cia. hering - 3q16 results

TRANSCRIPT

3Q16 Results Conference Call

October 28th, 2016 – 11:00 am (BrT) 09:00 am (NY)/ 02:00 pm (London)

3Q16 Results

DISCLAIMER

This presentation contains forward-looking statements regarding the

prospects of the business, estimates for operating and financial

results, and those regarding Cia. Hering's growth prospects. These are

merely projections and, as such, are based exclusively on the

expectations of Cia. Hering management concerning the future of the

business and its continued access to capital to fund the Company’s

business Plan. Such forward-looking statements depend, substantially,

on changes in market conditions, government regulations,

competitive pressures, the performance of the Brazilian economy and

the industry, among other factors and risks disclosed in Cia. Hering’s

filed disclosure documents and are, therefore, subject to change

without prior notice.

• Financial Performance

• Outlook

• Q&A

2

FINANCIAL PERFORMANCE

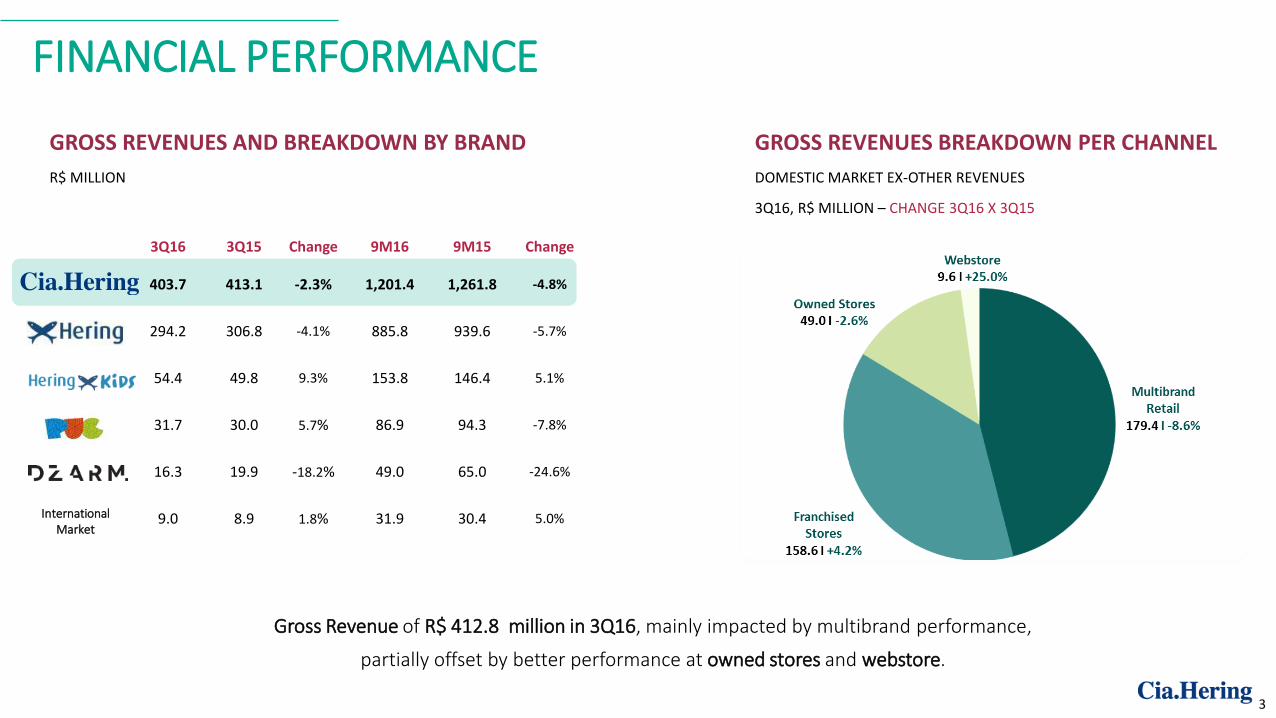

GROSS REVENUES AND BREAKDOWN BY BRAND

R$ MILLION

GROSS REVENUES BREAKDOWN PER CHANNEL

DOMESTIC MARKET EX-OTHER REVENUES

3Q16, R$ MILLION – CHANGE 3Q16 X 3Q15

Gross Revenue of R$ 412.8 million in 3Q16, mainly impacted by multibrand performance,

partially offset by better performance at owned stores and webstore.

3

3Q16 3Q15 Change 9M16 9M15 Change

403.7 413.1 -2.3% 1,201.4 1,261.8 -4.8%

294.2 306.8 -4.1% 885.8 939.6 -5.7%

54.4 49.8 9.3% 153.8 146.4 5.1%

31.7 30.0 5.7% 86.9 94.3 -7.8%

16.3 19.9 -18.2% 49.0 65.0 -24.6%

9.0 8.9 1.8% 31.9 30.4 5.0% International Market

HERING STORE NETWORK

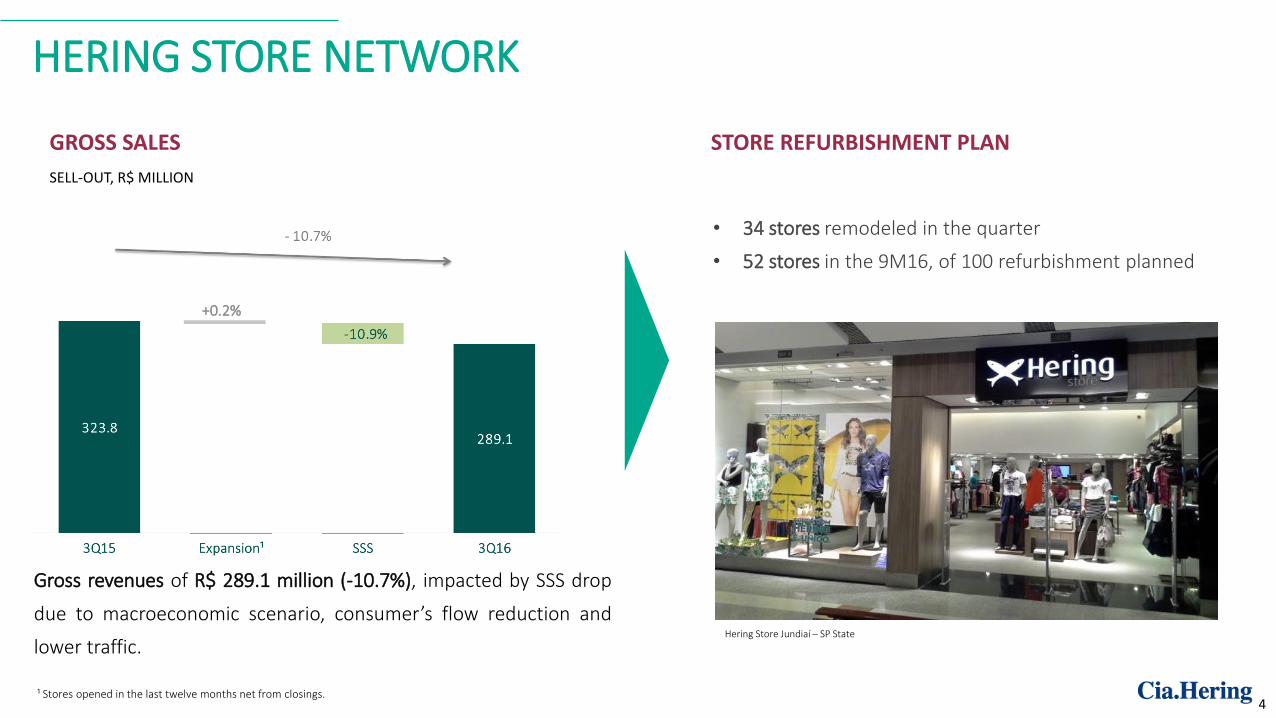

GROSS SALES

SELL-OUT, R$ MILLION

Gross revenues of R$ 289.1 million (-10.7%), impacted by SSS drop

due to macroeconomic scenario, consumer’s flow reduction and

lower traffic.

¹ Stores opened in the last twelve months net from closings.

STORE REFURBISHMENT PLAN

• 34 stores remodeled in the quarter

• 52 stores in the 9M16, of 100 refurbishment planned

Hering Store Jundiaí – SP State

4

+0.2%

FINANCIAL PERFORMANCE

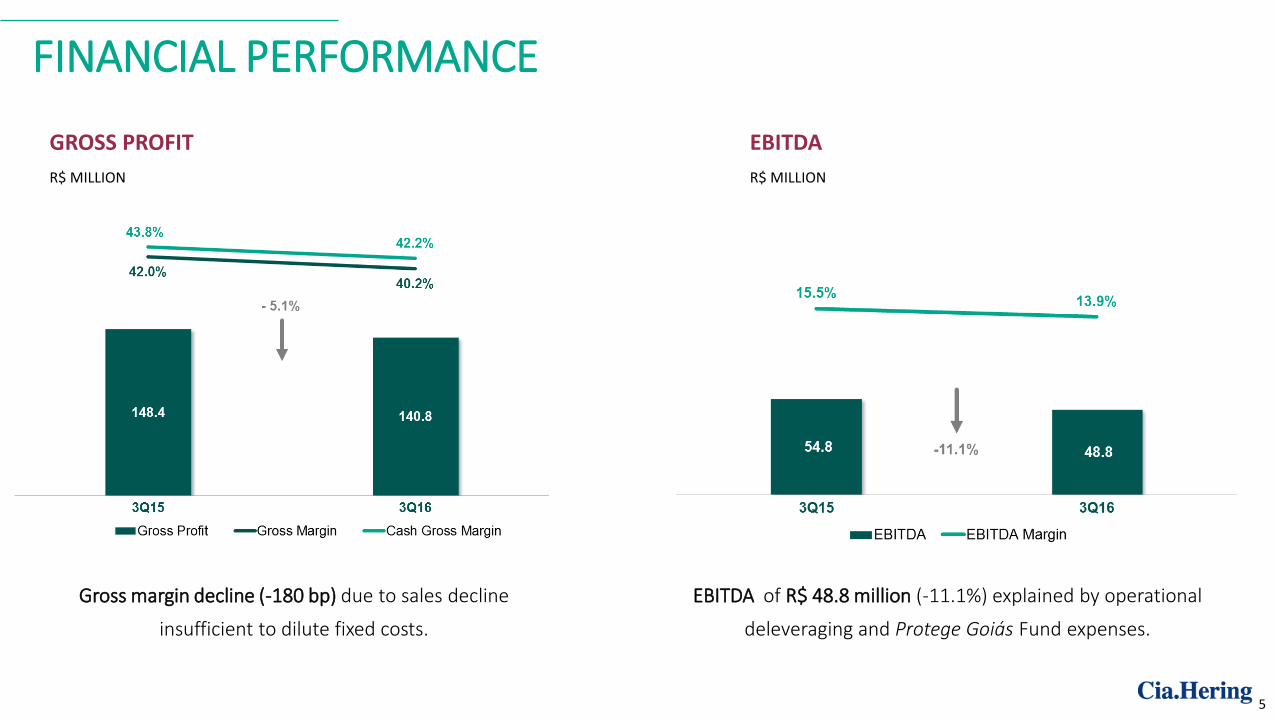

EBITDA of R$ 48.8 million (-11.1%) explained by operational

deleveraging and Protege Goiás Fund expenses.

Gross margin decline (-180 bp) due to sales decline

insufficient to dilute fixed costs.

GROSS PROFIT

R$ MILLION

EBITDA

R$ MILLION

5

FINANCIAL PERFORMANCE

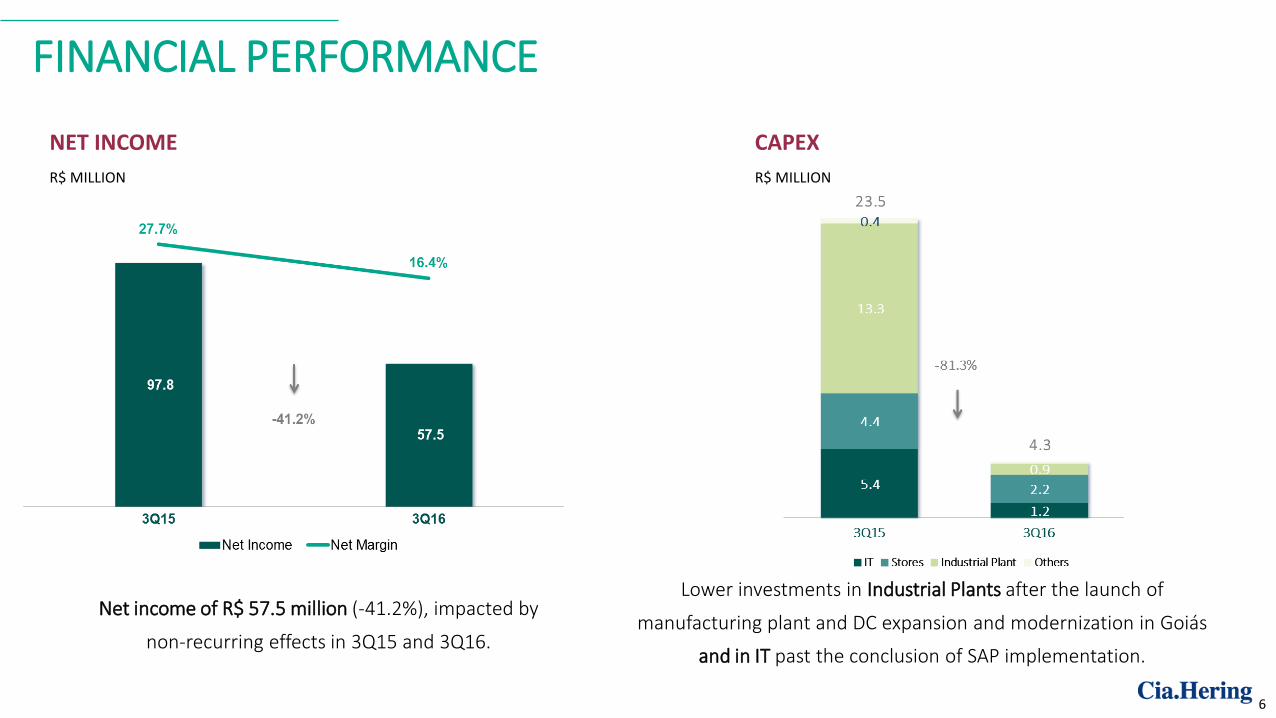

NET INCOME

R$ MILLION

CAPEX

R$ MILLION

Net income of R$ 57.5 million (-41.2%), impacted by

non-recurring effects in 3Q15 and 3Q16.

Lower investments in Industrial Plants after the launch of

manufacturing plant and DC expansion and modernization in Goiás

and in IT past the conclusion of SAP implementation.

6

FINANCIAL PERFORMANCE

Cash flow of R$ 27.8 million, R$ 19.1 million higher than 3Q15, as a result of a

reduction in working capital needs, by inventories decrease, and lower investments.

CASH FLOWS

R$ MILLION

7

Cash Flow - Consolidated 3Q16 3Q15 Chg. 9M16 9M15 Chg.

EBITDA 48,751 54 ,829 (6 ,078) 146,618 168,527 (21,909)

No cash items (5,475) 4,946 (10,421) (3,409) 20,020 (23,429)

AVP (Adjustment to Present Value) - Clients and Suppliers 3,858 3,551 307 14,715 13,024 1,691

Current Income tax and Social Contribution (4,365) 12,925 (17,290) (6,010) 1,738 (7,748)

Working Capital Capex (10,636) (44,031) 33 ,395 74,142 (44,020) 118,162

(Increase) decrease in trade accounts receivable 7,102 15,846 (8,744) 99,824 109,352 (9,528)

Decrease (increase) in inventories (32,013) (71,000) 38,987 (19,443) (102,231) 82,788

Increase (decrease) in accounts payable to suppliers 25,329 18,307 7,022 12,581 (7,966) 20,547

(Decrease) in taxes payable (4,418) (3,248) (1,170) (21,043) (31,214) 10,171

Refurbishment Project 2016 - Franchisee Financing (6,117) (979) (5,138) (8,612) (979) (7,633)

Others (519) (2,957) 2,438 10,835 (10,982) 21,817

CapEx (4 ,303) (23 ,443) 19 ,140 (14,258) (66,586) 52 ,328

Free Cash Flow 27,830 8 ,777 19 ,053 211,798 92,703 119,095

OUTLOOK

• In Q4, uncertainties in consumption environment can bring sales volatility;

• Company's inventories normalization should bear benefits based on the markdown level reduction;

• Product and Store (“P&S”) fronts, remain as priorities for the year:

• Product: High Summer collection already shows improvements in the cost-benefit ratio ('value for money')

• Stores: great network adhesion to Refurbishment Program, that should be over-delivered.

• Supply and inventories management as priority in pursuit of lower shrinkage, better shopping experience

through VM and stores profitability improvement by reducing markdown.

9

Fabio Hering – CEO Frederico Oldani – CFO and IRO

Bruno Salem Brasil – IR Manager Caroline Luccarini – IR Analyst

www.ciahering.com.br/ir +55 (11) 3371 – 4867/4805

INVESTOR RELATIONS TEAM