fourth quarter 2015 earnings conference call presentation · 2/3/2016 fourth quarter 2015 earnings...

TRANSCRIPT

2/3/2016

Fourth Quarter 2015 Earnings Conference Call Presentation

February 3, 2016

Forward‐Looking Statements

2

This presentation contains forward-looking statements within the meaning of federal securities laws regarding MPLX LP ("MPLX"), Marathon Petroleum Corporation ("MPC"), and MarkWest Energy Partners, L.P. ("MarkWest"). These forward-looking statements relate to, among other things, expectations, estimates and projections concerning the business and operations of MPLX, MPC, and MarkWest. You can identify forward-looking statements by words such as "anticipate," "believe," "estimate," "expect," "forecast", "goal," "guidance," "imply," "objective," "opportunity,” "outlook," "plan," "project," "prospective," "position," "potential," "pursue," "seek," "target," "could," "may," "should," "would," "will" or other similar expressions that convey the uncertainty of future events or outcomes. Such forward-looking statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond the companies' control and are difficult to predict. In addition to other factors described herein that could cause MPLX's actual results to differ materially from those implied in these forward-looking statements, negative capital market conditions, including a persistence or increase of the current yield on common units, which is higher than historical yields, could adversely affect MPLX's ability to meet its distribution growth guidance. Factors that could cause MPLX's or MarkWest's actual results to differ materially from those implied in the forward-looking statements include: risk that the synergies from the MPLX/MarkWest merger transaction may not be fully realized or may take longer to realize than expected; disruption from the MPLX/MarkWest merger transaction making it more difficult to maintain relationships with customers, employees or suppliers; risks relating to any unforeseen liabilities of MarkWest; the adequacy of MPLX's capital resources and liquidity, including, but not limited to, availability of sufficient cash flow to pay MPLX’s distributions, and the ability to successfully execute both companies' business plans and growth strategies; the timing and extent of changes in commodity prices and demand for crude oil, refined products, feedstocks or other hydrocarbon-based products; volatility in and/or degradation of market and industry conditions; completion of midstream infrastructure by competitors; disruptions due to equipment interruption or failure, including electrical shortages and power grid failures; the suspension, reduction or termination of MPC's obligations under MPLX's commercial agreements; modifications to earnings and distribution growth objectives; the level of support from MPC, including dropdowns, alternative financing arrangements, taking equity units, and other methods of sponsor support, as a result of the capital allocation needs of the enterprise as a whole and its ability to provide support on commercially reasonable terms; federal and state environmental, economic, health and safety, energy and other policies and regulations; changes to MPLX's capital budget; other risk factors inherent to MPLX or MarkWest's industry; and the factors set forth under the heading "Risk Factors" in MPLX's Annual Report on Form 10-K for the year ended Dec. 31, 2014, filed with the SEC; and the factors set forth under the heading "Risk Factors" in MarkWest's Annual Report on Form 10-K for the year ended Dec. 31, 2014, and Quarterly Report on Form 10-Q for the quarter ended Sept. 30, 2015, filed with the SEC (former ticker symbol: MWE).

Forward‐Looking Statements (cont’d)

3

These risks, as well as other risks associated with MPLX, MarkWest and the merger transaction, are also more fully discussed in the joint proxy statement and prospectus included in the registration statement on Form S-4 filed by MPLX and declared effective by the SEC on Oct. 29, 2015, as supplemented. Factors that could cause MPC's actual results to differ materially from those implied in the forward-looking statements include: risks described above relating to MPLX, MarkWest and the MPLX/MarkWest merger transaction; changes to the expected construction costs and timing of pipeline projects; continued/further volatility in and/or degradation of market and industry conditions; the availability and pricing of crude oil and other feedstocks; slower growth in domestic and Canadian crude supply; the effects of the lifting of the U.S. crude oil export ban; completion of pipeline capacity to areas outside the U.S. Midwest; consumer demand for refined products; transportation logistics; the reliability of processing units and other equipment; MPC's ability to successfully implement growth opportunities; modifications to MPLX earnings and distribution growth objectives; federal and state environmental, economic, health and safety, energy and other policies and regulations; including the cost of compliance with the Renewable Fuel Standard; MPC’s ability to successfully integrate the acquired Hess retail operations and achieve the strategic and other expected objectives relating to the acquisition; changes to MPC’s capital budget; other risk factors inherent to MPC’s industry; and the factors set forth under the heading "Risk Factors" in MPC's Annual Report on Form 10-K for the year ended Dec. 31, 2014, filed with Securities and Exchange Commission (SEC). In addition, the forward-looking statements included herein could be affected by general domestic and international economic and political conditions. Unpredictable or unknown factors not discussed here, in MPLX's Form 10-K, in MPC's Form 10-K, or in MarkWest's Form 10-K and Form 10-Qs could also have material adverse effects on forward-looking statements. Copies of MPLX's Form 10-K are available on the SEC website, MPLX's website at http://ir.mplx.com or by contacting MPLX's Investor Relations office. Copies of MPC's Form 10-K are available on the SEC website, MPC's website at http://ir.marathonpetroleum.com or by contacting MPC's Investor Relations office. Copies of MarkWest's Form 10-K and Form 10-Qs are available on the SEC website (former ticker symbol: MWE), MarkWest's website at http://investor.markwest.com or by contacting MPLX's Investor Relations office.

Non-GAAP Financial Measures Adjusted EBITDA and distributable cash flow are non-GAAP financial measures provided in this presentation. Adjusted EBITDA and distributable cash flow reconciliations to the nearest GAAP financial measure are included in the Appendix to this presentation. Adjusted EBITDA and distributable cash flow are not defined by GAAP and should not be considered in isolation or as an alternative to net income attributable to MPLX or other financial measures prepared in accordance with GAAP.

Highlights

Completed strategic combination with MarkWest on Dec. 4, 2015 Reported fourth quarter adjusted EBITDA of $286 million and distributable cash

flow of $227 million with a strong coverage ratio of 1.20x Declared distribution of $0.50 per common unit for the fourth-quarter 2015,

representing in a 29 percent increase in 2015 Continued decline in commodity prices have resulted in a challenging valuation

and higher yield environment for MLPs Revised 2016 distribution growth forecast to 12 - 15 percent MPC offered to contribute its marine assets to the partnership, at a supportive

valuation, anticipated to be funded entirely with MPLX equity issued to MPC

4

Marine Business Overview

5

Fully-Integrated Marine Transportation and Service Provider

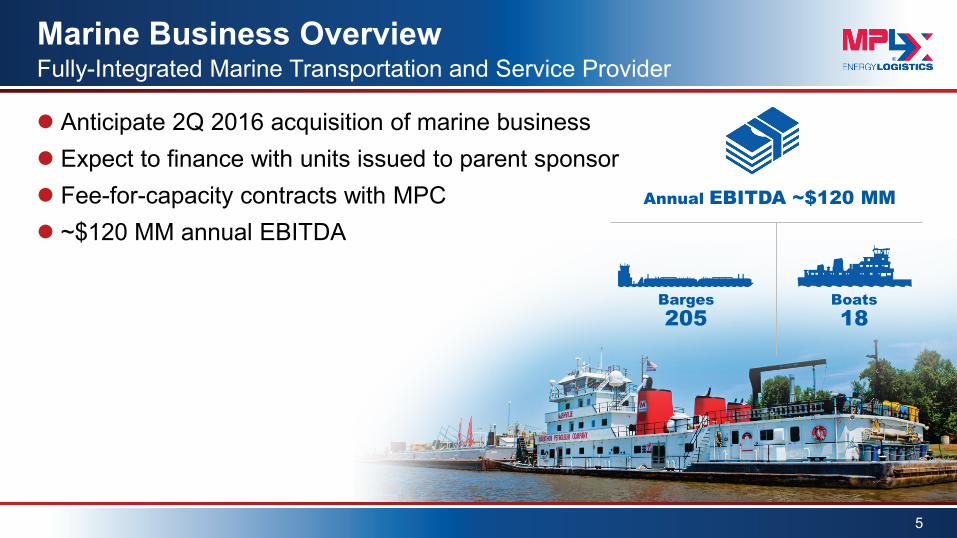

Anticipate 2Q 2016 acquisition of marine business Expect to finance with units issued to parent sponsor Fee-for-capacity contracts with MPC ~$120 MM annual EBITDA

Annual EBITDA ~$120 MM

Barges 205

Boats 18

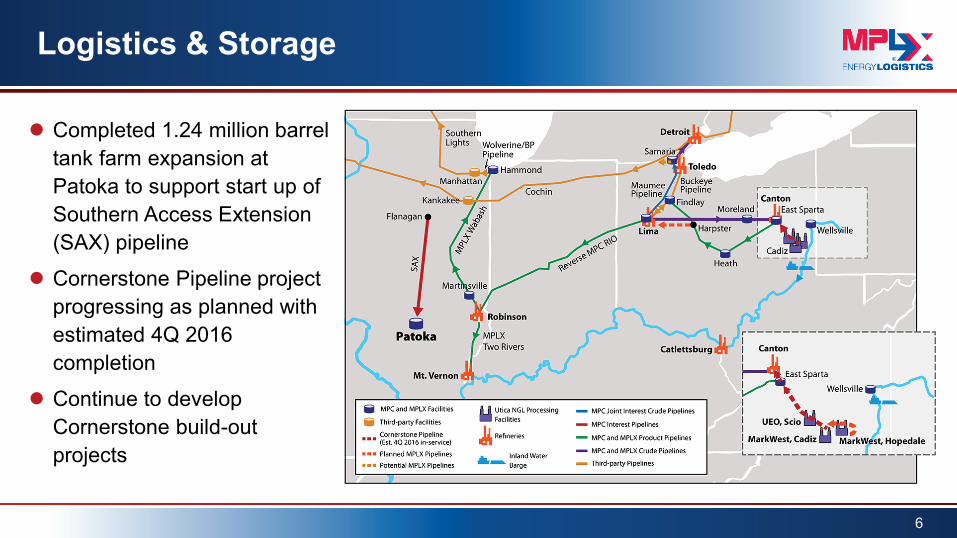

Logistics & Storage

6

Completed 1.24 million barrel tank farm expansion at Patoka to support start up of Southern Access Extension (SAX) pipeline

Cornerstone Pipeline project progressing as planned with estimated 4Q 2016 completion

Continue to develop Cornerstone build-out projects

Gathering & Processing

7

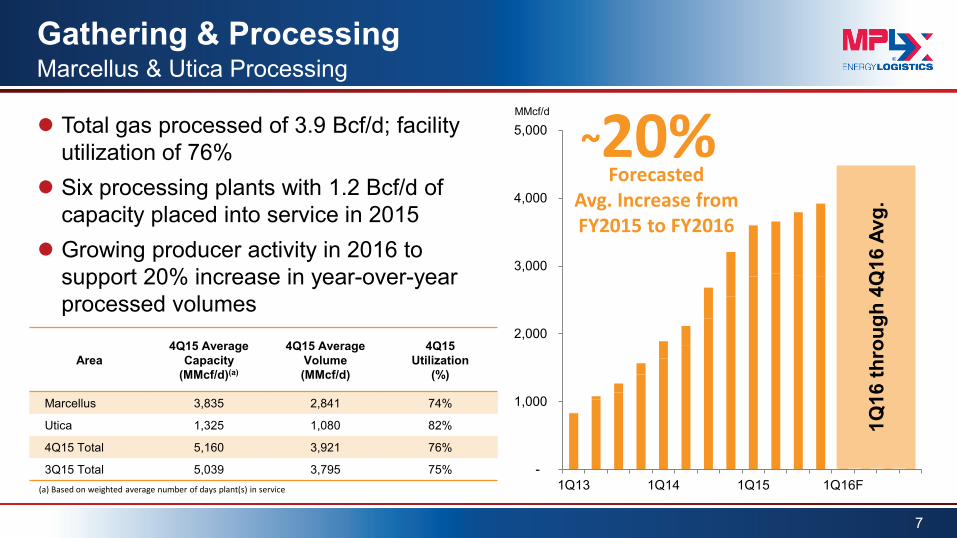

Marcellus & Utica Processing

Area 4Q15 Average

Capacity (MMcf/d)(a)

4Q15 Average Volume (MMcf/d)

4Q15 Utilization

(%)

Marcellus 3,835 2,841 74%

Utica 1,325 1,080 82%

4Q15 Total 5,160 3,921 76%

3Q15 Total 5,039 3,795 75% -

1,000

2,000

3,000

4,000

5,000

1Q13 1Q14 1Q15 1Q16F

MMcf/d

Forecasted Avg. Increase from FY2015 to FY2016

~20%

Total gas processed of 3.9 Bcf/d; facility utilization of 76%

Six processing plants with 1.2 Bcf/d of capacity placed into service in 2015

Growing producer activity in 2016 to support 20% increase in year-over-year processed volumes

(a) Based on weighted average number of days plant(s) in service

1Q16

thro

ugh

4Q16

Avg

.

Gathering & Processing

8

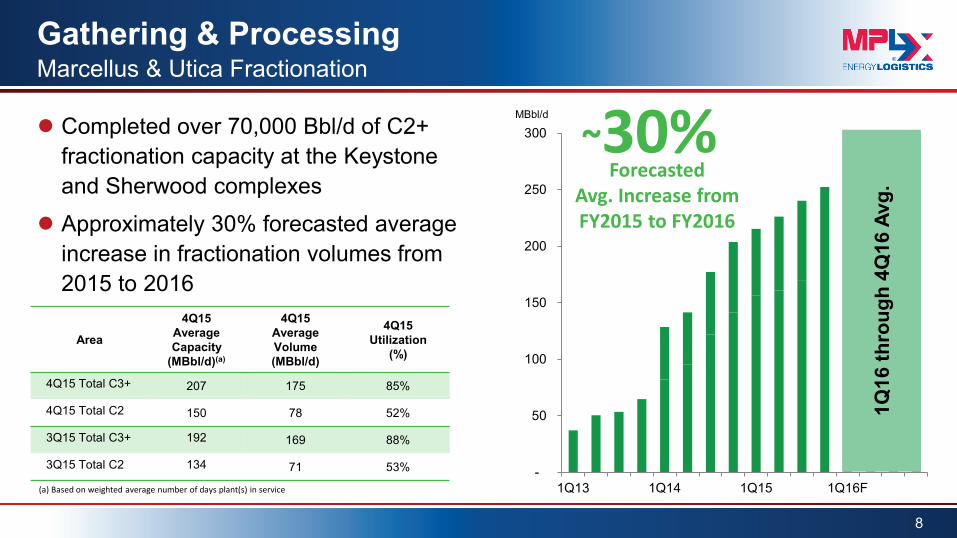

Marcellus & Utica Fractionation

Area

4Q15 Average Capacity

(MBbl/d)(a)

4Q15 Average Volume (MBbl/d)

4Q15 Utilization

(%)

4Q15 Total C3+ 207 175 85%

4Q15 Total C2 150 78 52%

3Q15 Total C3+ 192 169 88%

3Q15 Total C2 134 71 53% -

50

100

150

200

250

300

1Q13 1Q14 1Q15 1Q16F

MBbl/d

Forecasted Avg. Increase from FY2015 to FY2016

~30%

Completed over 70,000 Bbl/d of C2+ fractionation capacity at the Keystone and Sherwood complexes

Approximately 30% forecasted average increase in fractionation volumes from 2015 to 2016

(a) Based on weighted average number of days plant(s) in service

1Q16

thro

ugh

4Q16

Avg

.

-

200

400

600

800

1,000

1,200

1,400

1Q13 1Q14 1Q15 1Q16F

MMcf/d

Gathering & Processing

9

Southwest Processing

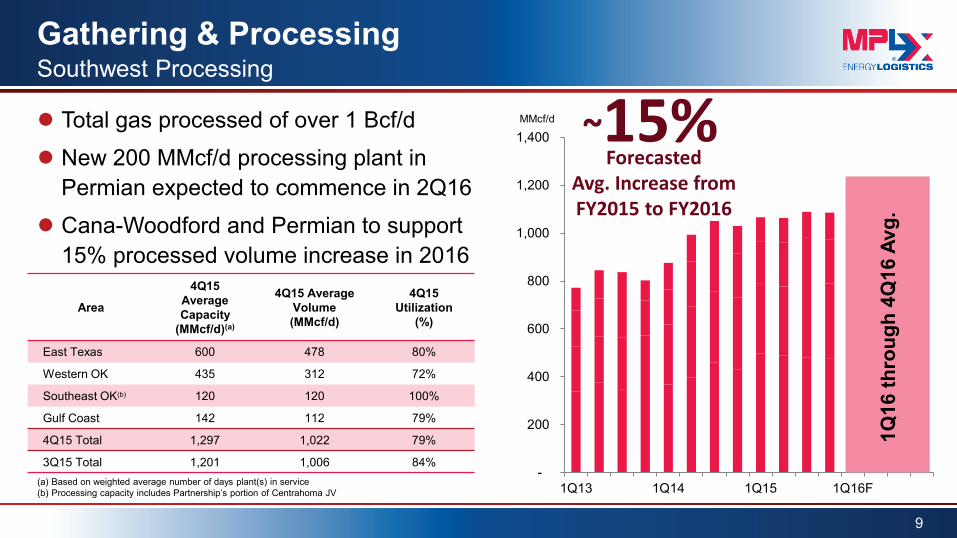

Area

4Q15 Average Capacity

(MMcf/d)(a)

4Q15 Average Volume (MMcf/d)

4Q15 Utilization

(%)

East Texas 600 478 80%

Western OK 435 312 72%

Southeast OK(b) 120 120 100%

Gulf Coast 142 112 79%

4Q15 Total 1,297 1,022 79%

3Q15 Total 1,201 1,006 84%

Total gas processed of over 1 Bcf/d

New 200 MMcf/d processing plant in Permian expected to commence in 2Q16

Cana-Woodford and Permian to support 15% processed volume increase in 2016

~15% Forecasted

Avg. Increase from FY2015 to FY2016

(a) Based on weighted average number of days plant(s) in service (b) Processing capacity includes Partnership’s portion of Centrahoma JV

1Q16

thro

ugh

4Q16

Avg

.

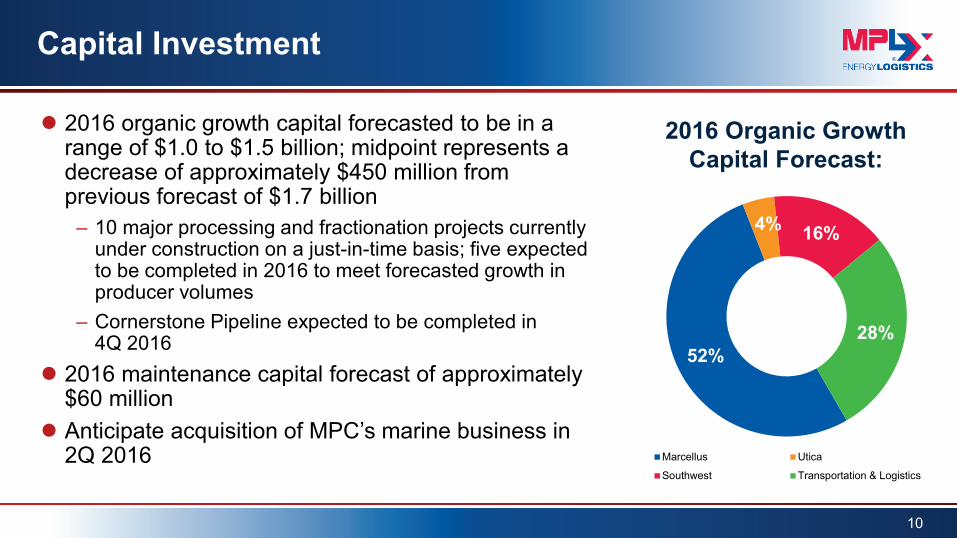

Capital Investment

2016 organic growth capital forecasted to be in a range of $1.0 to $1.5 billion; midpoint represents a decrease of approximately $450 million from previous forecast of $1.7 billion

– 10 major processing and fractionation projects currently under construction on a just-in-time basis; five expected to be completed in 2016 to meet forecasted growth in producer volumes

– Cornerstone Pipeline expected to be completed in 4Q 2016

2016 maintenance capital forecast of approximately $60 million

Anticipate acquisition of MPC’s marine business in 2Q 2016

10

2016 Organic Growth Capital Forecast:

52%

4% 16%

28%

Marcellus Utica

Southwest Transportation & Logistics

42

286

050

100150200250300350

4Q14 4Q15

$MM

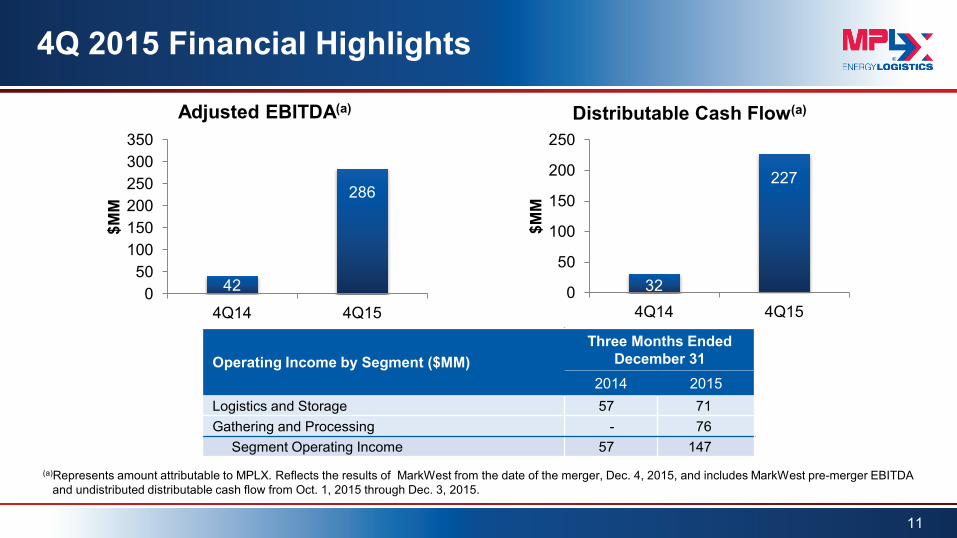

Adjusted EBITDA(a)

4Q 2015 Financial Highlights

11

(a)Represents amount attributable to MPLX. Reflects the results of MarkWest from the date of the merger, Dec. 4, 2015, and includes MarkWest pre-merger EBITDA and undistributed distributable cash flow from Oct. 1, 2015 through Dec. 3, 2015.

32

227

0

50

100

150

200

250

4Q14 4Q15

$MM

Distributable Cash Flow(a)

Operating Income by Segment ($MM) Three Months Ended

December 31 2014 2015

Logistics and Storage 57 71 Gathering and Processing - 76 Segment Operating Income 57 147

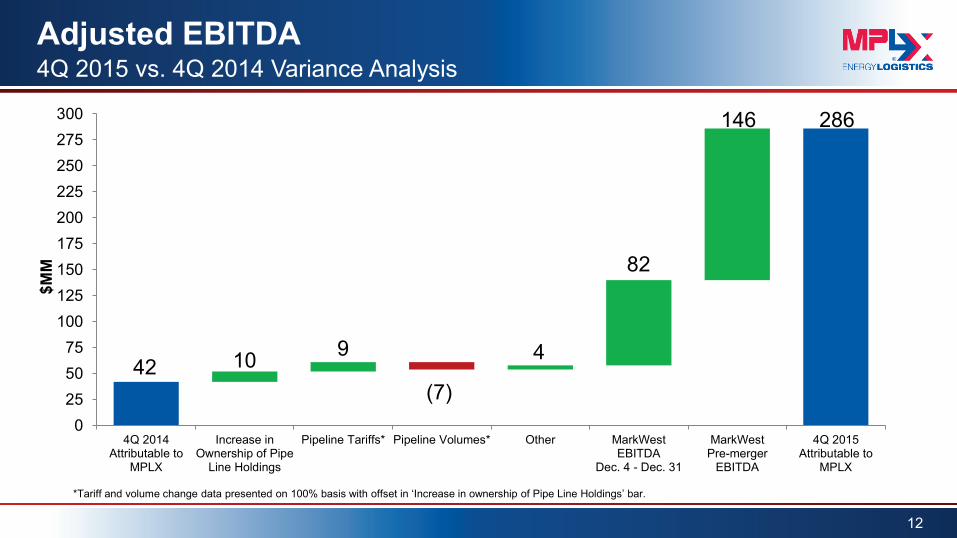

Adjusted EBITDA

12

4Q 2015 vs. 4Q 2014 Variance Analysis

42 10 9

(7)

4

82

146 286

0255075

100125150175200225250275300

4Q 2014Attributable to

MPLX

Increase inOwnership of Pipe

Line Holdings

Pipeline Tariffs* Pipeline Volumes* Other MarkWestEBITDA

Dec. 4 - Dec. 31

MarkWestPre-merger

EBITDA

4Q 2015Attributable to

MPLX

$MM

*Tariff and volume change data presented on 100% basis with offset in ‘Increase in ownership of Pipe Line Holdings’ bar.

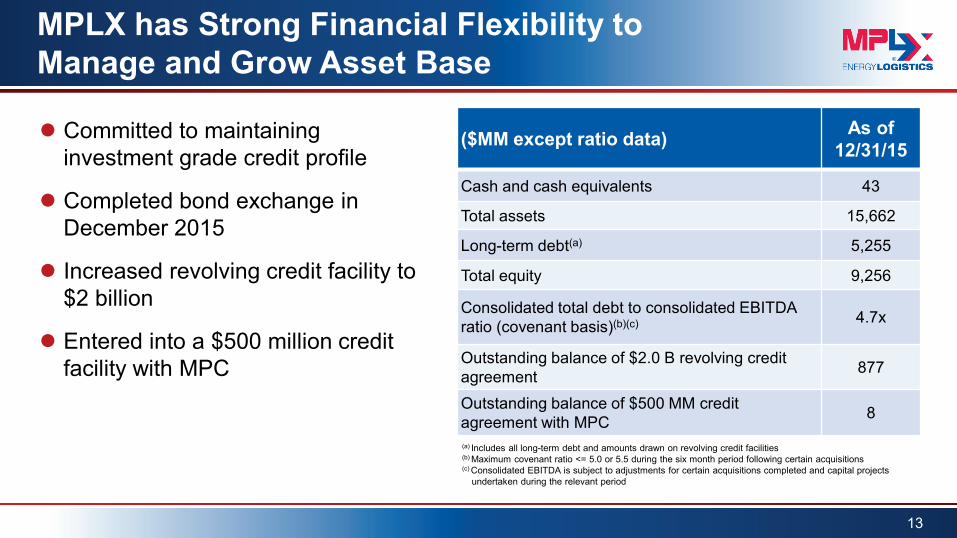

MPLX has Strong Financial Flexibility to Manage and Grow Asset Base

Committed to maintaining investment grade credit profile

Completed bond exchange in December 2015

Increased revolving credit facility to $2 billion

Entered into a $500 million credit facility with MPC

13

($MM except ratio data) As of 12/31/15

Cash and cash equivalents 43

Total assets 15,662

Long-term debt(a) 5,255

Total equity 9,256

Consolidated total debt to consolidated EBITDA ratio (covenant basis)(b)(c) 4.7x

Outstanding balance of $2.0 B revolving credit agreement 877

Outstanding balance of $500 MM credit agreement with MPC 8

(a) Includes all long-term debt and amounts drawn on revolving credit facilities (b) Maximum covenant ratio <= 5.0 or 5.5 during the six month period following certain acquisitions (c) Consolidated EBITDA is subject to adjustments for certain acquisitions completed and capital projects undertaken during the relevant period

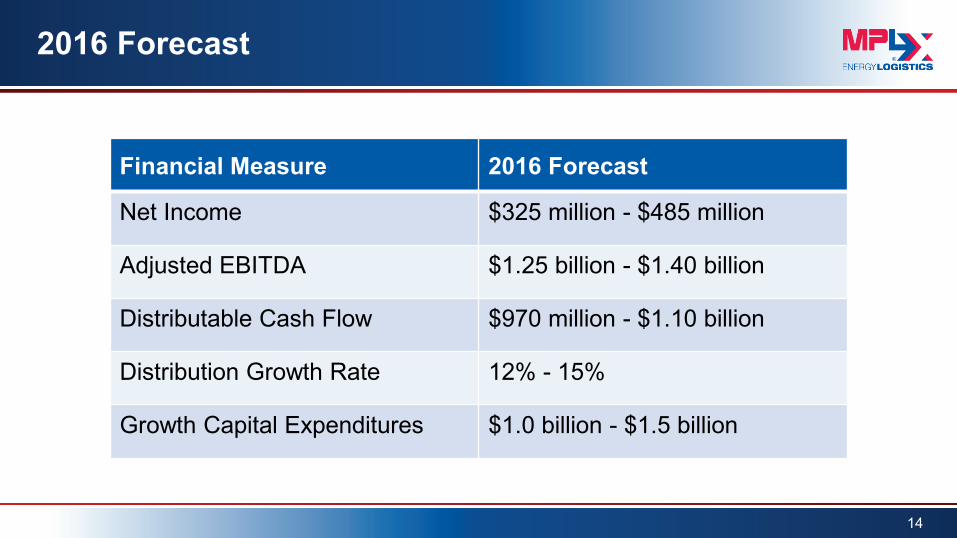

2016 Forecast

14

$X,X

XX-$

X,XX

X

$XXX

-$XX

X

Financial Measure 2016 Forecast

Net Income $325 million - $485 million

Adjusted EBITDA $1.25 billion - $1.40 billion

Distributable Cash Flow $970 million - $1.10 billion

Distribution Growth Rate 12% - 15%

Growth Capital Expenditures $1.0 billion - $1.5 billion

0.2625* (MQD)

0.2725 0.2850 0.2975 0.3125 0.3275 0.3425 0.3575 0.3825 0.4100

0.4400 0.4700

0.5000

0.20

0.25

0.30

0.35

0.40

0.45

0.50

0.55

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

$/U

nit

1.49x 1.37x 1.56x 1.47x 1.20x

Distribution Growth per Unit

*Represents minimum quarter distribution (MQD) for 4Q12, actual $0.1769 equal to MQD prorated

Coverage Ratio 1.36x 1.25x 1.25x 1.38x 1.19x

24% CAGR

0.97x 1.18x

15

1.13x

Forecasted distribution growth of 12% to 15% in 2016

16

Appendix

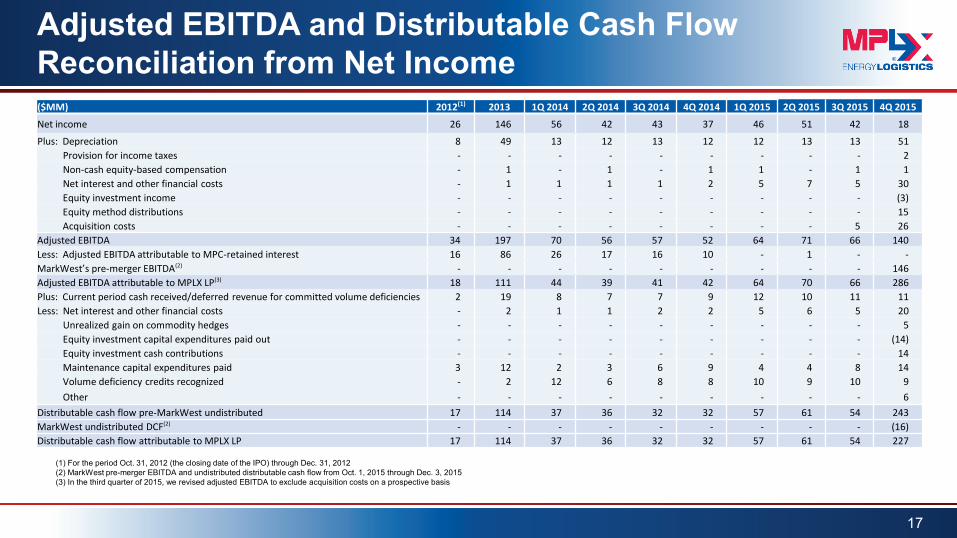

Adjusted EBITDA and Distributable Cash Flow Reconciliation from Net Income

17

(1) For the period Oct. 31, 2012 (the closing date of the IPO) through Dec. 31, 2012 (2) MarkWest pre-merger EBITDA and undistributed distributable cash flow from Oct. 1, 2015 through Dec. 3, 2015 (3) In the third quarter of 2015, we revised adjusted EBITDA to exclude acquisition costs on a prospective basis

($MM) 2012(1) 2013 1Q 2014 2Q 2014 3Q 2014 4Q 2014 1Q 2015 2Q 2015 3Q 2015 4Q 2015

Net income 26 146 56 42 43 37 46 51 42 18

Plus: Depreciation 8 49 13 12 13 12 12 13 13 51 Provision for income taxes - - - - - - - - - 2 Non-cash equity-based compensation - 1 - 1 - 1 1 - 1 1 Net interest and other financial costs - 1 1 1 1 2 5 7 5 30 Equity investment income - - - - - - - - - (3) Equity method distributions - - - - - - - - - 15 Acquisition costs - - - - - - - - 5 26 Adjusted EBITDA 34 197 70 56 57 52 64 71 66 140 Less: Adjusted EBITDA attributable to MPC-retained interest 16 86 26 17 16 10 - 1 - - MarkWest’s pre-merger EBITDA(2) - - - - - - - - - 146 Adjusted EBITDA attributable to MPLX LP(3) 18 111 44 39 41 42 64 70 66 286 Plus: Current period cash received/deferred revenue for committed volume deficiencies 2 19 8 7 7 9 12 10 11 11 Less: Net interest and other financial costs - 2 1 1 2 2 5 6 5 20 Unrealized gain on commodity hedges - - - - - - - - - 5 Equity investment capital expenditures paid out - - - - - - - - - (14) Equity investment cash contributions - - - - - - - - - 14 Maintenance capital expenditures paid 3 12 2 3 6 9 4 4 8 14 Volume deficiency credits recognized - 2 12 6 8 8 10 9 10 9 Other - - - - - - - - - 6 Distributable cash flow pre-MarkWest undistributed 17 114 37 36 32 32 57 61 54 243 MarkWest undistributed DCF(2) - - - - - - - - - (16) Distributable cash flow attributable to MPLX LP 17 114 37 36 32 32 57 61 54 227

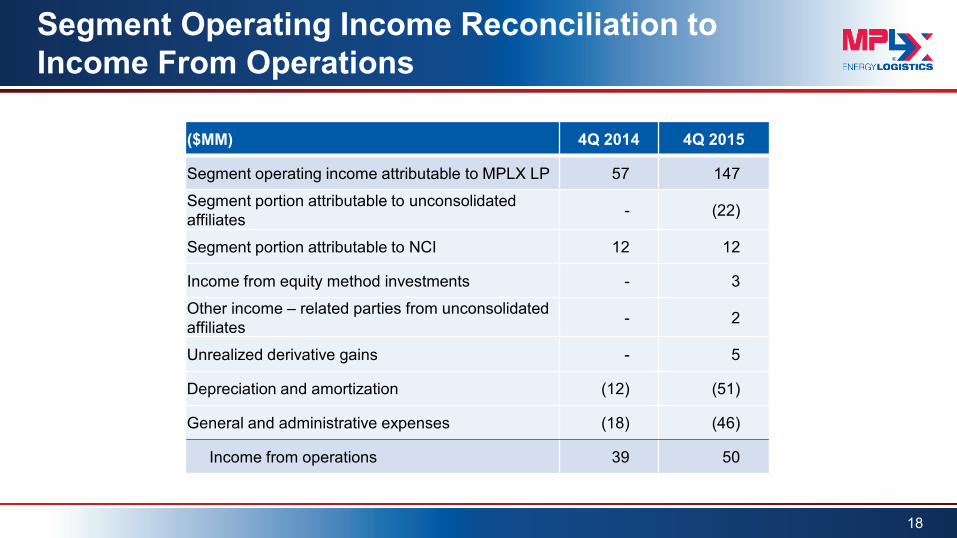

Segment Operating Income Reconciliation to Income From Operations

18

($MM) 4Q 2014 4Q 2015

Segment operating income attributable to MPLX LP 57 147 Segment portion attributable to unconsolidated affiliates - (22)

Segment portion attributable to NCI 12 12

Income from equity method investments - 3

Other income – related parties from unconsolidated affiliates - 2

Unrealized derivative gains - 5

Depreciation and amortization (12) (51)

General and administrative expenses (18) (46)

Income from operations 39 50

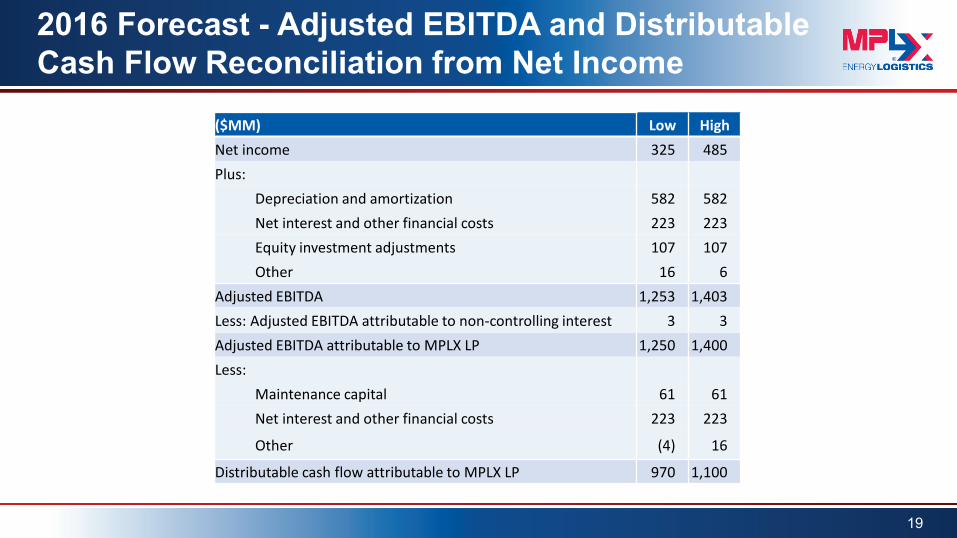

2016 Forecast - Adjusted EBITDA and Distributable Cash Flow Reconciliation from Net Income

19

($MM) Low High Net income 325 485 Plus: Depreciation and amortization 582 582 Net interest and other financial costs 223 223 Equity investment adjustments 107 107 Other 16 6 Adjusted EBITDA 1,253 1,403 Less: Adjusted EBITDA attributable to non-controlling interest 3 3 Adjusted EBITDA attributable to MPLX LP 1,250 1,400 Less: Maintenance capital 61 61 Net interest and other financial costs 223 223

Other (4) 16

Distributable cash flow attributable to MPLX LP 970 1,100

Doddridge

Marshall

Wetzel

Harrison

Noble

Butler

Washington

WEST VIRGINIA

PENNSYLVANIA

OHIO

Washington

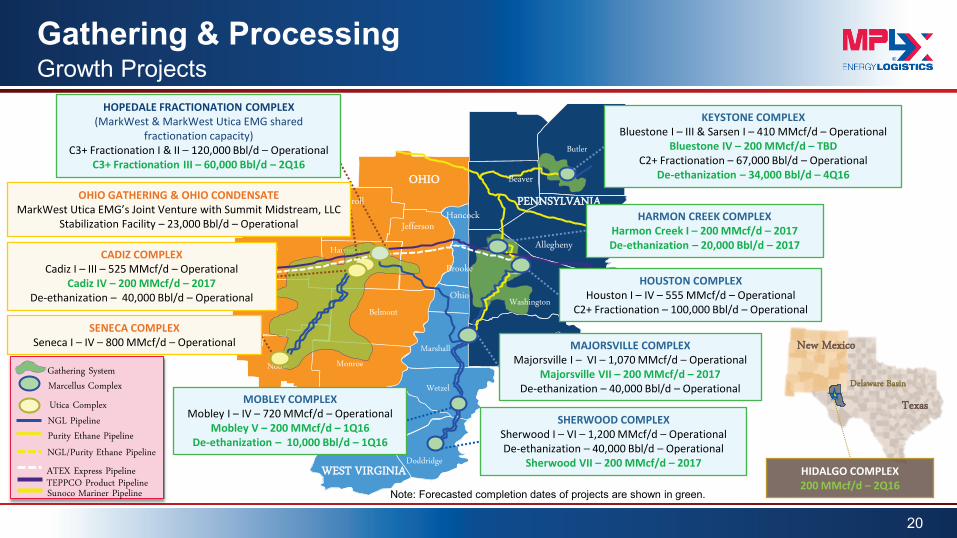

Gathering & Processing

20

Growth Projects

Utica Complex

ATEX Express Pipeline

Purity Ethane Pipeline NGL Pipeline

NGL/Purity Ethane Pipeline

Sunoco Mariner Pipeline

Marcellus Complex Gathering System

TEPPCO Product Pipeline

Belmont

Monroe

Jefferson

Carroll

Tuscarawas

Beaver

Allegheny

Brooke

Hancock

Ohio

Greene

KEYSTONE COMPLEX Bluestone I – III & Sarsen I – 410 MMcf/d – Operational

Bluestone IV – 200 MMcf/d – TBD C2+ Fractionation – 67,000 Bbl/d – Operational

De-ethanization – 34,000 Bbl/d – 4Q16

HARMON CREEK COMPLEX Harmon Creek I – 200 MMcf/d – 2017 De-ethanization – 20,000 Bbl/d – 2017

HOUSTON COMPLEX Houston I – IV – 555 MMcf/d – Operational

C2+ Fractionation – 100,000 Bbl/d – Operational

MAJORSVILLE COMPLEX Majorsville I – VI – 1,070 MMcf/d – Operational

Majorsville VII – 200 MMcf/d – 2017 De-ethanization – 40,000 Bbl/d – Operational

MOBLEY COMPLEX Mobley I – IV – 720 MMcf/d – Operational

Mobley V – 200 MMcf/d – 1Q16 De-ethanization – 10,000 Bbl/d – 1Q16

SHERWOOD COMPLEX Sherwood I – VI – 1,200 MMcf/d – Operational De-ethanization – 40,000 Bbl/d – Operational

Sherwood VII – 200 MMcf/d – 2017

HOPEDALE FRACTIONATION COMPLEX (MarkWest & MarkWest Utica EMG shared

fractionation capacity) C3+ Fractionation I & II – 120,000 Bbl/d – Operational

C3+ Fractionation III – 60,000 Bbl/d – 2Q16

CADIZ COMPLEX Cadiz I – III – 525 MMcf/d – Operational

Cadiz IV – 200 MMcf/d – 2017 De-ethanization – 40,000 Bbl/d – Operational

SENECA COMPLEX Seneca I – IV – 800 MMcf/d – Operational

OHIO GATHERING & OHIO CONDENSATE MarkWest Utica EMG’s Joint Venture with Summit Midstream, LLC

Stabilization Facility – 23,000 Bbl/d – Operational

HIDALGO COMPLEX 200 MMcf/d – 2Q16

Texas

New Mexico

Delaware Basin

Note: Forecasted completion dates of projects are shown in green.

21