montreal tea & coffee together! sharing one cup

DESCRIPTION

MONTREAL TEA & COFFEE TOGETHER! SHARING ONE CUP. WELCOME To Tea & Coffee Regional Updates and the SIAL 2005 Exhibition. AGENDA. Brief Association Updates-CAC/TAC NPD Presentation Jim Robinson Coffee from Jamaica Patrick Sibblies Questions. The Canadian Coffee Market. Net Imports. - PowerPoint PPT PresentationTRANSCRIPT

MONTREALTEA & COFFEE

TOGETHER!SHARING ONE CUP

WELCOMETo

Tea & Coffee Regional Updatesand the SIAL 2005 Exhibition

AGENDA

• Brief Association Updates-CAC/TAC

• NPD Presentation– Jim Robinson

• Coffee from Jamaica– Patrick Sibblies

• Questions

The CanadianThe Canadian

Coffee MarketCoffee Market

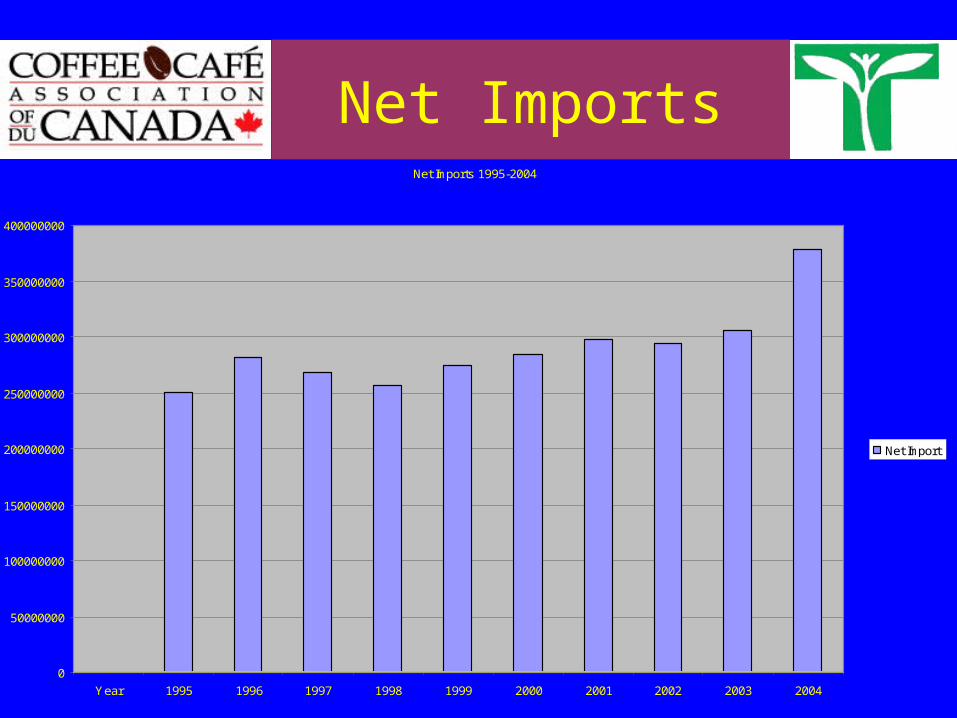

Net ImportsNet Imports 1995-2004

0

50000000

100000000

150000000

200000000

250000000

300000000

350000000

400000000

Year 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Net Import

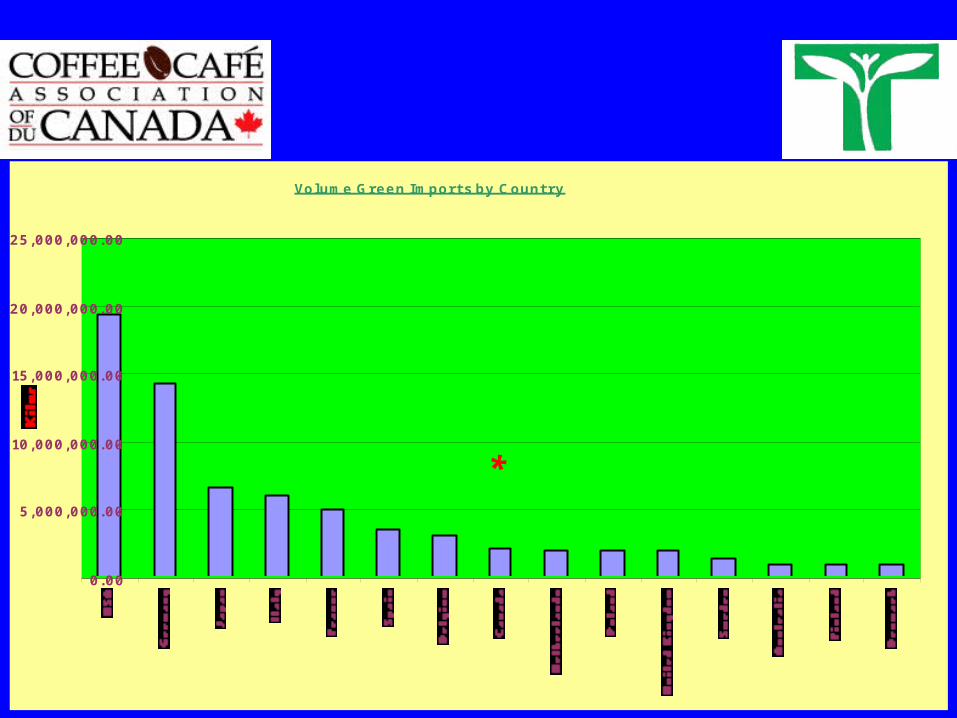

Volume Green Imports by Country

0.00

5,000,000.00

10,000,000.00

15,000,000.00

20,000,000.00

25,000,000.00

*

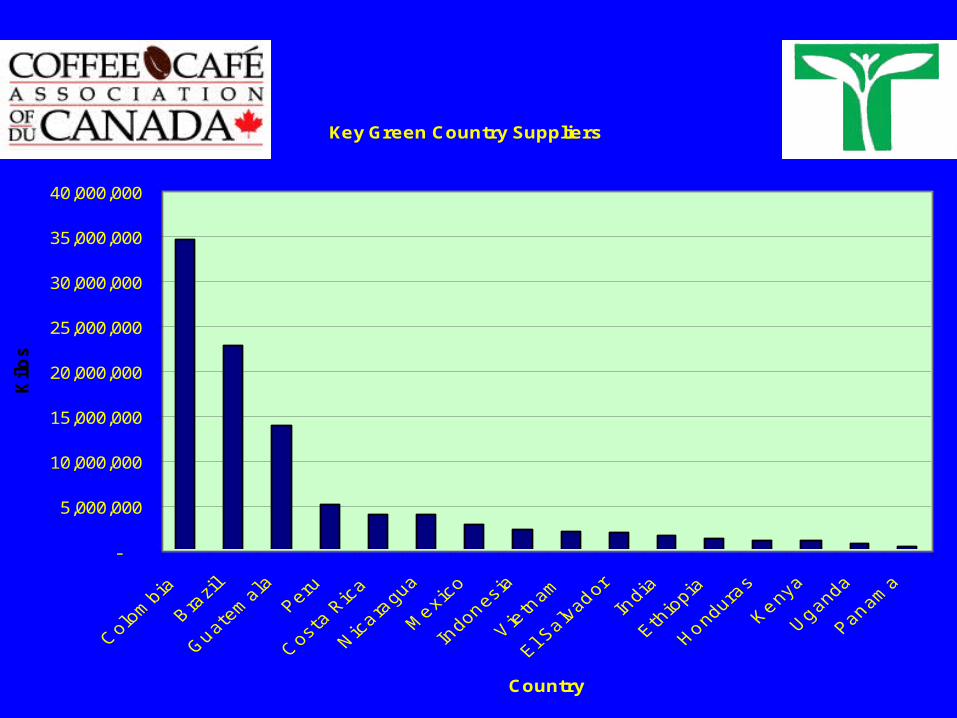

Key Green Country Suppliers

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

Country

Kilo

s

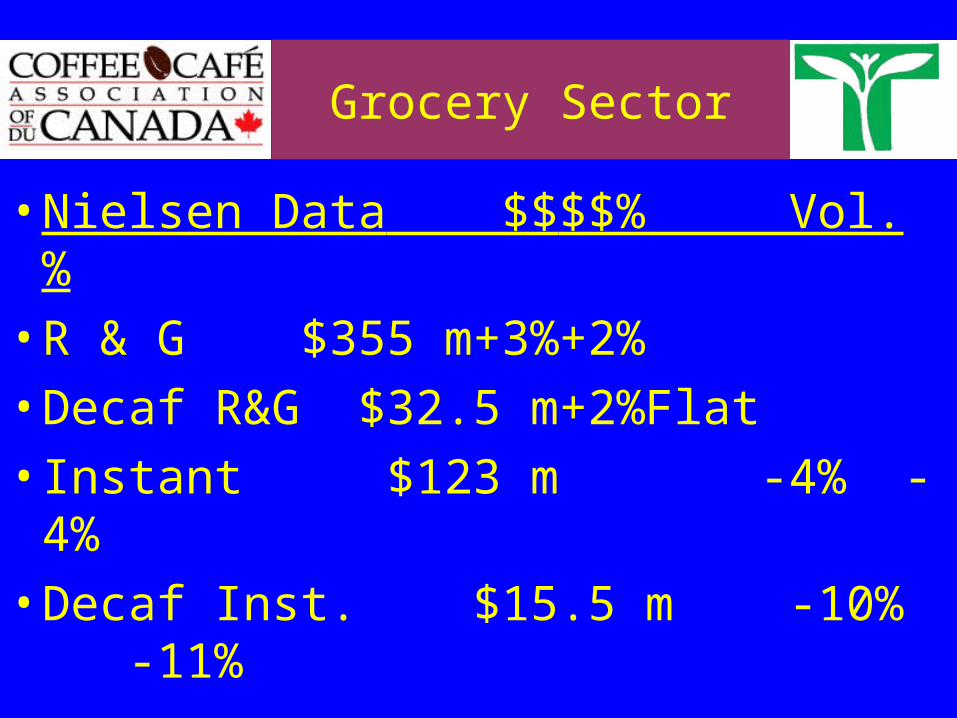

Grocery Sector

• Nielsen Data $$ $$% Vol. %

• R & G $355 m +3% +2%

• Decaf R&G $32.5 m +2% Flat

• Instant $123 m -4% -4%

• Decaf Inst. $15.5 m -10% -11%

Key Coffee Issues

• Pricing / (Sustainability)

• Pods, Packs & Potential Premiums

• Portability / Accessibility

• Premium Category (A Plus)

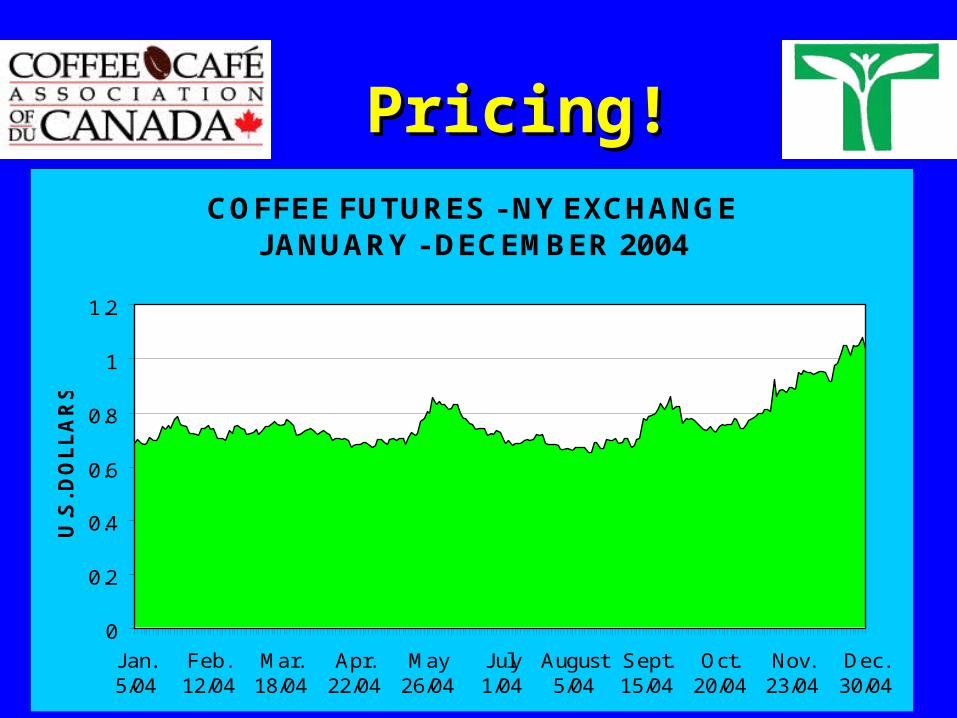

COFFEE FUTURES - NY EXCHANGEJANUARY - DECEMBER 2004

0

0.2

0.4

0.6

0.8

1

1.2

Jan.5/04

Feb.12/04

Mar.18/04

Apr.22/04

May26/04

July1/04

August5/04

Sept.15/04

Oct.20/04

Nov.23/04

Dec.30/04

U.S

. DO

LL

AR

S

Pricing!Pricing!

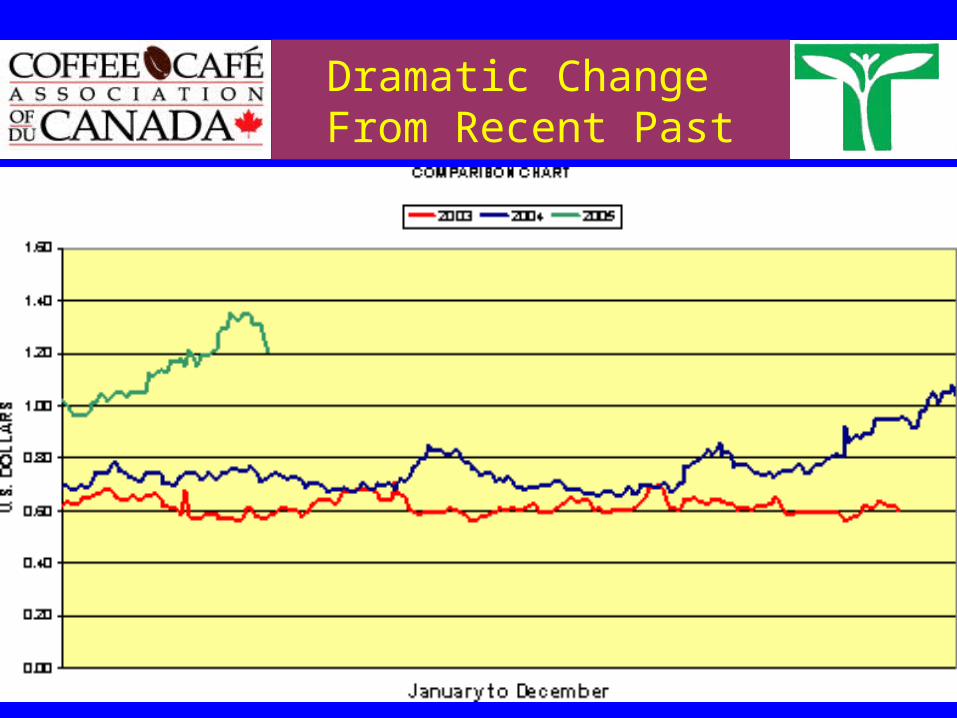

Dramatic Change From Recent Past

Pods, Packs andPods, Packs andPossible PremiumsPossible Premiums

PortabilityPortability

Premium Areas Growing

• Both Within Grocery and Foodservice Premium Products Are Experiencing the Strongest Growth----Driving Any Real Volume Growth Within At Home Sector and Creating Significant Dollar Growth in Away From Home Sector……..

Regulatory Issues

• Regulators Taking Some Form of Bureaucratic Viagara

• Many Issues Shared By Coffee and Tea—and Others Unique to One

• Share Advocacy and Information When Helpful –Often Sector With the Most at Stake Takes the Lead

LEADING TEA ADVOCATE

MEDIUM Priority HIGH Priority

LOW Priority

PESTICIDEMRL’S

Health &Safety Act

MANDATORY NUTRITIONLABELLING

Healthy Living

Fortification

HIGHLIGHTEDINGREDIENTS

Stewardship Ontario

Codex

WHO report

NHP’s

Product SpecificHealth Claims

CBSA-CFIA

Generic Health Claim

Caffeine Labelling

REGULATORY & ENVIRONMENT ISSUES for COFFEE

MEDIUM Priority HIGH Priority

LOW Priority On the Radar

PesticideM.R.L.’s

Social ActivismFair Trade/Oxfam

MANDATORY NUTRITIONLABELLING

Healthy Living

Ochratoxin A

HIGHLIGHTEDINGREDIENTS

Acrylamide

Canada’s Food Guide

Organic Standards

C.E.P.A.Product SpecificHealth Claims

C.B.S.A.

Decaf Solvents

Caffeine Labelling

Maintaining a LevelPlaying Field

“Import”StandardsFuran

“Green” Procurement

“Health”

G.I.P.

Key Regulatory Challenges

• C&T – Cementing MNL Victory• C&T -- “Bulk’ Import Labelling• C&T – Highlighted Ingredients and Flavours• T – Pesticide M.R.L.’s• T – Natural Health Products• C – Acrylamide• C – Decaf Solvents• C – Organic Standards

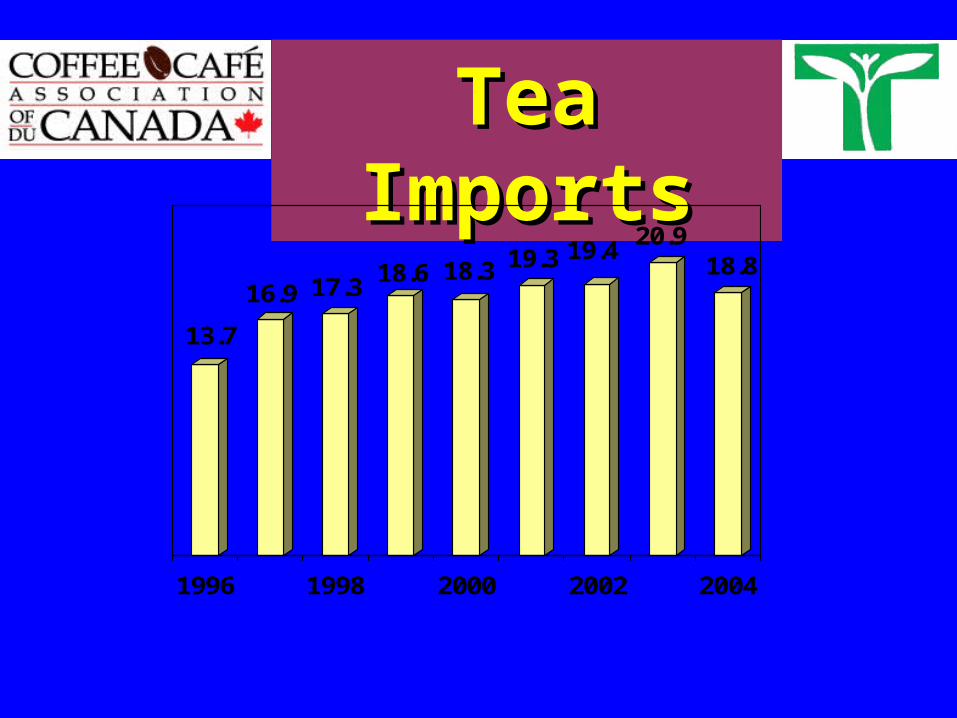

Tea ImportsTea Imports

13.7

16.9 17.318.6 18.3 19.3 19.4

20.918.8

1996 1998 2000 2002 2004

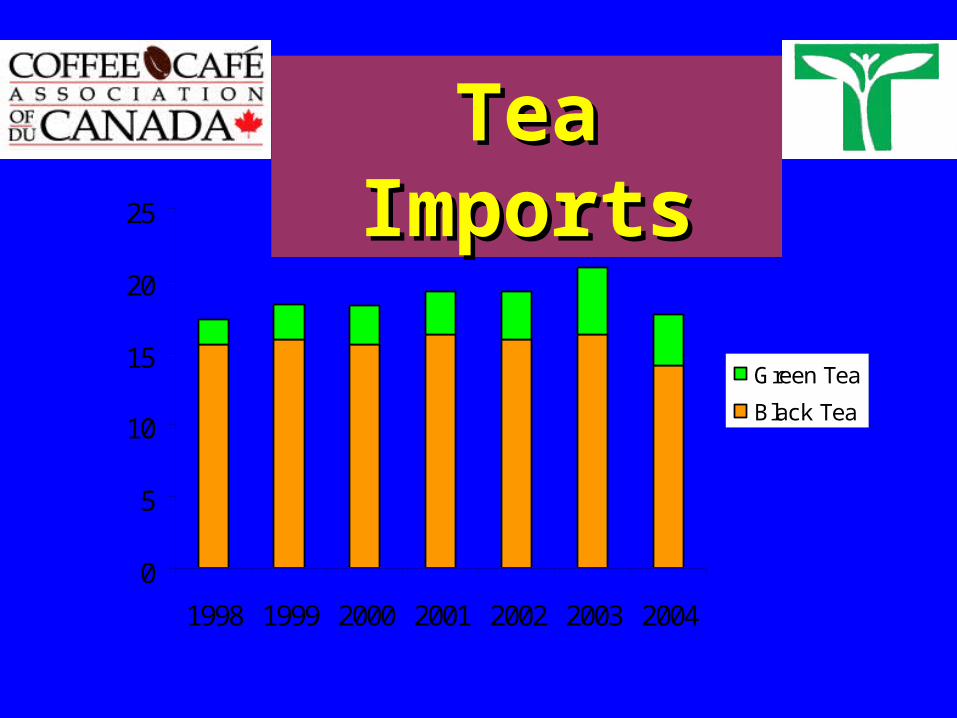

0

5

10

15

20

25

1998 1999 2000 2001 2002 2003 2004

Green Tea

Black Tea

Tea ImportsTea Imports

Tea ImportsTea Imports2004 Imports by Format (000 kg)

38.3%

11.9%

48.5%

Bags

Loose

Bulk

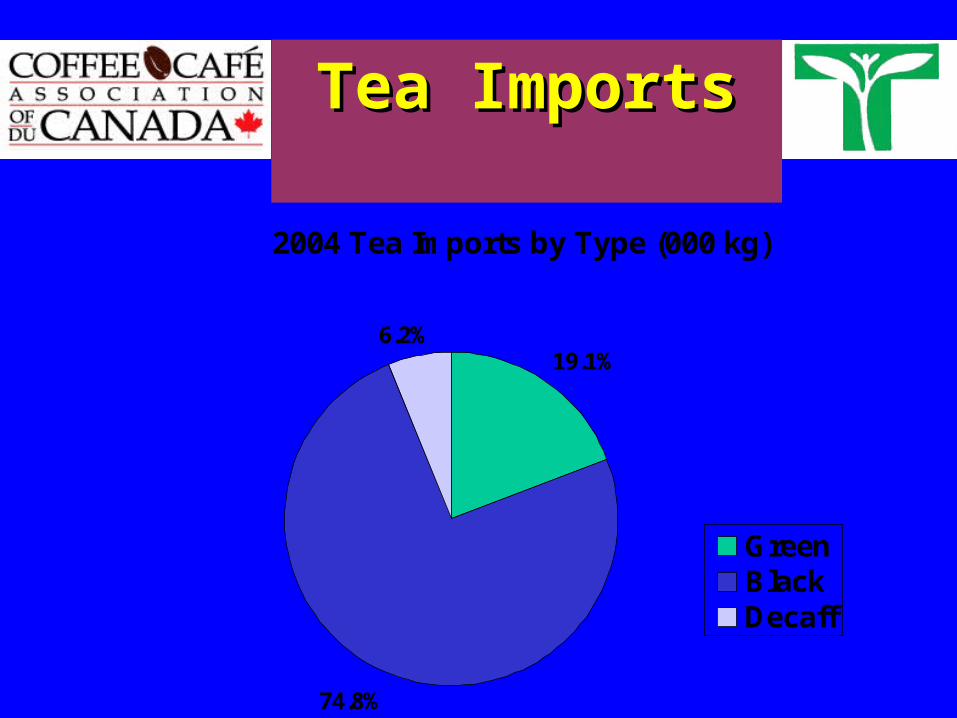

Tea ImportsTea Imports

2004 Tea Imports by Type (000 kg)

19.1%

74.8%

6.2%

GreenBlackDecaff

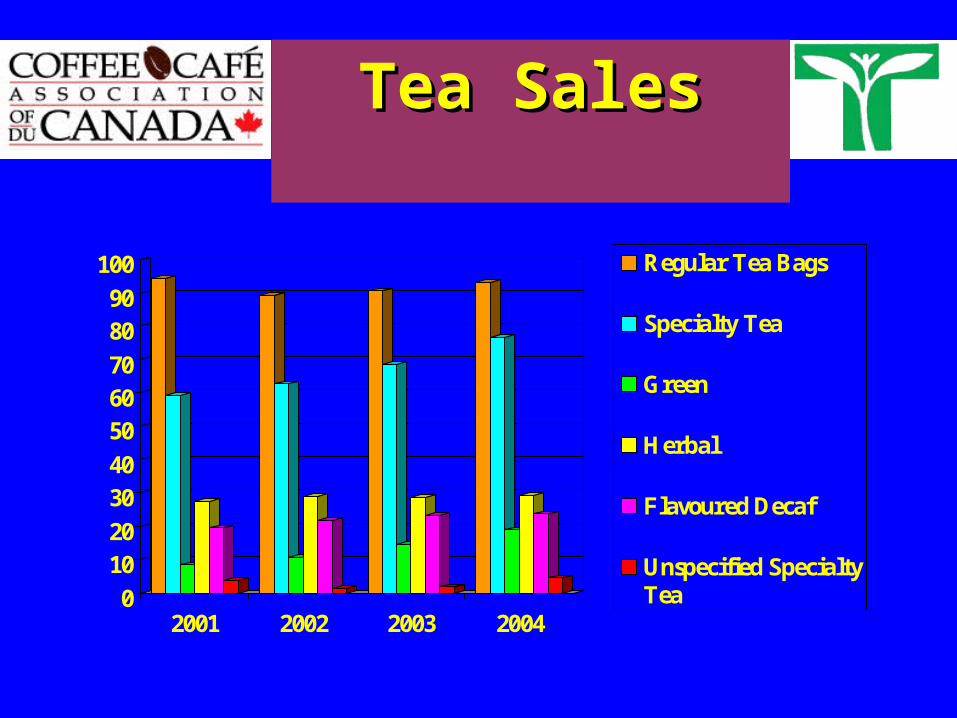

0

1020

3040

506070

8090

100

2001 2002 2003 2004

Regular Tea Bags

Specialty Tea

Green

Herbal

Flavoured Decaf

Unspecified SpecialtyTea

Tea SalesTea Sales

02468

101214161820

1997 2000 2001 2002 2003 2004

Green Tea SalesGreen Tea Sales

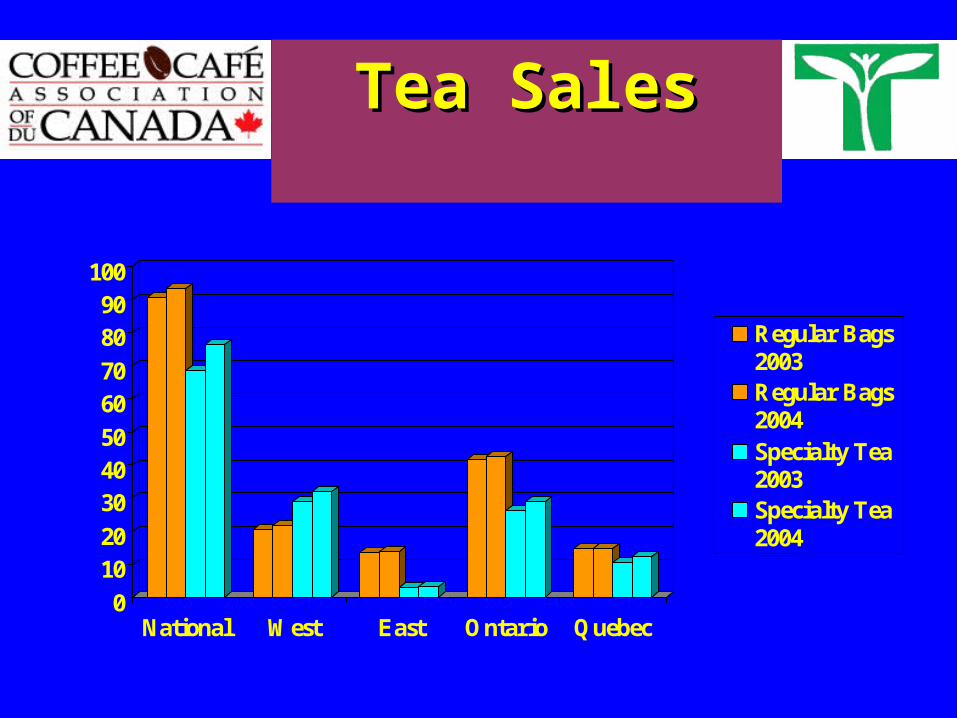

Tea SalesTea Sales

0

1020

304050

6070

8090

100

National West East Ontario Quebec

Regular Bags2003Regular Bags2004Specialty Tea2003Specialty Tea2004

Tea Sales - QuebecTea Sales - Quebec

0

2

4

6

8

10

12

14

16

2004

Total RegularTea BagsTotal SpecialtyTeaGreen Tea

Herbal Tea

Flavoured incl.DecafUnspecifiedSpeacialty Tea

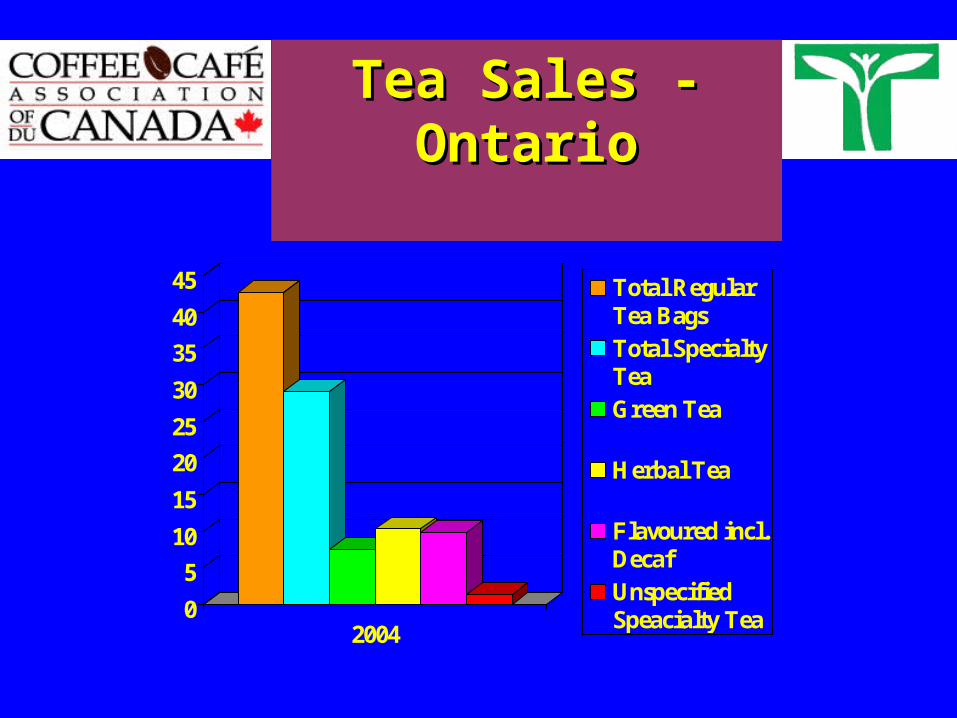

0

5

10

15

20

25

30

35

40

45

2004

Total RegularTea BagsTotal SpecialtyTeaGreen Tea

Herbal Tea

Flavoured incl.DecafUnspecifiedSpeacialty Tea

Tea Sales - OntarioTea Sales - Ontario

0

2

4

6

8

10

12

14

2004

Total RegularTea BagsTotal SpecialtyTeaGreen Tea

Herbal Tea

Flavoured incl.DecafUnspecifiedSpeacialty Tea

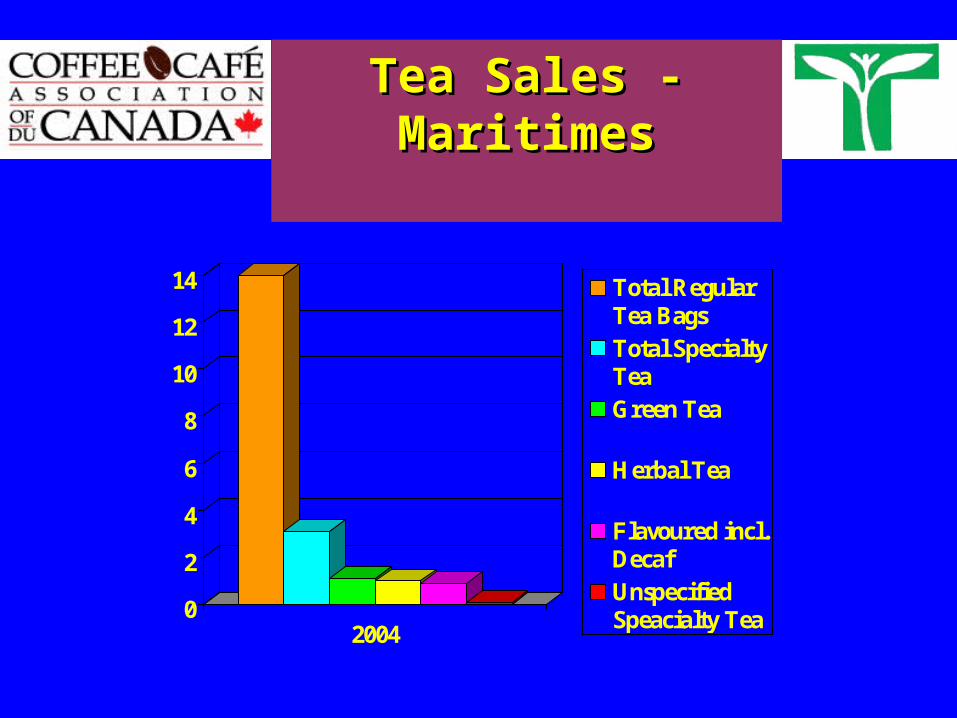

Tea Sales - MaritimesTea Sales - Maritimes

0

5

10

15

20

25

30

35

2004

Total RegularTea BagsTotal SpecialtyTeaGreen Tea

Herbal Tea

Flavoured incl.DecafUnspecifiedSpeacialty Tea

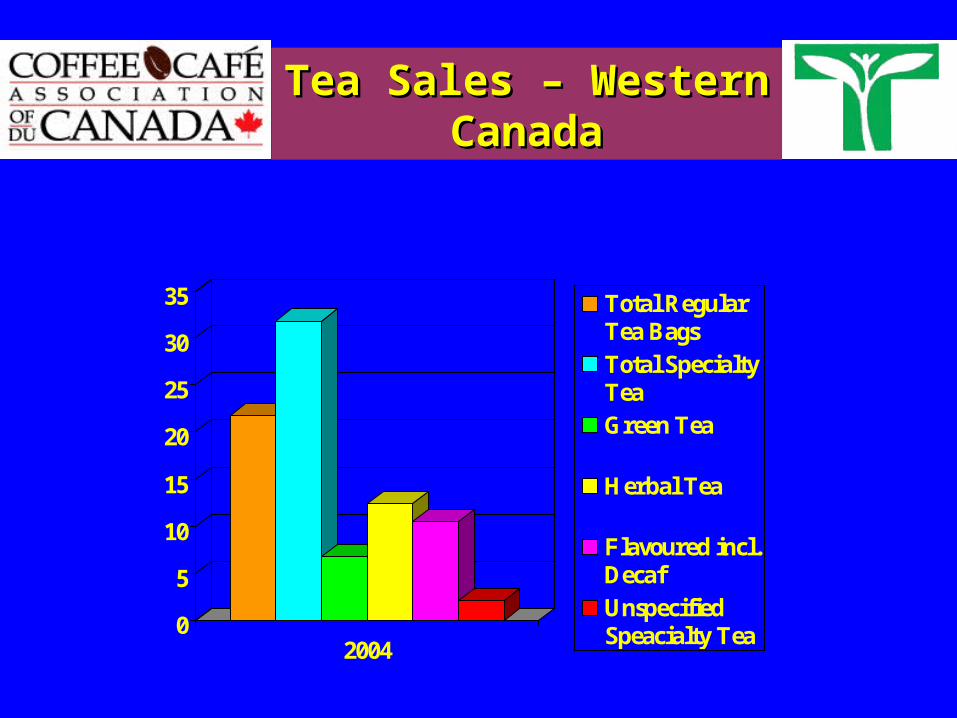

Tea Sales – Western Tea Sales – Western CanadaCanada

To provide proactive leadership on behalf of all members in the areas of advocacy, generic promotion, and education to ensure the long-term viability of the industry.

TAC MissionTAC Mission

Toronto Tea Briefing – May 5, 2005

Canada’s Tea Industry 13th Annual Fall Conference

“Steeped in Success!”

September 14 & 15, Deerhurst Resort, Huntsville, Ontario

www.tea.ca

Upcoming Events

COFFEE AND HEALTHPOSITIVE IMPACTS

Anti-oxidant properties –with implied positive impacts in terms of cancer prevention, positive impact on Coronary Heart Disease –parallels these properties of phytochemicals found in other vegetable and plant products such as tea Anti-depressant effect, mood elevator –connected to reduced risk for suicide Risk reduction for cirrhosis of the liver / liver disease Reduced risk for gallstone disease / gallstone formation Protects against / reduces risk for kidney stones / kidney stone disease Reduced risk for developing Parkinson’s disease Reduced risk for developing Type II Diabetes (this developed only months after coffee had been suggested as a potential contributor to diabetes risk and is indicative of how quickly the “best science” can move on the wellness spectrum Improves attention and concentration (and test scores) a physiological outcome if not a health benefit directly Positive impact on asthma –coffee functions as a bronchdilator Lowered risk for developing colo-rectal cancer Boosts metabolism –in effect a “thinning / diet impact” Reduced risk for death from a coronary heart attack (if heart incident occurs) Reduces dental scaries , in effect reduces cavities