navigating safely through turbulences - lufthansa … safely through turbulences. ... hedging with...

TRANSCRIPT

Wolfgang MayrhuberChairman of the Executive Board & CEO Deutsche Lufthansa AG

Frankfurt / June 4, 2008

Deutsche BankGerman Corporate Conference 2008

Navigating safelythrough turbulences

2 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

Agenda

Currenttrading

State ofthe industry

LHSet-up

3 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

Q1 laid a solid base for 2008

Chg. (vs. 12/07 in %)31.03.2008

Q1 2008 Chg. (yoy in %)Key figures LH Group

+15.6€ 888 mNet liquidity

-1.0P.29.9%Equity ratio

-89.7€ 57 mNet profit

+2.5P.3.5%Adj. operating margin

+422.2€ 188 mOperating result

+25.2€ 4,466 m- thereof traffic revenue

+19.0€ 5,587 mRevenue

4,6965,587

0

2000

4000

6000

LH Group results Q1 2008

36

188

0

50

100

150

200

+422%+19%

Revenue Operating Result

in € m / Change yoy Q1 2007 Q1 2008

Catering

IT Services

MRO

Logistics

Passenger Transportation

Operating resultby business segment

+79€ 38 m

Chg. (yoy in € m)Q1 2008

+4€ 5 m

+7€ 11 m

+11€ 71 m

+40€ 46 m

4 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

Outperformance has continued in 2008Traffic figures Passenger Transportation

� More than 18,000 passengers during the first four months

(+6.3%)

� Almost 7% higher capacity successfully sold in the market

� Future bookings altogether solid

Highlights YTD

Traffic figuresJanuary – April 2008, change in %

Passenger Transportation

-3

-1

1

3

5

7

Pax ASK RPK

LH Group* LH (excl. SWISS) AF/KLM BA-2

0

2

4

6

8

LH Group LH (excl.SWISS)

AF/KLM BA

-3

-1

1

3

5

7

LH Group LH (excl.SWISS)

AF/KLM BA

Sales per traffic regionRPK January – April 2008, change in %

Short-haul Long-haul

BA

* Lufthansa, regional partners & SWISS

SLF

5 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

Fuel costs are an issue

Source: Financial Times 24./25.05.2008

6 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

45

50

55

60

65

70

75

80

85

90

95

100

105

110

115

120

125

130

45 50 55 60 65 70 75 80 85 90 95 100 105 110 115 120 125 130

Fuel hedge scenario Lufthansa Group 2008

LH price 2008incl. SWISS

Market price

Oil price risk consistently hedged

USD/barrel

US

D/b

arre

l

Current price 30.05.2008: IPE Brent127,78 USD/bbl

appr. -20%

7 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

Agenda

Currenttrading

State ofthe industry

LHSet-up

8 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

International passenger traffic International freight traffic

Aviation is a growth industryM

onth

lyR

PK

s(in

bill

ions

)

Mar

01

Mar

04

Mar

07

Mar

02

Mar

03

Mar

05

Mar

06

Mar

08

Mar

00

6

7

8

9

10

11

12

13

14

Mon

thly

FT

Ks

(in b

illio

ns)

Mar

01

Mar

04

Mar

07

Mar

02

Mar

03

Mar

05

Mar

06

Mar

08

Mar

00

200

220

180

160

140

100

120Actual

Seasonally Adjusted

ActualSeasonally Adjusted

Source: IATA

9 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

Current trends and challenges

0

40

80

120

160

Sharp oil price increase (De-)Regulation

Industry loss expected Consolidation

2000 20082002 20062004

US

D/b

arre

l Kerosene

Crude Oil Pricing diff.

-2.3

5.6

-0.5

-4.1-5.6-6

-3

0

3

6

2008e2007200620052004

IATA net profit development (USD billion)

10 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

Industry developments divide airlines: The good, the bad and the gone

0 2000 4000 6000 -100 -50 0 50 100 150 200

Revenue (Jan-March 08 in m€) Operating income (Jan-March 08 in m€)

• MAXjet Airways , Dulles/USA • Aloha Airlines , Honolulu/USA • ATA Airlines , Indianapolis/USA

Airlines in bankruptcy and downsizings since Decemb er 2007

• Oasis Hongkong Airlines , Hongkong/China• Frontier Airlines , Denver/USA• EOS Airlines , Purchase/USA

& Downsizing of multiple carriers (e.g. American Airl ines)

11 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

Agenda

Currenttrading

State ofthe industry

LHSet-up

12 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

Our strategic course

Decentralized structures reinforce our proximity to the customer, flexibility and entrepreneurship

Focusing on our portfolio improves the positioningof the Lufthansa Group

Quality and innovations strengthen our attractiveness

Increasing revenue and cost management are cornerstones of our solid financial basis

First priority: Profitable growth & sustainable developm ent

13 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

Set-up for continued success

LufthansaSet-up

FinancialStrength

ProductExcellence

Balance &Flexibility

Partnerships &Alliances

14 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

Financial strength is the basis for a sustainable development of the Group

� Liquidity

� € 2 billion minimum liquidity

� Strong capital structure

� 30% equity ratio

� Financial flexibility

� Investment grade rating

� 70% unencumebered fleet

� Structured risk management

� Hedging with layer strategy

• High degree of autonomy from cyclical patterns

• Strategical freedom

15 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

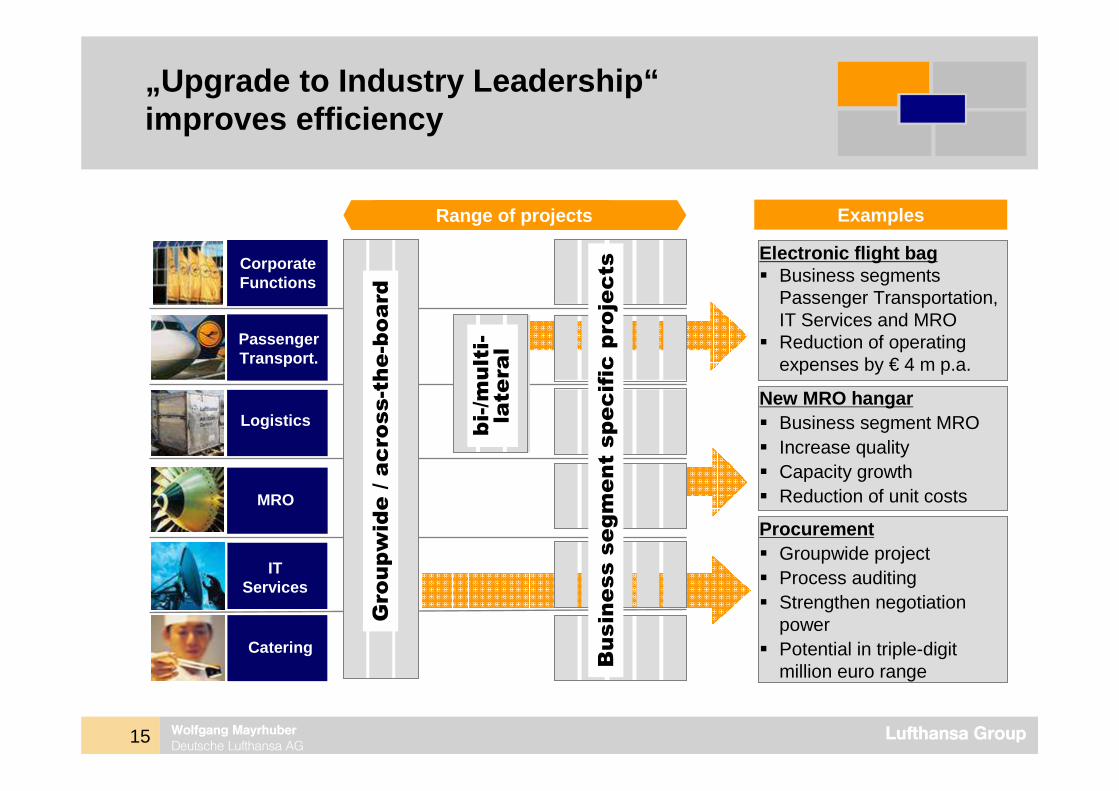

„Upgrade to Industry Leadership“improves efficiency

PassengerTransport.

Logistics

MRO

IT Services

Catering

Corporate Functions

Range of projects

Groupwide/ across-the-board

bi-/multi-

lateral

Procurement� Groupwide project� Process auditing� Strengthen negotiation

power � Potential in triple-digit

million euro range

Electronic flight bag� Business segments

Passenger Transportation, IT Services and MRO

� Reduction of operatingexpenses by € 4 m p.a.

Examples

Business segmentspecificprojects

New MRO hangar� Business segment MRO � Increase quality� Capacity growth � Reduction of unit costs

16 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

Product excellence and customer loyalty

Europe‘s leadingFrequent Flyer Program

6500

6800

7100

7400

2001 2002 2003 2004 2005 2006 2007

Cus

tom

erP

rofil

e In

dex

Investments in qualityand innovation

0

2

4

6

8

10

12

14

16

1993 1995 1997 1999 2001 2003 2005 2007

Miles&More

Miles&More members in millions

Rising premium revenue share

Increasing customer satisfaction

35%

40%

45%

50%

55%

2003 2004 2005 2006 2007

Lufthansa Group17 Wolfgang Mayrhuber

Deutsche Lufthansa AG

Lufthansa‘s revenue base is diversified

More than 50% of revenueson non-European routes*

69%Europe

17%Americas

11%Asia-

Pacific

3%Mid East& Africa

By Sales Origin

By Traffic Region

20%

7%

26%

47%

Corporate revenues are well diversifiedover the respective sectors*

Others23%

Production47%

Finance & Consulting

13%Services

17%

* figures relate to Lufthansa Passenger Airlines

Lufthansa Group18 Wolfgang Mayrhuber

Deutsche Lufthansa AG

Flexibility in revenue input is the basisfor high capacity utilization

Revenue split (by sales origin)

US: 43%

US: 45%

Revenue split (by travel class)

F/C-Class: 66%

F/C-Class: 59%

Utilization (SLF)

� Higher share of non-US-passengers

� Continued high level of utilization

� Share of premiumcustomers increased

Example: Frankfurt – New York (JFK), April 2008 versu s April 2007

SLF: 83%

SLF: 83%

Non-US: 57%

Non-US: 55%

M-Class: 34%

M-Class: 41%

2007

2008

2007

2008

2007

2008

Lufthansa Group19 Wolfgang Mayrhuber

Deutsche Lufthansa AG

Fleet Growth Flexibility (Continental Fleet)

2007 2008 2009 2010 2011 2012

Bull Case: 6.9% p.a.Increase capacity by delaying aircraft

phase-outs

Bear Case: 0.0% p.a .Reduce capacity by increase of roll-overs

and MRO checks

Base Case: 4.8% p.a6% on long-haul, 4% on short-haul

in SKO

Short-haul

Long-haul

Total

mid-term2008

5.1%

8.0%

7.1%

4%

6%

5%

Planned capacity growth

Our growth path can be adapted

Planned growth and scenarios Lufthansa Passenger Airli nes

Lufthansa Group20 Wolfgang Mayrhuber

Deutsche Lufthansa AG

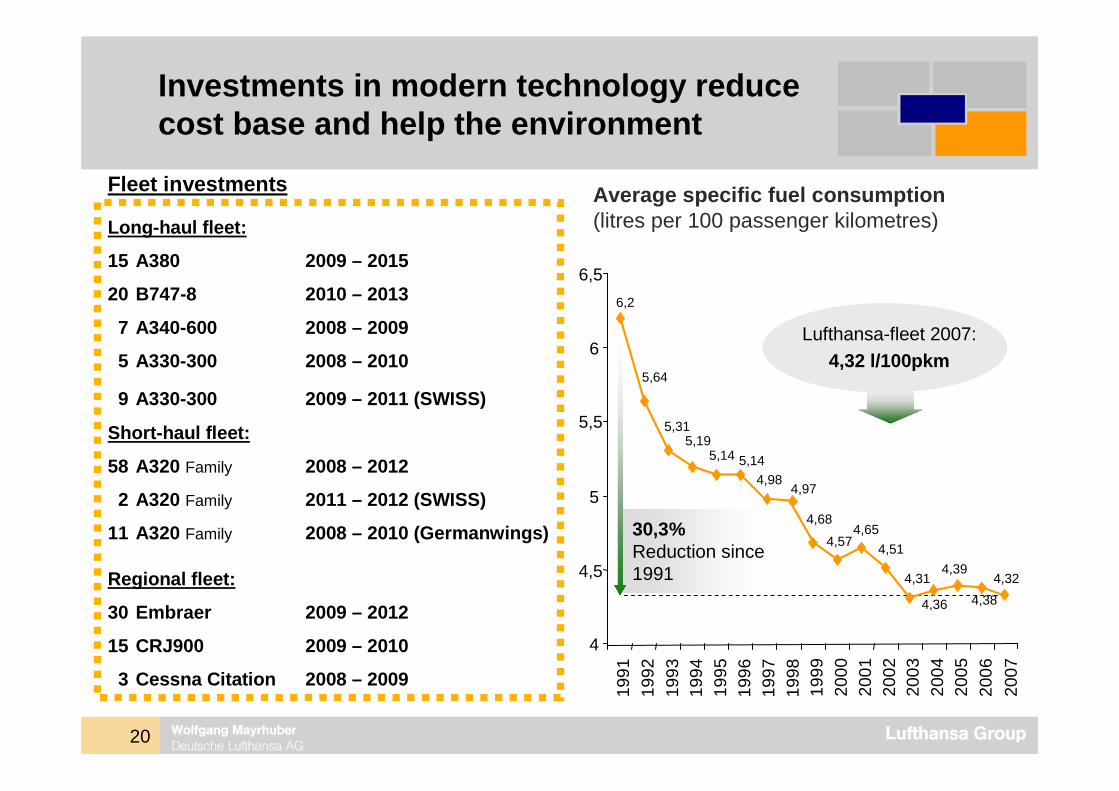

Investments in modern technology reducecost base and help the environment

Average specific fuel consumption(litres per 100 passenger kilometres)

30,3%Reduction since 1991

Lufthansa-fleet 2007:4,32 l/100pkm

4,31

4,36

4,39

4,38

6,2

5,64

5,315,19

5,14 5,14

4,984,97

4,68

4,574,65

4,51

4

4,5

5

5,5

6

6,5

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

4,32

Fleet investments

Long-haul fleet:

15 A380 2009 – 2015

20 B747-8 2010 – 2013

7 A340-600 2008 – 2009

5 A330-300 2008 – 2010

9 A330-300 2009 – 2011 (SWISS)

Short-haul fleet:

58 A320 Family 2008 – 2012

2 A320 Family 2011 – 2012 (SWISS)

11 A320 Family 2008 – 2010 (Germanwings)

Regional fleet:

30 Embraer 2009 – 2012

15 CRJ900 2009 – 2010

3 Cessna Citation 2008 – 2009

21 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

Star Alliance: the premium network

...and new partners in 2008

More than 17,000 flights to 897 destinations in 160 cou ntries

22 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

M&A: active role if conditions are right

I. Strategic fit: „Verbundsystem“

e.g. flet allocation

e.g. network strategy

e.g. branding, product

FRA MUC DEC LX

e.g. station management, …

e.g. HR, fuel,fleet-procurement, controlling

e.g. IT, traffic rights…

XY

scalability

Holding functions

Divisions / Airlines

Support functions

II. Economic fit: financial prerequisites

� Cost-synergies

� Revenue-synergies

� Stand-alone profitability

III. Cultural fit: important „soft facts“

� Governance

� Entrepreneurship

� Risk approach

Perfect fit: integration of SWISS

23 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

Success story SWISS

2004 2007

€ 3.16 bn€ 2.27 bn

€ 345 m€ -75 m

7580

12.2 m9.6 m

7669

7,1606,085

� ☺

Revenue

EBIT

Image

Aircraft

Passengers

Destinations

Employees

24 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

Partnership with jetBlue Airways

FRA

ZRH

MUC

Locations of jetBlue Airways

� Only 2% overlap with LH and Star Alliance networks

� Second largest carrier in JFK in terms of slots

� Highest customer satisfactionof all US carriers

� Numerous awards forinnovation and quality

� Highest labor productivity, lowest unit costs

Ideal complement to LH network

Next steps

� Alignment of bonus programs

� Codeshare operations

� Marketing cooperations

25 Lufthansa GroupWolfgang Mayrhuber

Deutsche Lufthansa AG

Lufthansa is fit for the future

Short-term:

� Good start into the year

� Booking trend remains stable

� Fuel hedging benefits

� Follow-up on 2007 profitability level remains achievable

Long-term:

� High oil price on current levels imposes significant risks to the industry

� Economic environment will shape and restructure the industry

� Lufthansa has financial strength, is flexible to adopt to market changes and cantherefore benefit

� Our commitment is the sustainable development in the interest of our shareholders

� Lufthansa is a value and growth proposition

Lufthansa Group26 Wolfgang Mayrhuber

Deutsche Lufthansa AG

Disclaimer

This presentation is for informational purposes only, contains preliminary financial and other information about Lufthansa and is subject to updating, revision, amendment and completion. This presentation does not and is not intended to constitute or contain any offer of securities for sale or a solicitation of an offer to purchase any securities of Deutsche Lufthansa AG or any other company and neither this presentation nor anything contained herein shall form the basis of any contract or commitment.

Certain statements contained in this presentation may be statements of future expectations and other forward-looking statements or trend information that are based on management's current views and assumptions and involve known and unknown risks and uncertainties. In addition to statements which are forward-looking by reason of context, including without limitation, statements referring to risk limitations, operational profitability, financial strength, performance targets, profitable growth opportunities, and risk adequate pricing, as well as the words "may, will, should, expects, plans, intends, anticipates, believes, estimates, predicts, or continue", "potential, future, or further", and similar expressions identify forward-looking statements. Actual results, performance or events may differ materially from those in such statements. Lufthansa assumes no obligation to update any such statements or any other information contained herein.