chapter 5- stake holder analysis -...

TRANSCRIPT

123

Chapter 5- Stake holder Analysis

124

5. Stakeholder Analysis

Defining Stakeholders

The actual word ―stakeholder‖ first appeared in the management literature in an internal

memorandum at the Stanford Research Institute (now SRI International, Inc.,), in 1963.

The term ‗stakeholder‘ has numerous definitions, many of which are linked to the context

in which the term is being used. Schmeer (1999) suggested that stakeholders can include

members, employees, related organizations, potential partners, suppliers, the public,

regulatory bodies, and the government. Not-for-profit organizations and the voluntary

sector may also add clients, community groups, community leaders, volunteers and donors

to their list of stakeholders. In commercial organizations customers and owners are also

included as key stakeholders. Freeman (1984), whose work is credited for the development

of stakeholder theory and his seminal book titled ―Strategic Management- a Stakeholder

Approach‖ defines stakeholders as:

“A stakeholder in an organization is any group or individual who can affect or is affected

by the achievement of the organization‟s objectives”.

Thus, for the current study, the stakeholder is defined as:

―An individual, group or organization which has a share or interest in insurer-provider

relationship and is a party that affects or can be affected (either positively or negatively) by

the proposed strategies for synergy between provider and insurer‖36

.

The notion of ―paying attention to key stakeholder relationships‖ (Freeman, 1999) is and

has been a major theme in the strategic management literature. In fact, superior stakeholder

satisfaction is critical for successful companies in a hypercompetitive environment

(D‘Aveni, 1994). Empirical research has begun to investigate what determines the success

or failure of relationships between exchange partners. This has been accomplished by

examining both the characteristics of the organization as well as the specific stakeholder

groups and the nature of the interaction between them (Pfeffer, 1981; Jensen & Meckling,

36

Note: The definition is linked to our theoretical model, unit of study and the strategic triangle.

125

1976; Morgan & Hunt, 1994; Parsons, 2001). An assumption has been made in much of

the empirical and conceptual work is that developing and maintaining relationships are

desirable goals for both the stakeholder and the organization (Dwyer, Schurr & Oh, 1987;

Wilson, 1995). The Canadian Association (2004) informs that whether an organization is

working on a strategic plan, developing a policy or planning to implement an action, it is

essential to consult with key stakeholders as this is an important factor in achieving

ultimate success.

The stakeholder concept is deceptively simple. It is ―simple‖ because it is easy to identify

those groups and individuals who can affect, or are affected by the achievement of any

organization‘s purpose. It is ―deceptive,‖ because once stakeholders are identified; the task

of managing the relationship with them is enormous. The variety of ―stakes,‖ the necessity

of looking at multiple levels of analysis and the need to invent processes for taking

stakeholder concerns into account make a stakeholder approach to strategic management

quite complicated (Freeman, 1984).

The stakeholders Map

Figure 5.1: Potential Other Stakeholders in the Health Insurance Market

Source: Author‟s own creation

126

Table 5.1: Stakeholders - Rational for engagement and Competency (I)

Stakeholder Rationale for engagement Competency

Insured

Customers

They are the ultimate beneficiary in the health insurance

market and a common customer to both the insurers and

the providers.

Competency is low

both at treatment

and health

insurance level.

Doctors Doctors play an important role at the time of treatment of

insured patients and their decision has a direct impact on

the claim cost. They are the final decision maker when it

comes to line of treatment and their authority cannot be

easily challenged.

High competency

level w.r.t

treatment part and

Medium to low

w.r.t. health

insurance

Nursing Staff They play a major role in the delivery of health care

services. They are in direct touch with the insured patient

and spend more time with the patients than the treating

doctors. They can act as a source of control and

verification. Also, as a sharing resource.

Medium level

w.r.t. treatment

and low w.r.t

health insurance

Brokers Brokers are the intermediary between the insured and the

insurer. As per law they act on behalf of the insured

customer and get their commission from the insurance

companies. In corporate health insurance they play a major

role in decision making.

High competency

w.r.t. insurance

knowledge , less to

moderate in terms

of treatment and

healthcare

Agents and

Advisors

They act as an important intermediary at an individual

level. They are the connecting link between the customer

and the insurance companies. As per law they need to have

appropriate licensing. In retail policy, they are the

individuals who fill the proposal form for health insurance.

Moderate to high

w.r.t. insurance

and low w.r.t.

treatment and care

part

TPA They are the extended arm of the insurance company and

are regulated by the IRDA. They play an important role in

extending cashless benefit, contract negotiation with

providers, enrollment and claim administration. Off late

they have started providing services like pre-policy check-

up, underwriting, value added services like health check-up

and fraud investigation services.

High w.r.t health

insurance and

moderate to high

w.r.t. treatment

and care part

NGOs and

Community

at large

In the rural space the role played by the NGOs is quite

critical. The social health insurance schemes depend

heavily on the support of the community at large. There are

NGOs which are working in the area of microfinance and

health insurance. They can help in the implementation of

social health insurance policies and also monitoring the

delivery of health care services at the local level.

High to moderate

in their respective

areas (NGOs).

Moderate to low

(community at

large)

127

Table 5.2: Stakeholders - Rational for engagement and Competency (II)

Stakeholder Rationale for engagement Competency

Regulator In India insurance industry is regulated by IRDA.

They are responsible for licensing of insurance

companies, TPAs, agents and brokers and ensure

orderly growth of the insurance industry. All the

health insurance products which are launched in the

market had to be filed with the regulator. They also

play a role in handling customer grievances. As

regulators they have extreme powers to change the

growth trajectory of the health insurance industry.

High w.r.t.

insurance.

Moderate to low

w.r.t. health care

and treatment part

Govt. Bodies The ministry like Finance, Health& family welfare can

play a major role in developing and launching policies

which can have a big impact in the Indian health

insurance market (affecting both the insurers and

providers) e.g. The increasing of FDI in insurance

sector from current 26 percent to 49 percent; health

insurance portability act; clinical establishment

(registration and regulation) bill. The State bodies can

also play an important role as health is a State subject.

High in their

respective areas

Pharmaceutical&

Medical

Equipment

Industry

They play a major role in healthcare industry and are

considered to have a strong lobby at the policy level.

They have the financial strength and power to directly

affect the cost of health care. They are the major

suppliers for the providers and has the potential to

create value added services for the insurance industry

e.g. offering discounts on pharmacy and diagnostics.

Their existing relationship with providers and doctors

can act as a source for developing synergy between

insurers and providers.

High in the area of

treatment and

medical care, low

in the area of

insurance

I.T Industry They affect both the insurance and the healthcare

industry. Information technology can play an

important role in bringing in efficiency and

effectiveness. They can help built a strong

communication bridge between the insurance

companies, intermediaries and the providers. It also

has the potential to affect the cost part apart from

supplying analytical tools for better decision making.

High in their

respective areas

Education

Institutions

In health insurance industry they play a major role in

supplying quality and trained manpower across the

levels and intermediaries. They can act as a source of

center for excellence in health insurance and fulfill the

talent gap currently existing in the health insurance

industry both at the technical and managerial levels.

High in their

respective areas

128

For the purpose of the current study and based on the above definition, the following are

identified as potential stakeholders: Insured; Doctors; Nursing Staff; Brokers; Agents and

Advisors; TPA‘s; NGOs and Community at large; Regulator; Govt. Body; Pharmaceutical

and Medical Equipment Industry; I.T. Industry and Education Institutions (Figure 5.1).

If one consider health insurance companies and health care providers as organizations

aiming to bring in synergy then studying their relationship with the above listed

stakeholders becomes important. The list of stakeholders had been tabulated stating the

rationale for engagement along with their competency in the areas of insurance and

healthcare respectively. Each of the stakeholders is directly or indirectly associated with

the health insurance industry and has the potential to affect the level of synergy among

insurers and providers (see Table 5.1 and Table 5.2). The level of competencies in the

areas of insurance and healthcare differ drastically.

At one end we have stakeholder like the insured customers where the level of competency

is low; stakeholders like government bodies, IT industry, education institution where the

competencies is high (in their respective area); and finally there are stakeholders like TPAs

where the competencies are high both at the insurance and the healthcare level. As could

be seen in the rational for engagements, each stakeholder affect or has the potential to

affect the relationship between the insurers and the providers. Each one of them plays a

participatory role in either developing or destroying synergy among insurers and providers.

As had been argued earlier it is important to undertake the stakeholder‘s analysis to

understand their areas of interest, relationship, attitude and their power to influence

synergy between insurers and providers. Any strategic framework developed for synergy

between insures and providers cannot be successful if it is not acceptable by the different

stakeholders. The stakeholder analysis that includes studying their interest, attitude,

relationship and power to influence would help identify factors affecting synergy among

insurers and providers.

During our investigations and interactions with different stakeholders group different

factors were identified that could either help develop or destroy synergy among insurers

129

and providers. For better understanding, the findings of the key stakeholder groups are

clubbed under five different categories i.e. insured, government and regulatory bodies,

health care professionals (doctor and nursing staff), intermediaries (agents, brokers, TPAs)

and other (NGOs, education institutions, pharmaceutical Co., etc.). This is then followed

by summarizing the key factors identified during the stakeholder analysis.

5.1 Insured

The insured customers are one of the most important stakeholders when it comes to

identify the strategy for synergy between insurers and providers. They are the major

connecting link between the insurers and the providers. In the absence of the insured

customer, the study of relationship between insurers and provided would be of no value.

The relationship of other stakeholders with the insured customer could be seen in Figure

5.2. There are many direct linkages and a few in-direct ones. There are also cross linkages

that have the potential to affect the relationship among insurers and providers.

Figure 5.2: Stakeholder’s Interaction Network

Source: Author‟s own creation

130

In the Indian context, the insured customer can be classified into three different categories.

The first category is that of the retail customers, a customer who either purchases the

insurance policy for either self or for family. The product offering are not as

comprehensive as in the other categories like group policies, but there are options

available. This section of insured population is currently low because of multiple reasons.

Some of the reasons includes: less importance given to health insurance over areas like

education, home, vehicle, children‘s marriage and alike; problems with claim processing;

limited product coverage; limited options for doctors and hospitals; agent and payment

related issues; expensive; complicated policy document and limited awareness. However,

this segment is being seen as a big opportunity by most of the upcoming health insurance

companies and there are efforts being made to lure the retail customers.

The second category is of corporate clients where the insured are the employees of

corporation or a business entity. In few cases in addition to the employees their dependents

are also covered. Here, the dependents may be defined as the immediate family (self,

spouse and children) or can include extended family (self, spouse, children and parents).

Since, this segment has been traditionally buying the health insurance cover in bulk; the

products offerings are more comprehensive. Here, additional benefits like the maternity

and outpatient are covered which are lacking in the retail segment. Because of its size this

segment is often further broken into special categories like small and medium enterprises

(SME), gold, silver and platinum clients. This categorization may not necessary be based

on the health insurance premium but could be on the overall health insurance premium

generated by the corporate clients. The corporate clients are more exposed to the concept

of health insurance and have a dedicated department responsible for managing the health

insurance piece.

The third category is of government sponsored scheme commonly termed as ―Mass‖

business. At times this category also falls under the definition of micro-insurance schemes.

The insured under this category are associated or member of a special group. This group

will have individuals of same occupation like weavers and artisan or of same socio-

economic strata like the below poverty lines.

131

Table 5.3: Stakeholder Analysis- Customer Awareness

Awareness

Potential

Customer

Insured Customer

without any Claim

Experience

Insured

Customer with

Claim

Experience

i. About Insurance Poor Poor Average

ii. Policy T&C Poor Poor Poor

iii. Cashless hospitalization Poor Poor Average

iv. TPA Poor Average Good

v. Insurance Company Poor Average Average

vi Network hospitals Poor Poor Average

Source: Summarized on the basis of Focus Group Discussions (FGD‟s) of different

categories of Insured Customers.

One of the examples of this category is the RSBY policy where the below poverty line

individuals and their family get cover for health insurance. It is only recently that the

IRDA has asked all the general insurance companies and the standalone health insurance

companies to submit the break-up health insurance data (for the year 2009-2010) for

individuals, corporate group and government sponsored schemes. For current filed study

the focused was on three types of insurance customer i.e. one who is a potential customer,

insured customer (with claim experience) and insured customer (without any claim

experience). Interestingly there were few factors which were common across all the

categories of customer like lack of awareness.

It was found that the level of awareness about insurance, policy terms and conditions,

cashless hospitalization process and details about network hospitals was poor for both

potential customer as well as customers without any claim experience. For those customers

who had experienced submitting a claim with either a TPA or an insurance company were

found to have fair idea about the TPA‘s and the cashless hospitalization process.

132

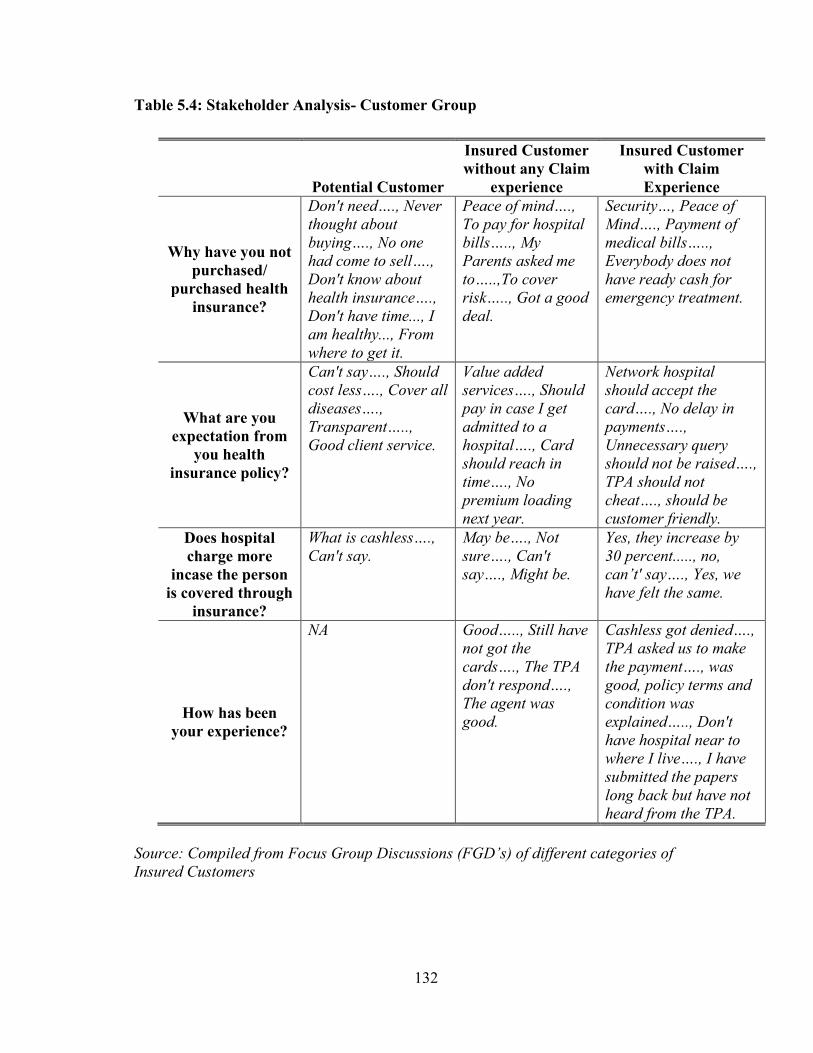

Table 5.4: Stakeholder Analysis- Customer Group

Potential Customer

Insured Customer

without any Claim

experience

Insured Customer

with Claim

Experience

Why have you not

purchased/

purchased health

insurance?

Don't need…., Never

thought about

buying…., No one

had come to sell….,

Don't know about

health insurance….,

Don't have time..., I

am healthy..., From

where to get it.

Peace of mind….,

To pay for hospital

bills….., My

Parents asked me

to…..,To cover

risk….., Got a good

deal.

Security…, Peace of

Mind…., Payment of

medical bills…..,

Everybody does not

have ready cash for

emergency treatment.

What are you

expectation from

you health

insurance policy?

Can't say…., Should

cost less…., Cover all

diseases….,

Transparent…..,

Good client service.

Value added

services…., Should

pay in case I get

admitted to a

hospital…., Card

should reach in

time…., No

premium loading

next year.

Network hospital

should accept the

card…., No delay in

payments….,

Unnecessary query

should not be raised….,

TPA should not

cheat…., should be

customer friendly.

Does hospital

charge more

incase the person

is covered through

insurance?

What is cashless….,

Can't say.

May be…., Not

sure…., Can't

say…., Might be.

Yes, they increase by

30 percent....., no,

can‟t' say…., Yes, we

have felt the same.

How has been

your experience?

NA Good….., Still have

not got the

cards…., The TPA

don't respond….,

The agent was

good.

Cashless got denied….,

TPA asked us to make

the payment…., was

good, policy terms and

condition was

explained….., Don't

have hospital near to

where I live…., I have

submitted the papers

long back but have not

heard from the TPA.

Source: Compiled from Focus Group Discussions (FGD‟s) of different categories of

Insured Customers

133

However, their awareness about the policy terms and conditions were found to be poor.

For summary of the findings about the level of awareness refer to Table 5.3.

During interview different set of questions were asked and the responses were noted. There

were similarities found in the need for purchasing of health insurance by different

categories of customers. The expectations of the insured customers with past claim

experience were higher than that of a potential customer. Also, this group suggested that

the providers charges higher in-case of cashless hospitalization. The overall experience

was different for customer without any claim history with that of customers who had

lodged either a claim with the insurers or had availed the cashless services. The sample of

the interactions is presented in Table 5.4.

5.2 Government and regulatory bodies

Some critics argue that the government intervention in the market place has real social

benefits that would not have occurred without government action. For example- the health

insurance policies for the below poverty line (RSBY scheme), where the BPL family gets

covered for a sum insured of 30,000 rupees by just paying a fee of 30 rupees.

Here, the total premium paid to the insurance company per BPL family is somewhere

around 800 rupees, where the balance 760 rupees is paid by the Central and State

government (Central share is 75 percent, whereas State share is 25 percent). Had the

government not initiated this policy, the BPL families would not have got the health

insurance cover. However, just paying the major chunk of the premium does not ensure

real improvements in health of the BPL family. This could be an important area of further

research, to see if schemes like RSBY are able to improve the health status of the families

who get benefit out of such health insurance schemes.

The insurance regulator has taken multiple initiatives for the orderly growth of health

insurance industry. For example, it has form a joint working committee to look in to the

area of health insurance. It has licensed few stand alone health insurance companies and is

looking into the recommendation of reducing the working capital requirement for

134

standalone health insurance companies. The insurance regulator has done quite a fair job in

handling customer grievances. Recently, it has opened a call center, where the customer

can lodge their complaints.

Based on the current investigations, it was found that the major areas of interest for the

government are in the area of awareness, trust and transparency and to improve the health

infrastructure in the Country. The key themes and factors that emerged are discussed

below:

5.2.1 Lack of Access

One of the concerns raised was the lack of access for the insured customer when it comes

to accessing cashless benefit at hospitals. It was told that currently only the private

hospitals are included in the list of insurers and most of these providers have profit

motives. Also, in spread of these providers are primarily in the urban areas. There is a lack

of access for insured those who live in rural and semi-urban areas. If health insurance fails

to provide access to hospital care for treatment of illness covered under health insurance

then one of its key utility will be lost. The reasons which could lead to lack of access are:

unavailability of hospitals in a given geography, no network tie-up by the insurance

company in a given geography, unavailability of hospital beds in the given hospital, denial

of admission or non-acceptance of health insurance card by the provider, etc.

To make health insurance successful, it was felt that there is a need for both insurers and

providers to come together and to provide access to care and cashless benefit to all sections

of society.

5.2.2 Need to improve trust and transparency

It was suggested that there is a pressing need to develop trust and transparency within the

health insurance system. There were also comments which highlighted that at times the

parties are not fair in their approach. This observation gets validated by one such instance

where few public sector insurers stopped cashless facility in metro cities due to losses in

their health insurance portfolio without consulting the providers. It was told that both the

insurers and providers question the honesty of each other. The insurers think that the

135

providers are not honest in their dealings and charges more money from insured patients

and on the other side the providers think that insurers are here to make profit and do not

care either about them or about the poor customers. It is important that both of them work

together to develop trust and transparency. This will help in the growth of Indian health

insurance industry.

5.2.3 Improve existing health infrastructure

As per the government and regulatory bodies the level of medical infrastructure is very

poor in our country and in most of the rural areas the private facility is almost negligible. It

was thought that if insurers and providers could come together then it would help build

health infrastructure in the rural areas. The example of RSBY was given to justify the

same. It was evident that the government has the powers to influence the current

relationship between insurer and providers not merely by introducing new schemes for the

general population who can‘t afford to pay the health insurance premium but also by

bringing changes in the current regulatory regime. The insurers and providers must make

efforts to affect the public policy in a way that helps develop synergy between them.

5.3 Healthcare professionals (Doctors, Hospital Administrators and Nursing Staff)

Health professionals are one of the key stakeholders in the relationship between insurers

and providers. It is this group that delivers the actual service to the insured customer and

determines the cost of care. Without this group neither the hospitals nor the insurers

(providing health insurance benefit) can survive. The interactions with this group were the

most interesting and insightful one. This may be because they are at the center of all the

activities linked to health insurance claims. It is on the advice of the treating doctors that

the cashless benefit is triggered. It is the treating doctor who decides the line of treatment

for the insured patient and not the insurer. It is the nursing staff that provides care to the

insured patient and not the sales staff of an insurance company. Thus, it may be argued that

the power of this group to influence customer satisfaction is the highest.

136

The key themes and factors that were brought into light includes: Lack of ownership by the

insurers and TPAs; Delays in provider payments; Lack of referral system; Poor doctor and

insurer relationship; Criteria‘s for selection of providers; Lack of standardization; Training

issues, and the need to have a robust grievance handling mechanism for addressing

provider issues. All these factors are briefly discussed as under:

5.3.1 Lack of ownership

During our interaction with the healthcare professionals it was informed that both the

insurers and the TAP‘s do not own the patient at the time of need. There are situations

where the patient is asked to speak to different parties to get the cashless claim processed.

During our interview with doctors, one critical comment which came was that there is no

effort by the insurance regulator to visit and meet network providers and seek their

feedback for insurance companies and TPA‘s i.e. to understand the problems faced by the

providers and then take corrective actions. Some suggested that there is no ownership by

the TPA‘s ( the issue linked to lack of ownership is discussed separately), few of them

pointed out that they are not able to control cost, are just profit making agency without

focusing on service, have poor quality of manpower and are involved in fraudulent

practices and sharing data with competitors.

5.3.2 Delay in provider payments

The study findings suggest that the providers do not receive payment in time and that it is

perceived as a critical factor by the providers while evaluating the services of the TPAs

and insurance companies. It was observed that delays in payment to providers are at times

being used as a rationalization for charging more money from the insured patients. During

our discussion with this group it was found that if the payments to providers are made well

within the agreed timeframe then it would help built confidence in the minds of the

providers for the services promised by the insurers. This will also affect the level of

services offered to the insured patients. For example, when asked why the providers take

advance deposit from insured patients it was told that this is because there had been past

cases wherein the payments were delayed either by the insurers or the TPAs.

137

5.3.3 Lack of referral system

During our interaction with doctors and the hospital administrators it was told that in the

Indian context we don‘t follow any referral system in the private space. This has a direct

impact on the hospital occupancy rate and cost of treatment. It was informed that even for

a normal cold and fever the insured visits a super specialty hospital and get consultation

from a super specialist. It was felt that even though the percentage of business from health

insurance was low, there is an opportunity to have close network polices to control the

flow of patients to providers and also the concept of gatekeeper was thought to be a

workable solution. However, since it‘s not easy to change the behavior of customers at

least some steps may be taken to ensure that there is balance between the demand and

supply of healthcare.

5.3.4 Poor doctor-insurer relationship

It was felt that the doctor and patient relationship is quite strong in the Indian context.

However, there is hardly any relationship between the doctors and insurers. It is either the

hospitals or the TPAs those who interact at regular intervals and have some sort of on-

going relationship. The interaction between the insurers and doctors is hardly seen. It was

told that hardly anyone from the insurance companies talk with the doctors. It is either the

TPA desk or the accounts team of the hospital that interacts with the insurance companies.

Currently, there are many doctors who work on freelance basis and are not exclusively

tied-up with any specific providers. These doctors have no incentive to reduce the cost of

care for insure patients. If insurance company can initiate building relationship then it

might help manage the health insurance claims cost. For example- there are many hospitals

wherein the consultant charges are not fixed. It is up to the consultant to decide how much

will he charge and from whom. If insurance company can tie-up with these consultant and

work towards a fixed consultant charge (in lieu of patient flow) then this would help

minimize the claim cost. It was felt that building doctor and insurer relationship will help

in bringing more transparency in the system and will benefit both the providers and the

insurers.

138

5.3.5 Criteria for selection of providers

There was a common perception that the selection of providers is not done fairly. That, it is

the discretion of the TPAs or the insurance company and that there is no standard process

followed for undertaking this activity. It was also suggested that there are few TPA‘s

which charge kick-back from the providers for getting into their panel. There was a

pressing need to have a standard process that should be followed for selection of providers

and it should be transparent in nature, to an extent that the providers know the reasons for

not getting selected for extending cashless benefit.

5.3.6 Lack of standardization

It was felt that there is lack of standardization in both the treatment part well as the

processes followed by the insurer and TPA‘s. For example- it was told that there is no

standard treatment guideline followed by most of the providers. By implementing standard

treatment guidelines there could be more transparency in the existing system. However, it

was argued by the doctor‘s community that there are cases which are complex and involve multiple

line of treatment and one cannot have standard guidelines for the same (for example, multiple

organ failure). It is also being thought that it will restrict the freedom of the doctors in deciding the

line of treatment.

An example of lack of standardization in the processes was that most of the TPA‘s have

their own Service Level Agreement (SLA) and thus it becomes extremely difficult for

providers to measure and monitor the same. It was argued by the hospital administrators

that the benefits of standardization of SLA and inclusion of common industry benchmarks

will help bring in focus and clear expectation from the service provider, whether it is the

TPA‘s , the providers or the insurers.

5.3.7 Training issues

It was a common feedback from the healthcare professionals that there is a lack of training

given to them either by the TPA‘s or the insurance companies. On critical examination it

was found that lack of training in the area of health insurance is because of multiple

reasons, which includes: lack of funds; lack of trained manpower (trainers) and

infrastructure; focus on just selling and not focusing on quality of sale; health insurance

139

being a loss making portfolio, thus any expenses in training was never thought as an

investment; Incase of providers there is high level of attrition at the insurance desk and

also due to lack of time, given the work pressure. It was suggested that by providing

training to healthcare professional on health insurance and its processes more synergy

could be developed among insurers and providers.

5.3.8 Lack of robust grievance handling mechanism for providers

A common feedback received was that the current grievance handling mechanism of the

insurers to handle provider query and complaints are not robust. There are many instances

when the issues highlighted by the providers and or doctors are not addressed by the

providers. Also, there are delay in responses received from insurers and TPAs. There are

payment issues which had not been resolved since years. A robust grievance handling

mechanism will help build confidence in the minds of the providers and would help

develop synergy.

5.4 Intermediaries (Agents, Advisors, Brokers, TPA’s)

The intermediaries are an important stakeholder group as they not only help in sales and

distribution activity but also in the servicing of health insurance policies. The key themes

and factors highlighted by the intermediaries were in the area of provider tariff,

communication, underwriting, product innovation and health insurance fraud. The

summary of the same is presented below:

5.4.1 Dual provider tariff

There was a common complaint that most of the providers follow a dual tariff i.e. one for

patients who pays out-of-pocket and the other for insured patients. It was told that such

practices hamper the relationship among insurers and providers. It was also informed that

such practices had started with the introduction of cashless services by the insurance

companies. It is because of such instances that the TPA‘s and insurance companies are

coming up with their own package rates. Even, in the mass scheme like RSBY standard

140

package rates are followed. It was felt that such practices destroy synergy among insurers

and providers.

5.4.2 Improve communication between parties

It was commonly felt that there are opportunities to improve communication between all

parties involved in the health insurance mechanism and working on the same would help

develop synergy among insurers and providers.

5.4.3 Lack of prudent underwriting

During our interview with the intermediaries it was told that it becomes extremely difficult

for them to understand few conditions in the policy which is incorporated at the time of

underwriting. For example- if the policy document simply says that there is a room rent

capping of say 10 percent. Then, it is not clear if the hospital should ask the insured patient

to pay 10 percent of the room rent charge or all the charges which is associated with room

rent. So, at the time of underwriting adequate care should be taken while writing any

special conditions so that it is clearly understood by the providers. It was also highlighted

that the pricing of the health insurance products does not take into account medical

inflation. Prudent underwriting guidelines are hardly followed by the insurance companies

due to market pressure and lack of available data on morbidity and past claim history.

5.4.4 Inadequate cover and product innovation

The common feedback was that there is inadequate cover and product innovation in the

area of health insurance. The problem with limited cover is that it restrict the provider to

offer services and make it troublesome for the insured (as well as the provider) to

understand the If‘s and But‘s of the policy. It was also told that there is a perception among

the insured population that insurance companies want to cover only young and healthy

people so that they can make heavy profits. This gets fuelled by the fact that most of the

insurance companies don‘t extend cover if you are more than 80 yrs old. The need for

product innovation was highlighted and it impact on synergy among insurers and providers

was reflected.

141

5.4.5 Health insurance fraud

The presence of fraud in the health insurance business was acknowledged. It was informed

that there are different types of fraud prevalent in the Indian health insurance market. For

example- lodging of fraudulent reimbursement claims; mis-representation of material fact

at the time of policy issuance; manipulation of claim documents including bills and

receipts; kick-back from providers and intermediaries. There concept like ‗rent a patient‘,

‗unbundling‘, ‗up-coding‘ are becoming visible in the area of provider fraud. Few of them

told that the insured patients are made to stay more than that of patients who pay out-of-

pocket. Insured patient are prescribed high end diagnostic test like Computed Tomography

(CT scan) and Magnetic Resonance Imaging (MRI), even when the same is not linked to

the treatment. There are cases where fixed commission is being paid to the prescribing

doctors by the diagnostic centers. In case of providers, it was told that since they invest lot

of money buying the latest technology, they tend to use the technology on patients for

regular income flow and decreasing the idle time of the equipment. There was a common

feeling that the saving brought about by mitigating health insurance fraud risk will not only

benefit the insurers but all the other stakeholders in the industry.

5.5 Others (NGOs, Education institutions, Pharmaceutical Co. etc.)

The key themes those were raised by the remaining stakeholders (i.e. NGO‘s, educational

institution, etc.) were in the area of value creation, training, co-payment and deductible and

linked to insurance cover (over and under insurance). A brief summary of these are

presented below:

5.5.1 Lack of value creation: There was a common feedback that there is lack of value

creation in multiple areas. These include activities like the health insurance product

development, cashless processing and customer service (both at insurer and provider). It

was felt that the level of customer satisfaction may be increased by creating value for the

customer. For example, by reducing the premium of health insurance products and offering

care with quality of international standards.

142

5.5.2 Lack of specialized training institutions and courses: One of the issues raised was

lack of specialized training institution and courses designed to address the training needs of

the Indian health insurance market. It was told that as the health portfolio was bleeding

with high claim ratio, it was never thought a good idea to spend money in training. The

NGO‘s and the educations institutions were more vocal on this issue. A pressing need to

develop course curriculum based on the needs of the health insurance industry was felt. It

is though these specialized training institutions and courses that the industry would be able

to produce trained manpower required to sustain the current growth level of health

insurance in India.

5.5.3 Co-payment and high deductibles: The NGO‘s were of the opinion that insurance

companies had started putting co-payment and deductible clauses in their products to

safeguard themselves from financial loss but such activities are completely against the

customers. It becomes very difficult for a poor patient to pay out-of-pocket when he is

covered through insurance. It was also told that such activities are not welcomed by them

and should be stopped.

5.5.4 Over and under insurance: Here again the NGO‘s were of the opinion that over and

under insurance is not customer friendly. What is the value for the customer if he is under

insured? If the sum insured is less than the treatment cost then what is the fun in buying a

health insurance cover? Over insurance is where the customer is offered higher sum-

insured but is not that prevalent in the Indian scenario due to in-capacity to pay for the cost

of higher premium. Also, it becomes difficult for the providers to process claims where the

total treatment cost is not paid by the insurers.

Thus, there are multiple factors that can affect synergy between insurers and providers.

Each stakeholder group had an interest in the relationship between insurer and provider

and can affect the implementation of potential strategies for synergy. However, if the

identified factors and issue are kept in mind while developing strategies for synergy, then

the chances of failure for implementation would be minimized.

143

5.6 Content Analysis and Competitive Diamond

5.6.1 Content Analysis

On analyzing the contents published in one of the leading national news paper of India

(Times of India) from 2007 to 2009, it was found that a total of 223 headlines were

published in the area of health insurance. These headlines contain words like health,

insurance, insurer, insured, cashless and or mediclaim and were related to the health

insurance domain. The number of headlines published in year 2007 was the highest

followed by 2009 and the least number of headlines were published in the year 2008

(Figure 5.3).

Figure 5.3: Number of Headlines on Health Insurance (TOI: 2007, 2008 and 2009)

Source: Content analysis undertaken by the author

The location source of these articles covered sixteen States. The maximum number of

headlines published on health insurance was observed in the state of Maharashtra 34

percent, followed by Delhi 31 percent. Thus, 65 percent of the articles on health insurance

were found to get reported either from the State of Maharashtra or Delhi. This may be

because of the reason that most of the insurance corporate houses are located in these two

States. Also, the number of corporate houses extending cashless benefit to its employees

would be the highest in these two states. 21 percent of the headlines were reported from

Karnataka, Tamil Nadu and Punjab. This may be because; in these three States the social

health insurance schemes are active.

144

Figure 5.4: Number of Headlines: State wise percentage distribution

Source: Content analysis undertaken by the author

Table 5.5: State wise City representation

State Name City Representation (Headlines)

Andhra Pradesh Hyderabad

Bihar Patna, Bhagalpur

Delhi New Delhi

Goa Panaji

Gujarat Ahmedabad,Vadodara, Amreli, Surat

Haryana Panipat

Himachal Pradesh Shimla

Karnataka Bangalore, Mangalore, Davanagere, Hubli

Kerala Thiruvananthapuram, Kochi

Kolkata Howrah

Madhya Pradesh Jabalpur

Maharashtra Mumbai, Pune, Nagpur

Punjab Chandigarh, Ludhiana

Rajasthan Jaipur

Tamil Nadu Chennai, Coimbatore

Uttar Pradesh Allahabad, Lucknow, Kanpur, Varanasi

Source: Content analysis undertaken by the author

145

Table 5.6: Content analysis: stakeholder wise issues and interest

Stakeholders Issues/ Interest

Community at large

Life insurance, Unique Cover, Insurance scam, Standalone

health insurance, Affordability (high premium), Access,

Differential rate, Lack of cover, New products, Growth

potential, Role of doctors, Career prospects, Tax benefits,

Commission paid to agents.

Government (Center

and State)

FDI, Insurance for Poor, Need for cover, Tax savings,

Coverage, Policy exclusions, Lack of Access and Awareness,

RSBY, Aam Adami Bima Yojana, Cashless Facility,

Divestment in PSU, Delay in processing claim and provider

payment, Forcible sale of insurance policy.

IRDA

Training of Agents, Agent Commission, Definition of Pre-

Existing disease, Cover for Sr. Citizen, De-tariff, Policy holder

Interest, Misselling, Agents recruitment exams, Premium

loading, Demand for skill set, Merger and Acquisition, Rising

number of disputes, Norms for insurance IPO, Bancassurance.

GIC Low penetration, Portability in mediclaim, Standardization,

Common definition of Pre-Existing disease

Insured Differential Premium, Poor claim processing, blacklisted

hospitals, Insurance related fraud

Insurer

TPA services, Claims & Cost, Need for Cover, Product

development, PED, lack of training and standardization, Fraud,

Huge opportunity

Insurance industry High Loss, Joint ventures, Brokerage and commission,

Uniform hospital rates

Industry (general) Competition, Investments, joint ventures

International

Community Outsourcing, Need for Care

Courts (High and

Supreme) Coverage, Health insurance Fraud

Consumer forum Deficiency in service, Policy T&C, PED, Negligence

Teaching and Training

Institution

Shortage of hospital, Lack of coordination between hospital

and insurer, Career prospects in insurance, Cover for students

Source: Content analysis undertaken by the author

146

The balance 14 percent of the headlines were reported from States like Gujarat, Uttar

Pradesh, Bihar, Kerala, Goa, Kolkata, Andhra Pradesh, Haryana, Himachal Pradesh,

Madhya Pradesh and Rajsathan (Figure 5.4). The Cities representation is given in Table

5.5. The stakeholder wise issues and interest are summarized in Table 5.6.

5.6.2 Competitive Diamond

Michael Porter introduced a model that allows analyzing why some nations are more

competitive than others are, and why some industries within nations are more competitive

than others are, in his book ―The Competitive Advantage of Nations‖. Porter‘s diamond of

national competitive advantage is a modern international trade theory (Porter, 1990). It was

derived and used to conceptualize the four conditions that are important when conducting

international business. These four factors originate from earlier country and firm-based

theories.

Figure 5.5: Competitive Diamond of Indian Health Insurance Industry

Source: Adopted from porter Competitive Diamond for Nations.

147

In simple terms, the country based theories relate to the international trade theories of

nations as a unit of business and the firm-based theories are those which relate to the firm

as a unit of business. It recognizes four pillars of research (factor conditions, demand

conditions, related and supporting industries, firm structure, strategy and rivalry) that one

must undertake in analyzing the viability of a nation competing in a particular international

market, but it also can be used as a comparative analysis tool in recognizing which country

a particular firm is suited to expanding into. The Indian health insurance industry currently

has provisions for 26 percent of FDI as per regulations. There is discussion going on to

increase this limit to 49 percent. Most of the private players have foreign partners. For

example - Max Bupa, Apollo Munich, ICICI Lombard etc., also, there are health insurance

products that compete in the international market like the international medical emergency

and travel policy (with health cover). Any foreign partner of the existing insurance

companies and those willing to enter this market would examine the above mentioned four

factors before taking the decision.

The current study attempts to examine the competitive diamond of Indian health insurance

industry. The findings and discussion are based on the desk and field research undertaken.

The Figure 5.5 depicts the competitive diamond. Under each factor the positives (+) and

opportunities for improvement (-) are listed. If Indian health insurance industry wants to

attract more foreign investment and participation then the negatives needs to be converted

into positives. The four factors are discussed briefly here under:

Factor Condition: the factor conditions are divided into basic and advanced factors. Under

the basic factors the opportunities for improvement are in the area of poor sanitation and

hygiene, poor accessibility and access of healthcare, low doctor to patient ratio and low

bed to patient ratio. The strengths are in the area of nursing education and medical

education. In the advanced category the opportunities for improvement are in the area of

poor communication between parties (insurer, provider, TPA, customer etc.), delay in

payments and funds transfer to providers, lack of trained and skill manpower and lack of

scientific research. The strengths include the technology resource available within the

country.

148

Demand Condition: the overall demand for health insurance in India is low but in the times

to come due to rising cost of healthcare and increase in disposable income this scenario

will change. The opportunities for improvement under demand condition includes lack of

awareness about the benefits of health insurance products, poor distribution strategy, lack

of value creation for the customer, need to care, need for cover and poor penetration of

health insurance. The strengths include introduction of mass policies like RSBY (the

demand is created by the government) and the rising healthcare cost (in the current

context).

Related and Supporting Industries: the opportunities for improvement include: poor re-

insurance support, medical equipments manufacturing, medical tourism, lack of ownership

by intermediaries, high level of fraud (both provider and customer related) and lack of

initiatives in the area of preventive healthcare. The strengths include support from the

banks and MFIs in serving this market segment.

Firm Strategy, Structure, and Rivalry: the opportunities for improvements include:

increasing the FDI limit from current 26 percent to 49 percent, over regulated insurance

industry, lack of specialized insurance body for health insurance, lack of standardization

and lack of trust and transparency among stakeholders. The strengths include the entry of

standalone health insurance company, de-tariffication and product innovation.

Thus, to build home based advantages and to create competitive advantage in relation to

others on a global front, the Indian health insurance industry needs to act on the

opportunities for improvements (identified above) and keep developing the strengths. On

national level, governments can (and should) consider the policies that they should follow

to establish national advantages, which enable the health insurance industry to develop a

strong competitive position globally. According to Porter, governments can foster such

advantages by ensuring high expectations of product performance, safety or environmental

standards, or encouraging vertical co-operation between suppliers and buyers on a

domestic level etc.