monthly perspectives - geopolitics - october 2016

TRANSCRIPT

GeopoliticsOctober 2016Monthly Perspectives Portfolio Advice & Investment Research

This document is for distribution to Canadian clients only. Please refer to the last page of this report for important disclosure information.

Martha Hill, CFA, AVP, Portfolio Advice & Investment Research

In this issue

The rise of populismA conversation with Marko Papic ���������������� 2

Geopolitics and your portfolioA conversation with Kevin Hebner and Todd Mattina �������������������������������������� 5

Important information �������������������������������� 8

With no shortage of political debates and ongoing risks associated with geopolitical events, this month, we continue our discussion on politics and the potential impact on financial markets� To get more insights on the issues that are top of mind for investors, we reached out to experts for their opinions on the political trends shaping the financial landscape�

In this issue of Monthly Perspectives, we spoke with Marko Papic, Chief Strategist, Geopolitical Strategy, at BCA Research, who provided us with his views on the rise of populist sentiment, the shifting sands of global power, and current global affairs�

We continue our conversation with Kevin Hebner, Managing Director and Global Equity Strategist at Epoch Investment Partners, and Todd Mattina, Chief Economist at Mackenzie Investments to uncover the potential impacts the current environment may have on investments and your portfolio�

2 Monthly Perspectives October 2016

The rise of populism

Chris Blake, CFA, Manager, North American Equities

We recently had the opportunity to speak with Marko Papic, Chief Strategist, Geopolitical Strategy at BCA Research, about his views on the rise of populist sentiment, the shifting sands of global power, and the lens through which investors should view media reports on current global affairs�

Marko, we see an apparent increase in anti-establishment sentiment around the world; examples of this are the rise of Donald Trump in the United States, the U�K� vote

to "Brexit" the European Union, and the populist movements in South Africa and across Europe� What are the short-term and long-term implications of this risk to global trade, and more specifically, how will this manifest itself in North America? Are there differences in the impact for Canada and the United States?

Global trade has been growing at a slower pace than global growth for several years, well before the populist trend became self-evident� Over the past two decades,

such distribution between global economic and trade growth has only occurred amidst global recessions� As such, there is clear evidence that trade has been impaired post-2008 by structural factors already� Anti-establishment policymakers will reinforce this macroeconomic trend in three ways:

1. They will overtly use protectionist policies, if they come to power, or they will force establishment politicians to adopt elements of protectionism in order to stay in power�

2. Success of populist politicians will encourage establishment parties to experiment with unorthodox monetary policy, which could lead to further currency devaluations, which may prompt a new “competitive currency regime” to come about� This would further impair trade�

3. Populism and jingoism go hand in hand� More aggressive foreign policy will mean more geopolitical risk� More geopolitical risk means more opportunities to use trade and finance as tools of war, which means less trade�

It is highly unlikely that we will see any of the three in Canada� However, Canada could be impacted by what the U�S� does� Either directly—through tariffs or “renegotiation” of NAFTA—or indirectly� For example, imagine a trade war between the U�S� and China� On one hand, it is very likely that Canada would be forced to choose sides in such a conflict� On the other hand, Canada is somewhat insulated from protectionism due to the fact that it is a major commodity producer� As we have seen with Russia, protectionist policies rarely impact a country’s commodity sector�

We have heard you speak of an increase in “multi-polarity” in the world� How has the world arrived at this point and how do you see it evolving over the coming

five to ten years� Are there aspects of multi-polarity that have investment implications?

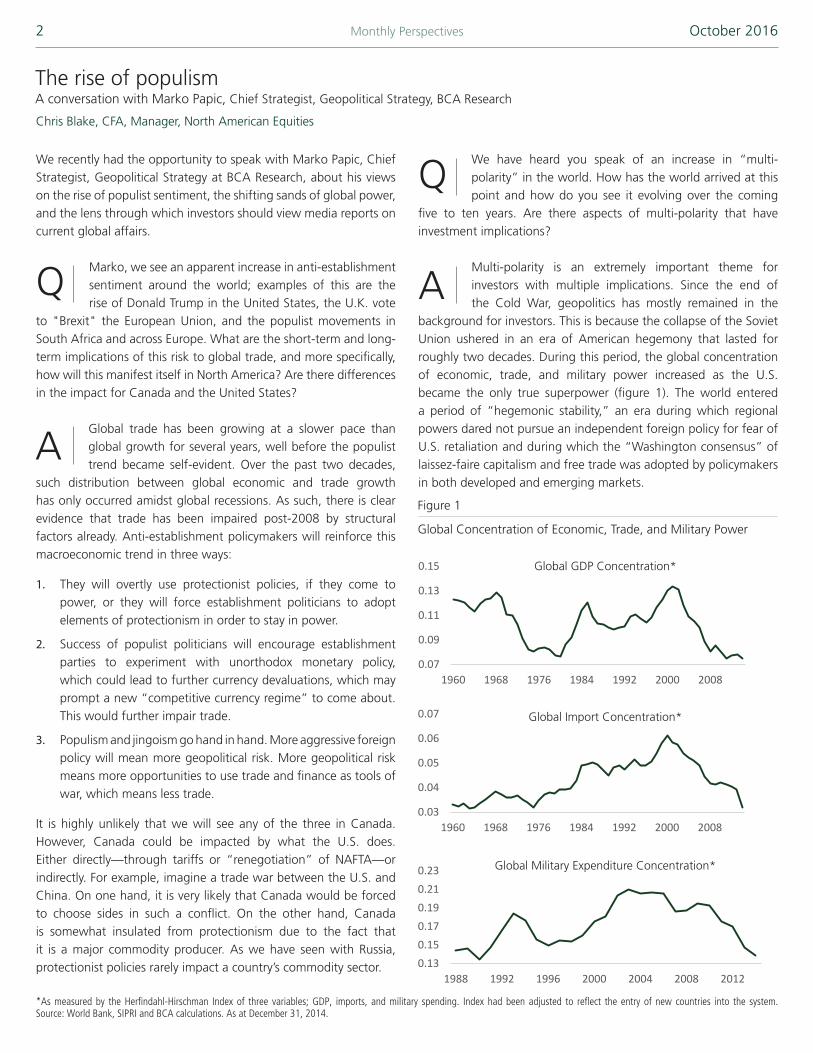

Multi-polarity is an extremely important theme for investors with multiple implications� Since the end of the Cold War, geopolitics has mostly remained in the

background for investors� This is because the collapse of the Soviet Union ushered in an era of American hegemony that lasted for roughly two decades� During this period, the global concentration of economic, trade, and military power increased as the U�S� became the only true superpower (figure 1)� The world entered a period of “hegemonic stability,” an era during which regional powers dared not pursue an independent foreign policy for fear of U�S� retaliation and during which the “Washington consensus” of laissez-faire capitalism and free trade was adopted by policymakers in both developed and emerging markets�

Q

A

A conversation with Marko Papic, Chief Strategist, Geopolitical Strategy, BCA Research

Q

A

*As measured by the Herfindahl-Hirschman Index of three variables; GDP, imports, and military spending. Index had been adjusted to reflect the entry of new countries into the system. Source: World Bank, SIPRI and BCA calculations. As at December 31, 2014.

Figure 1

Global Concentration of Economic, Trade, and Military Power

0.07

0.09

0.11

0.13

0.15

1960 1968 1976 1984 1992 2000 2008

Global GDP Concentration*

0.03

0.04

0.05

0.06

0.07

1960 1968 1976 1984 1992 2000 2008

Global Import Concentration*

0.130.150.170.190.210.23

1988 1992 1996 2000 2004 2008 2012

Global Military Expenditure Concentration*

3 Monthly Perspectives October 2016

Multi-polarity implies that the number of states powerful enough to pursue an independent and globally relevant foreign policy is greater than one (unipolarity) or two (bipolarity)� Today, multi-polarity is the product of America’s decaying unipolar moment� The U�S� remains, by far, the most powerful country in the absolute sense, but it is experiencing a relative decline as regional powers become more capable on both the economic and geopolitical fronts (figure 2)�

Figure 2

U�S� Geopolitical Power Index (Relative to World)

7780838689929598

1989 1993 1997 2001 2005 2009 2013

The Geopolitical Power Index measures a country's power based on a weighted aggregation of its economic, military, political, technological, and geographical endowments.

A conversation with Marko Papic (cont’d)

Multi-polarity is not a popular theme with investors� It augurs uncertainty, rising risk premia, and unanticipated “Black Swan” events� We know from formal modeling in political science, and from history, that a multi-polar world is unstable and more likely to produce military conflict (figure 3)�1 There are three reasons:

1. During periods of multi-polarity, more states can effectively pursue foreign policies that lead to war, thus creating more potential “conflict dyads” in the parlance of International Relations theory�

2. Power imbalances between states are more likely if there are more states that matter geopolitically� And power imbalances invite conflict as they are more likely to produce a situation in which one country’s rising capabilities threaten another�

3. The probability of miscalculation rises due to the number of relevant states making geopolitical decisions simultaneously�

There are a number of derivatives from the multi-polarity thesis that will be relevant for investors� For example, despite Brexit, a multi-polar world will support European integration�2

Figure 3

National Capability Index

0

5

10

15

20

25

30

35

40

1816 1826 1836 1846 1856 1866 1876 1886 1896 1906 1916 1926 1936 1946 1956 1966 1976 1986 1996 2006

U.S. U.K. FRANCE GERMANY CHINA JAPAN RUSSIA

Source: Correlates of War Database by Singer, Bremer, and Stuckey. As at December 31, 2007. The national capability index measures the material capability of countries in the form of iron and steel production, military expenditures and personnel, primary energy consumption, and total and urban population.

1 Mearsheimer, The Tragedy Of Great Power Politics (New York: Norton, 2001).2 BCA Geopolitical Strategy Special Report, “After BREXIT, N-Exit?” dated July 13, 2016, and BCA The Bank Credit Analyst, “Europe’s Geopolitical Gambit: Relevance Through Integration” dated November 2011.

4 Monthly Perspectives October 2016

How should investors view the relevance of day-to-day news? Should they react or would they be better served by looking at short-term news flows to help them find

opportunistic spots to invest in a more macro thematic manner?

At the end of the day, I really just read news for a living� But to be a successful investment strategist doing so, my team and I build geopolitical net assessments—

frameworks—through which to interpret that news flow� During Brexit, our net assessment told us that the probability of the U�K� exiting the European Union (EU) was much closer to 50% than the 30% implied by various betting markets� We adjusted our strategy accordingly�

The opportunities for investors in politics and geopolitics come when the daily news flow drives investors� In those situations, the media narrative takes over and the market prices risks according to the conventional wisdom du jour� But media does not represent reality, only one interpretation of reality� And investors who focus on doing their own fundamental political and geopolitical analysis—based on an analysis of objective constraints facing policymakers—can find opportunities in those moments when the daily news flow drives the market�

With geopolitical uncertainty rising in Europe’s neighbourhood—particularly in the Middle East—and with Russia reasserting itself, Europe’s core countries will not follow down the “exit” path that the U�K� pursued� However, the geopolitical disequilibrium in East Asia is deepening, with China’s pursuit of a sphere of influence in the South and East China Seas likely to continue to raise tensions in the region�

But the overarching concern for investors should be how multi-polarity impacts the global economy� Global macroeconomic imbalances—such as the current combination of insufficient demand and excessive capacity—can be overcome either by unilateral policy from the hegemon or through coordination among the major economic and political powers� A multi-polar world, however, lacks such coordination�

Globalization is therefore at risk from multi-polarity�3 Not only are regional powers pursuing spheres of influence, which is by definition incompatible with a globalized world, but the world lacks the hegemon that normally provides the expensive, and hard to come by, global public goods: namely economic coordination and geopolitical stability�

The investment implications of multi-polarity center on three broad themes:

Apex of globalization Going forward, the world is going to be less, not more, globalized� This will favour domestic over global sectors and consumer-oriented economies over the export-oriented ones� Globalization is also a major deflationary force, which would suggest that, on the margin, a world that is less globalized should be more inflationary�

Developed markets over emerging markets Multi-polarity is more likely to produce a number of conflicts, some of which lay dormant throughout the Cold War and subsequent era of American hegemony� These conflicts tend to be in emerging or frontier markets�

Safe havens With the frequency of geopolitical conflict on the rise, safe haven assets like U�S� Treasuries, the U�S� dollar, gold, and Swiss and Japanese government bonds, should continue to hold an important place in investors’ asset allocation�

A conversation with Marko Papic (cont’d)

Q

A

3 BCA Geopolitical Strategy Special Report, “The Apex Of Globalization: All Downhill From Here,” dated November 12, 2014.

See Marko Papic on MoneyTalk

Tune in to see Marko on MoneyTalk October 19, 2016

7:00 p�m�

Marko Papic is Chief Strategist for Geopolitical Strategy at BCA Research� Marko has been a guest on MoneyTalk with Kim Parlee, which can be seen Wednesdays at 7 p�m� ET on BNN and Saturdays at 3:30 p�m� ET on CTV�

with Kim Parlee

5 Monthly Perspectives October 2016

We are living in a period of heightened geopolitical risks across the globe, which have been exemplified by events such as the Brexit vote and the rise of populist movements in different regions in the world� In order to get some perspective on how the current environment could impact your investments, we spoke with Kevin Hebner, Managing Director and Global Equity Strategist at Epoch Investment Partners, and Todd Mattina, Chief Economist at Mackenzie Investments� Below is a summary of their views:

Do these events represent investable themes or just short-term noise?

Todd Mattina: Geopolitical risks, ranging from the impact of Brexit to the U�S� presidential race, remain top of mind for investors� However, forecasting the outcome of

political events and their highly uncertain impact on market returns does not usually serve investors well in the long run� For example, forecasters failed to predict the outcome of the Brexit referendum or its immediate economic impact� Diversification across asset classes, geographies and equity factors provides the best defense, especially for investors with longer time horizons� Strategic use of currency hedging can also be important to reduce portfolio risk�

What are the specific catalysts that are likely to move internationally-focused investments?

Mattina: While many factors drive the returns of internationally focused funds, three potential catalysts worth monitoring include long-run shifts in the Canadian

dollar, the global mix between monetary and fiscal policies and the emerging markets (EM) market rally following a multi-year bear market�

The 25% decline in the Canadian-U�S� dollar exchange rate during 2014-2015 contributed to the over-performance of many unhedged internationally focused funds� Over the longer run, Canada’s slow and uneven rebalancing from resource- to manufacturing-led growth suggests a weaker loonie may still be needed, supporting international funds with unhedged foreign currency exposure�

The diminishing effectiveness of ultra-loose central bank policies to boost economic growth, especially in the euro zone and Japan, could lead to a shift towards greater fiscal stimulus by already indebted governments with potentially negative implications for longer duration interest rates�

Weak EM markets in recent years reflected the prospect of U�S� Federal Reserve (Fed) rate tightening, falling commodity prices and slower Chinese growth� Looking ahead, the expected glacial pace of Fed rate tightening and the stabilizing outlook for commodity prices and China’s economy suggest the EM market rally can continue�

Kevin Hebner: The three long-term themes that could have an outsized impact on the investment landscape for years to come are 1) secular stagnation, 2) the importance

of technology as a driver of productivity growth and profit margins and 3) the rebalancing of China's economy�

Secular stagnationEpoch believes the U�S� economy is consigned to a secular 2% growth rate� This century, when the U�S� has grown faster than 2%, as it did in 2003-2007, it has come alongside a dangerous level of borrowing, which is not likely to be repeated, because the prior episode contributed to a housing bubble� Noted economist, Larry Summers, has popularized the decades old term “secular stagnation,” which stems from excess savings over investment acting as a drag on demand, growth, inflation, and real interest rates� The causes of secular stagnation include an aging population that saves more and consumes less, deleveraging on the part of households and governments, and muted capital spending by businesses in light of new technologies and a more service-oriented economy� Since 2011, the International Monetary Fund (IMF) has repeatedly lowered their growth estimates� The IMF is currently forecasting 1�8% growth in developed countries for 2016 and 2017� Regarding inflation, 30 of 35 Organization for Economic Cooperation and Development (OECD) countries currently have 2% or less inflation rates� The investment considerations of secular stagnation include a lower ceiling on earnings growth than might otherwise be the case and worried central bankers that err on the side of policy accommodation to thwart the potential risks of deflation� While the economic impact of quantitative easing (QE) and negative interest-rate policies (NIRP) can be debated, such measures have been shown to support risky asset prices�

The importance of technologyTechnology is enabling firms to operate with higher returns on equity (ROE)� First, technology has allowed firms to operate with lower labour costs as an input to sales, leading to improved profit margins� The World Economic Forum (WEF) surmises that office and administrative jobs have been most at risk of being replaced by disruptive technologies and more robot substitution should take place where robots are already in use, such as in manufacturing and production� Second, technology has made it possible to produce sales with less investment in property, plant, equipment, and inventories, leading to better asset utilization� It is becoming increasingly common for firms to carry low or zero inventories, due to advances in supply chain management� A by-product of lower inventories is reduced possession and facility costs� Third, technology’s impact on supply and demand has contributed to low interest rates� Low interest rates have encouraged many companies to increase their leverage�

A

Geopolitics and your portfolioA conversation with Kevin Hebner, Managing Director and Global Equity Strategist at Epoch Investment Partners, and Todd Mattina, Chief Economist at Mackenzie Investments

Darim Abdullah, CFA, Senior Analyst, Managed Investments

QA

Q

A

6 Monthly Perspectives October 2016

China’s rebalancing should provide a meaningful tailwind for companies catering to domestic consumption and services� Conversely, this rebalancing could represent a headwind for commodities and capital spending in the decade ahead� China's over-capacity and high leverage is a key element of secular stagnation� We agree and conclude that Chinese deleveraging and rebalancing has several important consequences: Excess capacity has resulted in China exporting goods price deflation to the rest of the world� Less investment in China has driven lower commodity prices (e�g�, iron ore, steel, coal and copper)�

Mr� Mattina, can you comment on Mackenzie Investments' views on the imbalances in China?

Mattina: China’s unbalanced growth and rapid credit growth set the stage for a difficult macroeconomic adjustment� Years of credit-financed investment resulted

in excess productive capacity, high debt, low profits and low producer prices� In fact, China’s total debt increased by about 80% of GDP since 2008 to reach almost 2�5 times the size of the economy� At the same time, rapid credit growth has delivered an increasingly smaller kick with economic growth falling from double digits in the mid-2000s to about 6�7% today� Such a rapid increase in credit with slower growth seldom occurs without a financial

The rebalancing of China's economyChina’s economy is slowly and gradually rotating away from investment and heavy industries and towards consumer spending and services (figure 4)� In the decade ahead, consumption should pass the 50% of GDP threshold for the first time ever� By way of comparison, consumption is typically 65% to 75% of GDP in developed economies� Likewise, investment as a share of GDP should contract�

crisis� Fortunately, China’s reserves of about $3�2 trillion provide sizable buffers to absorb financial shocks or currency pressure� The greatest risk for China is getting stuck in a “middle income trap” of prolonged sluggish productivity due to misallocated capital and troubled loans�

The European Commission recently hit Apple Inc� (AAPL-Q) with a €13 billion clawback of unpaid taxes in Ireland� Do you believe that such action by the European

Commission could undermine foreign investments in the region, specifically by American multi-national companies?

Mattina: Many core European Union (EU) states, supported by the Organization for Economic Co-operation and Development (OECD) and other international

organizations, have warned about a race to the bottom in setting corporate tax rates, threatening government revenues in all countries� According to reports, Ireland’s generous tax concessions to Apple implied an effective tax rate of just 0�005% in 2014� Ireland’s spectacular growth in recent decades depended on strong foreign investment, motivated in part by access to the EU common market at very low tax rates� Other EU countries suspect investments in their economies may have suffered because of perceived “unfair” tax policies� In this way, the EU decision reflects a broader policy debate between EU countries rather than a targeting of successful U�S� multinationals� However, the implication is that multinationals face increased risk from the uncertain political and regulatory environment, which threatens to hold back new investment�

One of the key themes discussed nowadays is the high degree of cross-asset correlation where various asset classes seem to be moving together� Many have attributed

this to all markets being focused on Central Banks' policies� To what extent do you believe global asset prices have been driven by Central Banks' policies versus fundamentals?

Mattina: Central banks played an important role in boosting asset prices after the Great Recession through unprecedented low interest rates and asset purchases,

dampening market volatility� However, today’s continuing low rates and high asset prices reflect three key longer run macro forces that have lowered the discount rate for asset pricing� First, population aging and low productivity slow the supply-side growth engine of the economy� Second, a legacy of high debt means the days of credit-financed spending are behind us� Finally, a glut of global savings keeps downward pressure on real interest rates� These macro headwinds imply that trend economic growth, inflation and real interest rates will remain below average, keeping downward pressure on discount rates and supporting high asset prices�

Q

A

Q

A

A

A conversation with Kevin Hebner and Todd Mattina (cont’d)

Figure 4

Changing Composition of China’s GDP

Source: McKinsey, March 2016.

Q

-10

0

10

20

30

40

50

60

Consumption Investment Government Net Trade

2000 - 2010 2010 - 2020 2020 - 2030

%

7 Monthly Perspectives October 2016

Hebner: The U�S� stock market has recently recorded new all-time highs� Since 2012, a significant portion of the total return has been attributed to higher price-

to-earnings ratios, rather than earnings growth or dividends� This unusual contribution to returns through expanding market multiples is largely the result of very accommodative monetary policies and “lower for longer” discount rates� During this period, an appetite among investors for companies with a demonstrated track record of producing cash flow and returning it to shareholders has contributed to defensive stocks outperforming cyclical ones� While this may have created a limited number of opportunities in cyclical sectors, investors need to be wary of potential “value traps,” especially in the global materials and industrials sectors� Many of these companies could fall short on generating sustainable cash flow growth�The S&P 500 Index second-quarter earnings season is completed now, and although profits are down slightly versus the same period a year ago, forward estimates are no longer being revised lower� This means the worst for earnings has largely concluded, and a more predictable earnings environment should ensue� Going forward, companies that allocate capital wisely and can consistently produce earnings and cash flow growth should be in an enviable position�

The aftermath of the June 23 Brexit vote was the latest reminder that central banks will loosen their policies to combat unwanted risks and volatility� In this low-yield environment, it is important to remember that the dividend yield on developed market equities exceeds that on government bonds� And, the dividend yield does not include other aspects of shareholder yield, such as cash returned to shareholders in the form of stock buybacks�

Going forward, returns are expected to come from profits and cash flow growth, as well as dividends� Firms that make smart capital allocation choices, while returning cash to shareholders via dividends, share purchases, and debt reduction should occupy the commanding heights in a slow-growth environment with low interest rates�

Where do you see the most attractive opportunities looking out over the next 6-12 months and which areas might you be avoiding?

Mattina: Mackenzie’s Asset Allocation team expects tactical opportunities in three areas: the asset mix between stocks and bonds, relative equity markets and currencies�

We currently favour stocks relative to bonds because of exceptionally stretched bond valuations� Despite a recent bottom in high-quality government bond yields, fixed income markets remain highly overvalued even as inflation shows tentative signs of gradually returning to normal�

Across global stock markets, we remain overweight in British and EM stocks and underweight in the relatively overvalued U�S� and Japanese stock markets� Our bearish view of U�S� stocks reflects the more advanced stage of the U�S� business cycle and tighter monetary policy� Our bullish view of EM stocks reflects attractive valuations following a multi-year bear market and strong market sentiment following a sharp rebound� U�K� stocks benefit from the weaker pound as about three quarters of foreign earnings of FTSE 100 companies originate from overseas�

In currencies, we remain bearish of the British pound given highly negative market sentiment and unattractive macroeconomic conditions that may demand additional rate cuts by the Bank of England�

Hebner: To summarize, our view on capital markets over the next 12 months is as follows:

Fixed income: There is not much upside to holding bonds�

Commodities: A V-shaped recovery is unlikely given the tepid global growth outlook and headwinds facing investment spending�

Equities: A tough environment for top-line growth� Consequently, we prefer a diversified collection of high quality companies with strong track records regarding cash flow generation, shareholder distributions and capital allocation policies where returns on invested capital are greater than cost of capital�

A

A

Q

A

A conversation with Kevin Hebner and Todd Mattina (cont’d)

8 Monthly Perspectives October 2016

The information has been drawn from sources believed to be reliable. Where such statements are based in whole or in part on information provided by third parties, they are not guaranteed to be accurate or complete. Graphs and charts are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment, trading, or tax strategies should be evaluated relative to each individual’s objectives and risk tolerance. TD Wealth, The Toronto-Dominion Bank and its affiliates and related entities are not liable for any errors or omissions in the information or for any loss or damage suffered.

Certain statements in this document may contain forward-looking statements (“FLS”) that are predictive in nature and may include words such as “expects”, “anticipates”, “intends”, “believes”, “estimates” and similar forward-looking expressions or negative versions thereof. FLS are based on current expectations and projections about future general economic, political and relevant market factors, such as interest and foreign exchange rates, equity and capital markets, the general business environment, assuming no changes to tax or other laws or government regulation or catastrophic events. Expectations and projections about future events are inherently subject to risks and uncertainties, which may be unforeseeable. Such expectations and projections may be incorrect in the future. FLS are not guarantees of future performance. Actual events could differ materially from those expressed or implied in any FLS. A number of important factors including those factors set out above can contribute to these digressions. You should avoid placing any reliance on FLS.

All credit products are subject to credit approval and various terms and conditions. Nothing contained herein should be construed as an offer or commitment to lend by the Toronto-Dominion Bank.

Full disclosures for all companies covered by TD Securities Inc. can be viewed at https://www.tdsresearch.com/equities/welcome.important.disclosure.action

Research Ratings

Overall Risk Rating in order of increasing risk: Low (7.2% of coverage universe), Medium (35.4%), High (43.5%), Speculative (13.9%)

Action List BUY: The stock’s total return is expected to exceed a minimum of 15%, on a risk-adjusted basis, over the next 12 months and it is a top pick in the Analyst’s sector. BUY: The stock’s total return is expected to exceed a minimum of 15%, on a risk-adjusted basis, over the next 12 months. SPECULATIVE BUY: The stock’s total return is expected to exceed 30% over the next 12 months; however, there is material event risk associated with the investment that could result in significant loss. HOLD: The stock’s total return is expected to be between 0% and 15%, on a risk-adjusted basis, over the next 12 months. TENDER: Investors are advised to tender their shares to a specific offer for the company’s securities. REDUCE: The stock’s total return is expected to be negative over the next 12 months.

Important information

Research Report Dissemination Policy: TD Waterhouse Canada Inc. makes its research products available in electronic format. These research products are posted to our proprietary websites for all eligible clients to access by password and we distribute the information to our sales personnel who then may distribute it to their retail clients under the appropriate circumstances either by e-mail, fax or regular mail. No recipient may pass on to any other person, or reproduce by any means, the information contained in this report without our prior written consent. Analyst Certification:The Portfolio Advice and Investment Research analyst(s) responsible for this report hereby certify that (i) the recommendations and technical opinions expressed in the research report accurately reflect the personal views of the analyst(s) about any and all of the securities or issuers discussed herein, and (ii) no part of the research analyst’s compensation was, is, or will be, directly or indirectly, related to the provision of specific recommendations or views expressed by the research analyst in the research report.

Conflicts of Interest: The Portfolio Advice & Investment Research analyst(s) responsible for this report may own securities of the issuer(s) discussed in this report. As with most other employees, the analyst(s) who prepared this report are compensated based upon (among other factors) the overall profitability of TD Waterhouse Canada Inc. and its affiliates, which includes the overall profitability of investment banking services, however TD Waterhouse Canada Inc. does not compensate its analysts based on specific investment banking transactions.

Mutual Fund Disclosure: Commissions, trailing commissions, performance fees, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus, which contains detailed investment information, before investing. The indicated rates of return (other than for each money market fund) are the historical annual compounded total returns for the period indicated including changes in unit value and reinvestment of distributions. The indicated rate of return for each money market fund is an annualized historical yield based on the seven-day period ended as indicated and annualized in the case of effective yield by compounding the seven day return and does not represent an actual one year return. The indicated rates of return do not take into account sales, redemption, distribution or optional charges or income taxes payable by any unitholder that would have reduced returns. Mutual funds are not covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer and are not guaranteed or insured. Their values change frequently. There can be no assurances that a money market fund will be able to maintain its net asset value per unit at a constant amount or that the full amount of your investment will be returned to you. Past performance may not be repeated.

Corporate Disclosure: TD Wealth represents the products and services offered by TD Waterhouse Canada Inc. (Member – Canadian Investor Protection Fund), TD Waterhouse Private Investment Counsel Inc., TD Wealth Private Banking (offered by The Toronto-Dominion Bank) and TD Wealth Private Trust (offered by The Canada Trust Company).

The Portfolio Advice and Investment Research team is part of TD Waterhouse Canada Inc., a subsidiary of The Toronto-Dominion Bank.

Trade-mark Disclosures: FTSE TMX Global Debt Capital Markets Inc. 2016 “FTSE®” is a trade mark of FTSE International Ltd and is used under licence. “TMX” is a trade mark of TSX Inc. and is used under licence. All rights in the FTSE TMX Global Debt Capital Markets Inc.’s indices and / or FTSE TMX Global Debt Capital Markets Inc.’s ratings vest in FTSE TMX Global Debt Capital Markets Inc. and/or its licensors. Neither FTSE TMX Global Debt Capital Markets Inc. nor its licensors accept any liability for any errors or omissions in such indices and / or ratings or underlying data. No further distribution of FTSE TMX Global Debt Capital Markets Inc.’s data is permitted without FTSE TMX Global Debt Capital Markets Inc.’s express written consent.Bloomberg and Bloomberg.com are trademarks and service marks of Bloomberg Finance L.P., a Delaware limited partnership, or its subsidiaries. All rights reserved.

TD Securities is a trade-mark of The Toronto-Dominion Bank representing TD Securities Inc., TD Securities (USA) LLC, TD Securities Limited and certain corporate and investment banking activities of The Toronto-Dominion Bank.All trademarks are the property of their respective owners.®The TD logo and other trade-marks are the property of The Toronto-Dominion Bank.

Percentage of subject companies under each rating category—BUY (covering Action List BUY, BUY and Spec. BUY ratings), HOLD and REDUCE (covering TENDER and REDUCE ratings). As at October 3, 2016.

Distribution of Research Ratings

0%10%20%30%40%50%60%70%80%

BUY HOLD REDUCE

REDUCE2.9%

BUY56.3%

HOLD40.8%

61.42%

37.06%

1.52%

Percentage of subject companies within each of the three categories (BUY, HOLD and REDUCE) for which TD Securities Inc. has provided investment banking services within the last 12 months. As at October 3, 2016.

Investment Services Provided

0%10%20%30%40%50%60%70%80%

BUY HOLD REDUCE

REDUCE2.9%

BUY56.3%

HOLD40.8%

61.42%

37.06%

1.52%