of tax i.e. Rs 3,274 million

Particulars FY13 FY14 FY15

Revenue 36,473 43,730 53,025

Revenue growth % 24% 20% 145%

Operating EBITDA 5,946 9,211 12,742

Operating EBITDA Margin 16.3% 21.1% 24.0%

EBITDA 6,438 10,253 13,691

EBITDA Margin 17.7% 23.4% 25.8%

Depreciation 1,449 1,903 3,329

Finance cost 1,977 2,352 2,829

PBT 3,013 5,997 7,533

PAT 2,248 4,195 5,398

PAT Margin 6.2% 9.6% 10.2%

EPS (Rs) 22.4 41.8 53.8

Cash Profit # 4,178 6,237 9,01733

Financial Highlights: Balance Sheet

Debt increase in FY14 mainly on account of backward integration capex

(Rs. Million except Ratios )

Average interest cost of long-term debt

at ~7%

** Net Current Assets does not include Cash & Cash Equivalents

Particulars FY13 FY14 FY15

Net Worth 9,902 11,097 14,318

Short Term Loans 9,166 11,349 10,034

Long Term Loans 11,079 18,944 20,817

Net Debt 17,446 26,635 26,094

Capital Employed 29,589 40,036 42,451

Net Fixed Assets (incl CWIP) 18,615 25,609 26,049

Net Current Assets** 8,221 9,991 13,155

Total assets 38,579 51,684 56,953

Net Long Term Debt 8,280 15,286 16,060

Solvency ratios FY13 FY14 FY15

Fixed assets/Long term debt 1.68 1.35 1.25

Gross debt/Equity 2.04 2.73 2.15

Net debt/Equity 1.76 2.40 1.82

Net debt/Op. EBITDA 2.93 2.89 2.05

EBIT/Interest 2.52 3.55 3.66

34

Financial Highlights: Improving Operating and Return Ratios

Strong improvement in ROE and ROCE over the years

Note : ROCE = EBIT / Average Capital Employed; ROE = Net Profit / Average Net worth

Total asset turnover = Sales/ (Fixed assets + Gross current assets)

* P&L figures annualised

Operational ratios FY13 FY14 FY15

Fixed Asset turnover 1.96 1.71 2.04

Total Asset turnover 0.95 0.85 0.93

Inventory days 82 84 76

Debtor days 28 34 31

Payable days 50 51 48

Cash conversion cycle 60 67 59

Return ratios FY13 FY14 FY15

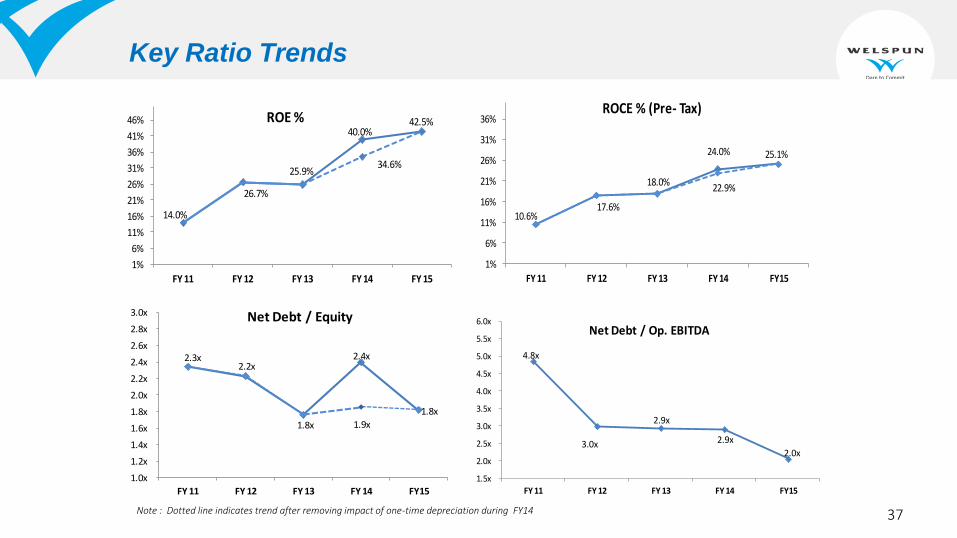

ROE 25.9% 40.0% 42.5%

ROCE (pre-tax) 18.0% 24.0% 25.1%

CROIC (Op EBITDA/NW) 60% 83% 89%

35

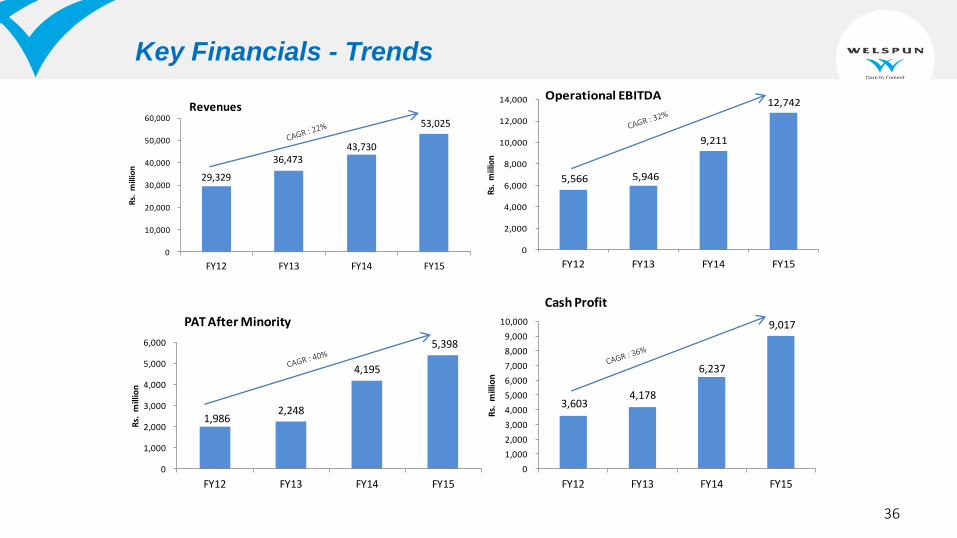

29,329

36,473 43,730

53,025

0

10,000

20,000

30,000

40,000

50,000

60,000

FY12 FY13 FY14 FY15

Rs.

mill

ion

Revenues

5,566 5,946

9,211

12,742

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

FY12 FY13 FY14 FY15

Rs.

miil

ion

Operational EBITDA

1,986 2,248

4,195

5,398

0

1,000

2,000

3,000

4,000

5,000

6,000

FY12 FY13 FY14 FY15

Rs.

mill

ion

PAT After Minority

3,603 4,178

6,237

9,017

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

FY12 FY13 FY14 FY15R

s. m

illio

n

Cash Profit

Key Financials - Trends

36

Key Ratio Trends

14.0%

26.7%

25.9%

40.0%42.5%

34.6%

1%

6%

11%

16%

21%

26%

31%

36%

41%

46%

FY 11 FY 12 FY 13 FY 14 FY 15

ROE %

10.6%17.6%

18.0%

24.0% 25.1%

22.9%

1%

6%

11%

16%

21%

26%

31%

36%

FY 11 FY 12 FY 13 FY 14 FY15

ROCE % (Pre- Tax)

2.3x 2.2x

1.8x

2.4x

1.8x

1.9x

1.0x

1.2x

1.4x

1.6x

1.8x

2.0x

2.2x

2.4x

2.6x

2.8x

3.0x

FY 11 FY 12 FY 13 FY 14 FY15

Net Debt / Equity

4.8x

3.0x

2.9x

2.9x

2.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

4.5x

5.0x

5.5x

6.0x

FY 11 FY 12 FY 13 FY 14 FY15

Net Debt / Op. EBITDA

Note : Dotted line indicates trend after removing impact of one-time depreciation during FY14 37

Dividend Policy – A Pioneering Initiative in the Industry

Dividend distribution policy announced along with FY15 results

Dividend Payout: 25% of PAT

FY15 Final Dividend at Rs. 7.5 per share. Total dividend for FY15 at Rs. 10.5 per share

FY15 Dividend Payout: ~25% of PAT

38

Way Forward

39

Way Forward : Sustaining growth momentum

New products

New channels

New markets

Leverage ‘FAST’

40

Thank You

For further details, please contact:

Altaf Jiwani

Director (Finance) - Welspun India Limited

Email: [email protected]

Akhil Jindal

Director – Group Finance and Strategy

Email: [email protected]

Company Website: www.welspunindia.com

Harish Venkateswaran

General Manager - Group Finance and Strategy

Email: [email protected]

41