what’s a rule 8…what’s a rule 9 take #2 check processing • volume considerations today...

TRANSCRIPT

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 1

Presented by:Sue Worley, NCPBank of America

Phyllis Meyerson, AAP, CCMECCHO

July 22, 2015

ECCHO Education Programs

What’s a Rule 8…What’s a Rule 9Take #2

Copyright© 2015 by the Electronic Check Clearing House Organization

Copyright© 2015 by the Electronic Check Clearing House Organization

NOTICEThis presentation provides information on various aspects of check payments and thelegal and rules framework for check image exchange. Responsibility for compliancewith image exchange rules, and/or the legal, operational and regulatoryrequirements applicable to check image exchange, remains at all times with thefinancial institution participating in check image exchange and/or the individual orcompany using a check image exchange service.

This presentation and the information contained herein is not intended as legal orcompliance advice or recommendation to any person or company. This documentcould include technical inaccuracies or typographical errors and individual users areresponsible for verifying any information found in this presentation and any relatedrecorded playback.

Financial institutions should consult with their legal counsel regarding legal andoperational requirements applicable to any check image exchange program they mayoffer or in which they participate.

These materials may not be reproduced or published, in whole or in part, without the express permission of ECCHO.

2

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 2

Copyright© 2015 by the Electronic Check Clearing House Organization

Agenda & Speakers• Background

– Price v Neal– Clearing House Rules

• Regulatory Environment• Rule 8 – Unauthorized Remotely Created Check

– Warranty– Claims Process– EPC digit for RCCs

• Rule 9 – Forged or Counterfeit Check– Warranty– Opt‐Out– Claims & Disclaimer Process– Risks & Benefits

• Q&A

• Today’s Speakers: – Sue Worley, NCP

• VP, Client Relationship Management – Bank of America– Phyllis Meyerson, AAP, CCM

• EVP – ECCHO

3

Background

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 3

Copyright© 2015 by the Electronic Check Clearing House Organization

• Why are these rules referred to as Rule 8 and Rule 9??– We’ll get to that in a minute

• What Section of the ECCHO Rules contain Rule 8 and Rule 9– Section XIX(N) and XIX(O) respectively

Rule 8 & Rule 9

5

Copyright© 2015 by the Electronic Check Clearing House Organization

• 1762 English Case

• Ruling by Lord Mansfield– “Nobody knows the hand of the drawer but the Plaintiff”

– “Negligence in the Plaintiff is greater than can possibly be imputed to the defendant”

– “Where the loss has fallen, there it must lie”– “One innocent man must not relieve himself by throwing it on another”

Price V Neal

6

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 4

Copyright© 2015 by the Electronic Check Clearing House Organization

Price V Neal• Outcome

– Person who can verify signature assumes loss on unauthorized checks

– Under UCC – paying bank, is holder of signature cards

– The forger was hanged

7

Copyright© 2015 by the Electronic Check Clearing House Organization

• Depositor – Strong Incentives to take check– Merchant in best position to verify identification

• UCC creates risk‐free transaction if forged signature– Risk is transferred to paying bank

• Depositor/Merchant recoups costs, makes profit, but– Depositor decision cause paying bank losses

• Language of UCC presentment warranty, “No knowledge of any unauthorized signatures”

Why “Need” for Rule

8

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 5

Copyright© 2015 by the Electronic Check Clearing House Organization

• As Law – Does not reflect how society’s payments systems operates

• Unnecessarily exposes banks (as paying bank) to fraud losses

• Best defender is party who give value• Underlying justification for Price v Neal is

essentially obsolete• Fraud controls in 1762 England

– Eyewitness identification– Signature verification– No photo ID’s– No thumbprint signature– Extreme punishment

Relevance of Old Law

9

Copyright© 2015 by the Electronic Check Clearing House Organization

• Modern Check Processing– MICR encoding checks serve as carrier of electronic data• Image only furthered electronification of check

– Subsequent to BOFD, checks rarely touched by human hand • No human eye examines written information

– Minimum signature verification

• Signature verification has been made defunct – New technologies

• MICR

• Image

• Remote deposit capture (RDC) and mobile RDC

Modern Check Processing

10

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 6

Copyright© 2015 by the Electronic Check Clearing House Organization

Modern Check Processing• Volume considerations today versus 1762

– Clearly not feasible to examine every check

• Demands of modern business commerce recognized by UCC– Definition of “ordinary care” in 1990 version of UCC

• “..does not require a bank to examine an instrument..”

– Discussion on observance of reasonable commercial standards:• If bank takes a negotiable instrument for processing by automated means, reasonable commercial standards do not require the bank to examine the instrument if:– Does not violate the bank's prescribed procedures; and

– Bank's procedures do not vary unreasonably from general banking usage

11

Copyright© 2015 by the Electronic Check Clearing House Organization

Clearing House Rules & Rule 8• Clearing house can vary provisions of UCC

– Fraud personnel worked within clearing houses to address risk•Attempted to move risk outside banking industry

• Mid 1990’s: California paper clearing house developed rules for unauthorized unsigned draft (Rule 8)– Developed claim process that mirrored ACH–Worked with state legislator to modify UCC

•Still refer to claims for unauthorized unsigned items as “Rule 8” claim

12

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 7

Copyright© 2015 by the Electronic Check Clearing House Organization

Clearing House Rules & Rule 9• Texas through its clearing house developed

similar rule for signed items (Rule 9) – Forged or counterfeit check warranty and claim process

– Still refer to claims for breach of this warranty as a “Rule 9” claim

• Rule 8 & 9 were implemented in clearing houses all over the country– Eventually both were included in National Uniform Paper Rules

– Later incorporated in ECCHO Rules for image exchange

13

Regulatory Environment

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 8

Copyright© 2015 by the Electronic Check Clearing House Organization

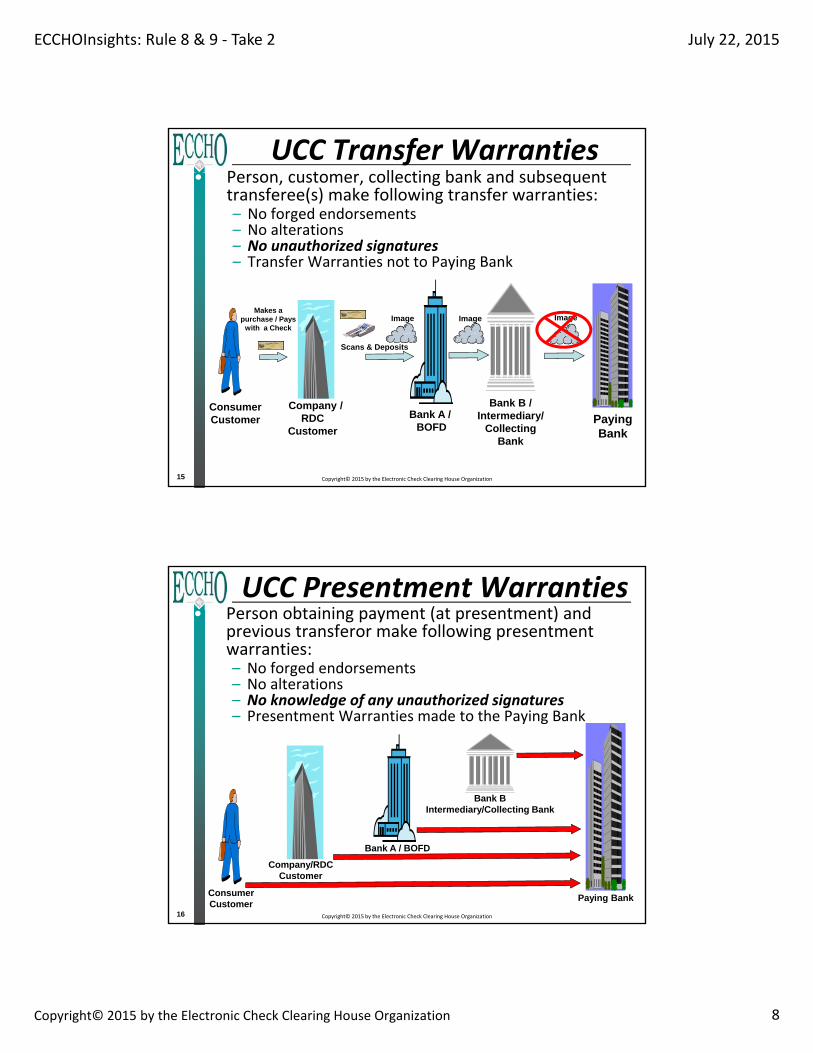

UCC Transfer Warranties• Person, customer, collecting bank and subsequent

transferee(s) make following transfer warranties:– No forged endorsements– No alterations– No unauthorized signatures– Transfer Warranties not to Paying Bank

Bank A / BOFD

Bank B / Intermediary/

Collecting Bank

Paying Bank

Company / RDC

Customer

ConsumerCustomer

Scans & Deposits

Makes a purchase / Pays

with a CheckImage Image Image

15

Copyright© 2015 by the Electronic Check Clearing House Organization

UCC Presentment Warranties• Person obtaining payment (at presentment) and

previous transferor make following presentment warranties:– No forged endorsements– No alterations– No knowledge of any unauthorized signatures– Presentment Warranties made to the Paying Bank

Bank A / BOFD

Bank B Intermediary/Collecting Bank

Paying BankConsumerCustomer

Company/RDC Customer

16

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 9

Copyright© 2015 by the Electronic Check Clearing House Organization

Return Forged Item?• Paying Bank must return expeditiously

– Reg CC requirement – Must return timely•Timing starts when the Paying Bank receives the item; when the item is considered “presented”

• Return or notice must be received by the depositary bank not later than 4:00 p.m. (local time of the depositary bank)– Second business day following the banking day on which the check was presented to the paying bank

17

Copyright© 2015 by the Electronic Check Clearing House Organization

Claims and Timing• Under UCC, Paying Bank cannot make

claim for counterfeit/unauthorized item after midnight deadline– If altered (not counterfeit), Paying Bank can make claim after midnight deadline•3‐year statue of limitations under UCC

18

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 10

Rule 8

Copyright© 2015 by the Electronic Check Clearing House Organization20

Rule 8• Remotely Created Checks – Non‐signature item

– Unsigned draft– Not signed by the drawer

• During RFC on Check 21 changes to Reg CC Fed requested input on including RCC warranty in Reg– Industry extremely supportive– Updated Reg CC for RCC 2006

• ECCHO Rules no longer impose warranty obligation on Depositary Bank– Definition and warranty for RCCs in Regulation CC – Definition of Remotely Created Check

• Check that is not created by paying bank and that does not bear signature applied or purported to be applied, by person on whose account check is drawn

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 11

Copyright© 2015 by the Electronic Check Clearing House Organization

Rule 8• Definition of RCC does not include

– Check created by paying bank (e.g. bill payment service)

• Reg CC Request For Comment (RFC 2014)– Proposed changes to narrow scope of RCC definition

• Remotely created check: An item that does not contain the signature of the drawer and was created by the payee or agent or service provider of payee

IMAGE

BOFD Intermediary Bank

IMAGE

Paying Bank creates & sendsUnsigned Draft

Deposit

Paying BankCompanyUnsigned

Draft

Bill Pay

RCC Warranty Claim?

Unauthorized

Consumer Customer

21

Copyright© 2015 by the Electronic Check Clearing House Organization

Remotely Created Check• Reg CC includes definition of RCC and

warranty provisions, but. . .does not establish a process for RCC claims– Process in industry image exchange rules:

• Federal Reserve Operating Circular 3 (OC3)

– §20.10 – Warranty Claims Regarding Remotely Created Checks Transferred or Presented by the Reserve Bank

• ECCHO Operating Rules & Commentary

– §XIX(O) – Remotely Created Checks

– §XII ‐ Adjustments

22

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 12

Copyright© 2015 by the Electronic Check Clearing House Organization

RCCs and Federal Reserve• FRB services established adjustment type for unauthorized

item– Warranty/Indemnity Claim (WIC) Associated with Unauthorized

Remotely Created Checks (URCC)• Used only if remotely created check processed through Fed

• Adjustment Requirements– Timing: 90 days from settlement of cash letter

• Signed affidavit must accompany claim

• No ability to disclaim– Documentation

• Copy of customer's written statement asserting under oath item in question was unauthorized– No specific language or form required

– Must clearly indicate that it was asserted under oath

– Must contain Reg CC language that serves as the basis for the warranty claim:

» “. . .that the person or entity on whose account the remotely created check is drawn did not authorize the issuance of the check in the amount stated on the check to the payee stated on the check”

• Legible photocopy of the front and back of the item in dispute23

Copyright© 2015 by the Electronic Check Clearing House Organization

RCCs and ECCHO Rules• Claim process – Rule 8

– Process within ECCHO rules use return mechanism (Section XIX(N)) but is not return but a breach of warranty claim

– Sets forth process for Paying Bank to make an Unauthorized RCC warranty claim• Claim sent to BOFD via return mechanism• To location BOFD receives returns

– Rules outline warranty claim process & timing• Paying Bank’s customer completes, signs and delivers a written statement under penalty of perjury (WSUPP) to Paying Bank

• Paying Bank delivers claim to BOFD within 90 calendar days after presentment of item in question

• BOFD may request copy of WSUPP– Not allowed to disclaim RCC claim

• Sample forms included in exhibits to Rules24

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 13

Copyright© 2015 by the Electronic Check Clearing House Organization

Rule 8 Timeline

25

Copyright© 2015 by the Electronic Check Clearing House Organization

RCCs and ECCHO Rules• Unauthorized RCC in Adjustment Matrix

– Section XII and Adjustment Matrix– Allow unauthorized RCC claim through adjustments•Mirrors Fed process and timing for URCC

•BOFD can not disclaim RCC adjustment claim by stating Paying Bank’s customer authorized RCC

26

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 14

Copyright© 2015 by the Electronic Check Clearing House Organization

Uses of RCCs• Should RCCs be Used

– Recent Fed study says 2.2% of checks are RCCs•21.1 Billion checks written

– Use ACH rather than RCC– Legitimate uses of RCC

•Banks that do not accept ACH

•Transactions not eligible for ACH

•Desire to maintain as check transaction, including midnight deadline for return

•Ability to give same day credit for late payments

27

Copyright© 2015 by the Electronic Check Clearing House Organization

RCC Fraud• Concern in industry over potential fraud with use of

RCC– Fraudsters known to use RCCs– Potential high return rates– Regulatory penalties to banks that did not recognize fraudulent RCC use

– Regulators issued guidance to banks on use of RCCs

• Cases involving fraudulent RCCs been around for years– FDIC and OCC rulings

• Wachovia case

• Delaware case resulted in bank being closed

• Two recent Department of Justice (DOJ) consent decrees involving RCCs and third party processors

28

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 15

Copyright© 2015 by the Electronic Check Clearing House Organization

Use of EPC Digit for RCCs• EPC: External processing code defined in X9.100‐160‐2

MICR standard– Digit that conveys special information for correct handling or routing of check or check data to banks and other processors

• Challenge in today’s image process– Identifying fraud/misuse in remotely created checks

• Inability to isolate RCCs in payment process• No distinct identifier in MICR line

– Regulators have cited as an issue

• ANSI Standards approach (X9.100‐160‐2)– Updated for character “6” in EPC field for RCC identification• Approved Nov‐2014/eff. Nov‐2015; May be adopted any time

• Risk mitigation consideration– Particularly for banks providing services to payment processors generating RCCs

29

Copyright© 2015 by the Electronic Check Clearing House Organization

Use of EPC Digit for RCCs• EPC digit–Highlighted on business‐sized check

–To be used for RCC identification

• EPC digit– Image of business‐sized check used to create an IRD

– RCC Id (EPC code) visible in image

30

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 16

Forged & Counterfeit Checks

ECCHO’s Rule 9

Copyright© 2015 by the Electronic Check Clearing House Organization

Poll Question• #1 ‐ Does your bank actively participate in Rule

9– Yes– No– Not sure– N/A

• Please answer in the webinar Polling screen

32

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 17

Copyright© 2015 by the Electronic Check Clearing House Organization

Poll Question• #2a – What area of your bank handles

outgoing Rule 9 claims– Adjustments– Returns– Fraud– Customer Service– Other

• #2b – What area of your bank handles incoming Rule 9 claims– Adjustments– Returns– Fraud– Customer Service– Other

33

Copyright© 2015 by the Electronic Check Clearing House Organization

Definitions – Rule 9• Rule 9 Item – Signature item; forged or

counterfeit check–Warranty defined in ECCHO Rules

•Depositary Bank warrants to Paying Bank that:

– Signature of purported drawer is not forged or otherwise unauthorized, and/or

– Related physical check is not counterfeit

– Section XIX(O) Forged and Counterfeit Check Warranties•Generally referred to as Rule 9

34

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 18

Copyright© 2015 by the Electronic Check Clearing House Organization

Who / What / Why of Rule 9?• Who: Rule 9 – Available only for check

images exchanged among ECCHO members – Must agree to exchange under the Rules– Must not have opted out of Rule 9

• What: Purpose of Rule 9 is to handle forged and counterfeit items recognized by bank customer after midnight return deadline– Rule 9 provides Paying Bank an option

• Why: Paying Bank may file claim to recover from a fraudulent item – Ultimately shifts responsibility (assigned in UCC 4) to the depositing customer

35

Copyright© 2015 by the Electronic Check Clearing House Organization

Warranty• Warranty begins with BOFD

– Warranty only applies to exchanges under ECCHO rules• ECCHO Rules only cover image exchanges• ECCHO Rules cover only member‐to‐member exchanges

• ECCHO warranty does NOT apply:– If non‐ECCHO member exchange– For exchanges through Fed– To paper exchanges

• Rule 9 may apply to paper exchanges, if exchanged under paper rules that include Rule 9 provision

• Foreign bank deposits– If bank accepts deposit from foreign bank:

• BOFD still under Reg CC provisions, but. . .• BOFD does not make Rule 9 warranty under ECCHO rules

36

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 19

Copyright© 2015 by the Electronic Check Clearing House Organization37

Who Bears the Loss?• Rule 9 is an interbank warranty

– Does not provide Depositary Bank with authority to debit its customer’s account• Governed by applicable law including deposit agreement• Assumes Depositary Bank employs KYC policies

• BOFD does not maintain loss if depositing customer does not have funds in account– Sufficiency of funds provision allows BOFD to disclaim if claim exceeds available funds • On at least one day during claim period

– Only required to review account once

• No funds? – BOFD disclaims and loss moves back to Paying Bank

• Where loss typically would lie

• Funds in account? – BOFD liable to Paying Bank for amount of claim– Even if BOFD chooses not to charge its customer

Copyright© 2015 by the Electronic Check Clearing House Organization

Opt‐Out• Participation is the default in ECCHO Rules

– Opt‐out permitted• Unless member subject to agreement making rule mandatory

– Currently thirteen (13) ECCHO members out of nearly 3,000 have opted out (listed on ECCHO website)

– Process for opt‐out• Opt‐out election must be made by an authorized representative that is also officer of financial institution– Must communicate opt‐out request to ECCHO

– ECCHO will confirm receipt of your decision and will include the effective date of the opt‐out

• Opt‐out cancelled (default back to participation under rules), cannot elect to opt‐out again for 6 months

– Complete description of processes on website38

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 20

Copyright© 2015 by the Electronic Check Clearing House Organization

Opt‐Out• Why Allow for Opt‐out?

– Still some controversy over rule• Disagree with shifting liability to BOFD• Concerns about more risk

• Mixed legal opinions– Would like to reverse Price v Neal– No funds sufficiency requirement– BOFD takes risk

• Like in ACH and other payments

• Some believe rule is discriminatory– Question ability of clearing house rules to vary this aspect of UCC

– Finality of payment basic concept in check law and this allows return after midnight deadline

– BOFD in no position to know signature of Paying Bank customer

39

Copyright© 2015 by the Electronic Check Clearing House Organization40

Mandatory Rule 9• Some Support for Mandatory Rule 9

– Rule in effect for nearly 20 years with no known litigation

• Original premise was Paying Bank had original check– No longer the case today with image exchange

• Paying Bank needs relief

• No longer has original check

– Paying Banks post from MICR data• Little review of check or check image

– Original rule was from risk perspective• Should now consider operational perspective as well

• Rule 9 is pro‐image

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 21

Copyright© 2015 by the Electronic Check Clearing House Organization

Rule 9 Claim• Rule 9 claim – Breach of warranty claim

– ECCHO Rules [XIX (O)]: Use return process to make claim from Paying Bank to Depositary Bank

• Typically, under check law Paying Bank liable for forged drawer’s signature or counterfeit item– Rule 9 allows Paying Bank to make claim to Depositary Bank after drawer customer claims item is forged or counterfeit

• How to make Rule 9 claim other than through a return process?– Send warranty claim by letter to BOFD return location• Letter does not carry monetary value• Banks have to determine how to settle for the transaction

41

Copyright© 2015 by the Electronic Check Clearing House Organization42

Claim Process• Similar timing/process as RCC warranty claim (when using

returns process Section XIX(N))– Paying Bank must make claim to BOFD via return process

• Use return mechanism, but actually adjustment

• Customer written statement for unauthorized item required– Cannot send these claims through the Fed

• Return must contain notation of “Breach of Warranty” and/or “Do Not Redposit or Re‐Present” or similar language– Paying Bank may use reason code that reflects item is sent as

warranty claim• Image standards use return reason of “3” – Warranty Breach

– “5” – Forged and Counterfeit Warranty Breach (Rule 9) ‐ New

• Claim may be made via – Electronic image– Paper copy of front and back of electronic image– Substitute Check– Letter (Sample letter in Rules)

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 22

Copyright© 2015 by the Electronic Check Clearing House Organization

Rule 9 – Sample Letter[NOTE: This letter should be reviewed by Member’s legal counsel prior to use. Do not use this letter for items exchange through the Federal Reserve Banks. Before using this letter to make a claim, you should confirm that the BOFD has not opted out of Rule 9 coverage and that the item was exchanged under the ECCHO Rules by the BOFD.]

Date: ___________________

Attention: Incoming Domestic Returns or Collections Department Re: Breach of Warranty Claim ‐‐ Forged Maker or Counterfeit Check (a “Rule 9 Claim”) Our Reference Number: ________________

Dear Sir/Madam:

This letter constitutes our claim to your institution arising from your institution’s breach of warranty under ECCHO Rule XIX(O) (also known as a “Rule 9” claim) with respect to the enclosed item that was presented to us as an image in an exchange governed by the ECCHO Rules. ECCHO Rules permit us to make this warranty claim to the depository bank by delivering the claim to the location for returns of the depository bank.

We were the paying bank with respect to this item and your bank is the depository bank with regard to this item. ECCHO Rule XIX(O) provides a warranty given by every bank that transfers or presents an item that:

the signature of the purported drawer of the Related Physical Check is not forged or otherwise unauthorized, and/or

the Related Physical Check is not counterfeit.

Pursuant to this Rule, we are enclosing with this letter: (a) a copy of the item, and [(b) a statement of report fraud/unauthorized item from our customer.] [OPTIONAL AT TIME OF CLAIM]

We make demand on your institution for the face amount of the item, in accordance with the procedures and requirements of ECCHO Rule XIX(O). Within 15 days of the date of the receipt of this letter, please provide your institution’s response to this warranty claim, in accordance with Rule XIX(O).

If the warranty claim is accepted, payment for the claim can be made in accordance with the following settlement instructions:

[INSERT SETTLEMENT INSTRUCTIONS HERE]

We reserve any rights that may be available to us with respect to the item under applicable law or rule. Please note that a warranty claim under this Rule is not subject to the defense of a late return under the UCC midnight deadline.

If you have any questions concerning this matter, please contact __________________ at ###‐###‐####, extension ####, during the hours of __________________ (Monday through Friday).

Any written correspondence relating to this letter or the warranty claim, including a notice of acceptance or rejection of the warranty claim, can be directed to the following contact person:

[INSERT CONTACT INFORMATION HERE] __________________ __________________ __________________ Email address: ___________________________

Sincerely: Enclosures

Sample Letter Only – Review with your own legal counsel before sending as a claim

Include settlement instructions

Enclose copy of the item and (optionally) a copy of the customer’s WSUPP

43

Copyright© 2015 by the Electronic Check Clearing House Organization

Disclaim Process• Sending Bank / BOFD may disclaim

warranty claim for:– Account closed– Claim amount exceeds funds in account– Claim was not made timely as defined in rules

– Sending Bank is not first bank to which check was transferred

– Opt‐out in effect– Other defenses as provided by other applicable law

44

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 23

Copyright© 2015 by the Electronic Check Clearing House Organization

Rule 9 – Model Disclaimer

45

Copyright© 2015 by the Electronic Check Clearing House Organization Banks are all ECCHO Members

Current Process Flow“Rule 9” Claim: Section XIX (O)

Statement

Depositing Customer

Paying Bank

IMAGE IMAGEDepositedCheck

BOFD

Bank X

BOFD Requests Copy of WSUPPWithin 15 Business Days

of receipt of claim

Available $ to Cover Warranty Claim?YES: May Charge

Customer

-or- NO:

Disclaim – Back to Paying Bank

ImagePaperCopy

SubCheck

or or or Letter

Warranty Claim made directly to BOFDWithin 15 Business Days of receipt of WSUPP

Letter, Sub Check, Paper Copy (front/back), or Image46

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 24

Copyright© 2015 by the Electronic Check Clearing House Organization

Rule 9 Timeline

47

Copyright© 2015 by the Electronic Check Clearing House Organization

Yes

No

If < 61 Days

Send AffidavitTo Paying

Bank

Yes

No

Customer Claim Paying Bank

If < 16 Days

Send Claim toBOFD

No

BOFD

If < 16 Days

B

A

C

OrOr

Yes

No

BOFD

If < 11 Days

Send AffidavitTo BOFD

SendRequest

for Affidavit toPayingBank

Yes

No

Paying Bank

B

C

B

Or C

DE E

Yes

A

COr

Rule 9 Decision Table

48

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 25

Copyright© 2015 by the Electronic Check Clearing House Organization

If $s inCustomer’s

Account

No

Yes

Debit customer & avoid loss(if claim received without entry, settle

with Paying Bank)

BOFD

B

Receives disclaimer

Paying Bank

BOFD

Paying Bank retains loss

OrCustomer not debited

CBOFD has loss

D

E

BOFD

CSend

disclaimerto

Paying Bank

Rule 9 Decision Table

49

Copyright© 2015 by the Electronic Check Clearing House Organization

Compare Rule 8 and Rule 9

Rule 8 Rule 9

Remotely created check – Unsigned draft

Forged or Counterfeit check – Fraudulent signature item

Source of Warranty: ECCHO Rules

Source of Warranty: Regulation CC

Opt-out Option?

Exchanges in Which Warranties Arise?• Private sector exchange (ECCHO Rules)

Exchanges in Which Warranties Arise?• Federal Reserve Bank exchange• Private sector exchange (ECCHO Rules)• Correspondent exchanges (non-ECCHO)

50

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 26

Rule 9 Challenges in Image

Copyright© 2015 by the Electronic Check Clearing House Organization

Risks vs Benefits• Banks typically act as both Paying Bank and BOFD

– Both banks have opportunity to make claim or claim made to it

– Balanced and fair rules to share risks by all members• Paying bank

– Able to recover some money from the BOFD that would have previously been a loss

– Rules do not change way bank decides to reimburse customers for forged or counterfeit checks

• BOFD try to recover money from depositing customer for Paying bank– Balance risk of customer relationship in charging back customer for Rule 9 claim

– Customer service impact has been negligible– Recovering of funds paid from fraudulent item very positive

52

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 27

Copyright© 2015 by the Electronic Check Clearing House Organization

Risks vs Benefits• Average amount of items $400 or less• Millions of dollars savings based on Rule 9

claims over the years• Only about 5% or less are disclaimed by

BOFD• Much greater chance item will be

disclaimed if payable to individual– Fraud has occurred at both Paying Bank and BOFD

53

Copyright© 2015 by the Electronic Check Clearing House Organization

Challenges For Image• Paying Bank’s Rule 9 claim must be made

to BOFD via returns process– Claim cannot be made through Fed

• If bank returns through Fed– No mechanism to make claim– Claim made through Fed may be rejected as late return

54

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 28

Copyright© 2015 by the Electronic Check Clearing House Organization

Challenges For Image• Disclaim process, still needs work

– Rules developed in local clearinghouses where exchanges typically in person; banks in reasonable proximity to one another•When need to disclaim, item was exchanged between members

– Today with nearly 100% image exchange environment, members are no longer in same geographic location• Images exchanged through multiple banks and/or networks

– Rule 9 claim and disclaim cannot be made to intermediaries or Federal Reserve• Claim must be made directly to BOFD

• How to disclaim to appropriate party?55

Copyright© 2015 by the Electronic Check Clearing House Organization

BOFD

Intermediary(Correspondent or Fed) Paying Bank

SWITCH

Warranty Claim

Rule 8 /9 Warranty Claim

Dishonor Claim – How??

$$$$Receive Funds How & When??

Challenges For Image

Image Cash Letter

(ICL)

Image Cash Letter

(ICL)

56

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 29

Copyright© 2015 by the Electronic Check Clearing House Organization

Return Reason Code• Original rule required stamp to tell BOFD

Rule 9 claim– Stamp not practical in image– Allow for return reason code

•Return reason same for either customer or administrative return

– “3” – Warranty Breach

» Includes Rule 8 & 9 claims– “5” – Forged and Counterfeit Warranty Breach

» Rule 9 – New

57

Copyright© 2015 by the Electronic Check Clearing House Organization

ECCHO Rules Update• Presented at April 8, 2015 Operations

Committee meeting– Two changes to the Rules approved

•Allow longer time period for disclaim and settlement of claims if BOFD makes claim in manner not subject to automated settlement

– Extended to 15th business day after receipt of claim or disclaimer

•Delivery of warranty claim letter in paper form

– Sample letter included in Rules exhibits

58

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 30

Copyright© 2015 by the Electronic Check Clearing House Organization

Questions?

59

Copyright© 2015 by the Electronic Check Clearing House Organization

Additional Information• Exhibits from ECCHO Rules

– Disclaimer Form: Rule 8 and 9– Explanatory Charts for Rule 8 and 9 Process

• Events Timing• Decisions

– Model Customer Written Statement for Warranty Claim under Rules 8 and 9

– Sample claim letter (coming soon)• Available on ECCHO website

(www.eccho.org)– Rule 9 At‐a‐Glance– FAQs

• Rule 8, Rule 9– Understanding “Rule 8” and “Rule 9” Warranty and Claims processes

60

ECCHOInsights: Rule 8 & 9 ‐ Take 2 July 22, 2015

Copyright© 2015 by the Electronic Check Clearing House Organization 31

Thank You!

Copyright© 2015 by the Electronic Check Clearing House Organization

Electronic Check Clearing House Organization (ECCHO)

3710 Rawlins Street; Suite #1075

Dallas, TX 75219

www.eccho.org

July 22, 2015

ECCHO Education Programs