1p.g. kukreja associates. important amendment made in itr form –income tax rules for the...

TRANSCRIPT

P.G. KUKREJA ASSOCIATES 2

Important Amendment made in ITR Form –Income Tax Rules for the Assessment Year 2012-13

P.G. KUKREJA ASSOCIATES 3

(1) These rules may be called the Income-tax (3rd Amendment) Rules, 2012. (2) They shall come into force on the 1st day of April, 2012

P.G. KUKREJA ASSOCIATES 4

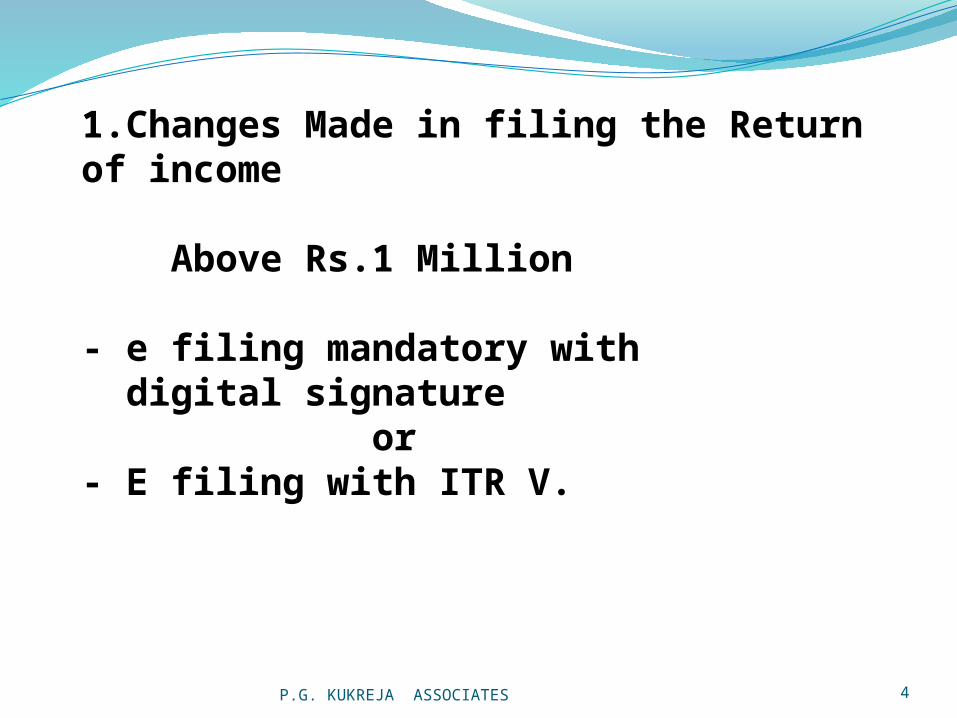

1.Changes Made in filing the Return of income

Above Rs.1 Million

- e filing mandatory with digital signature or - E filing with ITR V.

P.G. KUKREJA ASSOCIATES 5

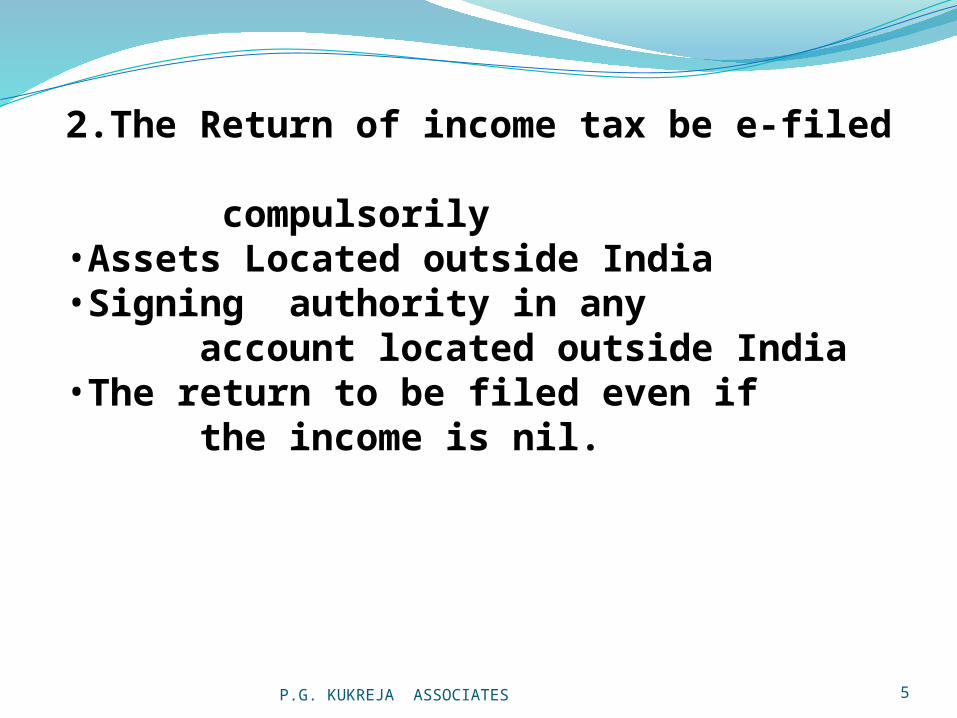

2.The Return of income tax be e-filed compulsorily •Assets Located outside India•Signing authority in any account located outside India•The return to be filed even if the income is nil.

P.G. KUKREJA ASSOCIATES 6

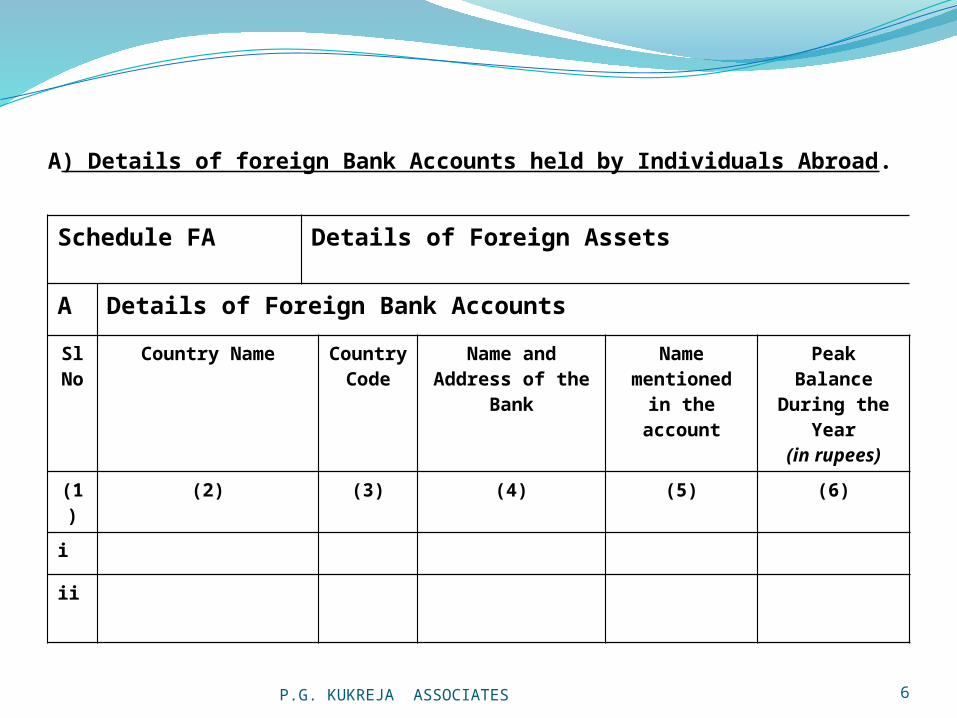

Schedule FA Details of Foreign Assets

A Details of Foreign Bank Accounts

SlNo

Country Name Country Code

Name and Address of the

Bank

Name mentioned

in theaccount

Peak Balance

During the Year

(in rupees)

(1)

(2) (3) (4) (5) (6)

i

ii

A) Details of foreign Bank Accounts held by Individuals Abroad.

P.G. KUKREJA ASSOCIATES 7

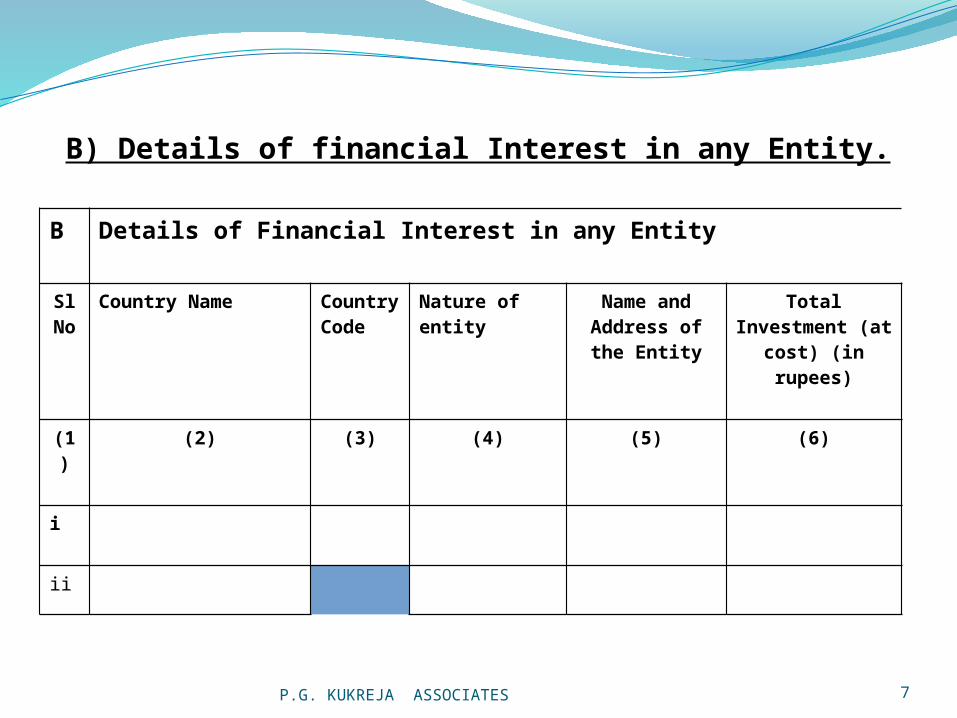

B Details of Financial Interest in any Entity

SlNo

Country Name Country Code

Nature of entity

Name and Address of the Entity

Total Investment (at

cost) (in rupees)

(1)

(2) (3) (4) (5) (6)

i

ii

B) Details of financial Interest in any Entity.

P.G. KUKREJA ASSOCIATES 8

C Details of Immovable Property

SlNo(1)

Country Name

(2)

Country Code

(3)

Address of the Property

(4)

Total Investment (at cost) (in

rupees)(5)

(i)

(ii)

C)Details of Immovable Property of any individual at abroad

P.G. KUKREJA ASSOCIATES 9

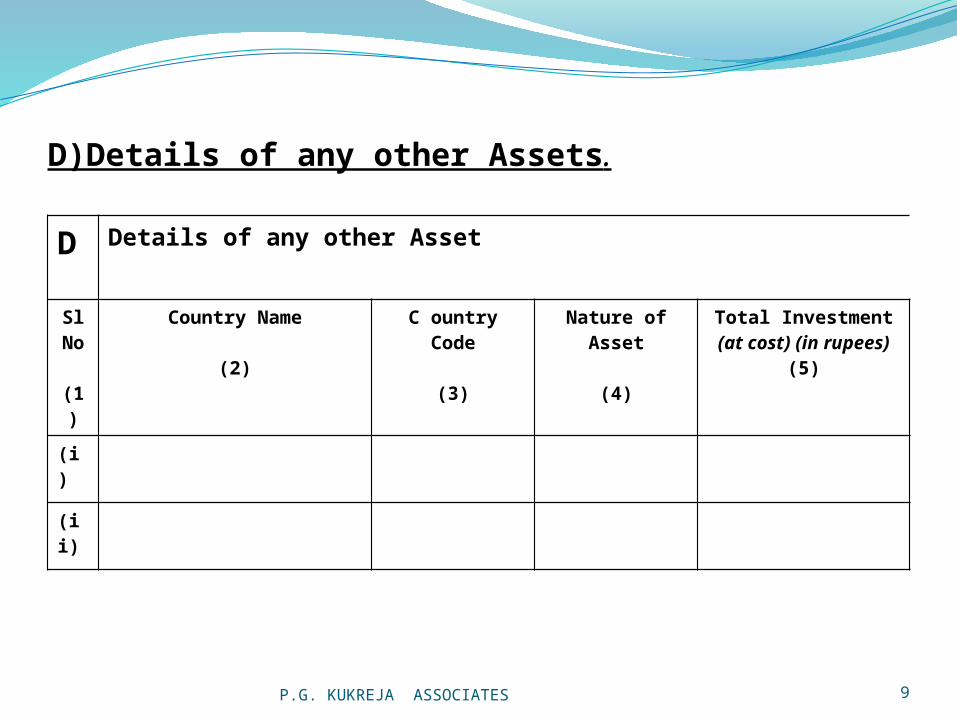

D Details of any other Asset

SlNo (1)

Country Name

(2)

C ountry Code

(3)

Nature of Asset

(4)

Total Investment (at cost) (in rupees)

(5)

(i)

(ii)

D)Details of any other Assets.

P.G. KUKREJA ASSOCIATES 10

E Details of account(s) in which you have signing authority and which has not been included in A to D above.

SlNo(1)

Name of the Institution in which the

account is held(2)

Address of the Institution

(3)

Name mentioned in the

account(4)

Peak Balance/Investment during the

year (in rupees)(5)

(i)

(ii)

E)Details of accounts in which one have signing authority and which has not been included in A and D above.

P.G. KUKREJA ASSOCIATES 11

New Filing Requirements for Foreign Assets SIMILAR UNDER US LAWS

The Foreign Account Tax Compliance Act (FATCA)Individuals with a Reporting Obligation under

FATCA .Employee Benefits Required to be Reported as

Foreign Financial Assets on Form 8938.

P.G. KUKREJA ASSOCIATES 12

Other Amendment in form ITR 2

Addition of Schedule TR – TAX RELIEF

tax relief claimed under sections 90/90A/91

P.G. KUKREJA ASSOCIATES 13

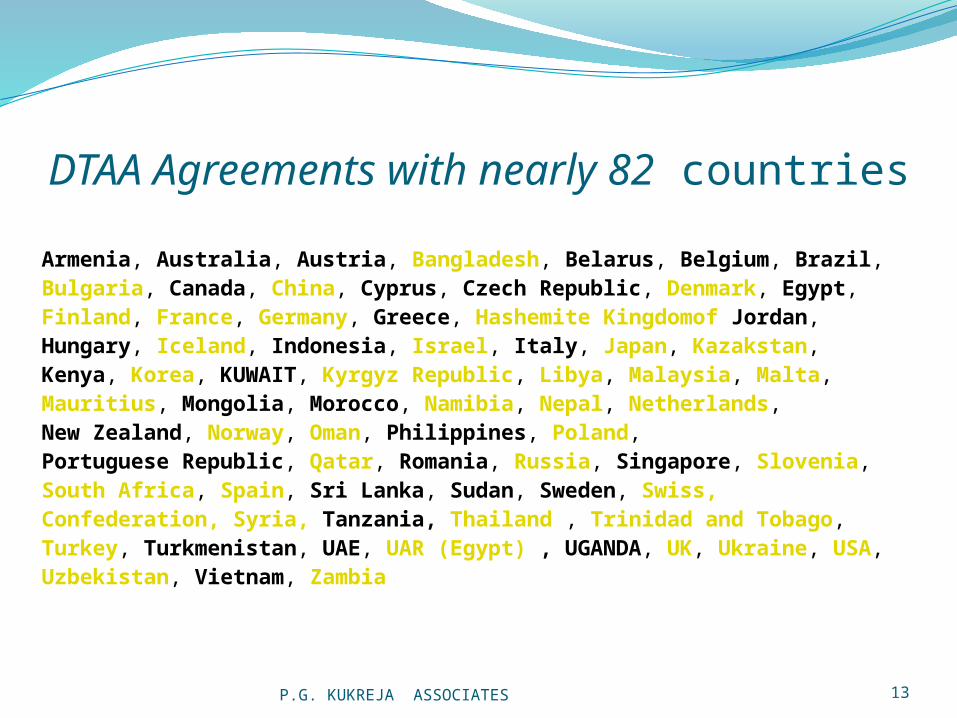

DTAA Agreements with nearly 82 countries

Armenia, Australia, Austria, Bangladesh, Belarus, Belgium, Brazil, Bulgaria, Canada, China, Cyprus, Czech Republic, Denmark, Egypt,Finland, France, Germany, Greece, Hashemite Kingdomof Jordan, Hungary, Iceland, Indonesia, Israel, Italy, Japan, Kazakstan, Kenya, Korea, KUWAIT, Kyrgyz Republic, Libya, Malaysia, Malta, Mauritius, Mongolia, Morocco, Namibia, Nepal, Netherlands, New Zealand, Norway, Oman, Philippines, Poland, Portuguese Republic, Qatar, Romania, Russia, Singapore, Slovenia, South Africa, Spain, Sri Lanka, Sudan, Sweden, Swiss, Confederation, Syria, Tanzania, Thailand , Trinidad and Tobago, Turkey, Turkmenistan, UAE, UAR (Egypt) , UGANDA, UK, Ukraine, USA, Uzbekistan, Vietnam, Zambia

P.G. KUKREJA ASSOCIATES 14

Section 206AA.

Tax shall be deducted at higher of the following rates :-

•At the rate specified in the relevant

provisions of this Act; or

•At the rates in force (as per treaty); or

•At the rate of 20 %.

P.G. KUKREJA ASSOCIATES 15

Addition of Schedule 80 G

Capital Gain (Para B-TI) :-

Schedule HP – House Property

Schedule UD :- Unabsorbed Depreciation :-

P.G. KUKREJA ASSOCIATES 16

AMENDMENTS RELATING TO REASSESSMENT IN

S. 147

P.G. KUKREJA ASSOCIATES 17

THE TERM FINANCIAL INTEREST

P.G. KUKREJA ASSOCIATES 18

SECTION 9(1)(i) Explanation 5

P.G. KUKREJA ASSOCIATES 19

Amendment to Section 149

P.G. KUKREJA ASSOCIATES 20

Amendment toSection 149(3)

P.G. KUKREJA ASSOCIATES 21

Sr No. Form No. Description / Summary

1 ITR - 1 (SAHAJ)*

Individual having income classified as: 1. Salaries 2. House Property (where the individual does not own more than one house property 3. Income from Other Sources (except winnings from lottery or income from race horses)

Summary of ITR -Forms

P.G. KUKREJA ASSOCIATES 22

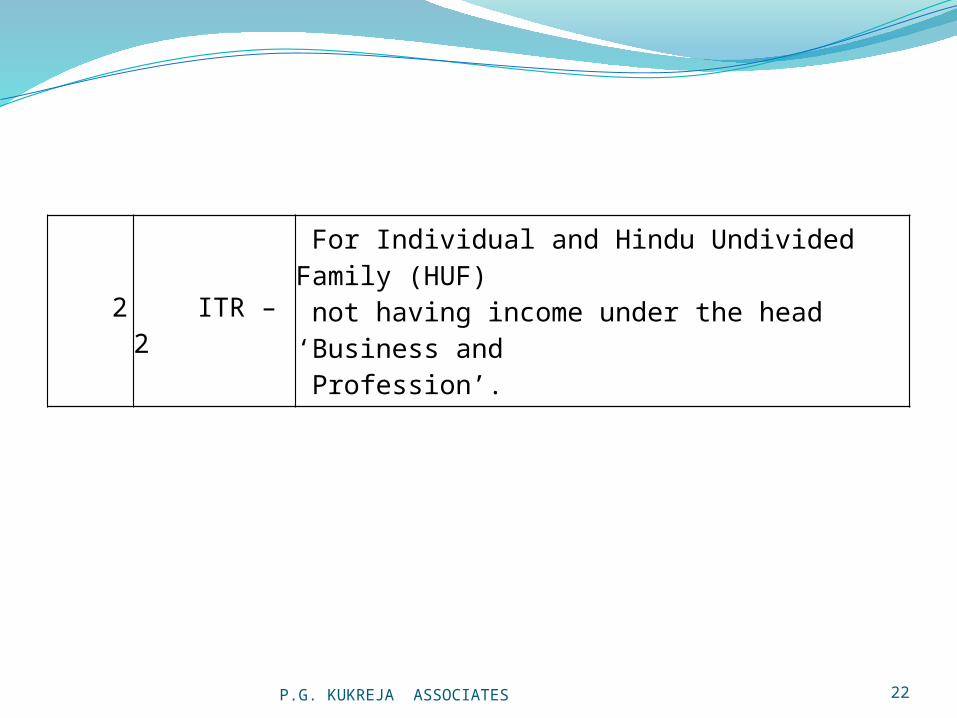

2

ITR – 2 For Individual and Hindu Undivided Family (HUF)

not having income under the head ‘Business and Profession’.

P.G. KUKREJA ASSOCIATES 23

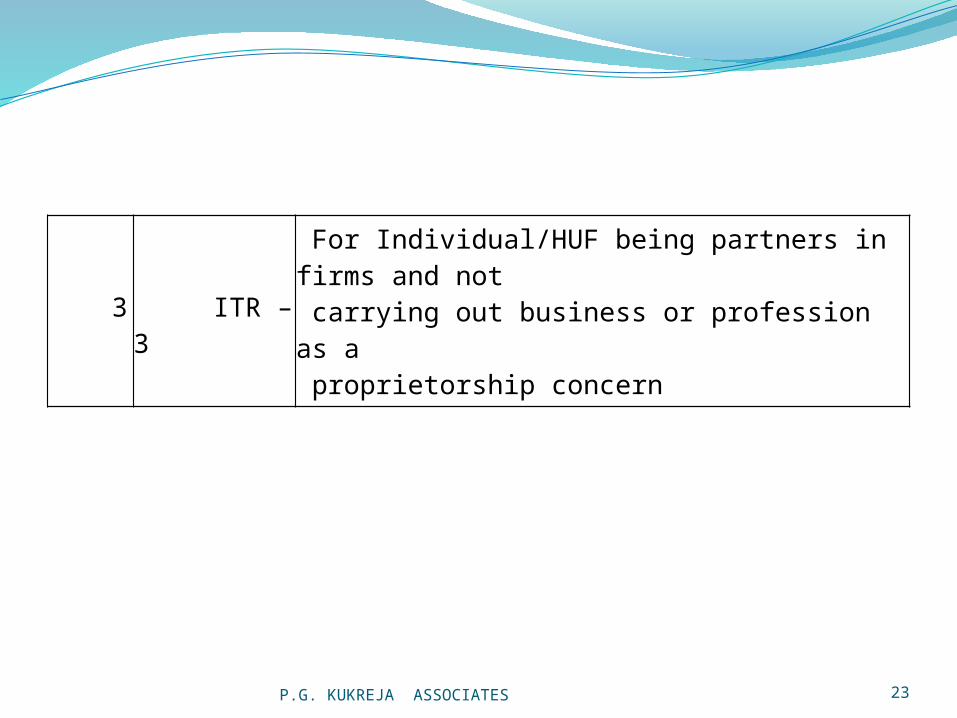

3

ITR – 3 For Individual/HUF being partners in firms and not

carrying out business or profession as a proprietorship concern

P.G. KUKREJA ASSOCIATES 24

4 ITR – 4S (SUGAM)*

For Individual/HUF deriving income under the head ‘Business and Profession’ and having opted for being taxed under sections 44AD and 44AE (presumptive basis of taxation)

P.G. KUKREJA ASSOCIATES 25

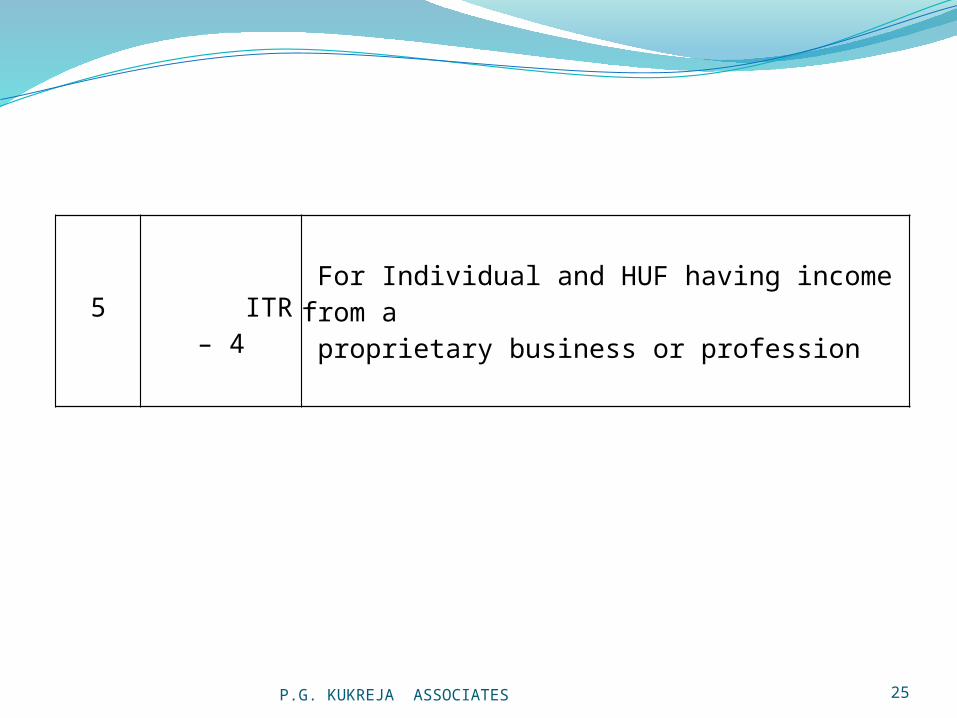

5

ITR – 4 For Individual and HUF having income from a proprietary business or profession

P.G. KUKREJA ASSOCIATES 26

Individual and HUF assessees, who are residents and have assets (including financial interest in any entity) located outside India or signing authority in any account located outside India, cannot use the Forms ITR-1 (SAHAJ) or ITR – 4S (SUGAM), as the case may be.

Form 1S and 4S not to be used

P.G. KUKREJA ASSOCIATES 27

Clarity on GAAR to attract long-term money

P.G. KUKREJA ASSOCIATES 28

Received on 07.05.2012Proposed changes in Finance Bill, 20121) Withdrawal of TDS on purchase of Immovable Property2) Retrospective amendment to Sec. 9 not applicable

where assessment order already passed3) GAAR : Provisions postponed, now effective from 01-04-

20144) GAAR : Provisions as to onus of proof shifted to revenue5) GAAR : Advance Ruling applicable to GAAR cases6) GAAR : Constitution of approving panel changed7) STT on sale of unlisted securities at 0.2%8) No excise duty on purchase of jewellery upto Rs. 5 lakhs

P.G. KUKREJA ASSOCIATES 29

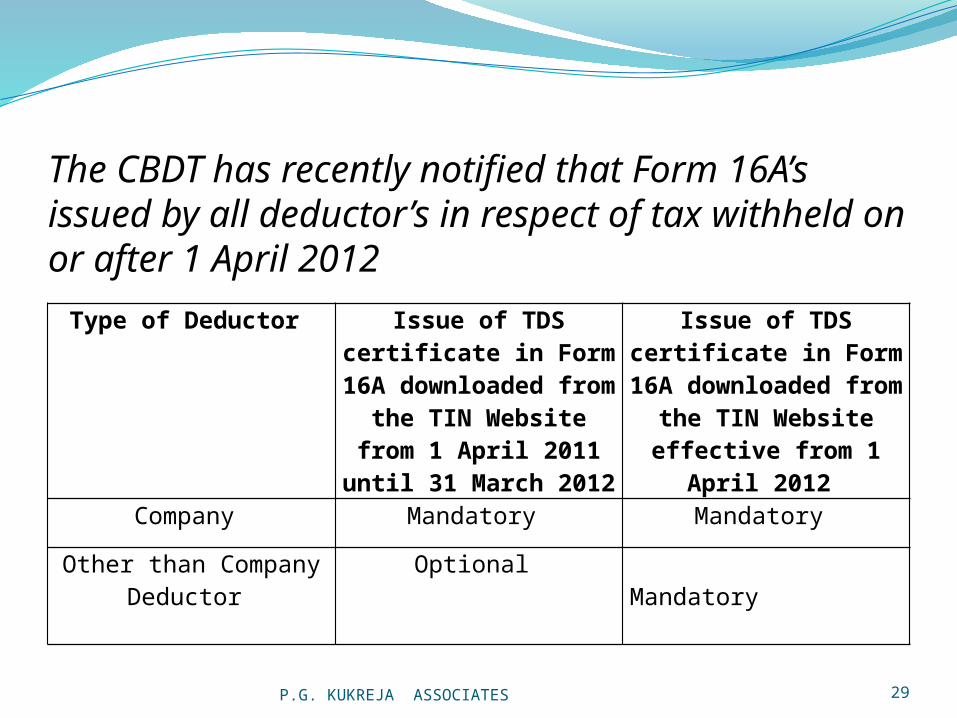

The CBDT has recently notified that Form 16A’s issued by all deductor’s in respect of tax withheld on or after 1 April 2012

Type of Deductor Issue of TDS certificate in Form 16A

downloaded from the TIN Website from 1 April 2011 until 31

March 2012

Issue of TDS certificate in Form 16A

downloaded from the TIN Website effective

from 1 April 2012

Company Mandatory Mandatory

Other than Company Deductor

Optional Mandatory

P.G. KUKREJA ASSOCIATES 30

P.G. KUKREJA ASSOCIATES 31

Thank youP. G. Kukreja AssociatesChartered Accountants3, Shewa Apartments, 33-B 3rd Road, Khar (W),Mumbai – 400 [email protected]