help! i’m drowning in debt. february 18, 2008 the university of texas medical school at houston...

TRANSCRIPT

HELP! I’m Drowning in Debt.

February 18, 2008The University of Texas Medical School at Houston

Presented by: James W. PrescottAssociate Administrator

Texas Medical Association Insurance Trust

Today’s Goals

Keep it clean and simple. Help you understand time honored truths

about money. Give you an action plan and details so you

can do what needs to be done.

Debt in the USA

2006 – 6 billion new credit card offers. 2006 - $807 billion in credit card debt in the

US. – CardTrack. 75% of Forbes 400 say the best way to build

wealth is to become and stay debt free. Sears makes more money on credit than

sales of merchandise. Debt Free Companies – Walgreens, Cisco,

Microsoft, and Harley-Davidson.

Debt in the USA

70% of Americans live paycheck to paycheck – Wall Street Journal.

80% of Americans have credit card debt - Wall Street Journal.

Truth Number 1

If you can control the person in the mirror, you can be skinny and rich.

Truth Number 2

I’m not your answer and other financial counselors aren’t your answer. YOU are the answer.

Truth Number 3

Personal finance is 80% behavior.

Truth Number 4

What to do isn’t the problem. Doing it is.

Truth Number 5

If you will live like no one else now, later you can live like no one else.

Truth Number 6

If you’ll make sacrifices now that most people aren’t willing to make, later you will be able to live lives as those folks will never be able to live. As physicians, you can do this exponentially.

Truth Number 7

The biggest financial difference between a retired physician and a retired carpenter is the size of the house they live in.

Truth Number 8

Live on less than you make and only spend when you have the cash.

Myths vs. Truths

Myth - debt consolidation saves interest and you have a smaller payment.

Truth - debt consolidation is dangerous because you treat only the symptom. 78% of the time the debt grows back. Why? No game plan and no savings for unexpected events.

Myths vs. Truth

Myth – Debt is a tool. Truth – Debt is NOT a tool.

Hurdles

Denial Ignorance Keeping up with the Joneses

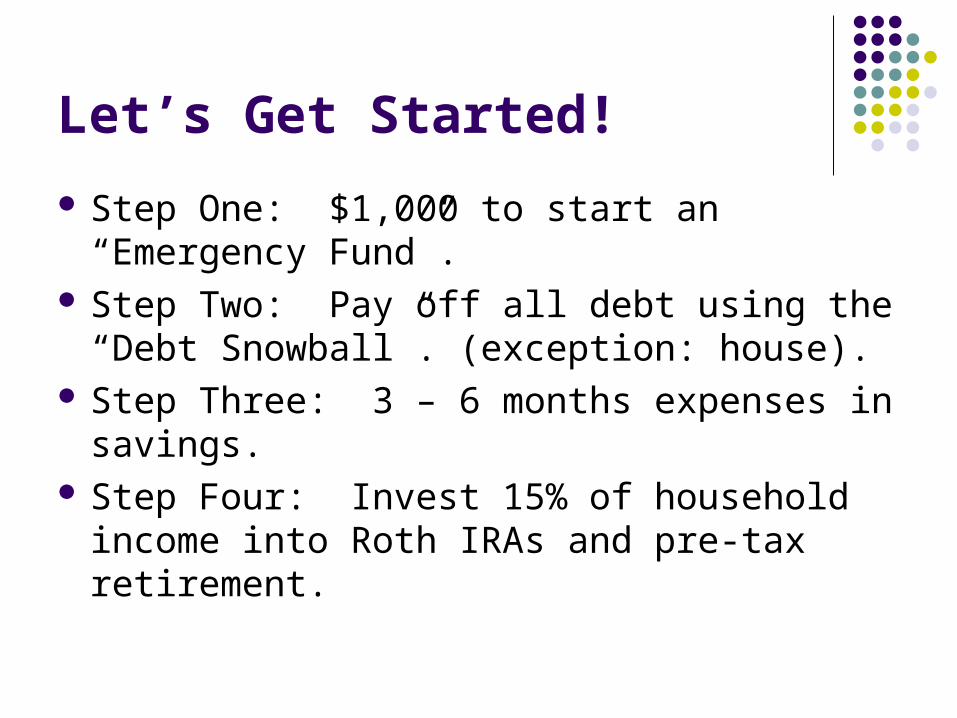

Let’s Get Started!

Step One: $1,000 to start an “Emergency Fund”.

Step Two: Pay off all debt using the “Debt Snowball”. (exception: house).

Step Three: 3 – 6 months expenses in savings.

Step Four: Invest 15% of household income into Roth IRAs and pre-tax retirement.

Let’s Get Started!

Step Five: College Funding. Step Six: Pay off home early. Step Seven: Build wealth and give!

(Mutual Funds/Real Estate)

How Much Do We Invest? (After You Are Debt Free and Have an emergency Fund)

Household income X 15% = Annual Investment Goal

How Much Do We Invest?

What Buckets Do I Put My Money In?#1 – Max your match on your employer sponsored

plan. (tax advantage for today)

#2 – Fully fund your Roth IRA. (tax advantage for the future)

#3 – Go back to your employer sponsored plan. (tax advantage for today)

How Much Do We Invest?

What Do I Invest The Money In? Aggressive Growth Growth Growth & Income Balanced International Bonds

How Much Do We Invest?

How Do Investment Professionals Get Paid? Classes of shares (Flavors) (One Fund Family) “A” – 5.75% - .75% - X “B” – X – 1.75% - 7% to 1% “C” – 1% - 2.25% - 1% Fee based accounts (multiple fund families) 1% -

3%.

Types of Accounts – Employer Retirement Accounts (Qualified)

What are the rules?#1 – Govt. tells us what the max contribution is.

#2 – Govt. tells us when we can take it out.

#3 - Govt. tells us when we have to start taking it out.

Types of Accounts – Employer Retirement Accounts (Qualified)

So, what are the benefits?#1 - Employer match is free money to you.

#2 - Tax on employee contributions is deferred until distribution.

#3 - Investment gains are not taxed until distribution.

How are the assets treated when you take them out?

Types of Accounts – Taxable – Non Qualified

Emergency Fund (Money Market)

Types of Accounts – Self Directed Retirement Accounts - Qualified

Traditional IRA – What are the rules?#1 – Govt. tells us what the max contribution is.

#2 – Govt. tells us when we can take it out.

#3 – Govt. tells us when we have to start taking it out.

Types of Accounts – Self Directed Retirement Accounts - Qualified

Traditional IRA – What are the benefits?#1 – You get to choose where to invest your money.

#2 – Contributions are tax deductible now.

How are the assets treated when you take them out of the bucket?

Types of Accounts – Self Directed Retirement Accounts - Qualified

Roth IRA – What are the rules?#1 – Govt. tells us what the max contribution is.

#2 – Govt. tells us when we can take it out.

#3 – Required Minimum Distribution? Not until death of the owner.

Types of Accounts – Self Directed Retirement Accounts - Qualified

Roth IRA – What are the benefits? How are the assets treated when you take

them out of the bucket? Its like paying taxes on the seed but not the

bumper crop.

Major Components of a Healthy Financial Plan

Written cash flow plan. Will and/or estate plan. Debt reduction plan. Tax reduction plan. Emergency funding. Retirement funding. College funding.

Major Components of a Healthy Financial Plan

Charitable giving. Teach my children. Life insurance. Health insurance. Disability insurance. Auto insurance. Homeowners insurance. Professional liability insurance and other business

insurance.

Handouts

Basic Quickie Budget Monthly Cash Flow Plan

THANK YOU!

Q & A