introductory quiz - transtutors · web viewportfolio management - active and passive strategies...

TRANSCRIPT

INVESTMENT AND FUND MANAGEMENTMODULE HANDBOOK

2010/11SEMESTER 2

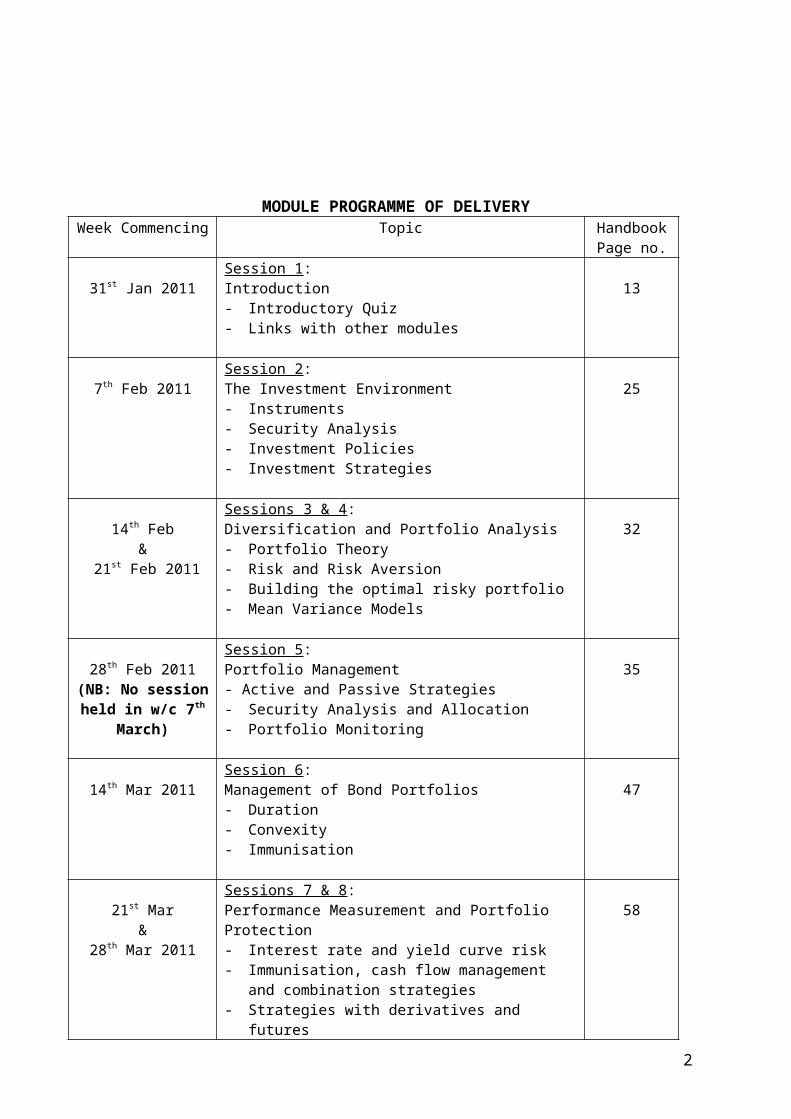

MODULE PROGRAMME OF DELIVERYWeek

CommencingTopic Handbook

Page no.

31st Jan 2011Session 1:Introduction- Introductory Quiz- Links with other modules

13

7th Feb 2011Session 2:The Investment Environment- Instruments- Security Analysis- Investment Policies - Investment Strategies

25

14th Feb &

21st Feb 2011

Sessions 3 & 4:Diversification and Portfolio Analysis- Portfolio Theory- Risk and Risk Aversion- Building the optimal risky portfolio- Mean Variance Models

32

28th Feb 2011 (NB: No session held in w/c 7th

March)

Session 5:Portfolio Management- Active and Passive Strategies- Security Analysis and Allocation- Portfolio Monitoring

35

14th Mar 2011Session 6:Management of Bond Portfolios- Duration- Convexity- Immunisation

47

21st Mar &

28th Mar 2011

Sessions 7 & 8:Performance Measurement and Portfolio Protection- Interest rate and yield curve risk- Immunisation, cash flow management and

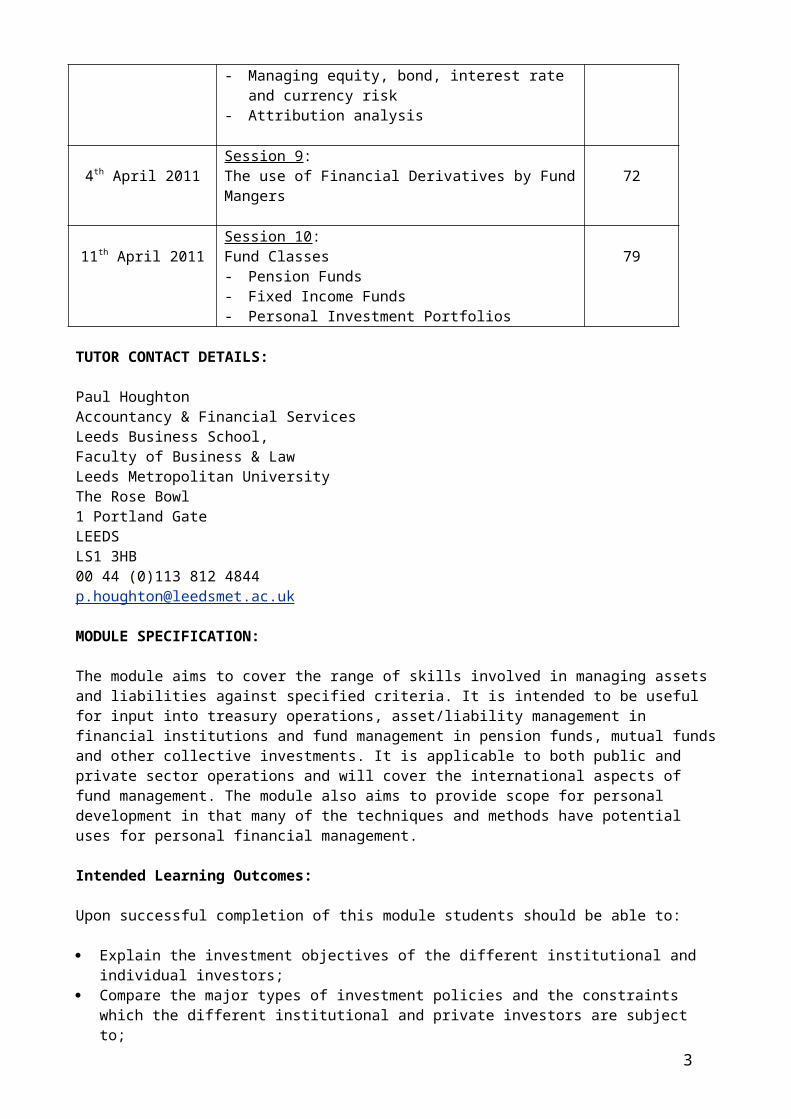

combination strategies- Strategies with derivatives and futures- Managing equity, bond, interest rate and

currency risk- Attribution analysis

58

4th April 2011Session 9:The use of Financial Derivatives by Fund Mangers

72

11th April 2011 Session 10:Fund Classes- Pension Funds- Fixed Income Funds- Personal Investment Portfolios

79

TUTOR CONTACT DETAILS:2

Paul HoughtonAccountancy & Financial ServicesLeeds Business School,Faculty of Business & LawLeeds Metropolitan UniversityThe Rose Bowl1 Portland GateLEEDSLS1 3HB00 44 (0)113 812 [email protected]

MODULE SPECIFICATION:

The module aims to cover the range of skills involved in managing assets and liabilities against specified criteria. It is intended to be useful for input into treasury operations, asset/liability management in financial institutions and fund management in pension funds, mutual funds and other collective investments. It is applicable to both public and private sector operations and will cover the international aspects of fund management. The module also aims to provide scope for personal development in that many of the techniques and methods have potential uses for personal financial management.

Intended Learning Outcomes:

Upon successful completion of this module students should be able to:

Explain the investment objectives of the different institutional and individual investors;

Compare the major types of investment policies and the constraints which the different institutional and private investors are subject to;

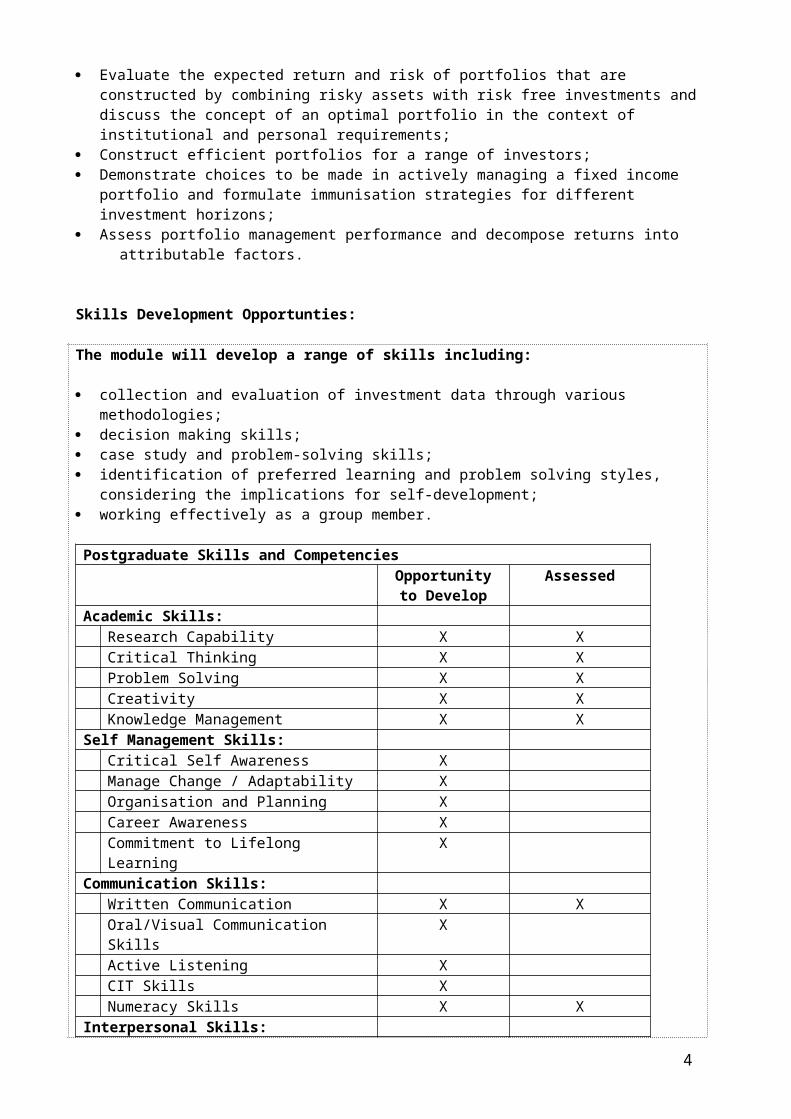

Evaluate the expected return and risk of portfolios that are constructed by combining risky assets with risk free investments and discuss the concept of an optimal portfolio in the context of institutional and personal requirements;

Construct efficient portfolios for a range of investors; Demonstrate choices to be made in actively managing a fixed income portfolio and

formulate immunisation strategies for different investment horizons; Assess portfolio management performance and decompose returns into attributable factors.

Skills Development Opportunties:

The module will develop a range of skills including:

collection and evaluation of investment data through various methodologies; decision making skills; case study and problem-solving skills; identification of preferred learning and problem solving styles, considering the

implications for self-development; working effectively as a group member.

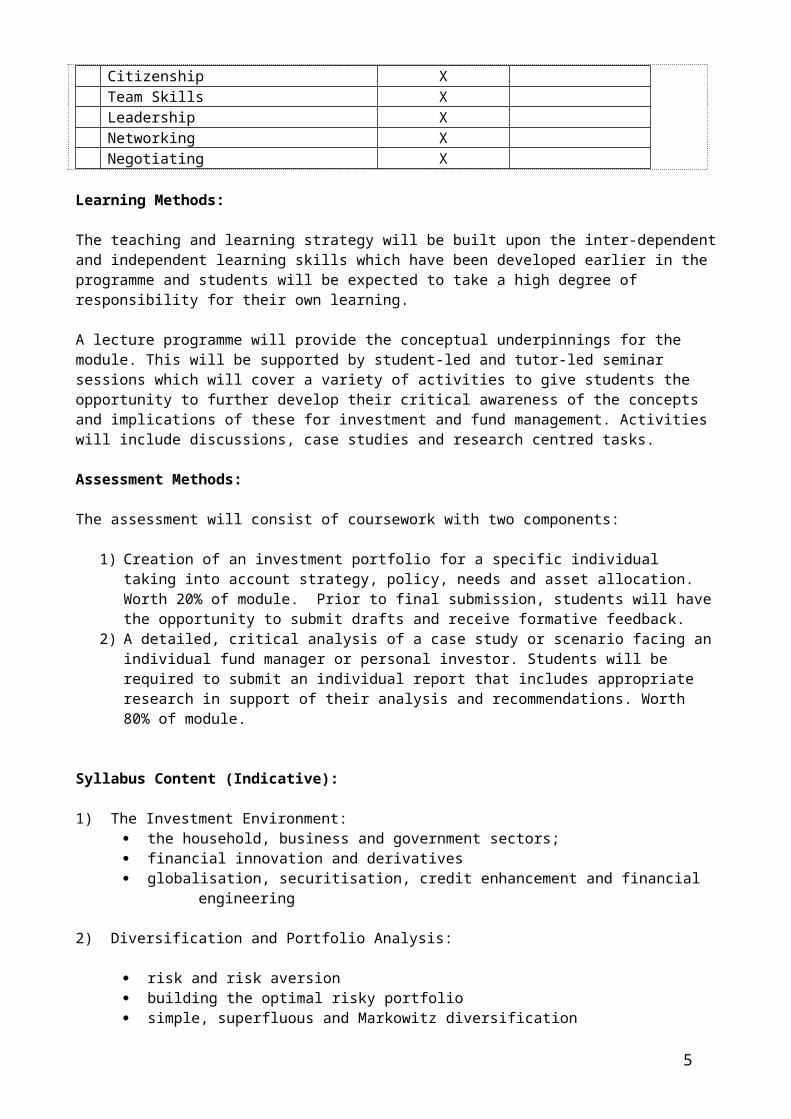

Postgraduate Skills and CompetenciesOpportunity to Develop

Assessed

Academic Skills:

3

Research Capability X XCritical Thinking X XProblem Solving X XCreativity X XKnowledge Management X X

Self Management Skills:Critical Self Awareness XManage Change / Adaptability XOrganisation and Planning XCareer Awareness XCommitment to Lifelong Learning X

Communication Skills:Written Communication X XOral/Visual Communication Skills XActive Listening XCIT Skills XNumeracy Skills X X

Interpersonal Skills:Citizenship XTeam Skills XLeadership XNetworking XNegotiating X

Learning Methods:

The teaching and learning strategy will be built upon the inter-dependent and independent learning skills which have been developed earlier in the programme and students will be expected to take a high degree of responsibility for their own learning.

A lecture programme will provide the conceptual underpinnings for the module. This will be supported by student-led and tutor-led seminar sessions which will cover a variety of activities to give students the opportunity to further develop their critical awareness of the concepts and implications of these for investment and fund management. Activities will include discussions, case studies and research centred tasks.

Assessment Methods:

The assessment will consist of coursework with two components:

1) Creation of an investment portfolio for a specific individual taking into account strategy, policy, needs and asset allocation. Worth 20% of module. Prior to final submission, students will have the opportunity to submit drafts and receive formative feedback.

2) A detailed, critical analysis of a case study or scenario facing an individual fund manager or personal investor. Students will be required to submit an individual report that includes appropriate research in support of their analysis and recommendations. Worth 80% of module.

Syllabus Content (Indicative):

1) The Investment Environment: the household, business and government sectors; financial innovation and derivatives

4

globalisation, securitisation, credit enhancement and financial engineering

2) Diversification and Portfolio Analysis:

risk and risk aversion building the optimal risky portfolio simple, superfluous and Markowitz diversification

3) Portfolio Management - practical applications:

active and passive strategies security analysis and allocation forecasting market movements portfolio monitoring

4) Performance Measurement and Portfolio Protection:

interest rate and yield curve risk immunisation, cash flow management and combination strategies strategies with derivatives and futures managing equity, bond, interest rate and currency risk attribution analysis

5) Fund Classes:

Pension Funds Fixed Income Funds Personal Investment Portfolios International Funds

ACTUAL ASSESSMENT:

The assessment for this module comprises two in-course assignments as follows:

Part A - an individual assignment to be submitted by Wednesday, 16th March 2011 (counts for 20% of total mark) (to be handed in to Reception, Rose Bowl, by 12 noon).

Part B – an individual assignment to be submitted by Tuesday, 3rd May 2011 (counts for 80% of total mark) (max of 3000 words) (to be handed in to Reception, Rose Bowl, by 12 noon)

RECOMMENDED TEXTS FOR BACKGROUND READING:

1) Main Text:

Reilly, F.K. & Brown, K.C. (2009)

Analysis of Investments and Management of Portfolios (International Edition) 9th Edition, Thompson (South Western – Cengage Learning) (ISBN: 0324658427)

5

2) Other Texts for Background Reading:

Bierman, H Jr (2006)

The Bare Essentials of Investing: Teaching the Horse to Talk, World Scientific Publishing (ISBN: 109812705406)

Boakes, B (2010) Reading and Understanding the FINANCIAL TIMES (update for 2010-2011), Prentice Hall (FT) (ISBN: 9780273731818)

Bodie, Z., Kane, A., & Marcus, AJ (2006)

Essentials of Investments McGraw Hill (London) (ISBN: 0071254455)

Campbell, J.Y. & Vicera, L.M. (2002)

Strategic Asset Allocation: portfolio choice for long-term investors Oxford University Press (ISBN: 0198296940)

Cuthbertson, K & Nitzsche, D (2008)

Investments 2nd Edition (Cass Business School), Wiley(ISBN: 9780470519561)

Elton, E.J, (2003) Modern Portfolio Theory and Investment Analysis 6th Edition, Wiley (ISBN: 0471238546)

Jones, C.P. (2007) Investments: Analysis & Management 10th Edition, Wiley (ISBN: 047004781X)

Litterman, B. (2003)

Modern Investment Management; an equilibrium approach John Wiley (ISBN: 0471124109)

Pilbeam, K (2005) Finance & Financial Markets 2nd Edition, Palgrave Macmillan (ISBN: 9781403948359)

Redhead, K. (2003) Introducing Investments: a personal finance approach FT Prentice Hall (ISBN: 027367305X)

3) Appropriate journal articles and relevant websites.

SEMINAR WORK

Session 1:

Introductory Quiz (Page 14)Presentations on:

Shareholder Value Analysis EMH CAPM

Session 2: 6

Group Discussion (page 27)

Exercises;

a) Imagine that your favourite aunt has just been advised to invest all her money in the following unit trusts:

Investec UK Smaller Companies Standard Life UK Equity High Income Artemis UK Special Situations Morgan Stanley Emerging Markets Debt Gartmore UK Focus

She is totally confused – advise her.

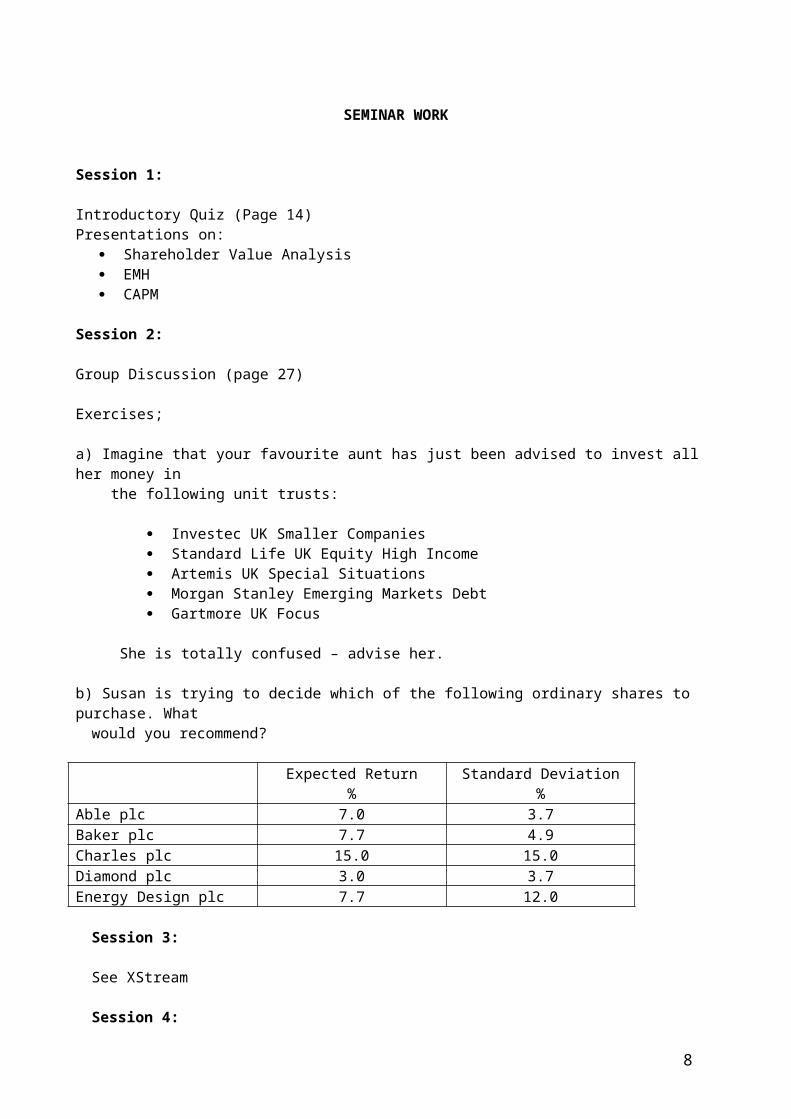

b) Susan is trying to decide which of the following ordinary shares to purchase. What would you recommend?

Expected Return%

Standard Deviation%

Able plc 7.0 3.7Baker plc 7.7 4.9Charles plc 15.0 15.0Diamond plc 3.0 3.7Energy Design plc 7.7 12.0

Session 3:

See XStream

Session 4:

See Page 34

Session 5:

See Page 40 and Page 46

Session 6:

See Page 57

Session 7:

See pages 65 and 67

Session 8:

See Page 71

Session 9:

See XStream

Session 10:

7

See page 84

ASSIGNMENT

Part A (worth 20%)

You are required to imagine that a friend of yours has just won £1 million on the British National Lottery. Your friend knows very little about investment and finance generally and she has asked for your advice.

She will definitely give up employment and retire and is looking for an income of about £100,000 per year. She wants her £1 million not only to remain intact but also to grow, at the very least, in line with inflation. She is quite risk averse, so she requires a good spread of investments so that only relatively small amounts are ‘at risk’ in any one instrument, company or country.

8

You are required to suggest a suitable portfolio of investments which might be expected to achieve your friend’s objectives. You are required to submit your suggested portfolio according to the following deadlines:

If you chose, you can E-Mail your first draft portfolio to [email protected] by 5pm on Friday, 25t February 2011, for feedback. You will receive comments and criticisms of your portfolio (by e-mail) by Friday, 4th March 2011.

Present a final portfolio (taking into account the comments and criticisms received) on Wednesday, 16th March 2011 – to be handed into 2nd Floor Reception, The Rose Bowl, by 12 noon. Please hand in paper copy and also copy on CD.

Your portfolio submission should include a brief explanation and justification of each of the investments you suggest.

Provisional marks for Assignment A will be available on X-stream by Monday, 6th April 2011.

Notes:

a) Brevity is important here – please try to keep your portfolio and justification to two pages maximum.b) Marks will be awarded for:

A sensibly diversified portfolio A logical justification of your choices of investment An attempt to meet the investment objectives of your friend

ASSIGNMENT

Part B (worth 80%)

An individual assignment based on the following case study is to be submitted by Tuesday, 3rd May 2011 (max 3000 words) – to be handed into 2nd Floor Reception, the Rose Bowl, by 12 noon.

Fortunes Inc is a successful London print shop. It is a co-operative which was set up ten years ago after an industrial dispute. The business is run by its 25 workers, including printers, graphic designers and sales staff. It has a flat management structure, which means that no-one is more senior than anyone else. Everyone earns

9

the same no matter how many years they have worked for the business. The ages of the members range from early twenties to mid fifties.

Staff turnover is very low largely, it is felt, because the members like having an equal say in the decision making. They can decide how to structure their hours, what benefits they should have and what equipment they need to buy for the business.

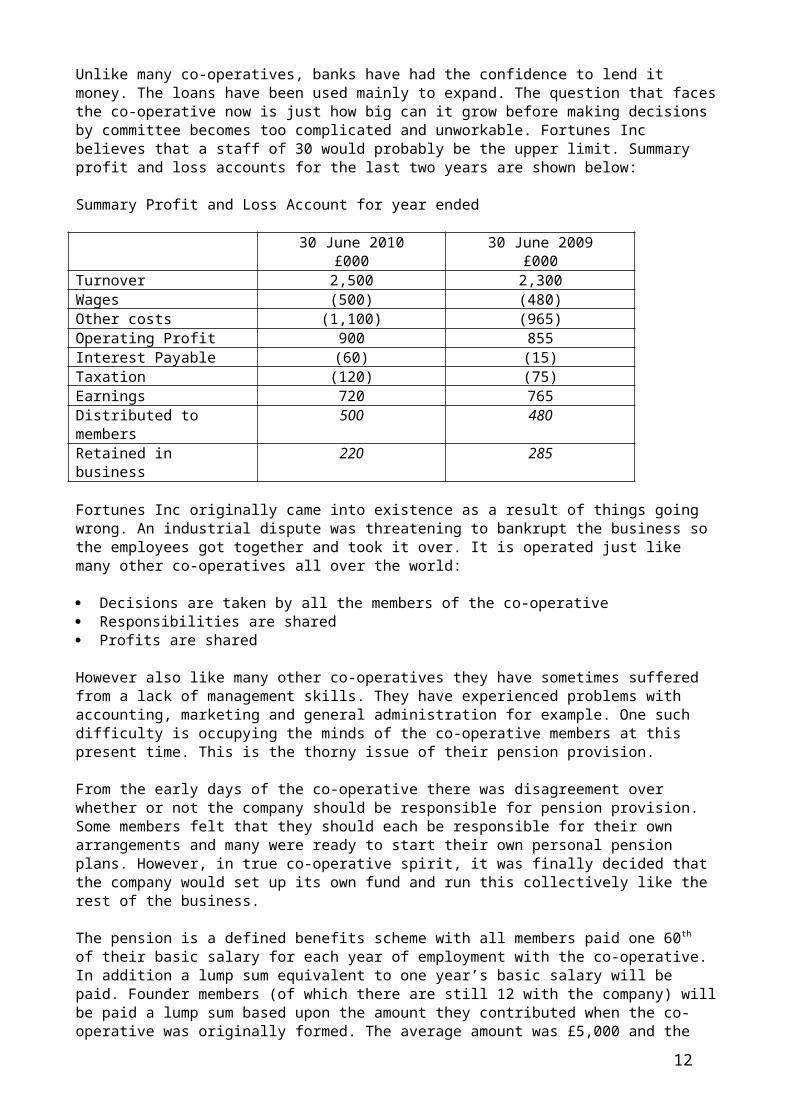

Unlike many co-operatives, banks have had the confidence to lend it money. The loans have been used mainly to expand. The question that faces the co-operative now is just how big can it grow before making decisions by committee becomes too complicated and unworkable. Fortunes Inc believes that a staff of 30 would probably be the upper limit. Summary profit and loss accounts for the last two years are shown below:

Summary Profit and Loss Account for year ended

30 June 2010£000

30 June 2009£000

Turnover 2,500 2,300Wages (500) (480)Other costs (1,100) (965)Operating Profit 900 855Interest Payable (60) (15)Taxation (120) (75)Earnings 720 765Distributed to members

500 480

Retained in business 220 285

Fortunes Inc originally came into existence as a result of things going wrong. An industrial dispute was threatening to bankrupt the business so the employees got together and took it over. It is operated just like many other co-operatives all over the world:

Decisions are taken by all the members of the co-operative Responsibilities are shared Profits are shared

However also like many other co-operatives they have sometimes suffered from a lack of management skills. They have experienced problems with accounting, marketing and general administration for example. One such difficulty is occupying the minds of the co-operative members at this present time. This is the thorny issue of their pension provision.

From the early days of the co-operative there was disagreement over whether or not the company should be responsible for pension provision. Some members felt that they should each be responsible for their own arrangements and many were ready to start their own personal pension plans. However, in true co-operative spirit, it was finally decided that the company would set up its own fund and run this collectively like the rest of the business.

The pension is a defined benefits scheme with all members paid one 60th of their basic salary for each year of employment with the co-operative. In addition a lump sum

10

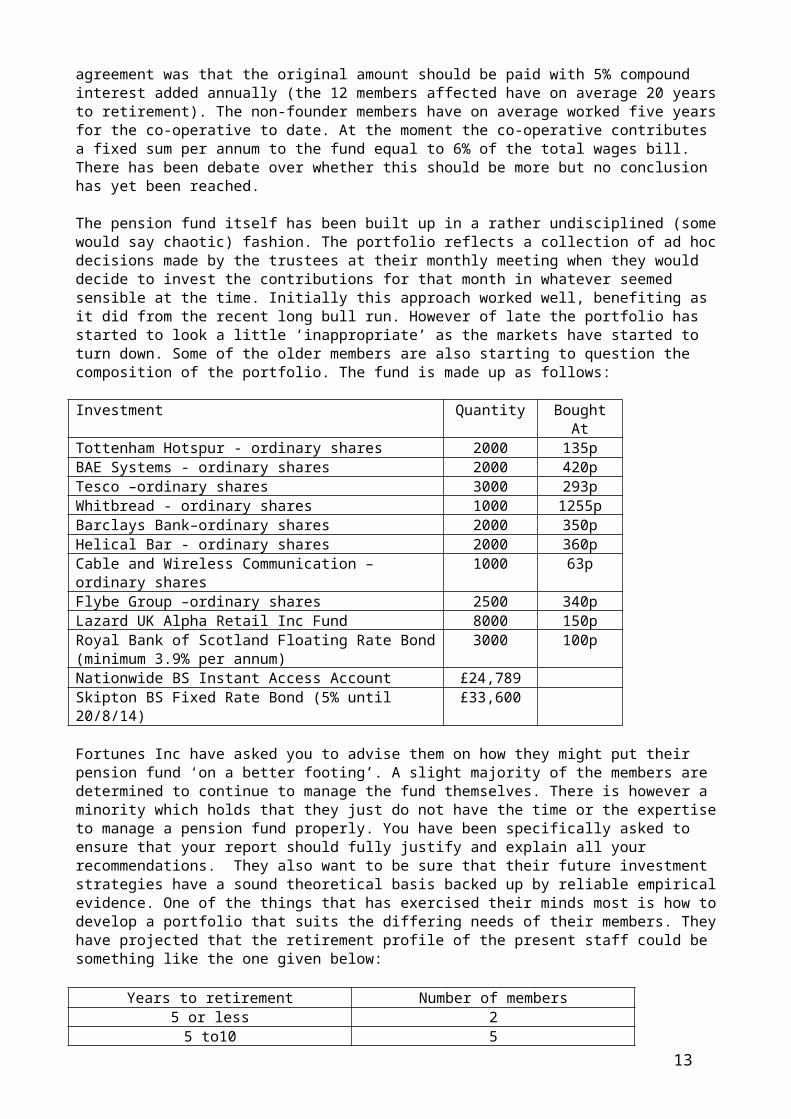

equivalent to one year’s basic salary will be paid. Founder members (of which there are still 12 with the company) will be paid a lump sum based upon the amount they contributed when the co-operative was originally formed. The average amount was £5,000 and the agreement was that the original amount should be paid with 5% compound interest added annually (the 12 members affected have on average 20 years to retirement). The non-founder members have on average worked five years for the co-operative to date. At the moment the co-operative contributes a fixed sum per annum to the fund equal to 6% of the total wages bill. There has been debate over whether this should be more but no conclusion has yet been reached.

The pension fund itself has been built up in a rather undisciplined (some would say chaotic) fashion. The portfolio reflects a collection of ad hoc decisions made by the trustees at their monthly meeting when they would decide to invest the contributions for that month in whatever seemed sensible at the time. Initially this approach worked well, benefiting as it did from the recent long bull run. However of late the portfolio has started to look a little ‘inappropriate’ as the markets have started to turn down. Some of the older members are also starting to question the composition of the portfolio. The fund is made up as follows:

Investment Quantity Bought At

Tottenham Hotspur - ordinary shares 2000 135pBAE Systems - ordinary shares 2000 420pTesco –ordinary shares 3000 293pWhitbread - ordinary shares 1000 1255pBarclays Bank–ordinary shares 2000 350pHelical Bar - ordinary shares 2000 360pCable and Wireless Communication –ordinary shares

1000 63p

Flybe Group –ordinary shares 2500 340pLazard UK Alpha Retail Inc Fund 8000 150pRoyal Bank of Scotland Floating Rate Bond (minimum 3.9% per annum)

3000 100p

Nationwide BS Instant Access Account £24,789Skipton BS Fixed Rate Bond (5% until 20/8/14) £33,600

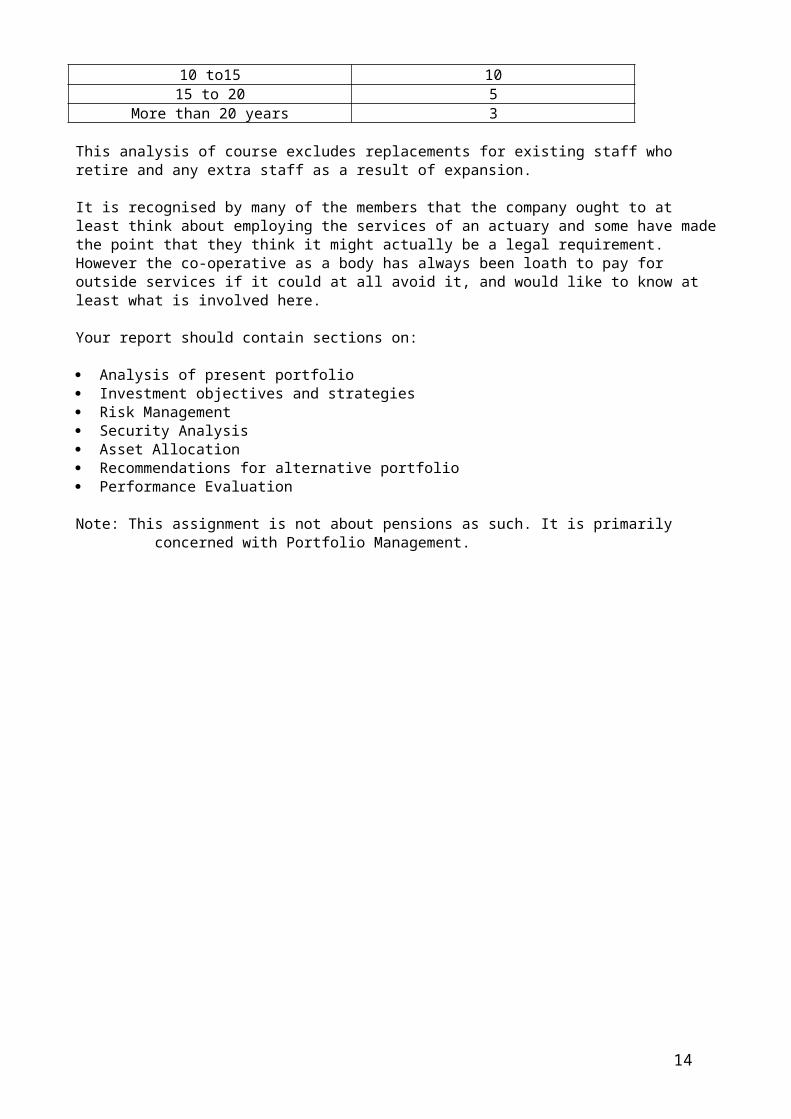

Fortunes Inc have asked you to advise them on how they might put their pension fund ‘on a better footing’. A slight majority of the members are determined to continue to manage the fund themselves. There is however a minority which holds that they just do not have the time or the expertise to manage a pension fund properly. You have been specifically asked to ensure that your report should fully justify and explain all your recommendations. They also want to be sure that their future investment strategies have a sound theoretical basis backed up by reliable empirical evidence. One of the things that has exercised their minds most is how to develop a portfolio that suits the differing needs of their members. They have projected that the retirement profile of the present staff could be something like the one given below:

Years to retirement Number of members5 or less 25 to10 5

10 to15 1015 to 20 5

11

More than 20 years 3

This analysis of course excludes replacements for existing staff who retire and any extra staff as a result of expansion.

It is recognised by many of the members that the company ought to at least think about employing the services of an actuary and some have made the point that they think it might actually be a legal requirement. However the co-operative as a body has always been loath to pay for outside services if it could at all avoid it, and would like to know at least what is involved here.

Your report should contain sections on:

Analysis of present portfolio Investment objectives and strategies Risk Management Security Analysis Asset Allocation Recommendations for alternative portfolio Performance Evaluation

Note: This assignment is not about pensions as such. It is primarily concerned with Portfolio Management.

12

Session 1

Introduction

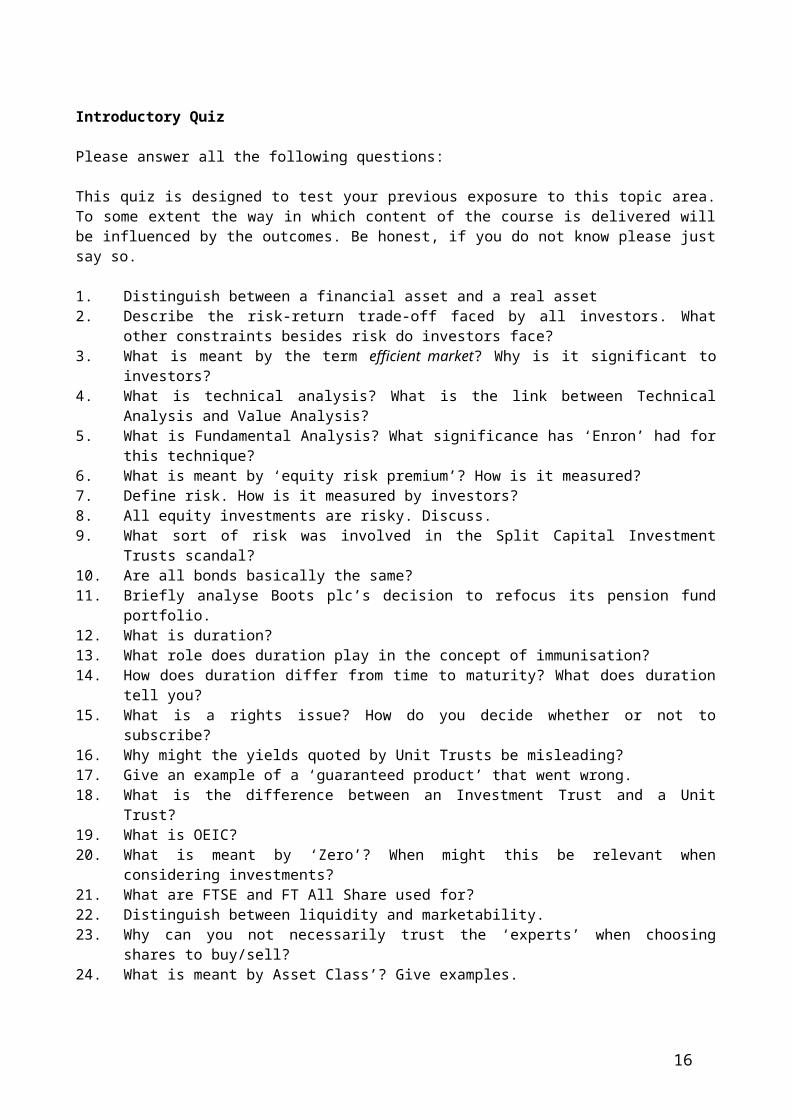

Introductory Quiz

Please answer all the following questions:

This quiz is designed to test your previous exposure to this topic area. To some extent the way in which content of the course is delivered will be influenced by the outcomes. Be honest, if you do not know please just say so.

1. Distinguish between a financial asset and a real asset2. Describe the risk-return trade-off faced by all investors. What other constraints

besides risk do investors face?3. What is meant by the term efficient market? Why is it significant to investors?4. What is technical analysis? What is the link between Technical Analysis and

Value Analysis?13

5. What is Fundamental Analysis? What significance has ‘Enron’ had for this technique?

6. What is meant by ‘equity risk premium’? How is it measured? 7. Define risk. How is it measured by investors?8. All equity investments are risky. Discuss.9. What sort of risk was involved in the Split Capital Investment Trusts scandal?10. Are all bonds basically the same?11. Briefly analyse Boots plc’s decision to refocus its pension fund portfolio.12. What is duration?13. What role does duration play in the concept of immunisation?14. How does duration differ from time to maturity? What does duration tell you?15. What is a rights issue? How do you decide whether or not to subscribe?16. Why might the yields quoted by Unit Trusts be misleading?17. Give an example of a ‘guaranteed product’ that went wrong.18. What is the difference between an Investment Trust and a Unit Trust?19. What is OEIC?20. What is meant by ‘Zero’? When might this be relevant when considering

investments?21. What are FTSE and FT All Share used for?22. Distinguish between liquidity and marketability.23. Why can you not necessarily trust the ‘experts’ when choosing shares to

buy/sell?24. What is meant by Asset Class’? Give examples.

You may find the list on the next two pages useful in completing this exercise.

14

Useful Books On Investment

The Alchemy of Finance George Soros

All About Bonds Esme Faerber

All About Options Russell, Wasendorf and McCafferty

All About Commodities Wasendorf and McCafferty

Art of Investment Barrie Dunstan

Beyong the Zulu Principle Jim Slater

Financial Prediction UsingNeural Networks Joseph S Zirilli

Guide to the AlternativeInvestment Market Finch and Woolfram

How to Read the Financial Pages Michael Brett

How the Stock Market Really Works Gough

The Investors Guide to Selecting Richard KochShares That Perform; Ten WaysThat Work

Investors Guide to Technical Analysis Elli Gifford

Personal Financial Planning T W McRae

Picking the Right Unit Trust Bruce McWilliams

A Random Walk Down Wall Street Burton G Malkiel

Theory and Practice of Investment T G Goff

Value Investing Made Easy Janet Lowe

What Works on Wall Street James P O’Shauhnessy

How the Stock Markets Work: Colin ChapmanA Guide to International Markets

How to Use Company REFS Jim Slater

An Introduction to Stock Janette Rutterford Exchange Investment

Investment Andrew Adams

Investment R G Winfield

Investment David Kerridge

Investment Jane Cowdell15

Investors Guide to Mark MobiusEmerging Markets

The New Paradigm for Financial Markets George Soros

The Crunch Alex Brummer

A list of available funds would include:

Pension Funds

16

Investment Funds

Unit Trusts

Open-ended Investment Companies (OEIC)

Bond Funds

Hedge Funds

Tracker Funds

Ethical Funds

Personal Funds

Money Market Funds

Currency Funds

Commodity Funds

Property Funds

Metals Funds

Innovation Funds

Charity Funds

Offshore Funds

Split Capital Trusts

Exchange Traded Funds

Venture Capital Trusts

Insurance Funds

Friendly Societies

Annuities

International Funds

Enterprise Initiative Funds

Links with other Modules

The following topics:

Shareholder Value Analysis 17

Efficient Market Hypothesis Capital Asset Pricing Model

Are not specifically part of this module. However an outline understanding of them will definitely aid your study and understanding of investment and fund management. Please study the notes on the following pages and ask any questions you may have on their content at the next seminar.

SHAREHOLDER VALUE ANALYSIS

Shareholder value analysis (SVA) is basically a novel way of linking the Net Present Value approach to Strategic Planning. It focuses on how a business can plan and manage its activities to increase value for shareholders and, at the same time, benefit other stakeholders. A number of large organisations have embraced SVA because it provides a way of linking management decisions and strategies to enhancing the value of the entity.

18

SVA is basically the net present value of future free cash flows. The simplest definition of free cash flow is:

Net operating profit after tax + depreciation – capital investmentRequirements – investment in additional working capital requirements

It is argued that the real benefit of SVA is that it encourages organisations to focus on value creating activities. Managers are expected to focus on value drivers i.e. the factors which are thought to have the most influence on shareholder value. Opinions may differ as to just what these value drivers are but they typically include:

Sales Growth Profit Margins Capital investment and acquisitions Working capital management cost of capital (i.e. cost of funds) Taxes (and their impact on investment decisions etc)

It is suggested that one of the other benefits of SVA is that it may encouragemanagement to focus more on long term aspects of operations and to see how shortterm profit related activities (e.g. padding the budget) may in fact destroy value.

Activity:Rolex Foods has a cost of capital of 12%. It has just produced the following forecastsfor the following year:

£000Sales 900Operating Expenses 600 (including £75,000

depreciation)Tax Paid 100Capital Investment in Fixed Assets

125

Additional Working capital 50 Total Borrowing is expected to increase to £90,000.

19

The company expects free cash flow to increase at 50% per annum for the next four years (after the one above) and then to level out and remain fairly constant for the foreseeable future.

Calculate shareholder value. What use is the figure produced?

ECONOMIC VALUE ADDED (EVA)

EVA is a technique closely related to SVA. It is basically residual income after charging for the use of assets. It attempts to measure economic profit as follows:

EVA = Net Operating Profit after TaxLess

(book value of net assets x cost of capital)

Activity:

Two companies A and B have both got capital employed of £100 million and a cost of capital of 15%. Company A made an after tax profit of £20 million last year and Company B £10 million

Calculate the EVA for each company.

20

EFFICIENT MARKET HYPOTHESIS

Investment Strategies:

1. ‘Fair return for risk strategy’:- the strategy suggested by Portfolio Theory and CAPM;- the individual risk and return characteristics of each investment are matched to

the profile of an investor’s portfolio;- only possible to beat the market if extra risk taken (CAPM);- prices of investments already incorporate market expectations regarding price

sensitive information.

2. ‘Picking winners’:- possible to beat the market without taking extra risk;- the assumption that some investments, allowing for their relative risk, will offer

higher returns than others;- Investors who follow this strategy must assume that they know something

about these investments that either the market does not yet know or has not yet incorporated into the price.

Efficient Markets:

- if markets are efficient then trying to pick winners will be a waste of time;- this is because in an efficient market the prices of investments will reflect the

best estimate of their expected return and risk taking into account all that is known about them;

- there will be no undervalued investments offering higher than expected returns given their risk;

- excess returns will not be possible – this means consistent (over a number of years) returns above those in the CAPM, given the level of risk involved.

Random Walk Theory:

- argues that there are no trends in investment prices;- tomorrow’s price cannot be predicted by looking at today’s price change;- one difference to note between share prices and commodities, for example, is

that in so far as shares have positive expected return share prices will exhibit an upward trend;

- however Random Walk Theory is a much misunderstood concept which does NOT mean:

i) investment analysis is a waste of time;ii) no one can ever beat the market;iii) share prices are determined by chance.

Efficient Market Hypothesis:

- basically an attempt to explain why investments follow a random walk;- in a perfectly efficient market information is freely and instantly available to all;- thus each investment will be ‘correctly’ valued in that all information will be

fully absorbed into its price;- whilst in practice perfectly efficient markets do not exist it would appear that,

from evidence available, markets do appear to be relatively efficient at reflecting new information in prices;

- the real question is how efficient the markets are;- Fama (1970) defined three different levels of efficiency:

21

1. Weak Form:- each share price assumed to reflect fully the informational content of all past share prices

2. Semi-Strong Form:- each share price assumed to reflect also all publicly available information

relevant to share prices

E.g. Company announcementsBrokers’ reportsIndustry forecastsCompany accounts

3. Strong Form:- each share price also fully reflects all known information whether publicly

available or notE.g. insider information

The EMH does not claim that investors will never beat the market and will never make large profits. What it does say is that over a period of time above average or excess returns will not be earned. Evidence available in general supports both the Weak and the Semi-Strong forms but not the Strong form.

Implications of the EMH for Investors:

Technical Analysis – even in its weak form the EMH casts severe doubts over the use of Chartism and Mechanical Rules

Fundamental Analysis – in its semi-strong form the EMH questions the time spent by Investment Analysts;- there is a persuasive argument however that markets would not

be as efficient without them;- they should however switch emphasis from straight picking

winners to constructing portfolios for investors which take into account their risk-return preferences.

THE CAPITAL ASSET PRICING MODEL

Originally developed as an alternative approach to portfolio management, the CAPM can also be used to calculate cost of capital. It can be used in two different ways:

22

a) To calculate the equity cost of capital of a company which can then be incorporated into the calculation for the company's weighted average cost of capital.

b) To calculate the required rate of return for individual projects taking into account their specific risk profiles.

Systematic and Unsystematic Risk:

The concept that the risk associated with any particular investment can be subdivided into two types is fundamental to the CAPM.

Systematic (market) Risk is that part of total risk stemming from those changes in the general political and economic climate which, more or less, affect all investments.

Unsystematic (specific) risk is that part of total risk caused by factors that do not affect all investments and may affect just one investment (eg incorrect decisions made by a company's management).

It is well accepted that the effect of unsystematic risk can be virtually eliminated by the development of a sensibly 'diversified' portfolio (Markowitz's Efficient Diversification).

Given that investors do diversify effectively; all that remains to concern them, therefore, is systematic risk and this is what the CAPM deals with.

The underlying rationale of the CAPM:

Given a market where efficient diversification is the rule, investors are basically concerned with systematic risk. Unfortunately different investments differ with regard to the amount of systematic risk they carry. For example a firm manufacturing consumer durables is more likely to be affected by an economic downturn than, say, a firm producing staple food items. Consequently, the systematic variability of the former's shares is likely to be greater than that of the latter.

The most widely used index of systematic risk is the BETA COEFFICIENT. This is simply the slope coefficient of a linear regression of the investment's return on the market's return for a representative number of periods.

Investments with Beta factors of less than 1 have very low systematic variability and thus tend to lower the risk of fully diversified portfolios. Investments with Beta factors of more than one become progressively less attractive for inclusion in a portfolio based on risk alone.

Since investors are assumed to make their decisions on the basis of two factors (expected return and systematic risk), it therefore follows from the CAPM that the following should hold for individual investments:

E(Ri) = Rf + B(Rm - Rf)

where E(Ri) = expected return on investment Rf = risk free rate of return Rm = market rate of return

23

B = Beta factor of i

The Calculation of the Beta Factor:

The London Business School publishes a quarterly Risk Measurement Service containing the betas of most UK companies. They are calculated using a standard least squares regression programme using the monthly returns for each security over the previous five years.

What the above, in effect, does is to compare the standard deviation of market returns with the standard deviation of the returns of an individual security. It is possible, therefore, to approximate a beta factor for a security (or portfolio) if you are given the required standard deviations.

Thus Beta* = Standard Deviation of Security Standard Deviation of market return

*assuming an efficient market and thus a correlation coefficient of 1.

Where the correlation coefficient is different from one then the formula becomes:

Beta = Correlation Coefficient x Standard Deviation of Security Standard Deviation of Market

For examination purposes an alternative formula, derived from the one above, is oftenuseful:

Beta = Covariance of security returns with market returns Variance of market returns

24

Session 2

The Investment Environment

THE INVESTMENT ENVIRONMENT

What is Investment?

There are several ways of answering the above question. The first might be to distinguish between Real Investments and Financial Investments:

Purchase of one’s own home Rare stamps or coins Antiques Gold (in some forms) Paintings Jewellery Wine

25

Furniture Chinese ceramics English and continental silver Property Carpets and rugs

As interesting as they are these are not the subjects of this module because of their highly specialised nature. Financial Investments include:

Equities Loan Stocks Gilts National Savings Investments Unit Trusts (at least 20 different kinds) Investment Trusts Insurance Policies (some) Pension Plans Property Bonds Managed Bonds Warrants Convertibles (debentures and preference shares) Foreign bonds and equities Offshore deposits Futures and options Cumulative convertible redeemable preference shares Guaranteed Income and Growth Bonds

These are the subjects of this module and some will be covered in more detail later.

Another way of answering the question – ‘what is investment’ is to examine it from the point of view of its purpose. Investment by the individual can be regarded as more considered and more specific than just savings. The investor aims generally to achieve one, or both, of the following:

A specific regular income or growing income Medium to long term capital growth

However it must be said that the distinction between investment and saving can be extremely blurred at times.

Yet another way of looking at the question ‘what is investment’ is to consider how it differs from Saving, Speculation and Gambling.

26

Group Discussion:

(a) Can you briefly differentiate between saving, investment, speculation and gambling.

(b) Why do you think the distinctions in (a) might be important?

(c) What do you think might be the common theme linking all four in (a)?

(d) What is the significance of (c ) to an investment adviser?

(e) In which category from (a) would you place Premium Savings

Risk and Return

An investor can obtain two different kinds of return from an investment in a financial security:

Return from price appreciation (or losses from price depreciation) – commonly called capital gains (losses)

Return from dividends or interest payments

Therefore return for any period can be expressed as:

Return = Price Change + Cash Inflow (if any) x 100 Price at beginning of the period

However every investment involves uncertainties that makes its future investment returns risky. Sources of uncertainty include:

Interest Rate Risk

If interest rates rise then investment market prices will fall, and vice versa.

Inflation Rate Risk

Inflation reduces the real rate of return on investments. (It is often claimed that equities provide a hedge against inflation because assets and incomes should be able to keep pace with

inflation. However evidence does not seem to support this view). Bull-Bear Market Risk

Bull markets indicate periods of sustained security price increases and Bear markets the reverse. (In the past Bear markets have lasted for up to 3 years (although the average is probably less than a year). They also vary greatly in

intensity (i.e. in some instances most stocks are effected; in others relatively few). In the long run, Bull markets more than

compensate for bear markets but they can still be a serious source of risk). Default Risk

This is the perceived risk that a company may go bankrupt or similar.

Liquidity Risk

This is the possibility of loss created by lack of marketability of the financial asset.

Political Risk

International political risk is most often cited but the problems can be just as real on a domestic basis e.g. changes to the tax laws.

Industry Risk

This is the variability of returns caused by association with a particular business sector. The causes may be economic, technical, marketing, social etc.

Management Risk

27

This is the variability of returns caused by the quality of management in the company, industry, country etc.

There are more but the above should serve to illustrate the complex nature of measuring risk.

Relationship of Risk and Return

Investors are risk averse i.e. they require expected returns that vary in line with the amount of perceived risk. However different investors exhibit different levels of risk aversion and it has been proved that risk aversion:

decreases with wealth;

increases with age;

is influenced by economic cycles;

is influenced by ‘thin trading’.

different investors have different perceptions of risk in relation to individual investments

This is covered by the economic principle of Utility and manifests itself in the form of ‘Risk Premiums’ demanded for riskier investments.

Measurement of RiskVariability of returns is the most accepted measure of investment risk and most of this variability tends to be caused by fluctuations in stock prices.

Standard deviation and variance are usually used to measure the degree of risk involved. However there are problems with the use of these as measures:

they assume that investment returns are normally distributed – in fact they almost always are skewed;

they are basically historical; they ignore the Fractal Dimension i.e. they only exhibit the ‘range’ of returns and

not the frequency of fluctuations.

(one way of measuring this would be to draw the movements of a stock price on a chart then measure the length of the line – the

longer the line the higher the fractal dimension and thus risk)

What is Meant by Investment Policy and Investment Strategy?

Investment policy should start with Investment Objectives. This is basically what the investment portfolio is required to achieve eg:

funds for retirement funds for charity purposes funds for major projects etc

The Investment Policy should then be driven by the individual needs/requirements of the investor(s). It will cover such things as:

appropriate risk/return profile liquidity requirements tax positioning

28

ethical constraints

The Investment Strategy is basically the means of achieving the investment objectives whilst observing the investment policies. They are largely to do with balancing risk and return. They are mostly influenced by the following factors:

Rates of interest Rates of return from alternative assets Potential for capital growth Risk of capital loss Time horizon Asset classes available

The following list illustrates some of the many Investment Strategies used by investors/fund managers:

(a) Adopt a passive (buy and hold) investment strategy. The logic here is that an investor is less likely to be affected by the ups and downs of the securities market if they hold investments for long periods. This often works but is not foolproof – for example a sudden change in circumstances may force liquidation of investments at the bottom of a bear market.

(b) Adopt an active investment strategy. Here the use of Technical and/or Fundamental Analysis is adopted either by the investor personally or by the use of ‘expert’ recommendations. Studies have been largely found against these techniques (especially Technical Analysis) but some have shown that they can have value.

(c) Invest only in investments where risk is perceived to be low e.g. bank accounts. However this will not reduce all risks and the investor would be rewarded by suitably lower returns.

(d) Try to identify under or over valued shares and invest or disinvest appropriately. One reasonably straightforward way of doing this it to use Gordon’s Growth Model.

(e) Diversify. Diversification will help to reduce risk. Portfolio Theory shows that effective diversification can be achieved with less than 15 securities if they are carefully chosen. It is necessary to choose stocks (for example) that do not display positive correlation. Ideally stocks should have perfectly negative correlated returns (i.e. when one goes up the other always goes down and by an equal amount). However this does not happen in practice, but less than perfect correlation will still help to reduce risks. The problems with this approach are:

Diversification is a problem for the small investor because dealing charges make the acquisition and trading of numerous small lots of securities uneconomic.

Choosing securities with negative correlation is not easy. Investors are often reduced to making sure that their shares come from different sectors e.g. retailers, engineering, banking etc.

(f) Diversify using Unit Trusts or Investment Trusts. This is a popular option but it does have problems:

Unit Trust charges can greatly reduce the return earned. For example Initial Charges can be as high as 6% (that is £600 on an investment of £10,000) and means that the investment must increase by 6% before the investor is back where he/she started. Add to this Annual Charges (1% +) and you can see why some unit trusts (even when held in an ISA) are often a poor alternative.

29

It is generally accepted that most (up to 90%) of Unit Trusts do not do as well as the market average.

The number of unit trusts available is huge making the choice of which to buy onerous; and the right choice is important because the gap between the best and worst performing is significant.

Investment Trusts do generally perform better than unit trusts and their charges are lower. But they are relatively less known about and understood than unit trusts, which may help to explain why their performance can be disappointing at times.

(g) Build up a portfolio using Beta Factors. Beta factors measure the systematic risk of shares by comparing the standard deviation of the returns on an individual share with the standard deviation of market returns. Beta factors can be purchased from such sources as the London Business School and are also available on Data Stream (although not as up to date). This, in theory, allows an investor to build a portfolio with a level of risk and return suitable to their circumstances. Whilst tests show that returns do relate to Beta’s they also show that returns also relate to other things as well. Nevertheless there is evidence that a portfolio with a high weighted average beta will often give higher than average returns.

(h) Make use of System Trading for management of investments. There are numerous systems used for investment. One important group of these is known as Filter Methods. Share price movements can be identified as follows:

Tertiary – smallish movements without any long run significance. Secondary – more significant movements but still not having any long run

significance. Primary – the primary movements have long run significance and in fact

contribute to the long-term trend.

Filter methods attempt to filter out secondary and tertiary movements and identify the trend. One simple example of a filter method is the Hatch System.

(i) Make use of International Diversification. International investments can have their problems but it does seem to be generally accepted now that the benefits far outweigh any problems. In fact it has been said that you need excuses not to invest internationally nowadays. There are several ways of introducing an international element to your portfolio:

Buy overseas stocks quoted on the domestic Stock Exchange (there are often a lot).

Invest in UK stocks with a high level of overseas exposure. Invest in a Unit Trust with specialist international funds. Invest in appropriate Investment Trusts. (IT’s are major overseas investors

with a long and acknowledged track record).

(j) Invest in one of the many ‘Guaranteed Return’ products. These give you some sort of guarantee in relation to Stock Market Returns – for example some guarantee a certain percentage of any increase in a particular index. The guarantee does not come free however and the cost may take the form of tying your investments up for long periods with heavy penalties for early withdrawal.

(k) Invest in a Tracker Fund. These funds are designed to track particular index’s (e.g. FTSE, FT All-Share, Dow Jones, S & P etc). They do it by either buying every stock in the index – in which case they track the chosen index perfectly – or they attempt to replicate the index by the use of futures and options or some

30

sort of statistical methods. They tend to have lower charges than conventional unit trusts – for example most do not have any Initial Charge and Annual Charges seem to be generally lower.

Sessions 3 and 4

Diversification and

Portfolio Analysis

31

What are the main aspects to be taken into account when planning a portfolio?

There are three main elements:

Diversification Risk Timing

Diversification

A portfolio must be balanced to guard against failure in any one specific area. Therefore a portfolio should be well diversified and contain elements of:

Liquidity- To provide accessibility of funds for essential/unexpected commitments.

Fixed-interest Holdings- To provide stability in the form of a guaranteed income (plus capital growth)

Equity Holdings- to provide growth of capital and income

Risk

The liquidity and fixed interest elements of the portfolio are specifically subject to interest rate risk (interest rates rise and you cannot benefit from them) and inflation risk. The equity holding mitigates against these risks but also introduces other risks. These risks, poor performance and corporate collapse, can be reduced however by diversification. Research points to the conclusion that investing in 15 different shares in different sectors minimises risk effectively (for cost effectiveness a minimum of £2,000 per share is recommended, otherwise the share has to increase too much to simply recoup dealing costs – if you do not have £30,000 to invest in shares then consider Unit or Investment Trusts).

Timing

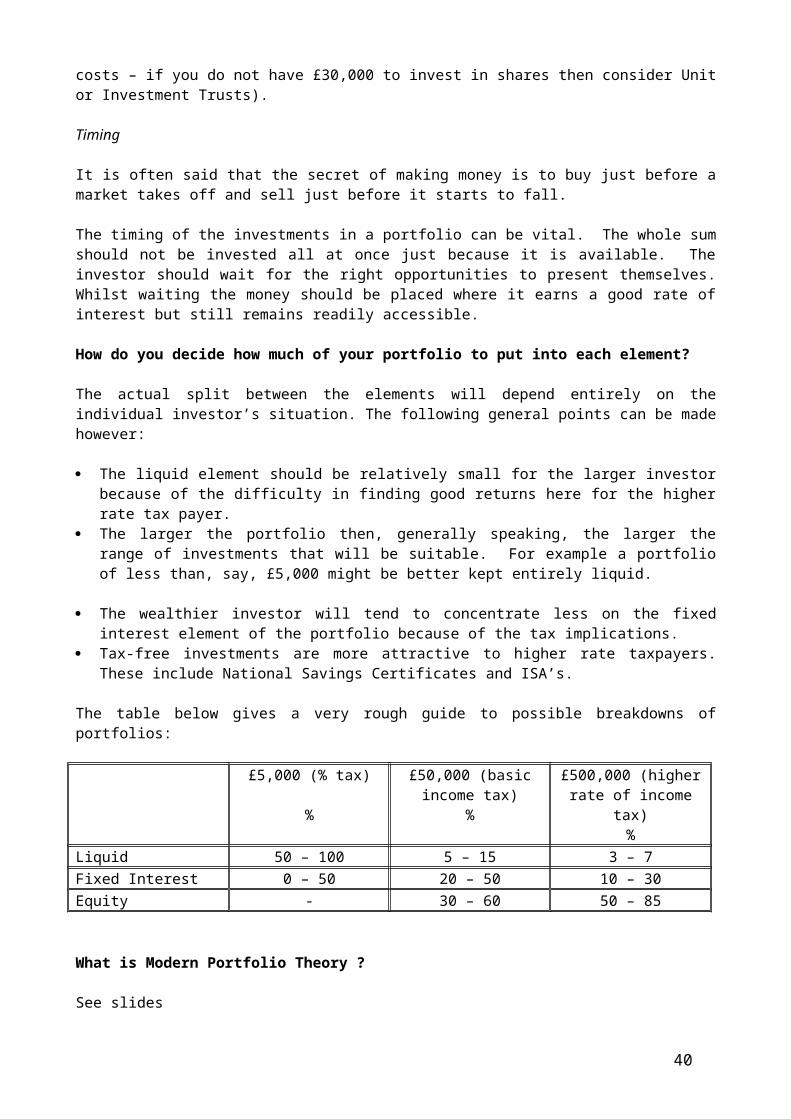

It is often said that the secret of making money is to buy just before a market takes off and sell just before it starts to fall.

32

The timing of the investments in a portfolio can be vital. The whole sum should not be invested all at once just because it is available. The investor should wait for the right opportunities to present themselves. Whilst waiting the money should be placed where it earns a good rate of interest but still remains readily accessible.

How do you decide how much of your portfolio to put into each element?

The actual split between the elements will depend entirely on the individual investor’s situation. The following general points can be made however:

The liquid element should be relatively small for the larger investor because of the difficulty in finding good returns here for the higher rate tax payer.

The larger the portfolio then, generally speaking, the larger the range of investments that will be suitable. For example a portfolio of less than, say, £5,000 might be better kept entirely liquid.

The wealthier investor will tend to concentrate less on the fixed interest element of the portfolio because of the tax implications.

Tax-free investments are more attractive to higher rate taxpayers. These include National Savings Certificates and ISA’s.

The table below gives a very rough guide to possible breakdowns of portfolios:

£5,000 (% tax)

%

£50,000 (basic income tax)

%

£500,000 (higher rate of income tax)

%Liquid 50 – 100 5 – 15 3 – 7Fixed Interest 0 – 50 20 – 50 10 – 30Equity - 30 – 60 50 – 85

What is Modern Portfolio Theory ?

See slides

Group Exercise

Discuss the theoretical and practical criticisms of MV Optimisation Models and produce a short report on the following:

a) To what extent the criticisms are justifiedb) Suggestions for possible solutions

33

Session 5

Portfolio Management

Strategic Asset Allocation

34

Having drawn up an overall financial plan which should cover:

How much money will be available to invest and when How much income will be required from the investments and when Where the investor is placed upon the risk/return scale

It is then necessary to decide how funds will be divided amongst the four asset classes and overseas investments:

Cash Bonds Property Shares Overseas investments

This is almost certainly the most important factor affecting portfolio performance. A recent American study showed that asset allocation alone accounted for most of the differences in performance as follows:

Asset allocation – 92% Stock Selection – 5% Timing – 2% Other – 1%

Finding the best mix of assets involves three key variables:

Risk Return Correlation

It is not just a matter of spreading the money around. In order to get the optimum portfolio providing the maximum return for the risk taken, asset classes must be chosen carefully. It is possible to choose a mix that will increase return without necessarily increasing risk – in other words to move the portfolio nearer to the efficient frontier.

There are two basic approaches to Strategic Asset Allocation:

Technical Approach

Initiative Approach

Technical Approach

This approach makes use of a computer and involves the following steps:

35

Establish historical benchmarks for risk, return and correlation for the range of investment options selected.

Establish as far as possible why the above happened – was inflation a factor? What about interest rates?

Attempt to establish a forecast of the expected relationships taking into account the future economic outlook. This process will mainly involve risk and return. Correlations tend to remain fairly stable.

Run an asset allocation model using suitable software.

Adjustments should be made if tax is a consideration.

Adjustments should also be made for special considerations e.g. requirements to keep a certain level of cash with overseas investments.

Initiative Approach

This is basically a common sense version of the computer-based approach. It takes into account the key characteristics of each asset class and of overseas investment:

Cash

- The safest asset class- Lowest returns- Low correlations with other asset classes- Tax ineffective for high earners.

Bonds

- Low to medium risk- Low correlations with cash- Fairly low correlations with shares and property.- Tax ineffective for high earners.

Property

- Medium to high risk- Low correlations with cash- Fairly low correlations with bonds- Moderate correlations with shares.- Returns highly susceptible to cycles.

Shares

- High risk- High returns in the long term- Short and medium term volatility

Overseas Investment

- Potentially high risk- Lack of correlation makes them very effective for diversification providing

moderate exposure.- Require special analysis of tax, risk, correlation, currency and political

factors.36

The overall approach recommended is to apply the characteristics of each asset class to the three main criteria of the investor profile:

Risk- The risk averse investor will put a larger proportion of their funds into

cash and bonds.- Those investors who are able to take on more risk will tend to put a larger

proportion of their funds into property, shares and overseas investments.- The medium risk investor will have a reasonable amount in each asset

class.

Tax - High earners will avoid tax ineffective asset classes.- Non-tax payers should avoid tax-free investments.

Time Horizon- Investors who wish to invest for the long term will find property and

shares relatively safe.- Short-term investors will tend to favour a less volatile portfolio containing

more cash and bonds.

Having decided the Strategic Asset Allocation it is then necessary to diversify at all rungs of the risk ladder:

Industry risk Firm specific risk Country risk

This can be achieved by using:

Tactical Asset Allocation

This is basically responding to current and forecast market conditions. The best way of achieving this without taking too many risks is to set a tactical allocation a few percentage points either side of the strategic allocations. The reason for keeping the allocation ranges fairly narrow is to avoid straying too far from the overall plan and thus endangering the achievement of the objectives.

Sub-sector Allocation

This involves selecting the appropriate sub-sectors within each class. The safest approach is to choose a representative range from each class but it might be sensible to be slightly ‘overweight’ in those sub-sectors thought to have better prospects.

Investment and Vehicle Selection

This basically involves the choice of investment medium – for example investment in shares can be carried out by investing in individual shares or by use of collective investments. Investment in property can be through insurance funds, property funds or directly. The choice will depend upon investment philosophy and funds available.

37

Active versus Passive Investment Strategies

Passive Portfolio Management

Passive portfolio management attempts to maintain an appropriate risk-return balance given market opportunities. Rather than attempting to ‘beat the market’ it accepts market prices of securities as correct. It accepts the principle of the Efficient Market Hypothesis. It tends to conform to the following:

Long-term buy-and-hold strategies. Index tracking Matching market performance Performance tracked against benchmark portfolios.

Active Portfolio Management

Active Portfolio Management attempts to outperform a passive benchmark portfolio by the use of superior insight or information. It tends to conform to the following:

Fundamental Analysis Technical Analysis Market Timing Value Analysis

Market Timing

“Someone can always tell you what you should have bought or sold in the past. No one, however, can guarantee you a successful portfolio for next year or any other specified period of time because no one can consistently forecast what will happen in the financial markets, including the professionals who are paid to make recommendations. Unanticipated events will affect the financial markets. Although the future is uncertain, it is manageable, and a thorough understanding of the basic principles of investing will allow investors to cope intelligently” (CP Jones, Investments, 2007, p13).

“No one on Wall Street has ever figured out how to time stocks’ swings perfectly. Most people, in fact, fail miserably at timing.” (Tom Petruno, LA Times: 4/9/97)

Market timers attempt to beat the market by use of the following types of approaches:

Technical Analysis Economic Indicators Specialised composite indexes

Group Discussion:

What do you consider to be the comparative advantages and disadvantages of Active and Passive investment strategies?

Is it always necessary to adopt one or the other strategy?

Security Analysis and Allocation

According to the Efficient Market Hypothesis it is not possible to find under or over valued shares except in unusual situations i.e. the so-called ‘anomalies’. Given a perfect market securities will always be valued at their true value.

38

However there is a lot of empirical evidence that seems to call the EMH into doubt. In fact there is a school of thought that suggests security prices are usually wrong; and that investors able to spot the mistakes can ‘beat the market’. The EMH suggests that the only way to earn higher than average returns is to take on higher than average risk. There are those that claim that it is in fact possible to earn higher returns and take on less risk.

Unfortunately most of the evidence seems to come from the USA but there is no reason to believe that the examples could not be replicated in the UK.

Walter Schloss (Tweety Browne) has outpaced the S&P 500 for the last 39 years. The funds he has managed have averaged a return of over 20% over that time compared with 10% on the S&P 500. Also whilst the S&P 500 has finished in the red nine times during the 39 years Walter Schloss has only lost money on six occasions.

Warren Buffett has an even more sparkling performance to show. Between 1965 and 1982 (when the S&P 500 averaged annual returns of 7%) he averaged 28%. Between 1983 and 1994 (when the S&P 500 averaged 14% per annum) he averaged 31%.

Charles Munger, Peter Lynch, John Neff, William Ruane, Benjamin Graham – all household names in the USA are just a few of the many examples of fund managers who have consistently ‘beaten the market’.

George Soros is another major investor who does not subscribe to the EMH. He contends that market values are always distorted. He also argues that share prices, far from being merely passive reflections of underlying values, are active ingredients in the process by which both share prices and the fortunes of the company are determined.

David Dreman (Investment Advisor and Author) quotes an investor who had been burned by the 86% fall in the value of Disney between 1972 and 1974. ‘When was the market efficient? When it took Disney up to $119 or when it put it back to $16?’

The general terms given to the non-EMH type of investors are Value Investors.

Who is right? EMH followers or ‘Value Investors?’

One way of looking at this problem might be to suggest that they are both right. Jack Clark Francis considers that security prices can be viewed as ‘a series of random fluctuations around their intrinsic value’. He illustrates this by considering two hypothetical groups of traders: Liquidity Traders and Information Traders.

Liquidity Traders have only limited access to relevant information and may not be able to interpret it properly. Their investment decisions are driven more by availability and need for funds (i.e. they invest when they happen to have a surplus and sell when they need the cash). They often make their decisions on whims or ‘hot tips’.

Information Traders on the other hand have access to much better information and know how to interpret it properly. They will buy and sell when they recognise deviations from intrinsic value and so force the market price into line with the intrinsic price.

It is thus agreed that the unsophisticated liquidity trader is responsible for the aimless price fluctuations observed in all shares and the information traders responsible for the fact that market prices at least meander around their true intrinsic value. This phenomenon was called the ‘intrinsic-value random-walk market’ by Professor Fama. The process is called a ‘random walk within reflecting barriers’ by mathematical statisticians.

39

This does not mean that any particular share will always keep the same intrinsic value – for some firms this may change on quite a regular basis. However it is the way in which investors react to these changes that may contribute yet another distortion to the so-called ‘perfect stock market’. Mark Johnson calls this the Overreaction Hypothesis. This argues that the prices of shares may well reflect the expectations of investors but ‘what if those expectations are wrong in some consistent (i.e. non-random manner). If so the market will not be perfectly efficient (returns will be related to more than just risk), and we ought to be able to formulate strategies to out-perform simple buy and hold strategies’. The evidence for this assertion comes from the psychological theories that hold that the human mind may have problems of sorting and filtering information, which will often lead to significant distortions in perceptions.

George Soros goes even further than this to maintain that:

Markets are always biased in one direction or another. Markets can influence the events that they anticipate. This point is in reaction to the assertion that markets always seem to be right.

Fundamental Analysis Methods

Shown below are some of the more common methods of share valuation:

1. Fixed interest securities

Most debentures and loan stocks are redeemable and thus their value is based upon the present value of future interest payments plus the present value of the redemption payment.

If a debenture or loan stock was irredeemable then its value can be calculated from:

Coupon Rate of Stock x nominal value Rate of Return Required

This is the same as the valuation of a perpetuity and can thus be used on those securities with a long time to redemption.

Variable rate securities are valued on a similar basis to shares (see below).

2. Shares

(i) Dividend Valuation Model

This is based upon the present value of a future stream of dividends allowing for dividend growth:

Po = D1 i-g Where Po = share price

D1 = next dividend i = market capitalisation rate g = dividend growth rate

(ii) Earnings Valuation Model

Po = P/E ratio x Earnings per share

Problems:40

How do you choose a representative P/E ratio?

Which earnings per share do you use?- Last years?- Next years?- Normalised?

Cash Flow Model

Use projected cash-flows discounted at a suitable cost of capital. Theoretically the soundest method but has obvious practical limitations – not least the forecasting of cash flows and the determination of a realistic cost of capital.

Capitalisation of Earnings Approach

Po = Maintainable Earnings per ShareExpected Rate of Return

Both denominator and numerator difficult to estimate.

Net Asset Basis

Po = Realisable Value of Assets – LiabilitiesNumber of Shares in Issue

Problems:

Valuation of Assets

Takes no account of future profits

Super Profits Approach

Po = Super Profits per Share x Suitable Multiplier + Net Asset Value

Problem is that this is a negotiated figure and as a result very arbitrary.

Capital Asset Pricing Model

This requires the determination of a realistic beta coefficient for the company – possibly by comparison with other similar firms. The standard CAPM formula is used to calculate the cost of capital (required return) which is then used in the Dividend Growth Model to produce a share price valuation.

Technical Analysis

This approach is usually used for valuing shares and is based upon a, sort of, behavioural approach. It makes use of charts (hence it is often called Charting) and weight of selling (or buying) to predict share price movements. The dedicated chartist makes use of moving averages and ‘patterns’ to value shares. It may sound crude and arbitrary but it is in fact a highly developed process requiring a lot of skill. There is also no evidence to show that it is more or less accurate than fundamental analysis.

Examples of ‘Value Investment’ Strategies

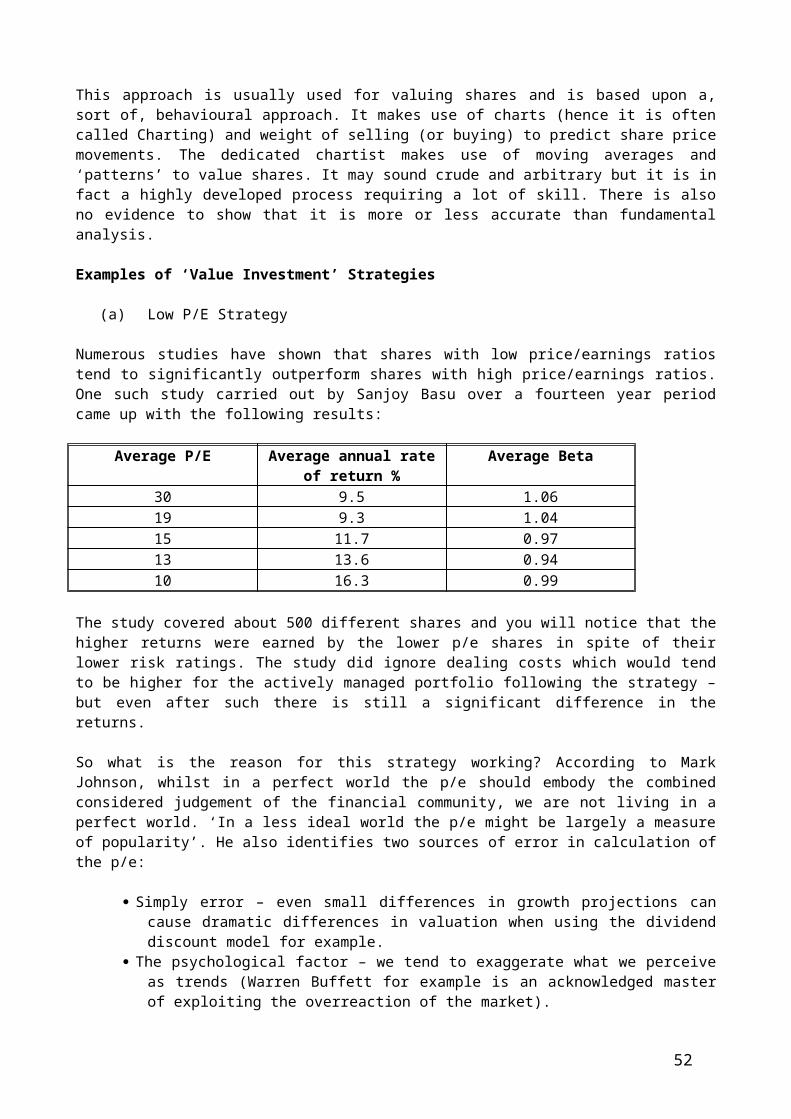

(a) Low P/E Strategy

41

Numerous studies have shown that shares with low price/earnings ratios tend to significantly outperform shares with high price/earnings ratios. One such study carried out by Sanjoy Basu over a fourteen year period came up with the following results:

Average P/E Average annual rate of return %

Average Beta

30 9.5 1.0619 9.3 1.0415 11.7 0.9713 13.6 0.9410 16.3 0.99

The study covered about 500 different shares and you will notice that the higher returns were earned by the lower p/e shares in spite of their lower risk ratings. The study did ignore dealing costs which would tend to be higher for the actively managed portfolio following the strategy – but even after such there is still a significant difference in the returns.

So what is the reason for this strategy working? According to Mark Johnson, whilst in a perfect world the p/e should embody the combined considered judgement of the financial community, we are not living in a perfect world. ‘In a less ideal world the p/e might be largely a measure of popularity’. He also identifies two sources of error in calculation of the p/e:

Simply error – even small differences in growth projections can cause dramatic differences in valuation when using the dividend discount model for example.

The psychological factor – we tend to exaggerate what we perceive as trends (Warren Buffett for example is an acknowledged master of exploiting the overreaction of the market).

(b) Market to Book Value Strategies

This approach was pioneered by Benjamin Graham and has stood the test of numerous empirical studies. His view was that when earnings seem to be inconsistent, unpredictable and so subjective then we ought to place greater emphasis on the balance sheet in determining share values. He developed a method of measuring a company’s Earnings Power (as he called it) from its balance sheet. Graham’s method focused on liquidation value:

Net Assets at book valueLessNon liquid assets such as land, buildings, equipment and goodwill

He then suggested that investors should purchase shares:

With market prices lower than two-thirds of the liquidation value per share Of companies with positive earnings Of companies that are paying dividends, and Hold them in a diversified portfolio

Various studies have shown returns well in excess of double (sometimes treble) the market returns. The beta factor of these ‘bargain issues’ as they are called does tend to be higher than the market average but not high enough to explain the differences in returns.

42

Walter Schloss favours this strategy. He prefers to consider asset values rather than earnings because he feels that accounting rules give too much room for manipulation. He generally prefers shares that are selling at one half to two thirds of book value – but admits that they are not easy to find so will occasionally go higher.

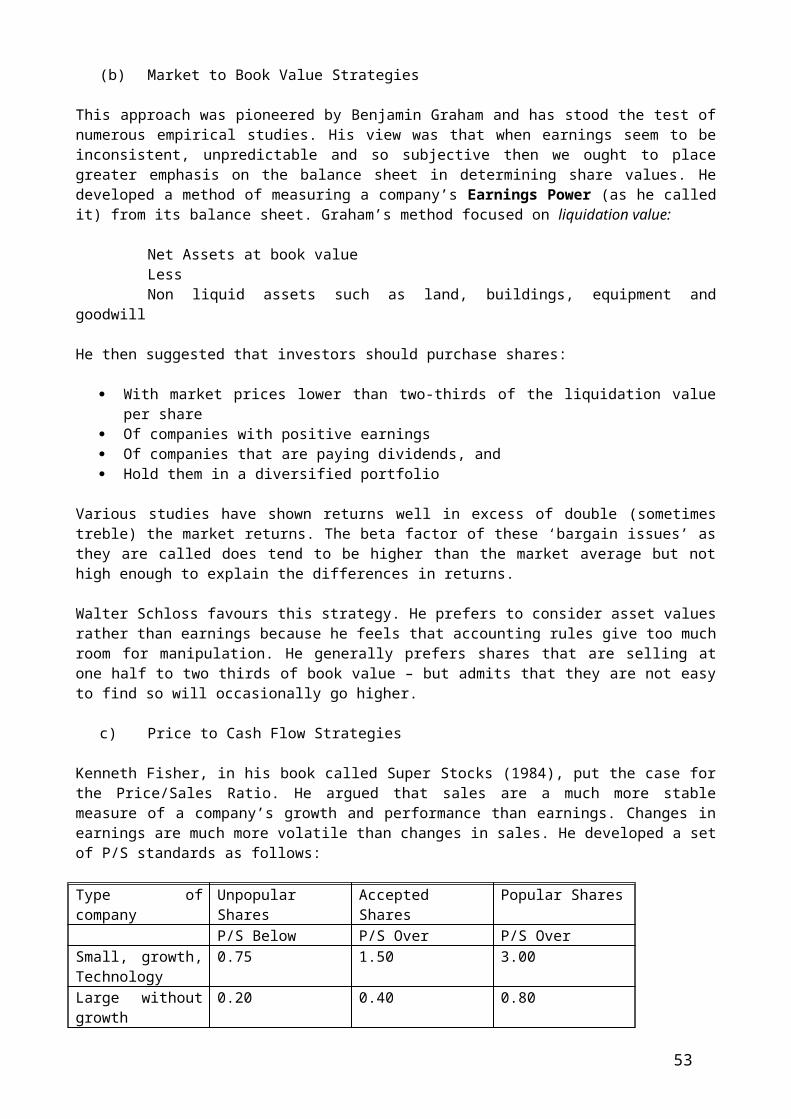

c) Price to Cash Flow Strategies

Kenneth Fisher, in his book called Super Stocks (1984), put the case for the Price/Sales Ratio. He argued that sales are a much more stable measure of a company’s growth and performance than earnings. Changes in earnings are much more volatile than changes in sales. He developed a set of P/S standards as follows:

Type of company Unpopular Shares

Accepted Shares Popular Shares

P/S Below P/S Over P/S OverSmall, growth, Technology

0.75 1.50 3.00

Large without growth

0.20 0.40 0.80

Low margin companies

0.03 0.06 0.12

Source: Fisher, 1984

Banks, securities firms, utilities and other firms whose profits are not based upon sales in the conventional sense could not be evaluated in this way.

Studies have shown that low P/S shares do outperform those with high P/S ratios and, as a strategy does seem to work at least as well as the low P/E strategy. Low p/s shares do seem to have higher betas though and probably the best way to use this measure is to find shares to avoid rather than those to purchase.

James O’Shaughnessy in “What Works on Wall Street” (McGraw-Hill, 1998) showed clearly that stocks with low price/sales ratios outperformed stocks with low P/E multiples.

So how can we explain the fact that the vast majority of fund managers under perform the market?

Possibly the strongest evidence in support of the EMH is the fact that most fund managers fail to do as well as the market. They are, after all, the professionals and do often profess themselves to be ‘value investors’. But study after study shows that most of them (more than 75% in some studies) are regularly beaten by the market.

Perhaps the answer lies in the fact that most fund managers are not actually ‘value investors’ even if they claim to be such. It is often claimed that the city institutions act more like lemmings than individuals driven by their own fundamental beliefs and analysis. It is often claimed that the fear of being seen to have missed an obvious buy or sell signal makes fund managers cautious and conformist. It is argued that on the contrary the true ‘value investor’ is a loner and somebody who goes their own way rather than following the herd.

Anomalies in the Efficient Markets Hypothesis

Many researchers have discovered anomalies in the EMH. Some of these include:

Low-Priced Stocks

43

Low priced stocks seem to out perform higher priced stock

Price-Earnings Ratio Effect

Shares with low P/E ratios tend to out perform shares with higher P/E’s.

January Effect

There is often a marked increase in share prices during January

Within-the-month Effects

Stock prices often tend to rise during the first part of the month – then level out until the end of the month – when they start to rise again.

Sales:Price Effect

It has been shown that the sales per share divided by the share price is a better indicator than the P/E ratio. Seems to be a flaw in the EMH because same sales could be unprofitable

Unsystematic Risk Effects

Some studies show that diversifiable risk does have a significant effect on share prices.

Agency effects

This implies that firms managed by their owners make better investments than firms that are managed by executives who are merely employees.

Effects of Earnings Surprises

This shows that abnormal price variations often occur as a result of financial information that was not anticipated.

Effects of trends in analyst’s earnings forecasts

This suggests that trends identified by analysts can effect share prices.

Effect of an earning ‘torpedo’

This suggests that share prices can sink like a torpedoed ship if worse than expected earnings are announced.

Effects of relative strength

Technical analysis suggests that some shares exhibit relative strength – that they rise faster during bull markets and/or decline slower during bear markets. Several studies have supported this.

Firm’s Size Effects

Small firms tend to earn better rates than larger ones

44

Effect of Neglect

Less popular stocks tend to perform better than well researched stocks.

Day of the week and time of the day effects

Shares tend to rise more on Fridays than on any other day of the week and have risen least often on Mondays. There are a number of times of the day effects – one involves an inordinate number of losses on Monday mornings.

Effects of the Book Value to Price Ratio

Evidence shows that shares having high book values per share relative to their share price tend to perform well. In particular when a share’s price falls below its book value then the share is judged to be a good buy.

Discussion Point:

Why, in spite of all the above anomalies, might the personal investor still be advised to follow the doctrine of the EMH?

Session 6

Management of Bond Portfolios

45

BOND PORTFOLIO MANAGEMENT

What are Bonds?

One way to explain this is to compare them with savings accounts.

Savings Accounts BondsAction Lending Money to Bank,

Building Society etc.Lending Money to Issuer of Bonds e.g. Government, Companies, Local Authorities etc.

Return Interest Interest plus possibility of capital gain or loss

Getting your money back

Withdraw from account (a) sell bond to other investors(b) wait for issuer to ‘redeem’

the bond

Why Invest in Bonds?

There are three main reasons:

The potential for higher returns than those earned on savings accounts The potential for capital gains through:

Falls in interest rates Investing in companies on the road to financial recovery

The ability to reduce UK taxes by investing in Government Bonds (Gilts)

Bond Terminology

Coupon Rate

This is the interest rate that the issuer of the bond promises to pay the bondholder. It must distinguish from Yield, which is described below. The coupon is invariably a fixed rate but it is possible to have bonds with floating (variable) rates of interest.

Par Value

46

The par value of the bond is the face value of a bond (usually £100). It is not necessarily the price at which they may be bought or sold.

Redemption Date

This is the date when the issuer of the bond will repay the par value of the bond.

Market Value

Bonds often trade at prices above or below their par value. A bond with a par value of £100 may trade below that (at a discount) or above (at a premium).

Yield

There are two measures of yield for bonds Flat Yield and Redemption Yield.

Flat Yield (sometimes called just Interest or Running Yield) measures the actual interest earned relative to the actual market price of the bond. If the bond is at par then the Flat Yield and the Coupon Rate will be the same.

Redemption Yield takes into account the flat yield and the fact that there may be a capital gain (or loss) for the investor on redemption of the bond.

Bid price

The bid price is the price that an investor will get if selling a bond

Offer Price

The offer price is the price an investor would have to pay for a bond.

Spread

This is the difference between the bid and offer price. It is the dealer’s profit on bond deals.

What different types of Bonds are available?

There are numerous different issuers of bonds. The following are some examples:

British Government Bonds (Gilts) Local Authority Stocks Corporate Debts

- Debentures- Loan Stocks

Foreign Bonds Eurobonds

In the English language there are many words with different meanings (e.g. return). The word bond is just the same. The following are not bonds in the strictest sense of the word:

Premium Savings Bonds Guaranteed Income Bond Insurance Bonds ( e.g. Property Bonds, Managed Bonds)

47

Building Society Bond Accounts

Mainly because they are not easily tradable, if at all.

British Government Bonds

We will now use British Government Bonds (Gilts) to illustrate the mechanics of investing in Bonds.

Gilts are traded on the Stock Exchange by Gilt Edged Market Makers (GEMMs). They form a very important segment of the business carried out on the exchange as can be illustrated from the figures below:

Indicative Market Values

Gilts £713.3 Billion

Equities £138.9 Billion

Monthly Turnover

Gilts £333.3 Billion

Equities £111.9 Billion (data from London Stock Exchange 6/09)

How are Yields Calculated?

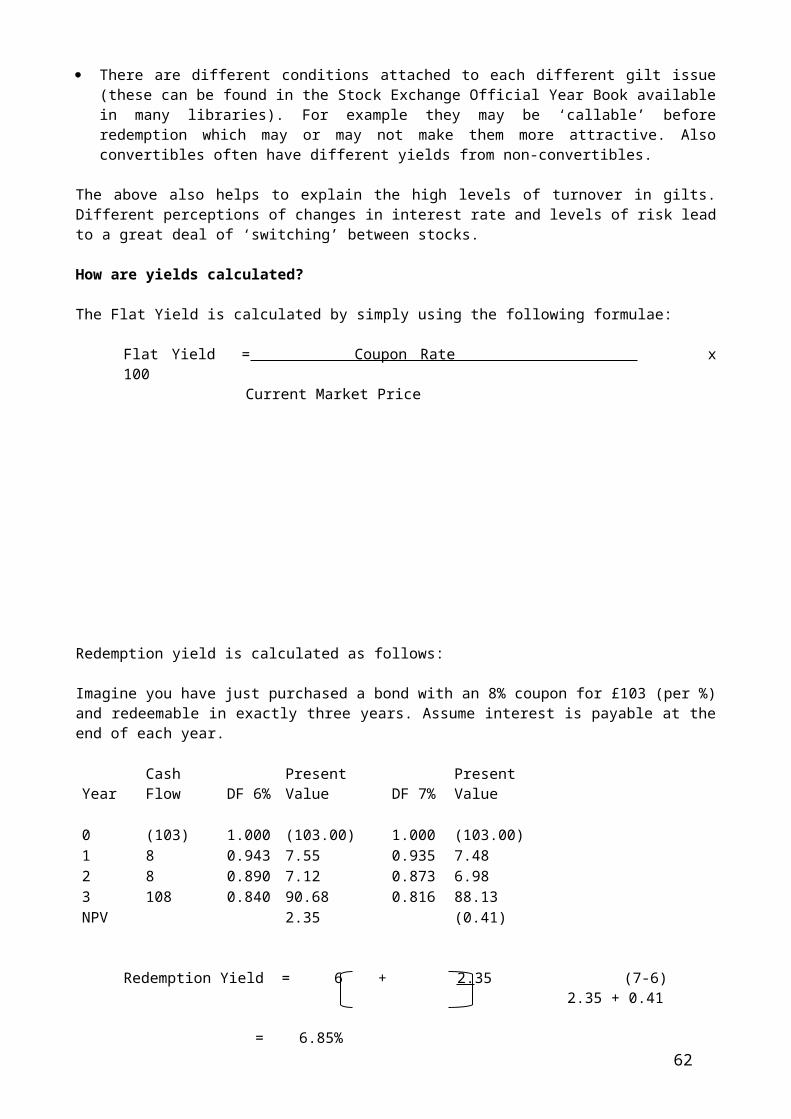

Flat Yield is simply by using the following formula:

Flat Yield = Coupon Rate Current Market Price

Redemption Yield is rather more difficult to calculate. If you have studied accountancy at all you will have come across the concept of Net Present Value and the measure known as Internal Rate of Return (IRR). The Redemption Yield is the IRR of the flow of interest payments and the final redemption payment.

What is the Significance of the Yields?

The flat yield simply informs the investor of the interest return on the stock at the current market price. It ignores the possibility of any capital gain or loss and is therefore a little limited in its use.

The better guide to overall or total return is redemption yield because it takes into account the capital gain or loss if the stock is held to redemption.

48

Exercise:

Calculate the flat yield for the Treasury 8% 2021. Compare this with the coupon rate and the redemption yield for the bond and try to explain the reasons for the differences.

There is no totally satisfactory way of calculating the overall return on a gilt if you do not intend to keep it until maturity because of the impossibility of knowing what gain or loss may be incurred. The best way to avoid the uncertainty is to try to match maturity of the stock you choose to your need for the funds.

What is it that causes the prices of gilts to change?

This happens to all bonds of course, not just gilts. It is basically because the required rate of return on the bonds changes and the only way for this to occur is by a change in the price.

The required rate of return will change for three specific reasons:

A general change in interest rates making the return on the bond look out of line (i.e. unattractive or too high).

The expectations of interest rate changes – the prices of bonds will move in the opposite direction to the expected change in interest rates.

A change in the levels of perceived risk surrounding the bonds.

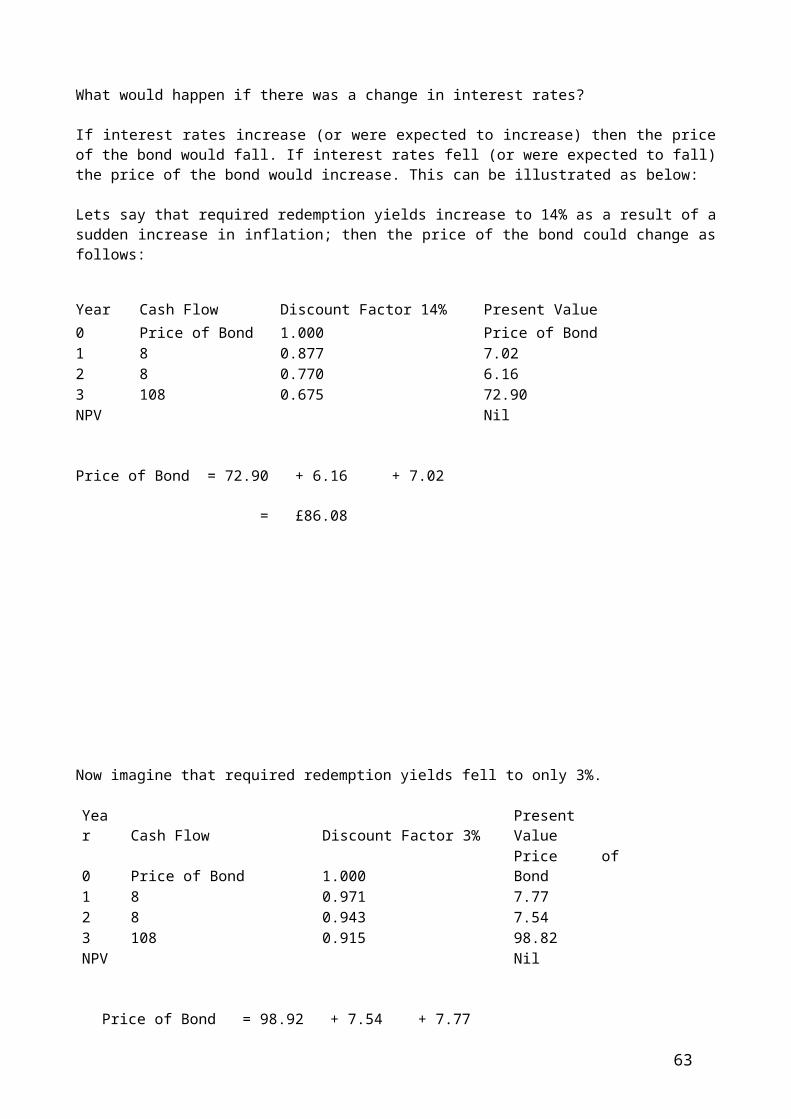

Why are the Redemption Yields on Gilts all different?

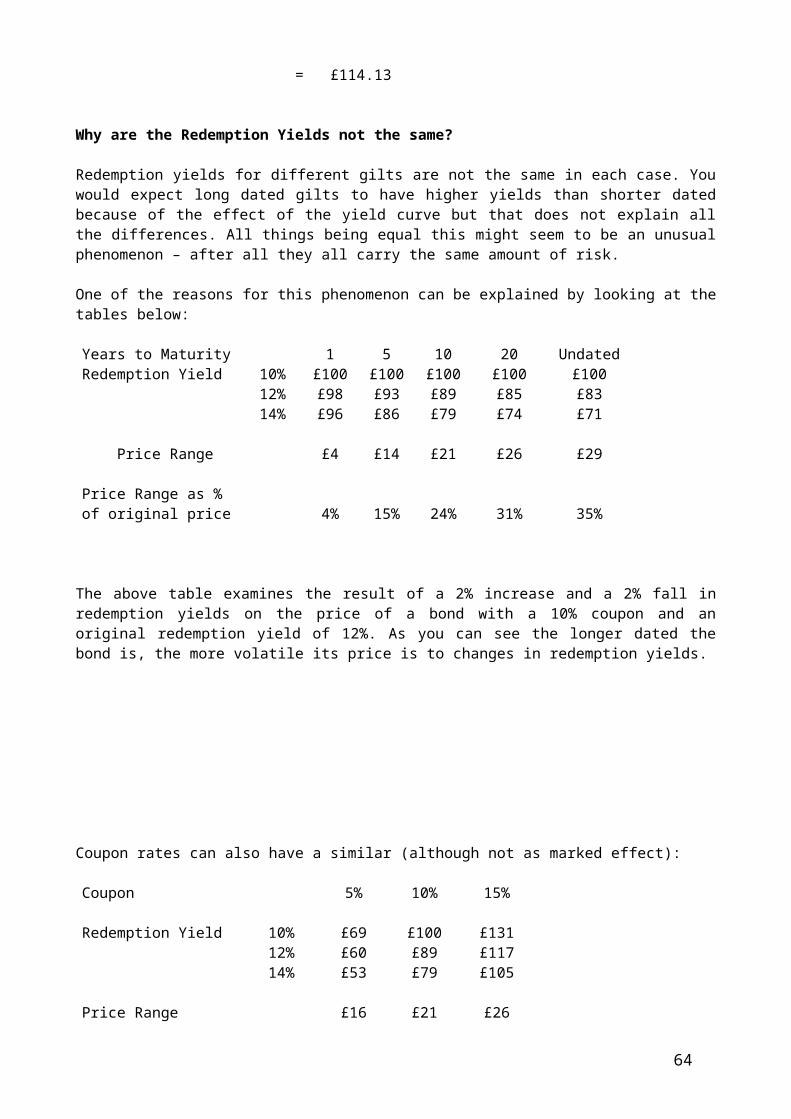

Look down the third column of the extract from the Financial Times and you will see that the redemption yields exhibit a range of values. Wouldn’t you expect them to be all the same? There are at least four basic reasons for the differences:

Long-term interest rates are usually higher than short-term rates for many different reasons.

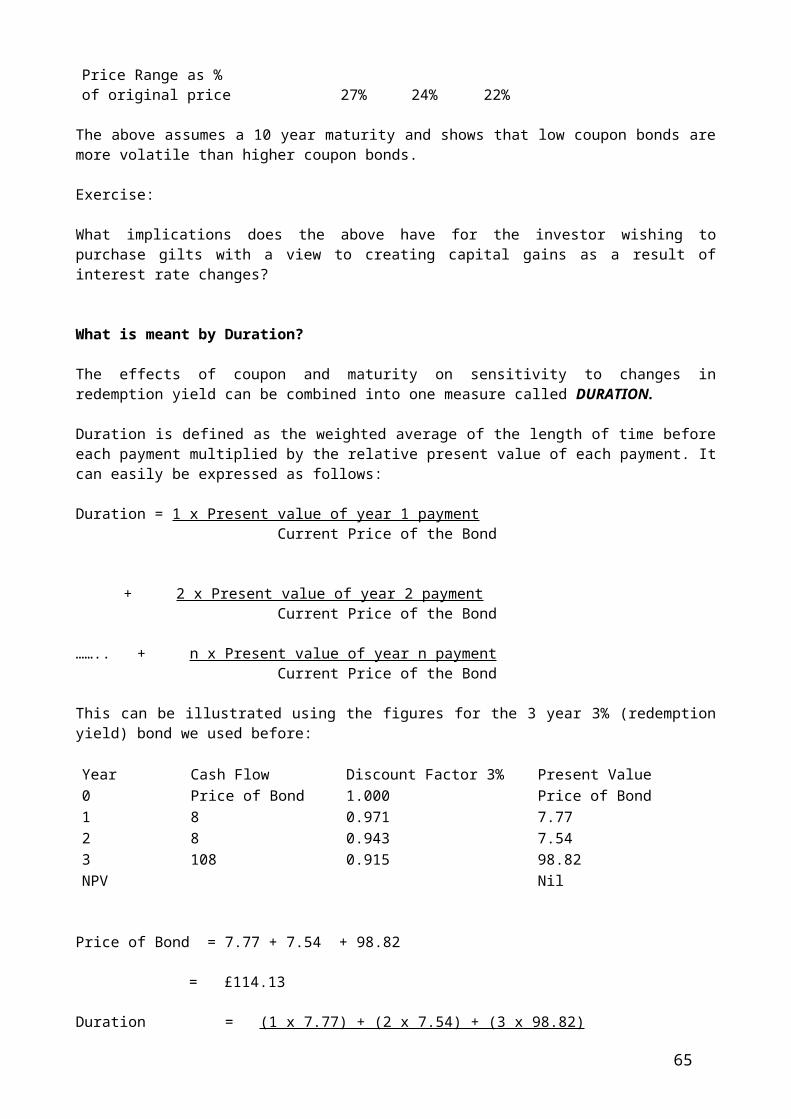

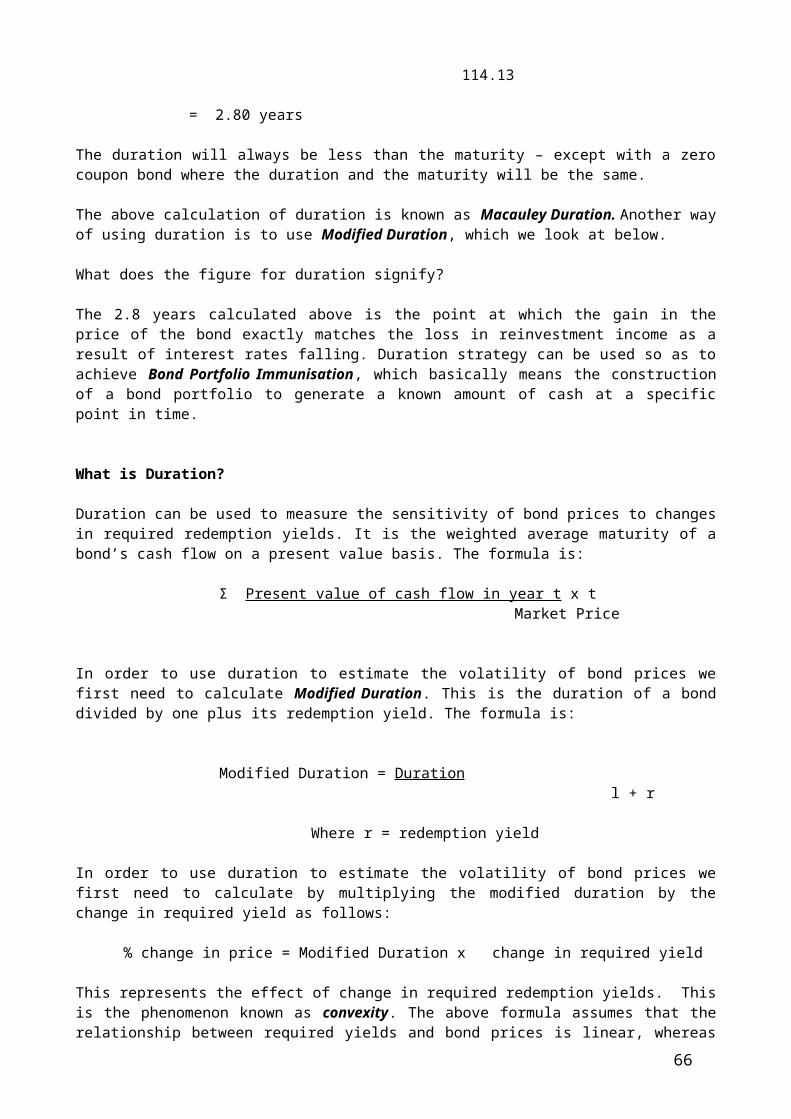

The longer a bond is from redemption the more volatile its price will be. The higher the coupon of a bond the less volatile it will be. This is an arithmetical effect known as Duration.

Low coupon bonds can be more attractive to higher rate taxpayers, which can push their prices up and hence, their yields down.