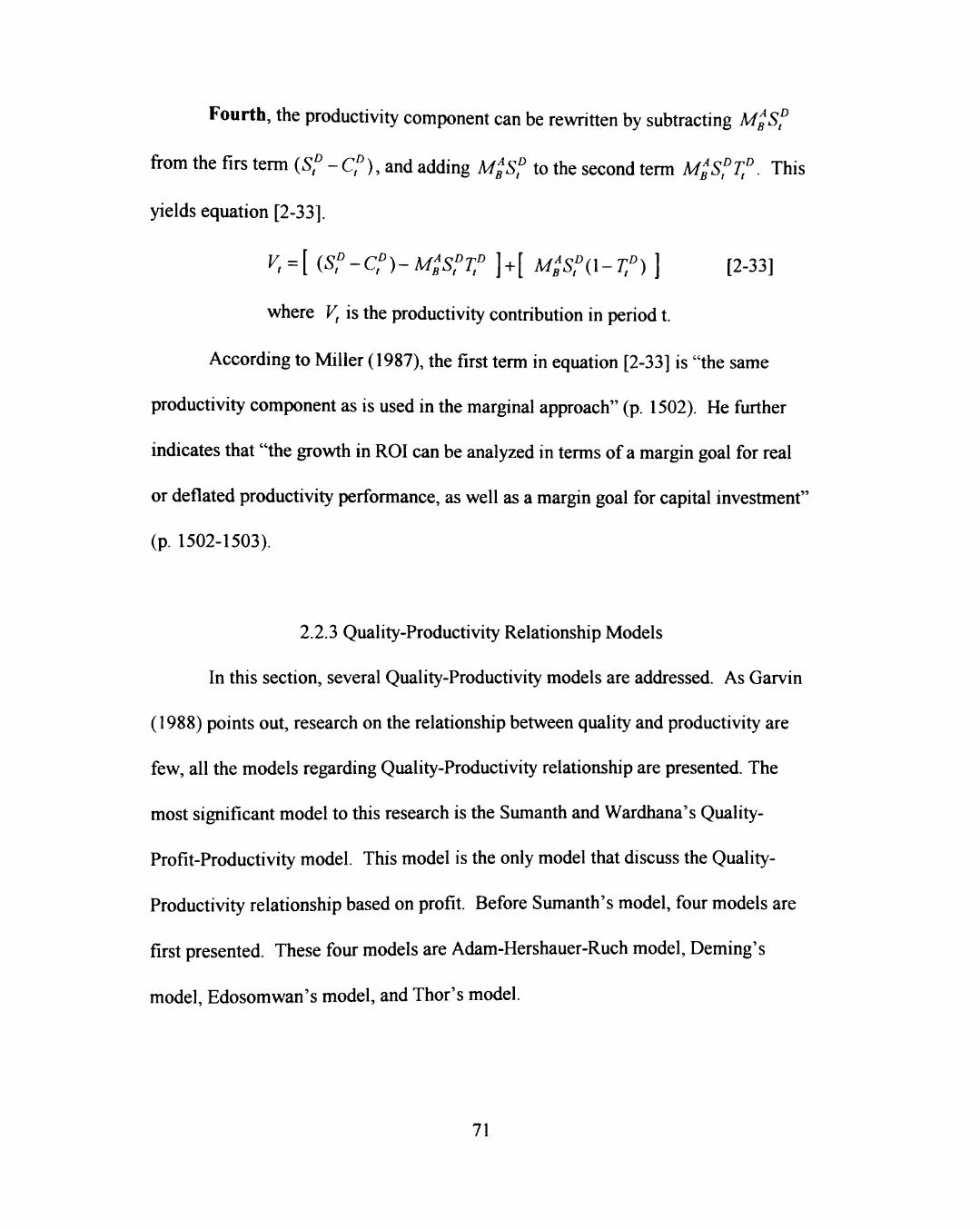

a study on the profit-based quality-productivity

TRANSCRIPT

A STUDY ON THE PROFIT-BASED QUALITY-PRODUCTIVITY

RELATIONSHIP MODEL AND ITS VERIFICATION

IN MANUFACTURING INDUSTRIES

by

WEN-RUEY LEE, B.E., M.S.E.

A DISSERTATION

IN

INDUSTRIAL ENGINEERING

Submitted to the Graduate Faculty of Texas Tech University in

Partial Fulfillment of the Requirements for

the Degree of

DOCTOR OF PHILOSOPHY

Approved

Accepted

May, 1997

ACKNOWLEDGMENTS AKS-B^I

l\oy ly ^ I would like to express my sincere gratitude to Drs. Mario G. Beruvides,

James L. Smith, Jerry D. Ramsey, Hong-Chao Zhang, and Paul H. Randolph for

serving on my dissertation committee and for the guidance they have given me. I also

sincerely thank Dr. William J. Conover for his sage counsel and provision of related

software to this work.

I am especially indebted to my advisor. Dr. Mario G. Beruvides, for his

valuable suggestions, and patient guidance throughout my Ph.D. study. To me. Dr.

Beruvides is not only an excellent advisor but also a dear friend. Without his help, I

would not be who I am now.

Many others have contributed to this work throughout the years. Their

support is gratefully acknowledged. Especially, I would like to thank Mr. Chien K.

Lin, Mr. Yi T. Lin, Mr. Chin Y. Wu, Mr. Min H. Liao, Mr. Ming T. Chen, and Mr.

Meng C. Lin who assisted this research with great zeal in the data collection in the

field study.

I am grateful to my loving wife, Huei-Jen Homg, who gave me full support

during the days of studying at Texas Tech University. Finally, I would like to

dedicate this work to my father in commemoration of his passing away after my

dissertation defense.

11

TABLE OF CONTENTS

ACKNOWLEDGMENTS ii

LIST OF TABLES xii

LIST OF FIGURES xiv

CHAPTER

I. INTRODUCTION 1

1.1 Research Problem Statement 4

1.2 Scope of This Research 5

1.2.1 Research Question 6

1.2.2 Research Purpose 6

1.2.3 Research Objective 7

1.2.4 General Hypotheses 7

1.3 Limitations and Assumptions 8

1.3.1 Limitations 8

1.3.2 Assumptions 9

1.4 Relevance 9

1.4.1 Need for This Research 10

1.4.1.1 Theoretical Research Needs 10

1.4.1.2 Practical Research Needs 11

1.4.2 Benefits of This Research 11 1.5 Expected Results 12

111

2. LITERATURE REVIEW 13

2.1 Background 13

2.1.1 History 13

2.1.1.1 History of Quality 14

2.1.1.2 History of Productivity 16

2.1.1.3 Review of the Relationship between Quality and Profit 19

2.1.1.4 Review of the Relationship between Productivity and Profit 25

2.1.1.5 Review of the Relationship between Quality and Productivity 29

2.1.2 Definitions 36

2.1.2.1 Definitions of Productivity 37

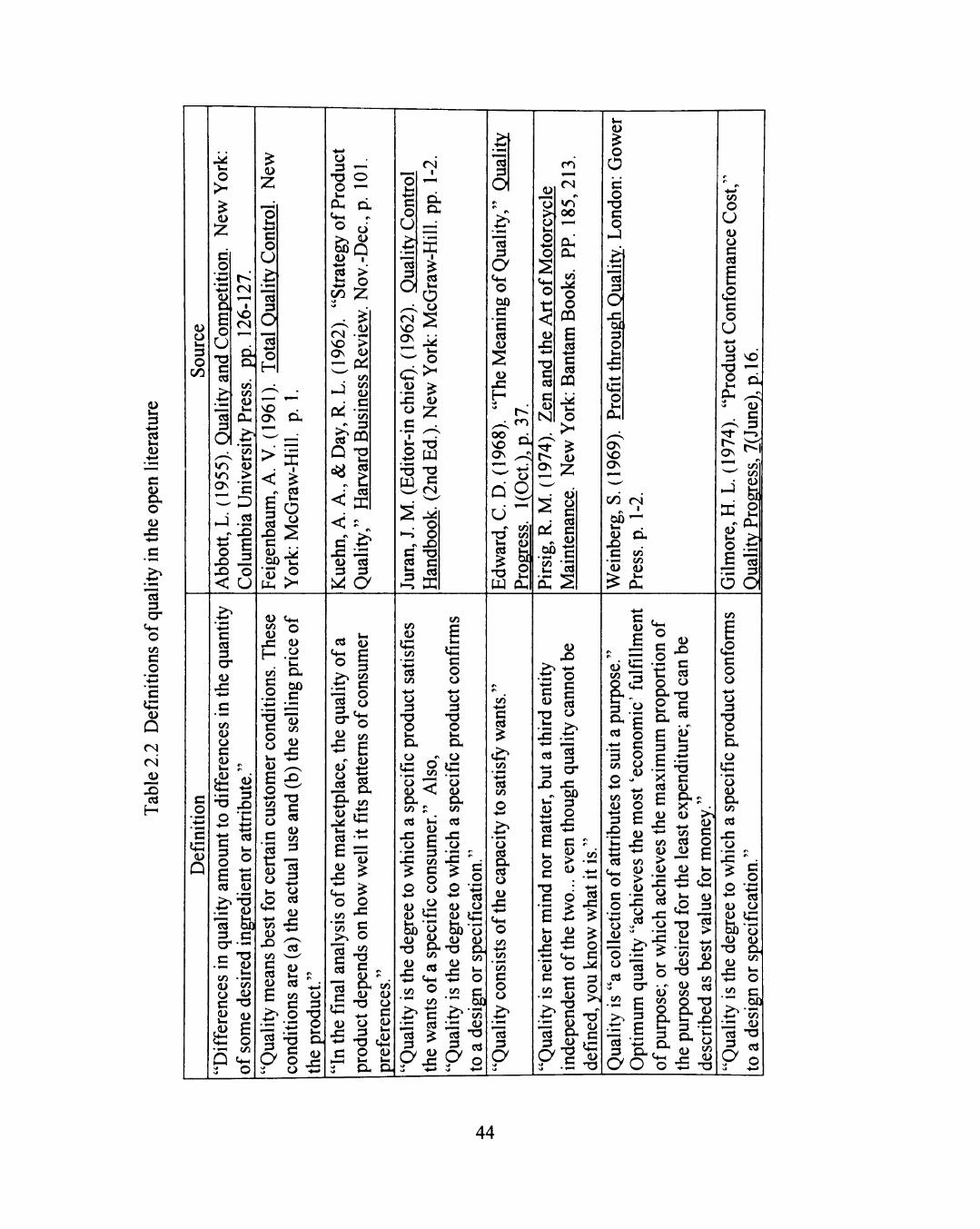

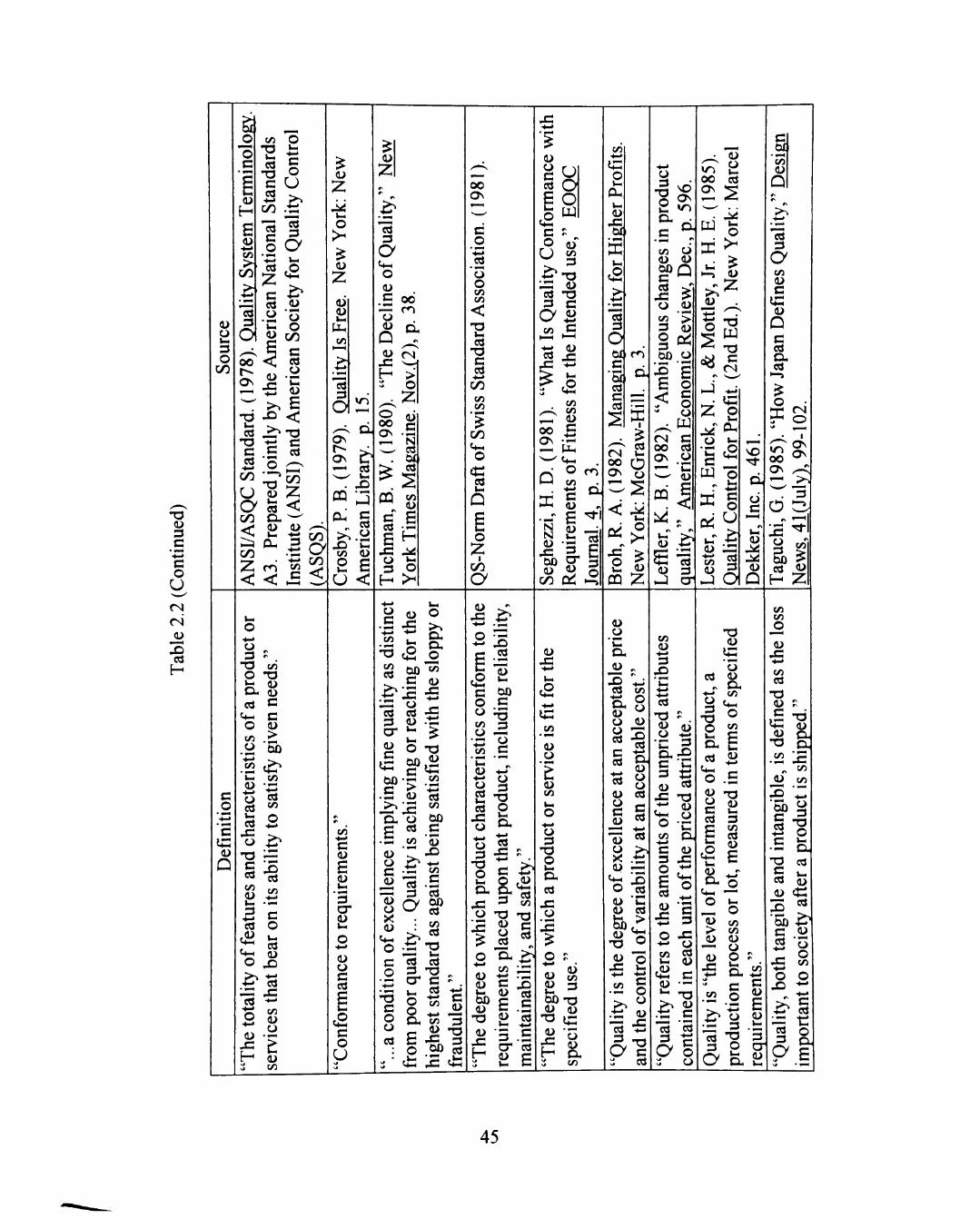

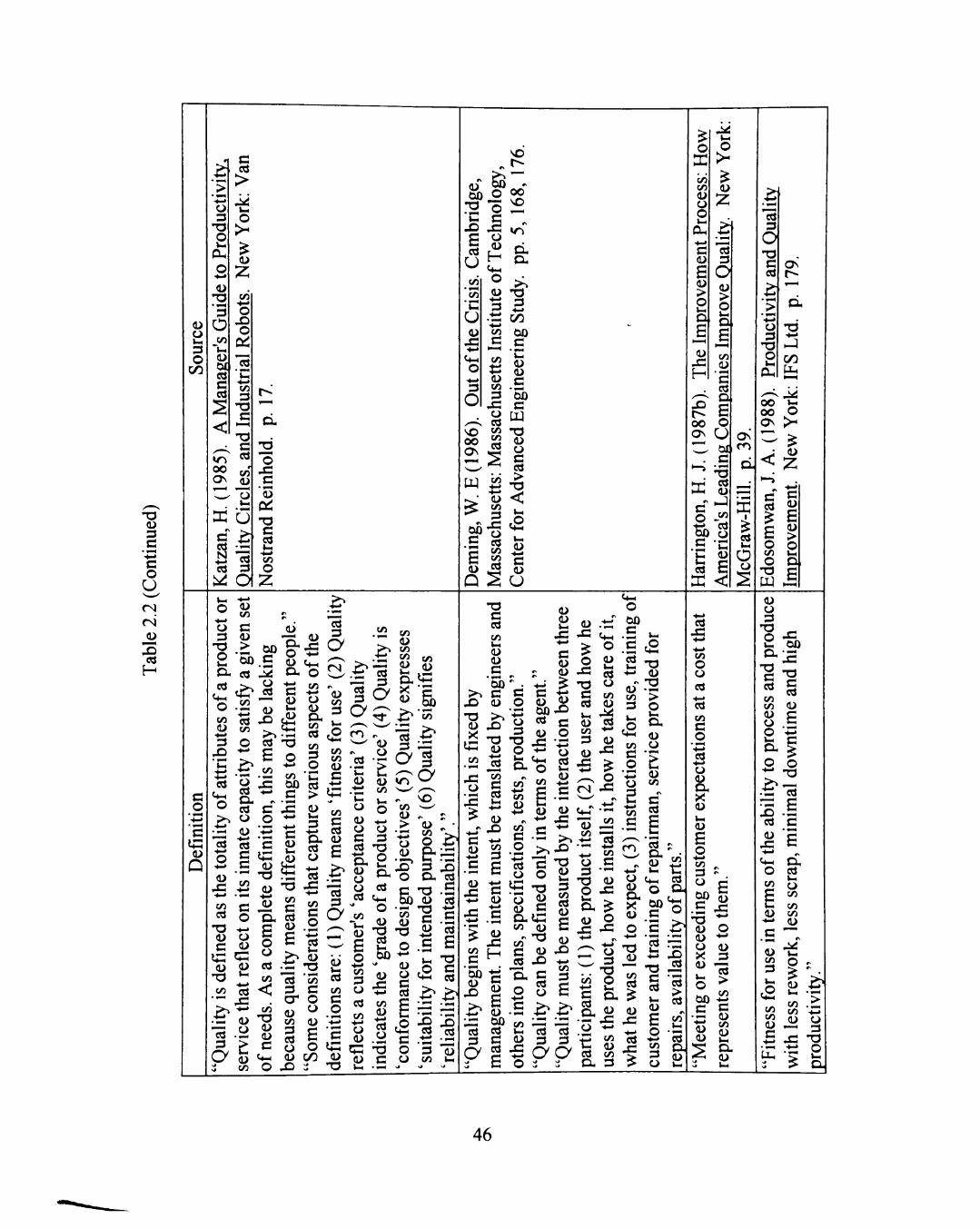

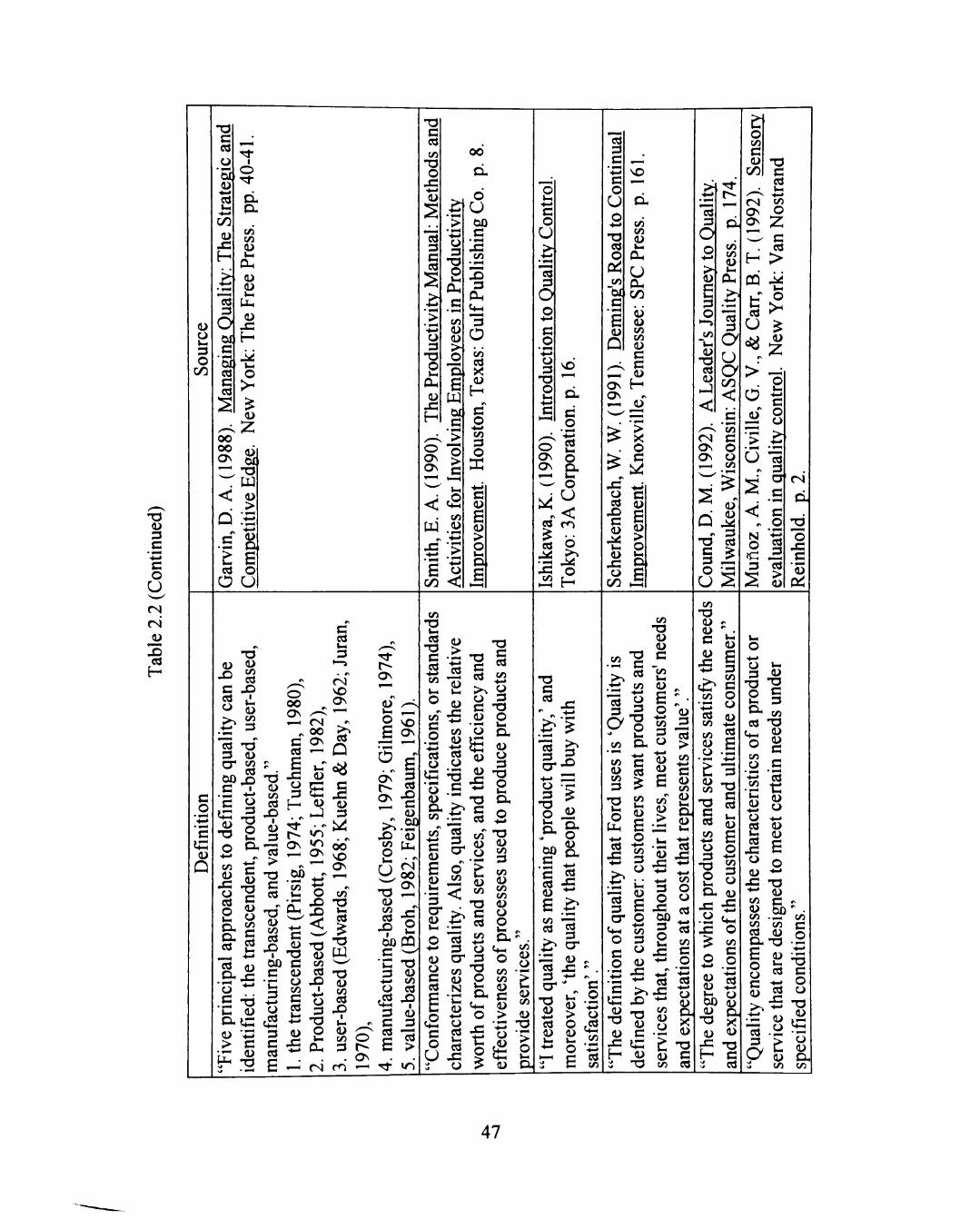

2.1.2.2 Definitions of Quality 43

2.1.2.3 Definitions of Profitability and Profit 49

2.2 Current Profit-Based Quality, Productivity Models 53

2.2.1 Quality-Cost Model 53

2.2.1.1 Optimum Quality Cost Model 54

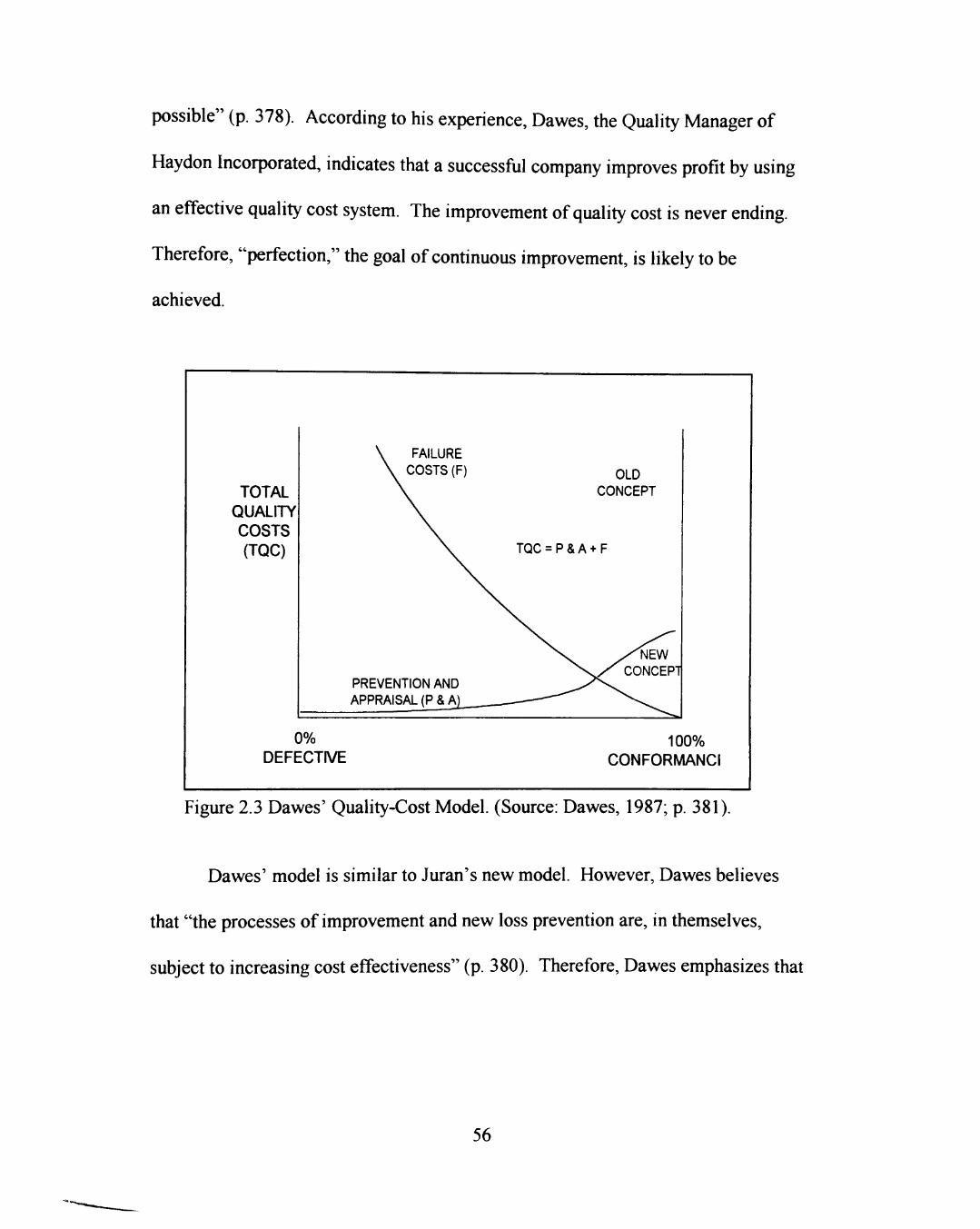

2.2.1.2 Dawes' Quality Cost Model 55

2.2.1.3 Poor-Quality Cost (PQC) Model 57

2.2.1.4 Taguchi's Quality Loss Function Model 59

2.2.2 Productivity-Profit Model 60

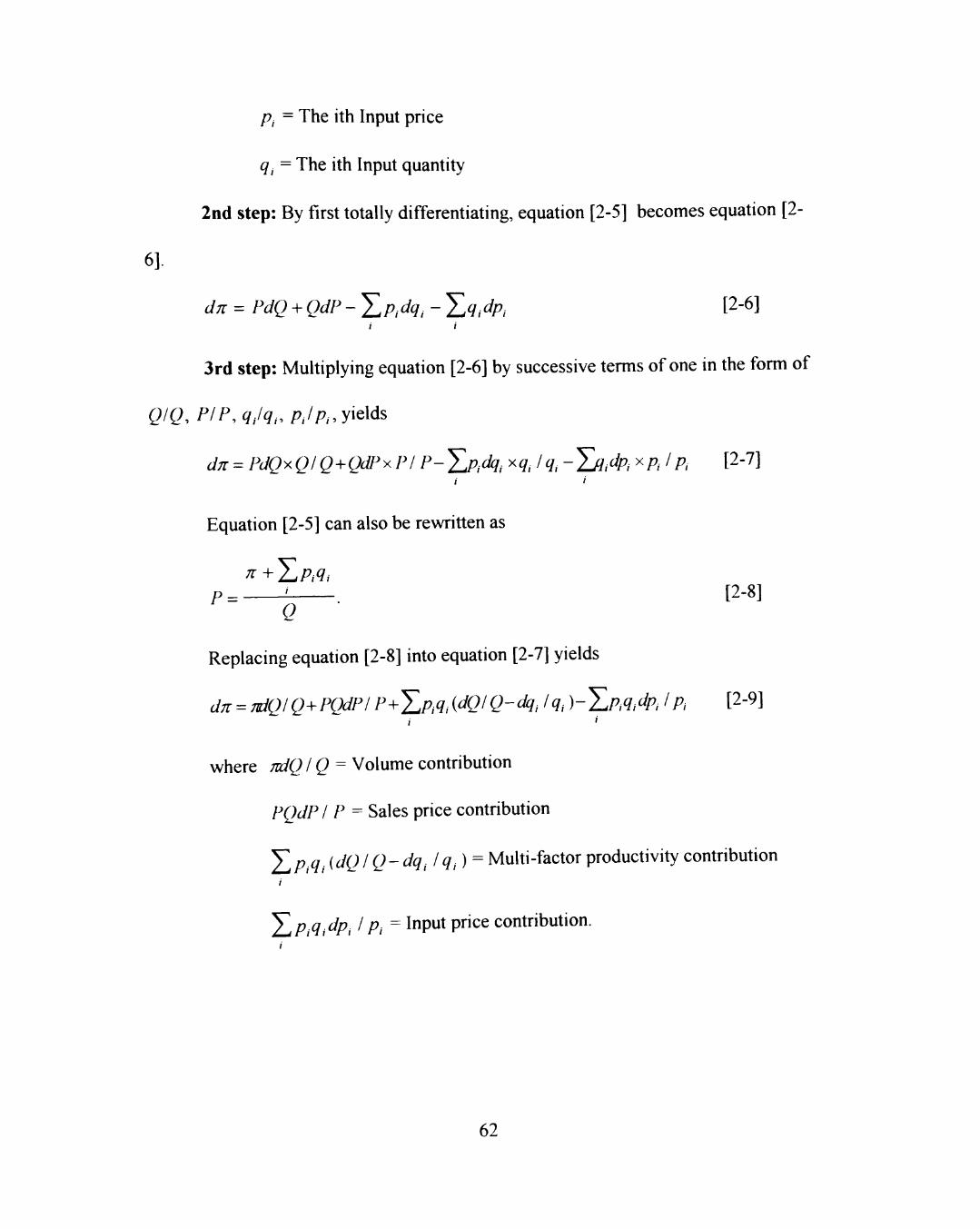

2.2.2.1 Adam-Hershauer-Ruch's Productivity-Profit Relationship Model 60

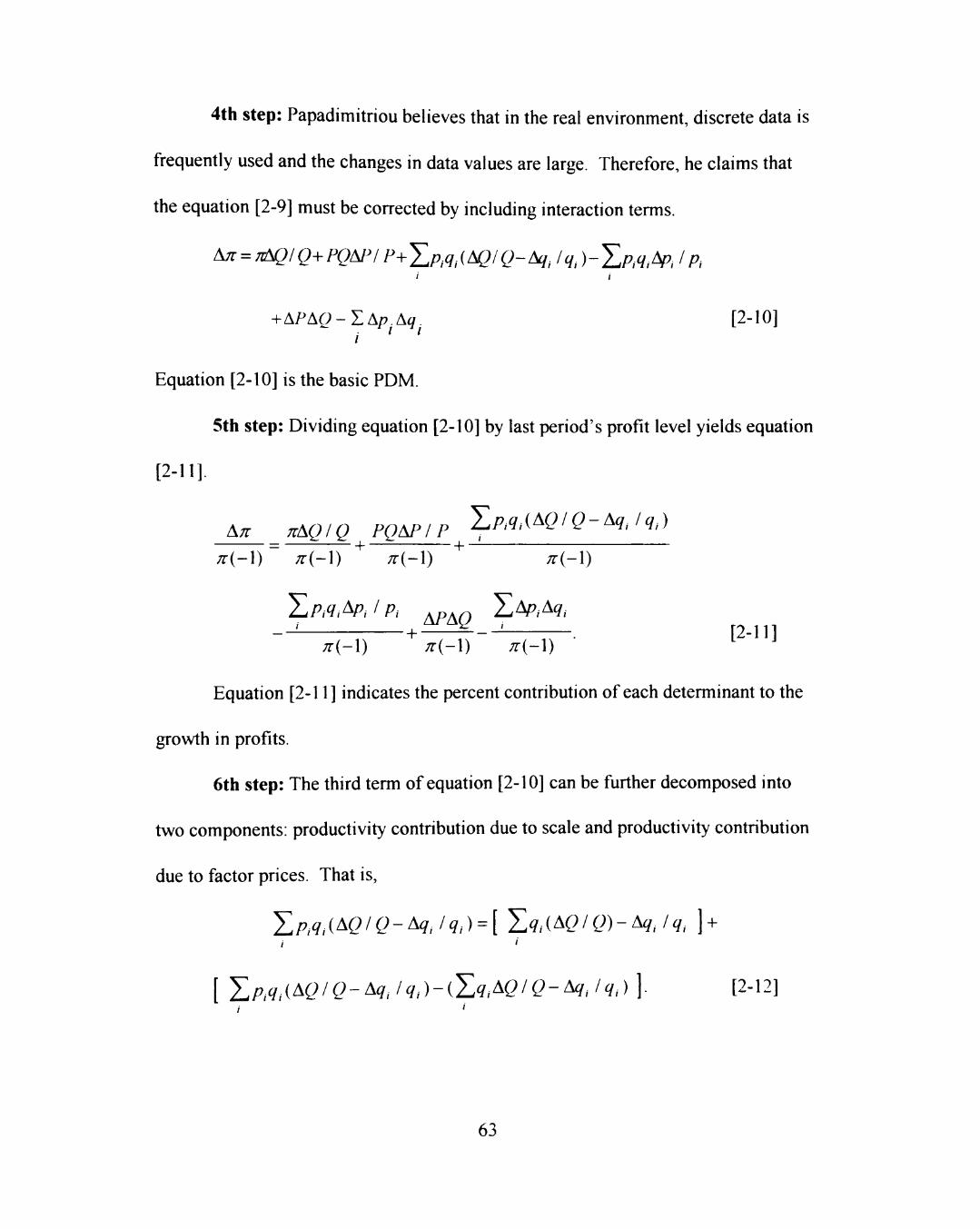

2.2.2.2 Papadimitriou's Profit Decomposition Model (PDM) 61

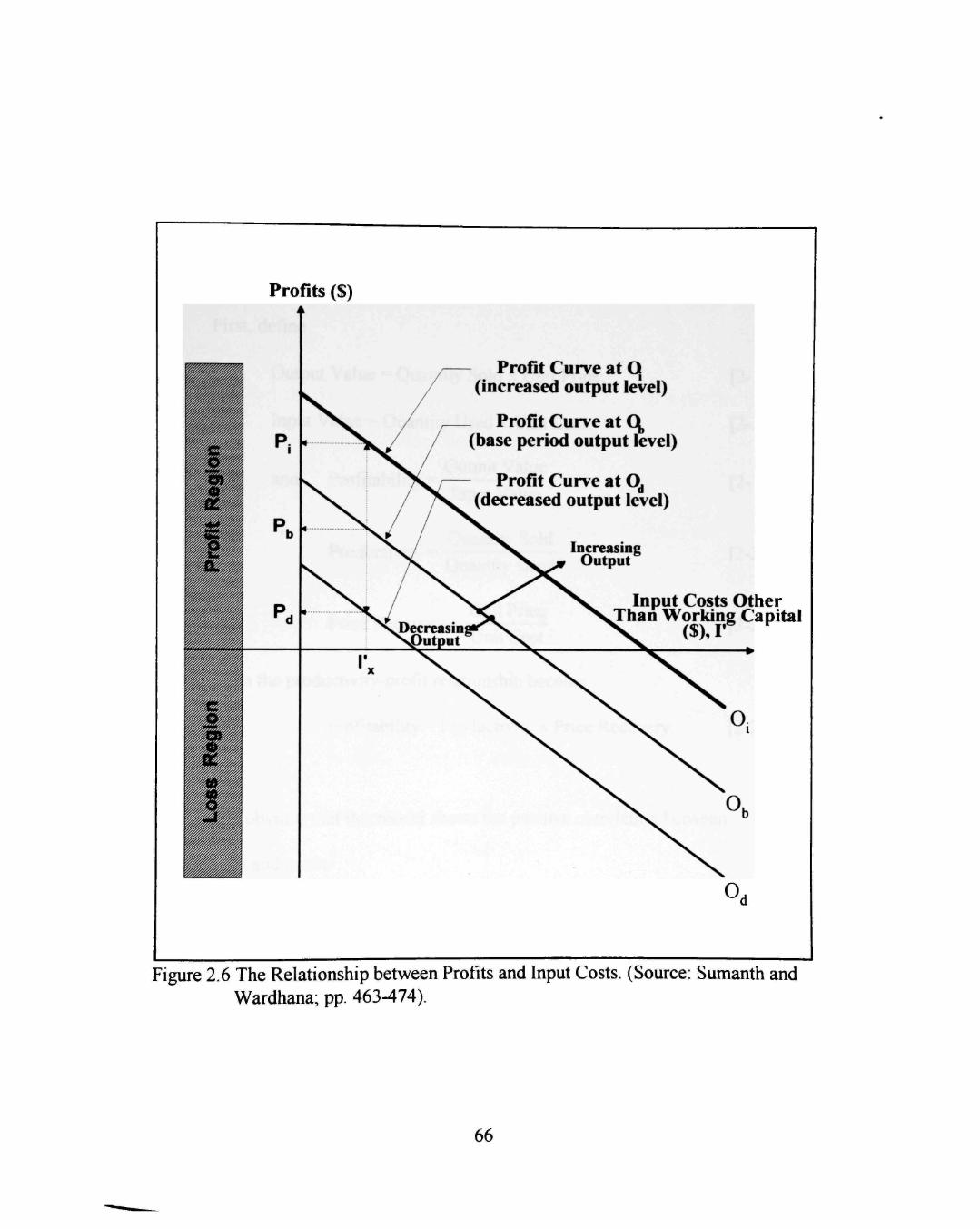

2.2.2.3 Sumanth's Productivity-Profit Relationship Model 64

iv

2.2.2.4 APC's Productivity-Profit Relationship Model 67

2.2.2.5 Miller's Productivity-Profit Relationship Model 67

2.2.2.6 Miller's Productivity-ROI Relationship Model 69

2.2.3 Quality-Productivity Relationship Models 71

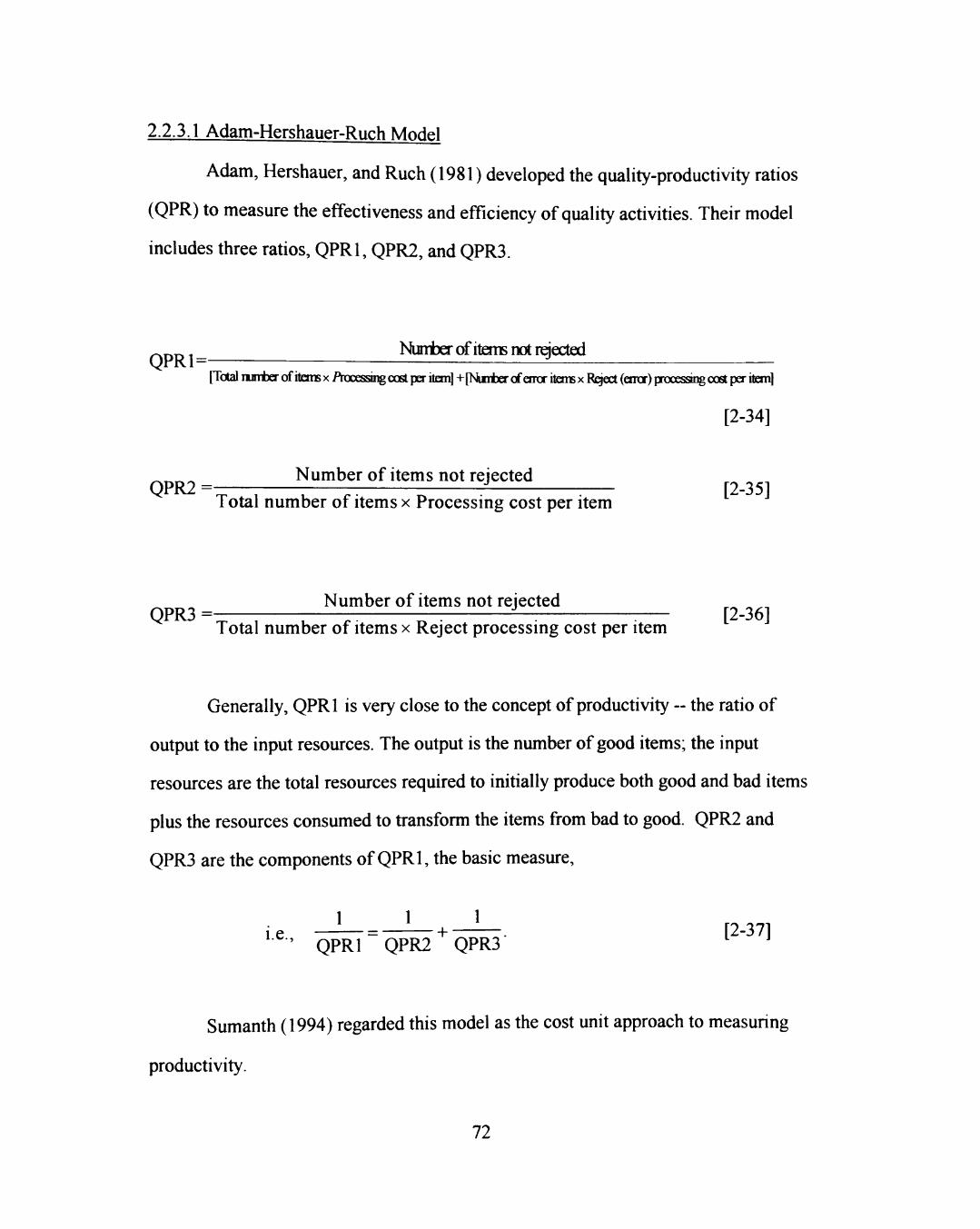

2.2.3.1 Adam-Hershauer-Ruch Model 72

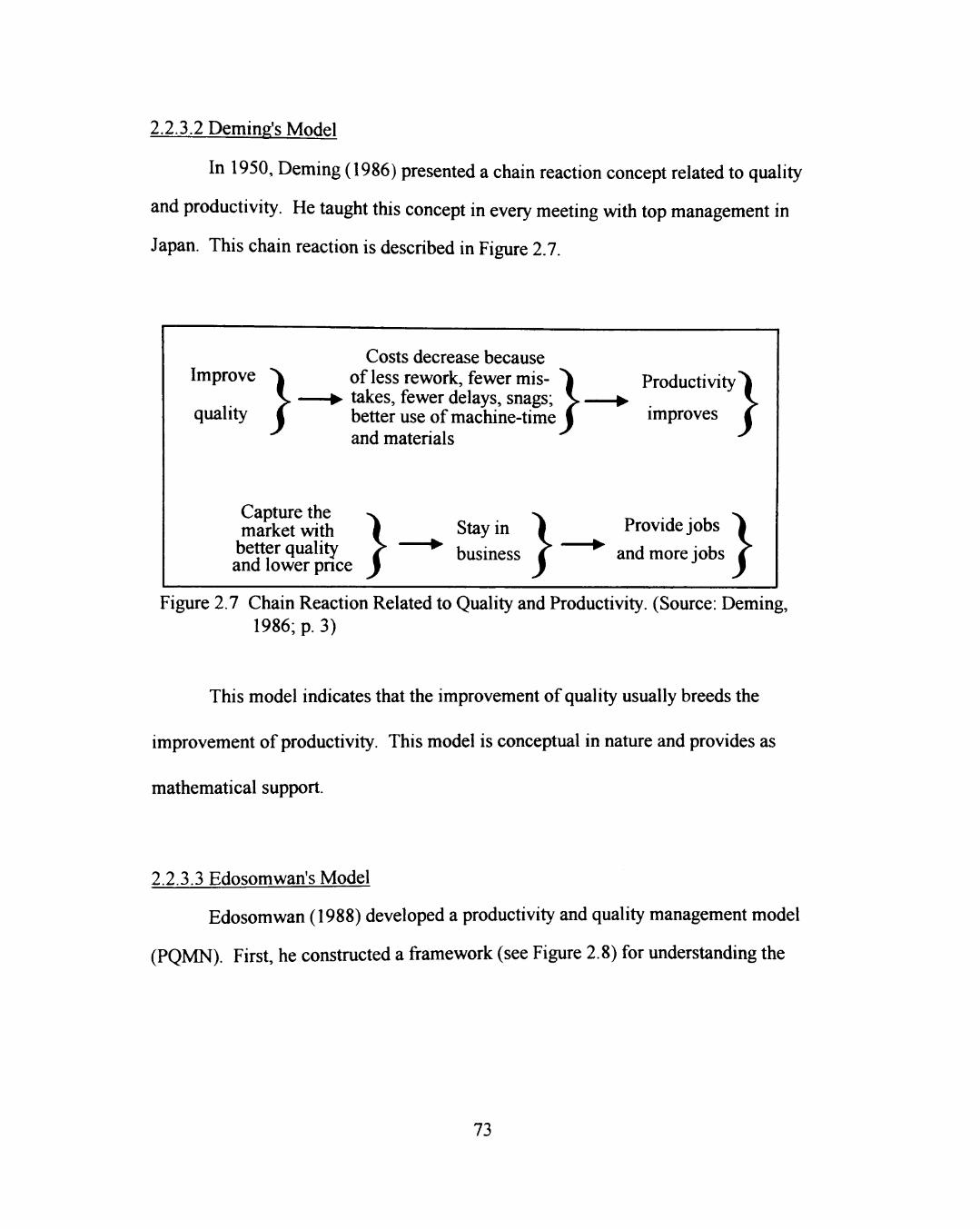

2.2.3.2 Deming's Model 73

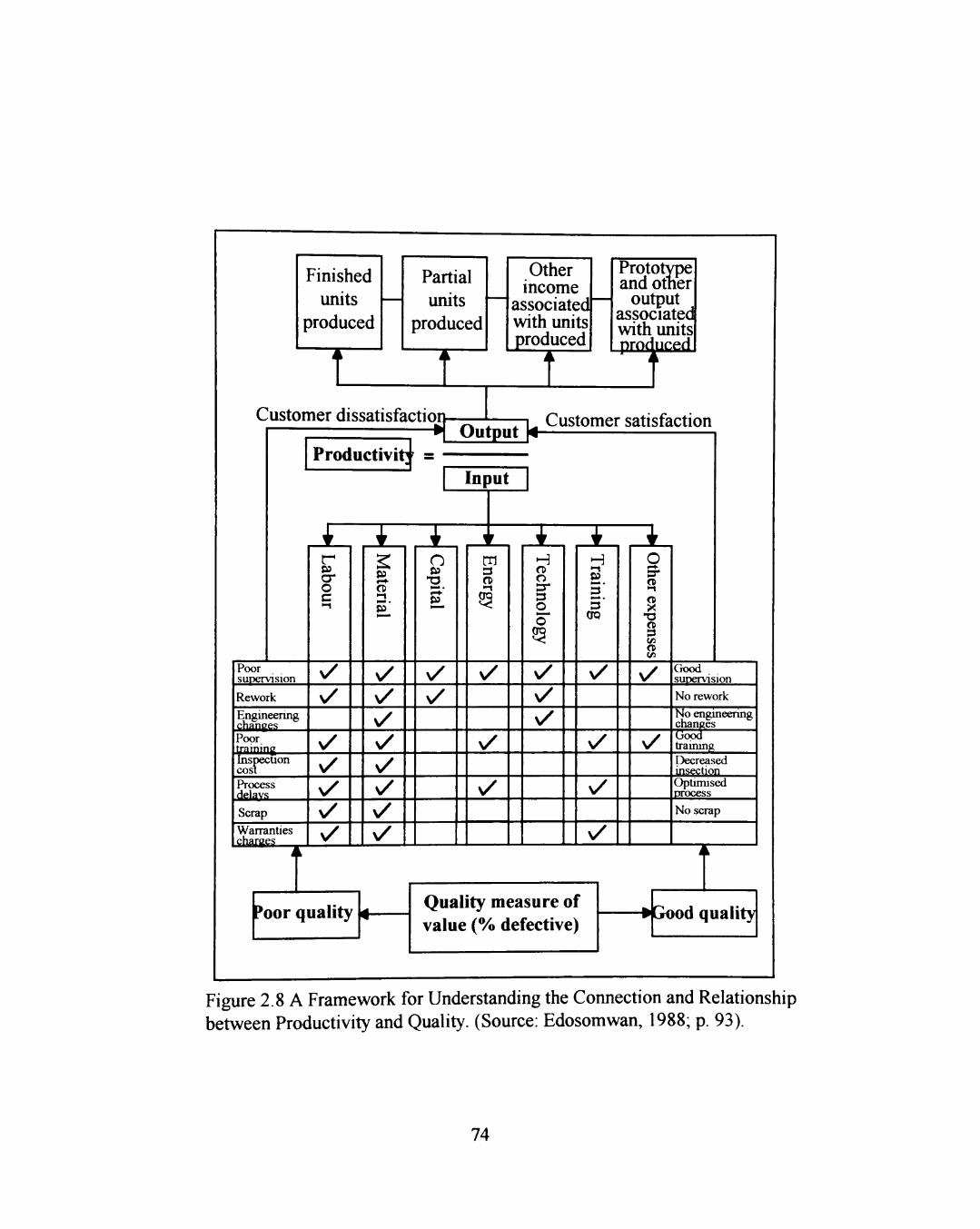

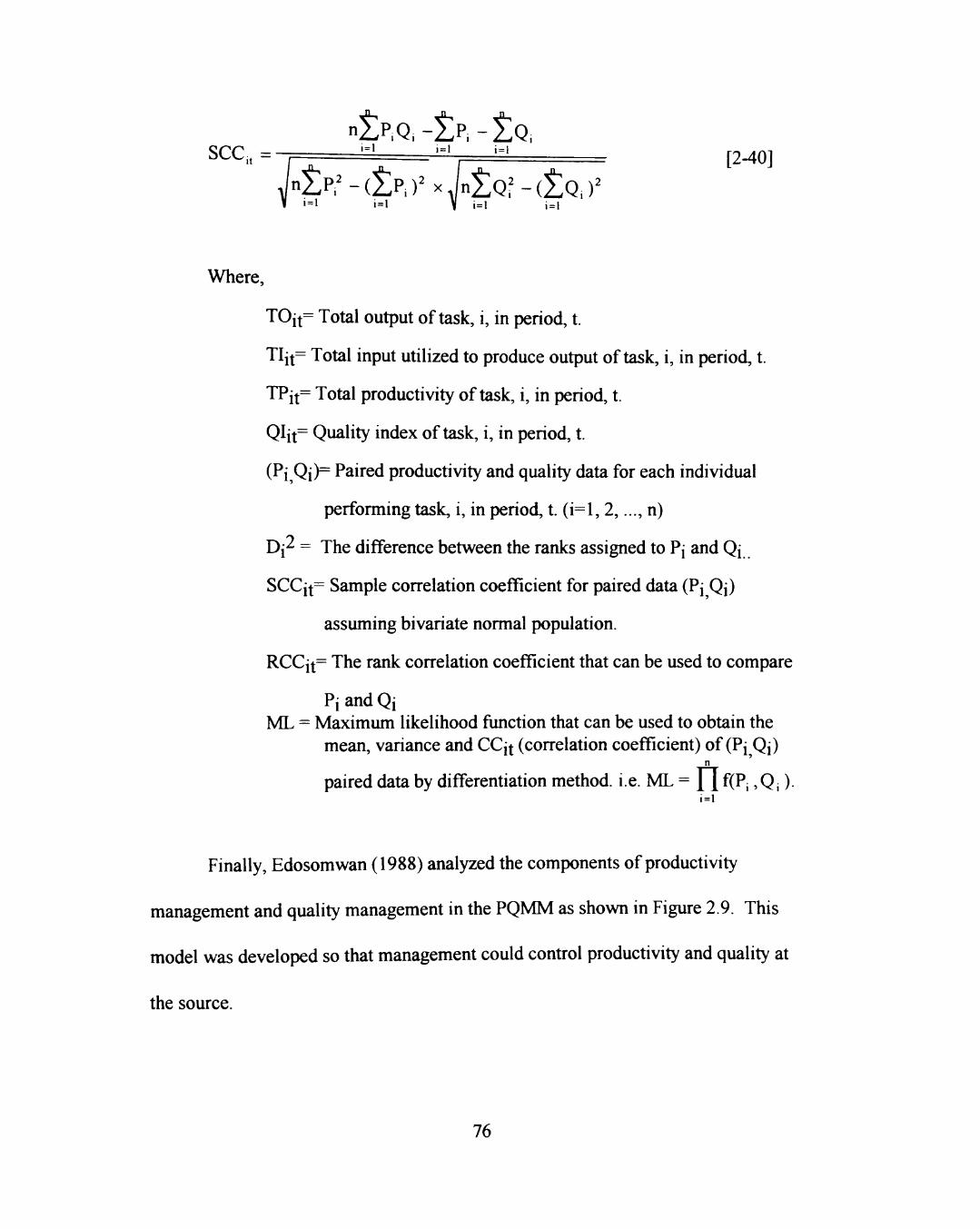

2.2.3.3 Edosomwan's Model 73

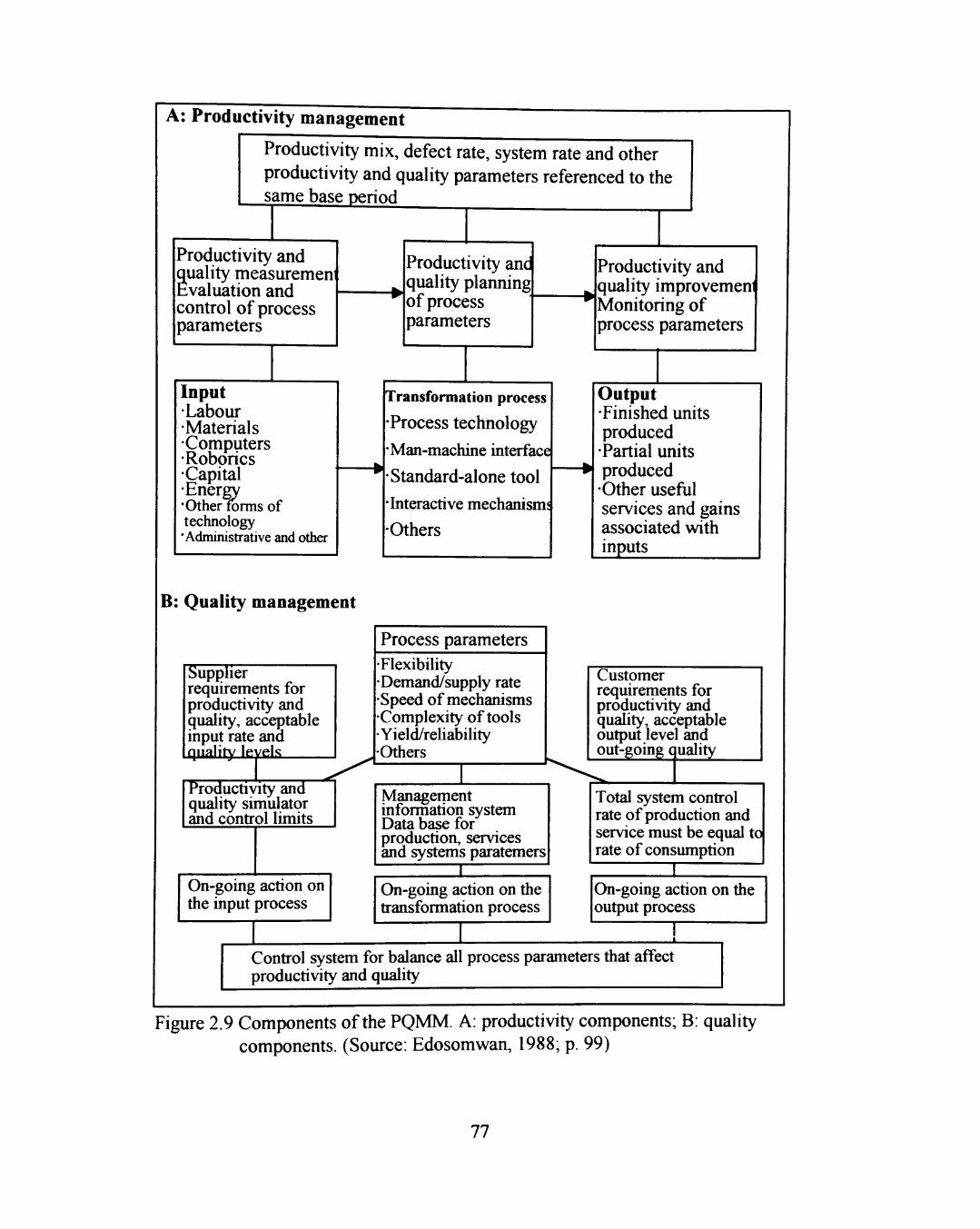

2.2.3.4 Thor's Model 78

2.2.3.5 Sumanth's Quality-Profit-Productivity Relationship Model 80

2.3 Deficiencies and Limitations of Current Models 84

2.3.1 Deficiencies and Limitations of Quality-Profit Model 84

2.3.2 Deficiencies and Limitations of Productivity-Profit Model 87

2.3.3 Deficiencies and Limitations of Quality-Productivity Model 90

2.4 Research Agenda 95

2.4.1 Definitions of This Research 95

2.4.1.1 Definition of Quality 95

2.4.1.2 Definition of Productivity 96

2.4.1.3 Definition of Profit 98

2.4.1.4 Definition of Cost 98

2.4.2 Conceptual and Mathematical Models 100

2.4.2.1 Relationships among Quality, Price, Revenue, Volume Sold, and Costs 100

V

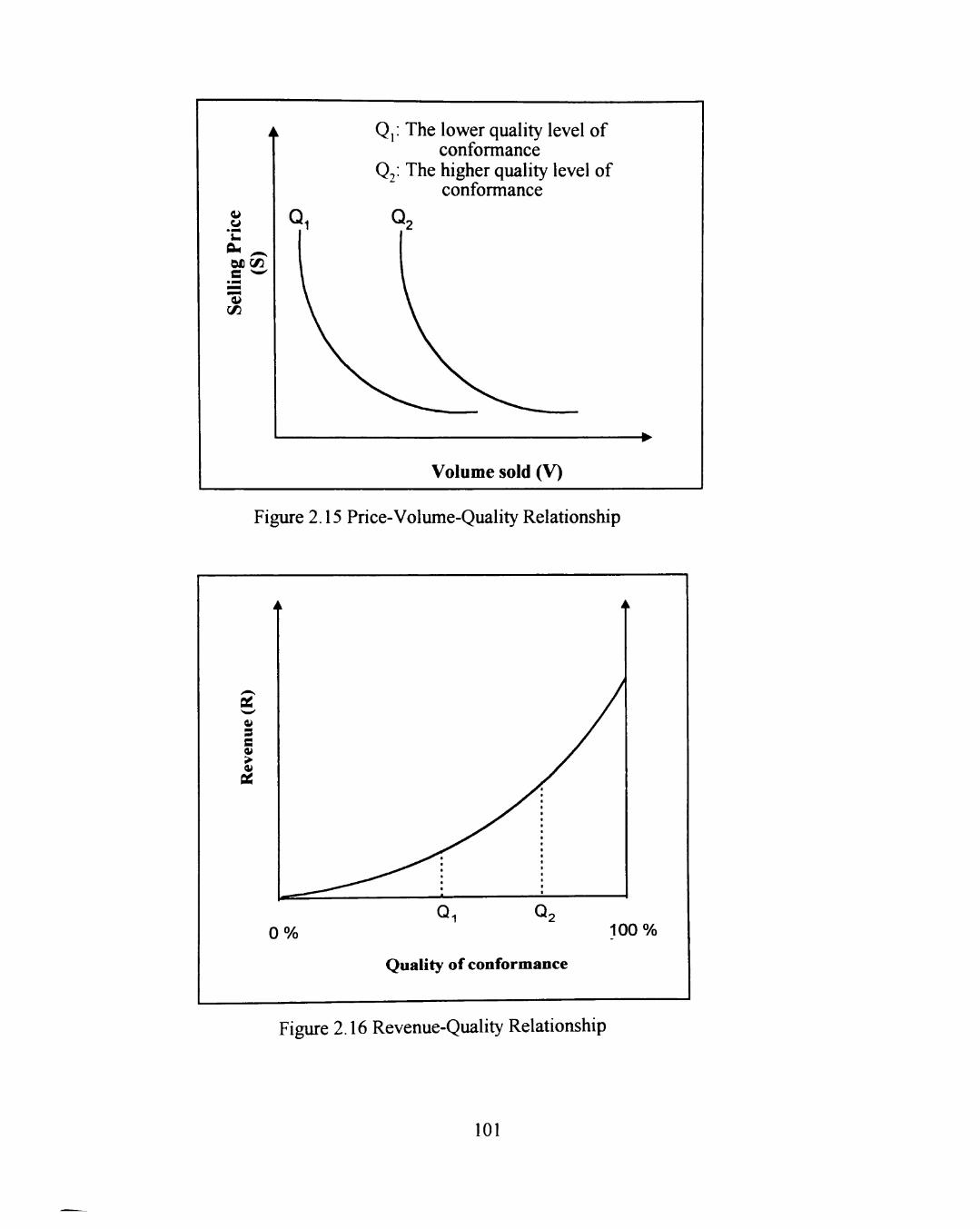

2.4.2.1.1 Price-Volume-Quality Relationship 100

2.4.2.1.2 Revenue-Quality Relationship 100

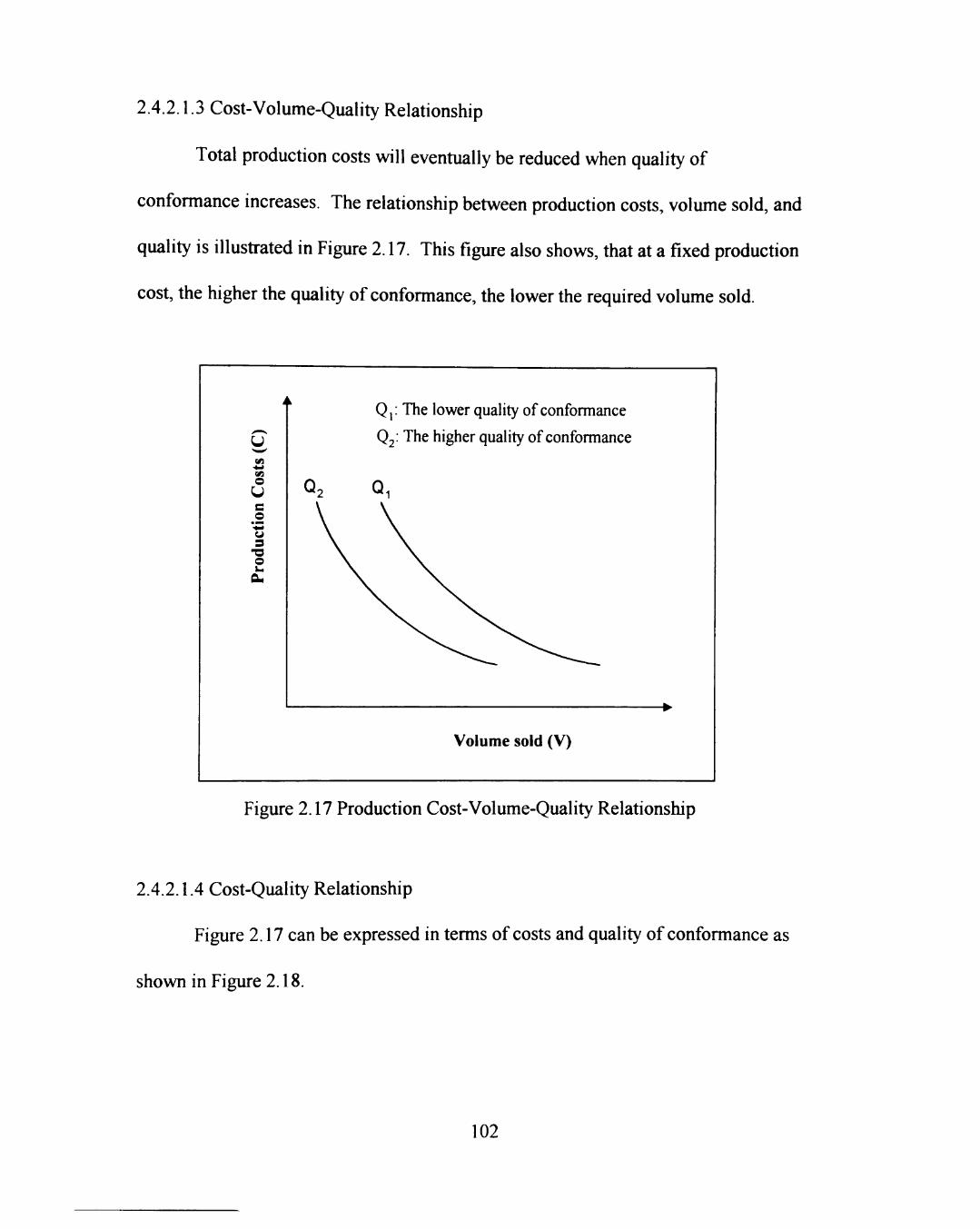

2.4.2.1.3 Cost-Volume-Quality Relationship 102

2.4.2.1.4 Cost-Quality Relationship 102

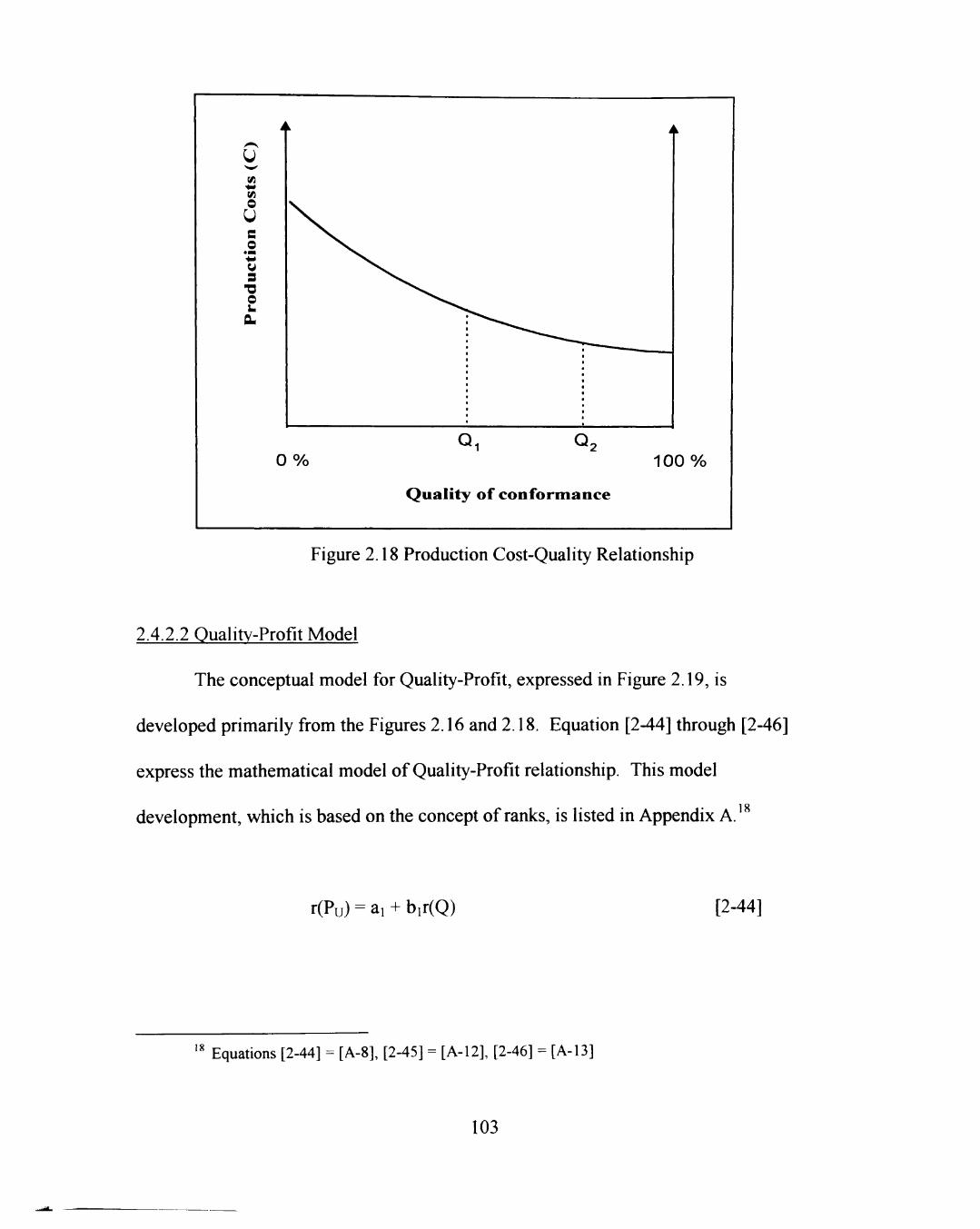

2.4.2.2 Quality-Profit Model 103

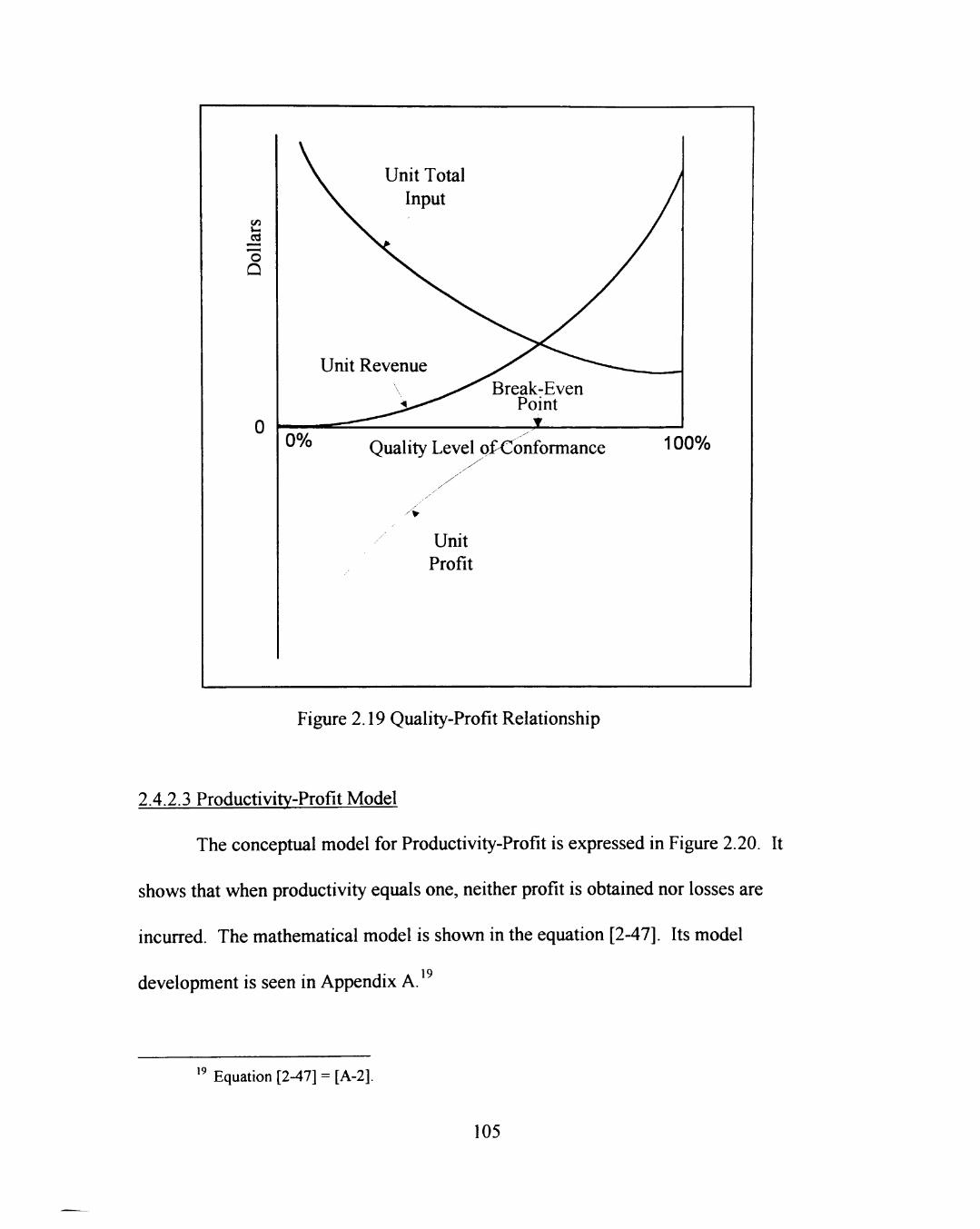

2.4.2.3 Productivity-Profit Model 105

2.4.2.4 Quality-Productivity Model 106

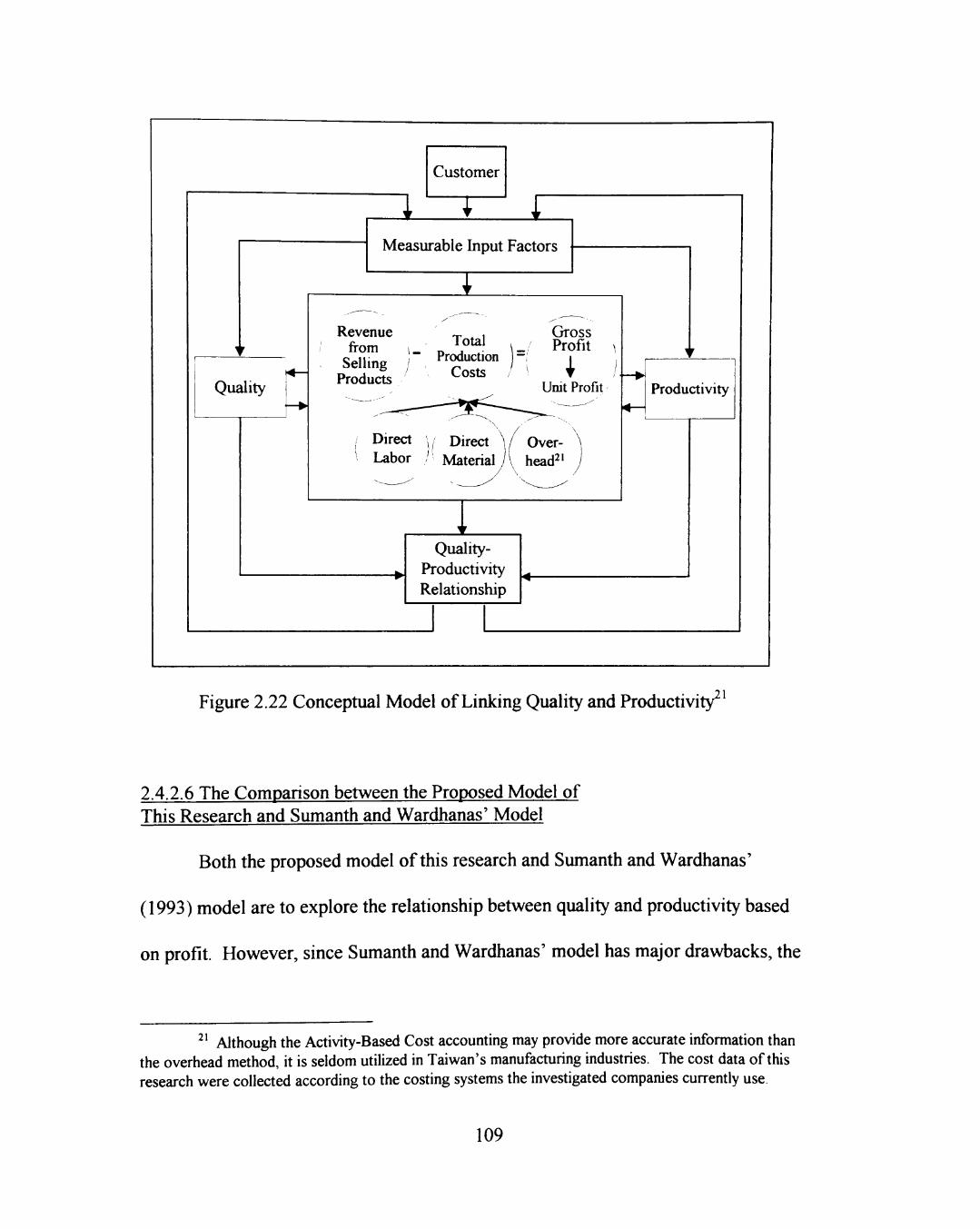

2.4.2.5 Conceptual Model of Linking Productivity and Quality in Confirmatory Study 108

2.4.2.6 The Comparison between the Proposed Model of This Research and Sumanth and Wardhanas' Model 109

2.4.2.7 Advantages of Relating Quality-Profit and Quality-Productivity

Models Based on Ranks 113

2.4.2.8 Contributions of This Research 114

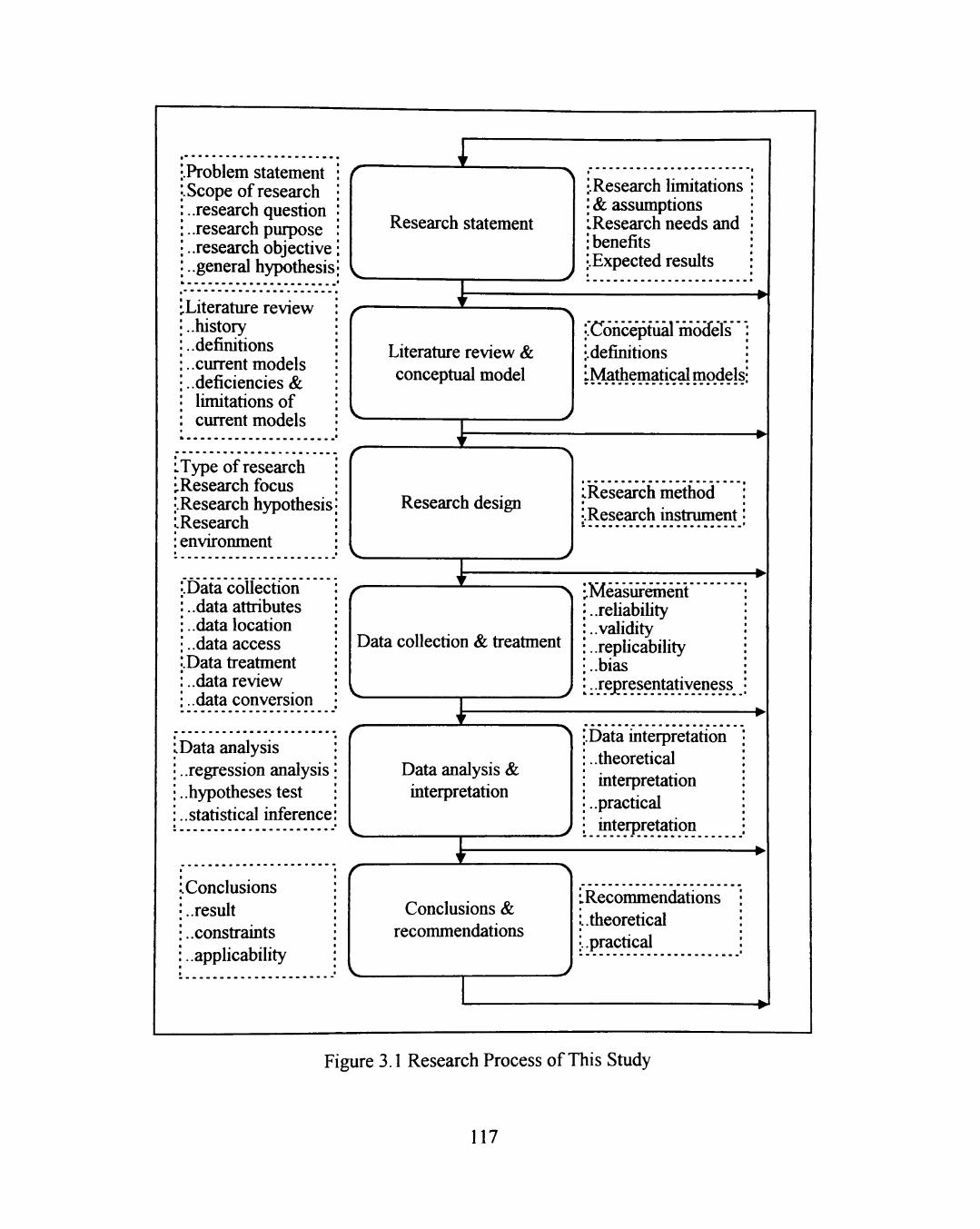

3. RESEARCH METHODOLOGY 116

3.1 Research Process 116

3.2 Research Design 118

3.2.1 Type of Research 119

3.2.2 Research Focus 119

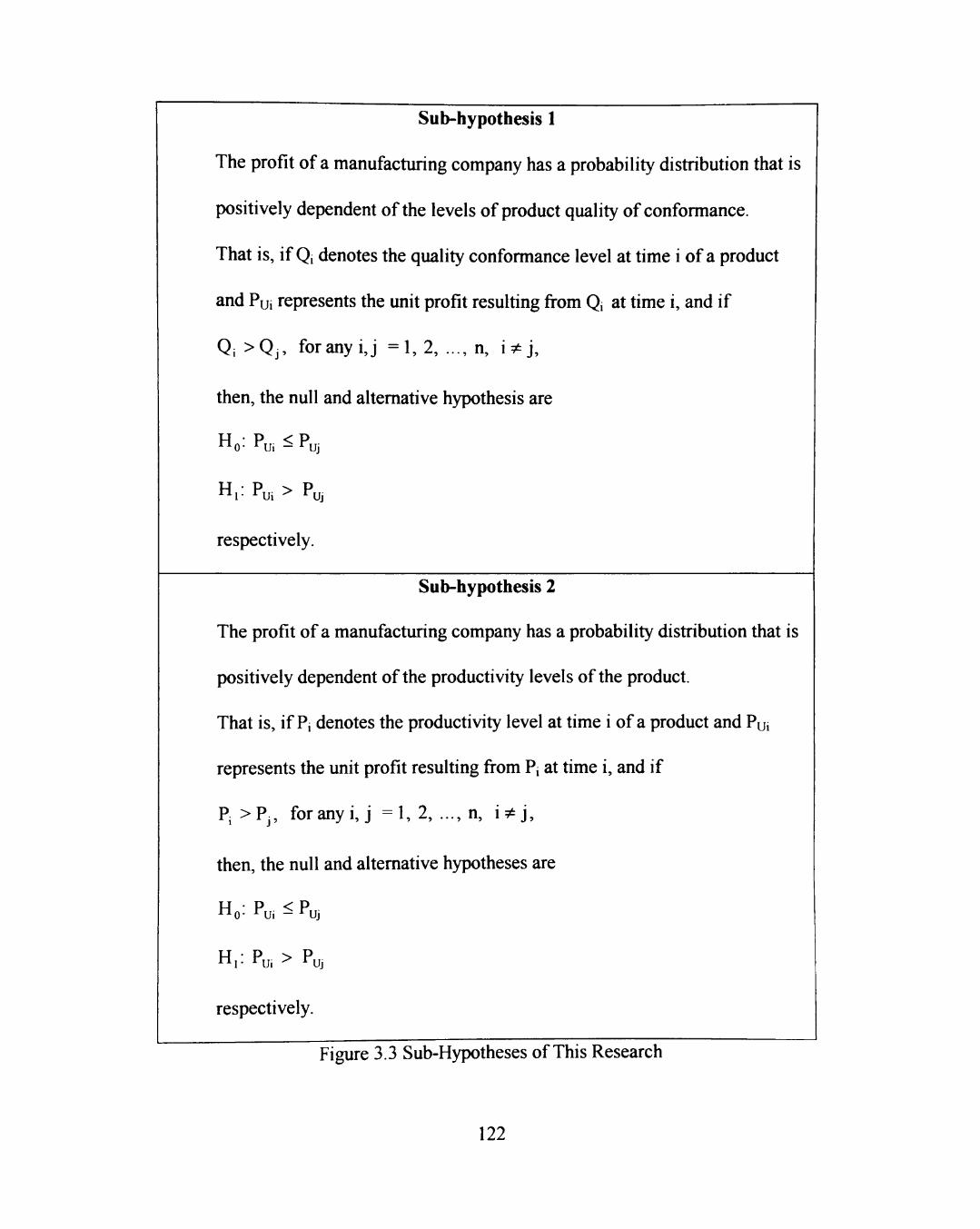

3.2.3 Research Hypotheses 120

3.2.4 Research Environment 123

3.2.4.1 ABC Company 123

3.2.4.2 XYZ Company 125

vi

3.2.5 Research Method 127

3.2.6 Research Instrument 127

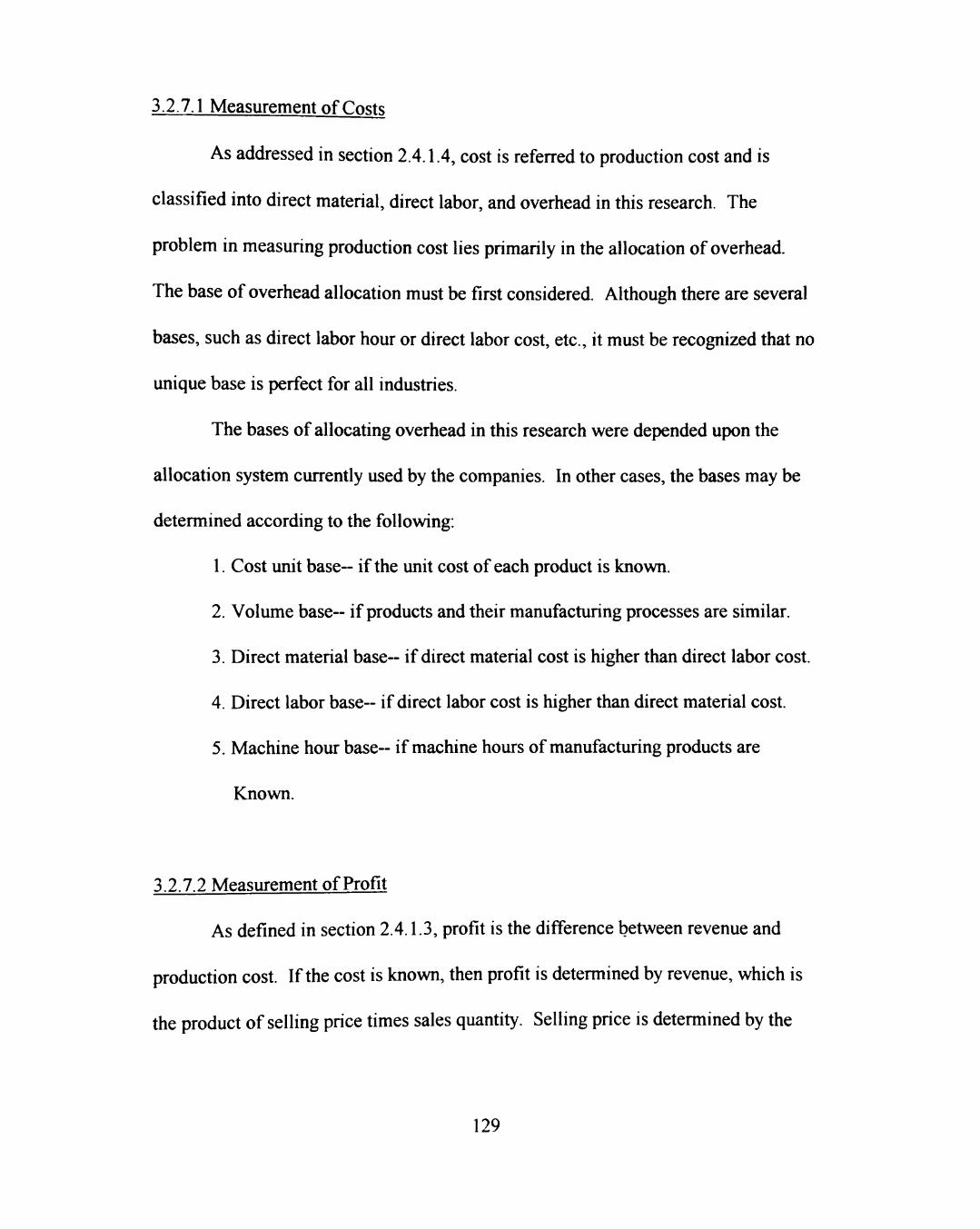

3.2.7 Measurement of Costs and Profit 127

3.2.7.1 Measurement of Costs 129

3.2.7.2 Measurement of Profit 129

3.2.8 Test Plans of This Research 130

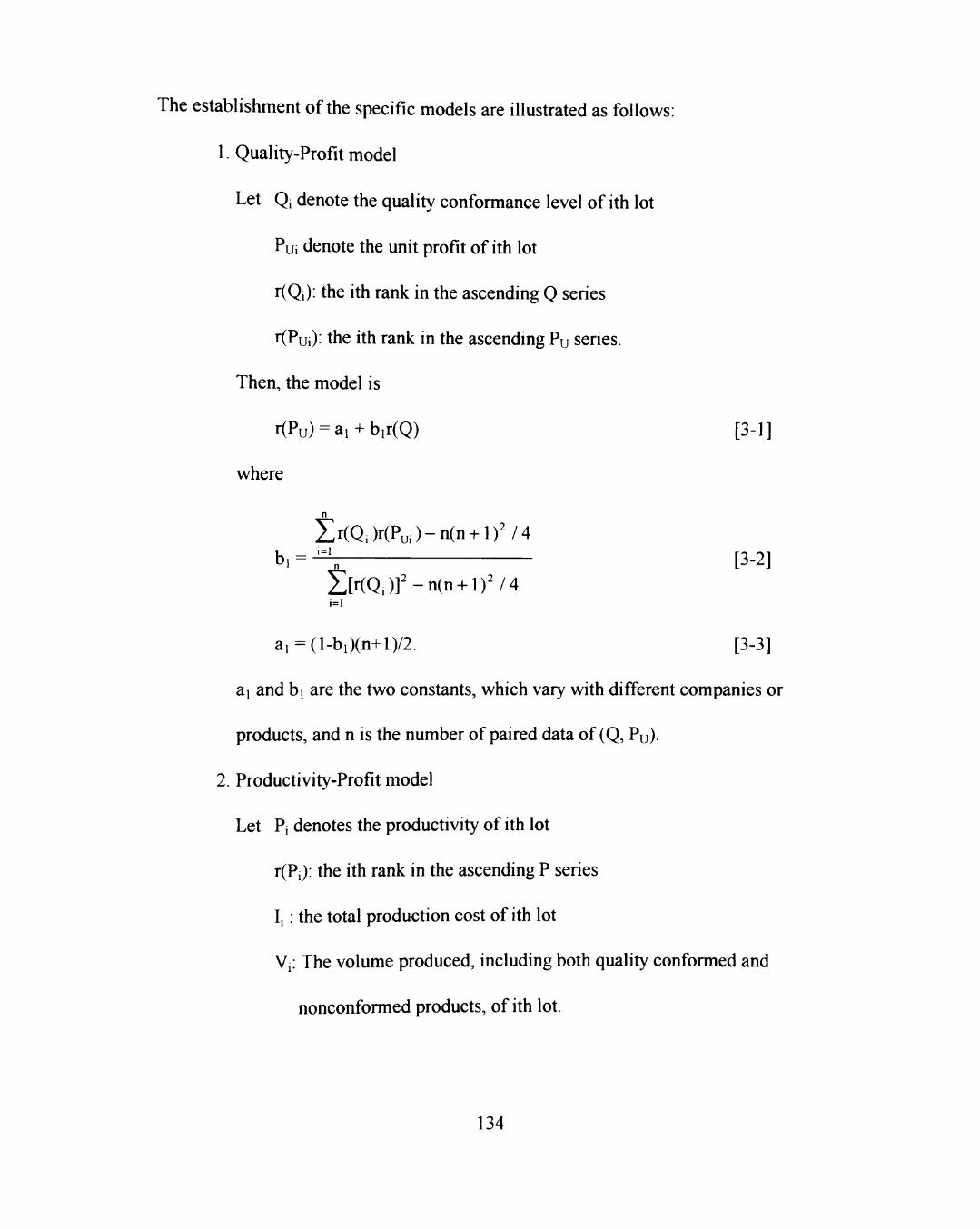

3.2.9 Specific Models Establishment 120

3.2.10 Unit of Analysis 135

3.2.10.1 ABC Company 135

3.2.10.2 XYZ Company 136

3.3 The Collection and Treatment of Data 136

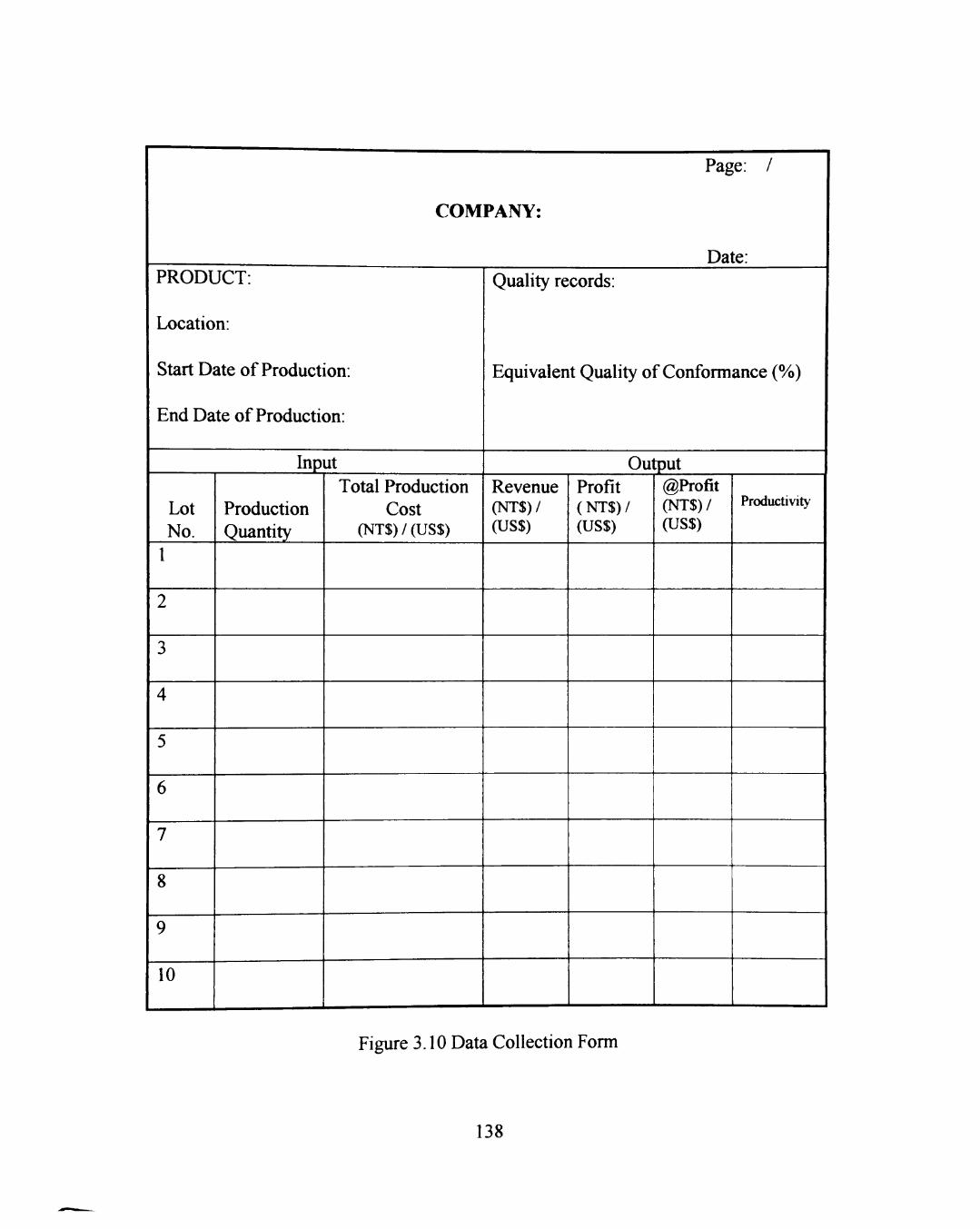

3.3.1 Data Collection 137

3.3.2 Treatment of Data 137

3.4 Methodological Issues 140

3.4.1 Reliability 140

3.4.2 Validity 142

3.4.3 Replicability 144

3.4.4 Bias 145

3.4.5 Representativeness 147

3.5 Research Constraints 147

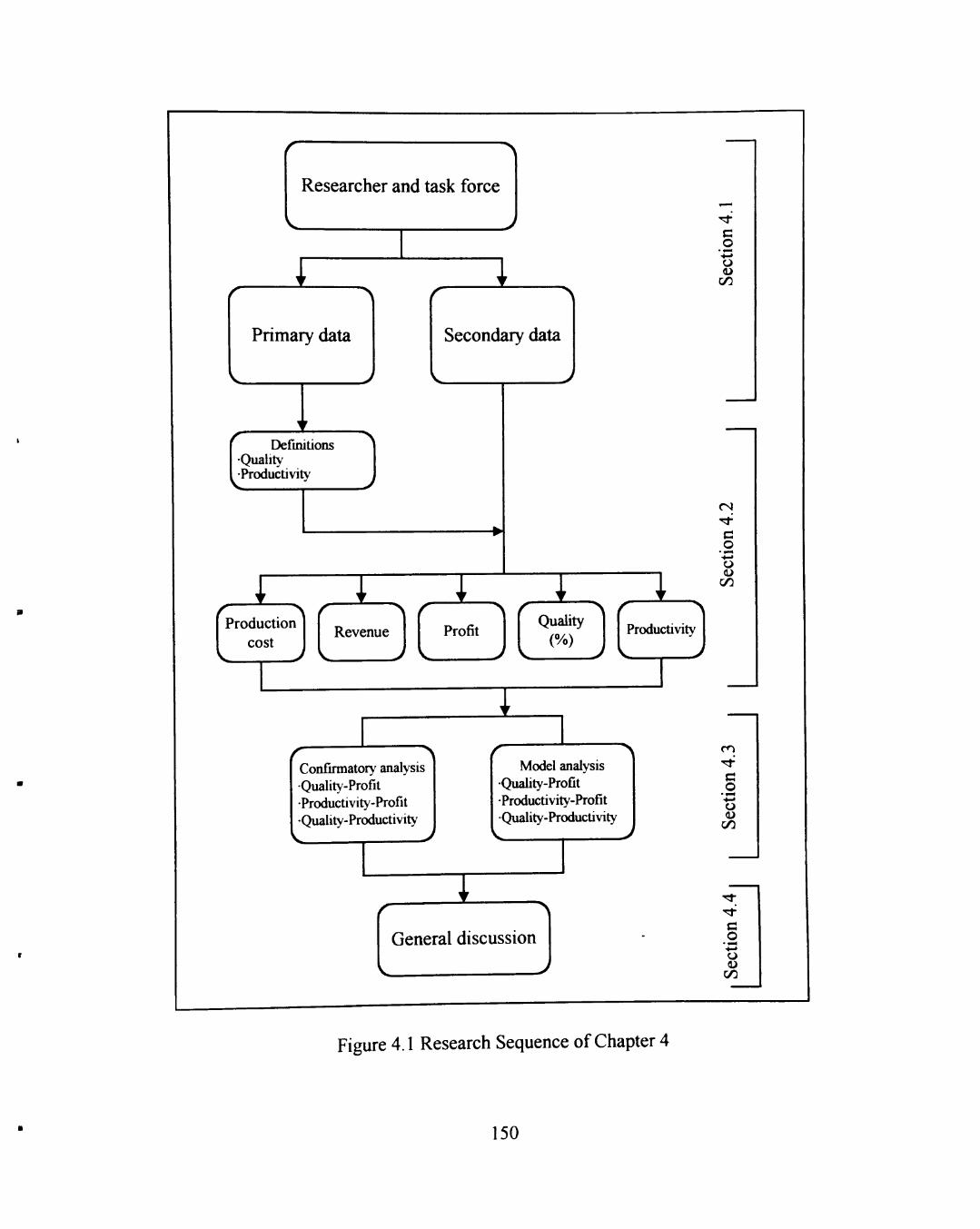

4. FIELD STUDY RESULTS, ANALYSIS, AND DISCUSSION 149

vu

4.1 Introduction 151

4.1.1 Company Contacts 151

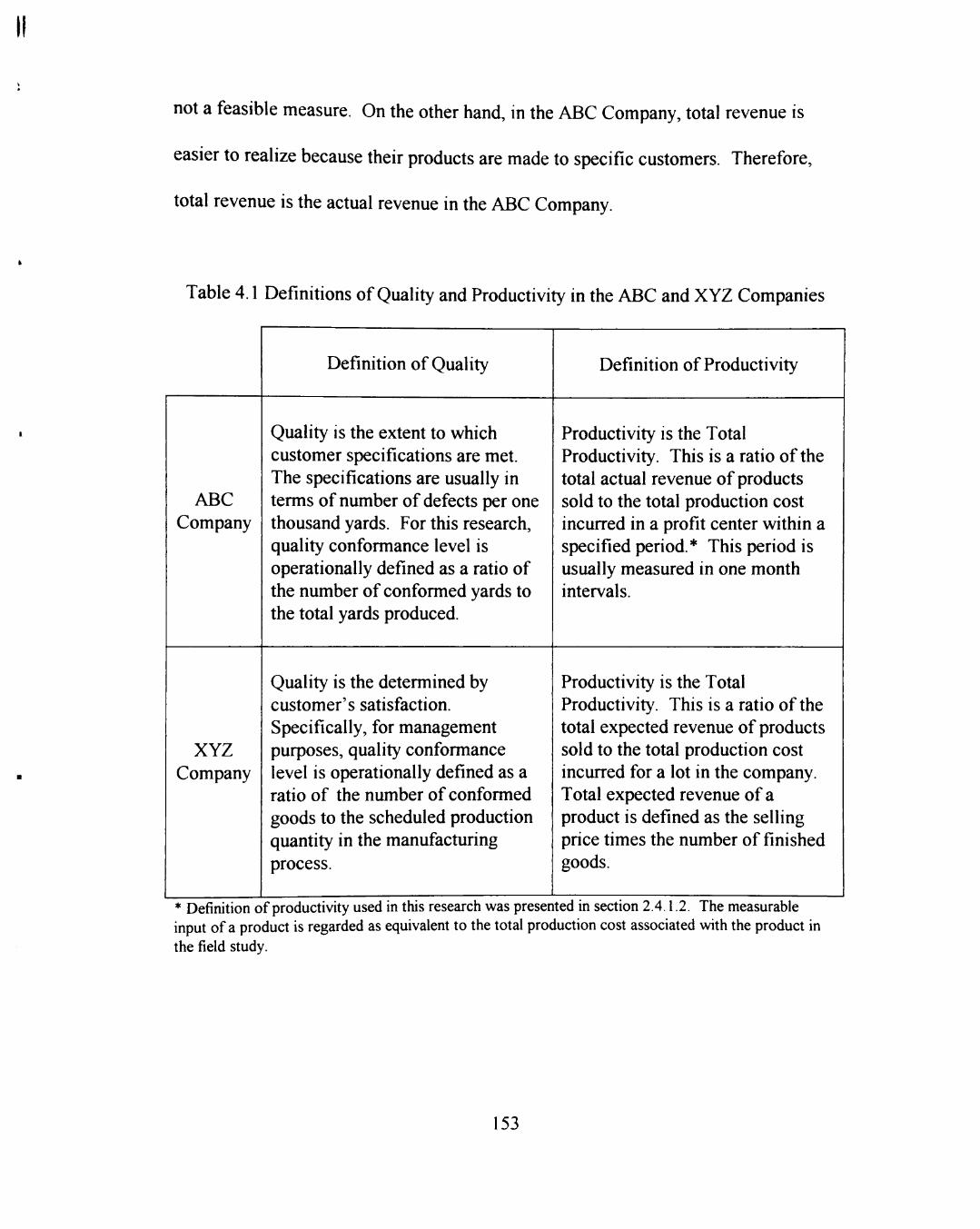

4.1.2 Operation Definition 152

4.1.3 Primary Data Collected 154

4.1.4 Secondary Data Collected 154

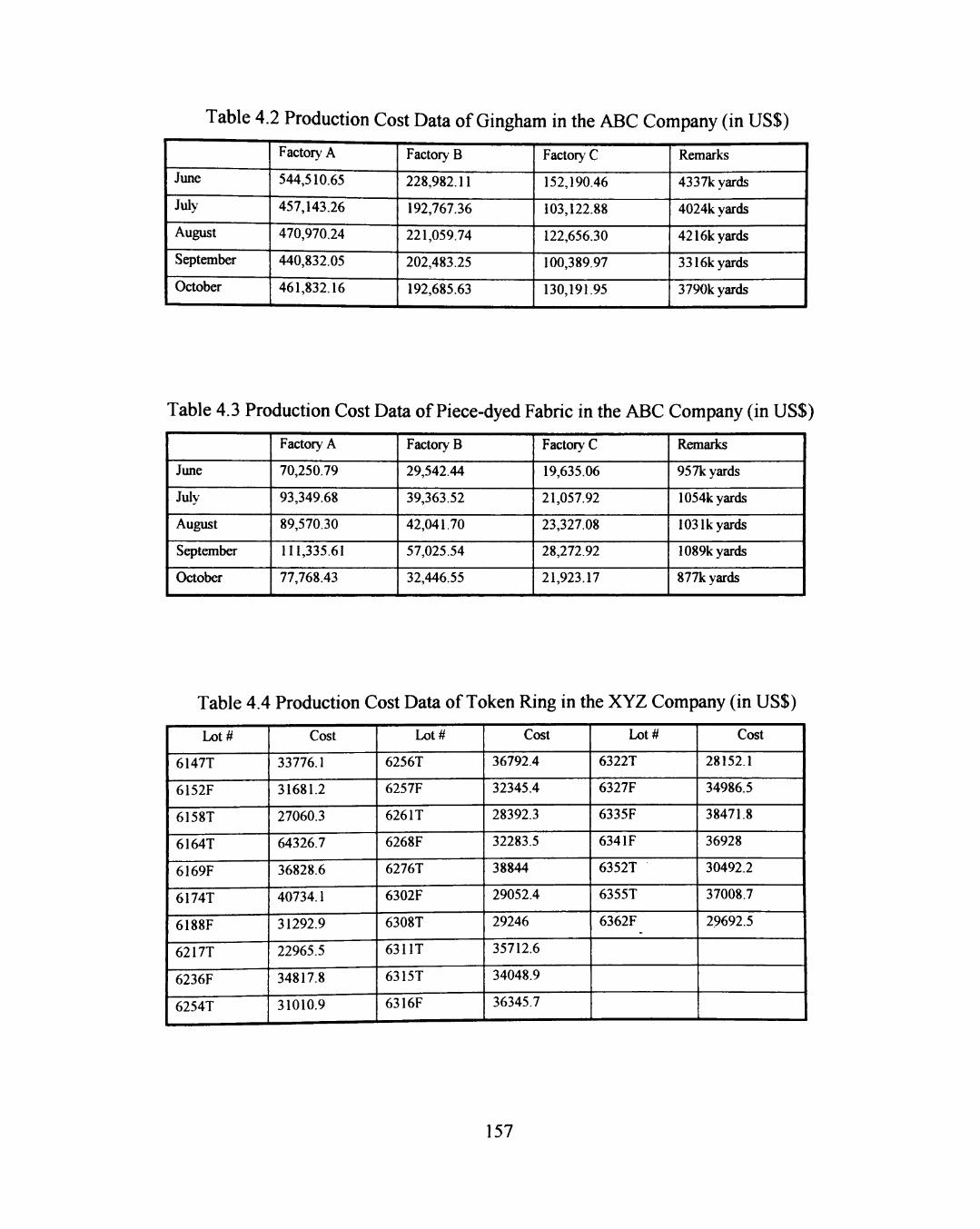

4.2 Results of Collected Data 156

4.2.1 Production Cost Data 156

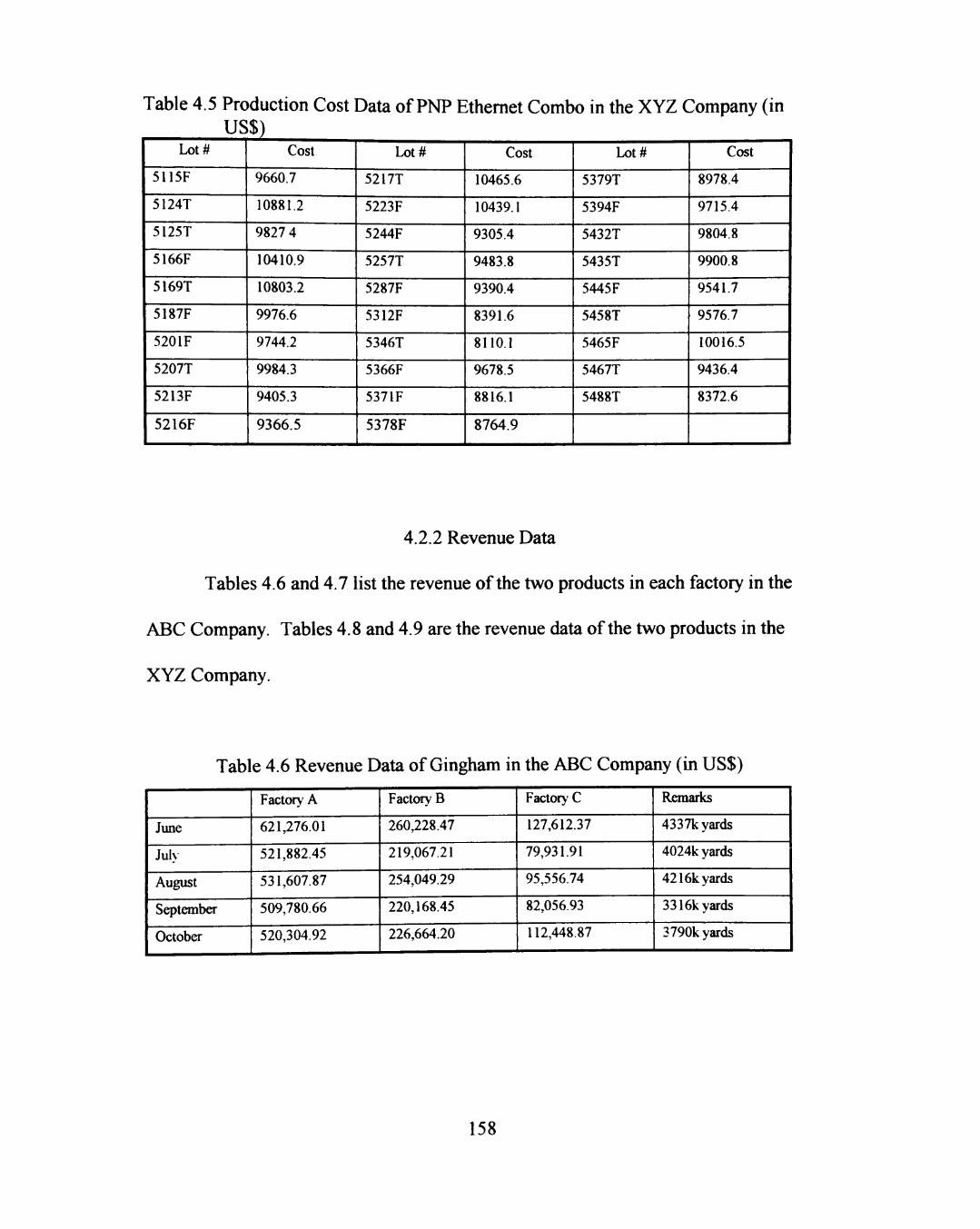

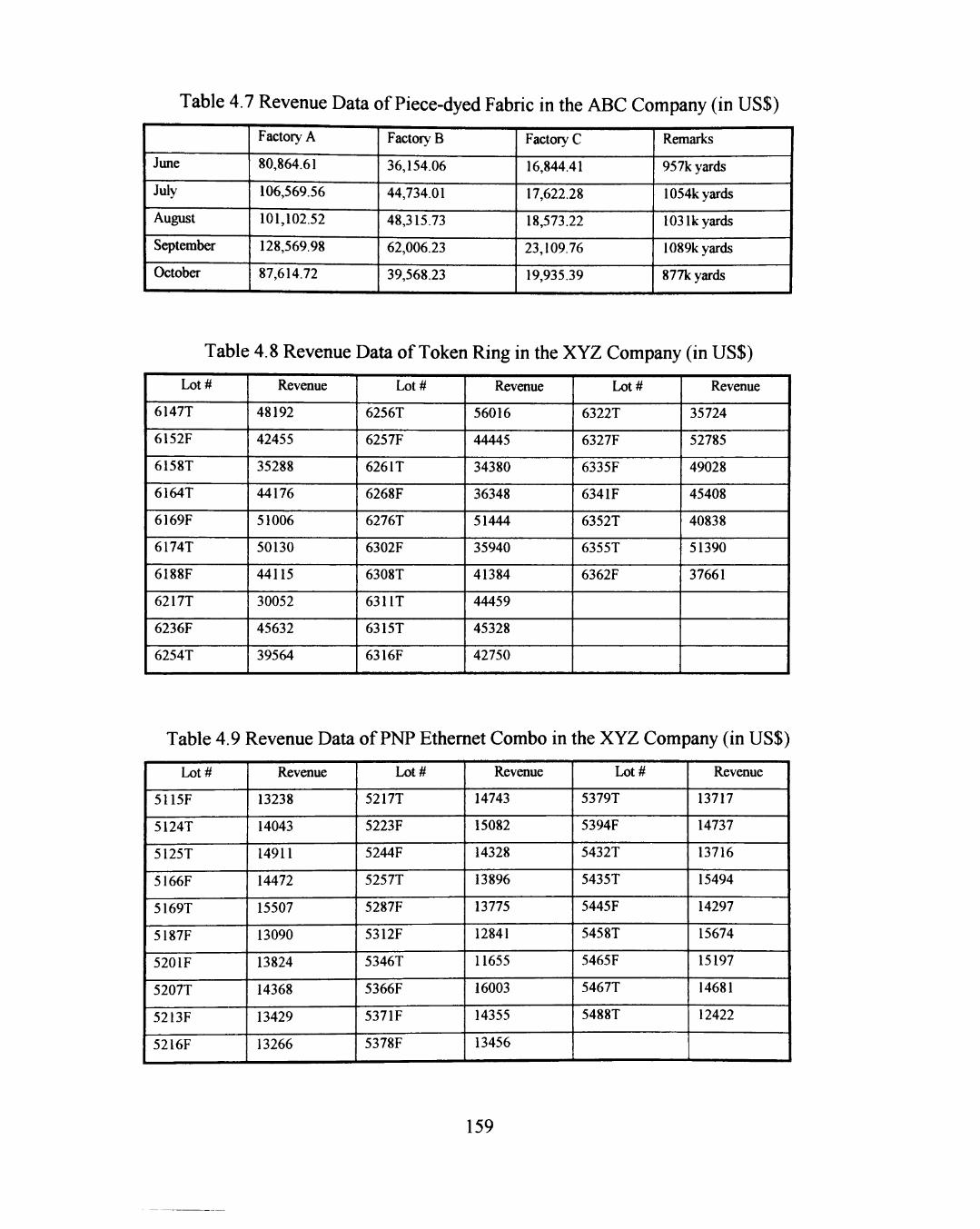

4.2.2 Revenue Data 158

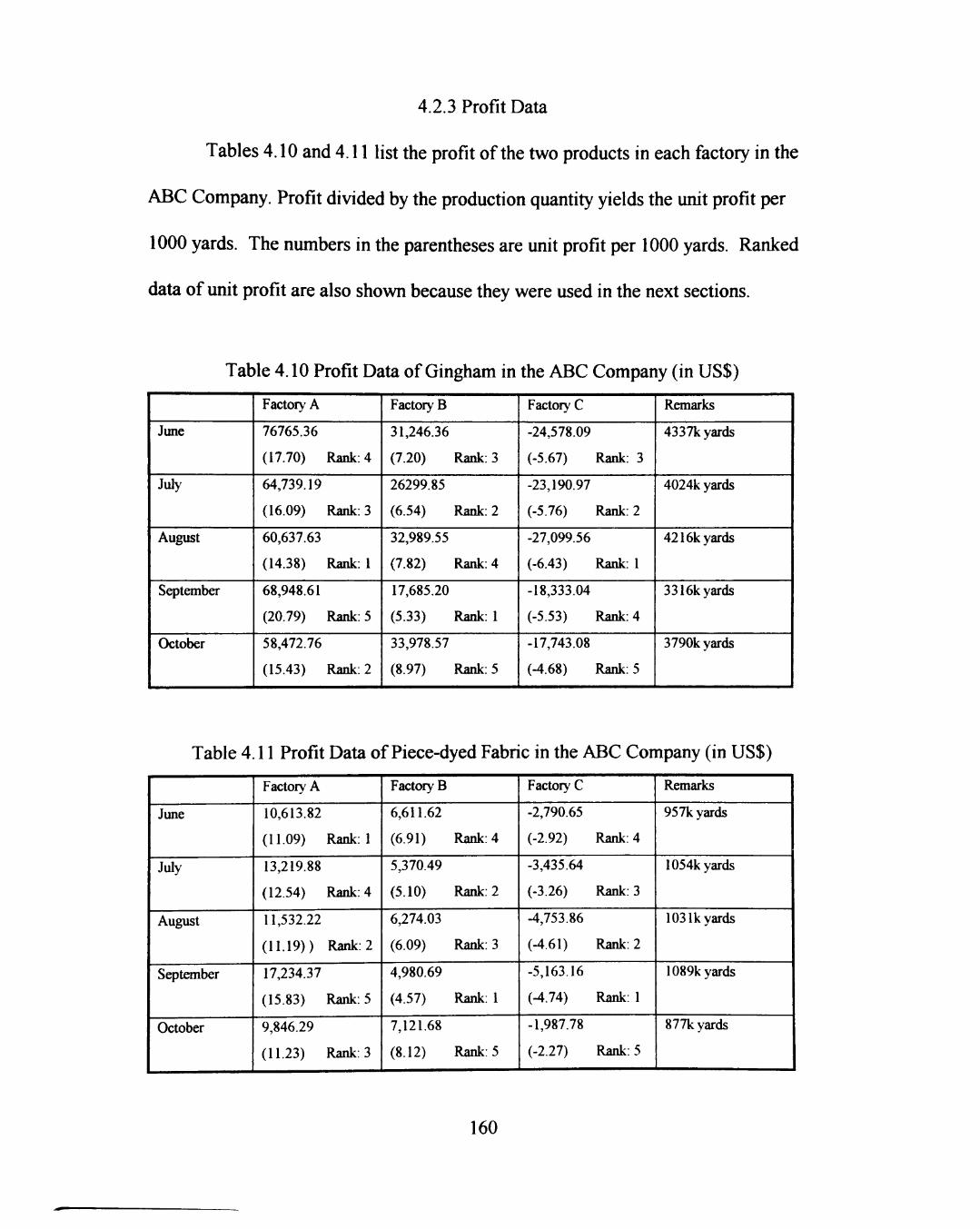

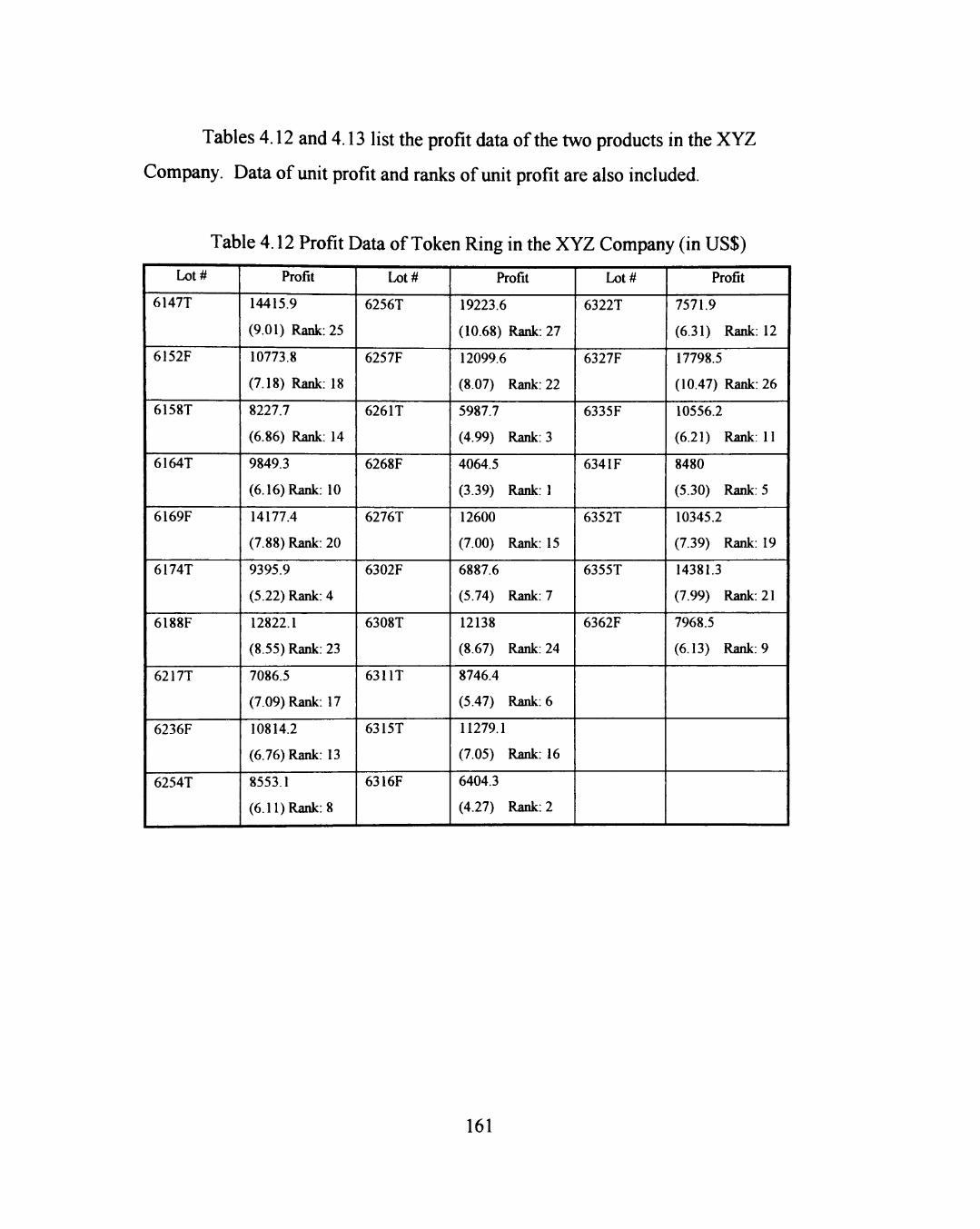

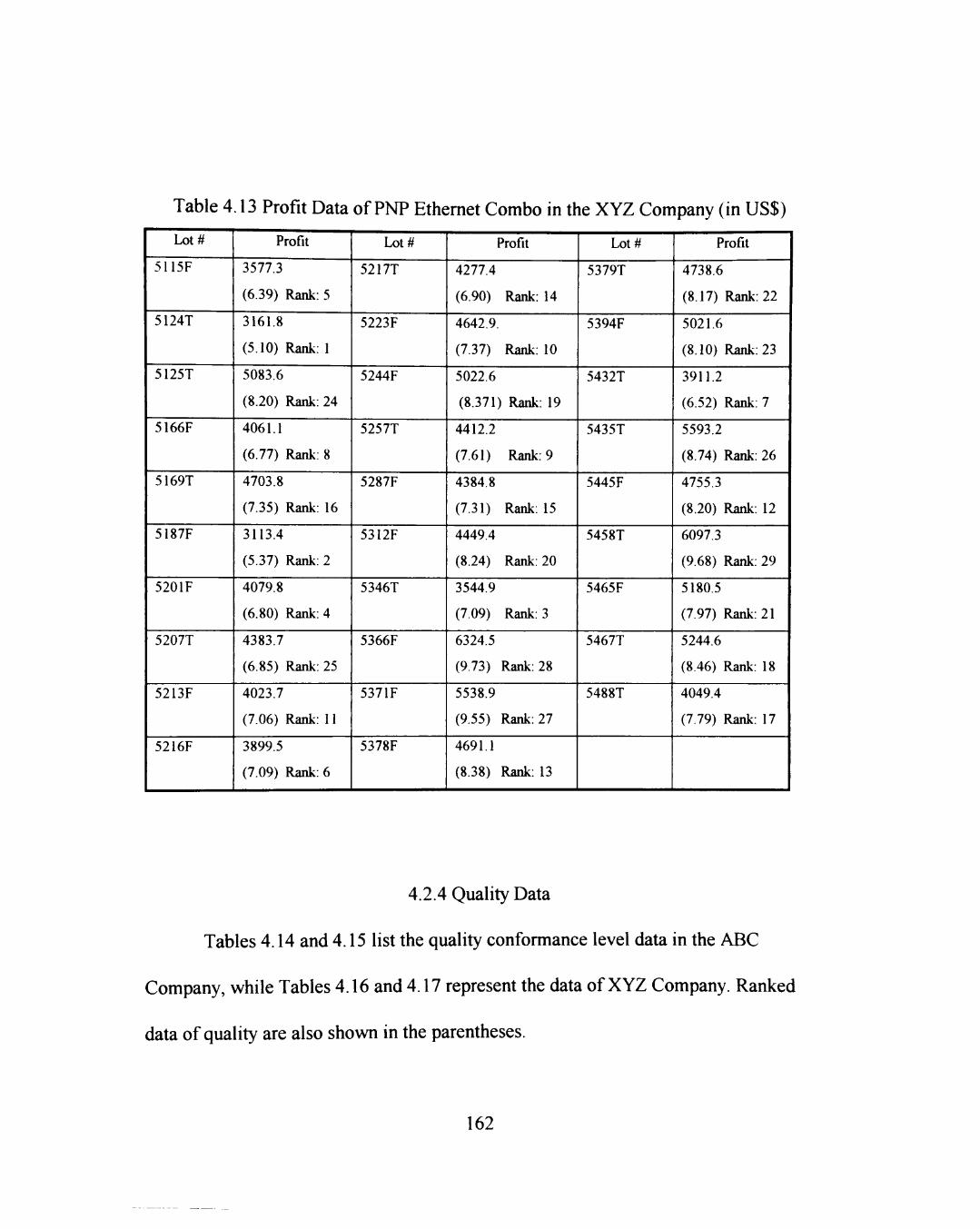

4.2.3 Profit Data 160

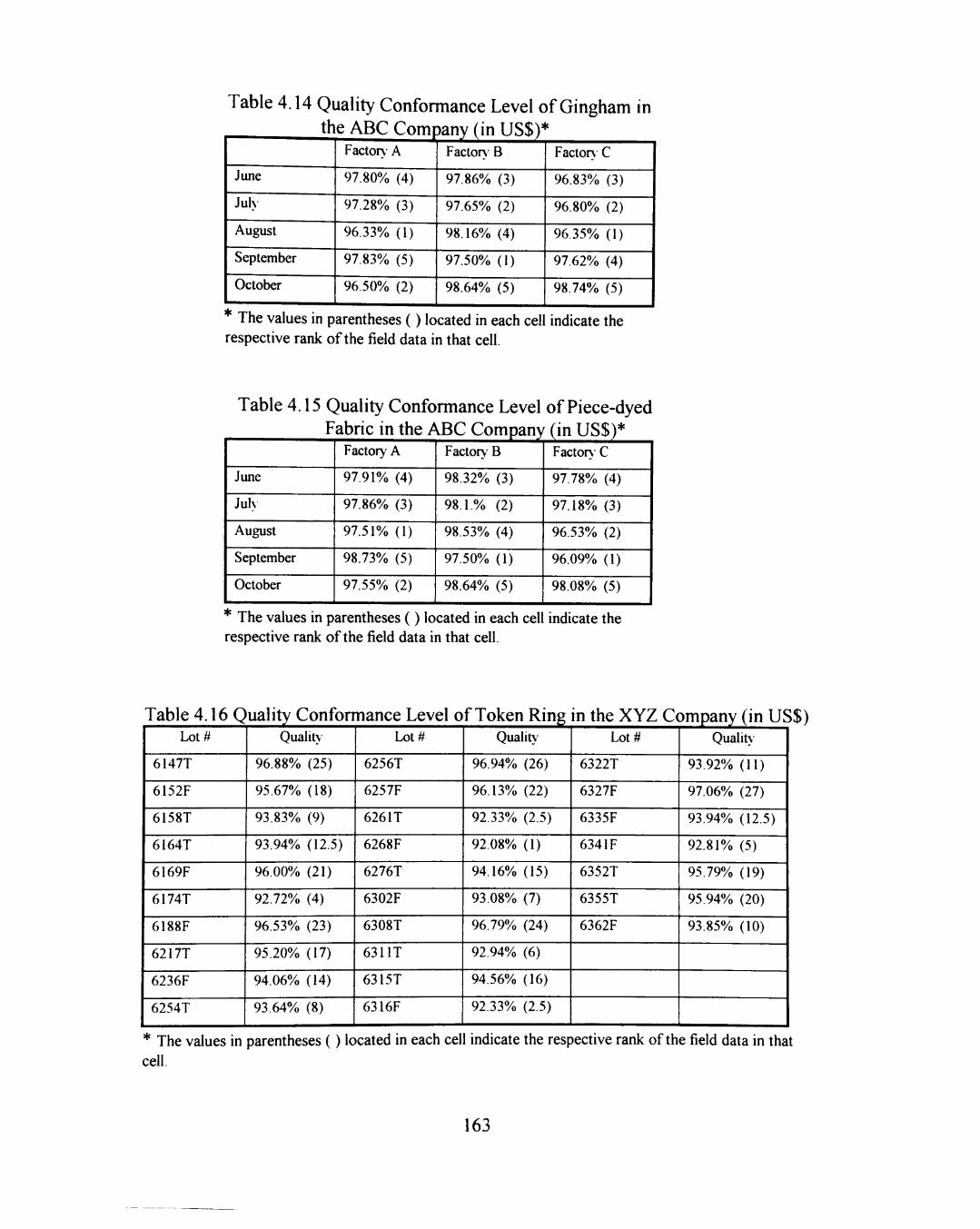

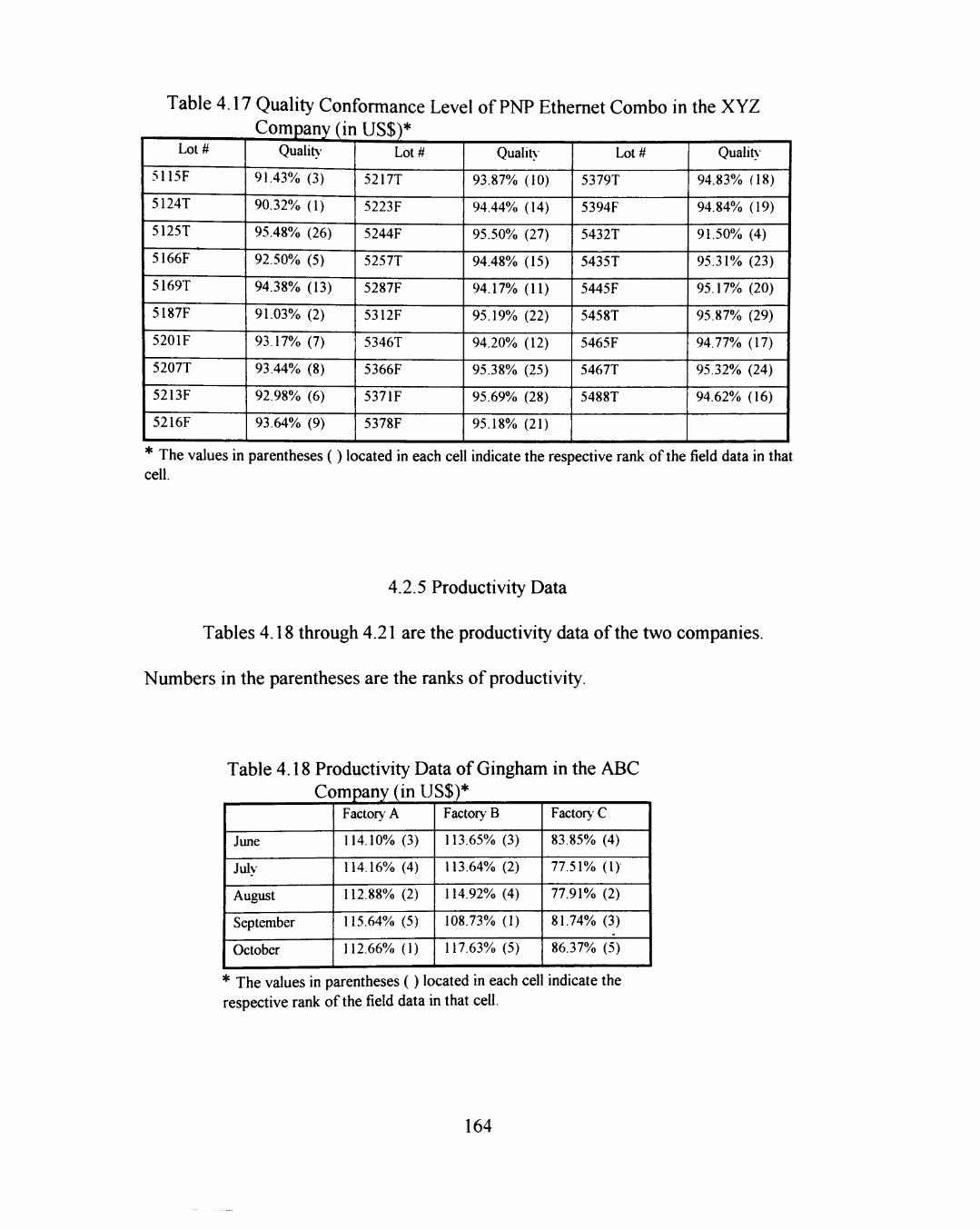

4.2.4 Quality Data 162

4.2.5 Productivity Data 164

4.3 Data Analysis 166

4.3.1 Confirmatory Analysis 166

4.3.1.1 Method of Analysis 167

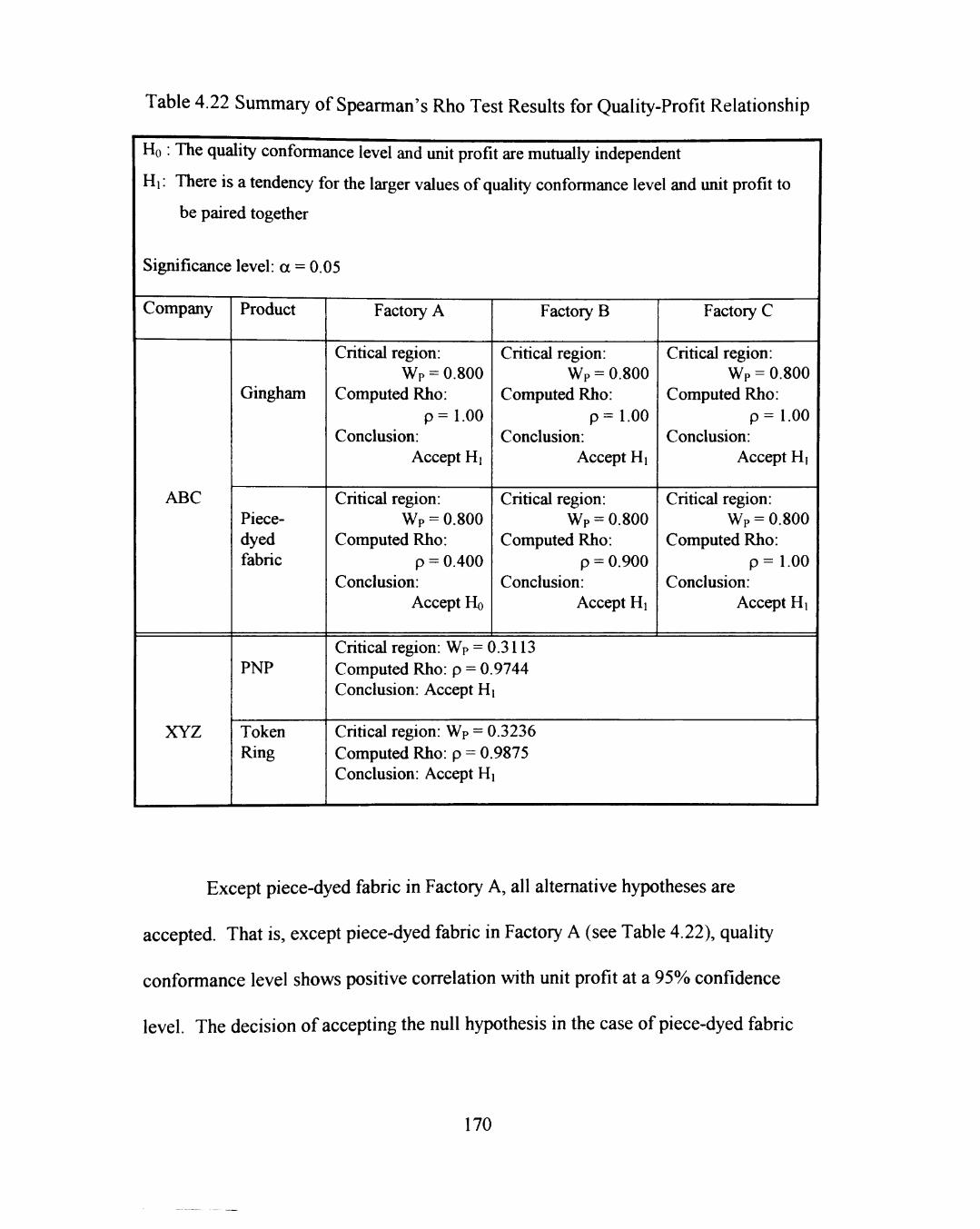

4.3.1.2 Quality-Profit Analysis 169

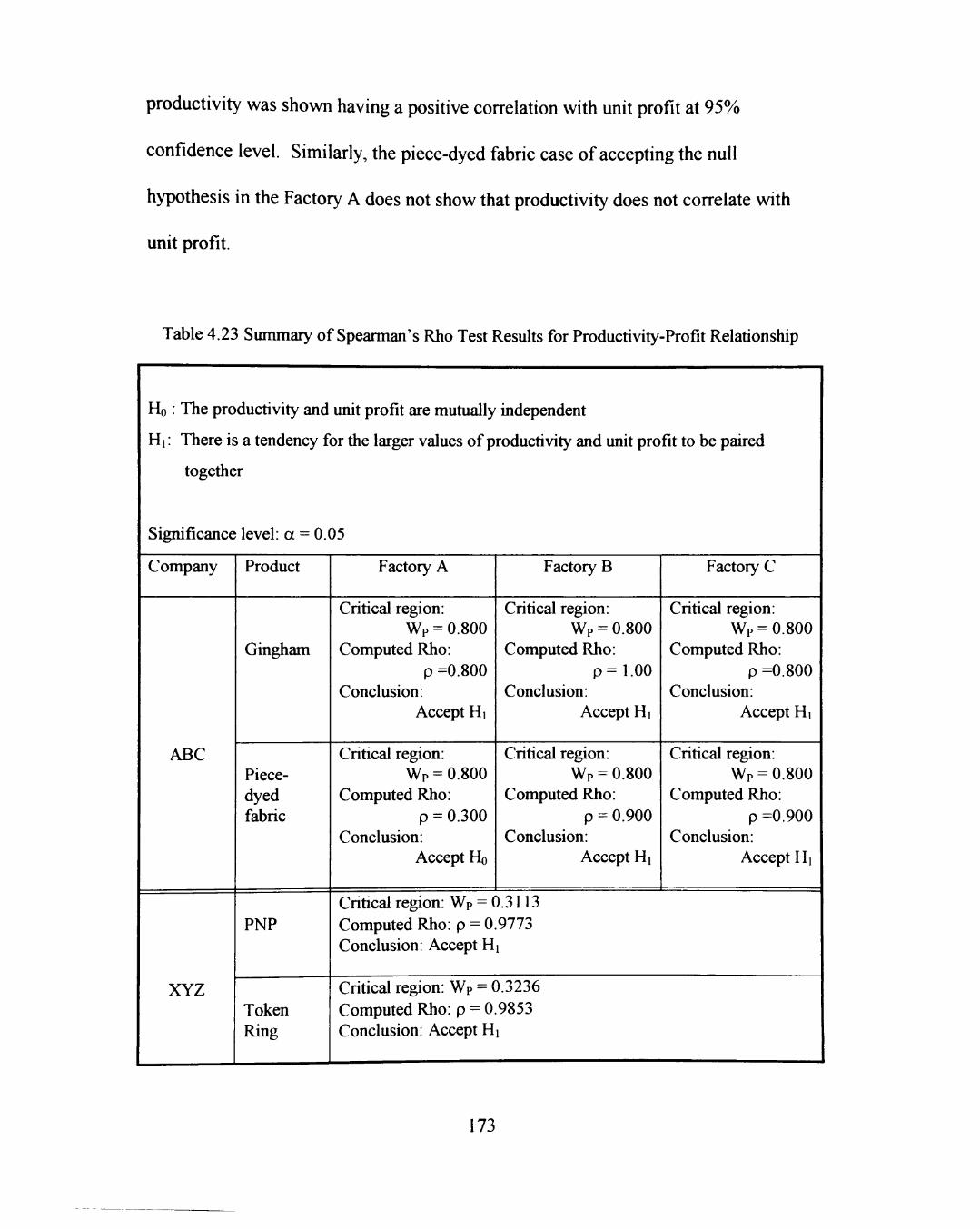

4.3.1.2.1 Spearman's Rho Test 169

4.3.1.2.2 Normality Test 171

4.3.1.2.3 Estimation of Confidence Interval of Correlation Coefficient 171

4.3.1.3 Productivity-Profit Analysis 172

4.3.1.3.1 Spearman's Rho Test 172

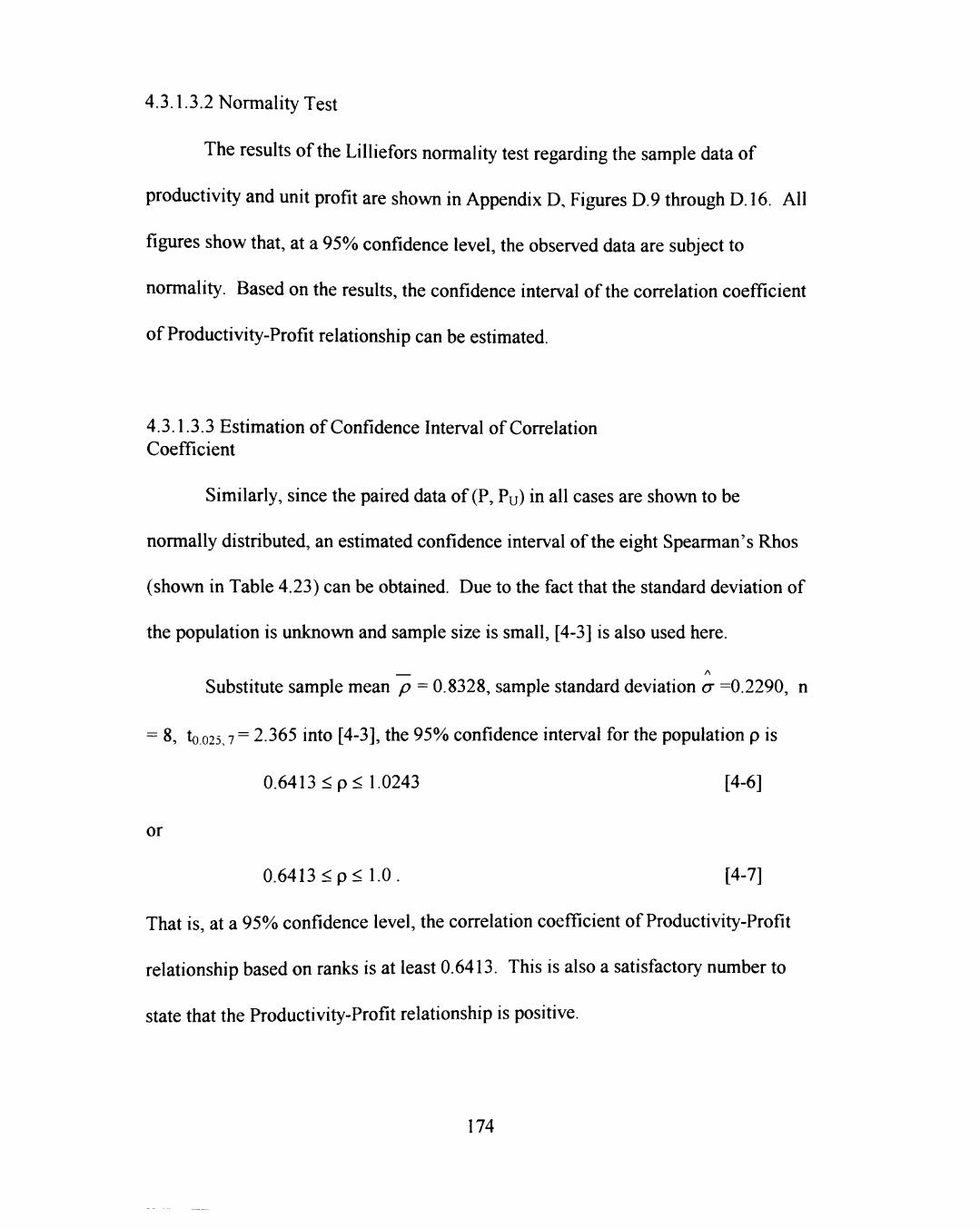

4.3.1.3.2 Normality Test 174

4.3.1.3.3 Estimation of Confidence Interval of Correlation Coefficient 174

viii

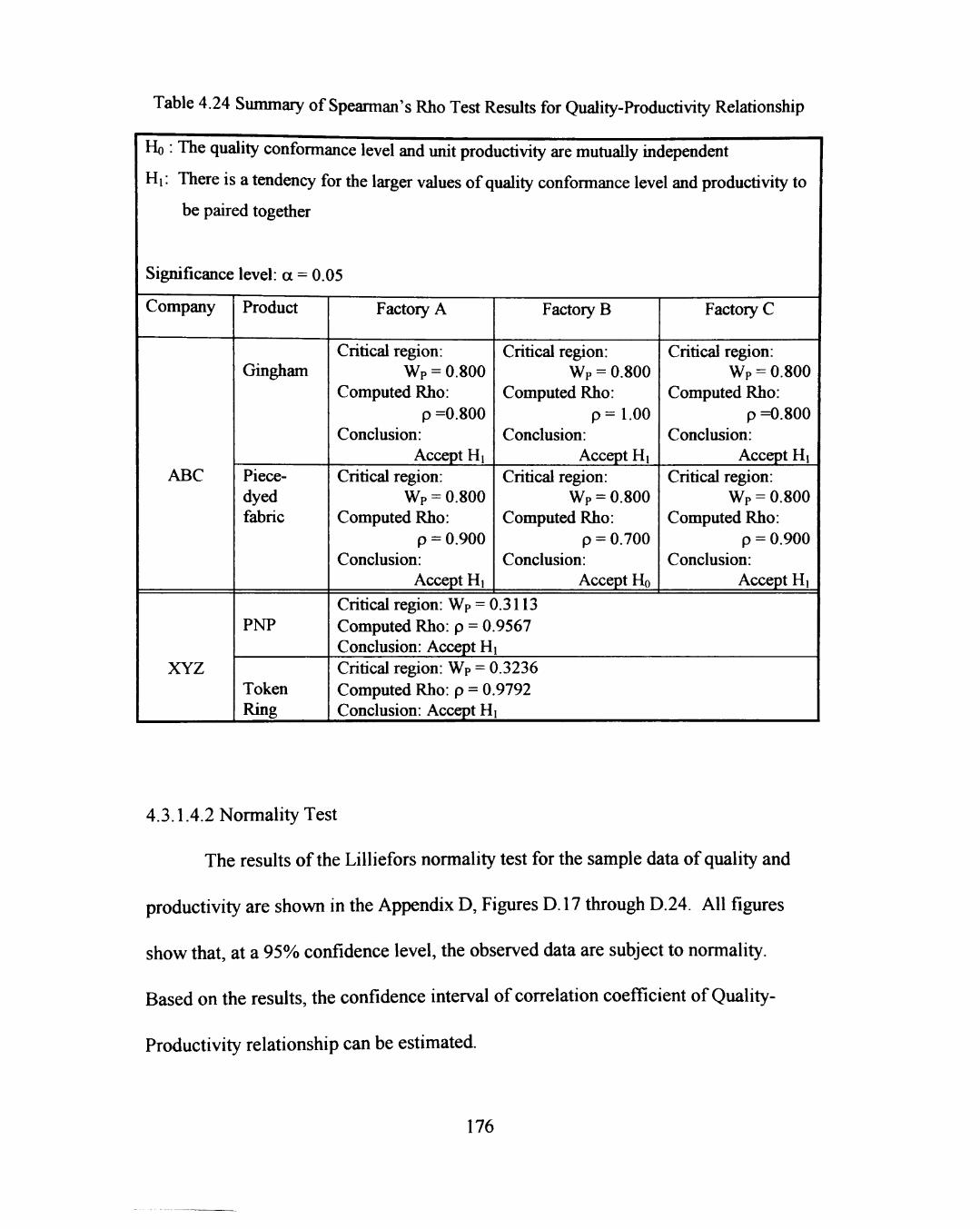

4.3.1.4 Quality-Productivity Analysis 175

4.3.1.4.1 Spearman's Rho Test 175

4.3.1.4.2 Normality Test 176

4.3.1.4.3 Estimation of Confidence Interval of Correlation Coefficient 177

4.3.2 Model Analysis 178

4.3.2.1 Method of Analysis 178

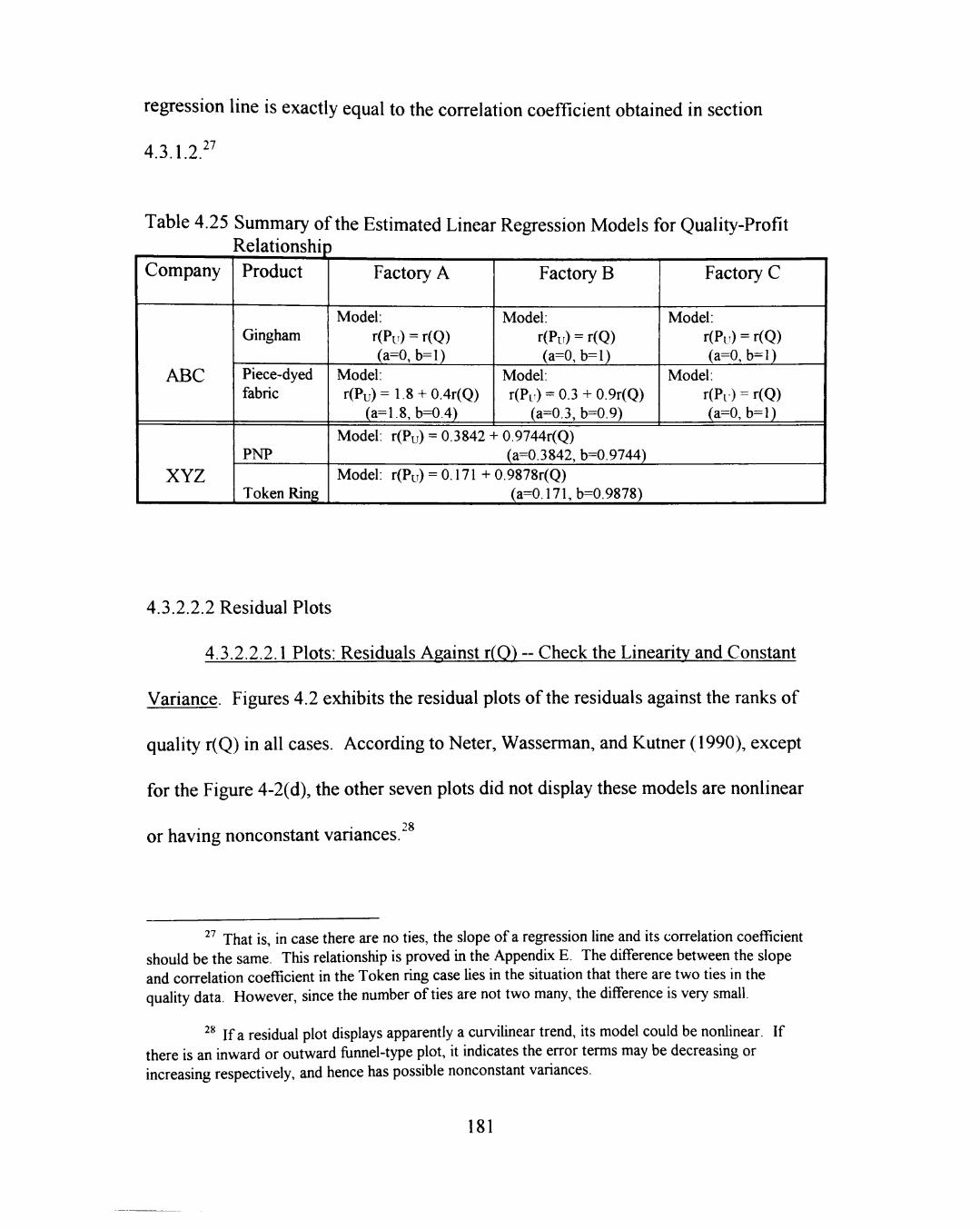

4.3.2.2 Quality-Profit Relationship Model Analysis 180

4.3.2.2.1 Specific Linear Regression Models 180

4.3.2.2.2 Residual Plots 181

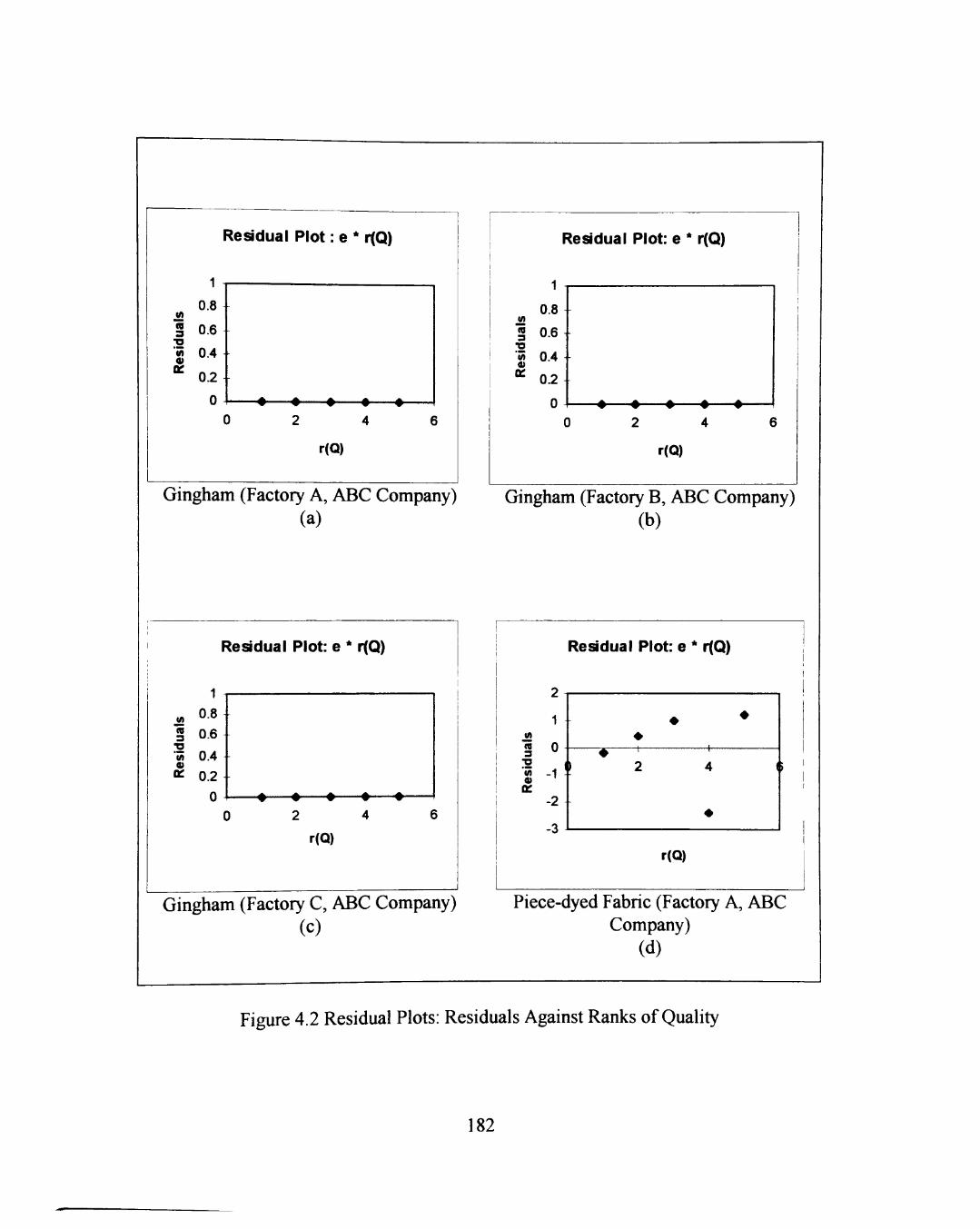

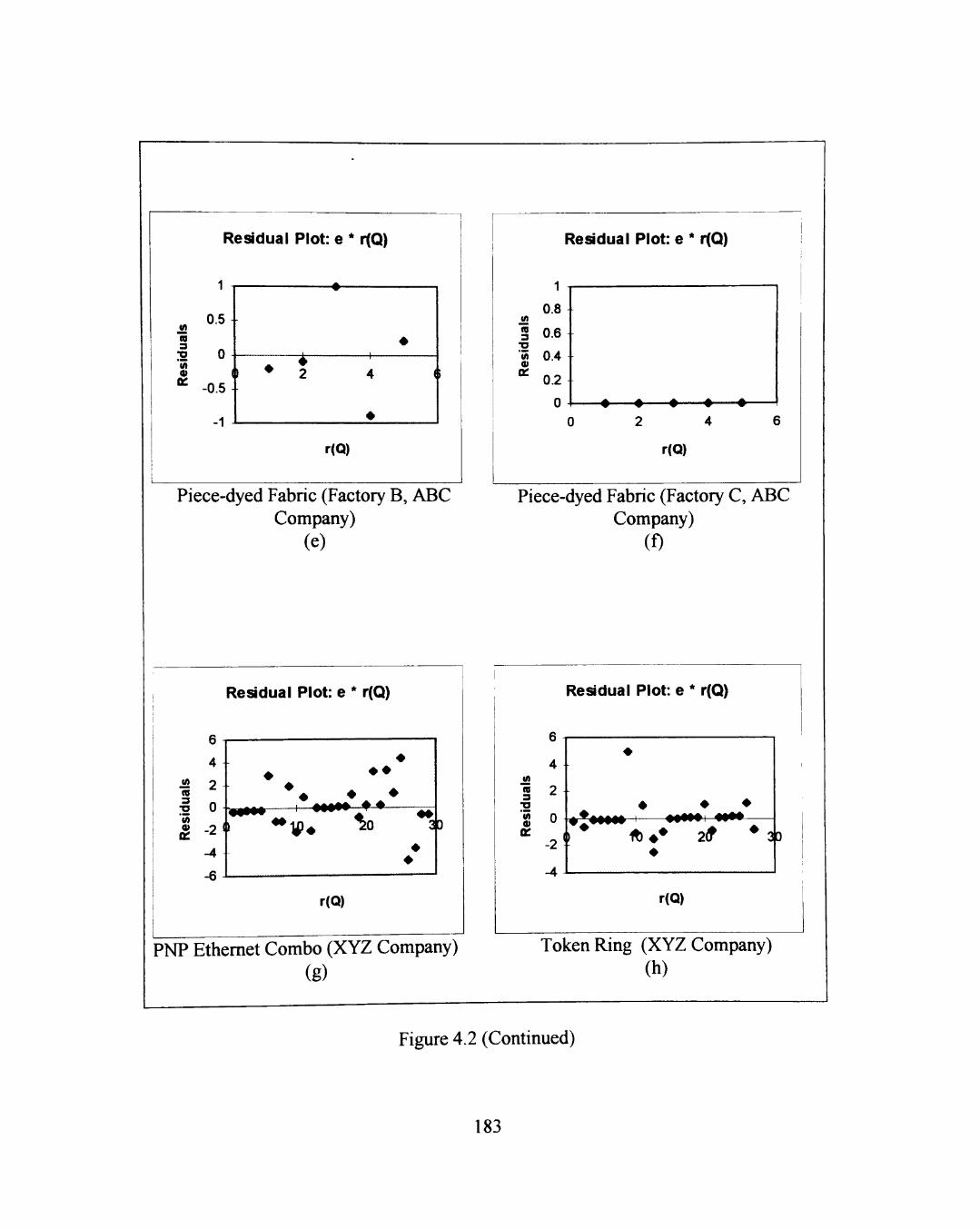

4.3.2.2.2.1 Plots: Residuals Against r(Q) ~ Check the Linearity and Constant Variance 181

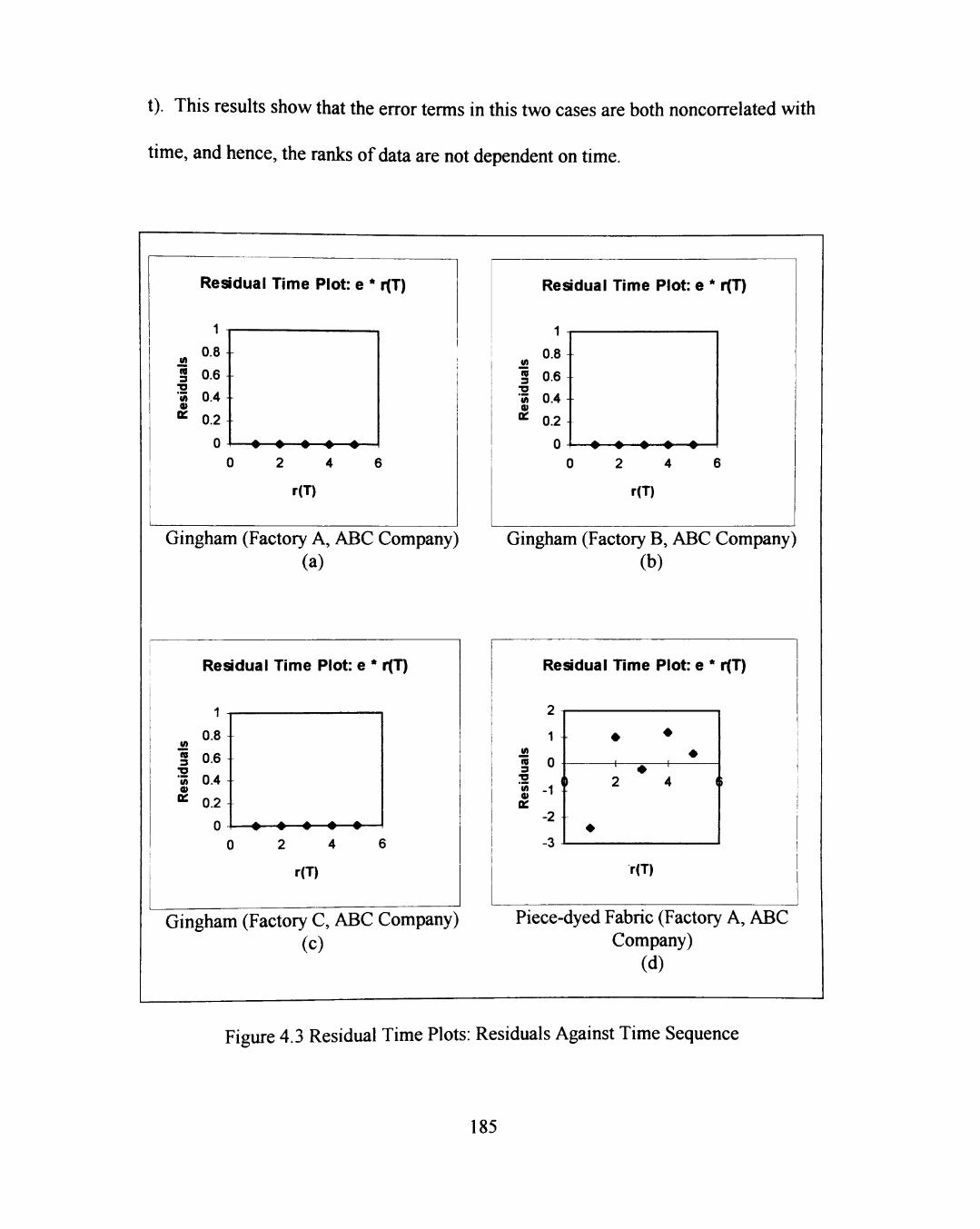

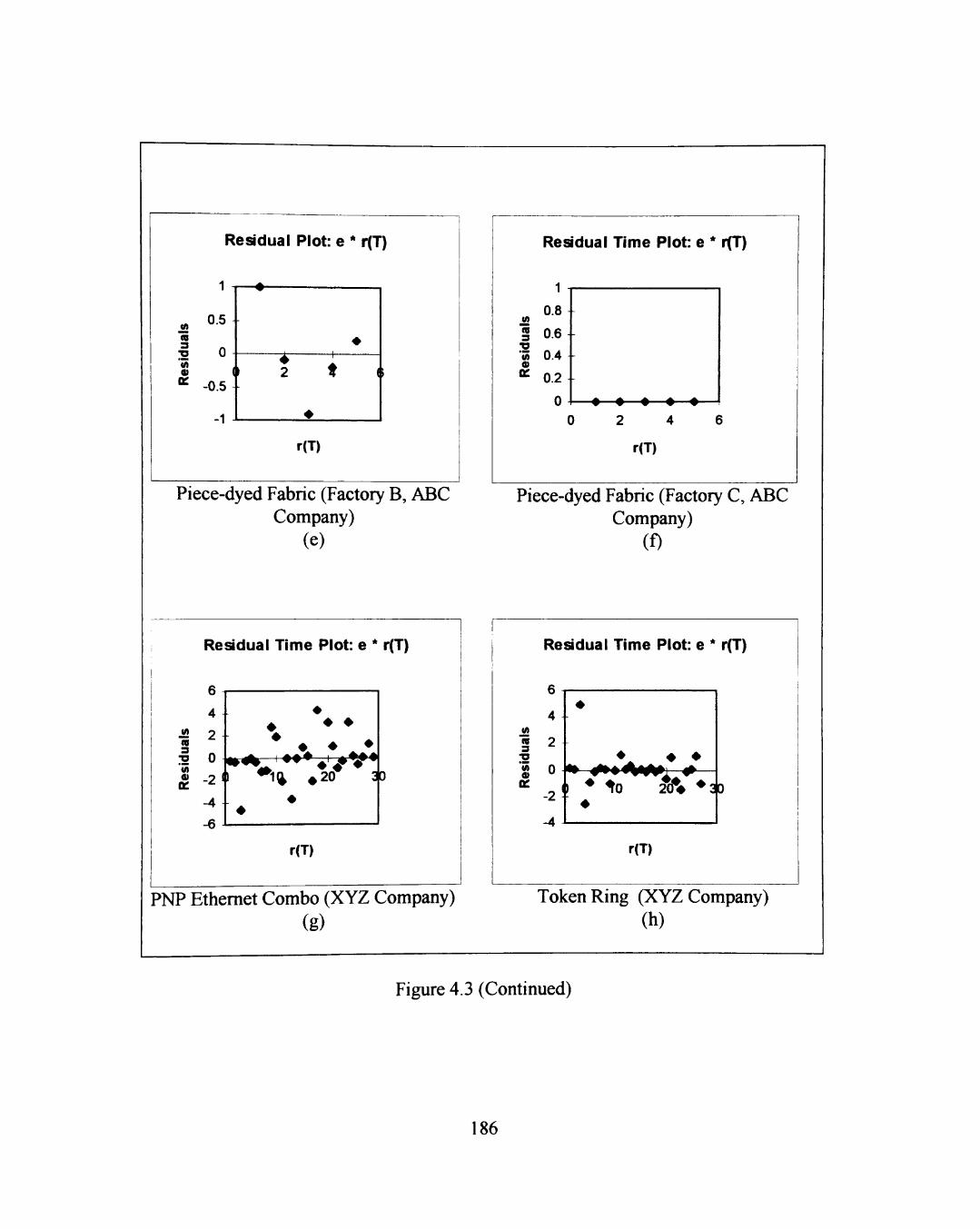

4.3.2.2.2.2 Plots: Residuals Against Time ~ Check the Nonindependence of Error Terms 184

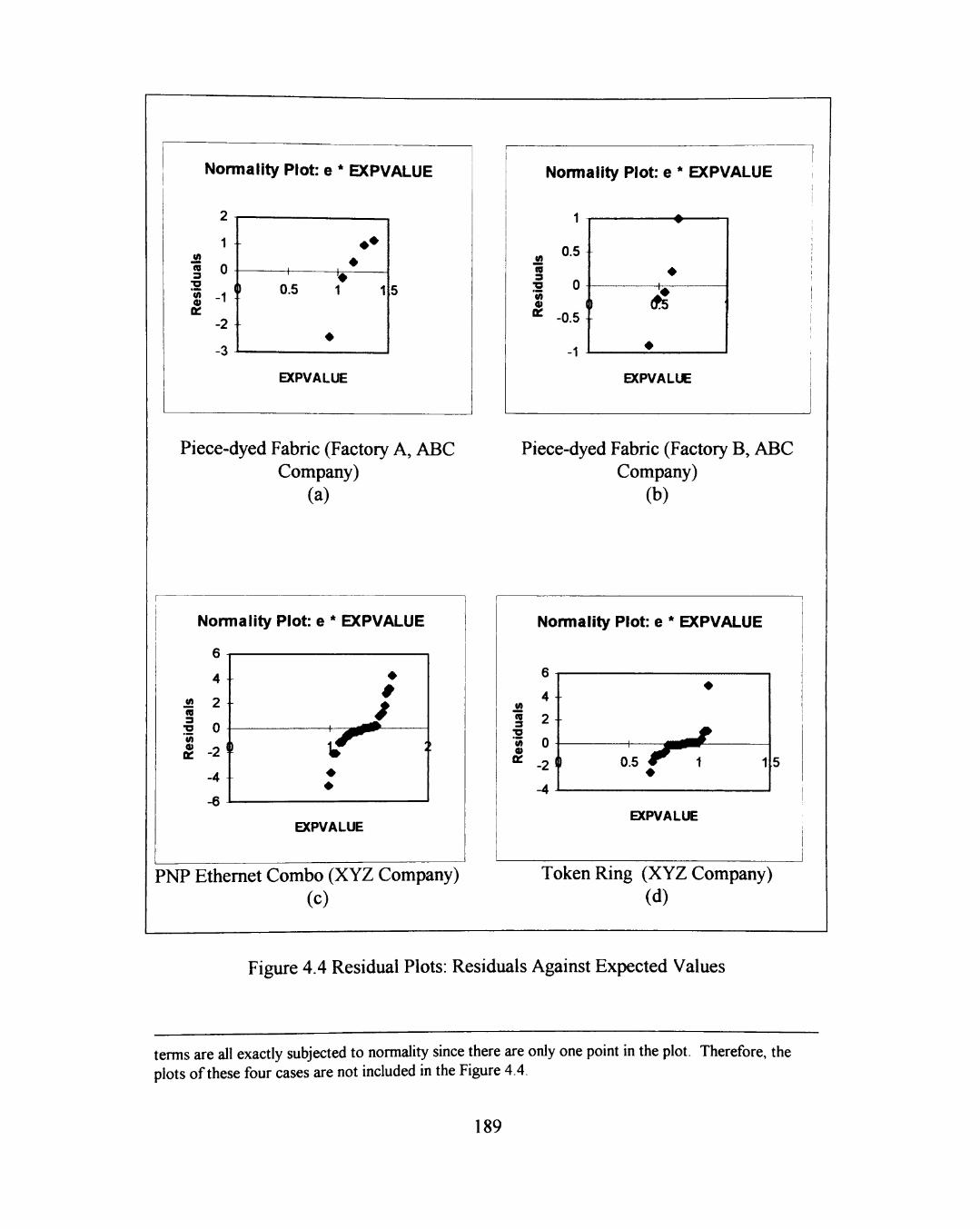

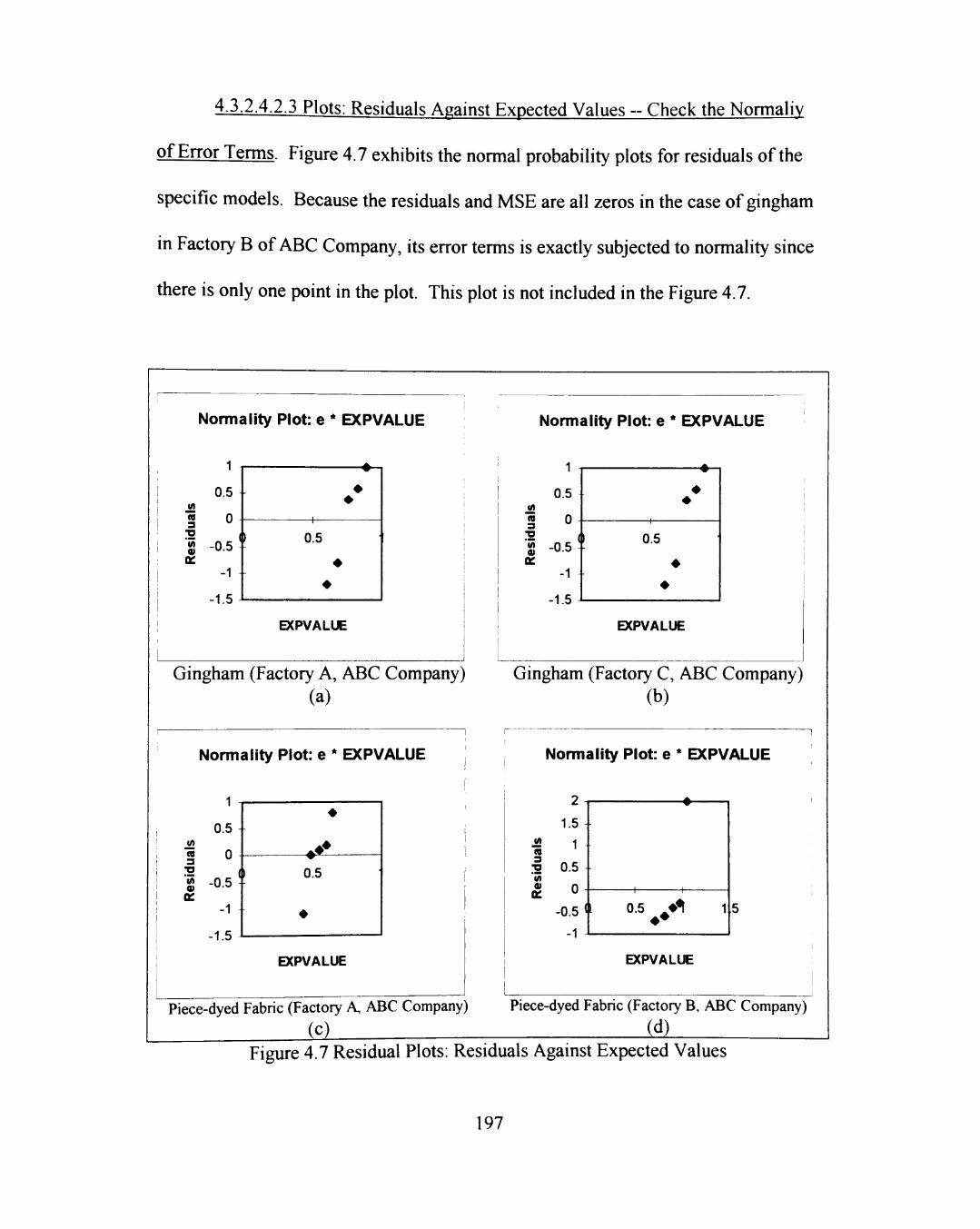

4.3.2.2.2.3 Plots: Residuals Against Expected Values ~ Check the Normality of Error Terms 188

4.3.2.3 Productivity-Profit Relationship Model Analysis 190

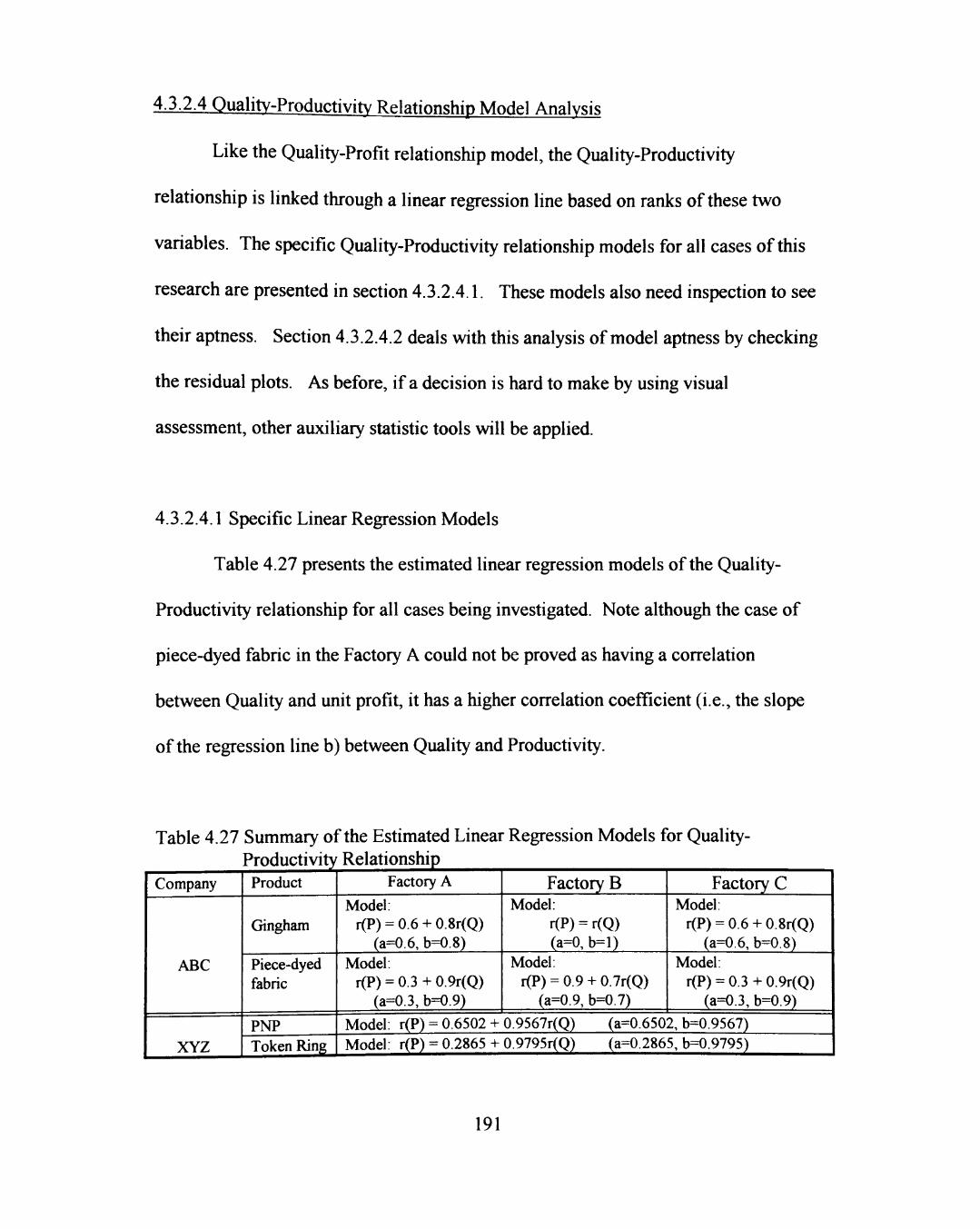

4.3.2.4 Quality-Productivity Relationship Model Analysis 191

4.3.2.4.1 Specific Linear Regression Models 191

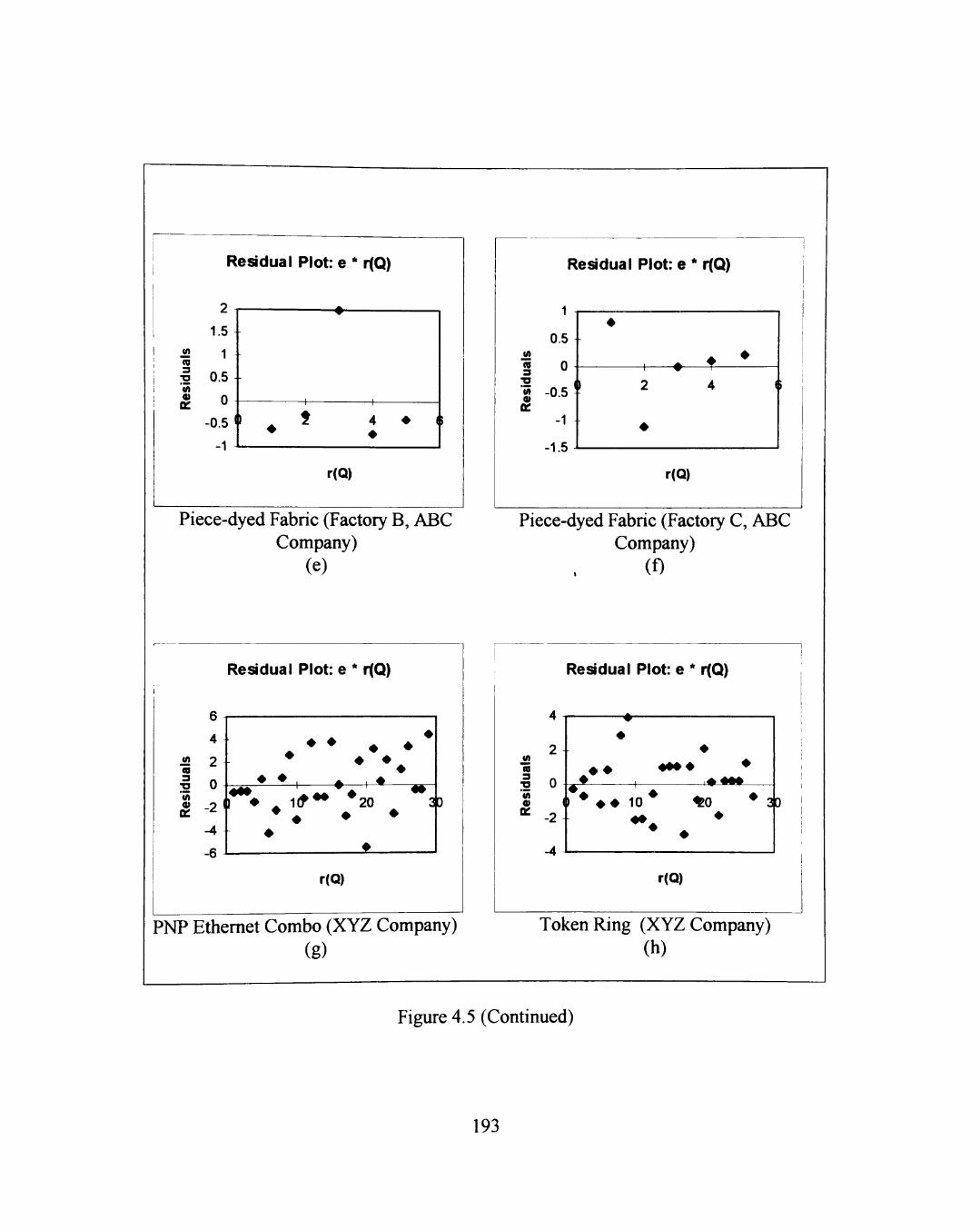

4.3.2.4.2 Residual Plots 192

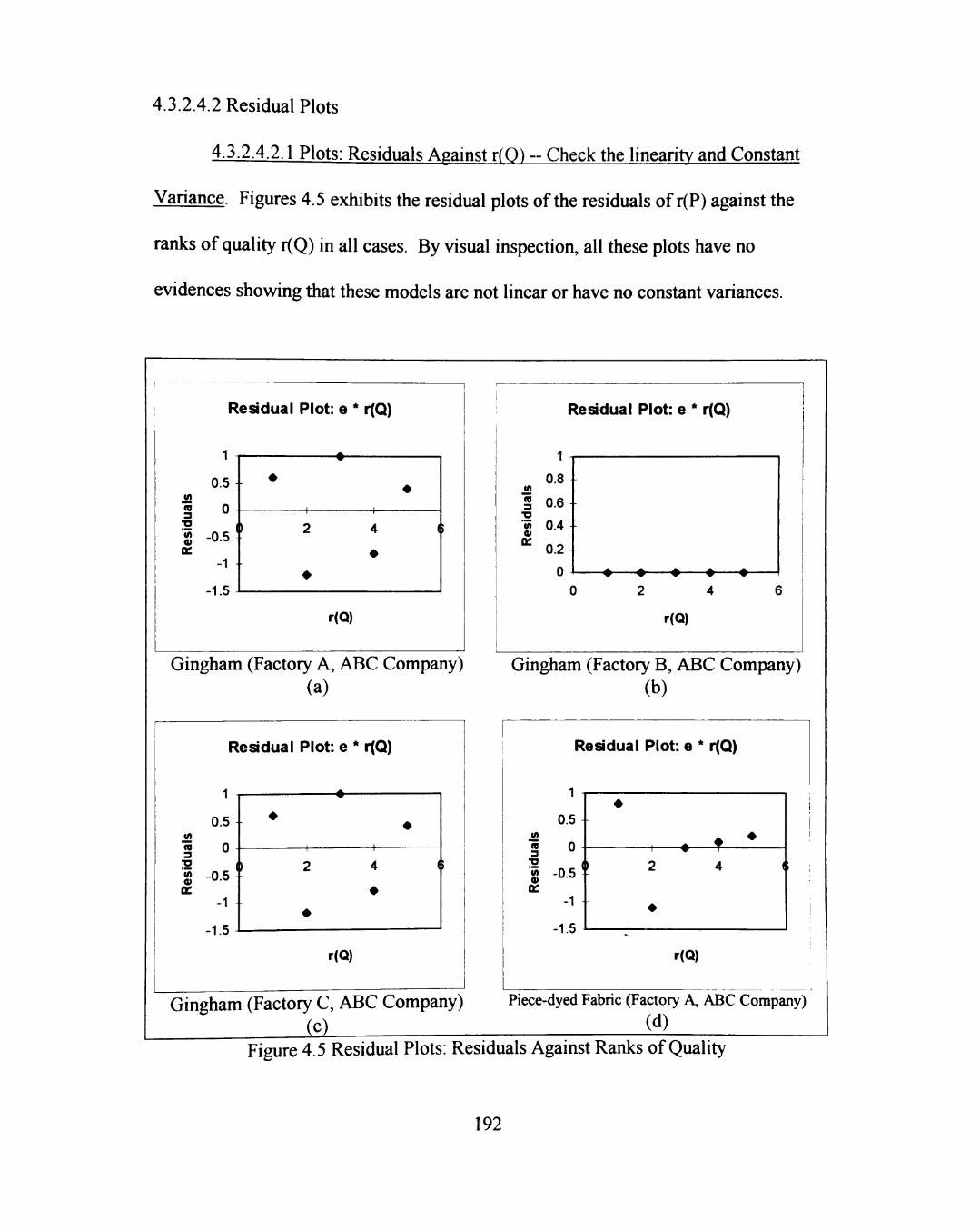

4.3.2.4.2.1 Plots: Residuals Against r(Q) ~ Check the Linearity and Constant Variance 192

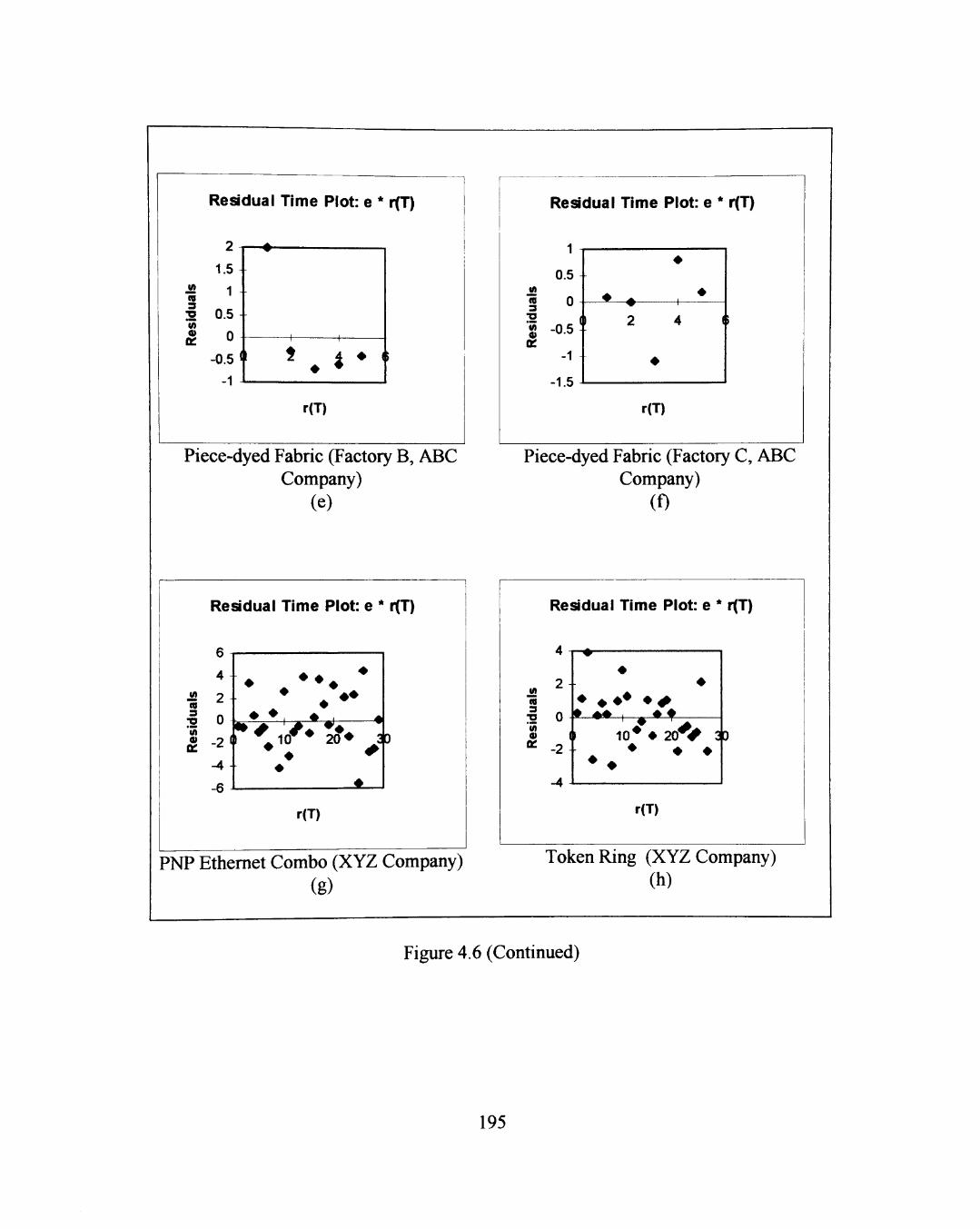

4.3.2.4.2.2 Plots: Residuals Against Time ~ Check the nonindependence of Error Terms 194

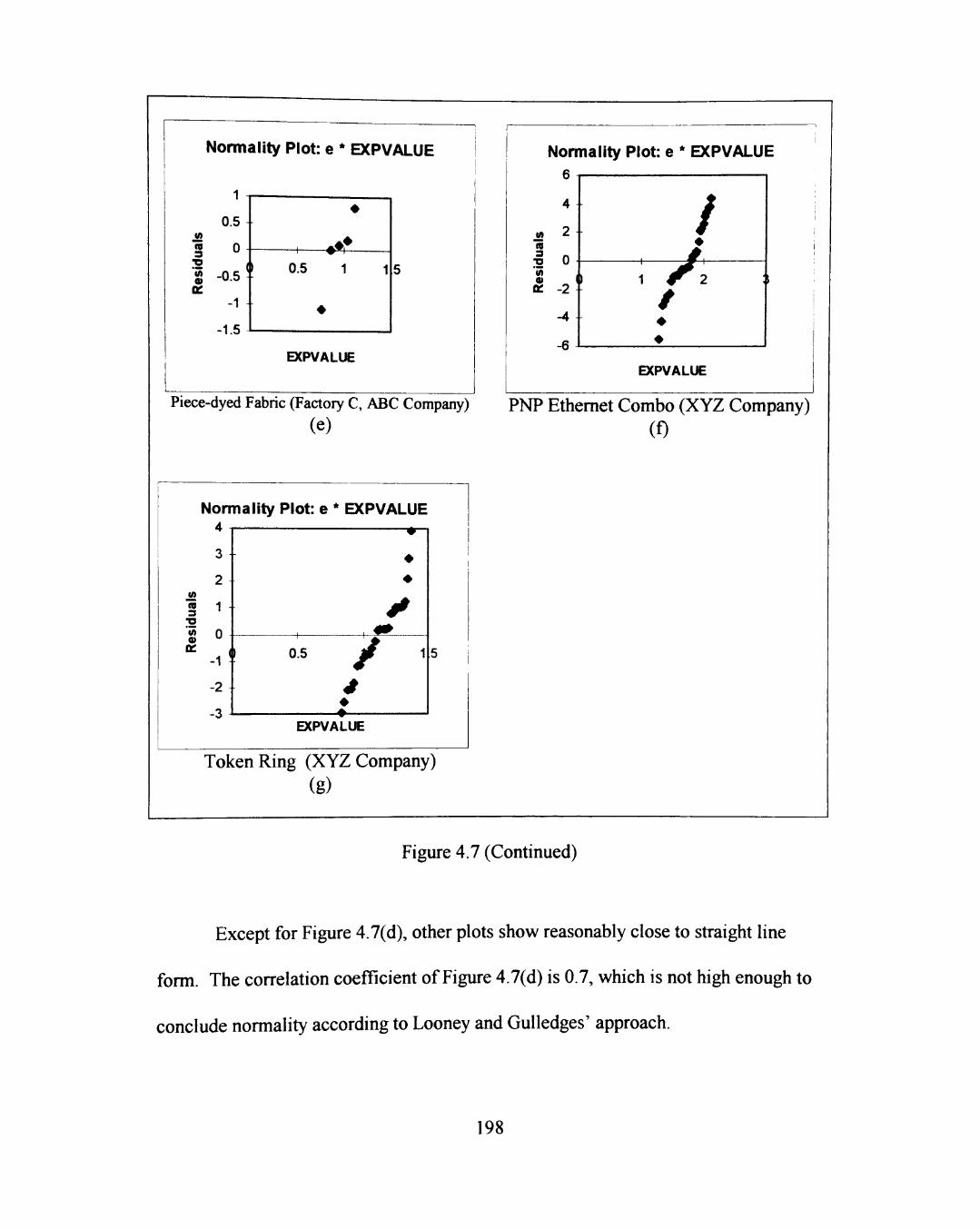

4.3.2.4.2.3 Plots: Residuals Against Expected Values ~ Check the Normality of Error Terms 197

IX

4.4 General Discussion 199

4.4.1 Discussion of Quality-Profit Relationship 199

4.4.2 Discussion of Productivity-Profit Relationship 200

4.4.3 Discussion of Quality-Productivity Relationship 202

4.4.4 Discussion of Data 204

5. CONCLUSIONS AND RECOMMENDATIONS 205

5.1 Summary 205

5.2 Further Discussion and Implications 208

5.2.1 Further Discussion 208

5.2.2 Implications 209

5.3 Conclusions 211

5.4 Recommendations 212

5.4.1 Theoretical Recommendations 212

5.4.2 Practical Recommendations 213

BIBLIOGRAPHY 214

APPENDIX

A: MATHEMATICAL MODELS DEVELOPMENT 234

B: QUALITY INSPECTION POINTS IN ABC AND XYZ COMPANIES 243

C. TABLE FOR THE SPEARMAN'S RHO TEST 246

D: RESULTS OF THE LILLEEFORS NORMALITY TESTS 248

E: A PROOF FOR THE RELATIONSHIP BETWEEN SLOPE OF A REGRESSION LINE BASED ON RANKS AND ITS CORRELATION 261

X

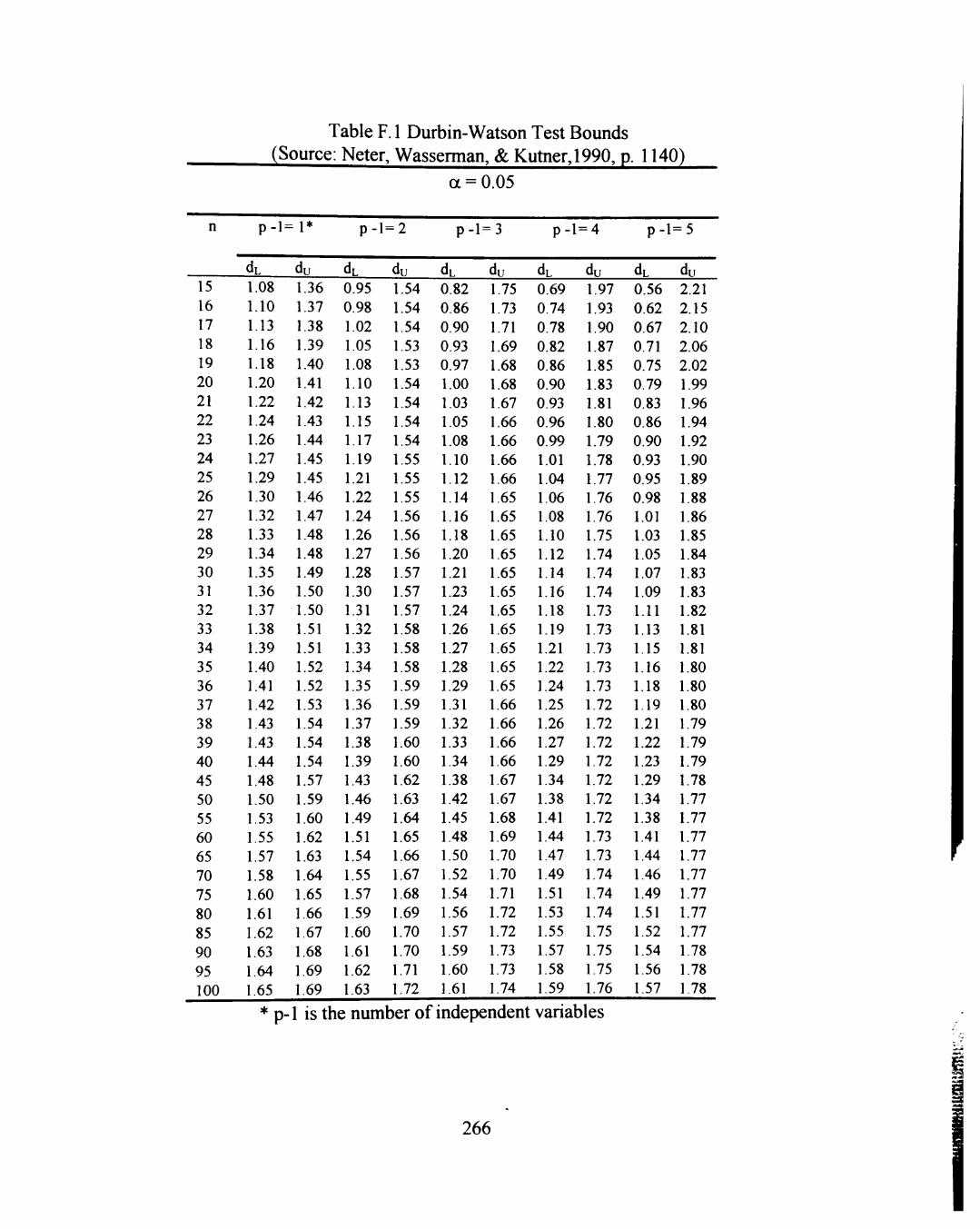

F: THE DURBIN-WATSON TEST PROCEDURE AND ITS TABLE 264

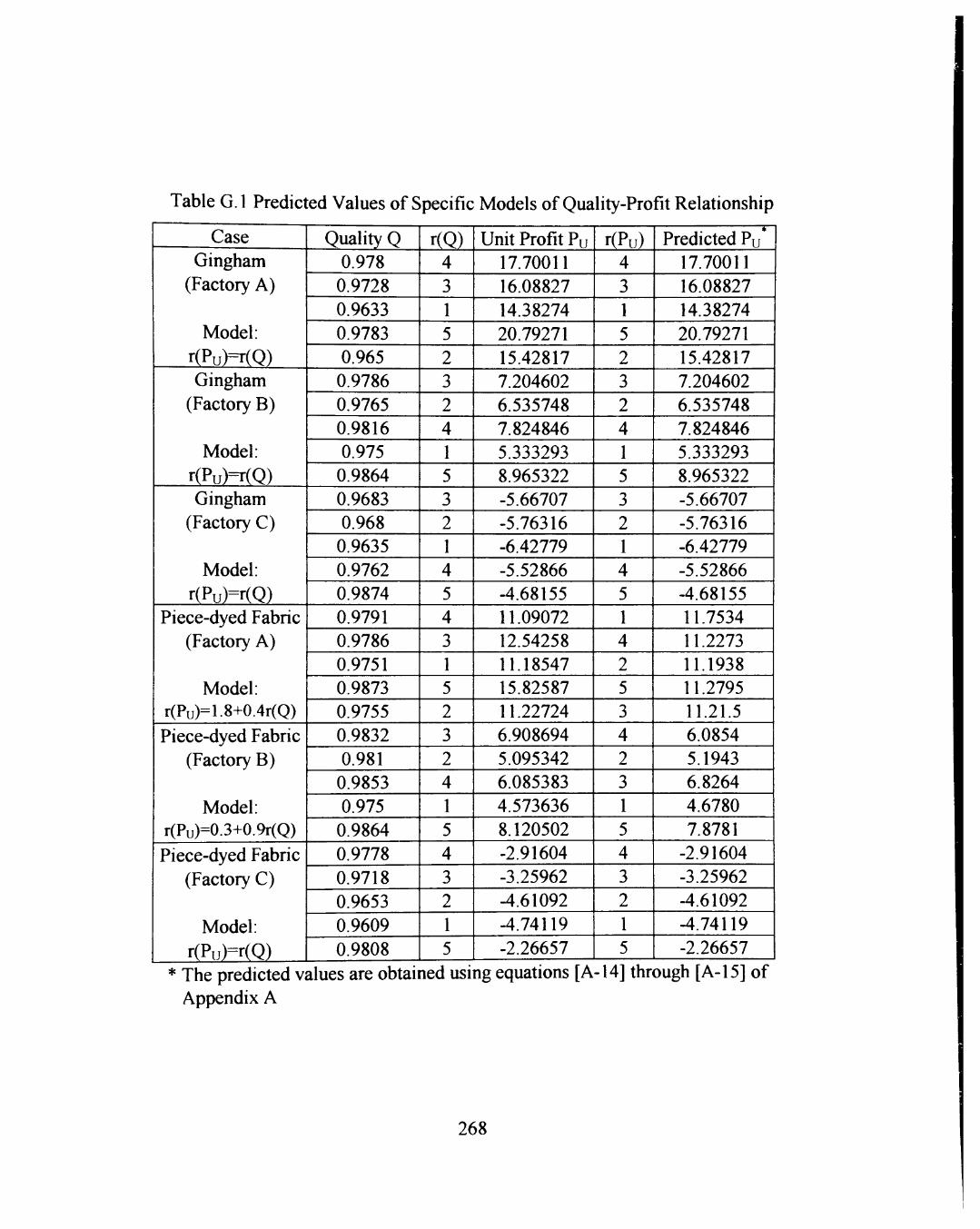

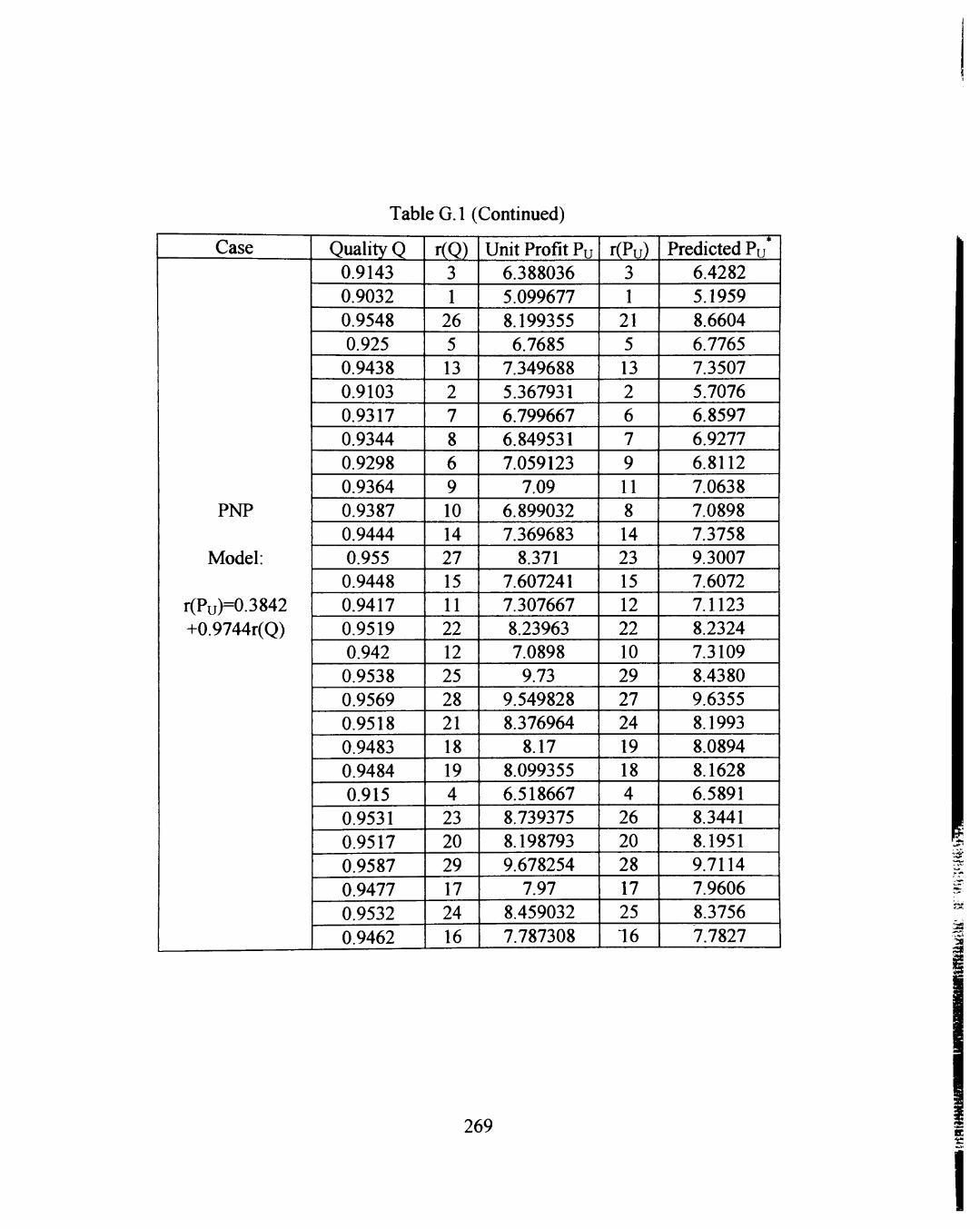

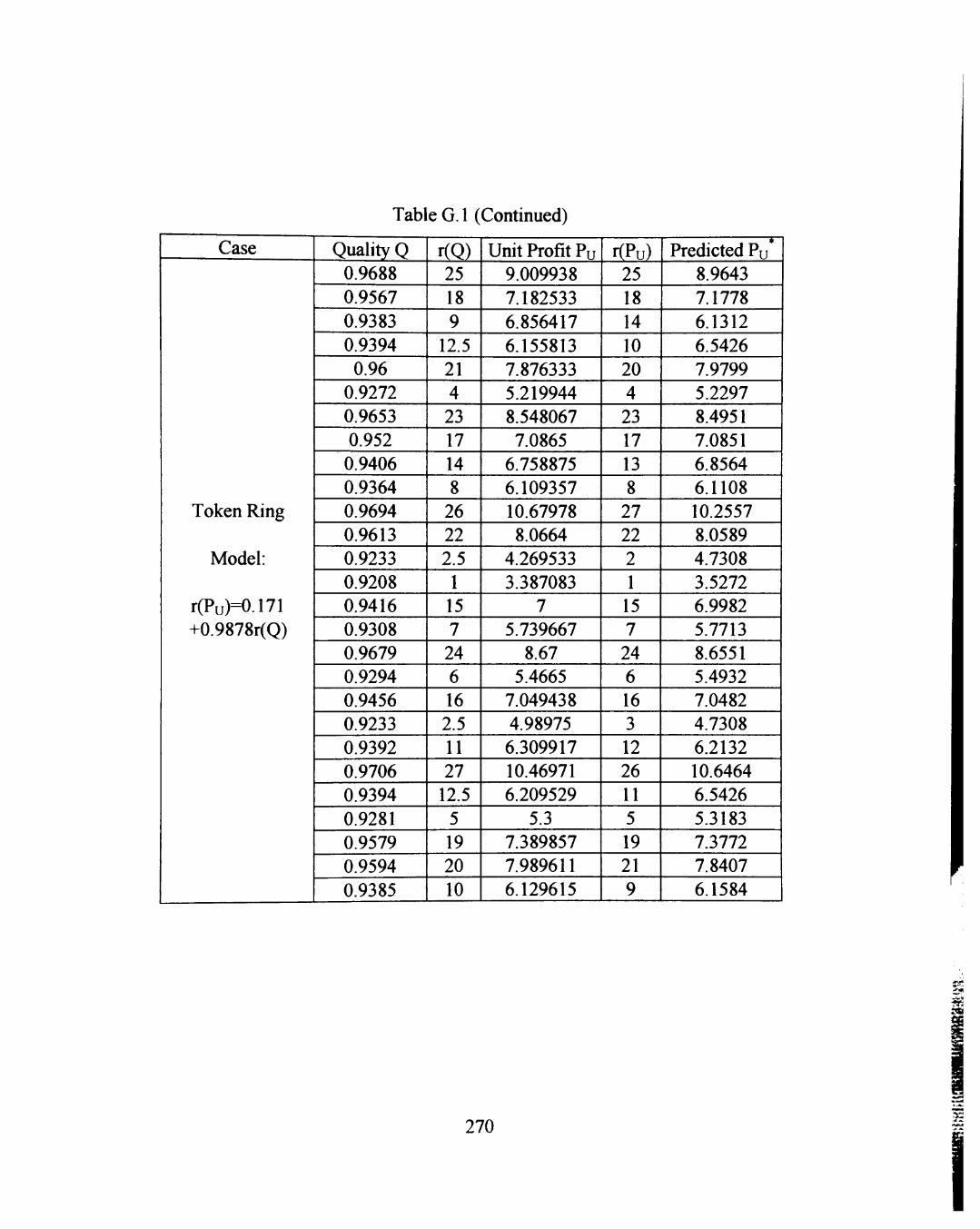

G: PREDICTED VALUES OF SPECIFIC MODELS OF QUALITY-PROFIT RELATIONSHIP 267

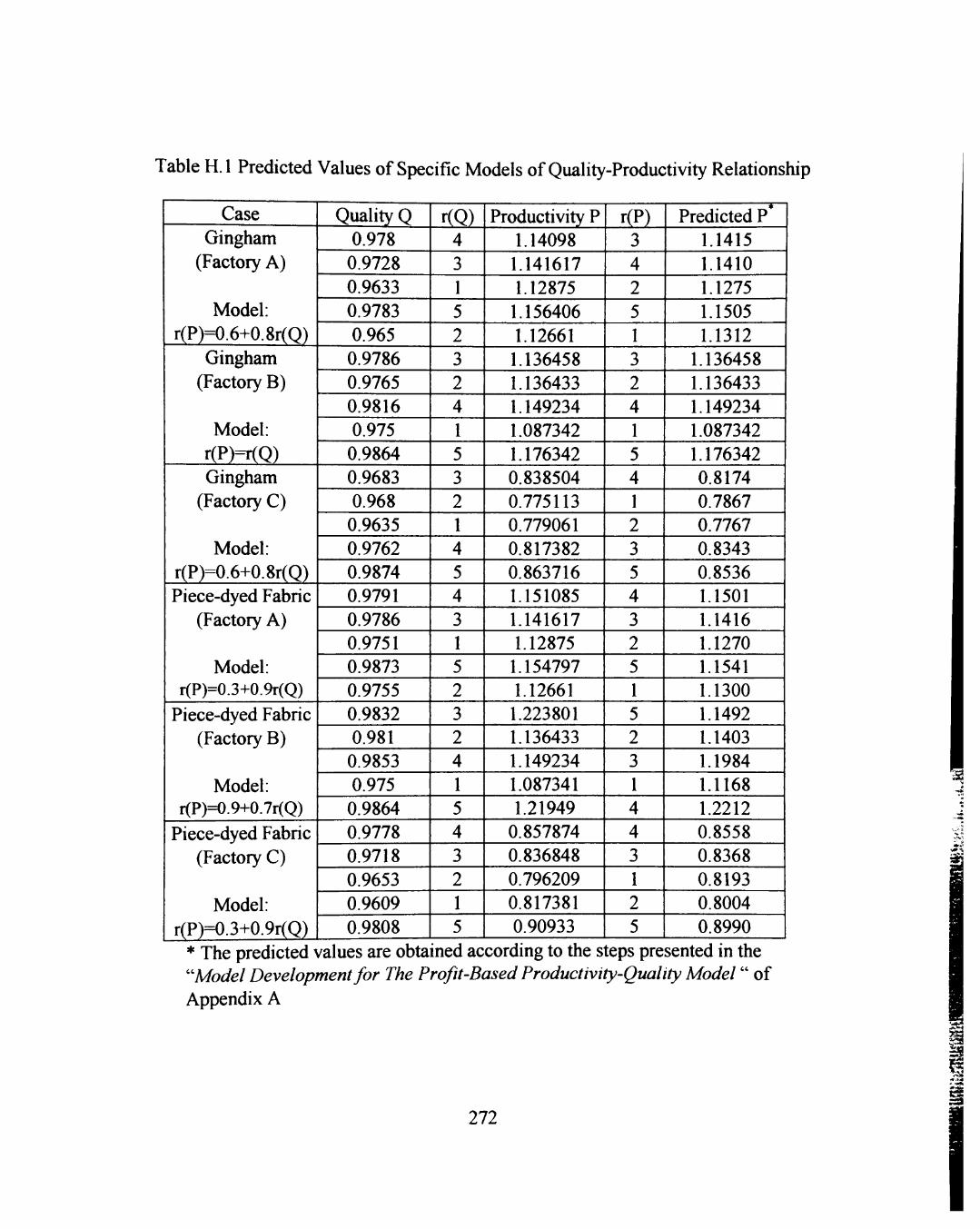

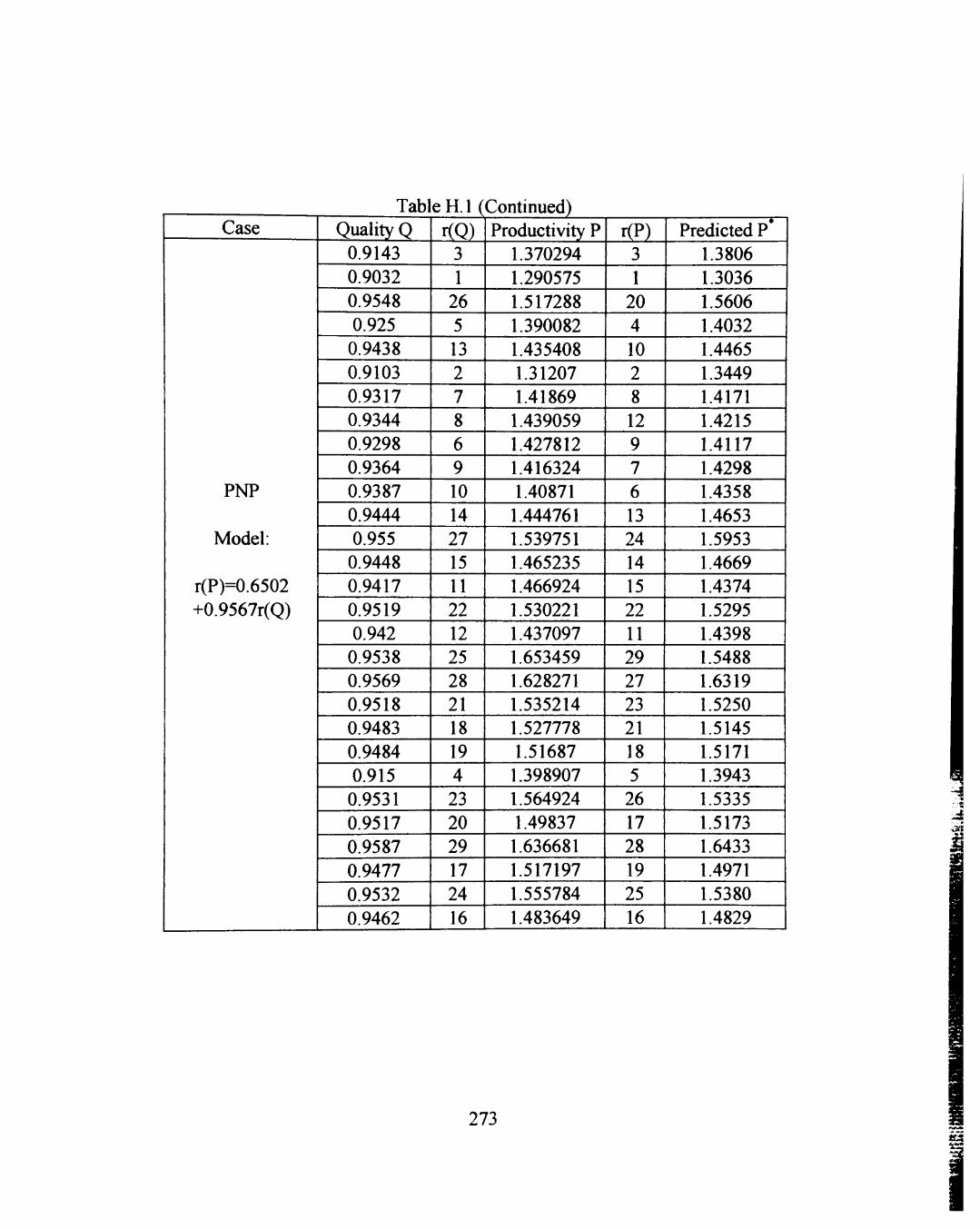

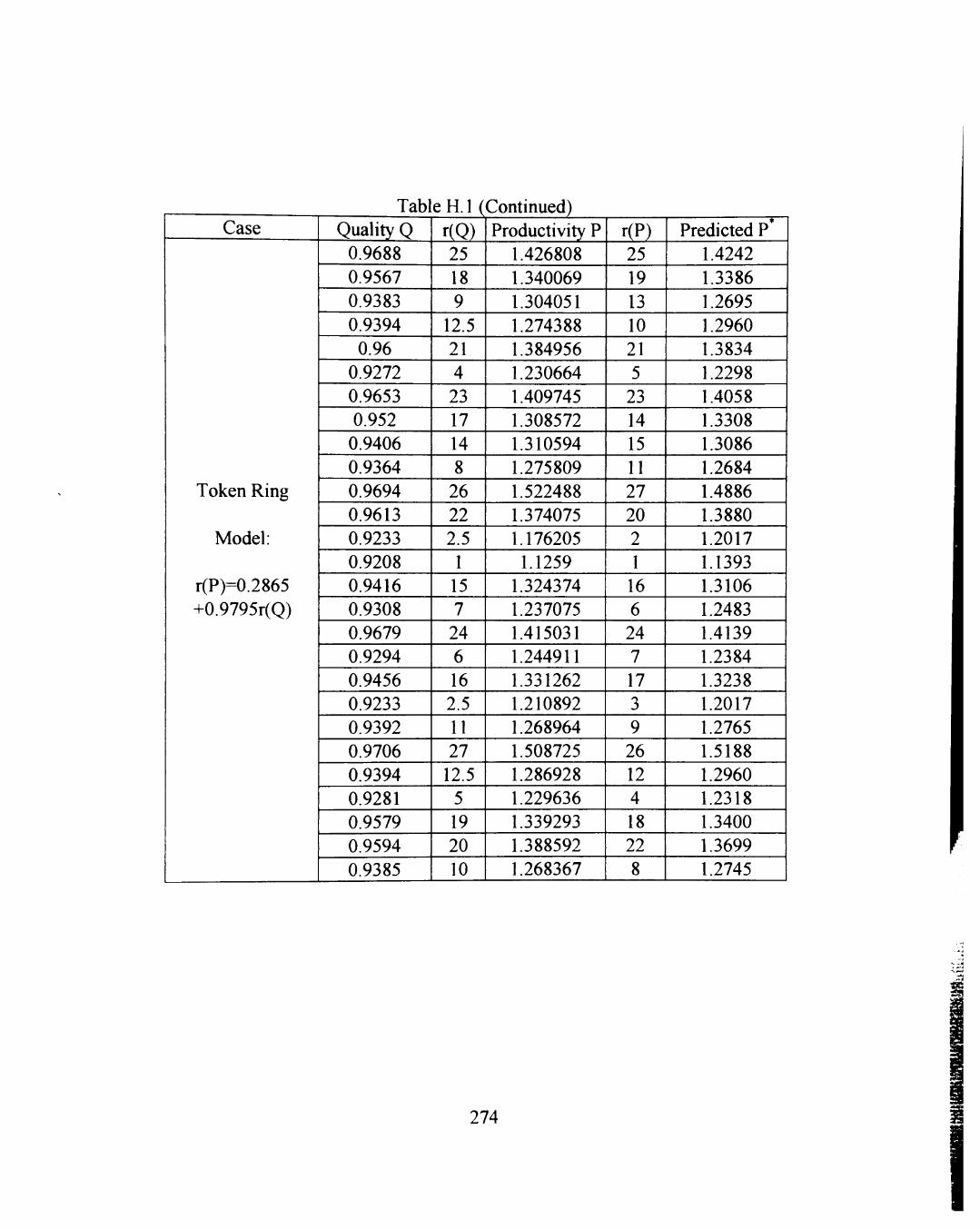

H: PREDICTED VALUES OF SPECIFIC MODELS OF QUALITY-PRODUCTIVITY RELATIONSHIP 271

XI

LIST OF TABLES

2.1 Definitions ofproductivity in the open literature 38

2.2 Definitions of quality in the open literature 44

2.3 Definitions of profitability and profit in the open literature 50

2.4 Comparison of QPR Values When Unit Reject Processing Cost Significantly Decreases 92

4.1 Definitions of Quality and Productivity in the ABC and XYZ Companies 153

4.2 Production Cost Data of Gingham in the ABC Company 157

4.3 Production Cost Data of Piece-dyed Fabric in the ABC Company 157

4.4 Production Cost Data of Token Ring in the XYZ Company 157

4.5 Production Cost Data of PNP Ethernet Combo in the XYZ Company 158

4.6 Revenue Data of Gingham in the ABC Company 158

4.7 Revenue Data of Piece-dyed Fabric in the ABC Company 159

4.8 Revenue Data of Token Ring in the XYZ Company 159

4.9 Revenue Data of PNP Ethernet Combo in the XYZ Company 159

4.10 Profit Data of Gingham in the ABC Company 160

4.11 Profit Data of Piece-dyed Fabric in the ABC Company 160

4.12 Profit Data of Token Ring in the XYZ Company 161

4.13 Profit Data of PNP Ethernet Combo in the XYZ Company 162

4.14 Quality Conformance Level of Gingham in the ABC Company 163

4.15 Quality Conformance Level of Piece-dyed Fabric in the ABC Company 163

Xll

4.16 Quality Conformance Level of Token Ring in the XYZ Company 163

4.17 Quality Conformance Level of PNP Ethernet Combo in the XYZ Company.. 164

4.18 Productivity Data of Gingham in the ABC Company 164

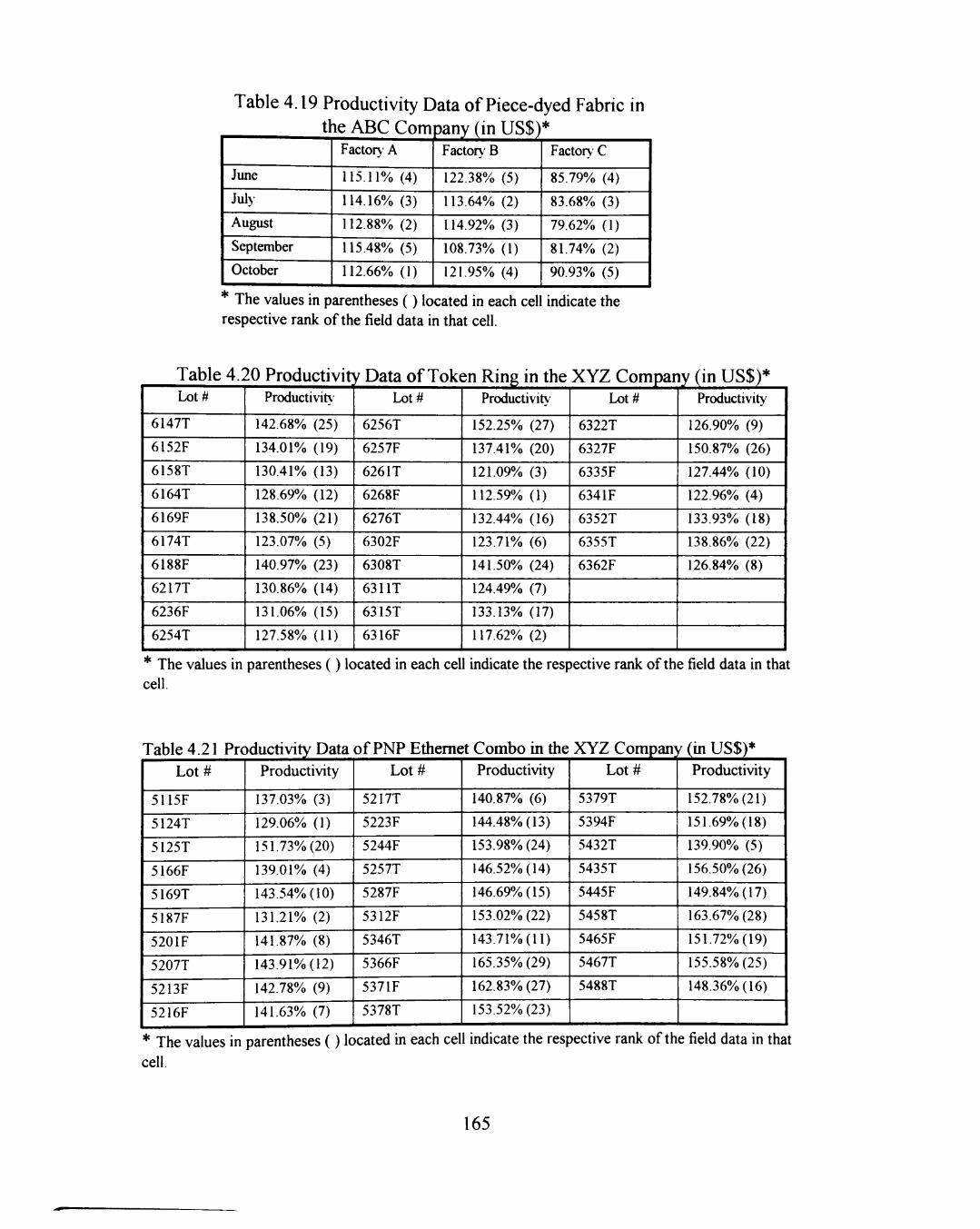

4.19 Productivity Data of Piece-dyed Fabric in the ABC Company 165

4.20 Productivity Data of Token Ring in the XYZ Company 165

4.21 Productivity Data of PNP Ethernet Combo in the XYZ Company 165

4.22 Summary of Spearman's Rho Test Results for Quality-Profit Relationship 170

4.23 Summary of Spearman's Rho Test Results for Productivity-Profit Relationship 173

4.24 Summary of Spearman's Rho Test Results for Quality-Productivity Relationship 176

4.25 Summary of the Estimated Linear Regression Models for Quality-Profit Relationship 181

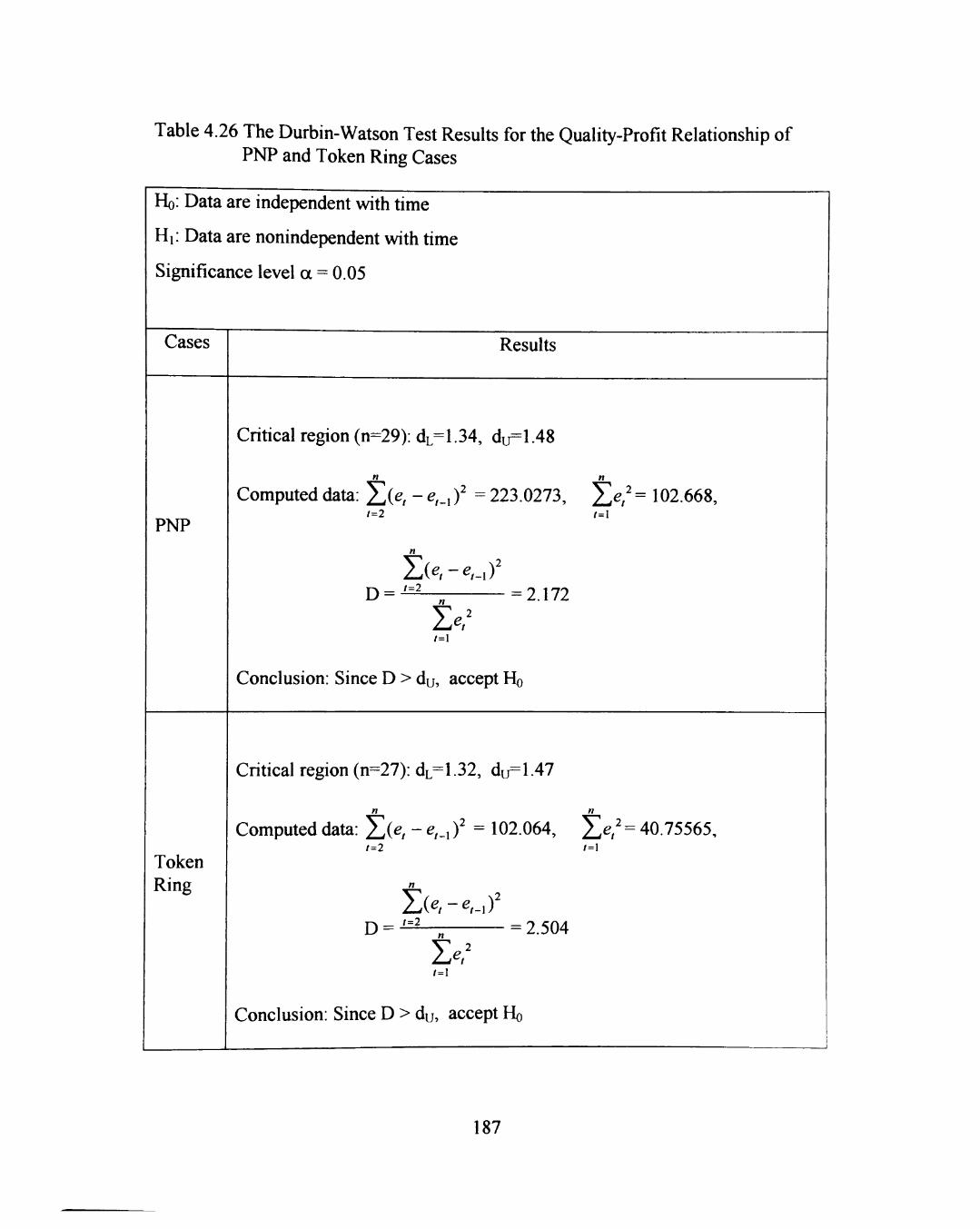

4.26 The Durbin-Watson Test Results for the Quality-Profit Relationship of PNP and Token Ring Cases 187

4.27 Summary of the Estimated Linear Regression Models for Quality-Productivity Relationship 191

4.28 The Durbin-Watson Test Results for the Quality-Productivity Relationship of PNP and Token Ring Cases 196

5.1 Summary of Mathematical Models of This Research 207

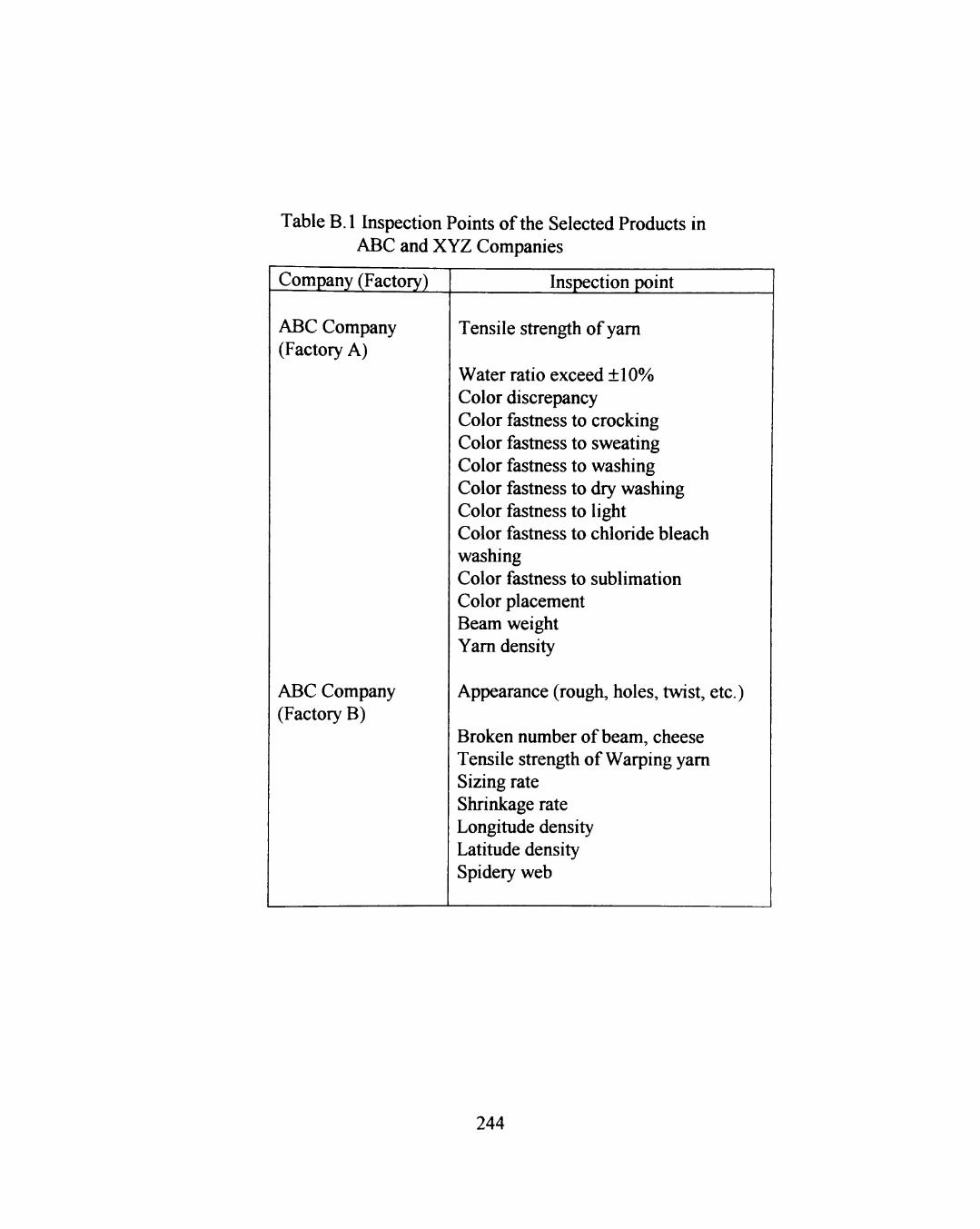

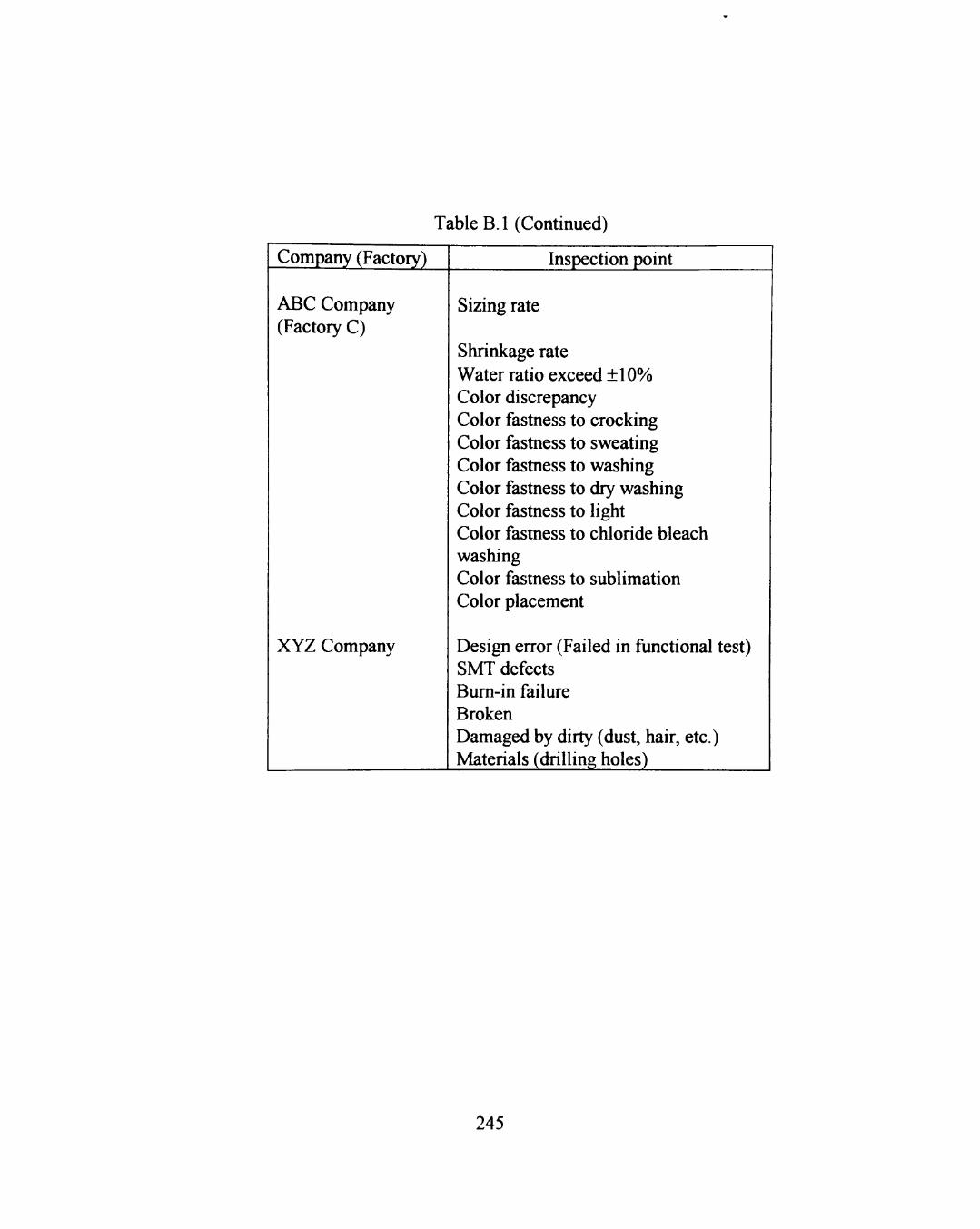

B.l Quality Inspection Points in ABC and XYZ Companies 244

C. 1 Quantiles of the Spearman Test Statistic 247

F.l Durbin-Watson Test Bounds 266

G.l Predicted Values of Specific Models of Quality-Profit Relationship 268

H. 1 Predicted Values of Specific Models of Quality-Productivity Relationship 272

xiu

LIST OF FIGURES

2.1 Model for Optimum Quality Costs 54

2.2 New model for Optimum Quality Costs 55

2.3 Dawes'Quality-Cost Model 56

2.4 Effect of varying controllable PQC 58

2.5 Taguchi's Quality Loss Function 59

2.6 The Relationship between Profits and Input Costs 66

2.7 Chain Reaction Related to Quality and Productivity 73

2.8 A Framework for Understanding the Connection and Relationship between Productivity and Quality 74

2.9 Components of the PQMM 77

2.10 Process Quality and Productivity Are Essentially the Same 78

2.11 A Complete Productivity and Quality Measurement System 79

2.12 Costs of Non Quality and Quality Efforts as a Function of Quality of Conformance 82

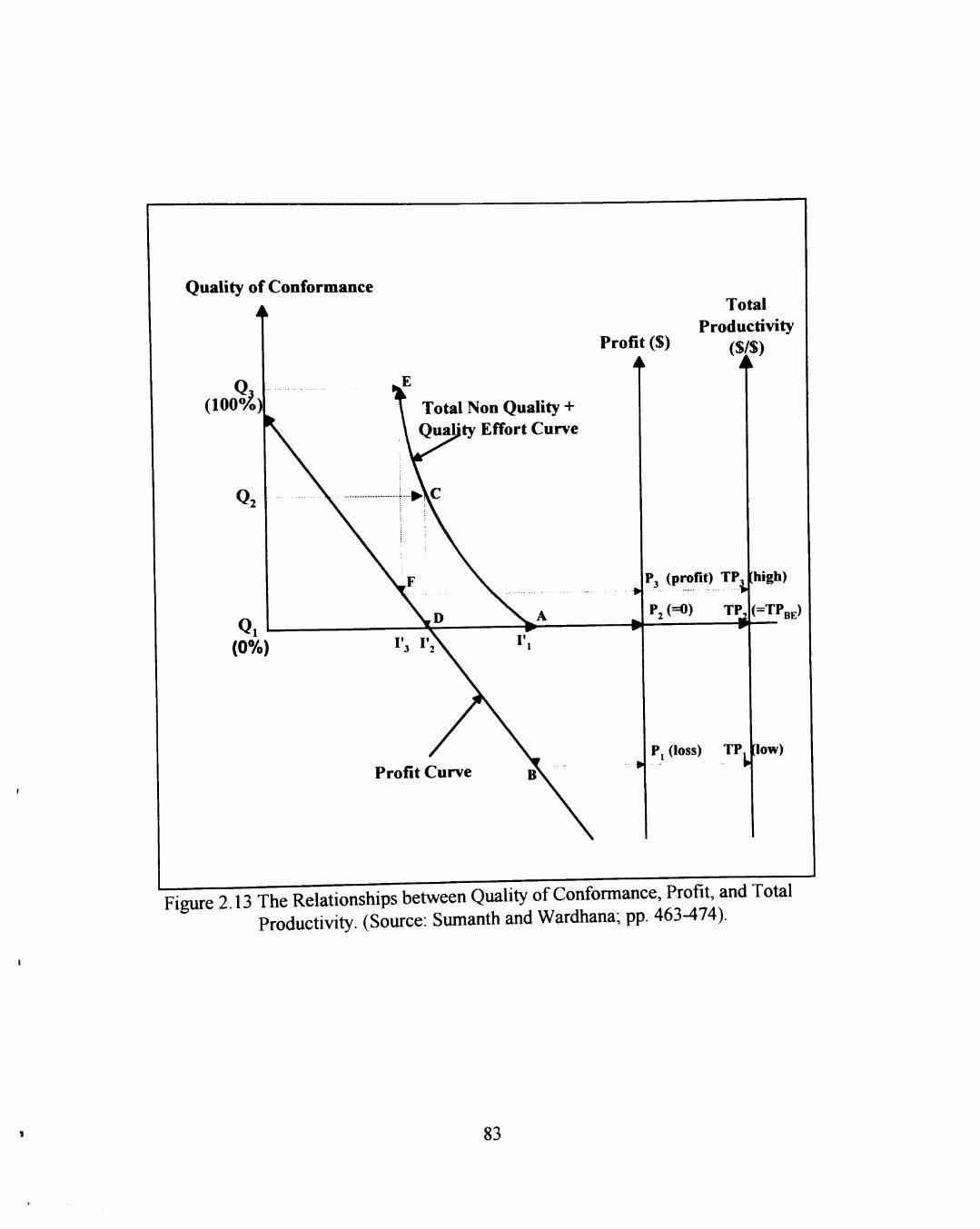

2.13 The Relationships between Quality of Conformance, Profit, and Total Productivity 83

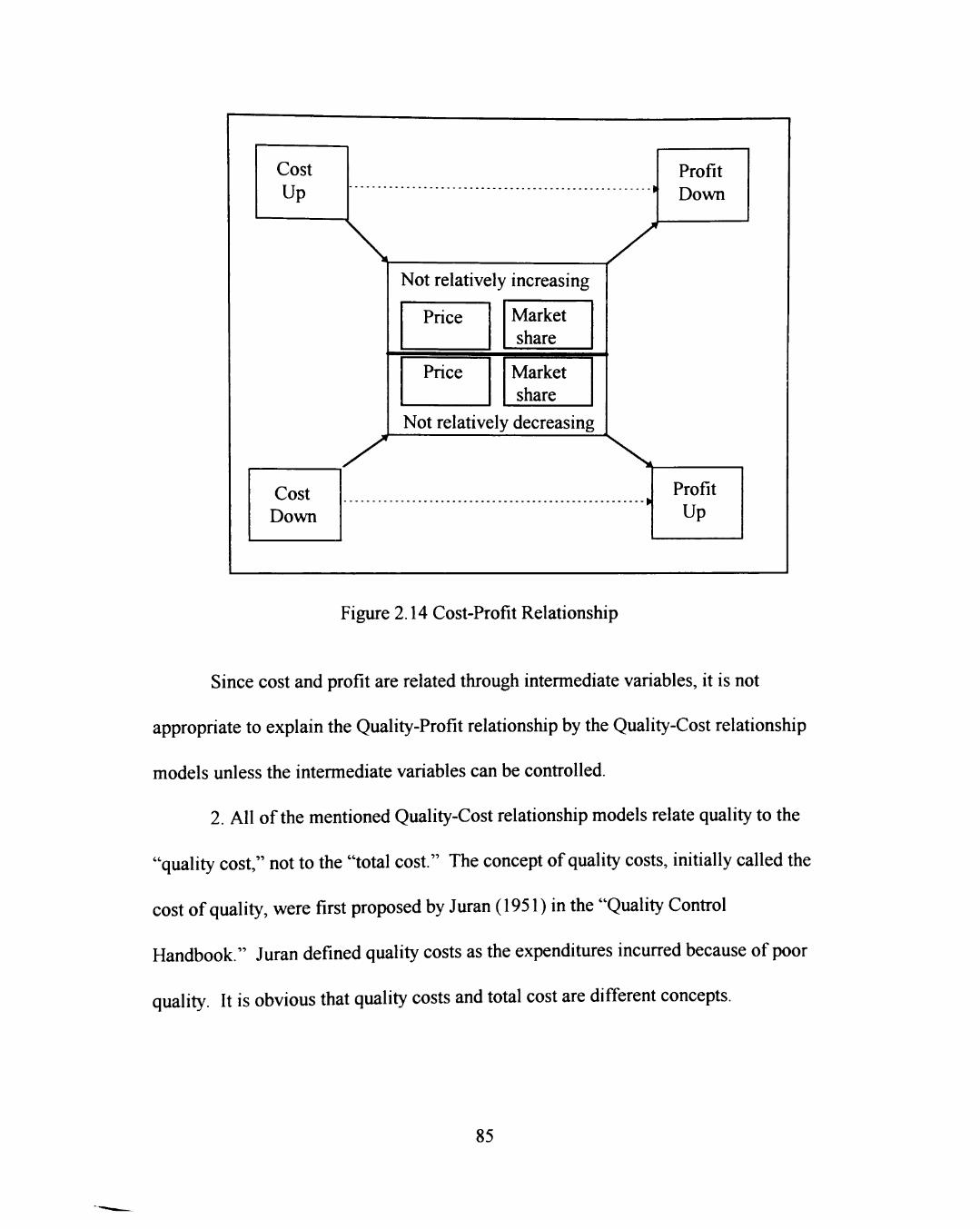

2.14 Cost-Profit Relationship 85

2.15 Price-Volume-Quality Relationship lOl

2.16 Revenue-Quality Relationship 101

2.17 Production Cost-Volume-Quality Relationship 102

2.18 Production Cost-Quality Relationship 103

XIV

2.19 Quality-Profit Relationship 105

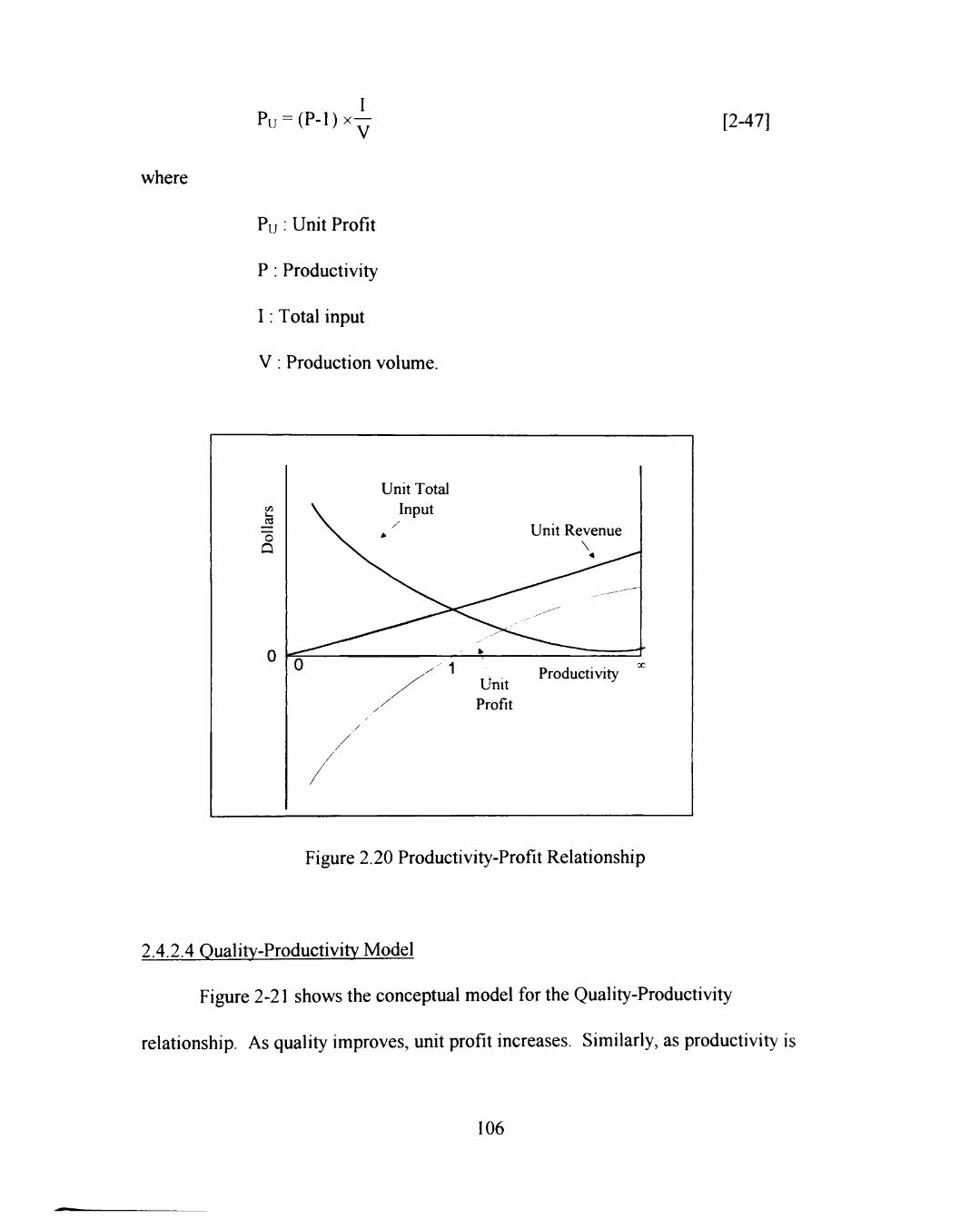

2.20 Productivity-Profit Relationship 106

2.21 Quality-Productivity Relationship 107

2.22 Conceptual Model of Linking Quality and Productivity 109

3.1 Research Process of This Study 117

3.2 Main Hypotheses of This Research 121

3.3 Sub-Hypotheses of This Research 122

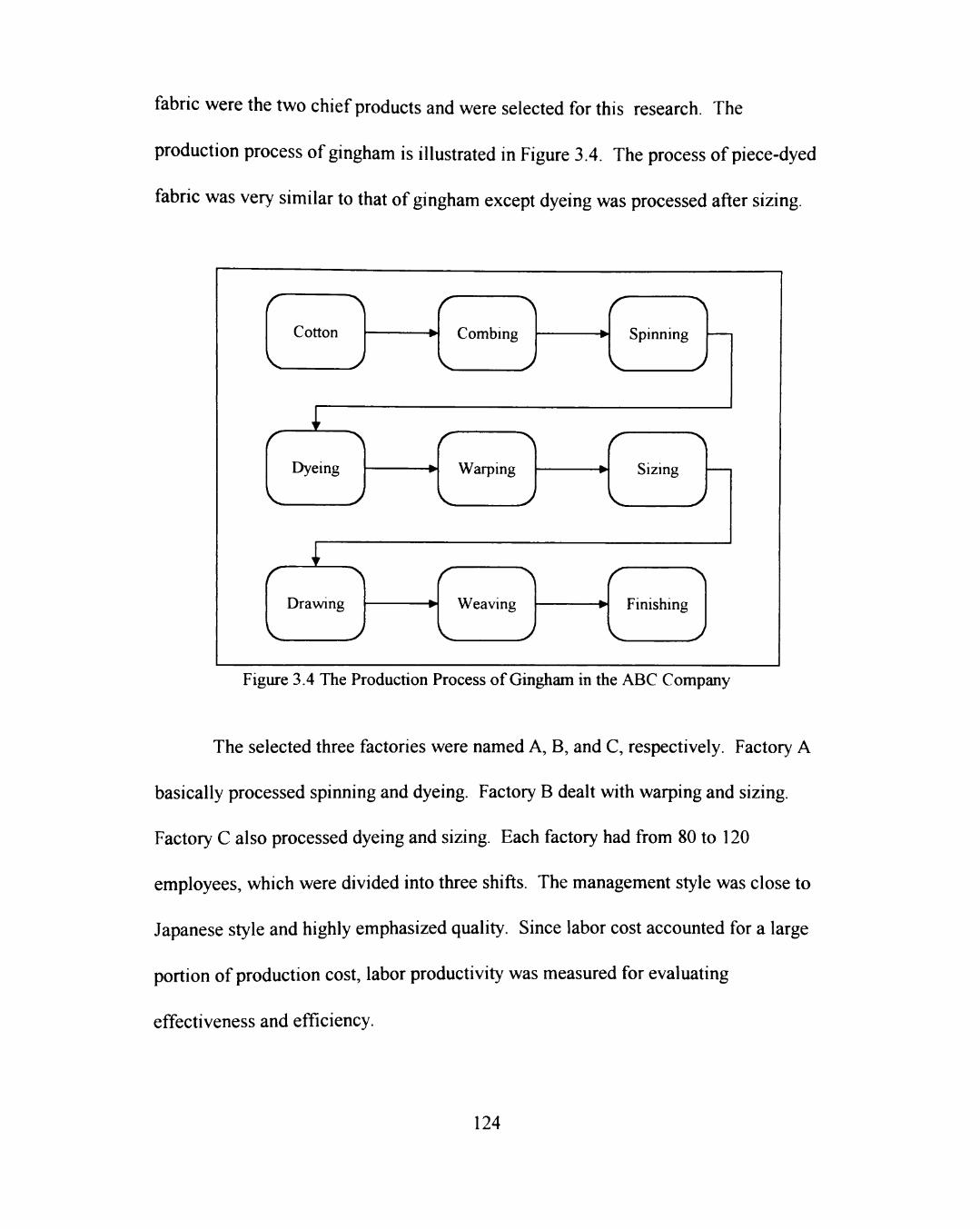

3.4 The Production Process of Gingham in the ABC Company 124

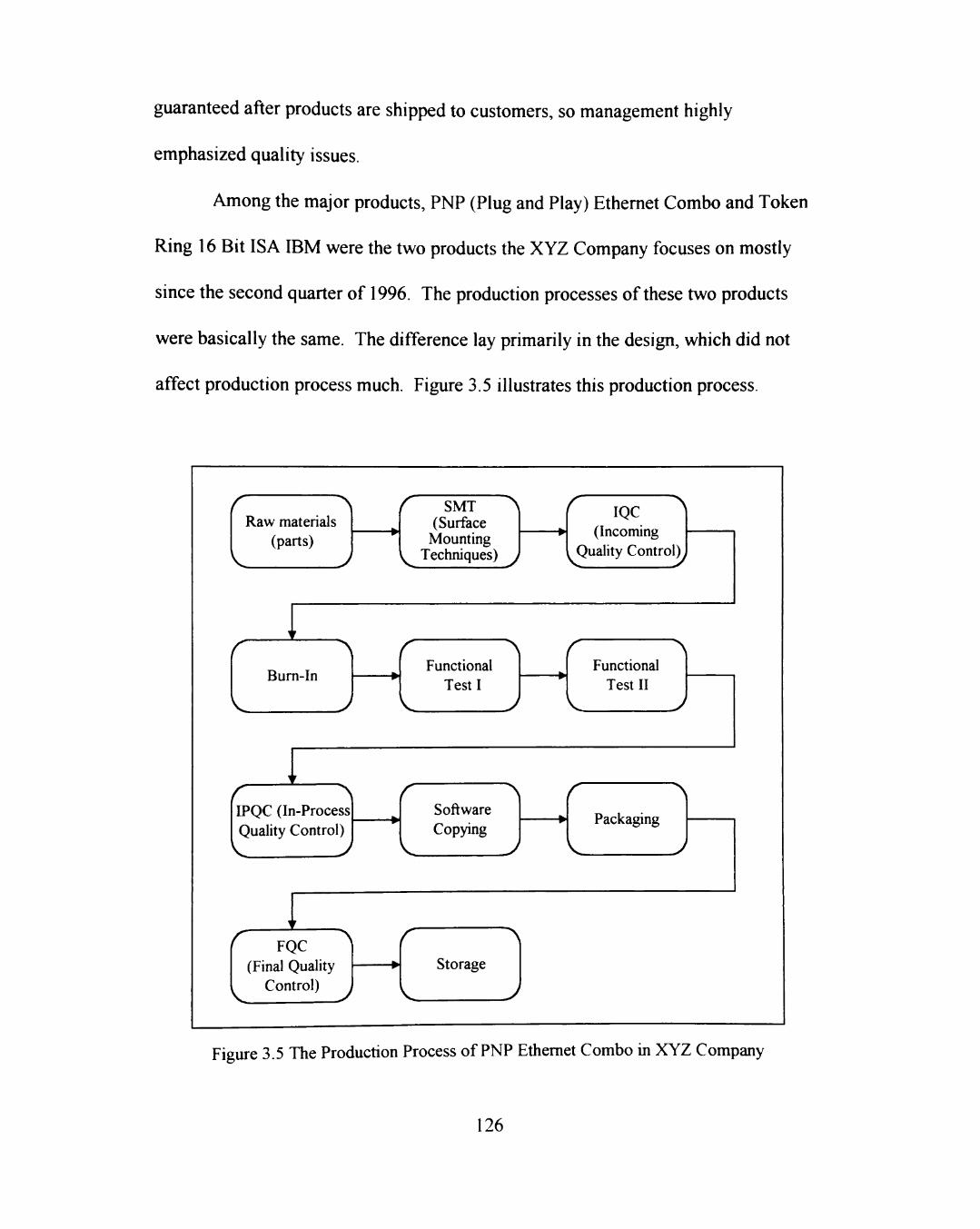

3.5 The Production Process of PNP Ethernet Combo in XYZ Company 126

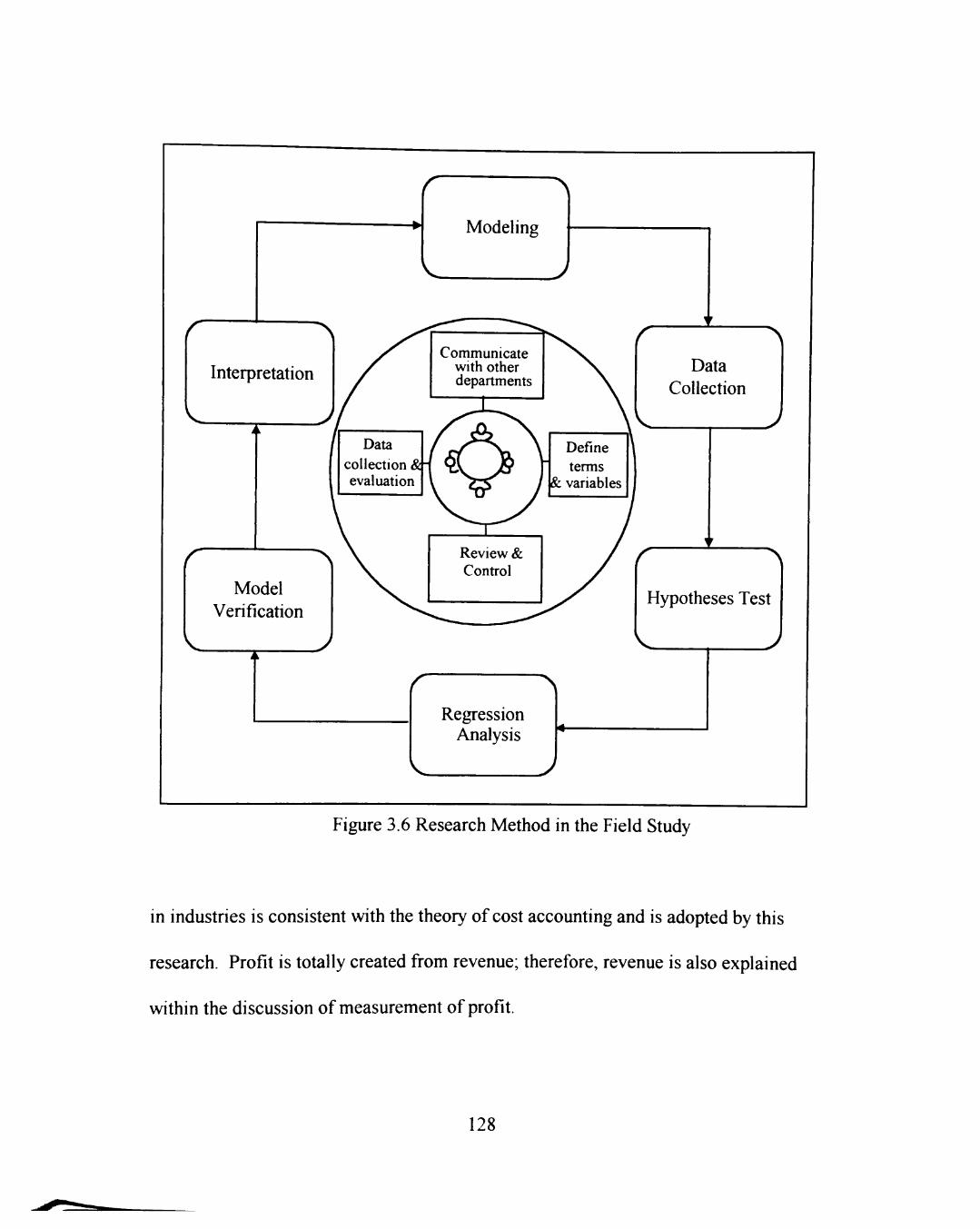

3.6 Research Method in the Field Study 128

3.7 Test Plan for Quality-Profit Relationship 131

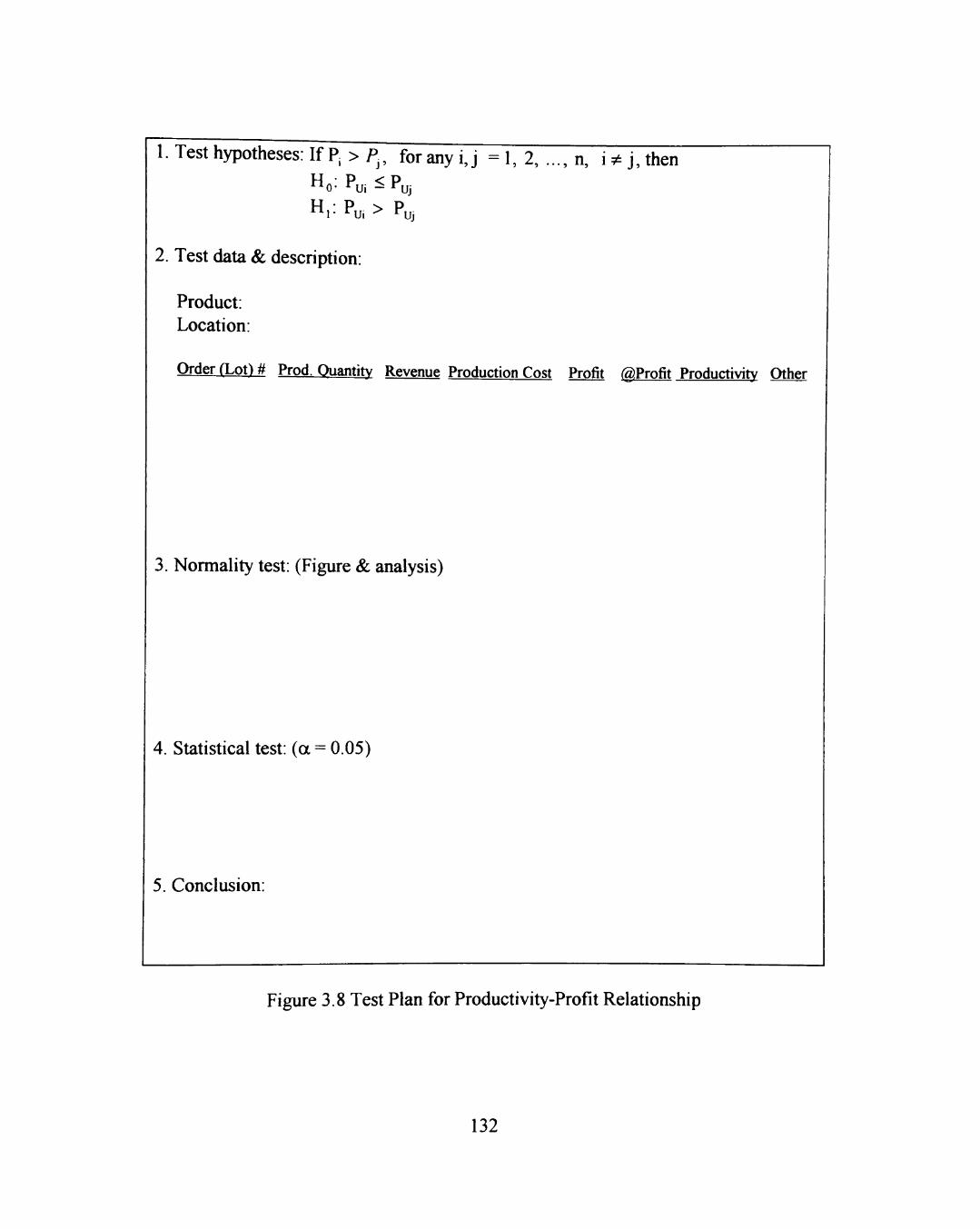

3.8 Test Plan for Productivity-Profit Relationship 132

3.9 Test Plan for Quality-Productivity Relationship 133

3.10 Data Collection Form 138

4.1 Research Sequence of Chapter 4 150

4.2 Residual Plots: Residuals Against Ranks of Quality 182

4.3 Residual Time Plots: Residuals Against Time Series 185

4.4 Residual Plots: Residuals Against Expected Value 189

4.5 Residual Plots: Residuals Against Ranks of Quality 192

4.6 Residual Time Plots: Residuals Against Time Series 194

4.7 Residual Plots: Residuals Against Expected Value 197

XV

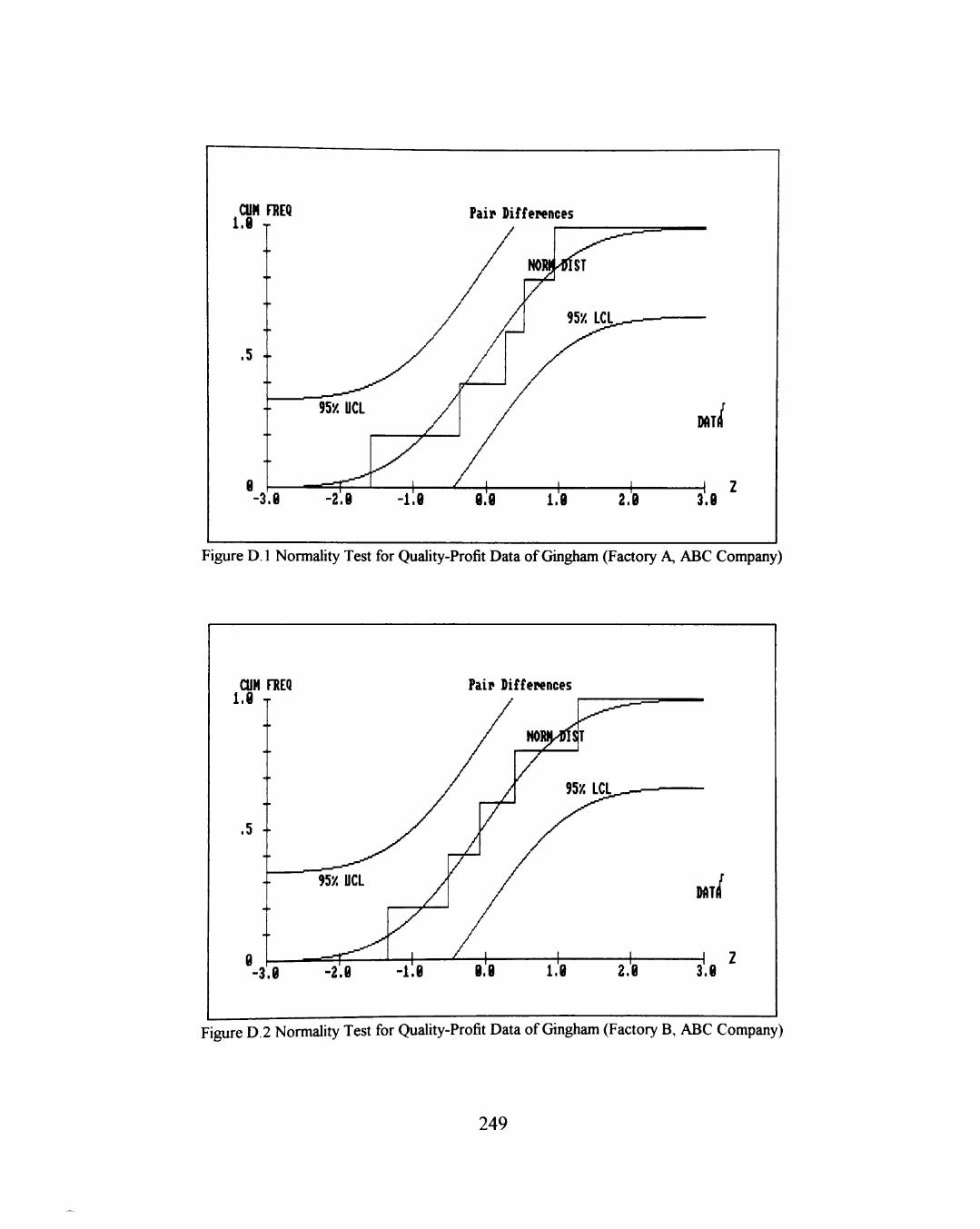

D. I Normality Test for Quality-Profit Data of Gingham (Factory A, ABC Company) 249

D.2 Normality Test for Quality-Profit Data of Gingham (Factory B, ABC Company) 249

D.3 Normality Test for Quality-Profit Data of Gingham (Factory C, ABC Company) 250

D.4 Normality Test for Quality-Profit Data of Piece-dyed Fabric (Factory A, ABC Company) 250

D.5 Normality Test for Quality-Profit Data of Piece-dyed Fabric (Factory B, ABC Company) 251

D.6 Normality Test for Quality-Profit Data of Piece-dyed Fabric (Factory C, ABC Company) 251

D.7 Normality Test for Quality-Profit Data of PNP Ethernet Combo 252

D.8 Normality Test for Quality-Profit Data of Token Ring 252

D.9 Normality Test for Productivity-Profit Data of Gingham (Factory A, ABC Company) 253

D. 10 Normality Test for Productivity-Profit Data of Gingham (Factory B, ABC Company) 253

D. 11 Normality Test for Productivity-Profit Data of Gingham (Factory C, ABC Company) 254

D. 12 Normality Test for Productivity-Profit Data of Piece-dyed Fabric (Factory A, ABC Company) 254

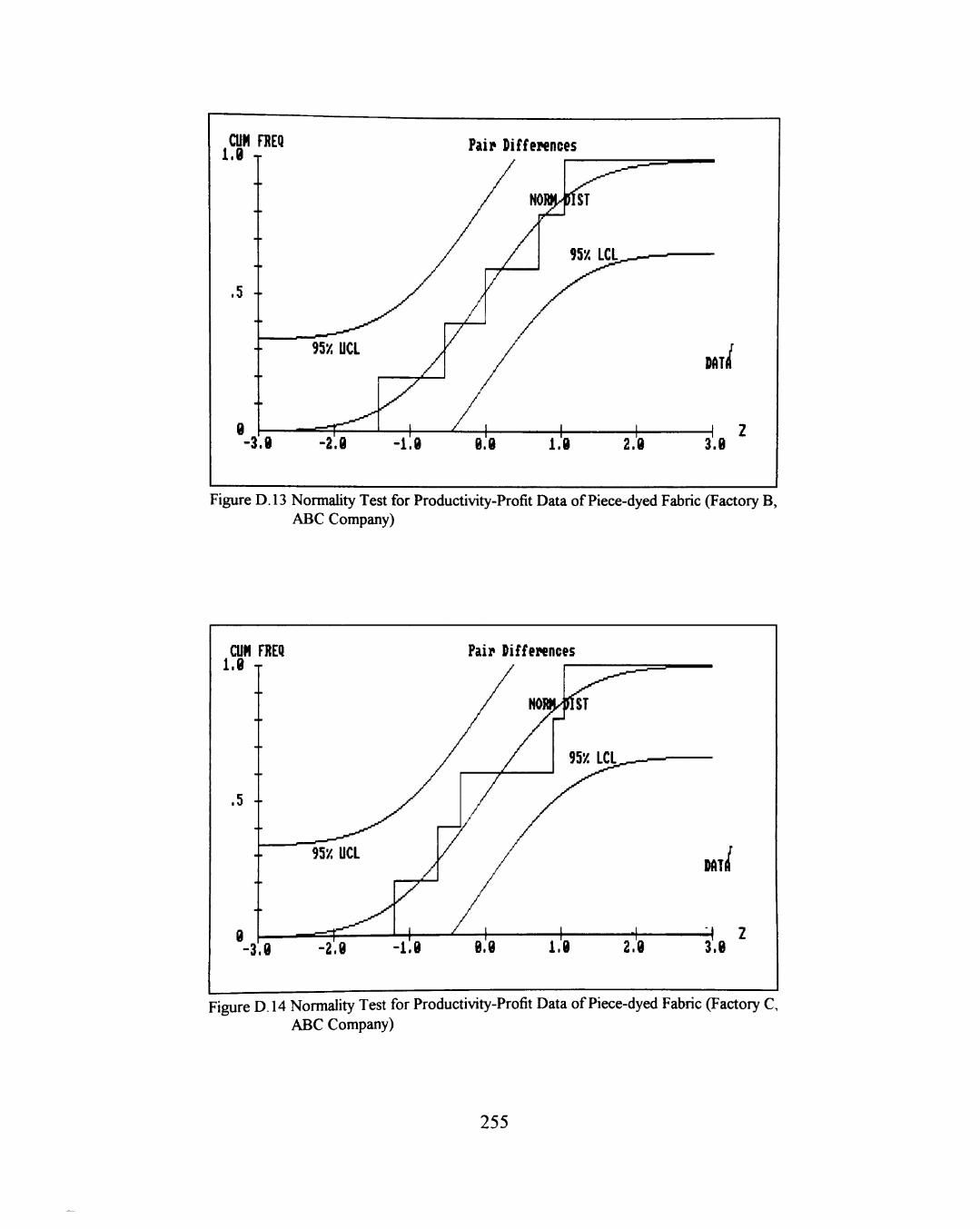

D.13 Normality Test for Productivity-Profit Data of Piece-dyed Fabric (Factory B, ABC Company) 255

D. 14 Normality Test for Productivity-Profit Data of Piece-dyed Fabric (Factory C, ABC Company) 255

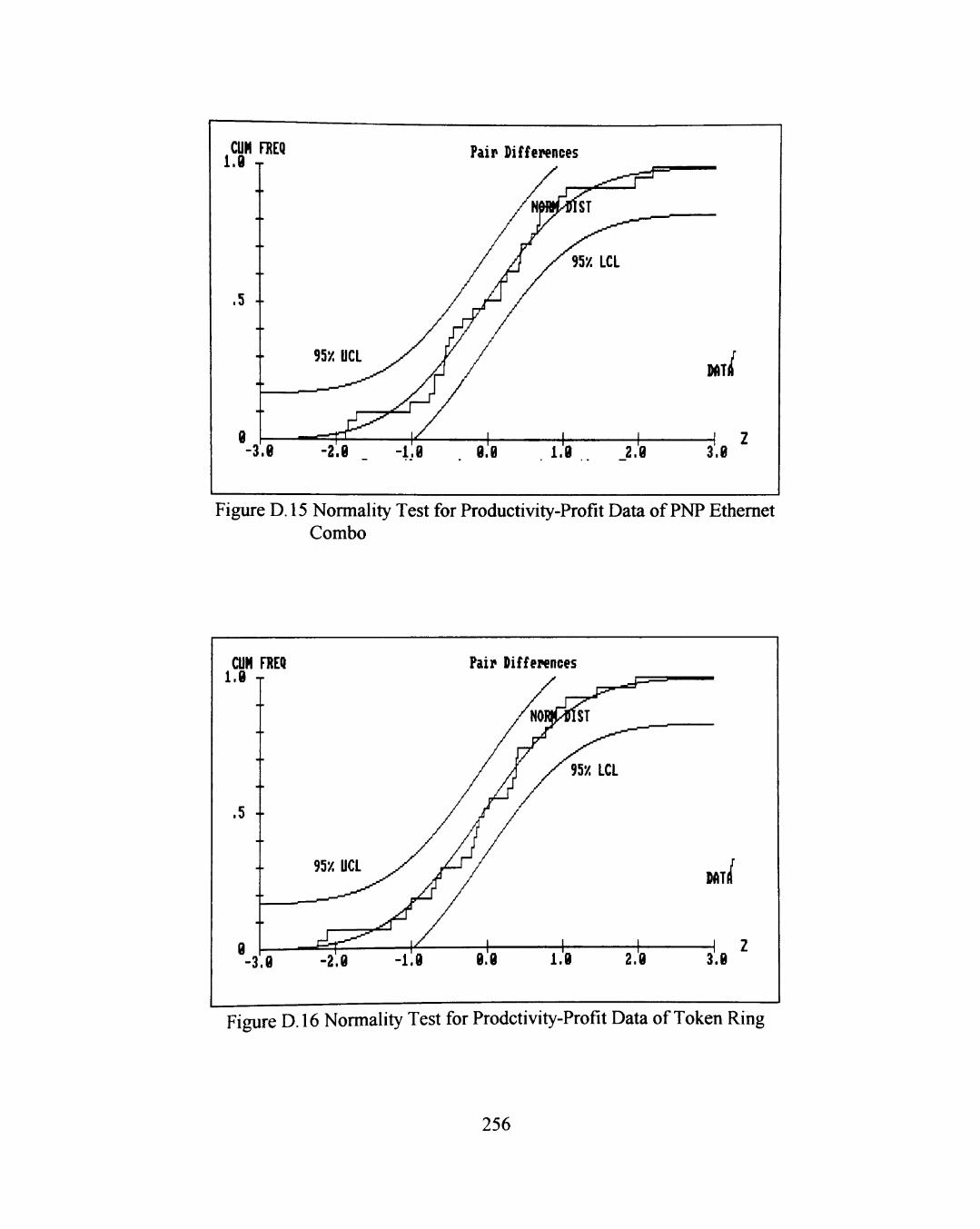

D. 15 Normality Test for Productivity-Profit Data of PNP Ethernet Combo 256

D. 16 Normality Test for Productivity-Profit Data of Token Ring 256

XVI

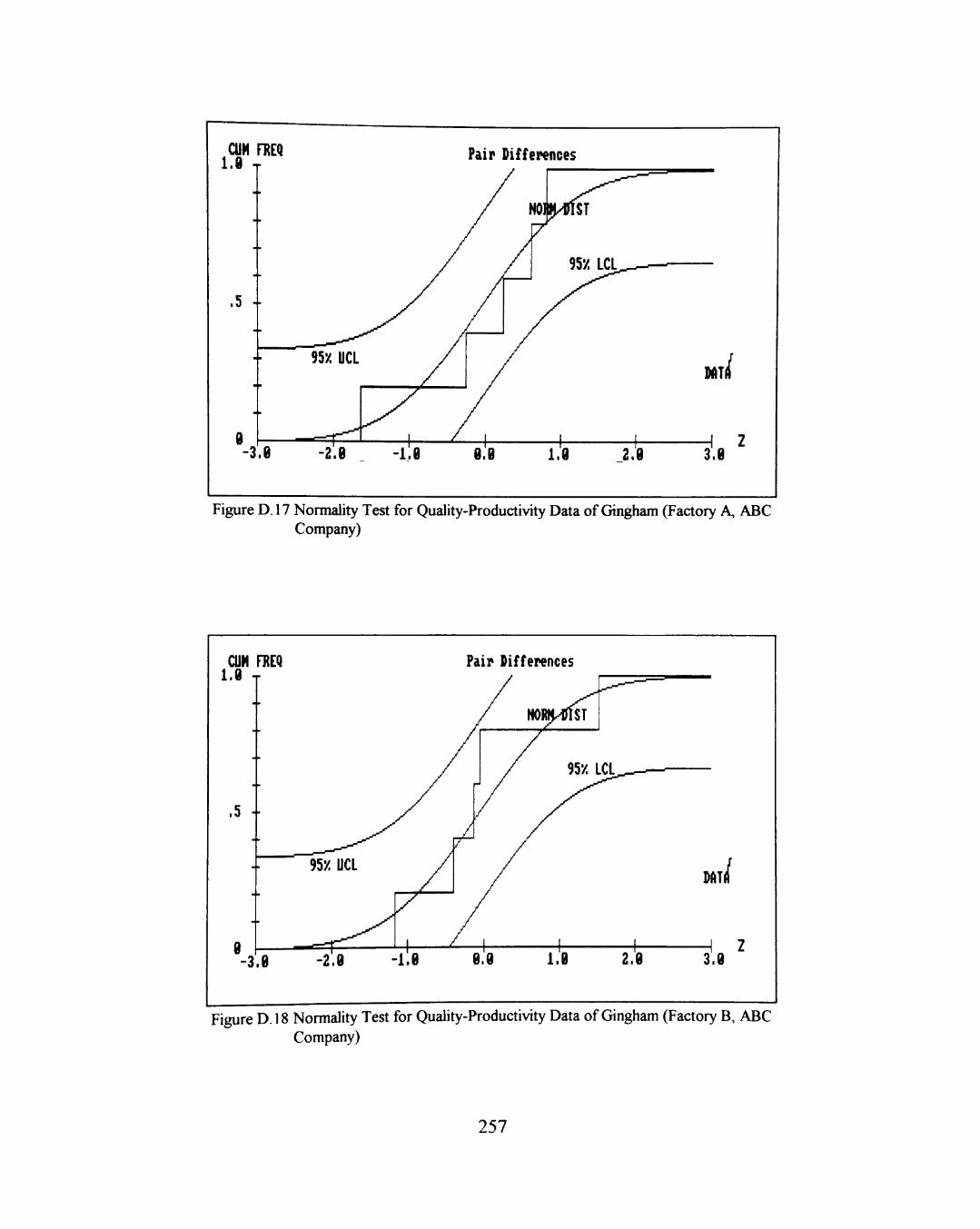

D. 17 Normality Test for Quality-Productivity Data of Gingham (Factory A, ABC Company) 257

D. 18 Normality Test for Quality-Productivity Data of Gingham (Factory B, ABC Company) 257

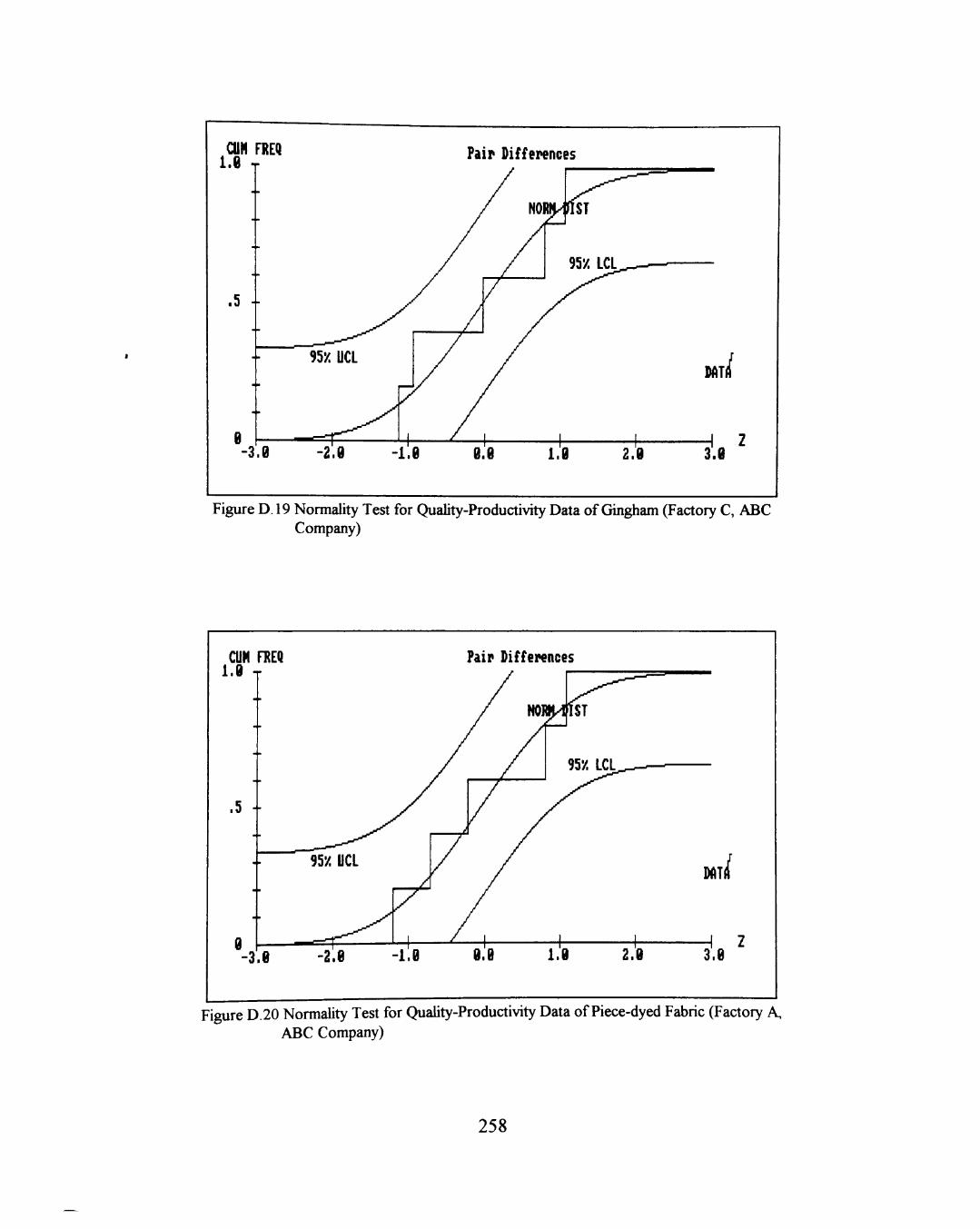

D. 19 Normality Test for Quality-Productivity Data of Gingham (Factory C, ABC Company) 258

D.20 Normality Test for Quality-Productivity Data of Piece-dyed Fabric (Factory A, ABC Company) 258

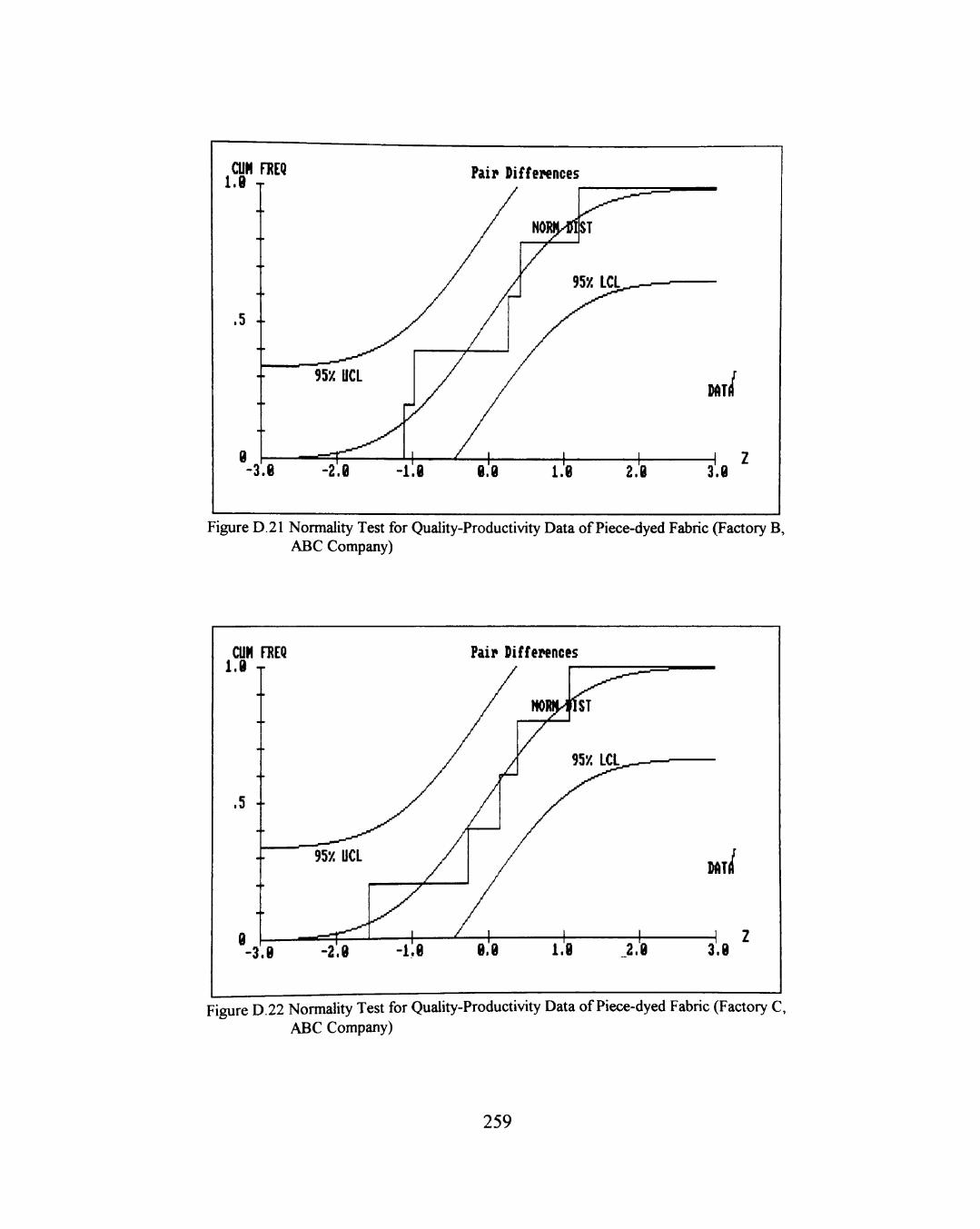

D.21 Normality Test for Quality-Productivity Data of Piece-dyed Fabric (Factory B, ABC Company) 259

D.22 Normality Test for Quality-Productivity Data of Piece-dyed Fabric (Factory

C, ABC Company) 259

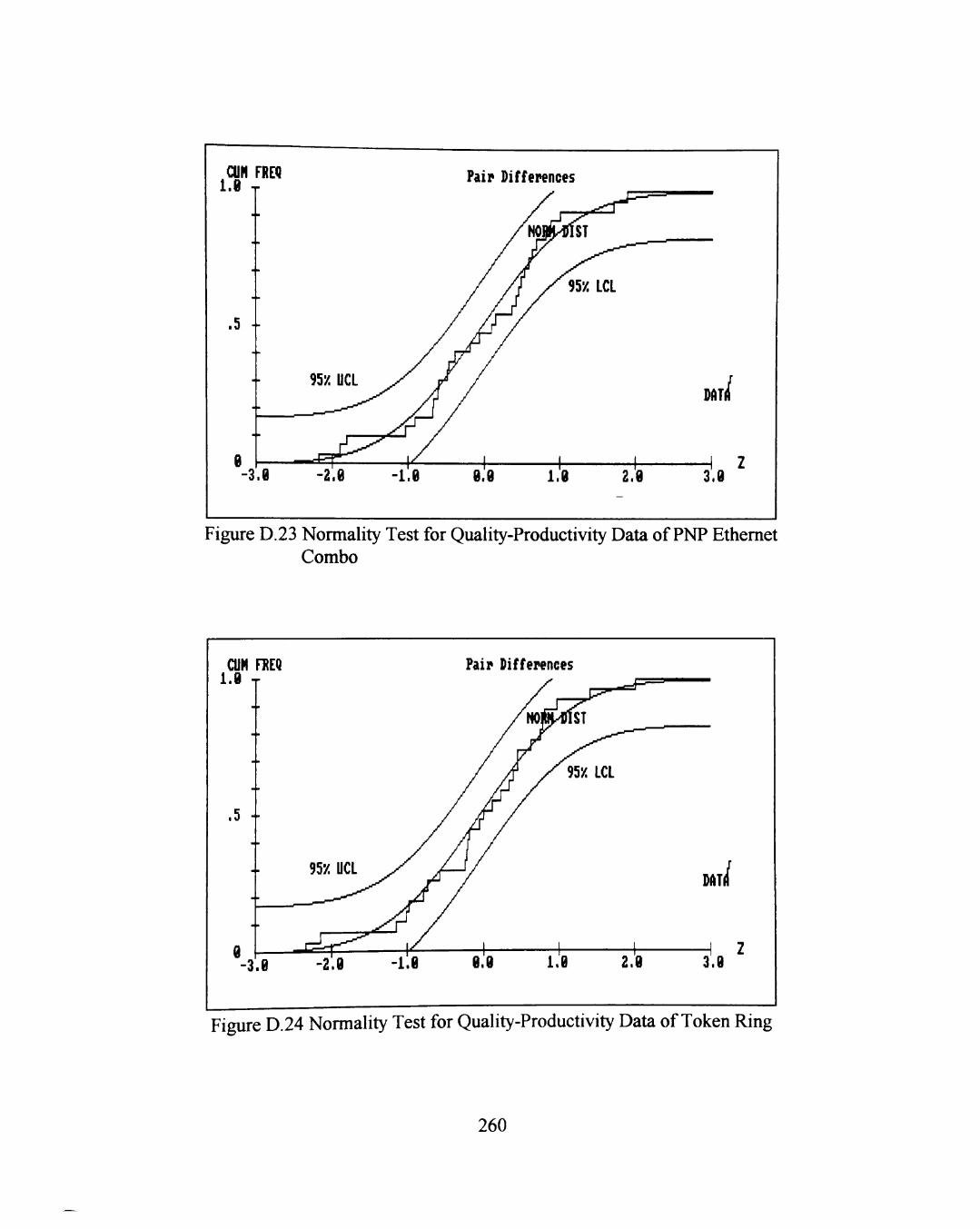

D.23 Normality Test for Quality-Productivity Data of PNP Ethernet Combo 260

D.24 Normality Test for Quality-Productivity Data of Token Ring 260

xvii

CHAPTER I

INTRODUCTION

For years quality and productivity have been regarded as two important

indexes of company performance. Many companies hope to pursue high quality and

high productivity at the same time. However, in most cases, these two variables are

not linked together in the production system mainly because of the variety of their

definitions (Human Resources Productivity, 1983; Garvin, 1988; Belcher, 1987;

Hoffherr & Moran & Nadler, 1994; Smith, 1990). Additionally, these two variables

are not taken into account together because: (1) the objectives of quality management

and productivity management are viewed as contradictory,^ (2) the definitions of

quality and productivity are difficult to define, (3) the affecting factors on quality or

productivity are too numerous, (4) seemingly, quality and profit have no direct

connection,^ and (5) many companies believe that they have distinct characteristics

which may not be subject to any model.

' Deming (1986), Belcher (1987), Darts (1990), Hart and Hart (1989), Kaydos (1991), and Omachonu and Ross (1994) also have noted this misconception in their research.

^ Pirsig (1974) believes quality cannot be defined. McNealy (1993) states that quality is as hard as "art" to define. Mohanty and Yadav (1994) also claim that quality is a difficult concept to define. Deming (1986) maintains that quality is defined by management. Kendrick (1984) asserts that productivity cannot be measured directly. Yet others, such as Smith (1986), Kaydos (1991), Price (1990), regard quality and productivity as the same thing.

^ Sumanth and Wardhana (1993) point that some companies do not believe "quality and profit go hand in hand," (p. 463)

The first reason, stated above, was especially prevalent in the past. Deming

(1986) asserts that this erroneous concept of quality and productivity management

contradiction is common in American industries; therefore, he firmly asserted that

improving quality will result in improved productivity. He believed the relationship

between quality and productivity is strongly positive. However, he interpreted this

relationship by reasoning, that is, Deming presented no mathematical model to

backup his assertion. Managers believe his assertion is correct because the logic is

reasonable.

The second reason that quality and productivity are difficult to define, lies in

the debatable definitions. So far the well-known definitions of quality are too

abstract to relate to productivity. On the other hand, productivity has different levels

(or units of analysis) and types.' Each level or type ofproductivity has different units

of measure. The type or unit of measure for productivity which should be used to

relate to quality is debatable.

The third reason, that the affecting factors on quality or productivity are too

numerous, illustrates the difficulties of relating quality and productivity. Generally,

the current quality-productivity relationship models can be classified into two

categories: qualitative models and quantitative models. The qualitative models

outnumber the quantitative models because the latter need measurable variables. A

'* Sumanth (1979) deals with productivity at four levels: International, National, Industry, Company. Sumanth (1994) classifies productivity into three types: Total Productivity, Total Factor Productivity, and Partial Productivity. Kendrick (1984) deals with productivity at another four levels: National, Industrial, Company, and Personal.

qualitative model is easier to understand, but has less applicability compared with a

quantitative model. However, because many factors are not easy to measure,

quantitative models have limitations in application. Therefore, companies may not

believe it is practical to link quality and productivity.

The fourth reason, that quality and profit have no direct connection, illustrates

that current models cannot reflect the impact on profit. Profit is the main concern of

management, ff a quality-productivity model cannot estimate the impact on profit, it

loses its attractiveness to the management. However, because quality is an abstract

concept, it is hard to directly link quality and profit together. Although productivity

can be measured in terms of profit, it is not common to quantitatively relate quality to

profit. Therefore, a quality-productivity model without profit as a base may not be

attractive to industries.

The last reason, that each company believes it has its own characteristics

which may not be subject to any model, illustrates their perception that their

production features are different from others. They believe that a model may be

applicable to others, but not to them. Each company has its own production features;

however, a generic model can be tailored to the user's own purpose. Most models

found in open literature are not originally developed for a specific company. Hence,

the notion that it is impractical to link quality and productivity for use is incorrect.

These five reasons leave the following questions unanswered: High quality

and high productivity are all pursued by companies, but how can they be related to

each other? Is this potential relationship model meaningful for companies? How can

the relationship be applied in practice? This study will answer all these questions.

This research focuses on the profit-based quality-productivity relationship

model and its verification in manufacturing industries. In this chapter, the problem

statement is presented in section 1.1. The scope of this research, including the

research question, purpose and objective, are addressed in section 1.2. The

limitations and assumptions of this research are presented in section 1.3. In section

1.4, needs and benefits of this research are explained. Finally, section 1.5 presents

the expected results.

1.1 Research Problem Statement

Quality and productivity are two measures of interest in most every company.

Their relationship is also a concern of management. From the open literature, it is

understood that productivity will increase as product quality increases (Shetty &

Buehler, 1985; Hayes, 1985; Deming, 1986; Hart & Hart, 1989; Darts, 1990; Kaydos,

1991; Tribus, 1992; Barrett, 1994; Omachonu & Ross, 1994). However, fewer

quality-productivity relationship models are expressed in a mathematical way. A

mathematical model of the quality-productivity relationship provides more clear

information for parameter control than does a descriptive model. Therefore, an

appropriate mathematical model relating quality and productivity is sought to meet

the needs of management.

Since multiple units of measure are used in quality as well as productivity

measures, a common measurement unit must be set in order to relate quality and

productivity. Perhaps a better common unit of measure in this quality-productivity

relationship is profit, since profit is most attractive to management. Hence, a study on

the profit-based quality-productivity relationship model is conducted in this research.

Finally, the applicability of the developed quality-productivity relationship

model must be discussed. A study on the verification of this proposed model in

Taiwan's manufacturing industries is surveyed. Taiwan's manufacturing industries

are chosen for the follovWng reasons: (1) Taiwan is a typical Newly Industrialized

State (NIS). The government adopts an export-oriented trading policy. This policy

encourages all enterprises to emphasize quality and productivity, (2) Many managers

in Taiwan's manufacturing industries possess common knowledge of quality control

and productivity management. This is especially helpful in communication when

conducting this research, (3) Information on Taiwan's manufacturing industries is

readily available for this research.

1.2 Scope of This Research

This section addresses the research question in which this study is interested.

The research purpose and objective are also included in this section to help direct the

efforts of this research.

1.2.1 Research Question

The main questions this work will address are as follows:

1. What is the quality-productivity relationship model based on profit?

2. Is the profit-based quality-productivity relationship model applicable in

manufacturing environment?

To answer the two main questions, it is necessary to understand further:

a. What is the quality-profit relationship?

b. What is the productivity-profit relationship?

c. How many quality-productivity relationship models are currently

available? Are they generic or specific? Do they need to be revised or

modified for this research?

1.2.2 Research Purpose

This research will attempt to provide an applicable profit-based quality-

productivity relationship model for manufacturing industries. This model will

convince the management of that quality and productivity are positively related, and

the enhancement of either quality or productivity will increase profit. An additional

purpose of this research is to show whether the developed quality-productivity

relationship model is applicable to an individual company. It is expected that the

developed model is not only theoretically sound, but also may be practically used by

companies in the real world.

1.2.3 Research Objective

This research has two main objectives: (1) develop a mathematical quality-

productivity relationship model based on profit, and (2) Investigate the applicability

of this model in the manufacturing industries.

In achieving these objectives, the following secondary objectives are included:

1. To review the existing models related to the quality-productivity

relationship.

2. To explore the relationship between quality and profit.

3. To explore the relationship between productivity and profit.

4. To conduct an empirical study in Taiwan in order to confirm the

developed model.

1.2.4 General Hypotheses

The general hypotheses regarding this research are:

1. Quality and profit are related, and a model may illustrate the relationship

between these variables.

2. Productivity and profit are positively related, and there is a model to relate

these two variables.

3. Quality and productivity are related, and a model may illustrate the

relationship between these variables.

1.3 Limitations and Assumptions

In this research, some determination of the limitations and assumptions is

required. These limitations and assumptions are helpftil in focusing this research. If

the model proposed in this research is tailored for a specific purpose, the limitations

or assumptions will possibly change.

1.3.1 Limitations

The limitations of this research are:

1. This research deals only with manufacturing companies. Service

organizations will not be included in the scope of this research.

2. The intangible factors of quality and productivity are not discussed in this

research.

3. The relationship between quality and productivity is linked based on profit.

4. The productivity measure (unit of analysis) used in this research is limited

to the company level. The productivity measures of national, industrial,

and individual levels are not considered in this study.

5. The productivity type used in relating productivity to quality is restricted to

the Total Productivity Model.

6. The study on the applicability of proposed model is conducted in Taiwan's

manufacturing organizations.

8

7 This research considers all issues within this research from an industrial

engineering perspective. Implications concerning other disciplines are not

addressed in depth.

1.3.2 Assumptions

The assumptions of this research are:

1. The manufacturing company is a profit-oriented company.

2. The company has the intention and capability of improving its quality and

productivity.

3. Quality can be linked wdth profit.

4. Productivity can be measured in terms of profit.

5. In general, the issues considered are applicable to manufacturing

companies.

6. Except where specified, all terms used in this research reflect the common

usage as found in the quality and productivity literature.

1.4 Relevance

This section describes the needs and benefits of this research. The needs of

this research provide the motive required for carrying out the research. Benefits of

this research are followed by the results of this study.

1.4.1 Need for This Research

This research deals with the theoretical relationships between quality,

productivity, and profit. A confirmatory study on the theoretical model is also

conducted to verify model's applicability. The specific theoretical and practical

research needs will be discussed in the following two subsections (1.4.1.1 and

1.4.1.2) respectively.

1.4.11 Theoretical Research Needs

Managers seek to improve quality by every possible means. They all

understand the importance of quality. However, the problem of how profit is affected

by quality is not easy to measure. In general, the relationship between quality and

profit is easier to explain in the descriptive approach; however, it lacks precision.

Perhaps a better way to realize how the quality level affects profit is to establish a

mathematical relationship model between these two variables. Through this

mathematical model, the optimal quality level in which the profit is maximum can be

identified.

The needs for research on the relationship between productivity and profit are

identical to those for quality and profit. The basic definition ofproductivity is a ratio

of output to input; therefore, if the output is measured in tenns of profit, it is easier to

quantitatively estimate the relationship between productivity and profit. However, it

10

is not easy to measure the relationship between productivity and profit without a

definite model. This research intends to determine such a mathematical model.

In addition, because productivity is strongly affected by quality, managers are

interested in their relationship. By establishing a Quality-Productivity relationship

model based on profit, it would help the managers and researchers realize more

firmly that profit can be increased by enhancing quality or productivity.

1.4.1.2 Practical Research Needs

This research is also interested in understanding the applicability of the

proposed model in manufacturing companies. Any model will undoubtedly be

accepted if it can be proved or confirmed. In general, management in industry is

more interested in the model's applicability than in the model's theory. Taiwan, as a

newly industrialized nation, has the desire to practically understand the relationships

between quality, productivity, and profit. This need is also a driving force of this

study.

1.4.2 Benefits of This Research

The benefits of this research are as follows:

1. Present an updated literature review on the quality-profit, productivity-

profit, and quality-productivity relationships.

11

2. Determine the relationship between quality and productivity from the profit

point of view.

3. Develop a relationship model of the quality and productivity that can be

analyzed and evaluated for the purpose of management.

4. Present a theoretical, quantitative research approach for measuring the

relationship between quality and productivity.

5. Confirm the proposed relationship model of quality and productivity

through field study.

1.5 Expected Results

This research should result in the following: (1) A mathematical model of the

quality-productivity relationship is to be set up fi-om the profit viewpoint. (2) The

applicability of the proposed model to manufacturing companies could be

investigated and verified. (3) The established specific model could be used as a

predictor for manufacturers. In addition to these three results, all of the relationship

models related to quality-profit, productivity-profit, and quality-productivity are to be

examined, analyzed, and classified through the literature review. Conclusions and

recommendations related to the findings of this research are also to be provided.

12

CHAPTER 2

LITERATURE REVIEW

2.1 Background

The quality-productivity relationship is linked by the measures of quality and

productivity. Because of the variety of quality and productivity measures, it is

necessary to base these two variables on a common unit of measure. Profit is

selected as this base because it relates to both quality and productivity. Besides,

profit is the most critical issue for management. In addition, to understand the basic

definitions and history of quality and productivity, it is also necessary to review the

relationships between quality, productivity, and profit. Therefore, in this section, the

history of quality and productivity are first briefly introduced. The relationships

between quality, profit, and productivity found in the open literature are then

presented. Various definitions of quality, productivity, and profitability are also

examined in this section.

2.1.1 History

History provides experiences and learning to deal with the future. It is helpful

to examine the history of quality and productivity before exploring the relationship

between the two variables. In addition to examining the history of quality and

productivity, these subsections illustrate the relationships between quality and profit.

13

productivity and profit, and quality and productivity. In order to more thoroughly

understand the quality-productivity relationship, review of this relationship is not

limited to profit-based.

2.1.1.1 History of Oualitv

The concept of quality has existed for a long time. According to Duncan

(1974), "Quality control is as old as industry itself (p. 1). Shewhart (1939) points out

more definitely that the inspection standard of a "go" tolerance limit appeared in

1840. About 30 years later, the improved concept of "go, no-go" tolerance limits

was developed. However, the management of quality, regarded as a professional

task, can be traced back to F. W. Taylor (1911). Known as the father of scientific

management, Taylor was the first to regard management and production as different

functions. In 1931, W. A. Shewhart (1931) introduced statistical quality control in

his book "Economic Control of Quality of Manufactured Product." In 1941, W. E.

Deming began to teach quality-control techniques in the U. S. War Department. He

later taught statistical quality control in Japan in 1950. To thank Deming for his

contribution, the Japanese established the Deming Prize in 1951. Another master in

quality control, J. M. Juran also gave seminars to the Japanese beginning in 1954.

^ In his book "The principles of scientific management," Taylor presented four principles for management. The fourth was "an almost equal division of the work and the responsibility between the management and the workmen," (p. 37). He indicated that nearly one-half of the production problem was up to the management. Therefore, he asserted that management was a professional task which should be separated fi-om the worker's job. According to Taylor's assertion, the management of quality should also be viewed as an independent function fi-om the worker's job.

14

This was "a turning point m emphasizing quality control for management" (Hosotani,

1992, p. 4).

It was not until the introduction of the concept of reliability that quality was

seldom measured relating to a product's life-time. Reliability engineering was

originated and conducted by the Advisory Group on Reliability of Electronic

Equipment (AGREE), formed in 1952, for studying and analyzing the failures of

electronic military equipment. The 1957 AGREE report formally defined the term

reliability and "formed the basis for modem methods and procedures" (Evans &

Lindsay, 1989, p. 255). In 1961, Martin Company developed the Zero Defects

Program and achieved zero defects in the American Army's Pershing missile system.

This Zero Defects concept was later introduced by J. F. Halpin, Director of Quality of

the Martin Company, in 1966. In the year of 1961, A. V. Feigenbaum first presented

the concept of Total Quality Control. K. Ishikawa introduced Quality Control Circles

in the following year. Mitsubishi's Kobe Shipyard in Japan first used Quality

Function Deployment (QFD) in 1972. The QFD technique was introduced to the U.

S. in 1983 by Professor Y. Akao of the University of Tamagawa. G. Taguchi, a

Japanese engineer, introduced a new approach in the early 1980s. His approach,

which later became known as the Taguchi Method, was used to design products and

reduce loss through what he termed the "Loss Function."

People are a very important factor to the quality. Research and

implementation related to the quality of work life (QWL) began to be emphasized.

15

According to Riggs and Felix (1983), the development of QWL can be traced to the

eariy 1970s. However, "Major efforts to make QWL an emerging fact in the

employees' work life have been under way since the 1980 National Memorandum of

Understanding was issued" (Shetty & Buehler, 1985, p. 135). Because of the risk

assumption, Shingo (1986) believes that traditional statistical methods cannot achieve

the zero defects level. In order to prevent and eliminate all possible defects, he then

proposed a mistake-proof system, called the poka-yoke system, and a source

inspection system. In 1987, the International Organization for Standardization (ISO)

published the ISO 9000 series to serve as the international standards of quality.

These standards were revised in 1994, and gradually have became more prevalent

since their adoption by many countries, especially the European Community nations.

The ISO 9000 series has become the supreme standards governing quality aspects.

Since the quality-productivity relationship is the key issue of this research, it

is also essential to understand the history ofproductivity. We will make a brief

introduction to its history in the following.

2.1.1.2 Historv of Productivity

According to Sumanth (1994), "probably, the first time the word 'productivity'

was mentioned was in an article by Quesnay in the year 1766" (p. 3). A more

detailed review ofproductivity is made by Kendrick (1977). In his book

Understanding Productivity, Kendrick mentioned that "the early estimates of

16

productivity were in terms of output per unit of labor input," (p. 19). This concept

was used by the eariy economists (e.g., Adam Smith in 1776) in the labor theory of

production and value (Kendrick, 1977). Kendrick recounted that in the latter

nineteenth century, Alfred Marshall advocated that man-made capital goods, labor,

and land were the basic factors of production. Marshall's recognition of the basic

factors of production became "the basis for the concepts of production function and

productivity" (Kendrick, 1977, p. 20).

The first estimates ofproductivity, in terms of output-per-hour, were

presented by the United States Bureau of Labor in the mid-1880s (Kendrick, 1977).

C. D. Wright, the first commissioner of labor in the U.S., published a report called

"Hand and Machine Labor," in 1898. According to Adam and Dogramaci (1981),

Wright's report, which studied company productivity and costs, is a remarkable

landmark in the history ofproductivity. Sumanth (1979) pointed out that probably the

first productivity index, a ratio of output to the number of wage earners, was

presented by F. C. Mills in 1899. Taylor (1911) in his renowned book The Principles

of Scientific Management, provided some examples for describing how the increase

in human productivity can be reached by applying the principles and methods of

scientific management. In addition, his work measurement is an effective tool for

improving labor productivity.

After the Great Depression of the 1930s, productivity estimates and analyses

were revived (Kendrick, 1977). During this period, the Bureau of the Census "began

17

publication of industry summaries on value added per man-hour" (Adam &

Dogramaci, 1981, p. 13). Since 1940, the Bureau of Labor Statistics (BLS)

investigated productivity performance in certain industries and published the first

regular government estimates ofproductivity. Today the BLS still "is the major

source of industrially based data on labor productivity" (Smith, 1990, p. xiii). The

initial development of the total factor productivity approach began after World War

II. According to Kendrick, productivity studies in the U. S. and abroad interacted

with the movement in many countries, beginning about 1950. The European

Productivity Agency, which became known as the European Association of National

Productivity Centers, was set up after 1952 to integrate the activities of the

international centers (Kendrick, 1977). Japan began its productivity movement in

1953. Two years later, the Japan Productivity Center began operation. The Asian

Productivity Organization, which is located in Tokyo, was established from the Japan

Productivity Center in 1961. No productivity agency was set up in the U. S. before

1970.

Due to "the failure to tax-finance the Vietnam escalation" and "the energy-

price revolution," inflation was actuated firom the mid-1960s to the early 1970s. This

inflation stimulated and reinforced the increased rate of improvement ofproductivity

in organizations (Adam & Dogramaci, 1981, p. 13). Also in the 1970s, the BLS

executed a large-scale measurement program to measure the employee's productivity

in federal organizations. In July 1970 the National Commission on Productivity was

18

created and its name was then changed to the National Center for Productivity and

Quality of Working Life in June, 1974 (Sumanth, 1994). In 1975, the U.S.

Department of Commerce began holding seminars to educate the company managers

in methods ofproductivity measurement (Adam & Dogramaci, 1981). In 1980, the

U. S. Senate first declared October 6-12 as the National Productivity Improvement

Week (Sumanth, 1994).

After briefly reviewing the histories of quality and productivity respectively,

the relationships between quality, productivity, and profit v^ll be subsequently

reviewed. In general, profit is the difference between total revenues and total costs,

while profitability is the ratio of total revenues to total costs. Theoretically, profit

and profitability have different definitions. However, unless otherwise specified in a

model or quoted materials, profit and profitability are considered interchangeable

terms when comparing quality and productivity in the following subsections. After

the relationship between quality and profit is examined, the relationship between

productivity and profit will be investigated,. Finally, the quality-productivity

relationship will be addressed.

2.1.1.3 Review of the Relationship between Quality and Profit

The relationship between quality and profit is inseparable. "Seeking profit by

making quality a priority" (Hosotani, 1984, p.23), and "Quality is the input,...

Profits, ROI,... are results" (Bhote, 1991, pp. 10-11) illustrate the remarkable

19

relationship between quality and profit. Some even regard quality as a synonym of

profitability. Undoubtedly, managers believe that better quality results in more

profit. However, on the surface, quality does not directly relate to profit. From the

quality viewpoints, the increase of profit is due to the following two approaches.

First, the cost decreases while the selling price and volume either remain the same or

increase. Second, the increase of purchasers leads to increased profit. Nevertheless,

these two ways are strongly cross-related.

The first approach is cost-driven, meaning that more profit is made because

the cost is reduced first. Weinberg (1969) believes that optimum quality, not highest

quality, means lower costs and is the most economic way to make profit. Crosby

(1979) emphasizes the inverse relationship between conformance quality and costs.

Therefore, he asserts that "Quality is Free," and places it as the title of his book. He

also indicates that as quality improves, costs reduce, and hence resulting in more

profits. John Heldt, an experienced consultant in implementing quality cost system,

states that "Reducing the cost of poor quality will increase your overall profit more

than doubling sales" (Harrington, 1987, p. 157). Duncan and Bowen (1984)

introduce an Integrated Metrology System to boost product quality for profit

improvement by reducing the cost of quality. Williams (1984) believes that the gross

profit of a company is enhanced by the improvement of quality and productivity, and

^ Ray Witt, a former president of American Foundrymen's Society, in a speech encouraged the foundrymen to emphasize quality. He stated that, "Quality and profitability are synonymous terms in the metalcasting industry." (From "Proactive Quality Control Is the Key to Profitability in the 1990s").

20

the reduction of cost. As quality improves, cost reduces and profit increases. Katzan

(1985) mentions that poor quality is costly and has a ripple effect, which it will eat

away profits. Lester, Enrick, and Mottley (1985) describe how lower quality cost,

through the reduction of scraps, reworks, inspections, etc., results in higher return on

investment, an index of profitability. Day (1988) demonstrates how profits can

double because of the elimination of scrap and rework through the improvement of

process capability. Price (1990) also points out that high quality, through quality cost

reduction, results in high profit.

The most impressive assertion regarding the cost-driven approach of the

quality and profit relationship is proposed by G. Taguchi. In the early 1980s, Taguchi

presents a "loss fimction" concept, which aims at reducing the variability of products.

The variability is product's deviation fi-om its target value. He believes that the loss

caused by the variability is incurred by society. Therefore, Taguchi (1985) defines

quality as the loss a product imposes on society after this product is shipped. He

maintains that variability must be decreased so that the total loss can be reduced.

Because of the reduction of loss, profits increase. Since the increased profit can be

quickly obtained fi-om the reduction of costs, Taguchi's method has been widely

applied in industries.

The second approach is market-driven, which emphasizes that profit is

increased by more customers. Halpin (1966) stresses that Zero Defects can deliver

the best possible product at the lowest possible price on time. This will "assure

21

management a strong market position in the years to come" (p. 186). In another

book, Crosby (1984) stresses that if the top management respected the rights of

customers like it respects the rights of the stockholders, then quality and profit will

both increase at the same time. Tuttle (1985) introduces an ACE (Acquisition and

analysis of Customer Experience) system believed to improve quality and profit.

This system mainly emphasizes customer response and takes advantage of customer

feedback to improve quality and profit. Buzzell and Bradley (1987) assert that with

higher quality, stronger customer loyalty and more repeat purchases can result. Owen

(1989) believes that attaining higher quality will cost more at first; however, this cost

will pay off and result in a higher return on investment. Ishikawa (1990) stresses his

quality assurance approach is "customer-first philosophy," which ensure that a

company is successful in market. Smith (1990) points out that quality is a strategic

and competitive weapon. With a higher level of quality, it is easier to attract

customers and increase sales. Bauer (1990), a retired director of IBM and winner of

National Quality Award in 1990, points out that "Market-Driven Quality" is IBM's

quality strategy, and aims at enlarging market shares. Both Huge (1990) and Bhote

(1991) indicate that PIMS(Profit Impact of Market Strategy) research shows a strong

relationship exists between quality and profitability. Huge also indicates more

definitely that if the quality improves fi-om low to high, market share and profit on

sales will at least double fi^om low to high. Tschohl and Franzmeier (1991) claims

that profit is determined by customer satisfaction. Although good product quality

22

alone will not guarantee profit, it helps to increase customer satisfaction and profit.

Munoz, Civille, and Carr (1992) think a strong relationship exists between quality

and customers' buying decisions. Customers not only care about quality, but also buy

quality. Munoz et al. believe this is the reason that Japanese businesses succeed in

U.S. markets. Oakland (1993) thinks quality is the most important factor that

determines an organization the reputation and hence results in maximum profit.

Research which simultaneously focuses on cost and customer is abundant.

Deming (1982) indicates that improved quality means costs and prices decrease,

making the company more competitive in market. Bravemman (1983) thinks an

appropriate quality assurance system can not only reduce waste, but can also attract

customer will. This an important issue in maximizing profits. Sink (1985) defines

profitability as a ratio of total revenues to total costs. Either increasing revenues or

reducing costs can produce higher profits. Feigenbaum (1986) maintains that quality

is the "most powerful corporate leverage point for achieving both customer

satisfaction and low costs" (p. 27). This means that more profit can result from

improving quality and reducing cost simultaneously. Evans and Lindsay (1989)

believe that "Better quality of design will eventually lead to better market share and

increased profits" (p. 43). They also think that quality cost analysis is a valuable tool

in increasing profitability. To maximize profit, Perigord (1990) suggests an

optimized Q/P (Quality/Price) ratio for reducing internal cost and increasing client

satisfaction. Christopher (1993) regards profitability as the interaction between costs

23

and revenues. Juran and Gryna (1993) explain the four reasons high quality produces

more profits: by the increase of market share, by earning premium prices, by

obtaining benefits of a larger production scale, and by attracting and sticking to

customer's loyalty. Omachonu and Ross (1994) describe the relationship between

quality and profit. They believe that good quality can reduce costs while

simultaneously improving market share and hence profit. According to Eureka and

Ryan (1995), Taguchi indicates that quality improvement is the most effective way to

reduce cost and increase sales at the same time.

Although all the research stated above agree that better quality will produce

more profit, this agreement implies an important assumption: the product

manufactured must have market value. Without this assumption, a quality product

may not result in profit. For example, a company was still producing slide rules after

the advent of the calculator, no matter how well the product quality resulted, it is

obvious that this product would not produce profit to the manufacturer. This product

may have zero defects, have minimal costs, but have no market value in the age of

calculators. Market influence can reverse the positive relationship between quality

and profit. Therefore, quality does not in and by itself imply profitability.

From the above review of the relationship between quality and profit, it is

significant to note that there is no mathematical model directly relating quality and

profit. Although most research concludes that quality and profit have a close

relationship, no theoretical research can prove the relationship. By surveying (e.g..

24

PIMS), this relationship could be confirmed. However, quantitatively examining the

relationship between quality and profit from cost or productivity viewpoints has been

studied (Juran & Gryna, 1970; Harmon, 1984; Taguchi, 1986; Dawes, 1987;

Harington, 1987; Day, 1988; Arora & Sumanth, 1992; Sumanth & Wardhana, 1993).

Therefore, it can be implied that the exploration for the quality-profit relationship

model is more likely through intermediate variables, especially the cost or

productivity.

2.1.1.4 Review of the Relationship between Productivity and Profit

Although some researchers, as previously described, may doubt that better

quality leads to higher productivity and hence increases profit, it is significant that no

one suspects that increasing productivity would reduce profit. It seems that everyone,

including managers and workers, believes firmly that productivity and profit have a

strongly positive relationship. The following review of the relationship between

productivity and profit also supports this belief

In 1911, Taylor, a man of great insight pointed out that the lack of

productivity undoubtedly resulted in a great loss to the society. From Taylor's work,

it can be implied that there is a positive relationship between productivity and profit.

Buehler and Shetty (1981) state that "At the company level, productivity is the key to

profitability" (p. 17). Feigenbaum (1983) regards productivity as one factor of

profitability. Kantzan (1985) thinks that it is obvious that productivity is directly

25

related to profitability. Sink (1985) suggests seven performance measures of an

organizational system- quality, profitability, and productivity are among them.^ He

believes these measures have a solid relationship amongst each other. Hayes (1985)

thinks that it is better to understand the relationship between productivity and profit

from a negative standpoint. That is, unproductive processes have a negative impact

on profit margins and have to be offset by additional sales. Deming (1986), who

regards productivity and quality as completely dependent, also believes that with

enhanced productivity, profit also increases. Cranberry (1987) defines productivity

as "measured by the price that must be charged for the product to produce an

acceptable level of profit" (p. 817). Belcher (1987) gives an example which

compares the profitability, price recovery, and productivity of two companies. He

concludes that the increase ofproductivity is sufficient to offset the decline of price

recovery, and hence results in profit growth. Edosomwan (1988) defines profitability

as changes in profits in terms of changes in total productivity and price recovery.

Smith (1990) presents examples ofproductivity ratios, some of which are measured

in terms of profit. Pritchard (1990) asserts that data used for measuring productivity

"must be reconcilable with profitability data" (p. 131). Karl5f (1993) also maintains

that productivity and profitability has a strong correlation.

^ The other four performance measures are effectiveness, efficiency, quality of work life, and innovation.

26

From the viewpoint of linking productivity and profit in a mathematical

model, Sumanth (1979) and Miller (1984) presented the most significant findings. In

his 1979 dissertation, Sumanth developed a model to show that profit is a fimction of

total productivity. He also introduces a concept of the break-even point in

determining total productivity. Sumanth found that the total productivity at the

break-even point was less than 1.0. In the dissertation, Sumanth fiirther proved that

the concept of "productivity-oriented profit" (POP), was the same as the concept of

conventional profit (COP). According to Sumanth, the difference between POP and

COP is that POP "considers revenues and costs in constant dollars of the based

period, whereas the COP is in current dollars" (p. 5.1). Sumanth (1980) later

presented a productivity benefit model to explain that the improvement of total

productivity in organizations can result in benefits to everyone, including consumers,

employees, stockholders, the society, and the nation. Based on Sumanth's findings in

his dissertation, Sumanth and Wardhana (1993) developed a mathematical

relationship model between quality of conformance, total productivity, and profit.

According to Kendrick (1984), the APC (American Productivity Center)

revised Von Loggerenberg's proposed basic system and presented a model of the

productivity-profitability relationship. This APC model is very similar to the

REALST model, developed by Von Loggerenberg at Data Resources Incorporated.

The APC model defines profitability as a fimction ofproductivity times price

recovery.

27

In 1984, Miller presented the PPP (Profitability = Productivity + Price

recovery) model, in which he defined profitability as equaling the sum ofproductivity

and price recovery. This model is theoretically similar to the APC's total factor

model. APC presented its model eariier than Miller's PPP model; however,

according to Miller and Rao (1989), there are a couple of differences between these

two models. First, the PPP model stresses the use of dollar figures, while APC's

model emphasizes the use of ratios. Second, the PPP model produces cumulative

values, whereas the APC model considers only a period-to-period data in the two

comparing periods. It does not take into account the inflation factor or sales prices in

the intervening periods. Miller (1987) believes that a company's true concern about

profitability is the return on investment (ROI), therefore, he also developed a model

to link productivity (total factor productivity) with profitability based on ROI.

In addition, other research is interested in developing the mathematical

relationship model of productivity-profitability. Adam, Hershauer, and Ruch (1981)

explain the relationship between productivity and profit by using an index of

profitability: a ratio of sales (output quantities x prices) to costs (input quantities x

unit costs). Papadimitriou (1992) also developed the Profit Decomposition Model

(PDM), in which the percent contribution of each determinant to profit growth is a

function of productivity, in addition to other variables. In the PDM model,

productivity contribution is further divided into two components: productivity

contribution due to scale and productivity contribution due to factor prices. Harmon

28

(1984), in her dissertation, agrees that productivity and profitability have a close

positive relationship. However, she added that the negative relationship, rising

profitability with declining productivity, may exist if there is a lot of backlog in

demand. She conducted a case study to investigate the relationship between

productivity and quality cost. Her study also demonstrates the positive relationship

between productivity and profit.

2.1.1.5 Review of the Relationship between Quality and Productivity

For many years, quality and productivity have been regarded as mutually

conflicting. Deming (1986) notes that it is typical for American management to

believe that the goals ofproductivity and quality conflict. As Belcher (1987) states,

"Management traditionally has viewed quality and productivity essentially as trade

offs" (p. 143). The explanation related to the negative correlation between quality

and productivity is noted in additional works. For example, "It is reasonable to think

that lowering quality standards will increase productivity because the amount of

'good' product made will increase slightly" (Kaydos, 1991, p. 22). Also, "On the one

hand, productivity is often synonymous with increased output. On the other hand,

thoughts of quality often conjure up visions of a quality control team insisting on

more careful production, resulting in decreased output" (Darst, 1990, p. 117). Or "It is

argued that a program to improve quality causes disruptions and delays that result in

^ She does not mention that another type of negative relationship, rising productivity results in declining profitability, may exist.

29

reduced output," (Omachonu & Ross, 1994, p. 179). But these explanations are

doubtftil. Hart and Hart (1989) pomt out that, "There is a misconception in the minds

of many people that quality and productivity are conflicting goals" (p. 3). Robson

(1990) states that many manufacturers believe that if they focus on productivity,

quality will be sacrificed. Sumanth and Arora (1992) also mention that the notion of

improved quality resuhing in a loss in productivity is a common fallacy in industries.

Most research indicates that the relationship between productivity and quality

is positive. Feigenbaum (1977) points out that, "a certain 'hidden' and non-productive

plant exists to rework and repair defects and returns, and if quality is improved, this

hidden plant would be available for increased productivity" (p. 21). Deming (1982)

makes an argument for the positive relationship between productivity and quality. He

believes that the reduced productivity resulted from quality defects, rework, and

scrap. Therefore, Deming concludes that the improvement of quality will transfer

waste of resources into the manufacture of good products. Christopher (1993) even

stresses that quality and productivity are inseparable. Hayes (1985) also thinks that,

"Quality and productivity are integrally bound and share common goals" (p. 59).

Garvin (1988) also agrees that a positive correlation between quaUty and productivity

does exist. He explains "Less rework means more time devoted to manufacturing

acceptable products, and less scrap means fewer wasted material" (p. 84). However;

he also points out that this explanation is too narrow and provides only limited

insight. Smith (1990) fiirther indicates that in order to reflect the conviction that

30

quality and productivity are related and occur simultaneously, the American

Productivity Center located in Houston was renamed the American Productivity and

Quality Center in 1988. Based on Boileau's (1984) experience as President of

General Dynamics, he concludes that quality and productivity are firmly related and

codependent. Barret (1994), Willbom and Cheng (1994), and Omachonu and Ross

(1994) all assert that productivity and quality are closely related.

Most of the assertions that quality and productivity are positively related are

based on the position that productivity is improved through the improvement of

quality. In other words, many researchers and managers believe that quality

improvement must precede productivity improvement. As mentioned in the previous

paragraph, Deming (1982) believes the reduction in productivity was caused by the

defects, rework, and scrap. In order to promote continuous improvement. Ford Motor

uses six guiding principles based on Deming's fourteen points for top management.

The first of these principles is "Quality comes first"'^ (Shetty & Buehler, 1985, p.

149). Shetty and Buehler (1985) believe that one of the characteristics of high-

performance companies is, "Quality improvement is a catalyst for productivity

improvement," (p.325). L. Jerry Hudspeth, Vice President of Productivity and

^ Sumanth (1994), who coined the term PQ team, or PQTs (productivity and quality teams), maintained that PQTs place more emphasis on productivity and quality than QC circles, although they both improve quality and productivity. However, he did not claim that quality was improved by the improvement ofproductivity.

'^ The other five principles are customer focus, continuous improvement, employee involvement, surpass competitors in overall performance, and partnership with suppliers/dealers. Here we see the emphasis placed on putting quality first. That is, quality before productivity.

31

Quality at Westinghouse Electric Corporation and the first director of the

Westinghouse Productivit>' and Quality Center, indicates that 'whenever you find you

have a problem with productivity, it usually translates into a dimension of quality"

(Ryan, 1983, p. 6). Butts (1984), in his paper "The relationship of quality to

productivity," describes poor quality as "a vampire-like creature which takes bite

after bite out ofproductivity" (p. 38). Pantera (1985) asserts that quality is the key to

productivity. Garry (1985) stresses that "the quality road to productivity is the

shortest and most effective route to higher productivity" (p. 90). Ferchat (1987)

regards productivity as an issue of quality. Townsend (1990), who believes quality

and productivity are different, affirms that "quality incorporates productivity" (p. 7).

He emphasizes that only through quality improvement can productivity be enhanced.

Tribus (1992) points out that the route to increase productivity is through increasing

quality. He further states that, "if you want productivity you have to focus on quality

first" (p. 98). Hayes (1985) writes "Quality influences productivity by its effect on

profit, and drives it two ways: (1) quality influences sales and consequent income

from such sales..., and (2) quality increases internal efficiency and capacity by the

degree that sundry corrective actions are prevented" (p. 59). Barrett (1994) states

that, "An increase in the quality,..., of a product or a service at no added cost

constitutes a productivity gain" (p. 128). Hart and Hart (1989) think that with

improved quality, increased productivity will follow. Gitlow (1990) believes that

emphasizing only productivity will sacrifice quality and may even lower output.

32

Darst (1990) stresses that following correct procedures to ensure quality will result in

heightened productivity. Sumanth and Arora (1992) review the literature and

conclude that "improvements in quality lead to improvements in productivity" (p.

151). Omachonu and Ross (1994) attribute the misconception that increased quality

results in decreased productivity to those who rank productivity higher than quality as

the top priority in production. Therefore, it can be deduced that, "productivity and

quality have a direct relationship. As quality increases, productivity increases ~ not

the other way around," (Kaydos, 1991, p. 22).

Not many studies can clearly describe the relationship between quality and

productivity in detail because it is difficult to reach a consistent definition for

various companies.'' Lawler and Ledford (1983) indicate that even though "There is

wide agreement about the conceptual meaning ofproductivity, the major difficulties

are in applying the concept to specific organizations" (p. 5). Garvin (1988) says that

the best way to understand the relationship between quality and productivity "requires

an examination of their common sources of improvement" (p. 84). He further

indicates that there are few systematic studies on the relationship between quality and

productivity. Belcher (1987) indicates that the problem lies in the definition.

Hoffherr, Moran, and Nadler (1994) think productivity lacks a clear-cut definition

that can be used as a basis for measurement and aggregation. Therefore, it is obvious

' ' Sumanth (1994) classified various definitions and interpretations ofproductivity into three basic types. Partial productivity, Total-Factor productivity, and Total productivity. However, he did not mention that the definition of quality could also be unified.

33

that the relationship between quality and productivity is, as Smith (1990) claims,

dependent on how the definitions of each concept are expressed.

Because quality and productivity are so directly related, some people think

that the two are nearly the same. Adam, Hershauer, and Ruch (1981) state that,

"Frequently, scholars and practitioners alike refer to 'productivity' and 'quality' as if

they were two separate performance measures. Yet a significant part of any

producfivity equation is quality" (p. 12). Shetty and Buehler (1984) point out that the

Japanese regard quality and productivity as two neariy synonymous terms. Kaydos

(1991) thinks that productivity and quality are neariy synonymous. Thor (1993)

illustrates process quality and productivity are essentially the same. In their articles,

Katzan (1985), Smith (1986), Price (1989), and Federal Express (1993) all firmly

claim that quality equals productivity.

Although the relationship between productivity and quality is thought to be

positively correlated, it varies depending on how each concept is defined (Smith,

1990). Shetty and Buehler (1985) point out that productivity and quality are not new

ideas, but most companies have not clearly defined these terms.'' Harrington (1987)

thinks that the ideal indicator for measuring quality and productivity simultaneously

is to measure "the sum of all inputs divided into the quantity of output that met

customer expectations" (p. 104). However, it is difficult to calculate this ideal

indicator. Because of the various functions and activities in different departments

' In order for both quality and productivity to be organizationally effective terms, they must be operationally defined For further information on operational definitions refer to Deming (1986)

34

and companies, unless specifically defined, a universal fimction of the relationship

between quality and productivity can not be developed. However, Thor (1991)

provides his principles of measurement for both productivity and quality:

• Meet the customer's need; • Emphasize feedback directly to the workers in the process that is being

measured; • The main performance measure should measure what is important; • Measures should be controllable and understandable by those being

measured, and • Base measures on available data. If not available, apply cost benefit

analysis before generating new data.

Mohanty and Yadav (1994) believe that Total Quality Management is the base

to provide integration of quality and productivity. They also suggest some ways to

link quality and productivity:

• Viewing customer as the future assets of an organization; • Identifying and providing flexible responses to the needs of the

stakeholders; • Adding value at each stage of each operation; • Fostering respect for the human system; • Shifting emphasis from maximizing individual capitalist gains to

improving quality of life for the society as a whole.

Sumanth and Arora (1992) also propose a conceptual framework to illustrate

the quality-productivity link. In addition to the descriptive method, if quality and

productivity are specifically defined, a mathematical model linking quality and

productivity can be developed. By measuring quality as quality of conformance and

by defining productivity as total productivity, Sumanth and Wardhana (1993) present

a mathematical quality-productivity relationship model. From the results of the case

35

study in her dissertation, Harmon (1984) concludes that a firm's productivity has a

definite relationship to the product quality.

However, Kendrick and Creamer (1965) has indicated that after the Worid

War II, many companies obtained higher profitability v^th less productivity because

of the backlog in demand. This situation, again, shows that the market influence can

reverse the positively correlation between quality and productivity. Therefore, when

discussing or developing the relationship models among quality, productivity, and

profit, it is important to consider the market influence first.

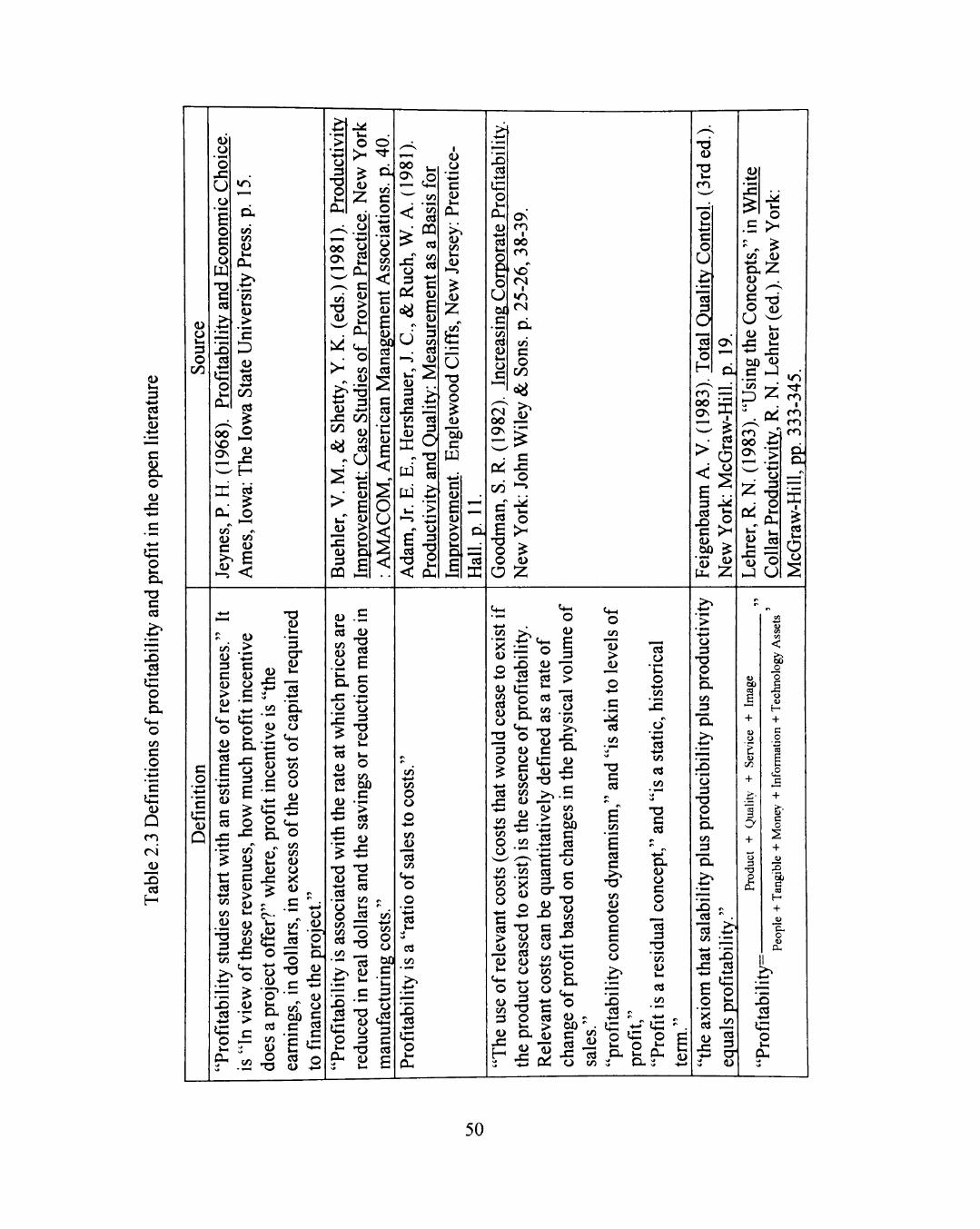

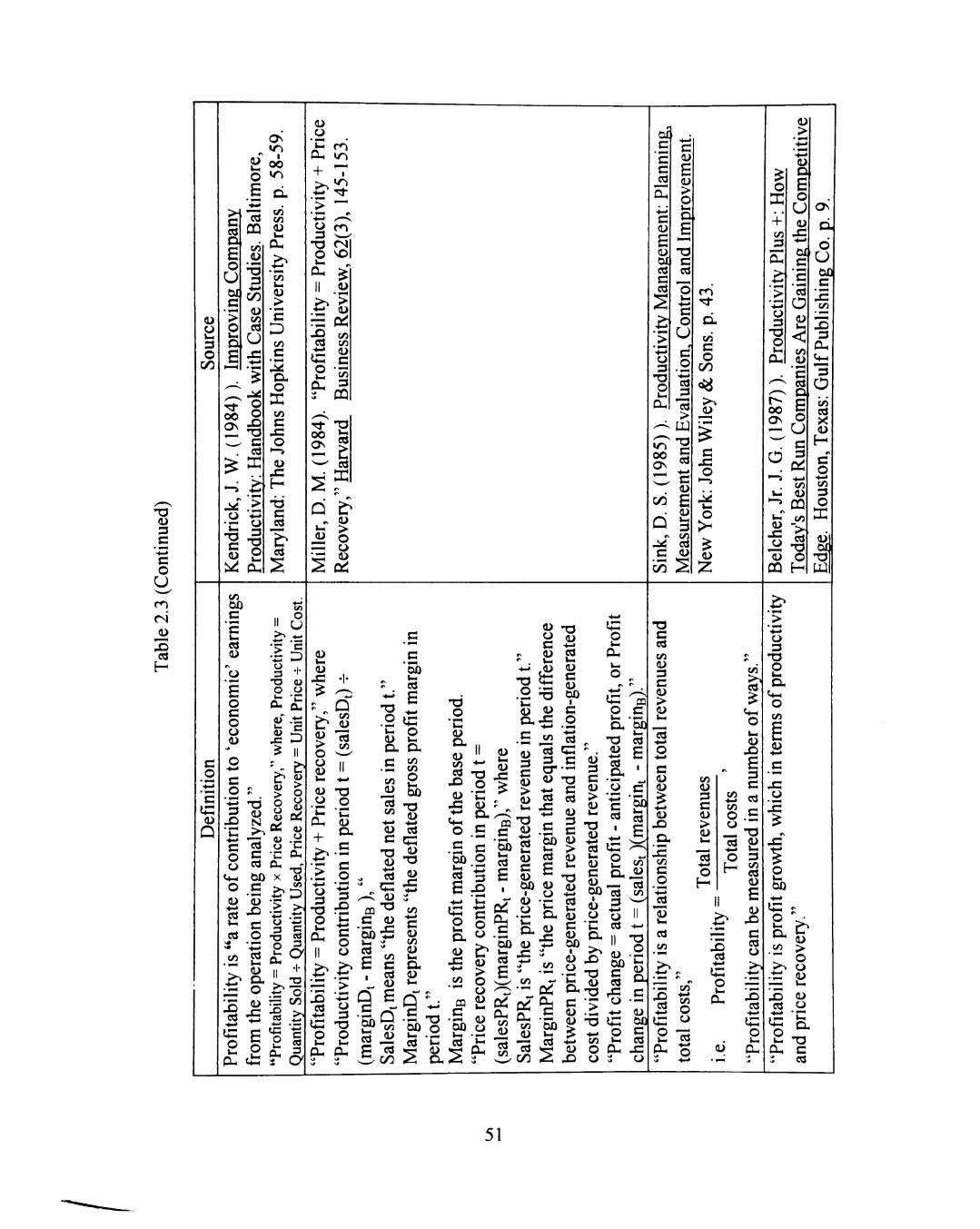

2.1.2 Definitions

Before developing the relationship between quality and productivity, it is

helpful to examine the definitions of these two terms. Although they are not new

concepts, people have created different definitions for each term. These definitions

are arranged in two tables (Table 2.1 and Table 2.2). In addition, since this research

is to link quality and productivity based on profit, summarized definitions of profit

and profitability are also listed in a table (Table 2.3). All definitions in both tables

are listed in chronological order. By examining these definitions, some findings

related to each term are also addressed.

36

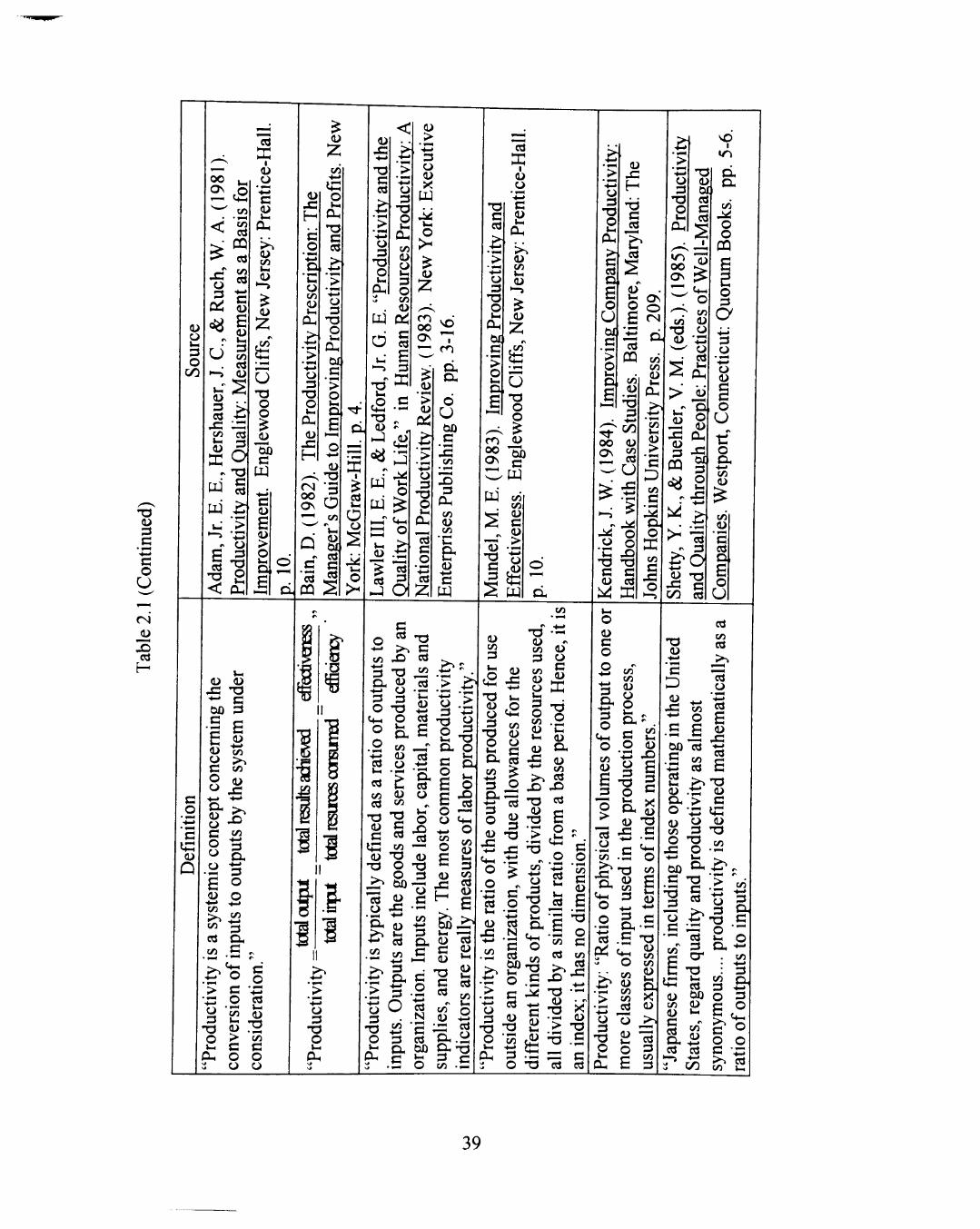

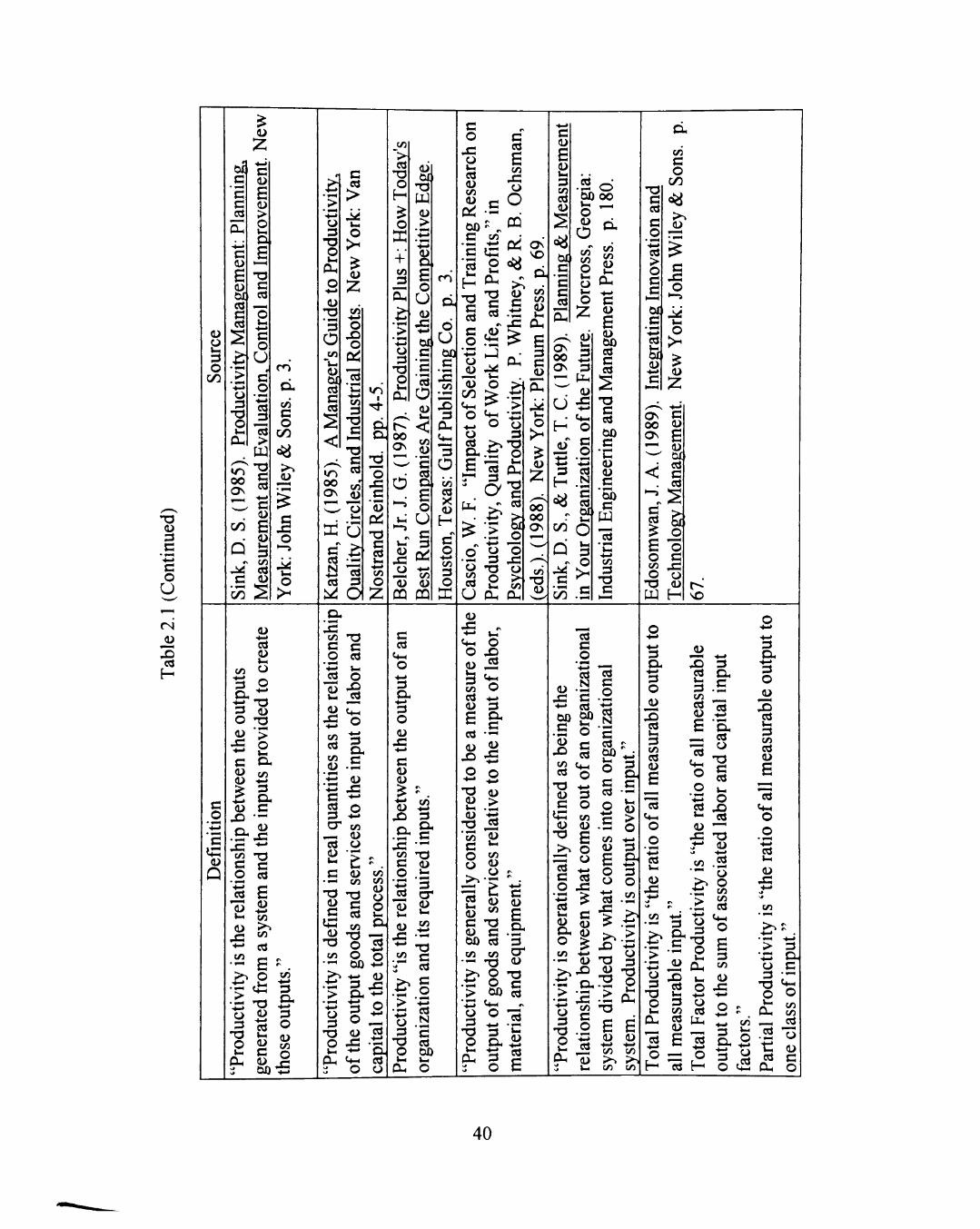

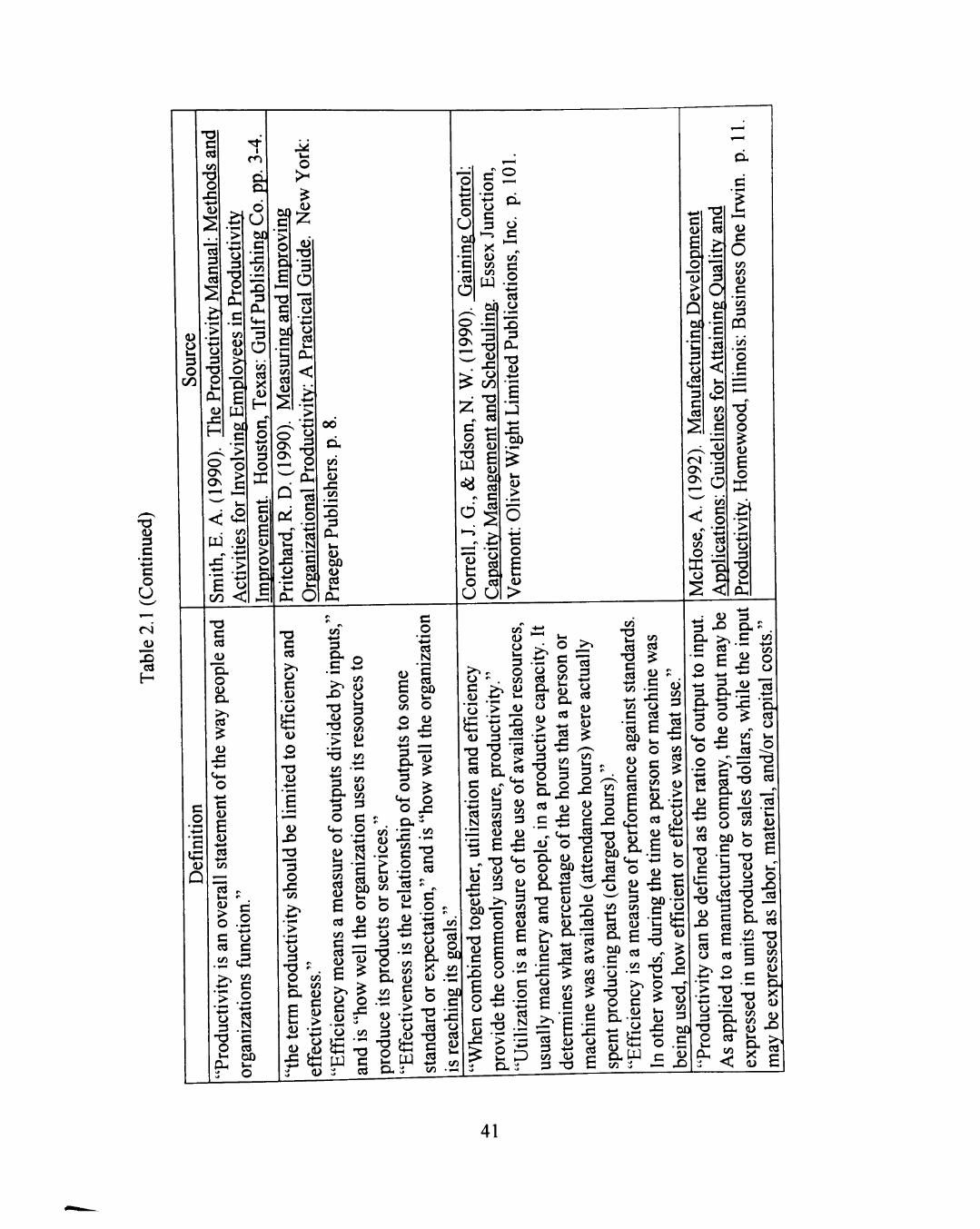

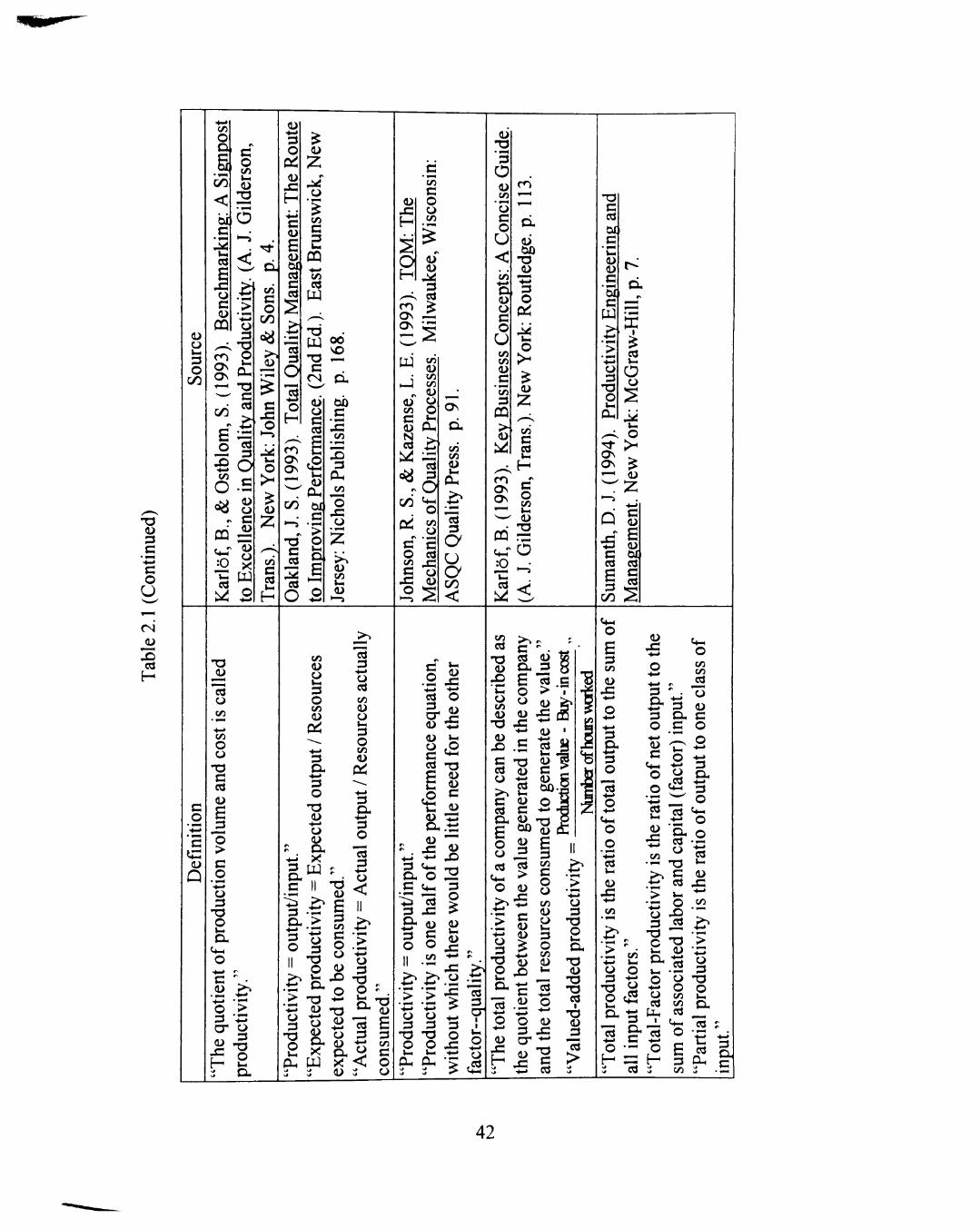

2.1.2.1. Definitions of Productivity

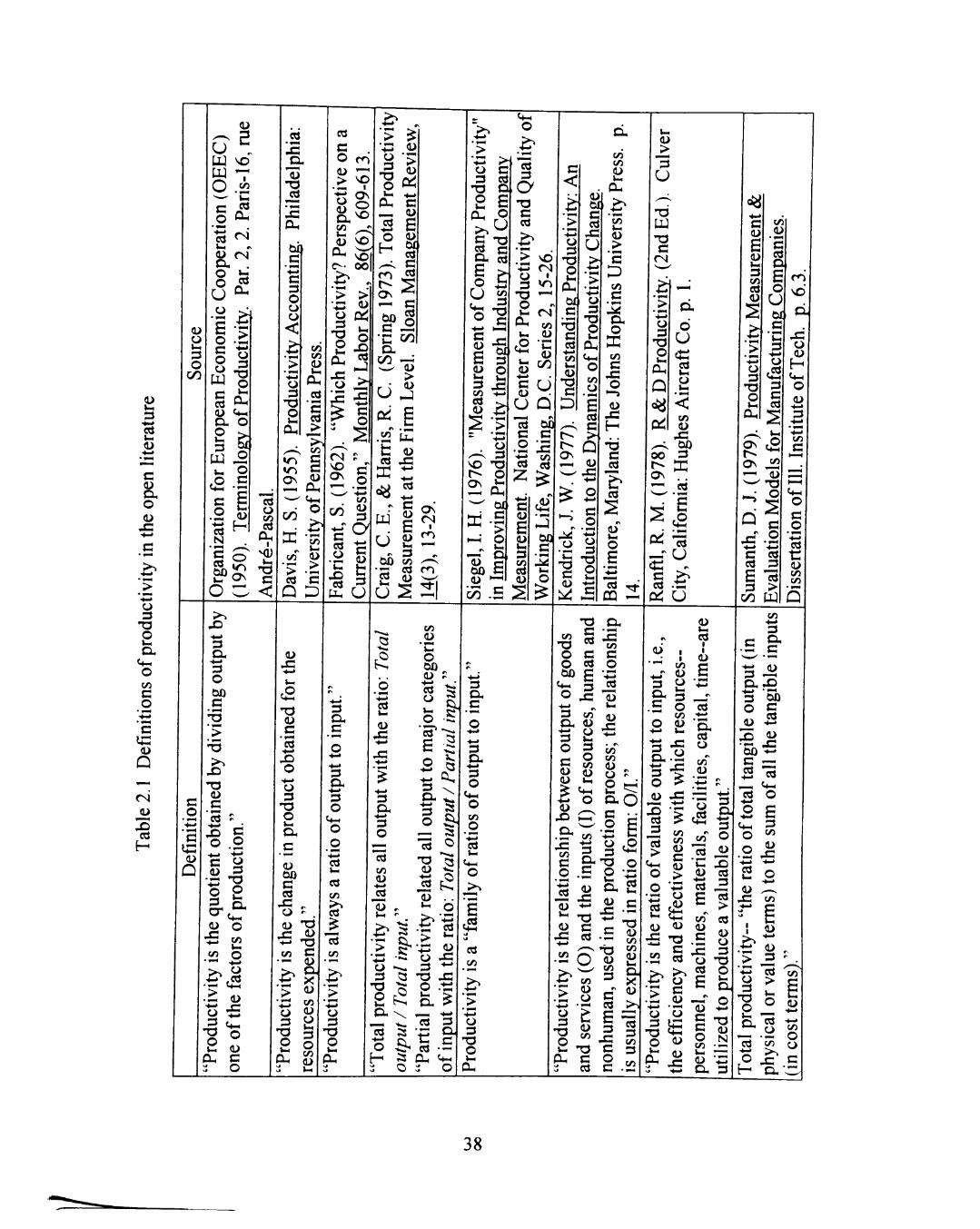

Table 2.1 presents some significant definitions ofproductivity in the open

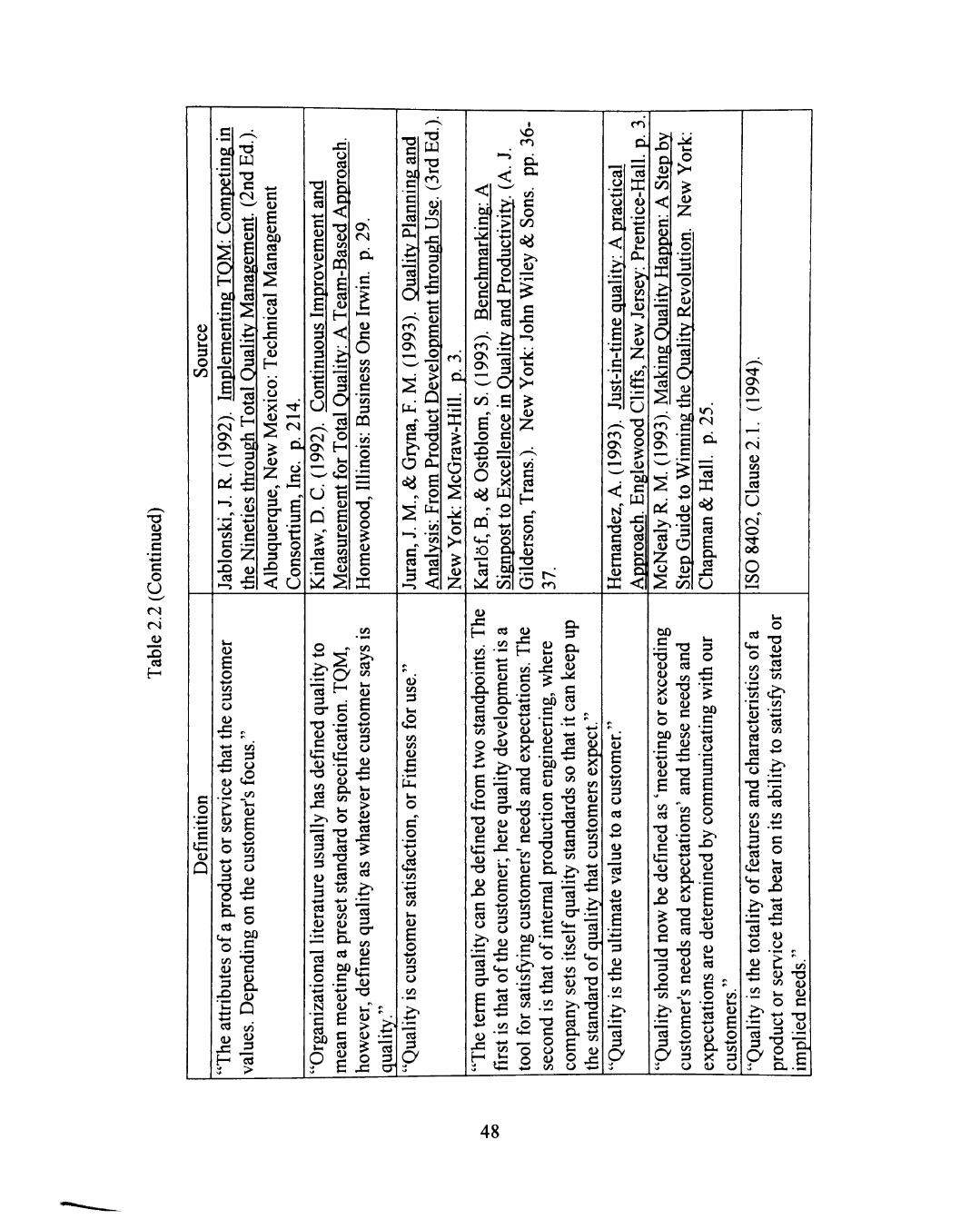

literature. From these definitions, several points can be concluded:

1. The core definition ofproductivity is the ratio of output to input.

2. Productivity ratios vary in measurement units. They can be measured in

%, dollars per hour, pieces per day, etc. If productivity ratio is measured

in revenue per cost, then it directly relates to profitability.

3. Productivity can only be measured for tangible inputs and outputs.

4. For different purposes of measuring productivity, there are a number of

different measurement approaches.

5. Productivity is closely related to effectiveness and efficiency.

6. The output ofproductivity assumes valuable product or services. That is,

the output does not include the valueless. Based on this assumption, it is

possible to relate productivity with quality.

37

<D •*->

* i » ^

C <u a-o

H—»

5 o 3 o

CO C o

c

38

(U

•4—» c o U

39

3

n o

U

o

3 o

00

t>4 c 'c c c3

c

c

3

o

oo ON

00

(L)

C (U

E > o l - l

D

B -o c

o U

o

>

C aj

• * - •

C U

s l - l

3 (/3

^ S CT)

( ^

en C o

I .§ o

o

u 3 o

0) T3

'3 O

a a >

o

o

X5 o

Vi 3

T3

N 3

Ol

<n

D.

c • 4 - j

O

C/3

CO -o o H

o

+ CO

•4-> o 3

TD O

0 0 ON

o

W

>

s o

U (U

c

O

o U c

3

(U

C/3

'S O Vi

&I

d U

C

3

(4-1 3 O X

H c o +-» 3 o

c

e V-i

3

c 'S c cd

.2 o bO 00 * - < 1 — 1

o ^ cL O

P 2e

^1 ON 0 0 ON

U H

3 H

l - l

3 • < - >

3 PH (D x :

••-» Ct-i

O c o

N ' c

U 3 ^ O

.S

(L>

cd C

c

"C u 0) C

'5Jb c

W

3

C3

c _o -4—>

> O

&4

'•4-»

•4-»

c

Vi c o

0 0

(L>

c x : o

o

O N G 00 u ON g

"-^ 04

< c

I s ^ o S -o o c 55 -G

t ^ vo

c '•4->

'5

Q

-4-» Cd

o -o > o

c a,

(U on

O d

l - l

x : •4-> cn

'•4->

o 3

ID •4-> cn > . cn

e . O ^

ci: 3

0) 3

CL» on O

x : 00

Vi TS

O cd •S »-' ed o

" -s

cn -S

«.s •S -G

2 o CT cn

- ^ 0) cd u

• — cn

S " ^ «« 'O o