gbta bti™ outlook – united states -...

TRANSCRIPT

2013 Q1

2014 Q3

GBTA BTI™ Outlook – United States Prospects for Domestic & International Outbound Business Travel 2014-2015

2012 Q2

2

GBTA BTI™ OUTLOOK – UNITED STATES 2014 Q3

GBTA BTI™ Outlook – United States 2014Q3

GBTA BTI™ Outlook – United States

2014 Q3

GoToMeeting WebEx

CONTACT:

GBTA BTI™ Outlook – United States

3

GBTA BTI™ OUTLOOK – UNITED STATES 2014 Q3

GBTA BTI™ Outlook –United States 2014 Q3

PROSPECTS FOR DOMESTIC & INTERNATIONAL OUTBOUND BUSINESS TRAVEL 2014-2015

Executive Summary

Our forecast for USoriginated business travelis more or less in line withthe expectations in our Q2outlook GBTA BTI™

Outlook – United States, July

2014)

Despite theslight downgrade in ourgrowth forecast for Person Trips for this year, we continue to be optimistic that the U.S. economywill remain on track, producing robust growth in business travel activity through the rest of 2014and into 2015.

As expected, the US economy quickly snapped back from its winter doldrums. GDPgrowth reached 4.6%

Personal consumption increased by 2.5%Investment advanced by 8.4%

Exports expanded by 10.1%Inventories rose by $84 billion in Q2

Many key indicators of business activity are signaling even stronger growth in the second half of2014 and 2015.

both signaling improvingperformance for equipment purchases, hiring, and business travel in the months and quartersahead.

With unemployment falling and GDP growth accelerating, attention has been shifting over to therisk of rising inflation.

Is

Private U.S. Jobs Scorecard

4

GBTA BTI™ OUTLOOK – UNITED STATES 2014 Q3

accelerating inflation an inevitable side effect of years of monetary stimulus?

Overall U.S. economic performance is very much about what the consumer is or is not doing.

Rising sentiment, jobs gains, and slowly advancing wages should spell gatheringstrength for consumer spending and housing activity over the next 18 24 months.

We expect that Group trip volume will decline 3.3% in2014 before rising 1.4% in 2015.

Momentum has been sustained thus far in 2014, evidenced by transient volumegrowth of 3.1% (qtr/qtr annualized) in the first quarter. For 2014 in total, we expect transientvolume to grow 2.3% versus 2013.

we have witnessedmomentum building in IOB business travel since the middle of 2013 and we expect that trend tocontinue through our forecast horizon. International outbound trip volume grew 1.1% in 2013 andwe expect 5.6% growth in 2014 followed by another 6.5% in 2015.

Led by expectations for increasingly higher F&B costs and airfares, we have raised expectations fortravel price increases over last quarter and now expect TPI growth of 2.9% this year and 3.5% in2015.

5

GBTA BTI™ OUTLOOK – UNITED STATES 2014 Q3

U.S. ECONOMIC PERFORMANCE

Current Conditions

As we had anticipated, the USeconomy quickly snappedback from its winterdoldrums. GDPgrowth reached 4.2%

Personal consumptionincreased by 2.5%

Investment advanced by 8.4%

Exports expanded by 10.1%

Inventories rose by $84 billion in Q2

JOBS

September brought another encouraging month of job growth.

Net JobGains(x1000)

2012 2013 2014

Total 2,294 2,365 1,983

Shading Key:

Job Loss 0 150k150200k

GT 200k

Private U.S. Jobs Scorecard

8

6

4

2

0

2

4

6

GDPGrowthin%

Q2 GDP Growth Snaps Back fromWeather Related Hiccup

Yr/Yr % Qtr/Qtr Annualized

Source: Bureau of Economic Analysis

Yr/Yr: 2014Q2 @ 2.5%

Qtr/Qtr: 2014Q2 @ 4.2%

6

GBTA BTI™ OUTLOOK – UNITED STATES 2014 Q3

During the current recovery, a commoncomplaint is that we are creating jobs, justnot high “quality” ones quality beingdefined as higher paying jobs.

GBTA BTI™ Outlook –United States,

BUSINESS PERFORMANCE INDICTORS

Many key indicators ofbusiness confidence aresignaling even strongergrowth in the secondhalf of 2014 and 2015.

The bottom line is that both

30

35

40

45

50

55

60

65

80

82

84

86

88

90

92

94

96

98

100 PurchasingManagersIndexGT50IndicatesExpansion

NFIBOptimismIndex1986=100

Rising Business Confidence Across the Board…

NFIB Business Optimism Index ISM's PMI

NFIB July 2014 @ 95.7

ISM Aug 2014@ 59.0

Source: National Federation of Independent Business, Institute for Supply Management

7

GBTA BTI™ OUTLOOK – UNITED STATES 2014 Q3

are signaling improving performance for equipment purchases, hiring, and business travel in the monthsand quarters ahead.

Yet another indicator of rising business optimismcomes from the Wells Fargo/Gallop SmallBusiness Index.

Monitoring the “dark” side of business health canalso lend insight into current and futureconditions.

EXPORTS

As mentioned earlier, exports added nicely toQ2 GDP growth, something that analysts hadbeen hoping for.

10,000

20,000

30,000

40,000

50,000

60,000

#ofCompaniesperQuarter

Declining Bankruptcies Suggest Healthier Biz Environment

Source: Administrative Office of the U.S. Courts

2014Q2 @ 30,113

20 yr Average

15%

10%

5%

0%

5%

10%

15%

20%

25%

30%

Yr/Yr%

U.S. Exports to the European Union Gathering

Steam

Source: U.S. Census Bureau

June 2014 @ 7.8%

8

GBTA BTI™ OUTLOOK – UNITED STATES 2014 Q3

.

Coupling themathematical relationship with the consensus outlook for exports suggests rising strength in U.S. IOB

INFLATION

With unemployment fallingand GDP growthaccelerating, attention hasbeen shifting over to the riskof rising inflation, however.

Is accelerating inflation aninevitable side effect of years of monetary stimulus?

3

2

1

0

1

2

3

4

5

6

Yr/Yr%ChangeinPrices

Inflation Currently at Fed Target But is Acceleration Ahead?

Consumer Price Index All Items Core Inflation (less food & energy)

CPI June 2014 @2.1%

Core June 2014 @ 1.9%

Source: Bureau of Labor Statistics

9

GBTA BTI™ OUTLOOK – UNITED STATES 2014 Q3

Why the confidence that the economy cancontinue to absorb this monetarystimulus with acceptable levels ofinflation?

From a demand sideperspective, consumer and businessspending has been on the sluggish sidesince the early days of the recovery.

“demand pull” inflationdeterminants are currently quite mild by historical standards

Employment Cost Index

With labor comprising upwardsof 50% of business costs, year on year change of 2.5% in the ECI suggests favorable inflation conditions ahead.

Commodity pricesacross the board have been moving sideways or actually declining

70

120

170

220

2005=100

Commodity Prices Have Been Flat to Down

Since mid 2011

All Commodities Metals Energy

Source: International Monetary Fund

20%

15%

10%

5%

0%

5%

10%

15%

20%

25%

Yr/Yr%Change

Import Prices Have Also Been Favorable...

July 2014 @ 0.8%

Source: U.S. Bureau of Labor Statistics

10

GBTA BTI™ OUTLOOK – UNITED STATES 2014 Q3

CONSUMERS

Overall U.S. economic performance isvery much about what the consumer isor is not doing.

Retail saleshave recently re accelerated, albeitmoderately, following the weather relatedslowdown of the first quarter.

15

10

5

0

5

10Retail Sales Re Accelerates After Winter Freeze

July 2014 @ 3.7%

Source: US Census Bureau

Yr/Yr in %

But recent growth has been

fueled more by borrowing than

rising income…

250

350

450

550

650

750

850

950

3,000

3,500

4,000

4,500

5,000

5,500

6,000Housing Market Improving But Still A Long Way to Go

Existing Home Sales (left)

Source: US Census Bureau

New Home Sales (right)

in thousands of units

6

8

10

12

14

16

18

20Vehicle Sales Already Past Previous Peak

Aug 2014 @17.5 million

Source: Autodata Corp

in millions of units

11

GBTA BTI™ OUTLOOK – UNITED STATES 2014 Q3

Economic Outlook

With the hangover from the winter doldrums over and underlying economic momentum breaking throughthe clouds, the U.S. economy is back on track to register solid gains in 2014, with even better performancenext year.

Households and businesses are feeling better about the near term future and their spending behavior willbegin to reflect that optimism.

Meanwhile, inflation will slowly yield to rising pressure from wages, falling productivity, and othermaterial cost gains.

Corporate profit growthwill begin to slow in the coming quarters.

2014 Q3 U.S. Economic Forecast for 2014-2015

Source: IMF, Wells Fargo Securities, Moodys Analytics, OECD, Rockport Analytics

Economic Driver 2011 2012 2013 2014 2015 Real GDP (Yr-to-Yr %) 1.8 2.2 1.9 2.3 3.4

Inflation (CPI) (Yr-to-Yr %) 3.1 2.1 1.5 2.1 2.5

Consumption (Yr-to-Yr %) 2.5 1.9 2.0 2.8 3.1

Equipment Investment (Yr-to-Yr %) 11.0 6.9 3.1 5.6 6.3

Real Exports (Yr-to-Yr %) 6.7 3.4 2.7 3.7 6.8

Corporate Profits Pre-Tax (Yr-to-Yr %) 7.3 6.8 4.6 2.6 5.9

Total Employment (x1000) Avg. Jobs/mo 175.3 182.8 194 227 223

12

GBTA BTI™ OUTLOOK – UNITED STATES 2014 Q3

U.S. Economic Driver of Business Travel –Latest Performance

Indicator Relationship

with Biz Travel Latest Value

Expected for 2014

Progress Versus Last Qtr

Real GDP (Yr/Yr%)

Positive –rising tide lifts all boats

+4.6% (2014 Q2)

+2.3% Better

Corporate Profits Before Tax

Positive financial & sentiment indicator -0.3%

(2014Q2) +2.6%

Slightly Worse

Job Growth (monthly nonfarm payroll gain)

Positive - more jobs indicates greater confidence, rising incomes, and more travelers

+248,000

(Sep’14)

+227,000/

Monthly Avg

Better

Unemployment Rate

Negative economic & sentiment indicator

5.9% (Sep’14)

6.2% Slightly Better

Oil Prices (Brent Crude)

Negative for prices & spending

$106.98/bbl (July ‘14)

$108.6/bbl Better

Real Exports

Positive for Int’l Outbound

+10.1% (2014Q2)

3.7% Better

CPI for: Air Fare Rental Cars Lodging

Negative for travel prices

-0.2% (Jul’14) 2.8% (Jul’14) 3.1% (Jul ’14)

4.0% 1.2% 4.1%

Slightly Better

ISM Sentiment Index (PMI-Mfg)

Positive for travel & hiring

59.0 (Aug ’14)

59.2 Better

13

GBTA BTI™ OUTLOOK – UNITED STATES 2014 Q3

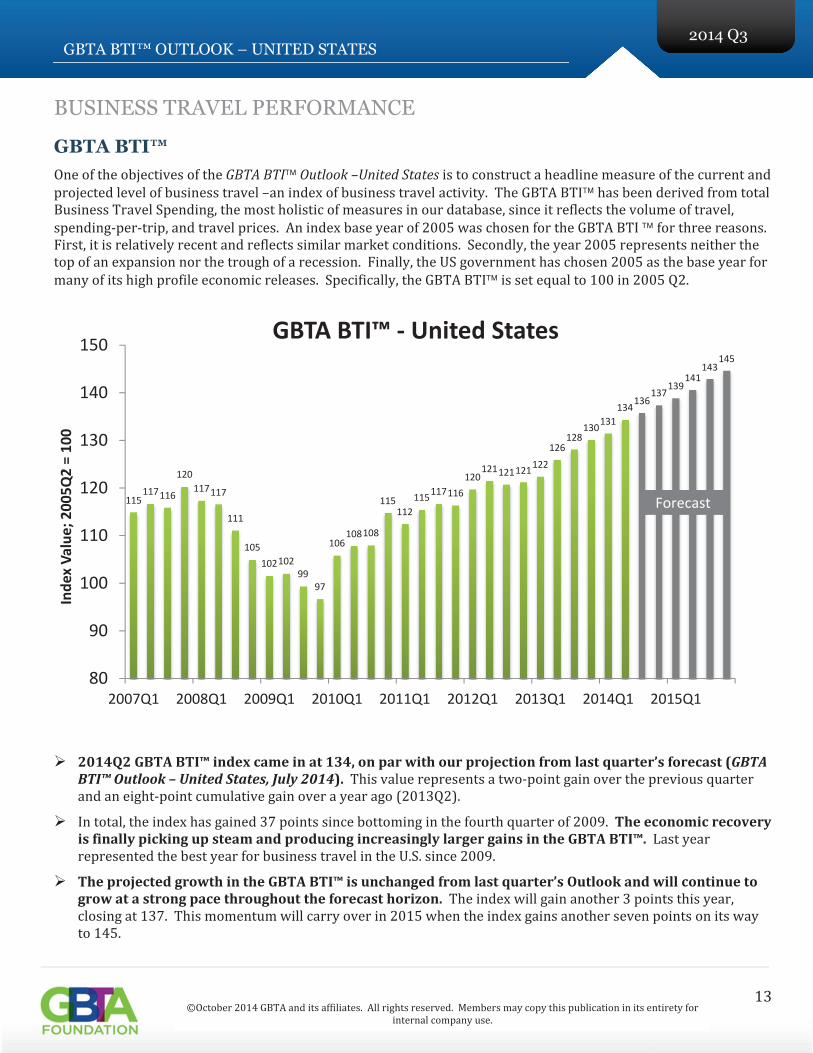

BUSINESS TRAVEL PERFORMANCE

GBTA BTI™

GBTA BTI Outlook –United States

2014Q2 GBTA BTI™ index came in at 134, on par with our projection from last quarter’s forecast (GBTABTI™ Outlook – United States, July 2014).

The economic recoveryis finally picking up steam and producing increasingly larger gains in the GBTA BTI™.

The projected growth in the GBTA BTI™ is unchanged from last quarter’s Outlook and will continue togrow at a strong pace throughout the forecast horizon.

115117116

120

117117

111

105

102102

99

97

106108108

115112

115117116

120121121121

122

126128

130131

134136

137139

141143

145

80

90

100

110

120

130

140

150

2007Q1 2008Q1 2009Q1 2010Q1 2011Q1 2012Q1 2013Q1 2014Q1 2015Q1

IndexValue;2005Q2=100

GBTA BTI™ United States

Forecast

14

GBTA BTI™ OUTLOOK – UNITED STATES 2014 Q3

BUSINESS TRAVEL QUARTERLY OUTLOOK DETAILS

Total U.S.-Originated Business Travel Spending & Trip Volumes3

GBTA BTI™ Outlook – United States, July 2014)

Group Meeting & Convention vs. Transient Business Travel

$65.0

$70.0

$75.0

$80.0

114

116

118

120

122

124

126

TotalSpending(BillionsUSD)

TotalPersonTripVolume(millions)

BT Forecast Comparisons: 2014 Q2 vs. 2014 Q3

Total Person Trips (Q2 Outlook) Total Person Trips (Q3 Outlook)

Total Spending (Q2 Outlook) Total Spending (Q3 Outlook)

15

GBTA BTI™ OUTLOOK – UNITED STATES 2014 Q3

American Express Meetings &

Events 2014 Global

Meetings Forecast,

International Outbound Business Travel

80

90

100

110

120

130

140

0

50

100

150

200

250

300

350

2010 2011 2012 2013 2014 2015

TotalSpending(billionsUSD)

PersonTrips(millionsUSD)

Group & Transient Business Travel: Person Trips &

Spending

Transient Person Trips Group Person Trips

Transient Spend Group Spend

Forecast

16

GBTA BTI™ OUTLOOK – UNITED STATES 2014 Q3

U.S. Business Travel Inflation

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

2010Q1 2011Q1 2012Q1 2013Q1 2014Q1 2015Q1

YroverYrPercent

Travel Price Inflation

Forecast

Source: US Bureau Labor Statistics, Rockport Analytics

6.5

7

7.5

8

8.5

9

9.5

10

10.5

1.5

1.55

1.6

1.65

1.7

1.75

1.8

1.85

1.9

1.95

2

2010Q1 2011Q1 2012Q1 2013Q1 2014Q1 2015Q1

Spending(BillionsUSD)

TripVolume(Millions)

International Business Travel from The U.S.

International Person Trips

International Spend

Source: U.S. Department of Commerce (OTTI), GBTA Foundation, Rockport Analytics

Forecast

17

GBTA BTI™ OUTLOOK – UNITED STATES 2014 Q3

Air

18%

Food

20%

Ground

9%

Lodging

22%

Rental Cars

6%

Other

25%

TPI Components and 2014 Inflation

ExpectationsColor Indicates Direction of Change in Estimate from Last Quarter:

red=falling, green=rising, grey=no change

+1.9%+2.4%

+2.4%+2.2%

+5.0%+0.8%

Source: Rockport Analytics, Moody's, DKSA

$535.5

$564.0$576.4 $575.4

$613.1

$638.1

1%

0%

1%

2%

3%

4%

5%

6%

7%

$480

$500

$520

$540

$560

$580

$600

$620

$640

$660

2010 2011 2012 2013 2014 2015

%Change

SpendperTrip($USD)

Growth In Business Travel Spend: More than Just Travel Price

Inflation

Spend per trip (left) Spend Per Trip Growth (right) Travel Price Inflation (right)

2.6%

1.2%

0.3%

1.4%3.6%

Source: GBTA Foundation, Rockport Analytics

0.6%

18

GBTA BTI™ OUTLOOK – UNITED STATES 2014 Q3

Forecast Tables 2014 Q3: Annual & Quarterly†

19

GBTA BTI™ OUTLOOK – UNITED STATES 2014 Q3