investment in indonesia what are the upcoming opportunities. energy.27 july2011.jakarta

TRANSCRIPT

Rajat Gupta, Consultant EPS Practice

Pradi Wigianto, Consultant EPS Practice

Investment in Indonesia: What are the upcoming opportunities ?

Investment Opportunities in:

ENERGY

2

Primary Objectives for Utilities by 2020

1. Increase Power Reliability

by minimizing interruptions in power delivery

2. Improve Energy Efficiency

by reducing waste in power delivery and energy losses

3. Accommodate Renewable Power

-

Prevent congestion on the power lines and interruptions

4. Preparing for Growing Power Load

3

Fuel Balance – Today and in 2020

Coal

Oil

Gas

Nuclear

Hydro

Wind

Solar, Other

Renewables

Coal

Oil

Gas

Nuclear

Hydro

Wind

Solar, Other

Renewables

0

5000

10000

15000

20000

25000

30000

2010 2020

Coal

Oil

Gas

Nuclear

Hydro

Wind

Solar, Other

Renewables

Coal

Oil

Gas

Nuclear

Hydro

Wind

Solar, Other

Renewables

0

5000

10000

15000

20000

25000

30000

2010 2020

3%

Coal

Oil

Gas

Nuclear

Hydro

Wind

Solar, Other

Renewables

Coal

Oil

Gas

Nuclear

Hydro

Wind

Solar, Other

Renewables

0

5000

10000

15000

20000

25000

30000

2010 2020

7%

4

2010 2020 2015

Power Demand

Growth

Major

Trend

New Age of

Natural Gas

Renewable Grid

Parity

Clean Coal

Commercia-

lisation

Low demand in West

offset by boom in Middle East

Outlook for the Energy & Power Industry Top 10 World Power & Energy Trends over the Next Decade

Commercial CCS viability established

and large-scale development commences

Big expansion of

electric/hybrid vehicles

World electrification

reaches 80%

Non-OECD countries

Surpass OECD China becomes

largest consumer

CCGT favourite generation technology

Shale gas boom in USA

Growth in World

pipeline network Massive boost in

LNG availability

Gas demand peaks in OECD but

keeps growing elsewhere

Ultrasupercritical technology

becomes prevalent Worldly

Carbon Capture and Storage

Pilot Plants

Solar and wind reach grid parity

in some European markets Grid parity reached in

majority of developed world

Renewables share in power generation

25% Worldwide and 30% in EU

Market

Liberalisation Focus on emerging

markets retail liberalisation

Growing trans-regional

power trading

Most power generation markets

fully liberalised Towards a World

emissions trading system

5

2010 2020 2015 Major

Trend

Energy

Efficiency

Smarter Grids

Demand

Management

Energy Storage

Outlook for the Energy & Power Industry Top 10 World Energy & Water Trends over the Next Decade

World coverage for energy-

efficient lighting

Smart meters

taking off In US

and Europe

Boosting breakthrough

for electric vehicles

Expansion of virtual

power plants

Smart meters reach

most consumers in

developed world

Green buildings become norm

in developed world Grid investments lead to

reduction in T&D losses

Grid-scale energy storage such as

pumped storage and CAES takes off

Improved existing battery technologies emerge

such as Li-ion, Nickel-Zinc, and Molten Salt

World penetration of micro-

renewables and micro-CHP

Direct load control of smart

appliances via remote management

Smart meters optimise consumer

usage patterns and flatten peak demand Peak shaving through energy efficiency

and promotion of embedded generation

6

Electricity consumption in China = 550 billion

kWh in 1990

2008 = 2,200 billion kWh in 2008

Forecast to increase further to 6,000 billion

kWh by 2030.

China’s share of the global market will increase

by a staggering 15% from 5% in 1990 to 20%

in 2030.

Other developing regions also up - rest of

Asia’s up from 13% to 15%, Latin America’s

from 4% to 7% and India’s from 2% to 6%.

Asia-Pacific is likely to witness the largest increase in the Electricity consumption owing to the economic development in countries such as China, India and so on.

Regional Share of Electricity Consumption, 1990

Source: Frost &

Sullivan and EIA.

Regional Share of Electricity Consumption, 2008

Regional Share of Electricity Consumption, 2030

7

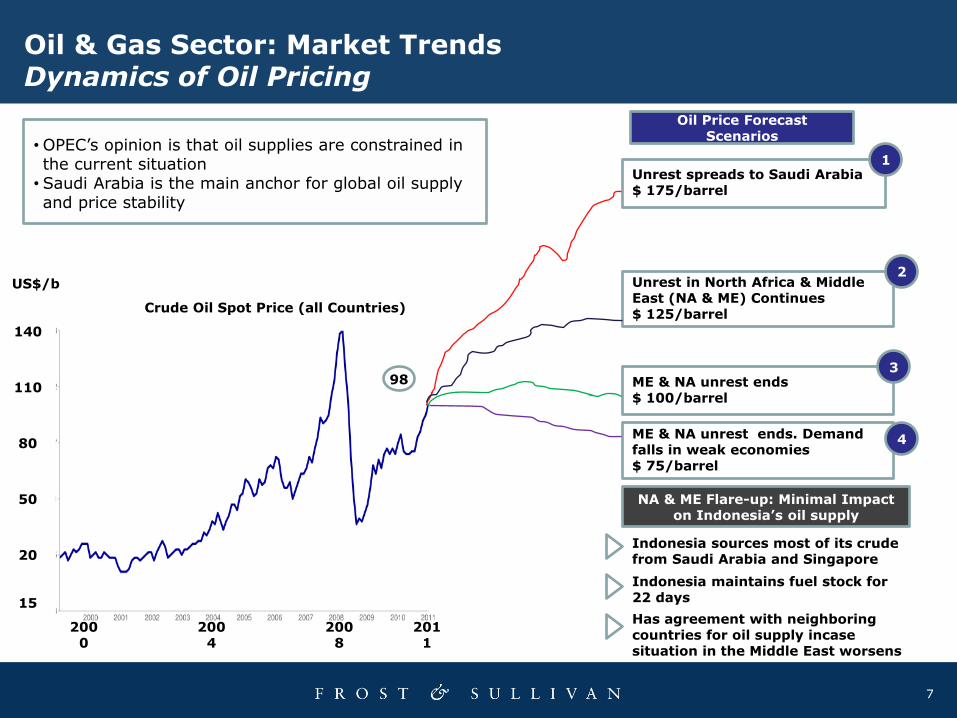

Oil & Gas Sector: Market Trends Dynamics of Oil Pricing

Unrest spreads to Saudi Arabia $ 175/barrel

ME & NA unrest ends $ 100/barrel

Unrest in North Africa & Middle East (NA & ME) Continues $ 125/barrel

•OPEC’s opinion is that oil supplies are constrained in the current situation • Saudi Arabia is the main anchor for global oil supply and price stability

ME & NA unrest ends. Demand falls in weak economies $ 75/barrel

140

110

80

50

20

15

98

Crude Oil Spot Price (all Countries)

2011

2008

2004

2000

Oil Price Forecast Scenarios

1

2

3

4

Indonesia maintains fuel stock for 22 days

Indonesia sources most of its crude from Saudi Arabia and Singapore

Has agreement with neighboring countries for oil supply incase situation in the Middle East worsens

NA & ME Flare-up: Minimal Impact on Indonesia’s oil supply

US$/b

8

Oil & Gas Sector: Market Trends Major Emerging Trends

Key Trend 1: Strong Demand Driving Prices Up

Middle East & North Africa unrest impacts supply and adds to speculation

Japan catastrophe to increase gas demand

Strong Demand from Asia

Shallow-water & Mature Onshore Fields Depleting

Domestic Demand Versus Import Commitments

Need to increase exploration efforts and work mature fields harder

Crude oil prices increase driving up subsidy bill

Indonesia

9 Source: Compiled by Frost & Sullivan

The gas reserves in relation to the size of the individual fields

There are around 6000 fields with reserves less than 5 trillion cubic feet (TCF). Most of them are considered stranded fields Stranded gas reserves refer to the natural gas, which have been discovered but cannot be developed due to their location disadvantage or negative economics of getting the natural gas delivered to the marketplace About 40% of global natural gas reserves are located far from the shores and are classified as stranded

• Floating LNG Terminals (FLNG) can monetize stranded reserves held in over 2500 gas fields containing 0.1 to 5 trillion TCF

Indonesia has identified 52 marginal fields (oil & gas) for development

Oil & Gas Sector: Market Trends Major Emerging Trends

Key Trend 2: The development of marginal fields

10

Source: Lambert Energy Advisory

Coal-Bed Methane (CBM) Potential, barrels of oil

equivalent

Shale Gas Potential, barrels of oil equivalent

US Shale Gas 100bn

US CBM 15bn+

Latin America Shale Gas 50-100bn

China Shale Gas 50-100bn

Europe Shale Gas 90bn Canada Shale Gas

20bn+

China CBM 75bn

Indonesia CBM 75bn

Australia CBM 40bn

Outlook for the Energy & Power Industry: Unconventional Gas World Hotspot (World), 2010

Outlook for the Energy & Power Industry Growth of Unconventional Gas

Outlook for Opportunities in Indonesia – Conventional Energy

Indonesia in the Global Context – Conventional Energy

Table of Contents – Conventional Energy

Contents

1

2

12

Key Opportunities in Indonesia

Sector Growth Commercial

Viability Time Frame

High Opportunity

Application

Coal VERY HIGH VERY HIGH NOW Production, CBM, CTL

and coal to gas

Natural Gas VERY HIGH HIGH NOW Exploration, production

FPSO and FSRU

LNG VERY HIGH HIGH NOW LNG plants

development, tankers

Oil HIGH VERY HIGH NOW Exploration and

production

Source: Frost & Sullivan analysis.

13

Opportunity Assessment – Energy Sector

Source: Frost & Sullivan analysis.

Sector Growth Commercial

potential Time Frame

High Opportunity Application

Electricity Power infrastructure

VERY HIGH HIGH NOW Gas and Coal

Gas Infrastructure and services

HIGH HIGH Next 1 – 3 years FPSO, FLNG, FSRT

Coal development HIGH HIGH NOW Low Calorie coal is rising

Oil Infrastructure and services

HIGH HIGH NOW Production equipment

Pipeline HIGH HIGH NOW Intercity gas distribution network

Brownfield services MODERATE to

HIGH MODERATE NOW Old oilfields

Fuel Infrastructure MODERATE MODERATE NOW Fuel station

Refinery facilities MODERATE HIGH NOW LPG and fuel

Drilling rigs MEDIUM HIGH Next 1 – 2 years Oil, Gas, CBM and geothermal

Decommissioning Services

Low MODERATE Next 3 – 5 years A lot of Indonesian oil gas

field are old fields with aging rigs and equipment

14

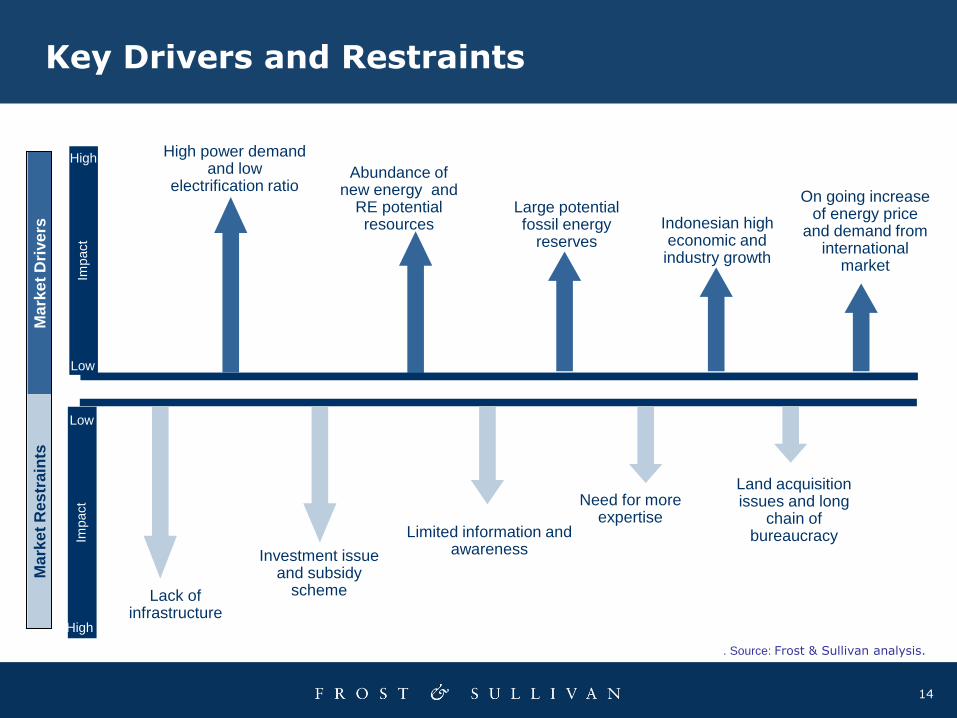

Key Drivers and Restraints Im

pact

Ma

rke

t D

rive

rs

Ma

rke

t R

es

train

ts

Impact

High power demand and low

electrification ratio Abundance of

new energy and RE potential resources

Investment issue and subsidy

scheme

Limited information and awareness

Lack of infrastructure

Low

High

High

Need for more expertise

Land acquisition issues and long

chain of bureaucracy

Large potential fossil energy

reserves Indonesian high economic and industry growth

On going increase of energy price

and demand from international

market

. Source: Frost & Sullivan analysis.

Low

15

Oil Energy Sector

Growth Potential 2011

0

1

2 3

4

5

5.0

1-2 Years 3-6 Years 7-10 Years

High

Growth

Medium

Growth

Low

Growth

• High power demand

• Industrial and automotive growth

• Conventional sources

Growth Factor

• Oil field exploration and production activities

• Oil production service provider

• Midstream and downstream sector

Opportunities

Source: Frost & Sullivan analysis.

16

Gas Energy Sector

Growth Potential 2011

0

1

2 3

4

5

5.0

1-2 Years 3-6 Years 7-10 Years

High

Growth

Medium

Growth

Low

Growth

• High power demand

• Industrial and automotive growth

• Decrease in oil production

Growth Factor

• Gas field exploration and production activities

• Gas production service provider

• CNG, LPG and LNG plant development

Opportunities

Source: Frost & Sullivan analysis.

17

Coal Energy Sector

Growth Potential 2011

0

1

2 3

4

5

5.0

1-2 Years 3-6 Years 7-10 Years

High

Growth

Medium

Growth

Low

Growth

• High power demand

• Industrial and automotive growth

• Decrease in oil production

Growth Factor

• Coal field exploration and production activities

• Coal production service provider

• Coal power plant development

Opportunities

Source: Frost & Sullivan analysis.

Indonesia in the Global Context – Conventional Energy

Outlook for Opportunities in Indonesia – Conventional Energy

Table of Contents – Conventional Energy

Contents

2

1

19 Source: Compiled by Frost & Sullivan

Exploration & Development

Refining

Downstream

Distribution

Oil & Gas Sector – Opportunities across the value

chain

Upstream

Production

Rejuvenate Brown Fields

Step Up Exploration

Efforts

Increase Refining Capacity

Phase Out Subsidies

Bring Projects

Onstream as Scheduled

Development of Marginal

Fields

Upgrade Existing Facilities

Strengthen Domestic Gas

Network Infrastructure

• Investment in Petroleum, CBM and Shale Gas acreages •Marginal field development

• FPSO • FLNG •Marine Support Vessels

• Brownfield services •Decommissioning Services

• Refinery products and services • Project investment

•Gas Network Infrastructure

• Retail Infrastructure for non-subsidised fuel • Addition of gasoline retail stations

Action I

tem

s

Opport

unitie

s

20

Environmental Impact Controversies

Restraining Growth of the Industry

Coal Seam Gas (CSG)/CBM to LNG

Projects

Commercial production of CBM is still at a nascent stage in Indonesia • The total CBM reserves in Indonesia is estimated to be 450 TCF • This is more than double its natural gas reserves and the world's second largest CBM reserves after

China. • At least 10 percent of these reserves can be extracted economically

Production Start-up in 2011; to be supplied to domestic power plants • By 2015, Indonesia’s total production of unconventional gas to reach 100 million cubic feet per day • By 2020, unconventional gas production to reach 500 million cubic feet per day • Unconventional gas and CBM are expected to account for 30.0 percent of Indonesia’s energy mix in

2025

Oil & Gas Sector: Unconventional Gas is set to emerge

as a viable option

Shale Gas Exploitation is a Possibility • Indonesia is estimated to have shale gas reserves of 1000 TCF • Shale gas can be produced in Indonesia by 2018 provided right steps are taken for harnessing this

energy resource.

21

Oil & Gas Sector: Exploration and Production Continue to remain a massive investment area

Tril

lio

n C

ub

ic

Mete

rs

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2002 2003 2004 2005 2006 2007 2008 2009 2010

Oil Proved Reserves

Th

ou

san

d M

illio

n

Barrels

•More gas provinces to increase proven natural gas reserves • Unconventional gas to add to reserves •More investments in gas projects

• Falling Oil Reserves •Oil projects are more complex now

Total Upstream Exploration & Production Expenditure in Indonesia for 2011 is forecast to be US$ 17 billion. 1TCM=35.3TCF

22

Oil & Gas Sector: Offshore opportunities

Deepwater Potential: Tarakan basin; Papalan Basin

Thrust from Government for faster development of gas projects for

meeting domestic and export gas demand

East Kalimantan

Masela Block

10 TCF Reserves; water

depth 300m to 1000m

Inpex to invest $ 4.9 billion

For floating LNG plant (2.5

mmtpa) with production

start-up in 2016

Makassar Strait

Gehem, Gendalo, Gandang, Maha and Bangka fields

Chevron to developing East Kalimantan deepwater fields,

Gehem and Gendalo.

Invest ment $ 7 to 8 billion.

Plan Of Development approved

Source: Planning Dept, Govt of Indonesia; Petroleum Geo-Services ;

Compiled by Frost & Sullivan

Shallow Water

• Terang/Sirasun FPSO (TSB),

• Pagerungan

• Madura

• Kakap Natuna

• Bukit Tua

Deep Water

• Gehem

• Gendalo

• INPEX Masela FLNG

• Petramina FSRU

Prospective FPSO Projects

23

Location : Jakarta Bay, West Java Start up plan : 2012 Capacity : 3 MTPA Contractor : Golar LNG Energy

Location : East Java Start up plan : 2013-14 Capacity : 2-4 MTPA

Location : Belawan, North Sumatra Start up plan : 2013-14 Capacity : 3 MTPA

Oil & Gas Sector : Floating Storage Re-gas Storage Units (FSRU) Projects

24

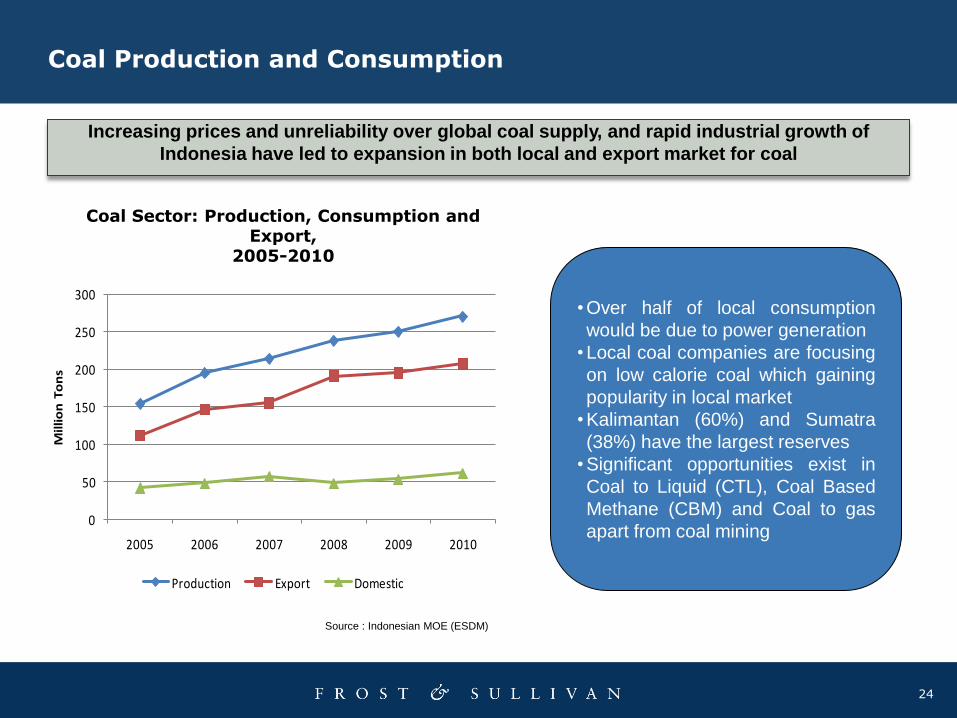

Coal Production and Consumption

Source : Indonesian MOE (ESDM)

0

50

100

150

200

250

300

2005 2006 2007 2008 2009 2010

Mil

lio

n T

on

s

Production Export Domestic

Coal Sector: Production, Consumption and Export,

2005-2010

Increasing prices and unreliability over global coal supply, and rapid industrial growth of

Indonesia have led to expansion in both local and export market for coal

•Over half of local consumption

would be due to power generation

•Local coal companies are focusing

on low calorie coal which gaining

popularity in local market

•Kalimantan (60%) and Sumatra

(38%) have the largest reserves

•Significant opportunities exist in

Coal to Liquid (CTL), Coal Based

Methane (CBM) and Coal to gas

apart from coal mining

25

Summary

3 Oil based power generating plants are likely to be replaced by energy efficient gas fired or coal fired power plants based on sub/super critical technology in the long term.

4 Unconventional gas especially CBM and shale gas will increasingly become popular to satiate energy needs.

2 Growth opportunities are expected to be very high in the following sectors – natural gas, LNG, and coal throughout the forecast period to meet the rapidly growing domestic energy needs and export market demand.

1 New investments is the key to sustain Indonesia energy security. Decreasing production of energy is happening in Indonesia due to the decrease of investment.

Outlook for Opportunities in Indonesia – New and renewable energy

Indonesia in the Global Context – New and renewable energy

Table of Contents – New and Renewable Energy

Contents

1

2

27

Indonesia Power Sector – An Overview

Source: Frost & Sullivan analysis.

Installed Capacity Forecast, 2010 and 2030

Indonesia

2010 2030

Total Installed Capacity (GW)

40 110

PT PLN Ownership 75.0% 60.0%

IPP Ownership 25.0% 40.0%

Demand (GW) 60 120 0

20

40

60

80

100

120

140

2010 2030

Total Installed Capacity (GW) Demand (GW)

Installed Capacity Forecast, 2010 and 2030

Indonesia

• Oil dominates the country’s energy mix. Oil reserves are depleting, although gas and coal reserves have been

increasing.

• Part of energy prices are still subsidized which burdens the state budget and interferes the development of alternative

energy.

• Electrification ratio was about 66.0% in 2008, increased to 72.0% in 2010 and is expected to reach 80.0% by 2014.

• Total installed power capacity is 40,000 MW in 2010; nearly 75.0% percent of the country’s installed base is run buy

PLN and its subsidiaries, IPP accounts the rest of 25.0%.

28

Renewable Energy Potential in Indonesia

Renewable Energy Type Potential Resources Installed Capacity Underdeveloped Potential

Geothermal 28534 MW 1189 MW 92.5%

Hydro 75670 MW 5705.29 MW 95.80%

Mini / Micro Hydro 769.69 MW 217.89 MW 71.70%

Biomass 49810 MW 1618.40 MW 96.80%

Solar 4.8 kWh / m2 / day 13.5 MWp 99%

Wind 3 - 6 m/s 1.87 MW 99%

Uranium 3000 MWt 30 MWt 100%

Source: MOE ESDM, US Department of Commerce obtained from PLN

29

Key Opportunities in Indonesia

Sector Relevance Commercial

Viability Time Frame

High Opportunity

Application

Bioenergy VERY HIGH HIGH NOW Biomass, Biogas and

Biofuel

Geothermal VERY HIGH HIGH NOW On grid applications

Hydro Power VERY HIGH MODERATE NOW Large and Mini Hydro

Waste to Energy HIGH MODERATE Next 3-5 years Municipal and Industrial

waste to energy

Solar PV HIGH LOW Next 3-7 years Rural offgrid

applications

Wind Power MODERATE MODERATE Next 4-8 years

Small capacity wind

farms and potential

offshore

Nuclear Power MODERATE LOW Next 15 - 20 years Utility scale power plant

Source: Frost & Sullivan analysis.

30

Opportunity Assessment – Key Products

Equipment Growth Commercial potential Time Frame

High Opportunity

Application

Electricity Meters VERY HIGH MODERATE NOW Last mile meters especially in

rural areas

Cable & Wire HIGH HIGH NOW Will be mostly MV and LV

cables

Transformer HIGH HIGH NOW Transformer needs for MV

group

CBM and Shale Gas development

MODERATE HIGH Next 2 – 3 years Specialized production

equipment

Geothermal MODERATE HIGH NOW Specialized tools and

equipment

Boilers, heat exchangers, turbines and

related auxiliary equipment

MODERATE HIGH NOW Rural offgrid applications

Drilling rigs MODERATE HIGH Next 1 – 2 years CBM and geothermal

Battery LOW MODERATE Next 3 – 7 years For renewable energy source

power production and EV car

Power Storage LOW MODERATE Next 3 – 7 years For renewable energy source

power production

Solar Cell LOW MODERATE Next 2 – 5 years In rural marginal area

Wind Blade LOW MODERATE Next 5 - 10 years In rural marginal area

31

Geothermal Energy Sector

Growth Potential 2011

0

1

2 3

4

5

3.0

1-2 Years 3-6 Years 7-10 Years

High

Growth

Medium

Growth

Low

Growth

• High demand new and renewable energy for national power security

• Investment in geothermal exploration and production

• The second biggest geothermal sourcing

Growth Factor

• Geothermal field exploration and production activities

• Geothermal production service provider

• Geothermal power plant development

Opportunities

Source: Frost & Sullivan analysis.

32

Bioenergy Sector

Growth Potential 2011

0

1

2 3

4

5

2.5

1-2 Years 3-6 Years 7-10 Years

High

Growth

Medium

Growth

Low

Growth

• High demand new and renewable energy for national power security

• Investment in biofuel

• Investment in biomass power production facilities

• Petroleum reserves is depleting

Growth Factor

• Biomass power electricity production development

• Biofuel plant

• Biofuel transportation technology

• Biomass energy source production (e.g waste processing plant)

• Biomass and biofuel tools and equipment

Opportunities

Source: Frost & Sullivan analysis.

33

Hydropower Sector

Growth Potential 2011

0

1

2 3

4

5

2.5

1-2 Years 3-6 Years 7-10 Years

High

Growth

Medium

Growth

Low

Growth

• High demand new and renewable energy for national power security

• Investment in hydro and micro hydro power plant

• The biggest power energy source potential in Indonesia

Growth Factor

• Hydro power plant development

• Equipment and service in hydro power plant

• Micro hydro power plant is the most popular for hydro energy source

Opportunities

Source: Frost & Sullivan analysis.

34

CBM Sector

Growth Potential 2011

0

1

2 3

4

5

2.0

1-2 Years 3-6 Years 7-10 Years

High

Growth

Medium

Growth

Low

Growth

• The third biggest resources in the world

• Investment in CBM field production

• New source of energy for Indonesia

• Multi used as power source and LNG

Growth Factor

• CBM field exploration and production activities

• Starting of CBM production in 2012 will need CBM specialized tools and equipment

• CBM production service provider

• Additional LNG facilities to convert CBM to LNG

Opportunities

Source: Frost & Sullivan analysis.

35

Solar Energy Sector

Growth Potential 2011

0

1

2 3

4

5

1.0

1-2 Years 3-6 Years 7-10 Years

High

Growth

Medium

Growth

Low

Growth

• High demand new and renewable energy for national power security

• Investment in solar energy power source

• High potential in solar source

Growth Factor

• Solar PV equipment (solar cell, battery and power storage) producer and provider

• Solar PV equipment service maintenance provider

• Solar energy for power electricity investment

Opportunities

Source: Frost & Sullivan analysis.

36

Wind Energy Sector

Growth Potential 2011

0

1

2 3

4

5

0.5

1-2 Years 3-6 Years 7-10 Years

High

Growth

Medium

Growth

Low

Growth

• High demand new and renewable energy for national power security

• High domestic demand for power electricity

• Investment in wind energy power production

Growth Factor

• Wind energy equipment (blade, battery and power storage) producer and provider

• Wind energy equipment service maintenance provider

• Wind energy for power electricity investment

Opportunities

Source: Frost & Sullivan analysis.

37

Key Drivers and Restraints Im

pact

Ma

rke

t D

rive

rs

Ma

rke

t R

es

train

ts

Impact

High power demand and low

electrification ratio Abundance of

new energy and RE potential resources

Investment issue and subsidy

scheme

Limited information and awareness

Lack of infrastructure

Low

High

High

Need for more expertise

Land acquisition issues and long

chain of bureaucracy

Large potential fossil energy

reserves Indonesian high economic and industry growth

On going increase of energy price

and demand from international

market

. Source: Frost & Sullivan analysis.

Low

Outlook for Opportunities in Indonesia – New and renewable energy

Indonesia in the Global Context – New and renewable energy

Table of Contents – New and Renewable Energy

Contents

1

2

39

Indonesia Power Sector – Opportunities across the value chain

Source: Compiled by Frost & Sullivan

Transmission Generation

Increase electrification

ratio

Diversify fuel mix

Promote energy

efficiency

Demand management

Increase power supply

reliability

Ensure long term power

security

Customer satisfaction

• Investment in renewable energy •Geothermal and biomass to be the key sourced of renewable energy

• Focus on coal based power generation • Increase in coal mining • Hydro power

• Increase in T&D infrastructure

•Grid automation

• Smart metering/Remote meter reading

Action I

tem

s

Opport

unitie

s

Distribution

• Upgrade and maintenance of existing network

• Utility process automation

•Distribution infrastructure

40

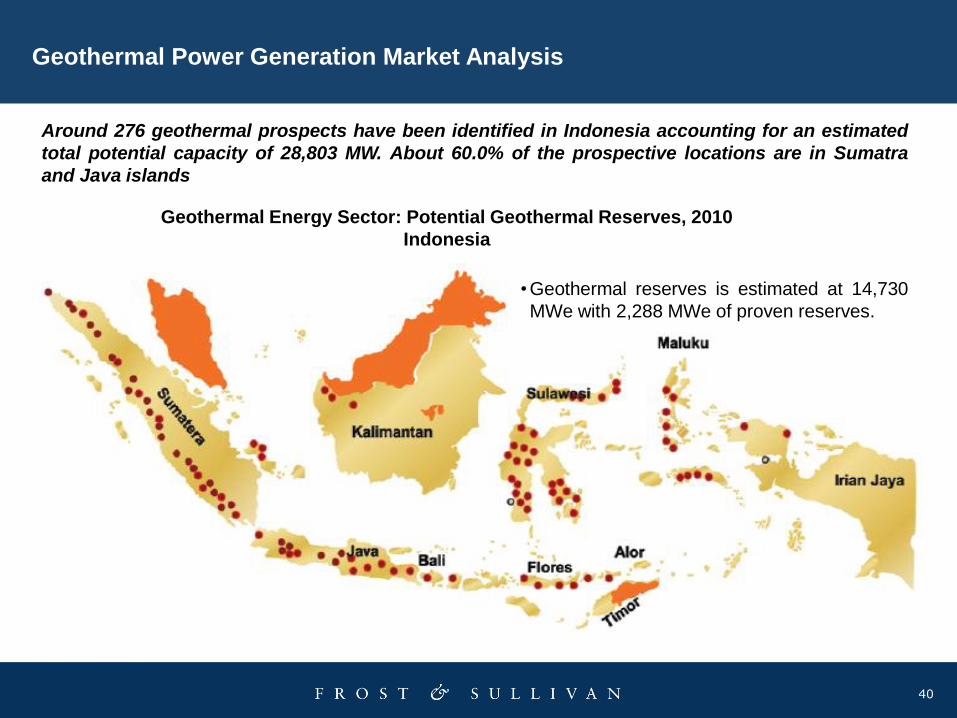

Around 276 geothermal prospects have been identified in Indonesia accounting for an estimated

total potential capacity of 28,803 MW. About 60.0% of the prospective locations are in Sumatra

and Java islands

Source: MOE (ESDM)

•Geothermal reserves is estimated at 14,730

MWe with 2,288 MWe of proven reserves.

Geothermal Energy Sector: Potential Geothermal Reserves, 2010

Indonesia

Geothermal Power Generation Market Analysis

41

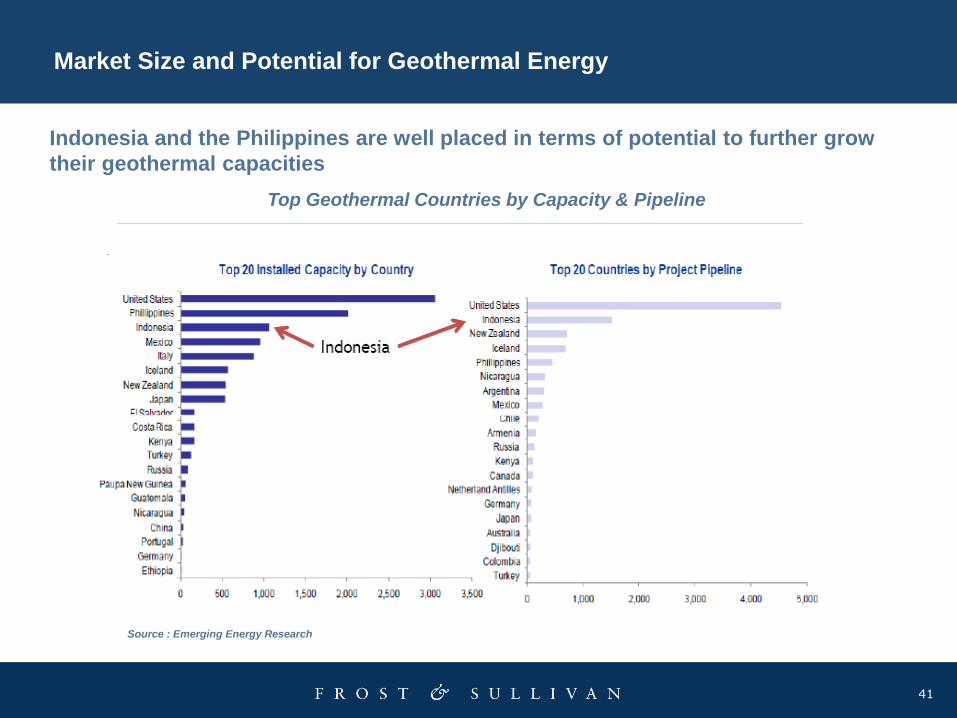

Indonesia and the Philippines are well placed in terms of potential to further grow

their geothermal capacities

Market Size and Potential for Geothermal Energy

Top Geothermal Countries by Capacity & Pipeline

Source : Emerging Energy Research

42

Summary

3 Feed in Tariff in power purchase agreement will become the most important factor

4 Geothermal and Biomass will be the key for short term investment. Hydropower will included for midterm investment. Whilst Solar, Wind and other source of RE will be the longer term investment

2 New and renewable energy will start to developed as government put their focus in this sector. Policies and incentives will boost the development of these energy sources.

1 The key in choosing investment in renewable energy sector will be eyeing the government focus in power infrastructure

Thank You

44

About Frost & Sullivan

Frost & Sullivan, the Growth Partnership Company, enables clients to accelerate growth and achieve best-in-class positions in growth, innovation and leadership. The company's Growth Partnership Service provides the CEO and the CEO's Growth Team with disciplined research and best-practice models to drive the generation, evaluation, and implementation of powerful growth strategies. Frost & Sullivan leverages 50 years of experience in partnering with Global 1000 companies, emerging businesses and the investment community from more than 40 offices on six continents. To join our Growth Partnership, please visit http://www.frost.com

Dewi Nuraini

Corporate Communications, Frost & Sullivan

Phone : (+6221) 571.0838 / 571.3246

Email : [email protected]

http://www.facebook.com/pages/Frost-Sullivan/

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

http://twitter.com/frost_sullivan

http://twitter.com/FROST_ID

About Frost & Sullivan