drivers in global fertilizer markets - european...

TRANSCRIPT

Drivers in Global Fertilizer Markets

Charlotte Hebebrand Director General, IFA

2024 prospects for EU agricultural markets Brussels, 5 December 2014

Drivers in Global Fertilizer Markets

• Fertilizers at a glance

• Overview of IFA

• Yield developments & grain quality

• Fertilizer Consumption

• Link to feedstocks

… To feed the world,

one must first feed

the crops…

NORMAN BORLAUG

… a few billion people

would have to die if we

hadn't come up with

fertilizer…

BILL GATES

Fertilizers represent an essential ingredient

in the drive towards world food security

… Fertilizers: world’s most

important humanitarian

product”…

IFA is a global association which:

Improves the operating environment along

the fertilizer supply chain

Encourages expertise-sharing among

members

Promotes efficient and responsible

production and application of fertilizer

products

Develops and disseminates statistics

Informs and contributes to public policy-

making at an international level

Drivers in Global Fertilizer Markets

Fertilizer use, cereal production and food security

| Source: FAO and IFA

Drivers in Global Fertilizer Markets

Wheat response (yield and protein content) to N fertilizer applications

| Source: Grant and Bruulsema

Drivers in Global Fertilizer Markets

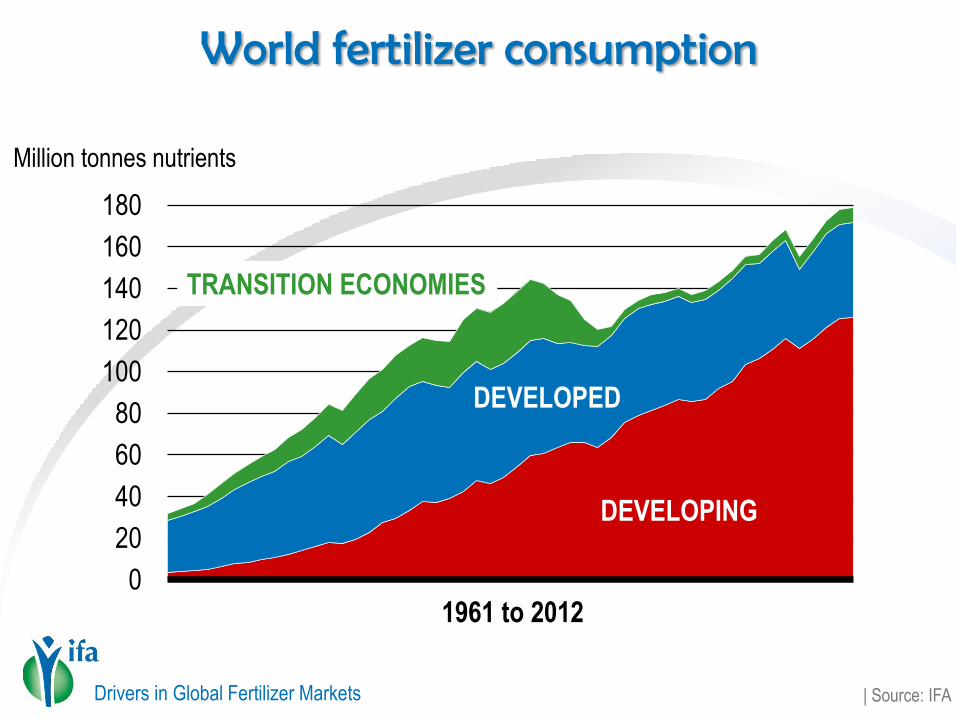

World fertilizer consumption

| Source: IFA

Million tonnes nutrients

0

20

40

60

80

100

120

140

160

180

DEVELOPING

DEVELOPED

TRANSITION ECONOMIES

1961 to 2012

Drivers in Global Fertilizer Markets

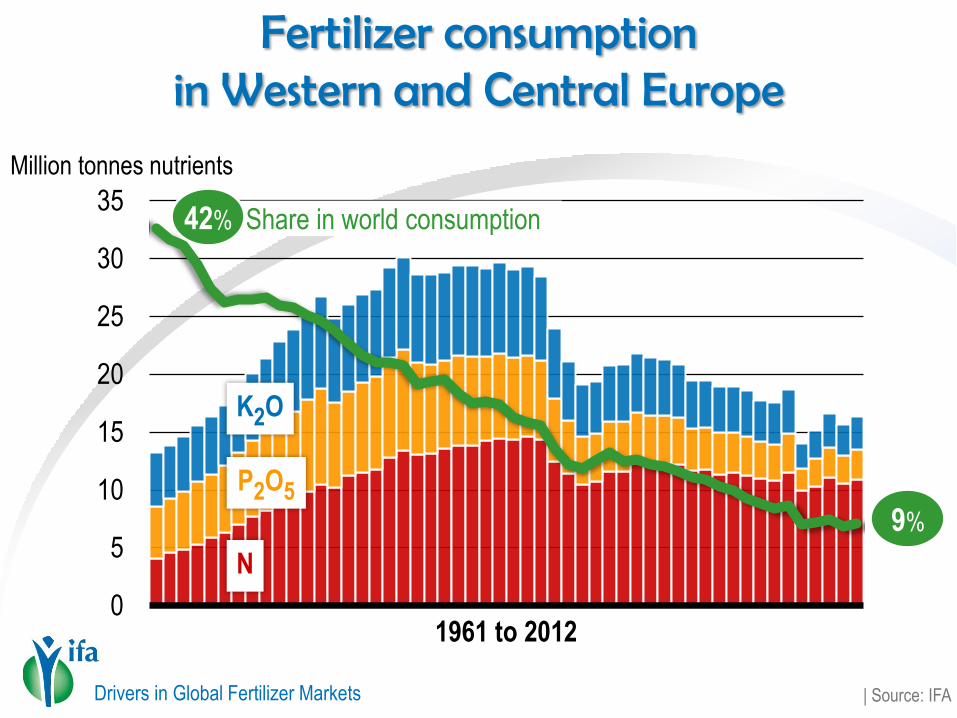

Fertilizer consumption in Western and Central Europe

| Source: IFA

Million tonnes nutrients

1961 to 2012 0

5

10

15

20

25

30

35

K2O

P2O5

N

9%

Share in world consumption 42%

Drivers in Global Fertilizer Markets

Evolution of cereals + rapeseed production relative to fertilizer-N deliveries in France

(100 = 1990)

| Source: SSP and UNIFA

100 = 1990

50

100

130

110

90

70

Development of

agricultural production

Integrated fertilization

120

60

80

140

Cereals production + rapeseed (est. 09/13)

Fertilizer-N deliveries

Drivers in Global Fertilizer Markets

Consumption by product in Western and Central Europe

43%

| Source: IFADATA

33%

82%

60%

Drivers in Global Fertilizer Markets

Fertilizer production and trade in Western and Central Europe

| Source: IFA

Million tonnes nutrients

0

5

10

15

20

25

30

35

0

2

4

6

8

10

12

14

16

18

1961 to 2012

Million tonnes nutrients

PRODUCTION EXPORTS

0

2

4

6

8

10

12

14

16

18

Million tonnes nutrients

IMPORTS

1961 to 2012 1961 to 2012

K2O

P2O5

N

Drivers in Global Fertilizer Markets

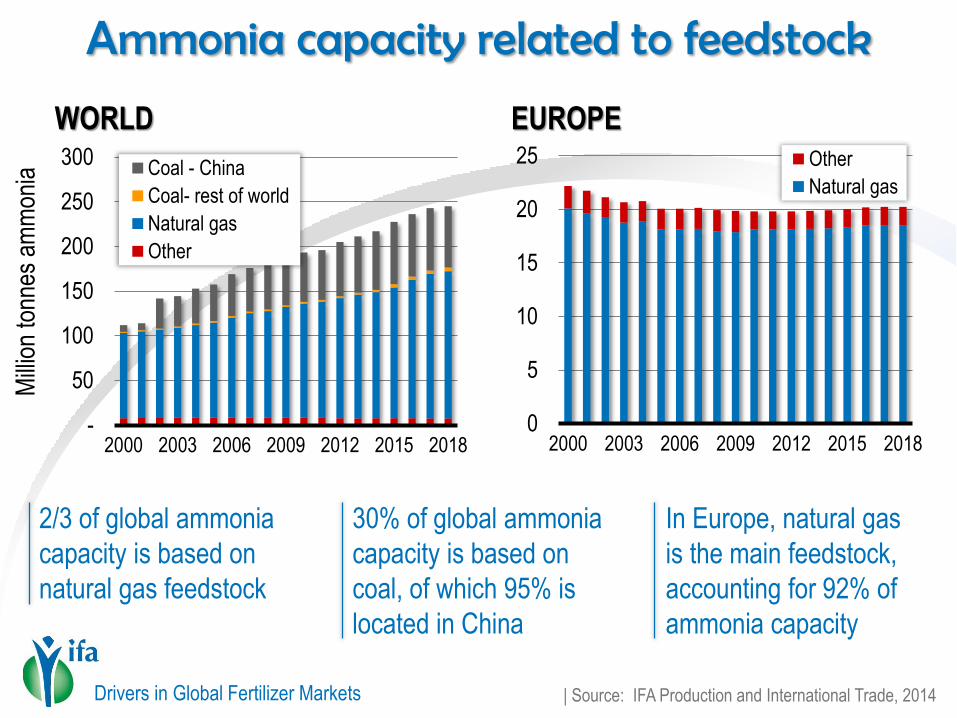

Ammonia capacity related to feedstock

0

5

10

15

20

25

2000 2003 2006 2009 2012 2015 2018

Other

Natural gas

WORLD EUROPE

| Source: IFA Production and International Trade, 2014

Mill

ion

tonn

es a

mm

onia

-

50

100

150

200

250

300

2000 2003 2006 2009 2012 2015 2018

Coal - China

Coal- rest of world

Natural gas

Other

2/3 of global ammonia

capacity is based on

natural gas feedstock

30% of global ammonia

capacity is based on

coal, of which 95% is

located in China

In Europe, natural gas

is the main feedstock,

accounting for 92% of

ammonia capacity

Drivers in Global Fertilizer Markets

Urea cash costs Influence of natural gas prices

0

50

100

150

200

250

300

350

400

450

5 6 7 8 9 10 11 12 13 14 15

other

natural gas cost

Ammonia and urea cash

costs are closely correlated to

feedstock prices.

The cost of natural gas

accounts for 87-95% of the

cash cost of ammonia

production;

and between 78% and 91%

of the cast costs of urea

production.

US$/MMBtu

US$/tonne

| Source: http://www.yara.com/tools/cashcost.htm

Drivers in Global Fertilizer Markets

Natural gas Regional wholesales prices 2013

| Source: IGU, 2014

US$/MMBtu

Comparative wholesales prices of natural gas show

significant disparities between regions.

0

2

4

6

8

10

12

14

16

NE Asia Europe Asia EECA SouthAsia

America WA Africa

Drivers in Global Fertilizer Markets

Urea cash costs vs natural gas prices Trend 2014 to 2015e

| Source: US EIA, Azotecon, CICCC, Argus, Yara cost model

US$/tonne

0

100

200

300

400

500 2014 2015

US Russia China WE_

Zeebrugge

Ukraine

West Asia

Africa

Drivers in Global Fertilizer Markets

Nitrogen supply/demand balances Europe 2011 - 2018

| Source: IFA Production and International Trade, 2014

Million tonnes nitrogen

-

4

8

12

16

20

2011 2012 2013 2014 2015 2016 2017 2018

Supply Demand

Drivers in Global Fertilizer Markets

Nitrogen fertilizer imports into Europe: 2013

| Source: IFA Production and International Trade, 2014

Mill

ion

tonn

es p

rodu

cts

0

1

2

3

4

5

6

7AN

CAN

Urea

Europe Belarus

Russia Ukraine

West Asia Americas

Africa Other

NITROGEN FERTILIZER IMPORTS

UREA IMPORTS

Europe

44%

Africa

27%

EECA

22%

West Asia

7%

Drivers in Global Fertilizer Markets

Regional urea capacity developments 2013 - 2018

| Source: IFA Production and International Trade, 2014

Africa

Europe

Russia USA

West Asia

Million tonnes urea

0

5

10

15

20

25

30

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

www.fertilizer.org

For more information…

0

2

4

6

8

10

12

14

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

US$/MMBtu

Source : US Energy Information Agency

USA: Natural gas industrial prices

Indigeneous production

34%

Russia 24%

Norway 23%

Algeria 9%

Qatar 6%

Other 4%

Europe: Natural gas supplies 2012

Total

5060 TWh

http://www.eurogas.org/uploads/media/Eurogas_Statistical_Report_2013.pdf