yangyang chen, monash university ferdinand a. gul, monash...

TRANSCRIPT

1

Executive Equity Risk-Taking Incentives and Audit Service Pricing

Yangyang Chen, Monash University

Ferdinand A. Gul, Monash University

Madhu Veeraraghavan, Monash University

Leon Zolotoy, Melbourne Business School, University of Melbourne

We are grateful to Chris Armstrong, Nampuna Dolok Gultam, Teh Chee Ghee, Steven Low,

C.H. Tee and seminar participants at Monash University for helpful comments and

suggestions. The usual disclaimer applies.

2

Executive Equity Risk-Taking Incentives and Audit Service Pricing

ABSTRACT: Using a sample of 11,120 firm-year observations for 1,873 U.S. firms

spanning the period 2000-2010, we show a positive association between the

sensitivity of CEO compensation to stock return volatility (vega) and audit fees. We

also show that the positive association between vega and audit fees is more

pronounced for firms that are susceptible to litigation risk and weakens in the post-

Sarbanes-Oxley Act (SOX) period. In supplementary tests, we show that CEO age

and power also affect the association between vega and audit fees. Collectively, our

results suggest that audit firms incorporate executive risk-taking incentives in the

fees they charge for their services.

Keywords: Executive Compensation; Audit Fees; Vega; Litigation Risk; SOX

JEL Classifications: M41; M42; M52

3

I. INTRODUCTION

In this paper we examine how auditors respond, in terms of audit fees, to risk-

taking incentives induced by CEO compensation portfolio. More specifically, we

examine whether CEO equity incentives, such as the sensitivities of CEO

compensation to stock return volatility (vega) and stock price (delta), are associated

with audit fees. We build on prior studies that argue that a higher vega is likely to

induce managers to be less risk averse and consequently engage more in financial

misreporting (Armstrong et al., 2013). The higher likelihood of financial misreporting,

in turn, is likely to affect audit risks and audit fees, ceteris paribus.

A primary motivation for our study is based on the call by the Public Company

Accounting Oversight Board (PCAOB) that auditors carefully evaluate and consider

client executive compensation practices (see PCAOB Release No. 2012-001

proposing a new auditing standard for related party transactions and amendments to

auditing standards regarding significant unusual transactions). The proposed

standard addresses three areas for auditors: (a) evaluating a company’s

identification of, accounting for, and disclosure of relationships and transactions

between the company and its related parties; (b) identifying and evaluating a

company’s accounting and disclosure of its significant unusual transactions; and

(c) obtaining an understanding of a company’s financial relationships and

transactions with its executive officers that is sufficient to identify risks of material

misstatement.

4

Our research question is motivated more specifically by the third area identified

in the release, since it requires auditors to perform procedures to obtain an

understanding of the company’s financial relationships with its executive officers.1 In

particular, PCAOB Release 2012-001 (p. 2) states that

“Incentives and pressures for executive officers to meet financial targets can

result in risks of material misstatement to a company’s financial statements.

Such incentives and pressures can be created by a company’s financial

relationships and transactions with its executive officers (e.g. executive

compensation including perquisites and any other arrangements)”.

Hence, examining the association between executive equity risk incentives and

audit fees constitutes an important step toward our understanding of the auditing

process, on the one hand, and the effect of executive compensation on the quality of

financial reporting, on the other. In addition, the use of equity-based compensation in

the form of stock and options has not only grown substantially in recent years but

has also attracted the attention of regulators (Perry and Zenner, 2000; Coles et al.,

2006; Murphy and Sandino, 2010).

Our study integrates the executive compensation literature with the audit fee

literature. Although the two literatures are rich and have generated significant debate

and research, empirical evidence linking them is almost non-existent (Wysocki,

1 Appendix 4 - Additional Discussion (p. A4-41) states that the auditor should perform procedures that include but

are not limited to (1) reading employment and compensation contracts and (2) reading proxy statements and other relevant company filings with the U.S. Securities and Exchange Commission (SEC) and other regulatory agencies that relate to the company’s financial relationships and transactions with its executive officers. Paragraph 10A of the proposed amendments to Auditing Standard No. 12 requires the auditor to perform procedures designed to identify risks of material misstatement related to the company’s financial relationships and transactions with its executive officers. Page A4-42 of PCAOB release No. 2012-001 states “understanding how a company has structured its compensation for executive officers can assist the auditor in understanding whether such compensation arrangements affect the assessment of the risks of material misstatement.” Page A4-43 of PCAOB release No. 2012-001 states that the proposed amendment requires “the auditor to consider inquiring the chair of the compensation committee or its equivalent and any compensation consultants engaged by either the compensation committee or the company regarding the structuring of the compensation for executive officers.”

5

2010). In a recent paper, Wysocki (2010, pp. 155-156) notes that “fertile ground

exists for future research on the links between the two compensation literatures.”

Our intuition regarding the link between risk-taking incentives induced by CEO

compensation portfolio on audit fees is straightforward and draws on two strands of

related literature. The first strand examines the association between audit risk and

audit fees. Auditors face audit risk, the risk of failure to discover material

misreporting, which exposes audit firms to substantial litigation risk. With a total of

$5.66 billion in private litigation payments paid by U.S. audit firms over 1996–2007

(Badertscher et al., 2011), exposure to litigation risk can also lead to severe

reputational damage, substantial loss of market share, and declarations of

bankruptcy (Seetharaman et al., 2002; Hilary and Lennox, 2005; Weber et al., 2008;

Skinner and Srinivasan, 2012). Prior studies also show that auditors charge higher

audit fees from clients with lower reporting quality and a higher likelihood of financial

misreporting (Pratt and Stice, 1994; Gul et al., 2003; Bédard and Johnstone, 2004;

Hogan and Wilkins, 2008; Charles et al., 2010).

The focus of prior research in the second strand is on the relation between

financial misreporting, equity risk, and CEO compensation portfolio sensitivities.

Studies show that managers who decide to engage in financial misreporting face

substantial monetary and non-monetary risks, suggesting that the decision to

misreport will alter managers’ perceived risk of their portfolio holdings (Karpoff et al.,

2008; Armstrong et al., 2013). Prior research also provides evidence consistent with

the argument that a lower quality of financial reporting increases the reporting firm ’s

equity risk by adversely affecting transparency and increasing information

asymmetry (Hribar and Jenkins, 2004; Gray et al., 2009; Kravet and Shevlin, 2010;

Rajgopal and Venkatachalam, 2011). Consequently, CEO equity incentives can

6

encourage or discourage financial misreporting, depending on whether the expected

benefits of misreporting outweigh its effect on manager risk aversion. In particular,

since vega measures the sensitivity of CEO wealth to stock return volatility, a higher

vega is likely to induce managers to be less risk averse and, consequently,

encourage misreporting (Armstrong et al., 2013).

Taken together, the evidence provided in prior research is consistent with the

notions that (a) auditors charge higher fees from clients with lower reporting quality

and a higher likelihood of financial misreporting and (b) a higher vega encourages

misreporting. These findings suggest that auditors are expected to increase their

assessments of audit risks and charge higher fees from firms with higher vega, a

prediction that forms the basis for our main research question. We also address two

subsidiary questions: In the first question we examine how this effect varies across

firms with different levels of litigation risk, while in the second we examine whether

the vega-audit fee relation is weaker in the post-Sarbanes-Oxley Act (SOX) period.

The motivation for the first subsidiary question is that prior studies document a

positive relation between audit fees and client firm litigation risk (Seetharaman et al.,

2002; Venkatachalam, 2008; Choi et al., 2009; Kim et al., 2012). If vega reflects

managerial incentives to engage in financial misreporting, then its effect on audit

fees will depend, among other factors, on how likely the failure to detect financial

misreporting will lead to subsequent legal actions from client firm stakeholders.

Therefore, we hypothesize that the effect of vega on audit fees should be stronger

for firms that are more susceptible to litigation risk.

The motivation for the second subsidiary question is that a major purpose of

SOX is to protect investors by improving the accuracy and reliability of corporate

disclosures and to restore investor confidence in the integrity of firms’ financial

7

reporting (Lobo and Zhou, 2006). In addition, SOX directs the Securities and

Exchange Commission (SEC) to require the CEOs and CFOs of all listed firms to

certify the material accuracy and completeness of financial statements. Prior

research provides evidence consistent with SOX regulations having a positive effect

on reporting quality (Lobo and Zhou, 2006; Bartov and Cohen, 2009; Iliev, 2010). In

addition, SOX imposes significant criminal penalties on CEOs and CFOs for

certifying financial statements that do not comply with the requirements of SOX. In

short, since regulatory scrutiny and penalties for aggressive financial reporting is

greater post-SOX, we hypothesize that the positive association between vega and

audit fees is weaker in the post-SOX period.

We establish four findings. First, using a sample of 11,120 firm-year

observations for 1,873 unique U.S. firms spanning 2000-2010, we show that firms

with a high vega, on average, pay significantly higher audit fees. Specifically, we

document that increasing vega from the first to the tenth decile leads to an increase

of approximately 29% in audit fees. Second, we show that the association between

vega and audit fees is more pronounced for firms susceptible to litigation risk. Third,

we find that the association between vega and audit fees, while remaining

significant, has weakened in the post-SOX period. Finally, we document that CEO

age and power have a significant impact on the association between vega and audit

fees. Collectively, our results suggest that audit firms incorporate executive risk-

taking incentives in their fees and that the strength of the association between audit

fees and vega depends in a predictable manner on firm litigation risk and changes in

regulatory environment, as well as CEO characteristics.

We perform a battery of robustness tests to validate our main findings. First, we

examine the sensitivity of our results to alternative measures of vega, suggested in

8

the prior literature (Armstrong et al., 2013). Second, we investigate whether the

effect of vega on audit fees remains significant after controlling for prior misreporting

and corporate governance. Third, we control for projected changes in firm’s business

risk induced by high vega (Coles et al., 2006), Last, we address endogeneity

concerns by employing changes-in-variables analysis (Anderson et al., 2004; Klock

et al., 2005) and two-stage least squares (2SLS) approach (Larcker and Rusticus,

2010). Our main results continue to hold.

Our paper makes four contributions to the literature. First, at a general level, we

contribute to the compensation and corporate governance literatures on how

compensation arrangements affect the pricing of audit services offered to the firm.

The issue of whether compensation policies can provide value-increasing or value-

decreasing incentives to managers still remains uncharted territory (e.g., Jensen and

Murphy, 1990; Garvey and Milbourn, 2006). By establishing a link between CEO

compensation portfolio sensitivities and audit fees, we make a major contribution to

this evolving literature. Second, our study responds to the concerns expressed by

the PCAOB that compensation incentives for executive officers to meet financial

targets can result in risks of material misstatement. We provide evidence that these

concerns are justified, at least in terms of auditors’ assessments of audit risks. Our

third contribution is to the auditor compensation literature. Prior studies in the auditor

compensation strand document audit fees to be associated with a variety of factors,

such as client firm size, corporate governance, business complexity, and auditor

characteristics (Hay et al., 2006). However, none of the prior studies examine the

relation between audit fees and managerial equity incentives. Our study is the first to

clearly establish such a link.

9

Last but not least, we contribute to a growing stream of research that examines

the association between executive compensation portfolio sensitivities and the

quality of reporting (Burns and Kedia, 2006; Erickson, 2006; Armstrong et al., 2010,

2013; Jiang et al., 2010; Feng et al., 2011). In particular, our study is related to the

work of Armstrong et al. (2013), who document strong evidence of a positive relation

between portfolio vega and misreporting. Our findings emphasize the economic

implications of vega in encouraging managers to misreport by showing that audit

firms incorporate an increase in audit risk associated with higher vega by charging

higher fees. Overall, our study improves our understanding of how compensation

portfolio sensitivities affect auditor assessments of audit risks.

The remainder of the paper is organized as follows. Section II discusses the

related literature and develops our testable hypotheses. Section III describes the

sample and variable definitions. Our main empirical results are presented in Section

IV and robustness checks are reported in Section V. Section VI presents the results

for litigation risk and Section VII presents the results for SOX. Section VIII examines

the effect of CEO characteristics on the association between vega and audit fees

and Section IX concludes the paper.

II. RELATED LITERATURE AND HYPOTHESIS DEVELOPMENT

Audit Fees

Prior studies have examined the association between the risk of client

misreporting, litigation risk and audit fees. Studies show that auditors incorporate

litigation risk by supplying higher audit effort or charging higher fees to clients with

higher risk of misreporting. For instance, Kim et al. (2012) develop an analytical audit

10

fee model in which auditors choose an optimal auditing effort to minimize total audit

costs. The authors show that audit fees are inversely related to the client’s reporting

quality, since an increase in the probability of client misreporting increases the

auditor's litigation risk. Consequently, auditors respond to a decline in reporting

quality by either increasing auditing effort (Simunic, 1980; Simunic and Stein, 1996)

or charging higher premiums to cover potential litigation losses (Pratt and Stice,

1994; Gramling et al., 1998), which leads to an increase in auditor remuneration

(Kim et al., 2012). In their review of the early audit fee literature, Simunic and Stein

(1996) conclude that the U.S. evidence is generally consistent with audit firms

increasing their fees in the face of higher than usual litigation risk. Among more

recent studies, Gul et al. (2003) find a positive association between earnings

management and audit fees. In a similar vein, Bédard and Johnstone (2004) report

that heightened earnings management risk increases planned audit effort and higher

auditor billing rates. Hogan and Wilkins (2008) find that audit fees are higher for firms

that disclose internal control deficiencies (ICDs), suggesting that auditors either

increase their effort or charge higher premiums for firms in the presence of increased

control and information risks. Charles et al. (2010) report a positive association

between audit fees and Audit Integrity’s proprietary measure of financial reporting

risk.

Vega, Misreporting and Firm Risk Taking

Misreporting increases the risk of managerial wealth for at least two reasons.

First, financial misreporting exposes managers to substantial risks, such as

restrictions on their future employment, and SEC fines (Karpoff et al., 2008). Second,

misreporting decreases the quality of financial reports and hence adversely affects

11

transparency, which, in turn, increases risk. These studies include, among others,

those of Francis et al. (2004, 2005), Hribar and Jenkins (2004), Gray et al. (2009),

Kravet and Shevlin (2010), and Rajgopal and Venkatachalam (2011).

Three prior studies are related to ours. Engel et al. (2010) investigate the

relation between compensation paid to members of the audit committee and demand

for monitoring the financial reporting process. The authors report a positive relation

between audit committee compensation and audit fees, suggesting that firms are

willing to deviate from a one-size-fits-all approach in director pay in response to

increasing demand for monitoring. Rego and Wilson (2012) examine the effect of

equity risk incentives on corporate tax planning and conclude that a high vega is

associated with greater tax avoidance. Armstrong et al. (2013) examine the role of

vega on managerial incentives to misreport and document strong evidence of a

positive relation between vega and misreporting, suggesting that a higher vega is

associated with a lower quality of financial reporting.

Our study differs from that of Engel et al. (2010) in that they focus on the relation

between the levels of compensation paid to members of the audit committee and

audit fees, whereas we focus on the effect of CEO compensation portfolio

sensitivities on audit fees. Similarly, while Rego and Wilson (2012) examine the

association between vega and corporate tax planning and Armstrong et al. (2013)

study the link between vega and financial misreporting, we extend their work by

considering audit fees.

Hypothesis Development

The studies outlined above find that deterioration in quality of reported earnings

is associated with a higher cost of equity and an increase in firm-specific volatility,

12

concluding that financial misreporting increases equity risk. Since vega measures

the sensitivity of CEO compensation portfolio to stock return volatility, higher vega is

likely to encourage managerial risk-taking behavior (Armstrong and Vashishtha,

2012). Rego and Wilson (2012) show that firms with a high vega engage in more

aggressive tax avoidance, consistent with the notion that a high vega encourages

managers to engage in more risky corporate tax planning. More importantly, since

financial misreporting increases equity risk, a higher vega provides managers with a

clear incentive to misreport. Consistent with this notion, Armstrong et al. (2013) find

strong evidence of a positive relation between vega and misreporting. They also

show that the effect of vega on misreporting is economically larger than many other

determinants of misreporting. In sum, prior studies suggest that (a) audit fees are

positively related to a client–firm’s propensity to misreport and (b) the propensity to

misreport is positively related to vega. This discussion leads to our first hypothesis.

HYPOTHESIS 1: Ceteris paribus, firms with greater CEO compensation portfolio

volatility sensitivity (vega) pay higher audit fees.

We note that in contrast to vega, the theoretical relation between delta, which

measures the sensitivity of CEO compensation portfolio with respect to share price,

and misreporting is ambiguous (Armstrong et al., 2013). On the one hand, high delta

might encourage misreporting by providing the CEO incentives to boost stock price

through manipulating financial statements (Smith and Stulz, 1985). On the other

hand, high delta might discourage misreporting by increasing CEO risk aversion.

Since the wealth of CEOs relies more on firm stock price, their incentive to engage in

risky misreporting is reduced (Ross, 2004; Lewellen, 2006; Armstrong and

Vashishtha, 2012). Consistent with the notion of delta having two countervailing

13

effects on managerial incentives to misreport, the prior literature provides

inconclusive evidence on the relation between delta and the quality of reporting.2

Hence, we control for delta in our analysis but do not have any theoretical

predictions and, consequently, do not offer any formal hypothesis on the relation

between delta and audit fees.

We next address two subsidiary questions. First, we examine how the vega-audit

fee relation varies across firms with different levels of litigation risk. Prior studies list

client business risk among the primary risks that need to be assessed by auditors in

their client-acceptance decisions (Huss and Jacobs, 1991; Johnstone, 2000; Bell et

al., 2001).

Seetharaman et al. (2002) and Choi et al. (2009) show that auditors charge

higher fees for firms that are cross-listed in countries with stronger legal regimes

than they do for non-cross-listed firms, concluding that higher audit fees reflect an

increase in auditors’ legal liability. Venkataraman et al. (2008) examine the

association between auditors’ exposure to legal liability and audit fees in an IPO

(initial public offering) setting. Legally, auditing an IPO-filing company exposes the

auditor to substantially higher litigation risk compared to that associated with auditing

the same company after it goes public. The authors show that auditors earn higher

fees in IPO engagements compared to post-IPO engagements, consistent with

auditor firms charging higher fees as compensation for an increase in litigation risk.

Based on prior studies, we predict that the effect of vega on audit fees will depend

on the perceived auditor risk resulting from engagement with the firm. If the vega

reflects managerial incentives to engage in financial misreporting, then its effect on

2 See, for example, Burns and Kedia (2006), Erickson (2006), Armstrong et al. (2010), Jiang et al. (2010), Feng

et al. (2011), and Armstrong et al. (2013).

14

audit fees will depend, among other factors, on how likely the failure to detect

financial misreporting will lead to subsequent legal actions from client-firm

stakeholders. Consequently, we predict that the effect of vega on audit fees will be

more pronounced for firms with a higher likelihood of litigation. This discussion leads

to our second hypothesis.

HYPOTHESIS 2: Ceteris paribus, the positive association between CEO

compensation portfolio volatility sensitivity (vega) and audit fees is stronger for firms

with higher litigation risk.

Second, we examine the effect of SOX on the association between vega and

audit fees. Enacted as a response to numerous incidents of accounting restatements

and corporate fraud, SOX’s primary goal was to improve the quality of financial

reporting and restore investor confidence by increasing governance requirements,

imposing more severe penalties for managerial misconduct, and implementing

incentives for firms to enhance internal control systems (Coates, 2007; Iliev, 2010;

Hirschey et al., 2012). Prior literature provides evidence consistent with SOX

regulations having a positive effect on reporting quality. For instance, Lobo and Zhou

(2006) document that firms tend to engage less in accrual-based earnings

management and resort to more conservative accounting reporting in the post-SOX

period. Bartov and Cohen (2009) document a decline in the downward management

of earnings expectations and upward accrual-based earnings management. Singer

and You (2011) find that firms that were required to comply with SOX during the first

two years of its implementation improved the quality of their financial reporting

compared to control firms that were not required to comply. Iliev (2010) documents

that following the introduction of SOX, firms report lower discretionary earnings,

15

concluding that SOX legislation leads to more conservative accounting. Given that

the primary goal of SOX was to improve the quality of financial reporting, it provides

an appealing setting to examine the informational content of vega and its effect on

audit fees. Our argument is that SOX should reduce managerial incentives to

misreport. Hence, if vega is incrementally informative about the managerial

propensity to misreport, we expect to observe a weaker effect of vega on audit fees

in the post-SOX period. This leads to our third hypothesis.

HYPOTHESIS 3: Ceteris paribus, the positive association between CEO

compensation portfolio volatility sensitivity (vega) and audit fees is weaker in the

post-SOX period.

III. DATA AND VARIABLES

We obtain the data for this study from three sources. The audit fee data are from

the Audit Analytics database. Audit Analytics collect information about the identity of

the auditor practice office that provides auditing services to the firm, as well as the

audit and non-audit fees they charge, from the audit report in SEC filings since 2000.

We collect CEO compensation data from the Standard and Poor’s (S&P)

ExecuComp database. This database contains detailed information of the options

and stock holdings of the top managers for S&P 1500 firms since 1992. Firm

financial information is obtained from Compustat annual files. Since the audit fee

data are available from 2000 onward, our empirical analysis spans the period 2000-

2010. Merging the three databases results in a final sample of 11,120 firm-year

observations for 1,873 unique firms. We winsorize the variables at both the upper

and lower one percentile to mitigate the effect of outliers.

16

We adopt the audit fee model developed by Simunic (1980) and follow prior

literature (Simunic and Stein, 1996; Johnstone and Bédard, 2003; Gul and Goodwin,

2010) in selecting the control variables. We define audit fees (AFEE) as the dollar

amount of audit fees the firm pays the auditor over the fiscal year. The Big 4 dummy

(BIG4) is a dummy variable equal to one if the firm is audited by one of the Big 4

auditors and zero otherwise. The auditor office size (OFC) is the number of clients of

the firm’s auditor practice office. Auditor tenure (TNR) is the number of years the firm

has retained the current auditor. Book assets (BVA) are the book value of the firm’s

total assets. Market-to-book (MB) is the ratio of the firm’s market capitalization over

its book value of equity. Leverage (LEV) is the ratio of long-term debt to total assets.

The current ratio (CURR) is the ratio of current assets to total assets. The quick ratio

(QUICK) is the ratio of current assets net of inventory to current liabilities. The return

on assets (ROA) is the ratio of operating income to total assets. The foreign currency

translation dummy (FRGN) is a dummy variable equal to one if the firm has foreign

currency translation and zero otherwise. The number of segments (SEG) is the

number of the firm’s business segments. Following prior research, our analysis uses

the natural logarithm of audit fees (LAFEE), auditor office size (LOFC), auditor

tenure (LTNR), book assets (LBVA), and the number of segments (LSEG).

We define CEO compensation portfolio volatility sensitivity or vega (VOLSEN) as

the change in the value of the CEO’s option portfolio in response to a 0.01 change in

the annualized standard deviation of the firm’s stock return, while we define CEO

compensation portfolio price sensitivity or delta (PRCSEN) as the change in the

value of the CEO’s stock and options portfolio in response to a 1% increase in the

firm’s stock price. We follow Guay (1999) and Core and Guay (2002) in computing

both variables. Partial derivatives of the option value with respect to stock return

17

volatility and stock price are based on the Black-Scholes model adjusted for

dividends by Merton (1973). Following prior research (Brockman et al., 2010;

Armstrong and Vashishtha, 2012; Armstrong et al., 2013), our analysis uses the

natural logarithm of the two variables (LVOLSEN and LPRCSEN).

Table 1 presents the summary statistics of the variables and shows that the

mean and median dollar values of the audit fees of our sample firms are

$2.663 million and $1.390 million, respectively. Regarding the incentive variables,

the mean vega indicates that, on average, CEO compensation increases by

$157,400 in our sample for a 0.01 increase in stock return volatility. The mean delta

in our sample implies that a 1% increase in stock price, on average, is associated

with an increase of $595,900 in CEO compensation. Further, 92.3% of our sample

firms are audited by Big 4 auditors. The average number of clients of the auditor

offices is 54.9 and the average auditor tenure is 14.4 years. Our sample firms also

have mean book assets of $4,512.4 million and a mean market to book of 2.889. On

average, these firms have long-term debt that is 18.6% of total assets and current

assets that are 44.4% of total assets. Their mean quick ratio is 1.883 and their mean

return on assets is 0.088. Table 1 also reports that 47.1% of our sample firms have

foreign currency translation and the average number of business segments is 2.642.

[Insert Table 1 about here]

IV. AUDIT FEES AND CEO COMPENSATION PORTFOLIO SENSITIVITIES

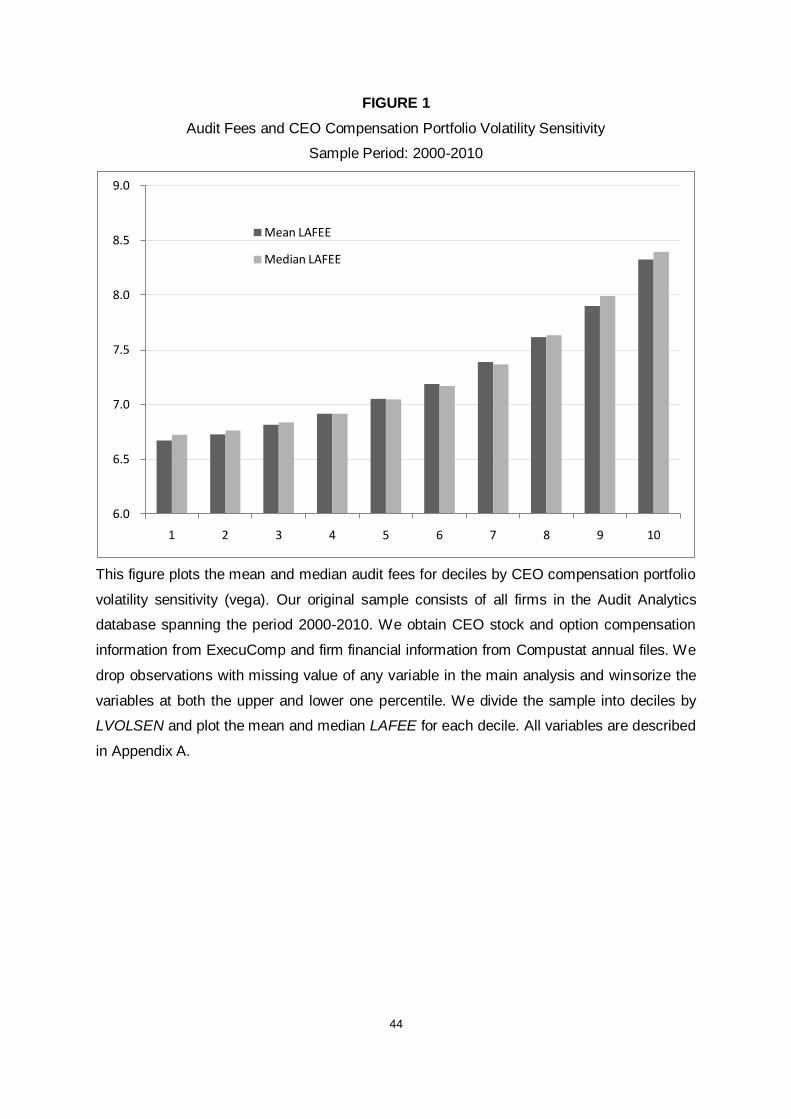

First, we report the results of the univariate analysis of the association between

vega and audit fees. The sample is split into deciles based on vega (VOLSEN). We

then calculate the mean and median audit fees (LAFEE) for each group. As shown in

Figure 1, the mean value of audit fees for the lowest vega group is around 6.67. It

18

increases monotonically with the increase in vega. The mean value of audit fees for

the highest vega group reaches 8.31. The difference in mean audit fees between the

lowest and highest vega deciles is 1.64 and is significant at the 1% level (t-statistics

37.16). The change in the median value of audit fees follows a similar pattern.

Univariate analysis demonstrates a positive and monotonic relation between vega

and audit fees. This finding is consistent with our first hypothesis.

[Insert Figure 1 about here]

We next proceed with the multivariate analysis by estimating the following regression

, 0 1 , 2 , 3 , 4 ,

5 , 6 , 7 , 8 , 9 , 10 ,

11 , 12 , 13 , ,

4i t i t i t i t i t

i t i t i t i t i t i t

i t i t i t i t

LAFEE LVOLSEN LPRCSEN BIG LOFC

LTNR LBVA MB LEV CURR QUICK

ROA FRGN LSEG Ind Yr

(1)

Here i denotes firm, t denotes the year, Ind is industry fixed effects based on two-

digit SIC codes, Yr is year fixed effects, and ε is the error term. The dependent

variable is LAFEE, the natural logarithm of audit fees. The independent variable of

interest is LVOLSEN, the natural logarithm of vega. Our first hypothesis predicts a

positive and significant coefficient for LVOLSEN. The regression is performed by

pooled ordinary least squares (OLS), with t-statistics robust to heteroskedasticity and

clustering at the firm level. We present the regression results in Table 2.

Column (1) of Table 2 presents the results of the regression with CEO

compensation portfolio sensitivity variables only. This column shows that LVOLSEN

is positively and significantly related to LAFEE, thus suggesting that auditors charge

higher fees for firms with higher vega. This finding is also consistent with our

univariate analysis. In column (2) we add several auditor characteristics and in

column (3) we further add a number of firm characteristics. We add both industry and

19

year fixed effects in column (4). In all four regressions, the coefficient of LVOLSEN

remains positive and statistically significant. Last, to facilitate economic interpretation

of our results, we rank each independent variable, except for the two dummy

variables (the Big 4 and foreign currency translation dummies) for each year, and

then partition the resulting ranks into deciles labeled from 1 (lowest decile) to 10

(highest decile). Next, we regress LAFEE against the decile ranking of independent

variables. The results are presented in column (5) of Table 2 and further confirm the

positive relation between vega and audit fees. The effect of vega on audit fees is

also economically significant. Specifically, the magnitude of the coefficient in column

(5) demonstrates that moving from the first to the tenth decile of vega increases log

audit fees by 0.032*(10-1) = 0.288, which constitutes, approximately, an increase of

29% in audit fees. Table 2 also shows that the effect of delta on audit fees is less

robust compared to that of vega. We find that the coefficient of LPRCSEN is

insignificant in columns (1), (2), and (5) and becomes negative and significant in

columns (3) and (4). Hence, no specific conclusion can be reached regarding the

effect of delta on audit fees, consistent with delta having two countervailing effects

on executive risk-taking behavior.

Table 2 also shows that LAFEE is positively related to BIG4, LOFC, and LTNR,

suggesting that Big 4 auditors, larger auditor practice offices, and auditors with

longer tenure charge higher audit fees. Further, LAFEE is also positively related to

LMVE, LEV, CURR, and FRGN and negatively related to MB, QUICK, and ROA.

These results suggest that larger firms, firms with a higher leverage ratio and current

ratio, firms with foreign currency translation (i.e., have foreign business), and firms

with more business segments are charged higher audit fees, while firms with a

higher market-to-book ratio, quick ratio, and return on assets are charged lower audit

20

fees. Overall, these findings are largely consistent with the prior literature (e.g., Gul

and Goodwin, 2010).

[Insert Table 2 about here]

V. ROBUSTNESS CHECKS

Alternative Measures of Vega

In this section, we conduct a number of robustness tests to validate our main

findings. We start by examining the sensitivity of our results to the way vega is

constructed to ensure that our results are robust to alternative definitions. We

employ four alternative measures of vega. In our first measure, we investigate

whether our results hold for the top five executives (including the CEO) instead of

only the CEO. Since firm decisions are usually made in teams (Aggarwal and

Samwick, 2003), we check how the aggregate compensation portfolio sensitivities of

the top five executives influence audit fees. The regression results for the top five

executives vega (LVOLSEN_MGM) and delta (LPRCSEN_MGM) are presented in

column (1) of Table 3. The table shows that the coefficient of LVOLSEN_MGM is

positive and significant, suggesting that a higher vega for the top five managers is

associated with higher audit fees.

In our second measure, we decompose the CEO vega into a vega from

previously granted options (LVOLSEN_OLD) and a vega of new options granted

during the year (LVOLSEN_NEW). Full information about the exercise price and time

to maturity is available from ExecuComp for new grants; however, such data are

unavailable for previous option grants. For the old grants we estimate vega using the

approximation method of Core and Guay (2002). We present the regression results

21

in column (2) of Table 3. We find the coefficients for both old and new option grant

vegas to be positive and significant, suggesting that our results are not driven by a

potential measurement error induced by the old option grants. In our third measure,

we decompose the vega of the option grants into a vega from exercisable options

(LVOLSEN_EX) and a vega of non-exercisable options (LVOLSEN_UNEX) and

report the results in column (3) of Table 3. Both coefficients are positive and

significant. In our last measure, we follow Armstrong et al. (2013) and examine the

component of vega that is unrelated to recent stock performance. Since vega is a

function of both current stock price and option grant features, variation in vega and

consequently its effect on audit fees can be driven by recent stock performance

rather than option grant features (Armstrong et al., 2013). To rule out this possibility,

we regress vega against stock returns over the past year and define performance-

unrelated vega (LVOLSEN_NONPERF) as the residuals from the regression. The

results in column (4) of Table 3 show that the coefficient for performance-unrelated

vega is positive and significant, suggesting that our results are not driven by recent

stock performance.

[Insert Table 3 about here]

Omitted Variables

We also investigate whether the association between vega and audit fees is

caused by omitted variables. To mitigate this concern we first examine whether our

main results hold after controlling for prior misreporting, which can be used by the

auditor in assessing the risk of a firm’s future misreporting. If the effect of vega on

audit fees is associated with it being informative about a CEO’s propensity to

misreport in the future, it should have an incremental effect on audit fees after other

22

potential indicators of misreporting are controlled for. Following the prior literature,

we employ two measures of misreporting. The first measure is the restatement

dummy (RST), a dummy variable equal to one if the firm restates its financial

statements in the previous year and zero otherwise. The second measure is the

MDD measure (MDD), which is Dechow and Dichev’s (2002) accruals quality

measure as modified by McNichols (2002). The measure is estimated over the past

five years and reflects the portion of current accruals left unexplained by the model.

Therefore, a higher value of the MDD measure indicates poorer accruals quality. We

present the results in Table 4. The coefficients for both the restatement dummy and

MDD measure are positive and significant, consistent with the notion that audit firms

require higher compensation from firms with higher past misreporting. More

importantly, the coefficient for LVOLSEN remains positive and statistically significant

when we include each of the prior misreporting measures individually, as well as

when both variables are included simultaneously.

Second, we examine whether our results remain robust after controlling for

corporate governance measures. We re-estimate our basic model with corporate

governance characteristics included as additional control variables. More specifically,

we include three measure of corporate governance: the governance index

(GINDEX), dedicated institutional ownership (DEDIO), and board independence

(BIDP).

We obtain the data from RiskMetrics and follow Gompers et al. (2003) in

constructing the governance index. The variable GINDEX is a count of the number of

antitakeover provisions in a firm’s charter and in the legal code of the state in which

the firm is incorporated. 3 Our second measure of governance is dedicated

3 Our results also hold for the entrenchment index of Bebchuk et al. (2009).

23

institutional ownership, which is the proportion of shares held by dedicated

institutional investors.4 Bushee (1998, 2001) defines dedicated institutional investors

as those with long investment horizons and concentrated share holdings. Dedicated

institutional investors are shown in the prior literature (Gaspar et al., 2005;

Ramalingegowda and Yu, 2012) to be the group of institutional investors that is most

likely to monitor managers. We obtain the institutional ownership data from Thomson

Financial and the institutional investor classification from Brian Bushee’s website.5

Our final governance measure is board independence, defined as the proportion

of independent directors on the board. Prior studies show that stronger boards are

negatively associated with earnings management, restatements, and fraud and

positively associated with audit effort and earnings quality (Dechow et al., 1996;

Beasley et al., 2000; Carcello et al., 2002; Klein, 2002; Bédard et al., 2004). The

results reported in columns (4) to (7) of Table 4 are consistent with those of Carcello

et al. (2002), in that we document a positive relation between governance measures

and audit fees. After controlling for governance measures, the coefficient of

LVOLSEN remains positive and significant, suggesting that the effect of vega on

audit fees is not driven by their correlation with corporate governance.

[Insert Table 4 about here]

Changes in Business Risk

Next we investigate whether the effect of vega on audit fees remains significant

after controlling for projected changes in a firm’s business risk. Prior studies

document strong causal relation between vega and firm risk, in that a firm with a high

4

We also employed total institutional ownership and the top five institutional ownership defined as the percentage of shares held by all institutional investors and the top five institutional investors as additional measures of institutional ownership. Our findings hold. 5 See http://accounting.wharton.upenn.edu/faculty/bushee/IIclass.html.

24

vega tends to implement riskier investment policies (Guay, 1999; Coles et al., 2006;

Low, 2009). Since auditing standards require auditors to gain an understanding of

client business risk to better identify areas that may create pressure on financial

reporting (Winograd et al., 2000), projected changes in business risk can potentially

affect audit fees.

To control for the effect of vega on business risk, we employ a two-step

procedure. First, we follow Coles et al. (2006) and regress measures of firm

investment policy - R&D intensity (R&D) and capital expenditure (CAPEX) - against

the lagged values of LVOLSEN and LPRCSEN, and a set of control variables. Next,

we re-estimate our basic regression, with the fitted values from the first step included

as additional control variables. If our results are not driven by the effect of vega on

firm investment policy, the coefficient of vega should remain positive and significant.

Consistent with Coles et al. (2006), we show in Table 5 that a higher vega is

associated with a riskier investment policy, as evident by its positive effect on R&D

intensity and negative effect on firm capital expenditure. More importantly, after

including the fitted values of both R&D and CAPEX in our basic regression, the

coefficient for LVOLSEN remains positive and significant, as reported in columns (3)

to (5) of Table 5. The effect of vega on audit fees remains significant irrespective of

whether we include the fitted measures individually or jointly 6 . Accordingly, we

conclude that our main results are not driven by changes in firm business risk. While

we use delta as a control variable, its effect on audit fees is also of some interest. In

particular, we note that when we include the fitted values of R&D intensity and

capital expenditure in our basic regression, the effect of delta on audit fees becomes

6 As an additional robustness test we repeat our analysis with actual values of CAPEX and R&D included as

control variables. The coefficient for LVOLSEN remains positive and statistically significant.

25

statistically insignificant, thus suggesting that the negative effect of delta on audit

fees as documented in Table 2 is likely due to its effect on firm business risk.

[Insert Table 5 about here]

Endogeneity

Since the relation between vega and audit fees could be driven by endogenous

effects, we also conduct tests for endogeneity. It is possible that both audit fees and

vega are correlated with some time-invariant firm characteristics, resulting in their

apparent relation. We adopt two methods in this section to address this potential

endogeneity problem.

The first method is the changes-in-variables approach (Anderson et al., 2004;

Klock et al., 2005; Jayaraman and Milbourn, 2012). In this approach, we regress the

annual change in LAFEE against the annual change in LVOLSEN, LPRCSEN, and

the control variables. Weber (2006) argues that changes-in-variables analysis is less

affected by endogeneity problems. In addition to providing time-series evidence of

the link between audit fees and vega, firm-specific changes regressions also help

alleviate concerns about correlated omitted variables (Jayaraman and Milbourn,

2012)The results are presented in Table 6. Column (1) presents the results with

changes in CEO compensation portfolio sensitivities only, column (2) presents the

results with changes in auditor characteristics as controls, and column (3) presents

the results with changes in additional firm characteristics as controls. In all three

columns, the change in LVOLSEN is positively and significantly associated with a

change in LAFEE, suggesting that an increase in vega results in an immediate

increase in audit fees. Therefore, the results from the changes-in-variables analysis

suggest that our findings are not driven by endogenous effects.

26

[Insert Table 6 about here]

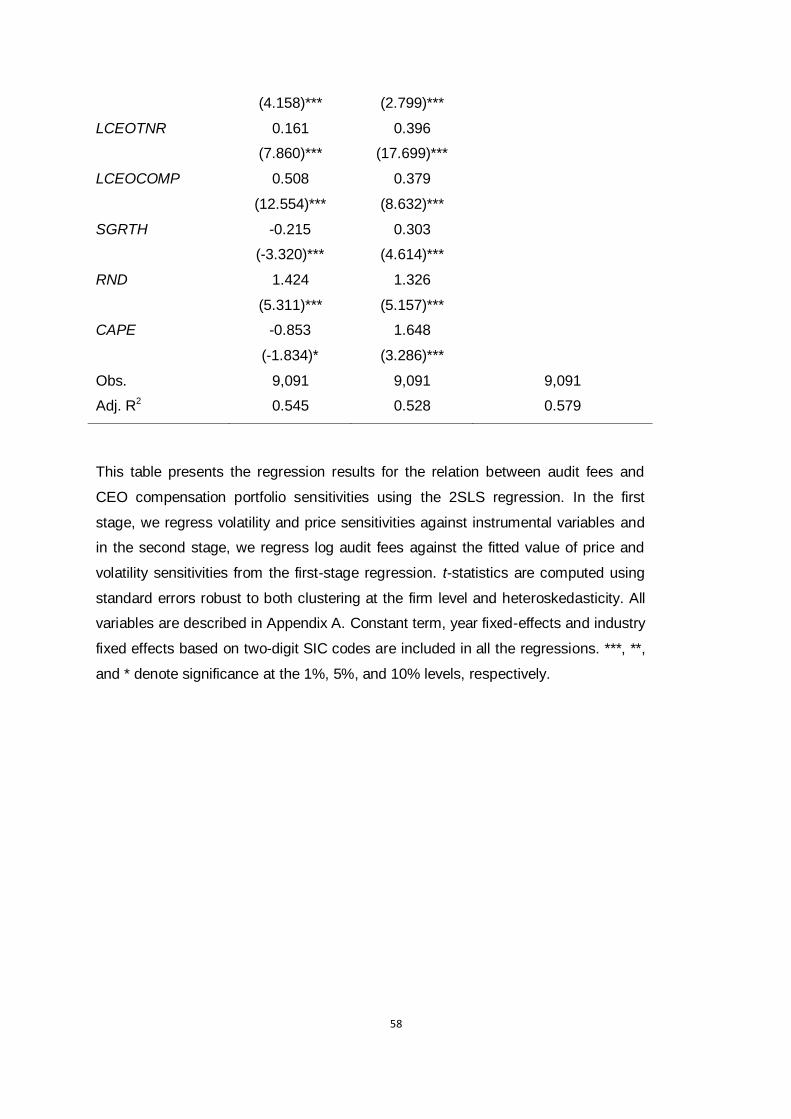

The second method is the 2SLS approach, a common method in accounting

research in addressing potential endogeneity problem (e.g., Larcker and Rusticus,

2010). In the first stage, we regress LVOLSEN and LPRCSEN against a set of

instrumental variables suggested by prior research (Himmelberg et al., 1999; Knopf

et al., 2002; Coles et al., 2006; Ortiz-Molina, 2006; Brockman et al., 2010), as well as

all the control variables in Eq. (1). The instrumental variables include the cash ratio

(CASH), log CEO tenure (LCEOTNR), log CEO salary and bonus compensation

(LCEOCOMP), sales growth (SGRTH), R&D (RND), and capital expenditure

(CAPEX). Specifically, the cash ratio is the ratio of firm cash holdings to total assets;

log CEO tenure is the natural logarithm of the number of years since the current

CEO became CEO; log CEO salary and bonus compensation is the natural logarithm

of the dollar amount of the CEO’s annual base salary and bonus; sales growth is the

annual growth rate of sales; R&D is the ratio of R&D expenses to sales; and capital

expenditure is the ratio of capital expenses to total assets. In the second stage, we

regress LAFEE against the fitted values of LVOLSEN and LPRCSEN from the first-

stage regressions.

The results for the 2SLS regression are presented in Table 7. Columns (1) and

(2) present the results for the first-stage regression and column (3) presents the

results for the second-stage regression. The table shows that the fitted value of

LVOLSEN is positively and significantly associated with LAFEE, further confirming

that our findings are not driven by endogenous effects.

[Insert Table 7 about here]

27

VI. VEGA, AUDIT FEES, AND LITIGATION RISK

In this section we test the second hypothesis by interacting vega with multiple

measures of litigation risk. Following prior research, we consider three measures of

litigation risk. Our first measure of litigation risk is firm size (LBVA). Prior studies

consistently show that auditor litigation risk increases with client size (Stice, 1991;

Carcello and Palmrose, 1994; Lys and Watts, 1994; Heninger, 2001). Our second

measure is the high litigation industry dummy (LITIND), a dummy variable equal to

one if the firm is in the biotechnology, computer, electronics, or retail industries and

zero otherwise. This measure was first suggested by Francis et al. (1994), who show

that firms in these industries are subject to a higher number of litigations compared

to other industries. The industry-based litigation measure is employed by Ajinkya et

al. (2005), Beatty et al. (2008), and Brown and Tucker (2011).

Our third measure is the high litigation risk indicator (LITRISK), which is the

principal component of a set of litigation predictor variables suggested by Shu (2000)

and Kim and Skinner (2012). A higher value of the measure indicates a higher

likelihood of litigation risk. The predictor variables include firm size (LBVA), a high

litigation industry dummy (LITIND), sales growth (SGRTH), stock return, return

volatility, and return skewness. Stock return is the cumulative stock return over the

fiscal year, return volatility is the standard deviation of monthly stock returns over the

fiscal year, and return skewness is the skewness of monthly returns over the fiscal

year. The results reported in column (1) of Table 8 show that the coefficient for the

interaction term between LBVA and LVOLSEN is positive and significant, suggesting

that the effect of vega on audit fees is stronger for larger firms. Column (2) presents

the results for the high litigation industry dummy and our findings show that the effect

28

of vega on audit fees is more pronounced for firms in high litigation risk industries.

Column (3) presents the results for the high litigation risk indicator and our findings

show that the interaction between LITRISK and LVOLSEN is positive and significant.

Since a higher value of LITRISK indicates higher litigation risk, our results suggest a

more significant effect of vega on audit fees for firms subject to higher litigation risk.

These findings are in line with our second hypothesis.

[Insert Table 8 about here]

VII. VEGA, AUDIT FEES, AND SOX

To test our third hypothesis, we interact vega with the SOX dummy (SOXD), a

dummy variable equal to one for the post-SOX era (after year 2002) and zero for the

pre-SOX era (before year 2002). The results presented in column (1) of Table 9

show that the coefficient for the interaction term between SOXD and LVOLSEN is

negative and statistically significant, suggesting that the effect of vega on audit fees

is less pronounced since the implementation of SOX.

To gain further insights into the effect of SOX on the association between vega

and audit fees, we distinguish between the pre- and post-compensation recovery

provision (commonly known as clawbacks) periods. These provisions, first

introduced by the passage of Section 304 of the SOX of 2002 (SOX 304), authorizes

the SEC to enforce the recovery of bonuses paid to corporate executives when a

firm’s financial restatements are due to noncompliance with financial reporting

requirements as a result of misconduct (Babenko et al., 2012; Chan et al., 2012).

Though SOX 304 has been successfully enforced in only a few cases (Salehi and

Marino, 2008; Fried and Shilon, 2011), voluntary adoption of clawback provisions by

companies has become increasingly popular over the last decade (Babenko et al.,

29

2012). Babenko et al. (2012) document that among the S&P 1500 firms, reported

usage of clawback provisions increased from less than 1% in 2000 to over 48% by

2011. The authors also report that by 2011 almost 70% of S&P 500 firms had

adopted a clawback policy. Chan et al. (2012) find that the voluntary adoption of

clawback provisions leads to a reduction in financial misstatements and is perceived

by auditors as associated with lower audit risk, consistent with clawback provisions

reducing managerial incentives to misreport. Since the adoption of clawback

provisions were rare prior to 2005 (Babenko et al., 2012; Chan et al., 2012), we

repeat our analysis on the SOX dummy for the pre-clawback provision sample (i.e.,

2000–2004) to investigate whether the diminishing effect of vega on audit fees in the

post-SOX era is driven by the popularity of clawback provisions.

The results reported in column (2) of Table 9 show that the interaction between

the SOX dummy and vega remains negative and significant, suggesting an

immediate drop in the effect of vega on audit fees since the passage of SOX. We

then investigate whether the adoption of clawback provisions further mitigates the

effect of vega on audit fees. Specifically, we interact vega with the clawback dummy

(CLAWD), a dummy variable equal to one for the years 2003-2005 and zero for the

years after 2005. We perform the test on the post-SOX sample (2003–2010) and the

results presented in column (3) show that the interaction term between CLAWD and

LVOLSEN is negative and significant. Therefore, the effect of vega on audit fees is

further mitigated in the 2005-2010 period. For robustness check purposes, we

conduct all three tests on a sample of firms with observations both before and after

the two events. The purpose of the exercise is to check whether our findings are

driven by differences between the group of firms that exit the sample before the

30

events and the group of firms that enter the sample after the events. Our untabulated

results available upon request are similar to those reported in Table 9.

[Insert Table 9 about here]

VIII. VEGA, AUDIT FEES, AND CEO CHARACTERISTICS

In this section we complement our analysis by examining the effect of CEO

characteristics on the association between vega and audit fees7. More specifically,

we investigate the effect of CEO age, tenure, and power on the relation between

vega and audit fees. Recent research in corporate finance documents that CEO

characteristics impact corporate policies. For example, Malmendier et al. (2011) and

Cronqvist et al. (2012) show that managerial characteristics have significant

explanatory power for corporate financing decisions, while Serfling (2013) suggests

that CEO personal traits may affect risk-taking behavior. Prior theoretical research

suggests that CEO age impacts risk-taking behavior, but the findings are mixed and

inconclusive. For instance, the theoretical models of Scharfstein and Stein (1990),

Hirshleifer and Thakor (1992), Zwiebel (1995), and Holmström (1999) suggest that

career concerns make younger CEOs more risk averse, leading to conservative

investment policies. In contrast, the managerial signaling model of Prendergast and

Stole (1996) suggests that younger CEOs invest aggressively, taking greater risks to

signal their superior ability. Following these studies, we define CEO age (CEOAGE)

7 We also investigate the effect of auditor characteristics on the association between vega and audit fees. For the

sake of brevity, we do not tabulate the results. We consider Big 4, office size, and auditor tenure auditor characteristics. We do not find a significant effect of Big 4 or office size on the relation between vega and audit fees. However, our results show that the relation between vega and audit fee is stronger if the auditor has longer tenure. This finding is consistent with those of Geiger and Raghunanadan (2002), Myers et al. (2003), Ghosh and Moon (2005), and Gul et al. (2007), since they suggest that auditors with longer tenure are able to provide higher-quality auditing services, since auditors need time to develop client-specific knowledge to perform an effective audit. Our intuition is that longer auditor tenure helps auditors understand the compensation policies of the firms they audit.

31

as an ordinal variable equal to one for CEOs with age below 35, two for CEOs with

age between 36-45, three for CEOs with age between 46-55, and four for CEOs with

age above 55. Chen and Zheng (2012) document a positive relation between CEO

tenure and risk taking, suggesting that longer tenure is associated with declining

career concerns. On the other hand, longer tenure is also related to CEO reputation

(Milbourn, 2003). Since misreporting increases firm risk, longer tenure may also

have an adverse effect on CEO incentives to misreport. This discussion suggests

that the effect of CEO age and tenure on the relation between audit fees and vega is

an empirical question, which we address here. We define CEO tenure (LCEOTNR)

as the natural logarithm of the number of years the current CEO became the CEO.

We examine CEO power in terms of unitary versus dual leadership styles.

Following Brickley et al. (1997), we define unitary leadership (CEOUNI) as the case

when the CEO and the chairman of the board titles are vested in one individual and

dual leadership as the case where the two positions are held by different individuals.

Overall, there is a general consensus that unitary leadership enhances CEO power

and leads to negative consequences (e.g., Conyon and Peck, 1998; Goyal and Park,

2002; Adams et al., 2005). Accordingly, we predict that greater CEO power

magnifies the positive relation between audit fees and CEO vega. Table 10 reports

the results for the effect of CEO characteristics (age, tenure, and power) on the

association between vega and audit fees in three columns. Column (1) shows that

the relation between vega and audit fees is stronger if the CEO is older, while in

column (2) we do not find a significant effect for CEO tenure. Our findings in column

(3) show that the relation between vega and audit fees is stronger if the CEO is also

the chairman of the board. Taken together, the findings reported in column (1) are

consistent with the theoretical prediction of the career concerns hypothesis of

32

Scharfstein and Stein (1990), Hirshleifer and Thakor (1992), Zwiebel (1995), and

Holmström (1999) and the results of column (3) are consistent with the notion that

unitary leadership enhances the ability of CEOs to misreport, since CEO power is

greater.

[Insert Table 10 about here]

IX. CONCLUSION

With Release No. 2012-001, the PCAOB proposed a new auditing standard for

related party transactions and amendments to auditing standards regarding

significant unusual transactions. The release stated that auditors must carefully

evaluate and consider the client’s executive compensation practices and specifically

consider executive compensation practices in the context of a company’s financial

relationships and transactions with its executive officers. Although auditors may have

considered these risks prior to the call by the PCAOB, little or no research exists on

the association between executive compensation and auditor compensation. Our

paper is the first attempt to fill the void.

For a large sample of U.S. firms spanning 2000-2010, we show that firms with

high vega, on average, pay higher audit fees. We also find that the association

between vega and audit fees is pronounced for firms that are more susceptible to

litigation risk and the vega-audit fee relation weakens in the post-SOX period. In

addition, we document that CEO age and power and auditor tenure significantly

affect the association between vega and audit fees. Taken together, our results

provide first major evidence that auditors incorporate audit risk associated with risk-

taking incentives induced by executive compensation by charging larger fees from

firms with a high vega.

33

REFERENCES

Adams, R. B., H. Almeida, and D. Ferreira. 2005. Powerful CEOs and Their Impact on

Corporate Performance. Review of Financial Studies 18: 1403-1432.

Aggarwal, R. K., and A. A. Samwick. 2003. Performance Incentives within Firms: The Effect

of Managerial Responsibility. Journal of Finance 58: 1613-1650.

Ajinkya, B., S. Bhojraj, and P. Sengupta. 2005. The Association between Outside Directors,

Institutional Investors and the Properties of Management Earnings Forecasts.

Journal of Accounting Research 43: 343-376.

Anderson, R. C., S. A. Mansi, and D. M. Reeb. 2004. Board Characteristics, Accounting

Report Integrity, and the Cost of Debt. Journal of Accounting & Economics 37: 315-

342.

Armstrong, C. S., A. D. Jagolinzer, and D. F. Larcker. 2010. Chief Executive Officer Equity

Incentives and Accounting Irregularities. Journal of Accounting Research 48: 225-

271.

Armstrong, C. S., and R. Vashishtha. 2012. Executive Stock Options, Differential Risk-

Taking Incentives, and Firm Value. Journal of Financial Economics 104: 70-88.

Armstrong, C., F. Larcker, G. Ormazabal, and D. Taylor. 2013. The Relation Between Equity

Incentives and Misreporting: The Role of Risk-Taking Incentives. Journal of Financial

Economics (forthcoming).

Babenko, I., B. Bennett, J. Bizjak, and J. L. Coles. 2012. Clawback Provisions, Working

paper, Arizona State University.

Badertscher, B., B. Jorgensen, S. Katz, and W. Kinney. 2011. The Effect of Private and

Public Equity Ownership on Litigation Risk and Audit Fees, AAA Annual Meeting

Proceedings.

Bartov, E., and D. A. Cohen. 2009. The "Numbers Game" in the Pre- and Post-Sarbanes-

Oxley Eras. Journal of Accounting, Auditing & Finance 24: 505-534.

Beasley, M. S., J. V. Carcello, D. R. Hermanson, and P. D. Lapides. 2000. Fraudulent

Financial Reporting: Consideration of Industry Traits and Corporate Governance

Mechanisms. Accounting Horizons 14: 441-454.

Beatty, A., J. Weber, and J. J. Yu. 2008. Conservatism and Debt. Journal of Accounting &

Economics 45: 154-174.

Bebchuk, L., A. Cohen, and A. Ferrell. 2009. What matters in corporate governance? Review

of Financial Studies 22: 783-827.

34

Bédard, J., S. M. Chtourou, and L. Courteau. 2004. The Effect of Audit Committee Expertise,

Independence, and Activity on Aggressive Earnings Management. Auditing: A

Journal of Practice and Theory 23: 15-37.

Bédard, J. C., and K. M. Johnstone. 2004. Earnings Manipulation Risk, Corporate

Governance Risk, and Auditors' Planning and Pricing Decisions. Accounting Review

79: 277-304.

Bell, T. B., W. R. Landsman, and D. A. Shackelford. 2001. Auditor's Perceived Business

Risk and Audit Fees: Analysis and Evidence. Journal of Accounting Research 39: 35-

43.

Brickley, J. A., J. Coles, and G. A. Jarrell. 1997. Leadership Structure: Separating the CEO

and Chairman of the Board. Journal of Corporate Finance 3: 189-220.

Brockman, P., X. Martin, and E. Unlu. 2010. Executive Compensation and the Maturity

Structure of Corporate Debt. Journal of Finance 65: 1123-1161.

Brown, S. V., and J. W. Tucker. 2011. Large-Sample Evidence on Firms' Year-over-Year

MD&A Modifications. Journal of Accounting Research 49: 309-346.

Burns, N., and S. Kedia. 2006. The Impact of Performance-Based Compensation on

Misreporting. Journal of Financial Economics 79: 35-67.

Bushee, B. J. 1998. The Influence of Institutional Investors in Myopic R&D Investment

Behavior. Accounting Review 73: 305.

Bushee, B. J. 2001. Do Institutional Investors Prefer Near-Term Earnings over Long-Run

Value? Contemporary Accounting Research 18: 207-246.

Carcello, J. V., D. R. Hermanson, T. L. Neal, and R. A. Riley Jr. 2002. Board Characteristics

and Audit Fees. Contemporary Accounting Research 19: 365-384.

Carcello, J. V., and Z.-V. Palmrose. 1994. Auditor Litigation and Modified Reporting on

Bankrupt Clients. Journal of Accounting Research 32: 1-30.

Chan, L. H., K. C. W. Chen, T.-Y. Chen, and Y. Yu. 2012. The Effects of Firm-Initiated

Clawback Provisions on Earnings Quality and Auditor Behavior. Journal of

Accounting and Economics 54: 180-196.

Charles, S. L., S. M. Glover, and N. Y. Sharp. 2010. The Association between Financial

Reporting Risk and Audit Fees before and after the Historic Events Surrounding

SOX. Auditing: A Journal of Practice and Theory 29: 15-39.

Chen, D., and Y. Zheng. 2012. CEO Tenure and Risk Taking. Working Paper, University of

Baltimore.

Choi, J.H., J.B. Kim, X. Liu, and D.A. Simunic. 2009. Cross-listing audit fee premiums: theory

and evidence. The Accounting Review 84: 1429-1463

35

Coates, J. C. 2007. The Goals and Promise of the Sarbanes–Oxley Act. Journal of

Economic Perspectives 21: 91-116.

Coles, J. L., N. D. Daniel, and L. Naveen. 2006. Managerial Incentives and Risk-Taking.

Journal of Financial Economics 79: 431-468.

Conyon, M. J., and S. I. Peck. 1998. Board Control, Remuneration Committees, and Top

Management Compensation. Academy of Management Journal 41: 146-157.

Core, J., and W. Guay. 2002. Estimating the Value of Employee Stock Option Portfolios and

Their Sensitivities to Price and Volatility. Journal of Accounting Research 40: 613-

630.

Cronqvist, H., A. K. Makhija, and S. E. Yonker. 2012. Behavioral Consistency in Corporate

Finance: CEO Personal and Corporate Leverage. Journal of Financial Economics

103: 20-40.

Dechow, P. M., and I. D. Dichev. 2002. The Quality of Accruals and Earnings: The Role of

Accrual Estimation Errors. Accounting Review 77: 35-59.

Dechow, P. M., R. G. Sloan, and A. P. Sweeney. 1996. Causes and Consequences of

Earnings Manipulation: An Analysis of Firms Subject to Enforcement Actions by the

SEC. Contemporary Accounting Research 13: 1-36.

Engel, E., R. M. Hayes, and X. Wang. 2010. Audit Committee Compensation and the

Demand for Monitoring of the Financial Reporting Process. Journal of Accounting

and Economics 49: 136-154.

Erickson, M., M. Hanlon, and E. L. Maydew. 2006. Is There a Link between Executive Equity

Incentives and Accounting Fraud? Journal of Accounting Research 44: 113-143.

Feng, M., W. Ge, S. Luo, and T. Shevlin. 2011. Why do CFOs Become Involved in Material

Accounting Manipulations? Journal of Accounting and Economics 51: 21-36.

Francis, J., R. LaFond, P. M. Olsson, and K. Schipper. 2004. Costs of Equity and Earnings

Attributes. Accounting Review 79: 967-1010.

Francis, J., D. Philbrick, and K. Schipper. 1994. Shareholder Litigation and Corporate

Disclosures. Journal of Accounting Research 32: 137-164.

Francis, J., R. LaFond, P. Olsson, and K. Schipper. 2005. The Market Pricing of Accruals

Quality. Journal of Accounting and Economics 39: 295-327.

Fried, J., and N. Shilon. 2011. Excess-Pay Clawbacks. Journal of Corporation Law 36: 721-

751.

Garvey, G. T., and T. T. Milbourn. 2006. Asymmetric Benchmarking in Compensation:

Executives Are Rewarded for Good Luck but Not Penalized for Bad. Journal of

Financial Economics 82: 197-225.

36

Gaspar, J.M., M. Massa, and P. Matos. 2005. Shareholder Investment Horizons and the

Market for Corporate Control. Journal of Financial Economics 76: 135-165.

Geiger, M., and K.Raghunandan. 2002. Auditor tenure and auditor reporting failures.

Auditing: A Journal of Practice and Theory 21: 67–78.

Ghosh, A., and D.Moon 2005. Auditor tenure and perceptions of audit quality. The

Accounting Review 80: 585–612.

Gompers, P., J. Ishii, and A. Metrick. 2003. Corporate Governance and Equity Prices.

Quarterly Journal of Economics 118: 107.

Goyal, V. K., and C. W. Park. 2002. Board Leadership Structure and CEO Turnover. Journal

of Corporate Finance 8: 49-66.

Gramling, A. A., J. W. Schatzberg, A. D. Bailey Jr, and Z. Hao. 1998. The Impact of Legal

Liability Regimes and Differential Client Risk on Client Acceptance, Audit Pricing, and

Audit Effort Decisions. Journal of Accounting, Auditing & Finance 13: 437-460.

Gray, P., P.S. Koh, and Y. H. Tong. 2009. Accruals Quality, Information Risk and Cost of

Capital: Evidence from Australia. Journal of Business Finance & Accounting 36: 51-

72.

Guay, W. R. 1999. The Sensitivity of CEO Wealth to Equity Risk: An Analysis of the

Magnitude and Determinants. Journal of Financial Economics 53: 43-71.

Gul, F. A., C. J. P. Chen, and J. S. L. Tsui. 2003. Discretionary Accounting Accruals,

Managers' Incentives, and Audit Fees. Contemporary Accounting Research 20: 441-

464.

Gul, A. F.A., B. Jaggi, and G. Krishnan. 2007. Auditor independence: evidence on the joint

effects of auditor tenure and nonaudit fees. Auditing: A Journal of Practice and Theory

26, 117–142.

Gul, F. A., and J. Goodwin. 2010. Short-Term Debt Maturity Structures, Credit Ratings, and

the Pricing of Audit Services. Accounting Review 85: 877-909.

Hay, D. C., W. R. Knechel, and N. Wong. 2006. Audit Fees: A Meta-analysis of the Effect of

Supply and Demand Attributes. Contemporary Accounting Research 23: 141-191.

Heninger, W. G. 2001. The Association between Auditor Litigation and Abnormal Accruals.

Accounting Review 76: 111-126.

Hilary, G., and C. Lennox. 2005. The Credibility of Self-Regulation: Evidence from the

Accounting Profession's Peer Review Program. Journal of Accounting and

Economics 40: 211-229.

Himmelberg, C. P., R. G. Hubbard, and D. Palia. 1999. Understanding the Determinants of

Managerial Ownership and Link Between Ownership and Performance. Journal of

Financial Economics 53: 353-384.

37

Hirschey, M., K. Smith, and W. Wilson. 2012. Financial Reporting Credibility After SOX”

Evidence from Earnings Restatements. AAA Annual Meeting proceedings.

Hirshleifer, D., D. Hirshleifer, A. V. Thakor, and A. V. Thakor. 1992. Managerial

Conservatism, Project Choice, and Debt. Review of Financial Studies 5: 437-470.

Hogan, C. E., and M. S. Wilkins. 2008. Evidence on the Audit Risk Model: Do Auditors

Increase Audit Fees in the Presence of Internal Control Deficiencies? Contemporary

Accounting Research 25: 219-242.

Holmström, B. 1999. Managerial Incentive Problems: A Dynamic Perspective. Review of

Economic Studies 66: 169-182.

Hribar, P., and N. T. Jenkins. 2004. The Effect of Accounting Restatements on Earnings

Revisions and the Estimated Cost of Capital. Review of Accounting Studies 9: 337-

356.

Huss, F. H., and F. A. Jacobs. 1991. Risk Containment: Exploring Auditor Decisions in the

Engagement Process. Auditing: A Journal of Practice and Theory 10: 16-32.

Iliev, P. 2010. The Effect of SOX Section 404: Costs, Earnings Quality, and Stock Prices.

Journal of Finance 65: 1163-1196.

Jayaraman, S., and T. T. Milbourn. 2012. The Role of Stock Liquidity in Executive

Compensation. The Accounting Review 87: 537-563.

Jensen, M. C., and K. J. Murphy. 1990. Performance Pay and Top-Management Incentives.

Journal of Political Economy 98: 225-264.

Jiang, J., K. R. Petroni, and I. Y. Wang. 2010. CFOs and CEOs: Who Have the Most

Influence on Earnings Management? Journal of Financial Economics 96: 513-526.

Johnstone, K. M. 2000. Client-Acceptance Decisions: Simultaneous Effects of Client

Business Risk, Audit Risk, Auditor Business Risk, and Risk Adaptation. Auditing: A

Journal of Practice and Theory 19: 1-25.

Johnstone, K. M., and J. C. Bédard. 2003. Risk Management in Client Acceptance

Decisions. Accounting Review 78: 1003-1025.

Karpoff, J. M., D. Scott Lee, and G. S. Martin. 2008. The Consequences to Managers for

Financial Misrepresentation. Journal of Financial Economics 88: 193-215.

Kim, I., and D. J. Skinner. 2012. Measuring Securities Litigation Risk. Journal of Accounting

and Economics 53: 290-310.

Klein, A. 2002. Audit Committee, Board of Director Characteristics, and Earnings

Management. Journal of Accounting & Economics 33: 375-400.

Klock, M. S., S. A. Mansi, and W. F. Maxwell. 2005. Does Corporate Governance Matter to

Bondholders? Journal of Financial and Quantitative Analysis 40: 693-719.

38

Knopf, J. D., J. Nam, and J. J. H. Thornton. 2002. The Volatility and Price Sensitivities of

Managerial Stock Option Portfolios and Corporate Hedging. Journal of Finance 57:

801-813.

Kravet, T., and T. Shevlin. 2010. Accounting Restatements and Information Risk. Review of

Accounting Studies 15: 264-294.

Larcker, D. F., and T. O. Rusticus. 2010. On the Use of Instrumental Variables in Accounting

Research. Journal of Accounting and Economics 49: 186-205.

Lewellen, K. 2006. Financing Decisions When Managers Are Risk Averse. Journal of

Financial Economics 82: 551-589.

Lobo, G. J., and J. Zhou. 2006. Did Conservatism in Financial Reporting Increase after the

Sarbanes-Oxley Act? Initial Evidence, Accounting Horizons 20: 57-73.

Low, A. 2009. Managerial Risk-Taking Behavior and Equity-Based Compensation. Journal of

Financial Economics 92: 470-490.

Lys, T., and R. L. Watts. 1994. Lawsuits against Auditors. Journal of Accounting Research

32: 65-93.

Malmendier, U., G. Tate, and J. O. N. Yan. 2011. Overconfidence and Early-Life

Experiences: The Effect of Managerial Traits on Corporate Financial Policies. Journal

of Finance 66: 1687-1733.

McNichols, M. F. 2002. Discussion of The Quality of Accruals and Earnings: The Role of

Accrual Estimation Errors. Accounting Review 77: 61-69.

Merton, R. C. 1973. Theory of Rational Option Pricing. Bell Journal of Economics &

Management Science 4: 141-183.

Milbourn, T. T. 2003. CEO Reputation and Stock-Based Compensation. Journal of Financial

Economics 68: 233-262.

Murphy, K. J., and T. Sandino. 2010. Executive Pay and “Independent” Compensation

Consultants. Journal of Accounting and Economics 49: 247-262.

Myers, J., L. Myers, and T. Omer. 2003. Exploring the term of the auditor–client relationship

and the quality of earnings: a case for mandatory auditor rotation? The Accounting

Review 78: 779–799.

Ortiz-Molina, H. 2006. Top Management Incentives and the Pricing of Corporate Public

Debt. Journal of Financial and Quantitative Analysis 41: 317-340.

Public Company Accounting Oversight Board (PCAOB). 2012. Proposed Auditing Standards

– Related Parties, Proposed Amendments to Certain PCAOB Auditing Standards

Regarding Significant Unusual Transactions and Other Proposed Amendments to

PCAOB Auditing Standards. PCAOB Release No – 2012-001, February 28, 2012.

39

Perry, T., and M. Zenner. 2000. CEO Compensation in the 1990s: Shareholder Alignment or

Shareholder Expropriation? Wake Forest Law Review 35: 123-162.

Pratt, J., and J. D. Stice. 1994. The Effects of Client Characteristics on Auditor Litigation

Risk Judgments, Required Audit Evidence, and Recommended Audit Fees.

Accounting Review 69: 639-656.

Prendergast, C., and L. Stole. 1996. Impetuous Youngsters and Jaded Old-Timers:

Acquiring a Reputation for Learning. Journal of Political Economy 104: 1105-1134.

Rajgopal, S., and M. Venkatachalam. 2011. Financial Reporting Quality and Idiosyncratic

Return Volatility. Journal of Accounting and Economics 51: 1-20.

Ramalingegowda, S., and Y. Yu. 2012. Institutional Ownership and Conservatism. Journal of

Accounting and Economics 53: 98-114.

Rego, S. O., and R. Wilson. 2012. Equity Risk Incentives and Corporate Tax

Aggressiveness. Journal of Accounting Research 50: 775-810.

Ross, S. A. 2004. Compensation, Incentives, and the Duality of Risk Aversion and

Riskiness. Journal of Finance 59: 207-225.