do not put content on the brand signature area leszek jedlecki ing investment management (poland)...

TRANSCRIPT

Leszek JedleckiING Investment Management (Poland) S.A.

Changes in pension system and their impact on asset management/investment funds industry

28th October 2011 – Kyiv Workshop

ING Investment Management 2

1. History

2. Asset Managers

a) Pension Funds

b) Investment Funds

3. Impact of Pension Fund Reform on the Market

4. Pension System Status

5. Challenges and Opportunities

Agenda

ING Investment Management 3

1. History

2. Asset Managers

a) Pension Funds

b) Investment Funds

3. Impact of Pension Fund Reform on the Market

4. Pension System Status

5. Challenges and Opportunities

Agenda

ING Investment Management 4

How it started in Poland?Milestones

• Polish capital market traditions go back to 1817, when Warsaw Mercantile Exchange was opened (12 May 1817).

• In 1938 130 equities were quoted on the Warsaw Stock Exchange (Warsaw generated 90% of country’s turnover, 6 other stocks only 10%).

• 1945 – unsuccessful attempts to re-open the Warsaw Stock Exchange.

• March 1991 - the Securities Trading & Trust Fund Act was passed by Parlament.

• April 1991 - the first session on the new Warsaw Stock Exchange.

• July 1992 - the first Polish investment fund was launched (Pioneer TFI).

• January 1999 - the reform of Pension System started.

ING Investment Management 5

1. History

2. Asset Managers

a) Pension Funds

b) Investment Funds

3. Impact of Pension Fund Reform on the Market

4. Pension System Status

5. Challenges and Opportunities

Agenda

ING Investment Management 6

Mandatory second pillar of the pension system

PLN 236,9 bln (€ 59,2 bln) of AuM

Equity holdings amount to 15.2% of Polish market capitalization

Legal owner of mutual fund

PLN 119.2 bln (€ 29,8 bln) of AuM (retail and special funds)

Equity holdings amount to 7.7% of Polish market capitalization

Responsible for managing funds according to given mandate

Often offers investment advisory services

Discretionary porfolios management PLN 8.6 bln

(€ 2,2 bln)

Polish asset management industryWho is who?

Open Pension Funds (OFE) 65% AuM

Mutual Funds

Asset Managers 2% AuM

Investment Funds Corporations (TFI)

33% AuM

Dual company structure

Source: IZFiA, Citi Investment Research and Analysis, Parkiet (30 June 2011)

ING Investment Management 7

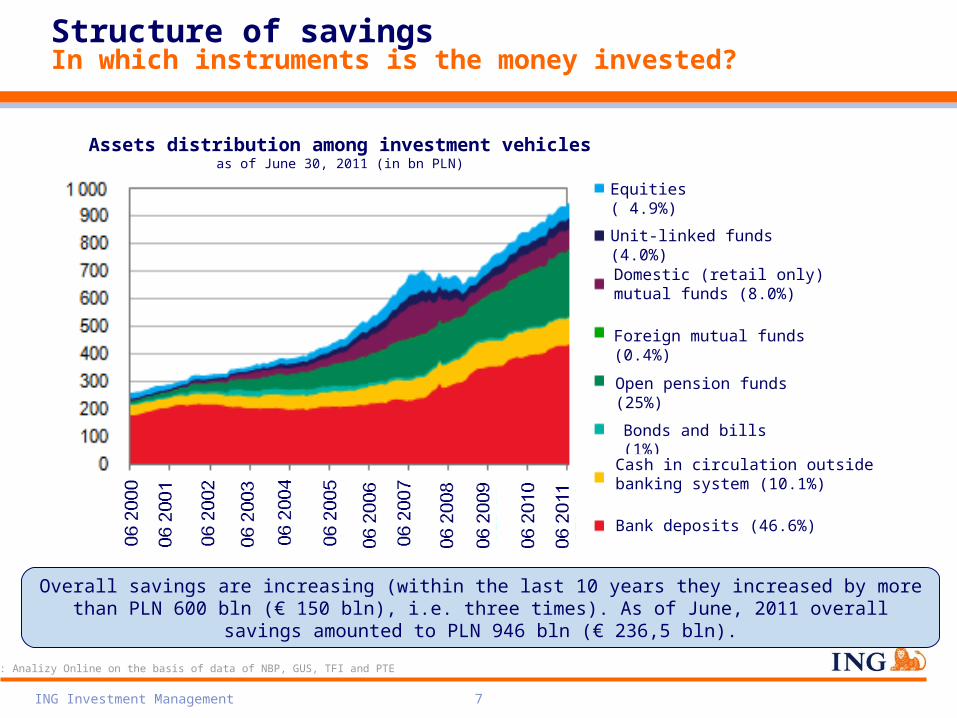

Source: Analizy Online on the basis of data of NBP, GUS, TFI and PTE

Structure of savingsIn which instruments is the money invested?

Equities ( 4.9%)

Unit-linked funds (4.0%)

Domestic (retail only) mutual funds (8.0%)

Foreign mutual funds (0.4%)

Open pension funds (25%)

Bonds and bills (1%)

Cash in circulation outside banking system (10.1%)

Bank deposits (46.6%)

Assets distribution among investment vehiclesas of June 30, 2011 (in bn PLN)

Overall savings are increasing (within the last 10 years they increased by more than PLN 600 bln (€ 150 bln), i.e. three times). As of June, 2011 overall savings amounted to PLN 946 bln (€ 236,5 bln).

ING Investment Management 8

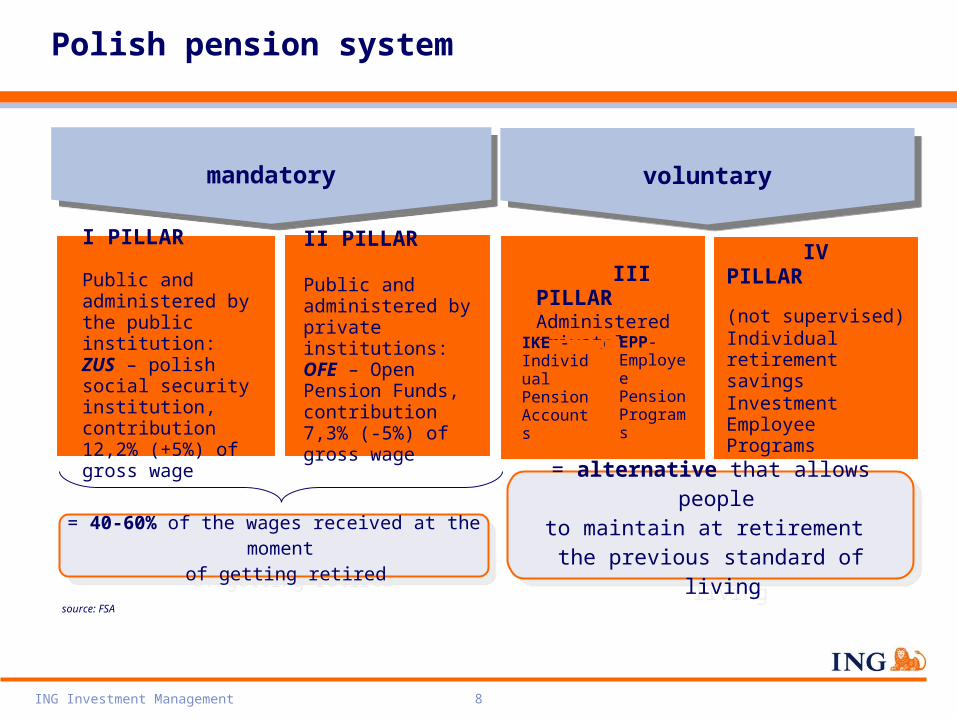

mandatorymandatory

I PILLAR

Public and administered by the public institution: ZUS – polish social security institution, contribution 12,2% (+5%) of gross wage

II PILLAR

Public and administered by private institutions: OFE – Open Pension Funds, contribution 7,3% (-5%) of gross wage

III PILLARAdministered privately

source: FSA

voluntaryvoluntary

IKE - Individual Pension Accounts

EPP- Employee Pension Programs

= 40-60% of the wages received at the moment of getting retired

= 40-60% of the wages received at the moment of getting retired

= alternative that allows people to maintain at retirement

the previous standard of living

= alternative that allows people to maintain at retirement

the previous standard of living

Polish pension system

IV PILLAR

(not supervised)Individual retirement savingsInvestment Employee Programs

ING Investment Management 9

Polish pension fundsMarket development since 1998

Source: KNF, Citibank. Assumed exchange rate for EUR/PLN = 4,00

ING Investment Management 10

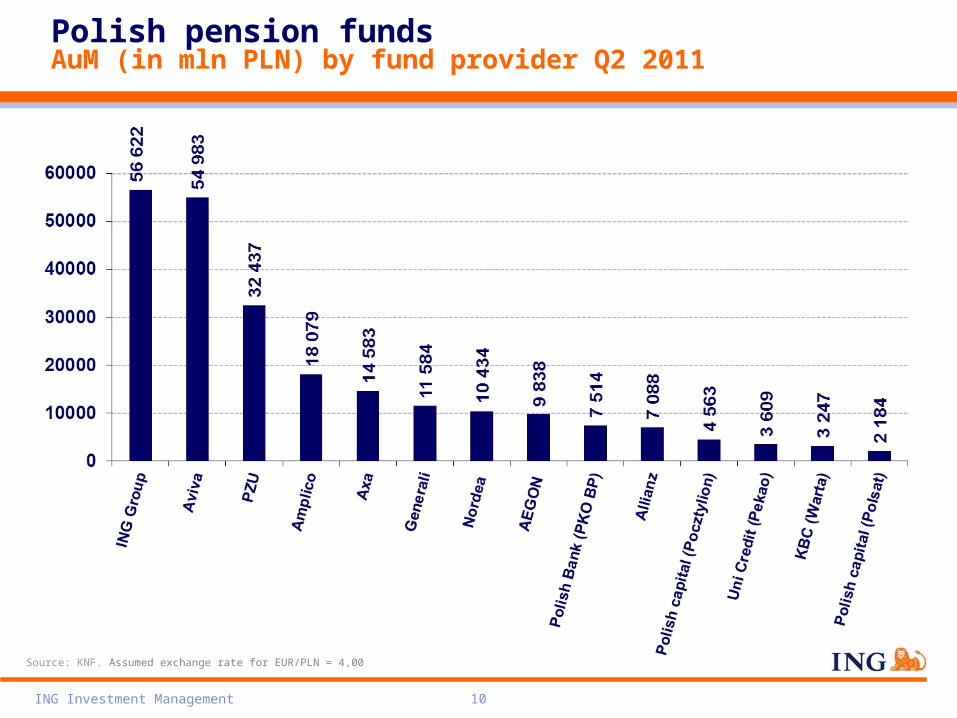

Polish pension fundsAuM (in mln PLN) by fund provider Q2 2011

Source: KNF. Assumed exchange rate for EUR/PLN = 4,00

ING Investment Management 11

1. History

2. Asset Managers

a) Pension Funds

b) Investment Funds

3. Impact of Pension Fund Reform on the Market

4. Pension System Status

5. Challenges and Opportunities

Agenda

ING Investment Management 12

Polish investment fundsMarket development since 1991

Secur

ites T

radin

g &

Trust

Funds

Act

Pionee

r mon

opoly

Mut

ual F

unds

Act

Capita

l Gain

s

Tax In

trodu

ction

Global

Financ

ial C

risis

Source: IZFiA. Assumed exchange rate for EUR/PLN = 4,00

ING Investment Management 13

Fund managers in PolandAuM (in PLN mln) by Fund Provider Q2 2011

13

6 out of 35 TFIs hold 56% of the market share

• Polish mutual fund market is expected to grow steadily due to above average economic growth, rising pension contributions and low current level of wealth allocation to mutual funds.

• Total AuM of Polish mutual funds: PLN 119.1 bln (€ 29.8 bln).

• Total AuM of foreign mutual funds constitute 3.3% of assets gathered in domestic funds and amount to PLN 4.1 bln (€ 1 bln).

• Concentrated market: 6 out 35 asset managers have over 56% of market share.

Source: Analizy Online as of June 30, 2011Assumed exchange rate for EUR/PLN = 4,00

ING Investment Management 14

Source: Citigroup Global Markets Poland – Investment Fund Strategy, EFAMA, IZFiA

What are the most popular strategies?Structure of investments

in EU mutual fundsin EUR mln

Structure of assets

ING Investment Management 15

Polish market versus Europe and CEEPoland – strong position in CEE

• AuM in CEE amount to roughly1% of the total European market

ING Investment Management 16

1. History

2. Asset Managers

a) Pension Funds

b) Investment Funds

3. Impact of Pension Fund Reform on the Market

4. Pension System Status

5. Challenges and Opportunities

Agenda

Impact of pension fund reform on the market

• The reform of Pension System in 1999 had a key role in development of asset management industry in Poland.

• The reform created strong institutional local asset managers.

• Local institutional investors played important role during privatization process.

• AuM of investment and pension funds increased from 5.5 bln PLN in 1999 to 355.9 bln PLN in mid 2011.

• Polish capital market is less dependent on foreign capital.

• Polish local institutional investors are key players on the Warsaw Stock Exchange. As of June 30, 2010 it was the largest national stock exchange in CEE and one of the fastest-growing exchanges in Europe among both regulated and exchange-regulated markets.

ING Investment Management 17

Impact of pension fund reform on the marketTotal assets in pension and investment funds

ING Investment Management 18

Source: Polish FSA, Analizy Online

ING Investment Management 19

1. History

2. Asset Managers

a) Pension Funds

b) Investment Funds

3. Impact of Pension Fund Reform on the Market

4. Pension System Status

5. Challenges and Opportunities

Agenda

ING Investment Management 20

Pension system status

• Aging population with lowering pension benefits.

• Governments will not able to keep present replacement rate.

• People should take care about their pensions themselves.

• Governments should boost (mainly by tax incentives and education) development of voluntary pension schemes.

• Growing awareness in Polish society about necessity for additional savings for pension (especially 40+ age).

ING Investment Management 21

Source: ZUS, Departament Statystyki, "Ważniejsze informacje z zakresu ubezpieczeń społecznych", Warsaw 2009

2002 2003 2004 2005 2006 2007 2008

Pension in PLN 999,77 zł 1 051,09 zł 1 096,97 zł 1 127,23 zł 1 214,75 zł 1 251,74 zł 1 370,81 zł

Pension vs. average remuneration in %1 63,70% 65,00% 65,00% 63,60% 63,60% 59,20% 57,10%

1 minus obligatory insurance contribution paid by insrured

Pension system statusAverage monthly pension paid by ZUS

ING Investment Management 22

21625 21254 20739

7380 8368 8997 9289 9622

23718 2250324571246002458424545

6414629561866082

0

5000

10000

15000

20000

25000

30000

2007 2008 2009 2010 2015 2020 2025 2030 2035

18-59/64 60+/65+

Source: Population projection for Poland for 2008 – 2035 Główny Urząd Statystyczny, Departament Badań Demograficznych, Warsaw 2009

2007 2008 2009 2010 2015 2020 2025 2030 2035

18-59/64 24 545 24 584 24 600 24 571 23 718 22 503 21 625 21 254 20 739

60+/65+ 6 082 6 186 6 295 6 414 7 380 8 368 8 997 9 289 9 622

Increase of percentage of the population at post-working age 60+/65+

Increase of percentage of the population at post-working age 60+/65+

Decrease of percentage of the population at

working age 18-59/64

Decrease of percentage of the population at

working age 18-59/64

Pension system statusPopulation projection by economic age group (in percentage)

ING Investment Management 23

1. History

2. Asset Managers

a) Pension Funds

b) Investment Funds

3. Impact of Pension Fund Reform on the Market

4. Pension System Status

5. Challenges and Opportunities

Agenda

ING Investment Management 24

• Impact on Polish capital market:

• less money will be invested in stocks by pension funds

• reputation risk of Poland

• Adverse change in savings structure – risk of real loss

• Uncertainty about future pensions

• Step back from public consensus solution from 1999

• Weaker impact of pension funds on future pensions may lead to greater interest in 3rd pillar’s solutions (PPE, IKE, IKZE - voluntary pension savings) which are offered by investment funds managers

• Pension funds may have more than one investment strategy

CHALLENGES OPPORTUNITIES

Pension reform poses threat to Polish equity market. On the other hand it may lead to bigger demand for 3rd pillar products.

The latest reform of pension funds system limited the amount of money transferred to 2nd pillar from 7.3% to 2.3% of salary.

Challenges & opportunitiesPension sector reform

ING Investment Management 25

CHALLENGES

OPPORTUNITIES

• For now, there are no strong incentives for people to save in 3rd pillar (example tax deduction)

• Uncertain future pensions• Great potential for growth in 3rd pillar products (according to PwC 20% of German and 13% of Finnish population participates in voluntary pension savings plans)

• Assets in 3rd pillar products are more „sticky” than the regular funds savings

We see a great potential in 3rd pillar products as Poles will become more aware of need for saving for their retirement.

Voluntary pension savings (3rd pillar) consists of individual pension acc. and employees retirement plans. Nowadays, only 7.3% of Poles have savings in them.

Lo

w g

ener

atio

n r

enew

al

– ag

ein

g p

op

ula

tio

n

Source: GUS

Source: Gazeta Wyborcza, Hewitt

Challenges & opportunitiesVoluntary pension savings

ING Investment Management 26

Challenges & opportunitiesVoluntary pension savings

In Poland despite access to voluntary pension schemes, penetration is still very low:

1.PPE – Employee Pension Schemes. Started in 1999. Penetration at 1.2% (PwC 2010). The main reason is not enough pressure on employers and bureaucracy

2.IKE – Individual Pension Account. Started in 2004. Penetration at 3% (PwC 2010). IKE grants tax benefits deferred in time.

3.IKZE – Individual Pension Protection Account. New program, will be launched on 1/01/2012. It grants immediate tax benefit.

Total penetration in Poland amounts to 4.2% of working population which is very low in comparison to other countries: 32% in Hungary, 20% in Germany and 18% in Slovakia (PwC 2010).

PPE Market in Poland

ING Investment Management 27

Source: Polish FSA

IKE Market in Poland

ING Investment Management 28

Source: Polish FSA

ING 29

Potential IKZE market

Source: Money.pl, PwC Comparison of systems of additional pension protection in Poland and othe UE countries, ZUS

24.1 mio people

1st tax threshold

0.34 mio people

2nd tax threshold

12 x Avg. Salary * 4%

100 000 PLN * 4%

Assuming 100% penetration

= 41.1 bln PLN

• according to PwC current penetration in 3rd pillar in Poland amounts to 4.2% (1.73 bln PLN).

• if penetration rises to level of:

• Slovakia 18% - 7.4 bln PLN

• Germany 20% - 8.2 bln PLN

• Hungary 32% - 13.2 bln PLN

ING Investment Management 30

Thank You

ING Investment Management 31

Disclaimer

Niniejszy materiał został przygotowany przez ING TFI przy dołożeniu należytej staranności i zgodnie z jego najlepszą wiedzą oraz przekonaniami. Wszelkie informacje zawarte w niniejszym materiale pochodzą ze źródeł własnych ING TFI lub źródeł zewnętrznych uznanych przez ING TFI za wiarygodne, lecz nie istnieje gwarancja, iż są one wyczerpujące i w pełni odzwierciedlają stan faktyczny. ING TFI nie może jednak zagwarantować poprawności i kompletności informacji zawartych w niniejszym materiale i nie ponosi żadnej odpowiedzialności za szkody powstałe w wyniku jego wykorzystania niezgodnie z jej przeznaczeniem. Wszelkie opinie i oceny wyrażane w niniejszym materiale są opiniami i ocenami ING TFI lub jej doradców będącymi wyrazem ich najlepszej wiedzy popartej informacjami z kompetentnych rynkowych źródeł, obowiązującymi w chwili jej sporządzania. Mogą one podlegać zmianie w każdym momencie, bez uprzedniego powiadomienia. Niniejszy materiał ma charakter wyłącznie informacyjny i został sporządzony wyłącznie dla tego celu do wyłącznego użytku adresata. Nie stanowi on oferty, doradztwa inwestycyjnego ani rekomendacji kupna lub sprzedaży instrumentów finansowych, nie zwalnia adresata z konieczności dokonania własnej oceny. Informacje zawarte w niniejszym materiale nie mogą stanowić podstawy do podejmowania decyzji inwestycyjnych.