lessons from the semiconductor industry

TRANSCRIPT

Fachartikel

Sinee Mareh of2001, Wolfram Irsa has held Industrial Engineeringresponsibility for Business Unit Emerging Businesses at PHILIPSSemieonduetors in San lose, California. For two years prior to that, he workedin Supply Chain Management at PHILIPS Semieonduetors in Hamburg,Germany. Other positions at Philips have included Business Line Identifieationin Gratkorn, Austria. He holds a Master of Seienee degree in IndustrialEngineering from the University ofGraz.Further he holds eertifieations ofAPICS in Integrated Resouree Managementand Production and Inventory Contro/. He teaehes Supply Chain Managementclasses for APICS sinee spring 2002. He is the past-president of the loealToastmaster club.

Lessons from the Semiconductor Industry -Supply Chain Management in a dynamic environment

Semiconductor Marltet in Billion cf US Dollars

International Sematech SemiconductorLogistics Forum 2002

Semicondudor Industry - Facts and FiguresIn 2002, semiconductor sales were $ 155billion on 322 billion units shipped.These numbers sharply decreased fromthe 2000 boom year with $ 220 billionon 453 billion units shipped. Exhibit 1shows the revenue roller coaster of thesemiconductor market from 1998 to2002; Exhibit 2 holds the top10 ranking of 2002.

Supplier 2002 sales$ 23.47 billion$ 9.18 billion$6.31 billion$ 6.20 billion$ 6.19 billion$ 5.36 billion$ 5.26 billion$ 4.73 billion$ 4.36 billion$ 4.05 billion

Exhibit 2

Top 10 Chip Suppliers in 2002[Source: WSTS]2002 rank1 Intel2 Samsung3 STMicro4 Texas Instruments5 Toshiba6 Infineon7 NEC8 Motorola9 Philips10 Hitachi

The industry experienced double-digitgrowth rates in 1999 and 2000. Afterthe drop in 2001 the industry is back tothe level of 1999. The major players arestrengthening their positions for the nextup-turn. The dominance of Intel is quitestriking; Intel revenue is 2.6 times higherthan ehe revenue of the following com-

200220012000.."....Exhibit 1

ReferenceAPICS CPIM (Certification in Production and Inventory Management):Master Planning of Re ourcesIn titute of Business Foreca tingSupply Chain Management, Arizona

tate UniversityStanford Global Supply Chain Management Forum

IntroductionHigh-value products that quickly become obsolete, a far-f1ung manufacturing network, rapidly declining prices,and adernanding customer base. Thesupply chain challenges facing the semiconductor industry are complex. Burthey are not necessarily unique. In factmany companies will experience thesevery same challenges (if they haven'talready). Here are three valuable lessonsfrom the semiconductor industry.

11 \\' WING-business 35 (2003) 3

Fachartikel

pany Samsung. The Topl0 Semiconductor companies account for 48% ofthe total market.

The Operating EnvironmentSemiconductor products are a fundamental building block of the information economy. Chips are smalI, extremeIy valuable, quick to become obsolete,and globally produced and distributed.Customers measure product life cydes inmonths. Inventory is precious early in aproduct's life cyde but its contributionto profit can drop by 80 percent in ayear. The essence of the business isMoore's Law - that is, every 18 monthsperformance capabilities double, puningcontinuous pressure on prices for olderchips.(Gordon Moore was a co-founder ofIntel Inc, Santa Clara, California; the'Law' is actually an observation thatproved to be astonishingly accurate forthe last 20 years and seems to continuevalid for at least another 10 years.)Faced with an absolute need for speed,chip manufacturers use airfreight as thedefault transportation mode, exceptwhere surface delivery is as fast or faster.Shipping across oceans, accommodatingextraordinary growth, and supplyingkey customers overnight are routinechallenges in the high-technology worldof semiconductor logistics. Exhibit 3shows the complex supply chain in semjconductors.

The lead-time from the start of the waferto finally distributing the chip to thecustomer is typically 9 to 13 weeks. Thedynamics within this long lead-timeneeds to be managed carefully to utilizethe very expensive - a state-of-the-artwafer fab costs $ 2 Billion - assets asgood as possible. A modern semiconducror operation needs at least 70% utiIization of its equipment to be profitable.

The operating environment for semiconductor logistics is influenced by threeelements:• the increasing level of customer expectations• the dispersed nature of the manufacturing nerwork,• and the sky-high costs of the operation as weil as the inventory.

Understanding the interplay betweenthese factors is fundamental to graspingthe problems and potential of supplychain management for semiconductormanufacturers.

Lesson 1: Keep the inventory upstream aslong as possible

In order to guarantee effective inventoryand asset management follow a simplerule: Don't make what the cu tomerdoesn't need. In a day-to-day operation

this means that only material gets started when a firm customer order is placed. This type of operation is called'Make-to-Order' .

evertheless in some instances, e.g. forhigh-volume products with steadydemand the type of operation can shiftinto 'Make-to-Stock'. Exhibit 4 showsthe major difference of these two concepts.

Make-to-Stock and Make-to-order

MTSSales forecasts are entered formake-to-stock products

D,lIerences be'ween 5 l4'P Iyard demaro IltslAt lnchangesin InYentory Iewl

MTOCustomer orders are enteredfo< make-to-order prodccts

Doflererces belween s_'yand demard resut In chargesIn baddog "''''''

--- 11

The further down the supply chain thematerial moves the less opportunityexists to change.And because every added value step inthe operation means substantial coststhe work-in-progress material - in abroader sense the inventory - is kept as longas possible upstream in the supply chain.

Certainly this implies that as soon a afirm demand need to be supplied theoperation executes as fast as possible tosatisfy customer expectations.

Semiconductor IndustryAGIobai, Complex Supply Chain

xfab

6 WeeksL S, \

Exhibit 3

Wafer Move Assembletest

1 Week 1 Week 1 Week

---

• Long lead limes• Chains of capacity

Final Distributetest

1 Week 1 \oI'kek

/

c

SToME:R

Some tailored programs with customerskeep inventory in the middle of the supply chain. The manufacruring process isthen completed when orders are received. This approach shortens the delivery lead-time by roughly 7 weeks. Theterm for this concept is called 'Assembleto-Order'.

Lesson 2: Treat customers unequally

Although it is important to provide aconsistent service to each customer, it isnot necessarily required or practical topresent the same service to all. Somehigh-volume, high-margin customer willneed a doser relationship, while some

~. WING-business 35 (2003) 3 __ I

Fachartikel

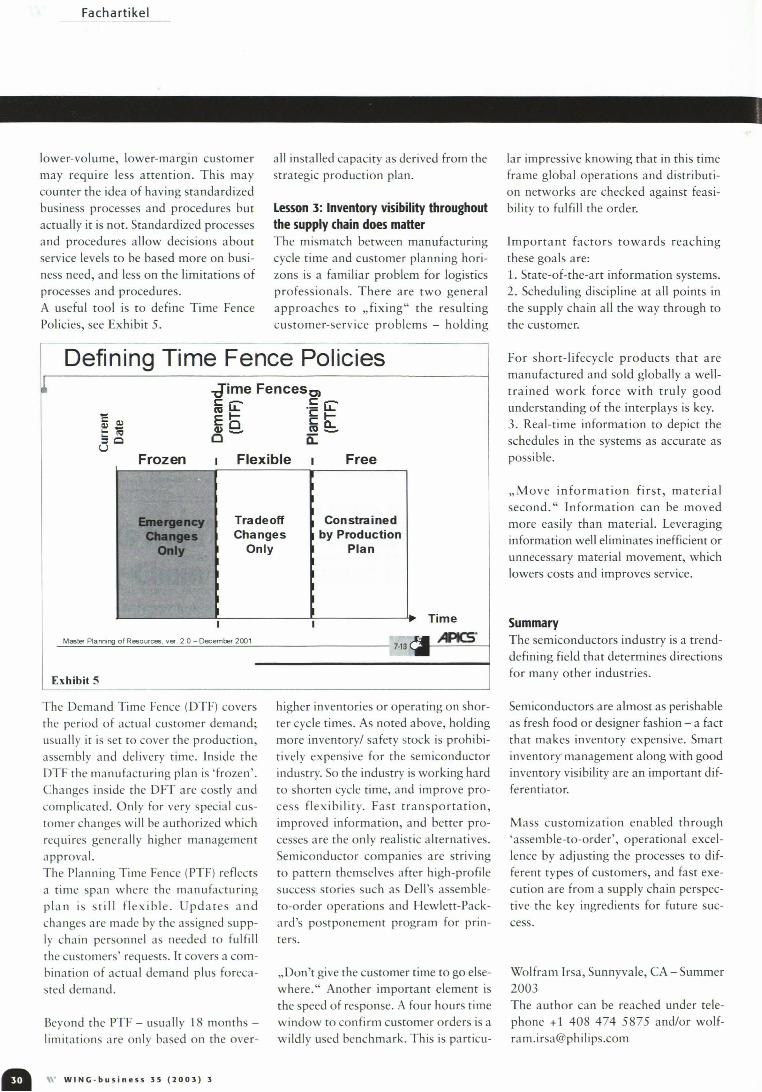

lower-volume, lower-margin customermay require less attention. This maycounter the idea of having standardizedbusiness processes and procedures butactually it is not. Standardized processesand procedures allow decisions aboutservice levels to be based more on business need, and less on the limitations ofprocesses and ptocedures.A useful tool is to define Time FencePolicies, see Exhibit 5.

all installed capacity as derived from thestrategic produetion plan.

Lesson 3: Inventory visibility throughoutthe supply (hain does matterThe mismatch between manufacturingcyele time and customer planning horizons is a familiar problem for logisticsprofessionals. There are two generalapproaches to "fixing" the resultingcustomer-service problems - holding

lar impressive knowing that in this timeframe global operations and distribution networks are checked against feasibility to fulfill the order.

Imporrant faetors towards reachingthese goals are:1. State-of-the-art information systems.2. Scheduling discipline at all poinrs inthe supply chain all the way through tothe customer.

Defining Time Fence Policies

• -Jime FencesO)fii (L .~ (L

:: l1l Er er~~ G>0 fiie:.=0 0- 0:::u

Frozen I Flexible I Free

Emergency Tradeoff Constrained

Cha Changes by ProductionOnly Only Plan

TimeI I

Master PlannlOg of Resources, ver 20 - Oecembef 20017-13 c;a- AReS"

Exhibit S

For shorr-lifecycle products that aremanufactured and sold globally a welltrained work force with truly goodunderstanding of the inrerplays is key.3. Real-time information to depict theschedules in the systems as accurate aspossible.

"Move information first, materialsecond." Information can be movedmore easily than material. Leveraginginformation weil eliminates inefficienr orunnecessary material movemenr, whichlowers costs and improves service.

SummaryThe semiconductors industry is a trenddefining field that determines directionsfor many other industries.

The Demand Time Fence (DTF) coversthe period of actual customer demand;usually it is set to cover the production,assembly and delivery time. Inside theDTF the manufacturing plan is 'frozen'.Changes inside the DFT are cosrly andcomplicated. Only for very special cusromer changes will be authorized whichrequires generally higher managementapproval.The Planning Time Fence (PTF) reflectsa time span where the manufacturingplan is still flexible. Updates andchanges are made by the assigned suppIy chain personnel as needed ro fulfillthe customers' requests. It covers a combination of actual demand plus forecasted demand.

Beyond the PTF - usually 18 months limitations are only based on the over-

__ \\' WING-business 35 (2003) 3

higher inventories or operating on shorter cyele times. As noted above, holdingmore inventory/ safety stock is prohibitively expensive for the semiconducrorindusrry. So the indusrry is working hardto shorten cyele time, and improve process f1exibility. Fast transportation,improved information, and better processes are the only realistic alternatives.Semiconductor companies are srrivingto pattern themselves after high-profilesuccess stories such as Dell's assembleto-order operations and Hewlett-Packard's postponement program for printers.

"Don't give the customer time to go e1sewhere." Another imporrant element isthe speed of response. A four hours timewindow to confirm customer orders is awildly used benchmark. This is particu-

Semiconductors are almost as perishableas fresh food or designer fashion - a factthat makes inventory expensive. Smartinvenrorymanagement along with goodinventory visibility are an important differentiator.

Mass customization enabled through'assemble-to-order', operational excellence by adjusting the processes to different types of customers, and fast execution are from a supply chain perspective the key ingredients for future success.

Wolfram Irsa, Sunnyvale, CA - Summer2003The author can be reached under telephone +1 408 474 5875 and/or wolf[email protected]