accounting for overheads - absorption...

TRANSCRIPT

CPA SPM Prior Learning

© Cenit Online 2016

Accounting for Overheads - Absorption Costing Overheads are the costs incurred in the course of making a product, providing a service or running a department, but which cannot be traced directly and in full to the product, service or department. The three types of accounting for overheads we need to study are:

• Absorption Costing

• Marginal Costing

• Activity Based Costing The objective of absorption costing is to include in the total cost of a product “an appropriate share of the organisation’s total overhead”. An appropriate share is generally taken to mean an amount which reflects the amount of time and effort that has gone into producing a unit or completing a job. Absorption costing is therefore a method for sharing overheads between products / services on

a fair basis.

The main reasons for using absorption costing are; inventory valuations, pricing decisions and establishing the profitability of different products. It is also worth noting that financial accounting standards and in particular “IAS 2 Inventories” recommend using absorption costing to value inventory. In theory management accountants can use any method to value inventory so therefore have a choice to use absorption, marginal or activity based costing. However, if the company’s cost accounting and financial accounting records are integrated into a single set of accounting records, this removes the choice and the management accountant will have to use absorption costing to comply with IAS 2.

The three stages of absorption costing are:

• Allocation

• Apportionment

• Absorption

• Allocation is the process by which whole cost items are charged direct to a cost centre. A cost centre is generally a department. So if we have a supervisor for department A, and a supervisor for department B, the wages of these supervisors will simply be “allocated” to the relevant department. A problem arises when one supervisor may be responsible for two departments or cost centres and here we have to apportion the wages. Apportionment is used where the overhead cost is shared over several cost centres when allocation is not feasible or possible. E.g. the salary of a supervisor who is responsible for a number of cost centres. (See Aug 2009 Q1 part a). The first stage of overhead apportionment is to identify all overheads such as light and heat, rent, canteen etc. It is considered important that overhead costs should be shared out on a fair basis. The basis for apportionment in most cases would be:

CPA SPM Prior Learning

© Cenit Online 2016

Rent, rates, light and heat, repairs and depreciation of buildings � floor area occupied by each cost centre Depreciation, insurance of equipment � Cost or book value of equipment HR, canteen, welfare, first aid etc. � Number of employees or number of labour hours worked in each cost centre

Example:

Swan Ltd has two production departments (A and B) and two service departments (maintenance

and stores).

Details of next year’s budgeted overheads are as follows:

Light and Heat 19,200 Repair Costs 9,600 Machinery Depreciation 54,000 Rent and Rates 38,400 Canteen 9,000 Machinery Insurance 25,000 Total 155,200

Details of each department are as follows:

A B Maintenance Stores Total

Floor Area 6,000

4,000

3,000

2,000

15,000

Machine Value 48,000

20,000

8,000

4,000

80,000

Number of

Employees

50

40

20

10

120

Allocated Overheads 15,000

20,000

12,000

5,000

52,000

If we want to apportion light and heat for example, the fairest method of apportionment would

be to use floor area. The total floor area is 15,000 sq. meters and Dept. A uses 6,000 sq. meters of

this.

So to apportion a fair amount to department A we take the total light and heat overhead of 19,200 and we multiply that by 6000/15,000 = 7,680. For Dept. B it will be 19,200 x 4,000/15,000 = 5,120. For maintenance it will be 19,200 x 3,000/15,000 = 3,840 For stores it will be 19,200 x 2,000/15,000 = 2,560 If we total up our apportioned overheads of 7,680 + 5,120 + 3,840 + 2,560 = 19,200, you can see we have our total light and heat overhead of 19,200 but it is now fairly apportioned between cost centres. Can you apportion the remaining overheads? Give it a try and see if you can fairly apportion each overhead to each cost centre. Your total apportioned overheads should = 155,200!!!

CPA SPM Prior Learning

© Cenit Online 2016

Solution:

Item of Overhead: Basis of

Apportionment

A B Maintenance Stores Total

Heat and Light Floor Area 7680 5120 3840 2560 19200

Repair Costs Floor Area 3840 2560 1920 1280 9600

Machine Dep. Machine Value 32400 13500 5400 2700 54000

Rent and Rates Floor Area 15360 10240 7680 5120 38400

Canteen No of employees

3750 3000 1500 750 9000

Machinery

Insurance

Machine Value 15000 6250 2500 1250 25000

Total Apportioned

Overheads

78030 40670 22840 13660 155200

Allocated

Overheads

15,000 20,000 12,000 5000 52000

Total Overheads 93030 60670 34840 18660 207200

Service Department costs:

In the above example we have apportioned the costs of the general overheads, but what about the costs associated with the service departments i.e. maintenance and stores? Service costs also need to be apportioned. We apportion service costs to both production departments and service departments that use their services. Again it is considered important that service department overhead costs should be shared out on a fair basis. The basis for apportionment in most cases would be:

• Stores � No or cost of materials requisitions

• Maintenance � Hours of maintenance work done for each cost centre

• Production Planning � Direct labour hours worked on each production cost centre

Taking the above example of Swan Ltd Total Overheads were as follows:

A B Maintenance Stores Total

93030 60670 34840 18660 207200

(Remember both allocated and apportioned overheads need to be re-apportioned.)

CPA SPM Prior Learning

© Cenit Online 2016

If we are told that usage of Swan Ltd.’s service departments were as follows:

A B

Maintenance

Stores Total

Maintenance Hours

Used

5,000

4,000

-

1,000

10,000

No of Stores

Requisitions

3,000

1,000

1,000

-

5,000

We must now re-apportion out the Maintenance and Stores Overheads. Total Maintenance Overheads are 34,840 and these must now be apportioned out between the other three departments. We will do this based on Maintenance Hours used of which there is a total of 10,000. For Dep. A we have 34,840 x 5,000/10,000 = 17,420 For Dep. B we have 34,840 x 4,000 / 10,000 = 13,936 For stores we have 34,840 x 1,000 / 10,000 = 3,484 We must now add these figures onto the total overheads figure for each (and reduce maintenance to 0 as it has been re-apportioned out).

A B Maintenance Stores Total

Total Overheads 93,030 60,670 34,840 18,660 207,200

Apportion

Maintenance

17,420 13,936 -34,840 3,484 0

New Total Overheads 110,450 74,606 0 22,144 207,200

Next we must re-apportion the stores overheads. These will be done based on no of stores requisitions of which there are 5,000. However as we have apportioned out Maintenance already we will not include the 1,000 requisitions relating to maintenance so we will have 4,000 instead. For Dep. A we have 22,144 x 3,000/4,000 = 16,608 For Dep. B we have 22,144 x 1,000/4,000 = 5,536 Again we now add these figures onto the total overheads figure for each (and reduce stores to 0 as it has been re-apportioned out).

A B Maintenance Stores Total

Total Overheads 93,030 60,670 34,840 18,660 207,200

Apportion

Maintenance

17,420 13,936 -34,840 3,484 0

New Total Overheads 110,450 74,606 0 22,144 207,200

Apportion Stores 16,608 5,536 0 -22,144 0

Final Total Overheads 127,058 80,142 0 0 207,200

CPA SPM Prior Learning

© Cenit Online 2016

As we can see the total overheads for Swan Ltd have at no stage changed from 207,200. It is just a matter of allocating and apportioning out the overheads fairly. Absorption is the process whereby overhead costs allocated and apportioned to cost centres are added to unit, job or batch costs. Overheads are usually added to cost units using a predetermined overhead absorption rate, which is calculated from the budget using a 4-step process:

1. Estimate the overhead likely to be incurred during the coming period. 2. Estimate the activity level for the period. This could be total hours, units or direct costs or

whatever we wish to base the overhead absorption rates upon. 3. Divide the estimated overhead by the budgeted activity level. This produces the overhead

absorption rate. 4. Absorb the overhead into the cost unit by applying the calculated absorption rate.

Example: Ace Co

Ace Co makes two products, the King and the Queen. Kings take 2 labour hours each to make and Queens take 5 labour hours. Ace Co estimates that 100,000 labour hours will be worked and overheads are expected to be €50,000 in the coming year. What is the overhead cost per unit for Kings and Queens if overheads are absorbed on the basis of labour hours?

Solution:

Step 1 � Overheads are estimated at €50,000 Step 2 � Labour hours are estimated at 100,000 Step 3 � €50,000 100,000 hrs. = €0.50 per labour hour Step 4 � King Queen Labour Hours per unit 2 5 Absorption Rate per labour hour €0.50 €0.50 Overhead absorbed per unit €1 €2.50

As we can see there is a great lack of precision about the way an absorption base is chosen. This

arbitrariness is one of the main criticisms of absorption costing, and if absorption costing is to be

used then it is important that the methods used are kept under regular review.

The most common bases of absorption are direct labour hour rate or machine hour rate.

• A direct labour hour basis is most appropriate in a labour intensive environment.

• A machine hour rate is used in departments where production is controlled by machines.

• A rate per unit would only be effective if all units were identical.

Example Overhead Absorption: The budgeted production overheads and other budget data of

BC Co are as follows:

Budget Dept. A Dept. B

Overhead Cost € 36,000 € 5,000

Direct Materials cost 32000

Direct Labour Cost 40000

Machine Hours 10000

Direct Labour Hours 18000

Units of Production 1000

Calculate the Overhead Absorption Rate of each department.

CPA SPM Prior Learning

© Cenit Online 2016

Solution:

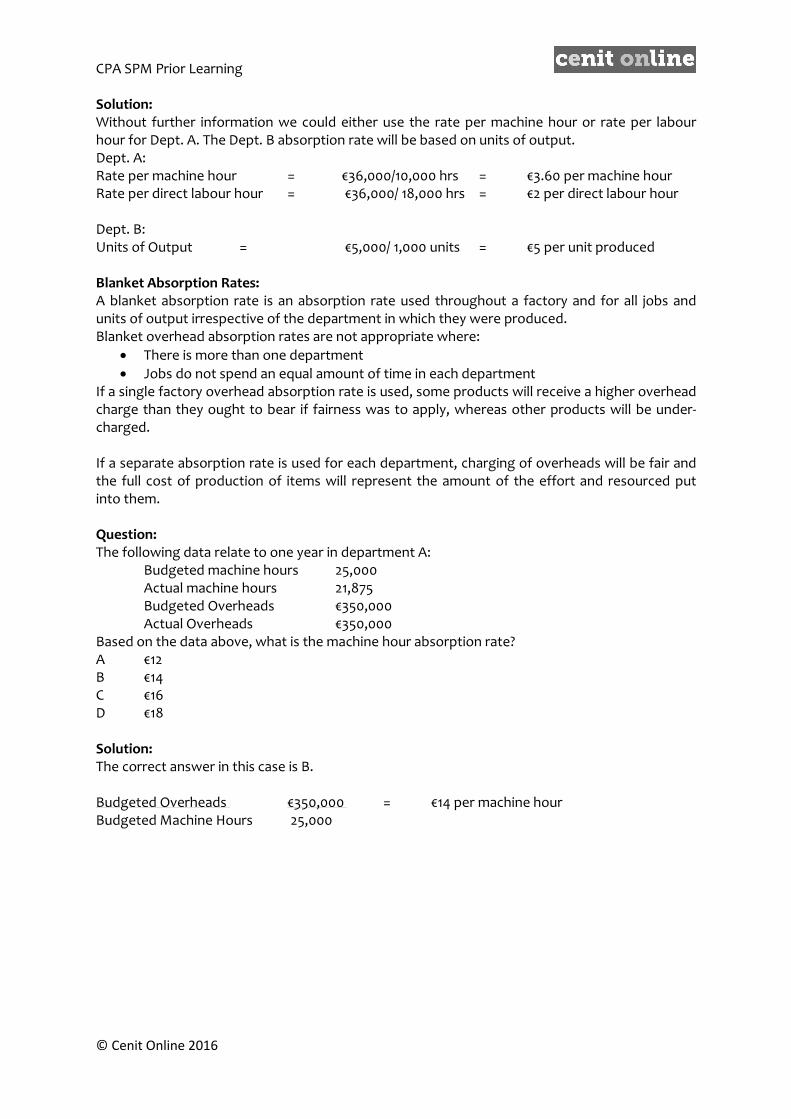

Without further information we could either use the rate per machine hour or rate per labour hour for Dept. A. The Dept. B absorption rate will be based on units of output. Dept. A: Rate per machine hour = €36,000/10,000 hrs = €3.60 per machine hour Rate per direct labour hour = €36,000/ 18,000 hrs = €2 per direct labour hour Dept. B: Units of Output = €5,000/ 1,000 units = €5 per unit produced Blanket Absorption Rates:

A blanket absorption rate is an absorption rate used throughout a factory and for all jobs and units of output irrespective of the department in which they were produced. Blanket overhead absorption rates are not appropriate where:

• There is more than one department

• Jobs do not spend an equal amount of time in each department If a single factory overhead absorption rate is used, some products will receive a higher overhead charge than they ought to bear if fairness was to apply, whereas other products will be under-charged. If a separate absorption rate is used for each department, charging of overheads will be fair and the full cost of production of items will represent the amount of the effort and resourced put into them. Question:

The following data relate to one year in department A: Budgeted machine hours 25,000 Actual machine hours 21,875 Budgeted Overheads €350,000 Actual Overheads €350,000

Based on the data above, what is the machine hour absorption rate? A €12 B €14 C €16 D €18 Solution:

The correct answer in this case is B. Budgeted Overheads €350,000 = €14 per machine hour Budgeted Machine Hours 25,000

CPA SPM Prior Learning

© Cenit Online 2016

Over and under absorption of overheads:

Over and under absorption occurs because the predetermined overhead absorption rates are based on estimates. It is quite likely that either one or both estimates will not agree with what actually occurs. Over absorption means that the overheads charged to the cost of sales are greater than the overheads actually incurred. Under absorption means that insufficient overheads have been included in the cost of sales. Example:

The budgeted overhead in a production department is €80,000 and the budgeted activity is 40,000 direct labour hours. The overhead absorption rate using a direct labour hour basis would be €2 per direct labour hour. Actual overheads in the period are €84,000 and 45,000 direct labour hours are worked. Calculate the under or over absorption of overheads.

Solution:

Overhead incurred (actual) €84,000 Overhead absorbed (45,000 x €2) €90,000 Over absorption of overhead €6,000

Question:

Solution:

CPA SPM Prior Learning

© Cenit Online 2016

Sample Q from F2 Man Acc

CPA SPM Prior Learning

© Cenit Online 2016

Solution:

CPA SPM Prior Learning

© Cenit Online 2016