deficits and debt chapter 12 copyright © 2010 by the mcgraw-hill companies, inc. all rights...

TRANSCRIPT

Deficits and DebtChapter 12

Copyright © 2010 by the McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

12-2

Deficits and Debt

• The core critique of fiscal stimulus focuses on the budget consequences of government pump-priming– How do deficits arise?– What harm, if any, do deficits cause?– Who will pay off the accumulated national debt?

12-3

Budget Effects of Fiscal Policy

• Keynesian theory highlights the potential of fiscal policy to solve macro problems– Fiscal policy: The use of government taxes and

spending to alter macroeconomic outcomes

• Use of the budget to stabilize the economy implies that federal expenditures and receipts won’t always be equal

12-4

Budget Surpluses and Deficits

• Deficit spending: The use of borrowed funds to finance government expenditures that exceed tax revenues

• Budget deficit: Amount by which government spending exceeds government revenue in a given time period

– 0Budget government taxdeficit spending revenues

12-5

Budget Surpluses and Deficits

• If the government spends less than its tax revenues, a budget surplus is created

• Budget surplus: An excess of government revenues over government expenditures in a given time period

12-6

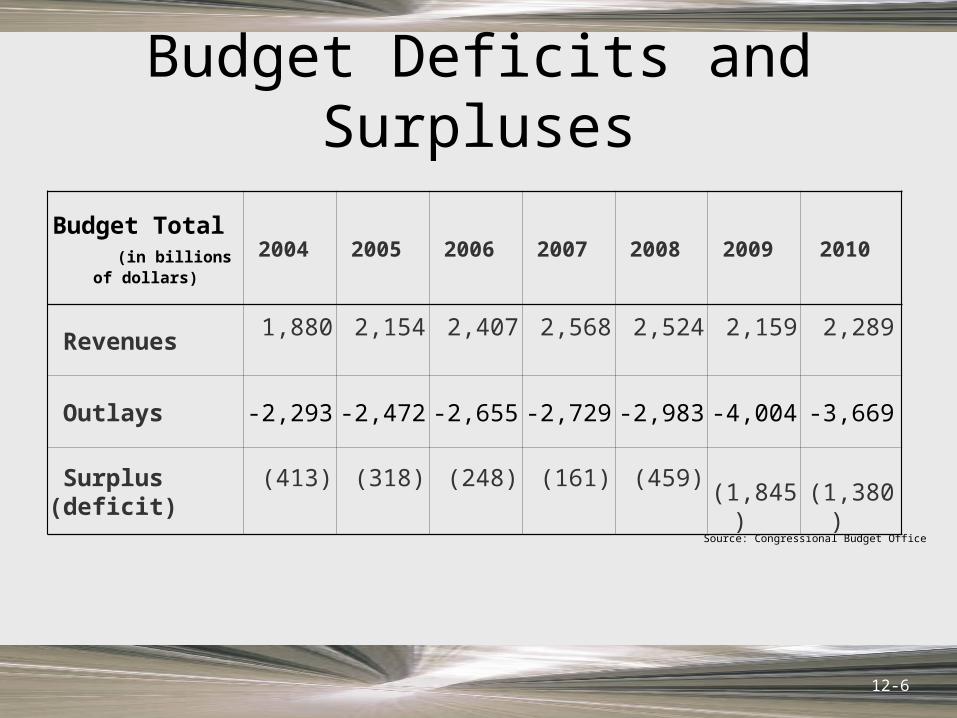

Budget Deficits and Surpluses

Budget Total (in billions of dollars)

2004 2005 2006 2007 2008 2009 2010

Revenues 1,880 2,154 2,407 2,568 2,524 2,159 2,289

Outlays -2,293 -2,472 -2,655 -2,729 -2,983 -4,004 -3,669

Surplus (deficit)

(413) (318) (248) (161) (459) (1,845) (1,380)

Source: Congressional Budget Office

12-7

A String of Deficits

Budget deficits are overwhelmingly the rule, not the exception.

12-8

Keynesian View

• Budget deficits and surpluses are a routine feature of counter-cyclical fiscal policy

• The goal of macro policy is not to balance the budget but to balance the economy at full-employment

12-9

Discretionary vs. Automatic Spending

• At the beginning of each year, the President and Congress put together a budget blueprint for the next fiscal year

• Fiscal year (FY): The 12-month period used for accounting purposes; begins October 1 for the federal government

12-10

Discretionary vs. Automatic Spending

• Current revenues and expenditures are largely the result of prior year’s decisions– Only about 20 percent is discretionary spending– Uncontrollables account for roughly 80 percent

• Discretionary fiscal spending: Those elements of the federal budget not determined by past legislative or executive commitments

12-11

Discretionary vs. Automatic Spending

• Since most of the budget is uncontrollable, fiscal restraint or stimulus is less effective

• Fiscal restraint: Tax hikes or spending cuts intended to reduce (shift) aggregate demand

• Fiscal stimulus: Tax cuts or spending hikes intended to increase (shift) aggregate demand

12-12

Automatic Stabilizers

• Most uncontrollable line items in the federal budget change with economic conditions

• Automatic stabilizer: Federal expenditure or revenue item that automatically responds counter-cyclically to changes in national income, like unemployment benefits, income taxes

12-13

Cyclical Deficits

• Cyclical deficit: That portion of the budget balance attributable to short-run changes in economic conditions– The cyclical deficit widens when GDP growth

slows or inflation decreases– The cyclical deficit shrinks when GDP growth

accelerates or inflation increases

12-14

Structural Deficits

• To isolate effects of fiscal policy, the actual budget balance is broken down into cyclical and structural components

Total budget cyclical structuralbalance balance balance

12-15

Structural Deficits

• Structural deficit: Federal revenues at full employment minus expenditures at full employment under prevailing fiscal policy

• Part of the deficit arises from cyclical changes in the economy; the rest is the result of discretionary fiscal policy

12-16

Cyclical vs. Structural Budget Balances(in billions of dollars)

Fiscal Year Budget Balance = Cyclical Component + Structural Component

2000 + 236 + 94 + 142 2001 + 128 + 19 + 109 2002 - 158 - 62 - 96 2003 - 378 - 84 - 294 2004 - 413 - 46 - 367 2005 - 318 - 21 - 297 2006 - 248 - 8 - 240 2007 - 161 - 28 - 133 2008 - 459 - 76 - 383 2009 - 1667 - 310 - 1357

Source: Congressional Budget Office (June 2009)

Changes in the structural component result from policy changes; changes in the cyclical component result from changes in the economy.

12-17

Structural Deficits

• Only changes in the structural deficit measure the thrust of fiscal policy– Fiscal stimulus is measured by an increase in the

structural deficit (or shrinkage in the structural surplus)

– Fiscal restraint is gauged by a decrease in the structural deficit (or increase in the structural surplus)

12-18

Economic Effects of Deficits

• Crowding out: A reduction in private-sector borrowing (and spending) caused by increased government borrowing

• Crowding out reminds us that there is an opportunity cost to government spending

• Government borrowing to finance deficits puts upward pressure on interest rates

12-19

Pu

blic

-sec

tor

ou

tpu

t

Private-sector output

Crowding Out

Increase in government spending . . .

Crowds out private spending

b

ca

g2

g1

h2 h1

12-20

Economic Effects of Surpluses

• Four potential uses for a budget surplus:– Spend it on goods and services– Cut taxes– Increase income transfers– Pay off old debt (“save it”)

• The economic effects are the mirror image of those for deficits

12-21

Crowding In

• Crowding in: An increase in private-sector borrowing (and spending) caused by decreased government borrowing

• When the government reduces borrowing, it takes pressure off market interest rates

• As interest rates drop, consumers will be more willing and able to purchase big-ticket items

12-22

Cyclical Sensitivity

• Crowding in depends on the state of the economy

• In a recession, a decline in interest rates is not likely to stimulate much spending if consumer and investor confidence is low

12-23

The Accumulation of Debt

• The U.S. government has had many more years of budget deficits than budget surpluses

• National debt: The accumulated debt of the federal government

12-24

Debt Creation

• When the Treasury borrows funds it issues treasury bonds

• Treasury bonds: Promissory notes (IOUs) issued by the U.S. Treasury

• The national debt is a stock of IOUs created by annual deficit flows

12-25

Historical View of the Debt/GDP Ratio

12-26

Who Owns the Debt?

• The national debt creates as much wealth for bondholders as liabilities for the government

• Liability: An obligation to make future payment; debt

• Asset: Anything having exchange value in the marketplace; wealth

12-27

Ownership of Debt

Source: U.S. Treasury Department (2008 data)

12-28

Ownership of Debt

• 72 percent of the national debt is internal

• Internal debt: U.S. government debt (Treasury bonds) held by U.S. households and institutions

• External debt: U.S. government debt (Treasury bonds) held by foreign households and institutions

12-29

Burden of the Debt

• The debt has historically been refinanced– Refinancing: The issuance of new debt in

payment of debt issued earlier

• Most debt servicing is simply a redistribution of income from taxpayers to bondholders– Debt service: The interest required to be paid each

year on outstanding debt

12-30

Burden of the Debt

• Opportunity costs are incurred only when real resources (factors of production) are used

• The true burden of the debt is the opportunity costs of the activities financed by the debt

12-31

The Real Trade-Offs

• Deficit financing tends to change the mix of output toward more public-sector goods

• The burden of the debt is the opportunity cost of deficit-financed government activity

• The primary burden is incurred when the debt-financed activity takes place

12-32

Economic Growth

• Future generations will bear some of the debt burden if debt-financed government spending crowds out private investment

• The whole debate about the burden of debt is really an argument over the optimal mix of output

12-33

Repayment

• Future interest payments entail a redistribution of income among taxpayers and bondholders living in the future

12-34

External Debt

• External financing allows us to get more public-sector goods without cutting back on private-sector production (or vice versa)

• As long as outsiders are willing to hold U.S. bonds, external financing imposes no real cost

12-35

External Financing

Extra output (imports)

financed with external debt

a

b d

h2 h1

g2

g1

Pu

bli

c-se

cto

r O

utp

ut

Private-sector Output

12-36

Repayment

• Foreigners may not be willing to hold bonds forever

• External debt must be paid with exports of real goods and services

12-37

Deficit and Debt Limits

• The only way to stop the growth of the national debt is to eliminate the budget deficit that created it

• Deficit ceiling: An explicit, legislated limitation on the size of the budget deficit

• Debt ceiling: An explicit, legislated limit on the amount of outstanding national debt

12-38

Dipping into Social Security

• Social Security Trust Fund has been a major source of federal funding for over 20 years

• Surpluses have largely resulted from Baby Boomers paying more in payroll taxes than are paid out in benefits to the retired

• The Trust Fund balance shifts from surplus to deficit soon after 2014

Deficits and DebtEnd of Chapter 12

Copyright © 2010 by the McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin