· pdf filedrugs key highlights ... – 8 products filed and 1 product approved in china...

TRANSCRIPT

Page I 1

LOTUSBUILDING A PAN-REGIONAL LEADER

NOVEMBER 2015

Page I 2

Safe Harbor Statement

Except for historical information contained herein, the matters set forth in this presentation are forward

looking statements that are subject to risks and uncertainties that could cause actual results to differ

materially. These forward looking statements are not based on historical facts but rather on

management’s expectations regarding future growth, results of operations, performance, future capital

and other expenditures, competitive advantages, business prospects and opportunities. Statements in

this presentation about our future plans and intentions, results, level of activities, performance, goals or

achievements or other future events constitute forward looking statements. Wherever possible, words

such as “anticipate”, “believe”, “expect”, “may”, “could”, “will”, “potential”, “intend”, “estimate”, “should”,

“plan”, “predict”, or the negative or other variations of statements reflect management’s current beliefs

and assumptions and are based on the information currently available to our management. Investors

are cautioned not to place undue reliance on these forward looking statements, which are made

as of the date of this presentation and we assume no obligation to update or revise any forward

looking statements.

Page I 2

Page I 3Page I 3

COMPANY OVERVIEW

Page I 3

Page I 4

COMPANY OVERVIEW

• A fast growing, pan-regional, generic and specialty

pharma company with access to advanced markets

through industry leading pipeline

• 63.4% owned by Alvogen, a specialty pharmaceutical

company with global presence

• 1 US FDA, EU EMA, and Japan PMDA approved

manufacturing facility, 2 KGMP approved

manufacturing facilities and R&D centers

• #1 in Korea in terms of sales from anti-obesity drug,

and strong presence in Taiwan for oncology and CNS

drugs

Key Highlights

• Robust international pipeline:

– Distribution rights of 2 biosimilars under development by Alvotech

– 10 products in pipeline / filed ANDA for US

– 8 products and CMO projects for Japan in pipeline

– 8 products filed and 1 product approved in China

– 4 products for EU Asia scope in pipeline

Strong Pipeline

Market Leader in the Highly Attractive Asia Pacific Generic Pharmaceutical Industry with Access to Other Advanced Markets

Page I 4

Strong Growth and Margin

Gross Profit

Net Profit

Gross Margin (%)

Revenue

Q2’15

760

125

56.8%

1,337

Q1’15

EPS (NT$) 0.37

Unit: NT$mm

Operating Income 91

Q3’15

873

17

61.6%

1,417

0.06

162

745

(21)

57.5%

1,294

(0.13)

70

Cash EPS1 (NT$) 0.95 1.150.43

1 Cash EPS = Cash flows from operating activities / number of outstanding shares

6.8% 11.4%5.4%Operating Margin (%)

Page I 5

COMPANY OVERVIEW

Lotus History and Key Milestones

1966

Page I 5

Manufacturing

Facility Obtained

Japan PMDA

Approval

Lotus Acquired

Dream Pharma

Founded in 1966

Manufacturing

Facility Obtained

US FDA Approval

First Product

Launch in the

US

Manufacturing Facility

Obtained EU EMA

Approval

First Product

Launch in Japan

US FDA

Compliance

Inspection Passed

Alvogen Became a Majority Shareholder of Lotus

Lotus Acquired Alvogen’s Korea, Taiwan and India Businesses

Aug 11

Dec 19

EU EMA

Compliance

Inspection Passed

Listed in GreTai

Stock Exchange

(1795.TT)

Jun 1Korea Operations, Kunwha and Dream

Pharma, Merged into Alvogen Korea

Page I 6

COMPANY OVERVIEW

Shareholding Structure

Note: as of September 30, 2015 Page I 6

Alvogen Asia Pacific

Holdings Ltd.

63.4%

Lotus Pharmaceutical

Co., Ltd.

(Taiwan)

Alvogen Taiwan

(Taiwan)

100.0% 100.0%

100.0%

100.0%

Lotus Lab, Ltd

(UK)

Lotus Pharmaceutical,

HK Inc.

(HK)

美喬生技有限公司

(Taiwan)

100.0%

Alvogen Korea

Holdings Ltd.

(Korea)

Alvogen Korea Co.,

Ltd.

(Korea)

82.5% 100.0%

98.0%

Alvogen Pharma India

Pvt Ltd.

(India)

Norwich Clinical

Services Pvt Ltd.

(India)

100.0%

100.0%

樂特仕生物科技諮詢

(上海)有限公司

(China)

Lotus International Pte.

Ltd.

(Singapore)

Merger between Kunwha

and Dream Pharma has

been completed on June

1, 2015

Page I 7

KEY OPERATIONS – LOTUS TAIWAN

Page I 7

Strong Presence in Taiwan

Key

Milestone

• Founded in 1966 and has been listed in Taiwan GreTai

market since 2010

• Strategic partnered with Alvogen in 2014

• Among the Top 3 of pharma companies in Taiwan by

revenue on consolidated basis

Product

Mix

• Specialized in CNS (~16-20% of total sales), oncology

(~8%-12% of total sales), and hormonal drugs (~14%-

18% of total sales)

• Also covering general care, including pain (~25%-30%

of total sales), CV, and others

R&D

• Strong R&D center with a special focus on US, Japan

and other APAC market

• Leading R&D personnel: 65% with a postgraduate

degree and extensive pharmaceutical career

experience

Production

• US FDA, EU EMA, Japan PMDA, and TFDA PIC/S

approved production facilities focusing on high potency

and cytotoxic products

Sales

Network

• 3 sales offices national wide

• c. 3,400 clinics and c. 480 general hospitals in Taiwan

Employee• 335 employees in total as of October 2015 – G&A (46),

R&D (76), S&M (74), Plant (139)

Head office in Taipei

Plant in Nantou

Sales office

in Taipei

Sales office

in Taichung

Sales office

in Kaohsiung

Page I 8

Comprehensive Footprints in Korea

KEY OPERATIONS – ALVOGEN KOREA

Page I 8

Key

Milestone

• Kunwha was founded in 1958 and acquired by Alvogen

in October 2012

• Dream Pharma was established as the pharmaceutical

division of Hanwha Corporation in 1996 and acquired

by Kunwha in December 2014

• Kunwha and Dream Pharma has merged and

become Alvogen Korea in June 2015

Product

Mix

• Anti-obesity drugs (~35%-40% of overall business): #1

player in Korea with 30+% market share

• Other prescription (“Rx”) drugs (~55%-60% of

business): competitive advantages in nephrology,

cardiology, urology, gastroenterology, and metabolic

disease treatment

R&D

• Leading R&D personnel: 74% with postgraduate

degree, 49% with pharmaceutical career experience

over 10 years

• Secured Korea’s New Drug Development Technical

Award for Bonviva Plus (Dream Pharma in February

2014)

Production• Two production facilities compliant with KGMP (Korea

Good Manufacturing Practice)

Sales

Network

• 12 sales offices national wide: 4 in Seoul and satellite

cities and 8 in other areas

• Accounts in network: ~6,000 clinics and ~670 general

& community hospitals in Korea

Employee • 576 employees in total as of October 2015 – G&A (61),

R&D (43), S&M (278), Plant (194)

Plant in Hyangnam

Head office in Seoul

Plant in Kongju

Page I 9

Strong CRO Capabilities Support to Lotus/Alvogen

KEY OPERATIONS – CRO CAPABILITIES IN INDIA

Page I 9

Norwich Clinical Services provides Biostudy, Clinical and pharmacovigilance services to

Lotus/Alvogen and 3rd party customers

Bangalore

• Clinical Area: 17,000 sq.ft

Located within a multi-specialty hospital

72 bed facility

Medical and surgical IC units

Emergency unit

Oncology center

Well equipped laboratory and pharmacy

• Office/Lab: 30,000 sq.ft

Corporate offices

Pharmacovigilance

Bio-analytical

PK, Biostats, and Medical writing

Clinical Data management

QA

Page I 10

2015 OUTLOOK & YTD PROGRESS

Page I 10

Goals in 2015

• Successful integration of Dream Pharma and Kunwha in Korea

Two companies completed the logistic integration on April 1st and has officially merged into one legal entity and

renamed as Alvogen Korea effective June 1st

The combined entity successfully launched Sarpogrelate XR and gained more than 30% market share in Korea as

of June 2015

The combined efforts also enhanced its product portfolio and successfully launched Seroquel (Quetiapine) to

establish a solid foothold in Korean CNS market

• Further expand Lotus’ export business by launching more products in the US

ANDA of Levonorgestrel has been officially approved by US FDA in June

• Officially launched with the first shipment to the US market in September

Tentative approval for ANDA of Paricalcitol Capsules from US FDA was granted in July

• Achieve solid profit and positive EPS

Profitability of New Lotus Group is improving as realizing the synergies of integration gradually with a reported

consolidated gross margin of 57.5% for Q1’15

• Gross margin further expanded to 61.6% in Q3’15

The continuous improvement of operational efficiency also makes the Company to report a positive EPS for Q2’15

and continue to grow in Q3’15

Page I 11

2015 OUTLOOK & YTD PROGRESS (CONT’D)

Page I 11

2015YTD MA recevied

Generic Name Indication Country Approval

Date

Remarks

Levetiracetam 750mg Tab CNS TW Jan 2015 Lotus

Thalidomide Oncology KR Feb 2015 Lotus

Entecavir Tab Antiviral KR Feb 2015 Alvogen Korea

Temozolomide 20mg, 100mg, 140mg, 180mg Brain cancer EU Mar 2015 Lotus

Meropenem 500mg, 1000mg Anti-infection TW Apr 2015 Lotus

Irbesartan + HCTZ 25mg Tab CV TW May 2015 Lotus

Lamotrigen 100mg Tab CNS TW May 2015 Lotus

Amlodipine/Losartan CV KR May 2015 Alvogen Korea

Tadalafil Erectile dysfunction KR May 2015 Alvogen Korea

Cefepime Anti-infection KR May 2015 Alvogen Korea

Levonorgestrel 1.5mg Contraceptive US Jun 2015 Lotus

Lamivudine Antiviral HK Jun 2015 Lotus

Rosuvastatin 10mg, 20mg, Tab CV TW Jun 2015 Lotus

Entecavir ODF Antiviral KR Jul 2015 Alvogen Korea

Rosuvastatin/Ezetimibe CV KR Sep 2015 Alvogen Korea

Imatinib 100mg, 400mg Oncology TW Sep 2015 Lotus

Temozolomide 20mg, 100mg Brain cancer HK Sep 2015 Lotus

Diosmin 500mg Metabolism TW Oct 2015 Lotus

Paricalcitol 1mcg, Softgel Cap Nephrology TW Oct 2015 Lotus

Note: as of October 31, 2015

Page I 12

2015 OUTLOOK & YTD PROGRESS (CONT’D)

Page I 12

2015YTD Product Launch

Generic Name Indication Country Launch Time Remarks

Bicalutamide Oncology TW Feb 2015 Lotus

Ceftriaxone Sodium Anti-infection TW Feb 2015 Lotus

Exemestane Oncology TW Feb 2015 Lotus

Doxorubicin Hydrochloride Oncology TW Mar 2015 Lotus

Epirubicin hydrochloride 10mg, 50mg Oncology TW Apr 2015 Lotus

Carboplatin Oncology TW May 2015 Lotus

Sarpogrelate 300mg Antithrombotics KR May 2015 Alvogen Korea

Celecoxib NSAIDs KR Jun 2015 Alvogen Korea

Ranitidine/Tripotassium Bismuth

Dicitrate/Sucralfate

Gastrointestinal KR Jul 2015 Alvogen Korea

Amlodipine/Losartan CV KR Aug 2015 Alvogen Korea

Buprenorphine/Naloxone 2/0.5mg, 4/1mg Addiction TW Jul/ Aug 2015 Lotus

Tadalafil Erectile dysfunction KR Sep 2015 Alvogen Korea

Nafamostat CV KR Sep 2015 Alvogen Korea

Cefepime Anti-infection KR Sep 2015 Alvogen Korea

Levonorgestrel Contraceptive TW/US Jul/ Sep 2015 Lotus

Irbesartan CV TW Sep 2015 Lotus

Quetiapine CNS KR Oct 2015 Alvogen Korea

Entecavir (Tab/Flim) Antiviral KR Oct 2015 Alvogen Korea

Note: as of October 31, 2015

Page I 13Page I 13

INVESTMENT HIGHLIGHTS

Page I 13

Page I 14

INVESTMENT HIGHLIGHTS

Lotus is Committed to Delivering Value-Driven Medicine

Strong in Highly Attractive and Fast Growth Markets, and Continue

to Grow Asia and Advanced Countries Sales (US/JP/EU)

Execute Strategic M&A

Strong Support from Majority Shareholder - Alvogen

2

3

6

1

Page I 14

Page I 15

INVESTMENT HIGHLIGHTS

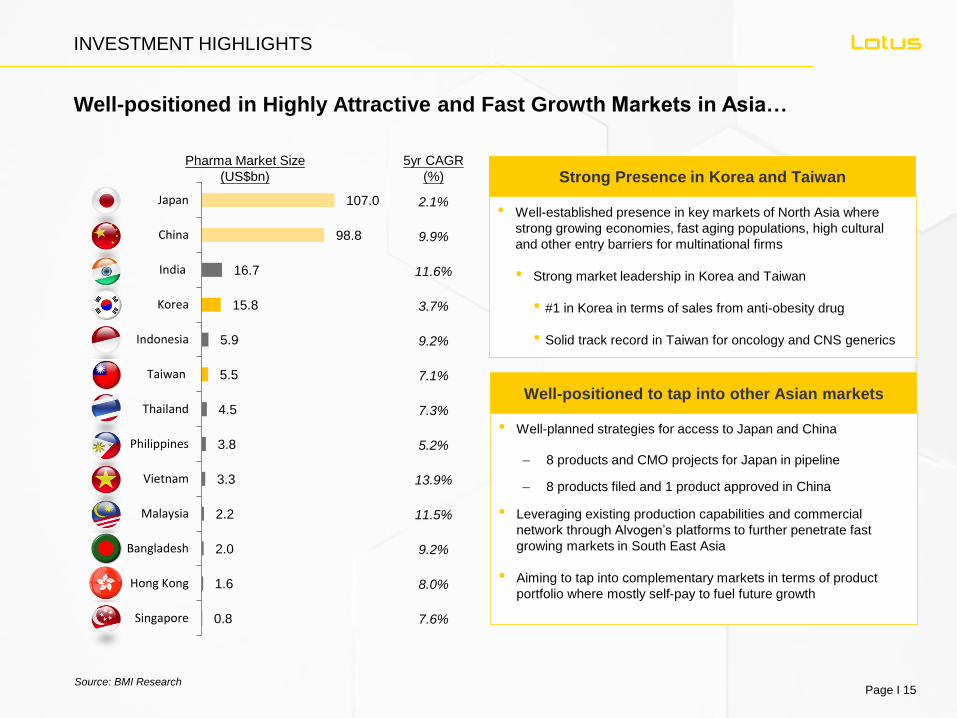

Well-positioned in Highly Attractive and Fast Growth Markets in Asia…

Page I 15

Pharma Market Size

(US$bn)

5yr CAGR

(%)

2.1%

9.9%

11.6%

3.7%

9.2%

7.1%

7.3%

5.2%

13.9%

11.5%

9.2%

8.0%

7.6%

• Well-established presence in key markets of North Asia where

strong growing economies, fast aging populations, high cultural

and other entry barriers for multinational firms

• Strong market leadership in Korea and Taiwan

• #1 in Korea in terms of sales from anti-obesity drug

• Solid track record in Taiwan for oncology and CNS generics

Strong Presence in Korea and Taiwan

• Well-planned strategies for access to Japan and China

– 8 products and CMO projects for Japan in pipeline

– 8 products filed and 1 product approved in China

• Leveraging existing production capabilities and commercial

network through Alvogen’s platforms to further penetrate fast

growing markets in South East Asia

• Aiming to tap into complementary markets in terms of product

portfolio where mostly self-pay to fuel future growth

Well-positioned to tap into other Asian markets

Source: BMI Research

0.8

1.6

2.0

2.2

3.3

3.8

4.5

5.5

5.9

15.8

16.7

98.8

107.0

Singapore

Hong Kong

Bangladesh

Malaysia

Vietnam

Philippines

Thailand

Taiwan

Indonesia

Korea

India

China

Japan

Page I 16

• Well recognized by clinics, hospitals and pharmacies / drugstores

• Effectively market and sell existing products and new products

• Foundation for cross-selling products targeting fast-growing / core therapeutic areas

INVESTMENT HIGHLIGHTS

… As Well As US with Strong Sales Forces and Distribution Channels

Solid Market

Position

Strong Brand

Recognition

Taiwan

South

Korea

UK

Shanghai

Indian

US

- Direct access with strong pipeline leveraging

US FDA approved manufacturing facility

- 2 products in market and 10 products in

pipeline/ filed ANDA in the US

- Product launch through Alvogen’s existing

sales forces or partnership

• Covering a network of ~10,000 clinics, hospitals and pharmacies / drugstores with internal sales force in key markets

• Experienced sales force with product expertise

• Strong management team with executives and regional managers who have years of experience in the pharmaceutical industry

Presence Access

Headquarter Branch Offices

Partnership

Page I 16

Page I 17

INVESTMENT HIGHLIGHTS

High Growth via Organic Growth and Strategic M&As

• Robust portfolio of existing products with additional

potentials from board pipeline to gain further market share

in existing and new markets

• Aggressive product launches across the APAC region – 26

products selected and roll out started into Korea and

other Asian markets

Organic Growth

• Supports from Alvogen to capture opportunities ahead of

industry consolidation in the region

• Strengthen product portfolio in focused therapeutic area

• Complementary/minimal overlap with existing product

portfolio or pipeline

M&A Strategies

Existing

products

Pipeline

potentials

Existing

products

Existing

products

Pipeline

potentials

M&As

Page I 17

Page I 18

INVESTMENT HIGHLIGHTS

• In-house R&D capabilities

• Collaboration with industry leading

companies and research institutions

• Systematically acquires and integrates

targets with solid development and

commercialization track record

Strong Development Capability

• Integrated capabilities spanning a wide-

range of therapeutic areas:

– Strategically focus on oral oncology,

high potency, and soft gel drugs

• Solid contract research organization in

India:

– Facilitates oncology studies

– Quick patient enrollment

Integrated R&D Platform

Integrated R&D

Capabilities with a

proven track record

of successful

innovations

• US FDA, EU EMA and Japan PMDA

approved production facilities focusing

on high potency and cytotoxic products

• Provides oncology contract manufacturing

organization services to Japanese

pharmaceutical companies

• Analytic process development for quality

control and assurance

Multiple Manufacturing Platforms

Strong R&D and Solid Manufacturing Capabilities Delivering Top

Quality Drugs…

Page I 18

Page I 19

INVESTMENT HIGHLIGHTS

… And Robust Product Portfolio

Page I 19

Robust Product Portfolio

CategoryProduct Offering

Growth Key Product Updates Taiwan Korea

Anti-obesity V V

• Phentermine IR/ER

• Phendimetrazine

• Orlistat

Nephrology V• Calcium Polystyrene Sulfonate

• Epoeitin

Oncology V • Temozolomide

CNS V V

• Trazodone

• Buprenorphine/Naloxone

• Seroquel (Quetiapine)

CV V V• Sarpogrelate

• Losartan/Amlodipine

Export Business V

• Mefenamic Acid

• Generic to TS-1

• Levonorgestrel

Page I 20

INVESTMENT HIGHLIGHTS

Broad Pipeline that Delivers Sustainable Growth

Data as of October 2015

Note: Target market numbers are FY2014 market sales from IMS data

Page I 20

For US market

Generic Name Indication

Target

Market

(US$mn)

For-

mulation

Clinical/

BE Study

Sub-

mission Approval Launch Remarks

Paricalcitol Nephrology 60Tentative approval received in Jul 2015 with final approval

expected in Q1'16

Budesonide

ER

Gastro

intestinal 500

PIV; filing acceptance received Jan 2015; sued on only 3 out of

the 6 patents listed in Orange Book

Calcium

acetate Nephrology 200

PIV; sued while the case has dismissed and settled on

confidential terms

Not Disclosed CNS 700 PIV

Not Disclosed CNS 550PIV; 500mg approved while other strength waiting for approval

with no outstanding regulatory issues

Buprenorphine/

NaloxoneAddiction 1,600 PIV; filing acceptance received Apr 2015; sued

Not Disclosed Brain cancer 260 No patent in Orange Book

Not Disclosed Cancer 600 Few expected competition

Not Disclosed Autoimmune 340 No patent in Orange Book

Not Disclosed Cancer 700 No patent in Orange Book

Page I 21

Generic Name Indication

Target

Market

(US$mn)

For-

mulation

Clinical/

BE Study

Sub-

mission Approval Launch Remarks

Not Disclosed Allergy 370

Not Disclosed Brain cancer 90

Not Disclosed Steroid 130

GefitinibNon-small-cell

lung cancer150

Capecitabine Colon cancer 100

Nalfurafine Pruritus 135

Not Disclosed Hormone 90

INVESTMENT HIGHLIGHTS

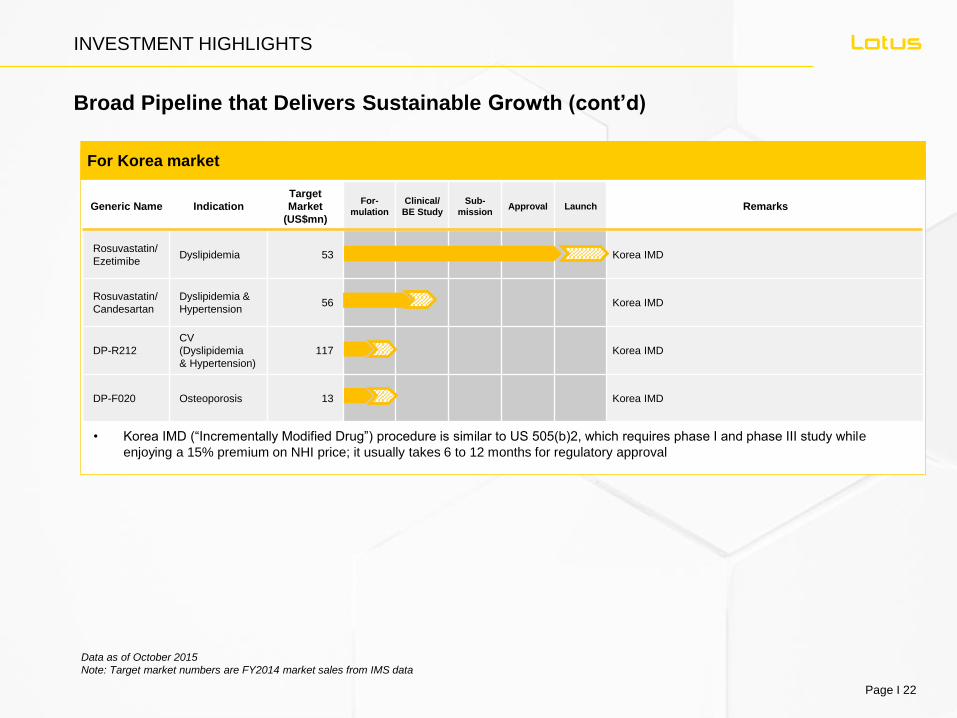

Broad Pipeline that Delivers Sustainable Growth (cont’d)

Page I 21

For Japan market

• For Japan market, we strategically work on CMO projects for partners to further penetrate into the local market

Data as of October 2015

Note: Target market numbers are FY2014 market sales from IMS data

Page I 22

Generic Name Indication

Target

Market

(US$mn)

For-

mulation

Clinical/

BE Study

Sub-

mission Approval Launch Remarks

Rosuvastatin/

EzetimibeDyslipidemia 53 Korea IMD

Rosuvastatin/

Candesartan

Dyslipidemia &

Hypertension56 Korea IMD

DP-R212

CV

(Dyslipidemia

& Hypertension)

117 Korea IMD

DP-F020 Osteoporosis 13 Korea IMD

INVESTMENT HIGHLIGHTS

Broad Pipeline that Delivers Sustainable Growth (cont’d)

Page I 22

For Korea market

• Korea IMD (“Incrementally Modified Drug”) procedure is similar to US 505(b)2, which requires phase I and phase III study while

enjoying a 15% premium on NHI price; it usually takes 6 to 12 months for regulatory approval

Data as of October 2015

Note: Target market numbers are FY2014 market sales from IMS data

Page I 23

Generic Name Indication Scope

Target

Market

(US$mn)

For-

mulation

Clinical/

BE Study

Sub-

mission Approval Launch Remarks

Temozolomide Brain cancerEU

APAC450 Already launched in Taiwan; approved in EU

Gimeracil/

Oteracil/

Tegafur (TS-1)

Colon cancer APAC 280 Already launched in Japan; filed in Taiwan/Korea

Vinorelbine Breast cancerEU

APAC160 Less than 3 producers as of now

Gefitinib Lung cancer EU

APAC380

5 ALA Cancer EU

APAC- No BE

Difficult API required

Complimentary to other oncology portfolio

INVESTMENT HIGHLIGHTS

Broad Pipeline that Delivers Sustainable Growth (cont’d)

Page I 23

For other markets

• More projects under evaluation and discussion – we are always assessing the market potentials of launching our existing

products/projects to different markets in the world and will decide on a most competitive strategy to maximize the value of pipeline

Data as of October 2015

Note: Target market numbers are FY2014 market sales from IMS data

Page I 24

Generic Name Indication

Target

Market

(US$mn)

CTP1 sub-

mission

Clinical/

BE Study

IDL2 sub-

mission Launch Remarks

Levonorgestrel Contraception 50 CTP submitted in Q2’10

Divalproex sodium Anti-epilepsy 100 CTP submitted in Q4’08

Lidocaine Local analgesic 30 CTP submitted in Q1’10

Glucosamine sulfate

+ Sodium chlorideOsteo-arthritis 150 CTP submitted in Q3’11

Acarbose Antidiabetic 380 CTP submitted in Q4’11

Levetiracetam Anti-epilepsy 40 CTP submitted in Q4’12

Temozolomide Brain cancer 90 CTP submitted in Q1’13

Memantine Anti-dementia 15 CTP submitted in Q2’13

INVESTMENT HIGHLIGHTS

Broad Pipeline that Delivers Sustainable Growth (cont’d)

Page I 24

For China market

• All the filings in China are the approved products in Taiwan, so no duplicate formulation is required

• For all the imported products, there are two applications needed – Clinical Trial Permit (“CTP”) submission goes first and then Imported

Drug License (“IDL”) submission is required once clinical/BE study is done

Data as of October 2015

Note: Target market numbers are FY2014 market sales from IMS data

Page I 25

INVESTMENT HIGHLIGHTS

Broad Pipeline that Delivers Sustainable Growth (cont’d)

Page I 25

Biosimilars

• Alvogen/Alvotech aims to create a leading presence in

biosimilars

• US$500 million is being invested in a new state-of-the-

art biotech plant and pipeline

• Lotus and Alvogen/Alvotech signed distribution

agreements for two key biosimilars currently under

development by Alvotech

• Lotus will market and distribute these biosimilars in the

following APAC markets: Taiwan, China, Vietnam, South

Korea, Thailand, Hong Kong, Philippines, Malaysia,

Indonesia, Singapore and Myanmar

Molecule Indication Target

Market (US$)

Expected

launch timing

Not Disclosed Oncology 154mn 2020

Not Disclosed Rheumatoid

arthritis;

Psoriasis

90mn 2020

Data as of October 2015

Note: Target market numbers are FY2014 market sales from IMS data

Page I 26

INVESTMENT HIGHLIGHTS

Solid Integration Capabilities and Management Team that Extract Synergies and Generate Value…

Extensive Experience

Senior management team has comprehensive

experience up to 20 years in the pharmaceutical

industries

In-depth Knowledge

Many have worked with leading global

pharmaceutical companies. They bring extensive

M&A and industry experience and in-depth

knowledge

Diversified Exptertise

Experience and expertise range from research

and development to manufacturing, sales,

marketing and distribution

Regional Supports –

David Young, Regional CFO

Dr. Jon Valgeirsson, Regional R&D VP

Mike Stradling, Regional Supply Chain VP

Dr. Chung R. Kim, Regional Quality Director

Jade Lee, Regional HR Director

Dr. Saral Thangam, CEO Norwich Clinical Services (CRO India)

Siegfried Gschliesser, VP of M&A and Integration – Global

Renaat JanssenCEO Lotus

Previously Executive Director at PPD with more than 20 years experience in pharma industry

Page I 26

Lotus Leadership Team in Taiwan –

Allen Hong, VP of Operations

Ben Chung, CFO

Kevin Huang, VP of Sales and Marketing

Vicky Lee, VP of Regulatory Affairs

Page I 27

INVESTMENT HIGHLIGHTS

… With Strong Support from Board of Directors

Page I 27

Charles Lin Chairman of BOD

• Founder of Lotus and has more than 30 years in pharmaceutical industry

• Leads Lotus as a R&D-based Taiwanese company with manufacturing facilities approved by global FDAs

Robert Wessman Director

• Chairman and CEO of Alvogen Group• Has grown Alvogen from a small US

business into an international pharma with commercial operations in 34 countries and with 2,000 employees within 5 years

Independent Directors

Benjamin Ku Partner at Cheng & Ku Law firm

Hjorleifur Palsson Previous EVP and CFO at Ossur hf., a listed company at NASDAQ OMX Copenhagen

Directors

Arni Hardarson Chief Legal Counsel, Alvogen

Kevin Bain CFO, Alvogen

Thor Kristjansson EVP M&A, Alvogen

Le Hong VP, Lotus

• Combined efforts from Lotus founding team as well as strong commitment from Alvogen Group with

seamless cooperation

• Eight distinguished members with an exceptional knowledge and experience in the related fields to

guide the Company in all aspects

Page I 28Page I 28

FINANCIAL HIGHLIGHTS

Page I 28

Page I 29

FINANCIAL HIGHLIGHTS

Robust Growth Momentum for Monthly Sales 2015 YTD

Unit: NT$mn

+3.3%• Robust Q1 sales as the merger between Lotus and Alvogen’s key operations

in Asia has been completed in 2014 with closing of Kunwha’s acquisition of

Dream Pharma in December

• In addition to continuous growth from subsidiaries, Q2 sales of Lotus itself

also increased by 9% quarter-over-quarter.

• Contributed by further sales increase from Alvogen Korea’s newly-launched

product and export sales to the US market, Q3 sales delivered a consecutive

growth of 6.0% over Q2.

Key highlights

Note: Monthly sales are management accounts

+6.0%

Page I 29

435 432 429 448 430 444

531

437 460 453

Jan Feb Mar Apr May Jun Jul Aug Sep Oct

1,294 1,337

1,417

Q1 Q2 Q3

Page I 30

(318)

70 91

162

Q4'14 Q1'15 Q2'15 Q3'15

43.4%

57.5% 56.8%61.6%

Q4'14 Q1'15 Q2'15 Q3'15

FINANCIAL HIGHLIGHTS

Improving Profitability Quarter over Quarter...

Page I 30

+18% from Q4’14

Unit: % Unit: NT$mn Unit: NT$mn

Turned positive in Q1 and

further improved throughout Q3

Gross Magin Operating Income Net Income

Significantly increased in Q2 and

maintained profitable in Q3

(257)

(21)

125

17

Q4'14 Q1'15 Q2'15 Q3'15

Page I 31

1,096 1,138

1,296

- - - -

1,445

102 19

28 37 2 -

105

17 2 -

102

61 226

-

274

-

- - -

Q4'14Cash

Balance

Generatedfrom

Operations

Generatedfrom

Investment

Used inFinancing

FX Impact Q1'15Cash

Balance

Generatedfrom

Operations

Used inInvestment

Used inFinancing

FX Impact Q2'15Cash

Balance

Generatedfrom

Operations

Used inInvestment

Used inFinancing

FX Impact Q3'15Cash

Balance

FINANCIAL HIGHLIGHTS

… and Increasingly Generating Cash Inflow to Fuel the Further Growth

- NT$274 million generated from operations in Q3

Page I 31

Continuously improved cash-generating capability

from daily operations

Unit: NT$mn

++

+

-

+

-

- - -

-

- -

Page I 32

FINANCIAL HIGHLIGHTS

EPS v.s. Cash EPS

Page I 32

EPS (NT$) Cash EPS (NT$)

Q4’14Q4’14

• EPS = Net Income / # of Outstanding Shares • Cash EPS = Cash flows from operating activities / # of

Outstanding Shares

• Better indicator as it represents real cash earned from

daily operations

• More cash EPS also illustrates a better financial shape

for further expansion

(0.13)

0.37

0.06

Q4'14 Q1'15 Q2'15 Q3'15

0.43

0.95

1.15

Q4'14 Q1'15 Q2'15 Q3'15

Page I 33

FINANCIAL HIGHLIGHTS

Page I 33

Q3’15 Results – Consolidated Statement of Operations

Page I 34

FINANCIAL HIGHLIGHTS

Page I 34

Q3’15 Results – Consolidated Balance Sheets

Page I 35

FINANCIAL HIGHLIGHTS

Page I 35

Q3’15 Results – Consolidated Statements of Cash Flows

Page I 36

FINANCIAL HIGHLIGHTS

Page I 36

Q3’15 Results – Consolidated Statements of Cash Flows (cont’d)