november issue of meet my banker

DESCRIPTION

November Issue Of Meet My Banker presented by Pinnacle FinancialTRANSCRIPT

1Version 1, Issue 1

2 Version 1, Issue 1

Contents

3 | Letter from the EditorA few words from Troy Fullwood

4 | Seven Serious Financial Mis-takes Small

Business Owners Make

5 |Traits of Those Who Will Survive The Recession

We have seen that those who have weath-ered this storm most effectively and with a minimum amount of trauma shared several characteristics:

6 | Must ReadsMust read books for November plus our top 10 list

7 | Including Real Estate Invest-ments within Your Retirement

Including Real Estate Investments within Your Retirement Portfolio

8 | Transactional Funding The traditional ways of making money in the real estate business as investor or broker, agent or mortgage

professional have changed.

9 |Keeping a Piece of the Action Including Real Estate Invest-ments within Your Retirement Portfolio

11 |Build Wealth Fast With A Powerful Personal

Financial Plan

13 |Profitable Real Estate Investing Is Alive

14 |Turn Key In-vesting For Out-Of-State Investors

15 |How To Raise Capital For Your Business

16 |Some Small Business Loans Explained

17 |MeetMYBANKERRound Table Inner Circle

3Version 1, Issue 1

Dear Reader,

Welcome to the very first edition of Meet My Banker Maga-zine. I want to take a moment and share with you the mis-sion behind Meet My Banker;

I have created this magazine to fill a void in the market place between Lenders and Borrowers – it is that simple! The goal is to bring the two sides together quickly and ef-fectively.

Every week I receive dozens of phone calls into my office from Lenders wanting to lend money on various types of projects throughout the US. At the same time, I receive doz-ens of phone calls from investors and entrepreneurs look-ing for money for their projects and investments.

The types of requests that I receive are everything from – Hard money, bridge financing, commercial lending (for purchase and rehabilitation work), mezzanine financing, busi-ness loans, unsecured loans, equity loans, Etc. – I think you get the picture.

What you will find in this edition and the up and coming editions are a number of direct institutional and private lenders that I will be profiling and interviewing for your benefit. From this day forward, the goal of this magazine is to put direct lenders in contact with di-rect borrowers – no matter what kind of project they are working on – simple but effective.

I truly feel that by putting the two parties together it will create a win – win environment for both sides.

The bottom line is; if we can keep the money in circulation then the business owners will be successful and so will the lending community.

Wishing everyone massive success.

Sincerely,

Troy Fullwood

Letter From The Editor

4 Version 1, Issue 1

Header Text Goes Here

Borrower BewareYour business needs money. No surprise there, every business needs money to take care of overhead...meet payroll...pay for supplies...grow...and to...well...stay in business.

But how you get that money...and what you do to get it...can have a critical impact on the future of your business.

That’s what this article is for. To warn you of the hazards and risks in following what might seem to be conventional wisdom in financing your business. And to show you an alternative.

Serious Mistake # 1Using personal credit to finance your businessIt’s also the most common mistake. And it rang-

es from paying for business expenses with your personal credit cards to obtaining personal loans to finance the business and its expenses.When you use your personal credit to buy business items, you reduce the amount of credit you have available for personal and family use. You’ve already used if for business expenses. And should you need that credit to see you through an emergency—such as an accident or illness that keeps you from working—you could be in a real bind.

How to avoid itObtain credit in your company’s name. Not yours.

Serious Mistake # 2Putting personal assets at riskThis one is a lot like #1 and it’s equally dangerous. It comes from putting your assets—your home, for example—up as collateral to guarantee repayment of a loan for your business. The danger is that if your business should fail—and 85% of all small busi-nesses do within their first year—you could lose not only your company but your home or any other asset you’ve pledged.Remember, if you have personally guaranteed any type of credit for your business and your business can’t pay off its debts, you’ll have to repay the loan. Personally.

How to avoid itIncorporate your business rather than estvablishing it as a sole proprietorship. When prepared properly incorporation can shield you from personal liability for the compa-ny’s debts and also offers other tax advantages as well.

Serious Mistake # 3Not paying bills on timeSounds like a no-brainer, doesn’t it. After all, how can you expect to build good credit if you don’t pay your bills on time? But when cash flow isn’t exactly flowing, it’s easy to get behind on the bills. And that can take your business down the tubes.As an en-trepreneur, you can’t afford even a single late payment. Your credit file is a complete history of your credit activity. One late payment can be held against you for years. And it can be the basis for denying you new credit when that credit is crucial to your company’s survival.

How to avoid it.Pay your bills—both personal and business—on time. If you should be late with a pay-ment, contact the lender immediately, explain the situation and promise it won’t happen again. If you’re lucky, you may head off a negative report.

Serious Mistake # 4Using your family’s money Maybe it’s persuading your spouse to use his or her credit card to help bail out the business. Or perhaps it’s borrowing from money you’ve set aside for paying for college or for retirement. Or investing your savings into your company. No matter. It all adds up to one big mistake.As we’ve pointed out, over half of all small businesses fail in their first year. Some say the percentage is actually much higher.

My point? If your business fails you could wipe out not only your own finances but those of your family as well. Just imagine how you’ll feel telling your kids they won’t be going to college.

How to avoid itMaybe investing the family nest egg into the business seems like a good idea. It isn’t. Keep your business and family finances separate and distinct.

Serious Mistake # 5Contaminating your creditThat happens if you fail to keep your credit history completely separate from your spouse’s. If your spouse isn’t as prompt in paying as you are you can, subsequently, end up with a lower credit score.

It gets even worse if you’re using personal credit to finance your business. The con-tamination can keep you from obtaining the financing you need to keep your company growing.

How to avoid itMaintain separate credit accounts. That way you’ll have separate credit histories so one spouse’s late payments won’t compromise the other’s rating. And keep your per-sonal credit separate from your business credit.

Serious Mistake # 6Failing to incorporateIncorporating your business sets its assets apart from your personal ones. Which means that if your company is ever sued—and the judgment goes against it—your home, car or other personal assets can’t be touched.

Equally important, incorporation puts you on the path to establishing corporate credit. And that is what will allow your business to ultimately grow.

How to avoid itIt isn’t rocket science but it does require a little paperwork. If you aren’t familiar with this, you may want to contact a lawyer who has an excellent reputation for setting up corporations. I may be able to assist you with this.

It’s also not a bad idea to maintain a physical office—even if it’s a home office—and get a local phone number in your company’s name. And if your business industry requires such, you’ll also need to obtain the appropriate business licenses.

Serious Mistake # 7Going it aloneYou know that if you go to your bank for a business loan, they’re going to require that you show them all of your business financials for the past two years. And if you’ve only been in business six months, that could be a problem.And you certainly don’t want to encumber your house or other personal property with a bank loan. Because if your business goes south, it’ll take your house and posses-sions with it. You’ve heard about corporate lines of credit. And that sounds perfect for your business. So you apply for one. And sit back and wait for the money you need.

If it were only that simple… Fact is: 8 out of 10 new business owners who apply for cor-porate credit lines are not approved. They are turned down flat and never know why.The reason? They’ve failed to present their businesses in a way that lenders can properly value them. Their companies may be strong and healthy but because of the way the information is organized, the lender can’t see it.

How to avoid itAllow us to obtain your lines of credit for you. After all, that’s what we’re here for.

UnCap, INC. is the leader in helping new small business owners get the financing they need in the new tightened lending environment. Up to $500,000 in fact.

All without having to present reams of documentation or encumber personal assets.

If your business could use capital with no strings attached, let’s get started. We’ll create a custom Business Aptitude Evaluation Report tailored specifically to you and your business which covers the 36 different parameters that we’ve found that can sig-nificantly impact the approval success of any loan application. The Report provides a thorough evaluation of your company and recommends the specific actions you should take to improve any deficiencies.

Authored by John W. Collins

___________________________________________________________________________________________________________ John W. Collins has led a diverse career in the financial services industry. He is currently the founder and President of UnCap, Inc., a business finance consulting firm fo-cused on educating and obtaining funding for new small business owners. You can contact UnCap, INC. at (800) 505-0013 or you can visit their website at www.TheFinanceFormula.com

Seven Serious Financial Mistakes Small Business Owners Make

5Version 1, Issue 1

We have seen that those who have weathered this storm most effectively and with a minimum amount of trauma shared several characteristics:

- They and their advisors were aware of potential exposures and were proactive in addressing them

- They are able to make their personal, family overhead commitments from ex-isting resources for an extended period of time, even without additional cash flow

- They were willing and able to adjust their lifestyles and expenditures to current economic conditions

- They lived very well, but well within their means, as opposed to at the limits of their means

- They had assets that allowed them to meet existing business financing burdens and other fixed costs in a form that they were able to liquidate at minimal delay and expense

- They had top counsel in place on tax, business and estate issues, and that counsel used a variety of strategies that not only served the primary goals but also protected those assets for the family. Some examples are the use of Insurance and Annuity Products and ILITS and Split Dollar agreements that preserve certain assets for the family by statute

- They had great credit and relationships with banks that allowed them to agree on terms that were best for all parties involved, and had these rela-tionships with several institutions

- They had long term assets that were able to be made liquid with minimal penalty and delay, despite that liquidation not being part of the original plan, i.e. long term investments with an escape or liquidity plan built in

No business is completely recession proof. Diversify and properly insulate your income streams if possible and be ready to be flexible and spot ways to identify new opportunities for your business and your skill set.

Realize that your niche, as you have defined it, may come to an end and know when to direct your assets and energy to those new opportunities. As examples, some of our clients who were major players in single family housing are now in the “economy” apartment market segment and are doing well. Doctors are expanding their practices and adding high value cash services like medically supervised weight loss to practices that were focused solely in other areas. Others have created booming new busi-nesses like debt and credit repair that directly reflect the current economy.

Don’t take your market position for granted. In a down economy discount solution, product and service providers emerge in every market. These competitors will be selling price first and many consumers won’t see the differences until they have been poorly served and you have lost the busi-ness. Some steps to fight this:

- Make sure that your network and professional relationships are as strong and developed now as they were before you reached your current level of success

Authored by Ike Z. Devji

Traits Of Those Who Will Survive the Recession

- Look for ways to distinguish yourself and your business and maintain the highest standards of professionalism and service

- Look for every way to add value and collaborate with other top services providers you work with so that you are a natural and logical part of every project or client they are involved with

- Become part of a best of class team of teams that delivers the highest value to the consumer. This is true of everything from medical services to commercial contracting

- Continue to be the best, or at least great at what you do. “Good enough” should not be part of your vocabulary

Guard your credit like gold. Good credit has always been important on both personal and business fronts, but it is now more important that ever. As credit markets have tightened even the wealthy are having trouble obtaining credit for every day issues like home and auto purchase or leasing. Banks are scared and have pulled in the reigns on lending to all but those who have sterling credit, “good” is no longer good enough. They are also using late payments of any kind to move to the default interest rates permissible under various types on loan and consumer credit agreements as a way to generate fees and increase revenue internally. On a personal level this could mean that your VISA ay 8.9% jumps to 29.99% APR if your spouse sends in the check late. On a business level it is much worse. If your course of business has been to pay certain credit lines down late to a friendly credi-tor, it could now put you into default or cause an acceleration.

We are also hearing that clients who have used revolving credit lines for years as part of their business model either for capitalization or to pay recur-ring expenses are suddenly finding that their credit lines have been termi-nated or drastically reduced as is permissible in the fine print of most such agreements. This is despite the fact that the client has had no change in income or credit. Banks are simply deciding that they have too much expo-sure and are proactively limiting your ability to draw that money out.

Solution? – If you have a credit line that you know you are going to need or cannot risk losing – draw the money out now and look at the interest cost like an insurance premium; you may not want to pay it but if you need the “insurance” of having that money available it will not be available at any cost, certainly not in any short term scenario.

There are services out there that we have referred friends and clients to with great results. For an investment of a few hundred dollars many negative or inaccurate items can be removed in a short period of time increasing your credit score by dozens of points. Check your business and personal credit reports and see if they are accurate.

We are also seeing that banks that are in financial trouble and which need to reduce their outstanding debt balances are playing dirty tricks like re-appraising property they financed over 18 months ago to “current market value” at ridiculously low valuations then going back to the borrower and saying they need more collateral or they will call they note as the “fine print” entitled them to do. How bad can this be? In one case the bank re-appraised my client’s multi-million dollar commercial property at about 50% of current fair market value and wanted an additional seven figures in collateral. For-tunately, this client had sterling credit and good professional relationships that allowed him to re-finance at a lower rate with a more solvent and ethical bank.

_________________________________________________________________________________________________________________________Mr. Ike Z. Devji, J.D. is the Executive Vice-President of the Wealthy 100 ™, a Phoenix Arizona based wealth management and wealth strategy firm with a network of advisors across the United States. Before joining the Wealthy 100, Mr. Devji, a litigator by training, acted as the Managing Attorney of the law firm of Lodmell & Lodmell, one of the nation’s leading Asset Protection only law firms, with a client base of over 3,500 clients and over $5 billion in protected assets. He was recently named as one of only 24 advisors in Worth magazine’s national list of “Leading Wealth and Legal Advisors.

6 Version 1, Issue 1

THE TOP 10 DO’S and DON’TS WHEN STARTING A BUSINESS

DO…

1. Live frugally and begin saving up money for starting your business.

2. Learn your intended business by working for someone else in the same business first. 3. Consider the benefits of starting a moonlight business. 4. Consider the advantages of operating a family business.

5. Objectively measure your skills and training against potential competition.

6. Consider subcontracting to low cost suppliers if you’re manufacturing a product.

7. Test market your product or service before starting or expanding.

8. Make “for” and “against” list describing the specific business you are considering.

9. Talk to lots of people in your intended business for advice.

10. Make a comparative analysis of all opportunities you are considering.

DON’T…

1. Think about leaving your job before you have completed start-up plans.

2. Consider starting a business in a field you do not enjoy.

3. Risk all the family assets. Limit your liabilities to a predetermined amount.

4. Compete with your employer in a moonlight business.

5. Hurry to select a business. There is no penalty for missed opportunities.

6. Select a business that is too high a risk or hurdle. Go for the two-foot hurdle.

7. Select a business in which you must have the lowest price to succeed.

8. Ignore the negative aspects of an intended business.

9. Permit self-confidence to outweigh careful diligence.

10. Allow the promise of a conceptual high reward deter reality testing first.

From www.myownbusiness.org

Execution: The Discipline of Getting Things Done

By Larry Bossidy and Ram Charan

AMAZON: $18.95

Disciplines like strategy, leadership develop-ment, and innovation are the sexier aspects of being at the helm of a successful business; actually getting things

done never seems quite as glamorous. But as Larry Bossidy and Ram Charan demonstrate in Execution, the ultimate difference between a company and its competitor is, in fact, the ability to execute. Execution is “the missing link between aspirations and results,” and as such, making it happen is the business leader’s most important job. While failure in today’s business environment is often attributed to other causes, Bossidy and Charan argue that the biggest ob-stacle to success is the absence of execution. --S. Ketchum

FreakonomicsBy Steven D. Levitt and Stephen J. Dubner

AMAZON: $16.77

In Freakonomics (writ-ten with Stephen J. Dubner), Levitt argues that many apparent mysteries of everyday life don’t need to be so mysterious: they could be illuminated and made even more fascinating by asking

the right questions and drawing connections. For example, Levitt traces the drop in violent crime rates to a drop in violent criminals and, digging further, to the Roe v. Wade decision that preempted the existence of some people who would be born to poverty and hardship. --John Moe

Must Reads

7Version 1, Issue 1

Including Real Estate Investments within Your Retirement Portfolio, Tax Free or Tax DeferredSelf-directed IRAs have quickly become the talk of the real estate community. Not only are real estate professionals self-directing their own IRA’s into property and projects, they are also using their knowledge about these plans to generate more business.

You can use your IRA or 401k to invest in real estate and harvest the same tax benefits of the retirement plan you may currently have invested in the stock market if you are using an administrative company that is equipped to handle such transactions. These alternative investment administrative companies manage all the record keeping, provide quarterly statements of investment status, and supply required reports to you and to the IRS.

Many investors today are discouraged by the recent events in the stock market. Additionally, today’s investors feel as if they have lost control over their retirement funds. Regain that control by investing in what you know best. IRA’s and qualified plans can provide funds for a unlimited array of real estate investments, including raising capital, bridge

financing, raw land, purchasing and developing commercial property, buying leases, and much more! Ironically, many financial advisors, accountants, attorneys and even real estate professionals are unaware of this option.Here are the key points to know about a Traditional IRA:

-Contributions may be tax-deductible. -Taxes are paid on earnings when withdrawn and are based on your tax rate at the time of withdrawal. -You may begin taking withdrawals without penalty at age 59 1/2. -You are required to take withdrawals at age 70 1/2. -Withdrawals before age 59 1/2 are subject to a 10% penalty, with some exceptions.

Why not opt for the truly self-directed form of any of the retirement plans available today including the Traditional IRA, the Roth IRA, an Individual (k), a SEP IRA, or a SIMPLE IRA? Most IRA administrators, such as banks or brokerage firms, limit your IRA investment choices to the products they sell – such as stocks, bonds, and CDs. These traditional brokerage firms also earn a fee and or commission for advising you, the investor. Instead, you can choose an independent administration firm that encourages and supports your desire to control your own investment decisions in what you know best.

Understand these real estate investments are just that, investments. The real estate investment must be one that is an “arms-length” transaction. This means that the IRA accountholder, as well as certain family members and business associates (disqualified persons) cannot live in a property, rent office space in a property, provide a service or be involved in transactions in which the IRA buys or sells the property. The critical issue for many is making sure the property remains strictly an investment by avoiding self-dealing or prohibited transactions with family members or business associates. And an investor needs to be aware that all expenses, fees, etc. will have to be paid out of the retirement account. But don’t let that discourage you as retirement accounts can partner together in an investment. Utilize the investment power of multiple retirement accounts from people you trust and may already be doing business with. You may find many objections from your current advisors such as “that’s illegal”, “it’s too complicated” or “I’ve never heard of that.” Within the Internal Revenue Code (IRC) section 408, the IRS defines an IRA as follows: ‘An individual retirement account means a trust created or organized in the United States for the exclusive benefit of an individual or his beneficiaries…..’ To simplify things even further, the IRC is not written to specifically address what you CAN invest in. It is written to address what you CANNOT invest in. The IRC only prohibits two types of investment transactions; collectibles and life insurance. You may find a detailed description of how the IRS determines exactly what qualifies as a collectible or life insurance transaction within the Internal Revenue Code (IRC) 4975.

Don’t be confused by the marketing term “self-directed.” All brokerage firms will offer you their version of self directed. This means you can self directed your money into any of the stocks, bonds or mutual funds they offer. That is where your investment choices end. Finding a truly self directed IRA admin-istrative firm is not difficult. Some refer to this specific type of IRA as a “Real Estate IRA.” While this is not technically the legal description of a real estate investment within an IRA you can see how this might be the perfect description for the investor who is new to this option.

Alternative investments within your retirement plan are not limited to real estate transactions. A retirement plan holder may hold a promissory note, invest in an LLC, tax lien certificates, auto paper, accounts receivables, joint ventures, commercial paper, precious metals, renewable energy, motorsports and the list goes on. The bottom line is, you can control your plan and self-direct it into investments other than or in addition to, stocks, bonds, and mutual funds.

________________________________________________________________________________________________________________________Entrust Arizona LLC is the leader in self directed IRA and 401k administration. Located in Phoenix, AZ and offering over 20 free educational workshops a month, you are encouraged to maximize the potential of your retirement assets as you see fit.

You can contact Entrust Arizona LLC at (480) 306-8404 or you can visit their website at http://www.entrustarizona.com/

Co-authored by – JP Dahdah and Timarie McClendon

Including Real Estate Investments within Your Retirement

8 Version 1, Issue 1

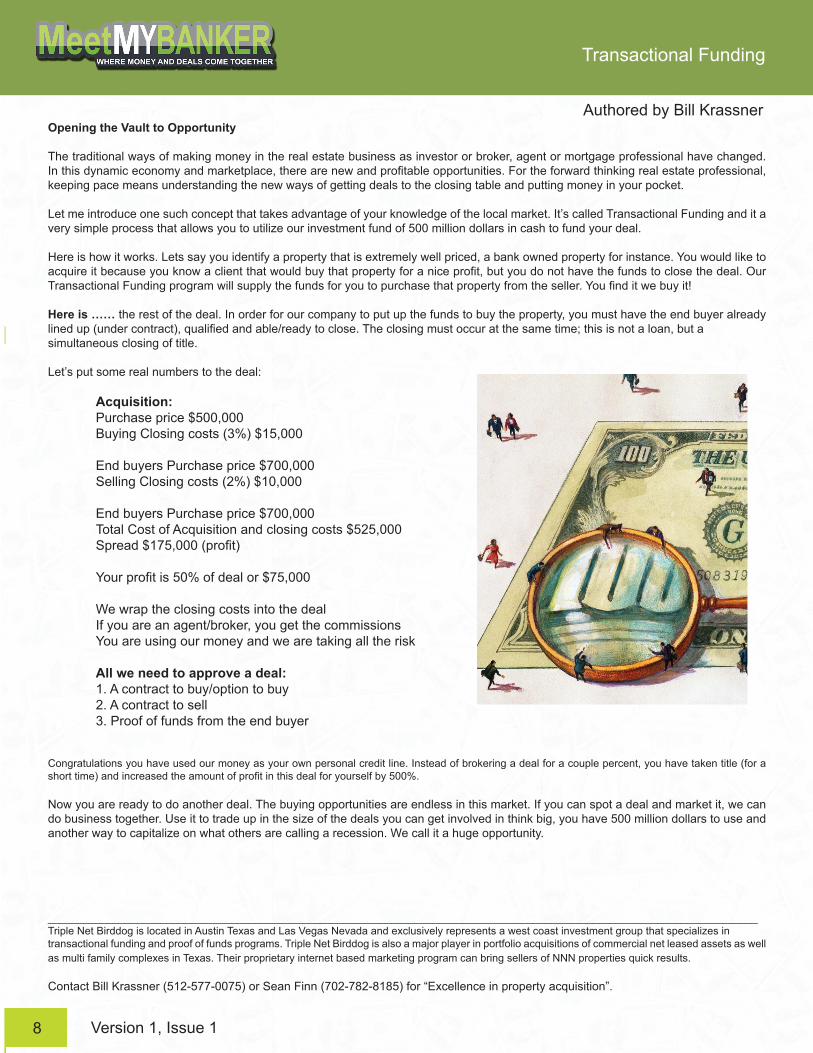

Opening the Vault to Opportunity

The traditional ways of making money in the real estate business as investor or broker, agent or mortgage professional have changed. In this dynamic economy and marketplace, there are new and profitable opportunities. For the forward thinking real estate professional, keeping pace means understanding the new ways of getting deals to the closing table and putting money in your pocket.

Let me introduce one such concept that takes advantage of your knowledge of the local market. It’s called Transactional Funding and it a very simple process that allows you to utilize our investment fund of 500 million dollars in cash to fund your deal.

Here is how it works. Lets say you identify a property that is extremely well priced, a bank owned property for instance. You would like to acquire it because you know a client that would buy that property for a nice profit, but you do not have the funds to close the deal. Our Transactional Funding program will supply the funds for you to purchase that property from the seller. You find it we buy it!

Here is …… the rest of the deal. In order for our company to put up the funds to buy the property, you must have the end buyer already lined up (under contract), qualified and able/ready to close. The closing must occur at the same time; this is not a loan, but a simultaneous closing of title.

Let’s put some real numbers to the deal:

Acquisition: Purchase price $500,000 Buying Closing costs (3%) $15,000

End buyers Purchase price $700,000 Selling Closing costs (2%) $10,000

End buyers Purchase price $700,000 Total Cost of Acquisition and closing costs $525,000 Spread $175,000 (profit)

Your profit is 50% of deal or $75,000

We wrap the closing costs into the deal If you are an agent/broker, you get the commissions You are using our money and we are taking all the risk

All we need to approve a deal: 1. A contract to buy/option to buy 2. A contract to sell 3. Proof of funds from the end buyer

Congratulations you have used our money as your own personal credit line. Instead of brokering a deal for a couple percent, you have taken title (for a short time) and increased the amount of profit in this deal for yourself by 500%.

Now you are ready to do another deal. The buying opportunities are endless in this market. If you can spot a deal and market it, we can do business together. Use it to trade up in the size of the deals you can get involved in think big, you have 500 million dollars to use and another way to capitalize on what others are calling a recession. We call it a huge opportunity.

________________________________________________________________________________________________________________________Triple Net Birddog is located in Austin Texas and Las Vegas Nevada and exclusively represents a west coast investment group that specializes in transactional funding and proof of funds programs. Triple Net Birddog is also a major player in portfolio acquisitions of commercial net leased assets as well as multi family complexes in Texas. Their proprietary internet based marketing program can bring sellers of NNN properties quick results.

Contact Bill Krassner (512-577-0075) or Sean Finn (702-782-8185) for “Excellence in property acquisition”.

Authored by Bill Krassner

Transactional Funding

9Version 1, Issue 1

Although debt paper can take many forms, ranging from mortgage notes to lottery winnings annuity contracts; we can usually describe the loan notes held by brokers and investors by placing them into one of two basic categories:

1. First lien notes that they can sell for a lump sum.

These notes have a beginning and an end, and when they are paid off, the note is canceled and no longer represents any debt.

2. Second lien notes that may be much smaller but offer the security of regular and gradual monthly installments of income.

These notes are created to take advantage of equity, for instance, and represent a new loan that will be paid off after the first lien has been satisfied. If someone owns a house with a first lien mortgage of $300,000 and they later borrow $15,000 against the value of their house in order to update a bathroom; the smaller note becomes the second lien.

By simply slicing up some of their debt paper pie, brokers can have their cake and eat it too, by creating a portfolio of diversified investments. Rather than putting all their eggs in one basket by only investing in first lien debt, they can rely on both short-term payments and longer-term payouts, by choosing to restructure some of their inventory of notes.

For example, if an investor wants to have a steady stream of income – maybe to plan for retirement or to help add principle to a college tuition savings account – the notes can be created with different maturation dates. By staggering the payments so that there are always some notes coming due while others are still “ripening”, the investor enjoys predictable monthly cash flow.

When the government advertises and sells treasury notes, the same idea is used to attract buyers. You can buy short-term notes of a year or less, and you can buy notes that don’t mature for many years. You might buy a long-term note to help finance a child’s education, and let the note sit for 15 or 20 years. A short note – say three years or less – might be more advantageous if you are planning to pull money out of the stock market temporarily and let it

accumulate interest only until the next stock market upswing.

When a first lien note is sold, the seller gets paid and the lien is transferred to the new Note Owner. As far as the seller is concerned, there is no more action to be had in that particular note and it is time to look for another investment. But if the seller creates a second lien note on the property, the transaction becomes two-tiered. Even though the first note is paid off in full, the paper is still active because of the remaining second note. The entire note may be for $100,000, and the second lien is only for $10,000 – but several of these smaller notes taken together can represent a substantial investment portfolio, with a prudent level of built-in diversity.

Brokers who trade in debt paper often keep an inventory of various types of notes, so that they can tailor their investment packages to suit a client’s needs. And those who find themselves with mostly first lien notes can create smaller second liens, to automatically gain a diverse portfolio with twice as many options and opportunities.

_________________________________________________________________________________________________________________________Mr. Troy Fullwood is a nationally known mortgage investor and real estate coach who frequently speaks and writes on the topic of Private Financing. With thirteen years of experience in the Private Financing arena, Mr. Fullwood has developed a strong network of relationships with a diverse body of lenders and real estate investors, and he has been involved in more than 12,000 mortgage transactions totaling over half a billion dollars.

Meet My Banker readers may contact Troy Fullwood at (888) 736-5353, or by email [email protected]

Keeping a Piece of the Action

Authored by Troy Fullwood

10 Version 1, Issue 1

11Version 1, Issue 1

Accounting for your own personal finances is the first step toward building lasting wealth. It is essential to know the amount of your Owner’s Equity before you can start to develop a good financial plan.

Once you know what your assets are, and you know what your liabilities are, then you can calculate your Owner’s Equity. Then you can develop a financial plan to reduce your debt and achieve your financial goals.

Here is the Generally Accepted Accounting Princi-ples (GAAP) accounting equation:

Assets = Liabilities + Owner’s Equity

Let’s start with the right side of the equation. First, you must calculate the amount of your outstanding liabilities. This means you write down in a list exactly how much you owe right now on your mortgage, credit cards, and any other bills or loans.

Next, let’s go back over to the left side of the equation where the assets are. Make a list of every asset you own. Examples would be your cars, home and cash you have in the bank. List all of your major assets.

Now we will determine your Owner’s Equity. Simply use this variation of the preceding equation to arrive at your present Owner’s Equity (how much you really own):

Assets - Liabilities = Owner’s Equity

If you want to increase your Owner’s Equity you must pay down your li-abilities and avoid borrowing more money to buy more assets. Responsible saving, investing and proper paying down of your debts is crucial to your financial success.

Most experts agree that you need to allocate money every month for all these areas of your financial plan. It is not enough to just save some money in the bank. Because if you are carrying a credit card balance at the same time, you are losing all the benefits of the interest coming from your savings account.

Here is an example of a good financial plan:

1. Take the money that you are presently putting in your savings account every month or investing in other places and divide the total amount by 3.

Then,

2. Pay down your outstanding debts with one third of this money every month.

3. Take one third of this monthly allocation and simply place it in your sav-ings account at your bank. This will be the pool of money you can use to balance out your monthly needs. As this money grows over time you can use it to finance your family’s future needs or apply it to the goals of your financial plan.

4. Use another one third of this money and buy 1-5 year Certificates of Deposit. It is best to save up enough money to buy a CD of $1000.00 every time you invest. A good rule of thumb is to buy one CD every three months to six months. Remember to keep enough cash in your checking and pass-book savings for any emergency.

By adhering to these tips you will pay off your liabilities in a timely manner. When you invest in 1-5 year CDs you will be earning interest and com-pounding your money by purchasing more CDs at specific intervals.

The biggest roadblock to financial success is accumulating a large credit card debt and not paying it off as fast as possible.

It is also recommended that when you have enough money saved up in your regular savings account, you begin to accelerate your mortgage payments every month. Check with your mortgage lender to see if your mortgage al-lows you to pay more per month than your regular payment. If so, start to pay more every month on your mortgage than you are required to. You will build equity in your home faster, save on interest charges and retire the mortgage much sooner.

By using a proven financial strategy such as this one you can reduce your debt faster, and build wealth for your family quickly. The above steps are by no means the only way to build wealth. These principles are basic and nec-essary though. Your family can be on the way to a brighter financial future when you prioritize your spending, saving and investing habits. After all, it’s your money; why not put it to its best use!

Build Wealth Fast With A Powerful Personal Financial Plan

Authored by Marc Entz

12 Version 1, Issue 1

13Version 1, Issue 1

People often ask me “when do you think we will see the real estate market bottom out?” And I answer with “well that depends”. The answer to this trick question has too many variables to mention here. However, as we watch and follow the news we can see that the “nation-wide” housing crisis is really only about 45 to 50 percent through it’s much needed and long overdue market retraction. As the next wave of foreclosures begin flooding most of the nationwide MLS databases, home prices in most of the U.S. will start to reflect this high volume of inventory by… yep, you guessed it, by dropping!

So why invest in real estate now when we know prices will drop another 15 to 30%? Well that’s an easy one! I had mentioned earlier that this is a “nation-wide” crisis, however there are parts of this country that hit rock bottom over 2 years ago and are starting to show signs of recovery and are NOT part of the next wave of fore-casted foreclosures.

These areas have an abundance of individuals and families that are hard working, loyal and ready to get their life back through taking ad-vantage of local affordable housing provided by a brand new innovative private bank that under-stands the power and value of rebuilding com-munities and providing loan terms that the home-

owner can afford with ease, and for years to come. This bank also understands that these home owners do not have excellent credit anymore due to a recent or pending foreclosure, however they are willing to dig a little deeper into the prospective homebuyer’s financial profile to assess the risk and provide financing when most major banks and lenders simply cannot…at least for now.

What is the name of this bank you ask? The bank is YOU! Private cash investors are now the bank during this current market retraction and these investors are cleaning up in more ways than one!

With an abundance of individuals and families ready, willing and able to get back into afford-able homeownership, the time is now to “clean up” these bedroom communities and for you to be the bank for huge returns on your investment.

Be part of the solution, not the problem! For more information on the above, including the locations I am writing about, please visit us at www.reoremedy.com

_________________________________________________________________________________________________________________________Jeff Wetzell founded REO Remedy in October of 2007. REO Remedy provides a full service, 100% turnkey, passive real estate investment strategy. Prior to starting REO Remedy, Jeff was a mortgage broker/ real estate investor and began his real estate career in 1991 as a part time residential property researcher in Southern California for a number of highly successful investors. This experience led him into a fulltime success by the late 90s to present.

Authored by Jeff Wetzel

Profitable Real Estate Investing Is Alive

14 Version 1, Issue 1

Are you having reservations about in-vesting in a property that may be 100 or even 1000 miles away? Worried about all the coordination and issues that may arise? This is a natural reaction. How-ever, when done properly with the right company, Turn Key Investing is much easier and less stressful than you would imagine. It sure beats today’s volatile stock market.

Step 1 – Do you need to invest out of state?

In many cases, this answer will be yes. In today’s market, there are fewer and

fewer positive cash flow and appreciating real estate markets. Therefore, many investors are turning to other markets like Birmingham, AL, Jack-son, MS and Memphis, TN. To earn $100-$200/ month positive cash flow in Southern California may require a property that can be several hundred thousand dollars or does not exist at all. In the smaller niche markets, you can achieve similar cash flow for a fraction of the cost. Often, our California investors drive cars that were more expensive than their rental properties.

Step 2 – How do you find the right city?This will be a matter of personal preference. There are great markets all across the United States. We have found that homes in the Southeast work best for us. However, I encourage you to do your research. Make a list of your criteria (average home price, revitalization potential, average rental amounts, potential cash flow, etc…). CNN/Money, Fortune, Nuwire Investor, Realty411 and the like are some great places to find information.

Step 3 - Finding the right Turn Key Company.If you have ever opened the yellow pages to “Real Estate”, you know that there is an ocean of companies wanting your business. It is important to keep an open mind and remember that you want a properly managed, leased, remodeled house with a crew on the ground in case of repairs and issues. You can’t drive over and fix a toilet flapper so your ‘team’ is going to have to be there for you. Your average big company agent is not going to be able to provide these things. Start with professional wholesalers with a good reputation and a history of success. Contact them, ask them some preliminary questions…. How long have you been in business? How many houses have you sold? Do you have references? What do you offer? Do you provide a new tenant if mine does not work out?, Do you personally own any property in the areas where you sell? , etc….

Then, the best question of all ”Can I fly out and visit your properties”. If they have any reservations about you coming to their town, red flags should be going up. After talking to a few companies you should be able to make an educated decision.

Authored by Chris Donaldson

Turn Key Investing For Out-Of-State Investors

There is also the very powerful Google Search Engine, www.Google.com. Try the phrase ‘wholesale residential property’ or ‘top cash flow markets’. Hopefully, this is going to be a long and productive relationship for both par-ties. You want to know who you are working with. I can’t count the number of times my partner and I have spent hours on the phone talking about eve-rything from our childhood to our favorite football team. At our company, we even have a checklist of ‘what to expect next’ that we give to all potential clients. It contains some information on obtaining insurance, lining up financ-ing, setting a closing date, etc… Many of our clients are first time buyers and need a little guidance. That is not a problem. Everyone had their first pur-chase at some point and we understand it can be a tense and nervous time. Inquire about their remodel practices. Do they refinish hardwood floors or use carpet? Do they replace the roof or guarantee it for ‘x’ amount of time? Are the houses electric, gas or both? What if something happens right after you buy it? i.e. – a pipe burst in the front yard or a leak is discovered. Do they update electrical systems? Do they do small things like installing ceiling fans or replace all the plugs and switches. Do they add insulation? Ask about their tenant placement. What is the average time on market for them to rent a home? Do they have a log of tenants? How do they obtain tenants? Do they use any government subsidies like Section 8 (see my pre-vious article in the last issue. We love this program). Do they have a leasing manager that will show your property? Do they cut the grass, take care of the utilities, secure the home if/when you are vacant? Do they provide help in obtaining another tenant if the first one moves out?

#1 ISSUE FOR OUT OF STATE INVESTORS – PROPERTY MANAGEMENTThis will be the absolute #1 most important factor you need to investigate. Good property management is like panning for gold. It is out there, but really hard to find. I have gone through several different managers in my career and have finally found what I was looking for. Here is what you want; prompt response to your calls or emails. Immediate notification if your tenant is pay-ing late or not at all. A clear explanation of what happens in the event you need to perform an eviction. Notification and approval of all repairs over ‘x’ dollar amount (you don’t want a surprise $4K air conditioning bill). A reliable and timely statement each month. 24/7 service for your tenants. Finally, a friendly staff that will honestly care about you, your property and your ten-ant. For this type of service, you can expect to pay 8-10% of collected rents. Worth every cent.

I hope I have shed some light on the great opportunities that are out there in today’s market. I believe that you can find the right fit by using some of the tips above. Investing out of state does not have to be a hassle. It is not al-ways perfect, nothing is, but overall we believe our clients are building great portfolios and we take pride in helping them. Good luck on your investing and feel free to contact me anytime.

________________________________________________________________________________________________________________________Chris Donaldson worked in the banking and web technology industry for 8 years. In late 2006, He and his partner Justin Harrison decided that they would partner up and buy an 8 unit apartment building. Before he knew it, he had to quit his ‘safe’ tech job and they started Premier Equity Group. Things started moving fast as they were doing foreclosure remodeling and hitting the California seminar trail. Since then, they have been involved in over 100 home sales and many large commercial deals

You can contact Premier Equity Group, LLC at (205) 201-6663 or you can visit their website at www.equitygrouponline.com

15Version 1, Issue 1

Authored by Patty Baldwin

How To Raise Capital For Your Business

Raising capital to start a new business may seem like a daunting task, but it need not be overwhelming if you follow a few basic business practices. If you have a viable idea that will net a return for your investors and prepare a compelling business plan the chances are good that you can find investors to join you.

Your first task is to create a business plan, sometimes known as a “business proposal” or “prospectus.” Your business plan needs to be very detailed and concise. You should include information about your educational background, experience and training in the area of business you are contemplating. Just like a resume for a job, include references and any other favorable personal qualities that you feel reinforce the reasons why an investor should trust in your ideas.

It can’t hurt to include any information you feel comfortable sharing with regard to your positive credit history. If you have records of various satisfied loans along with the payment history, that information could be helpful to prove your stability with regard to financial obligations.

If you are requesting financing for an existing business the rules are a bit different than a new business startup. The current owner should be able to provide you with profit and loss statements. If you are purchasing an online business, statistical information pertaining to traffic, number of units sold and paid advertising are definitely necessary. The purchase price of the business needs to be included along with detailed information about how you intend to service the debt as well as how the potential investor will benefit from your request.

If you are seeking investors for a new business, the information required increases. In addition to the information outlined above, you will need to include market research, projected costs and a detailed summary of how you intend to generate income. This information needs to be projected for a period of three to five years. It’s a good idea to project your expenses on the high side.

Have some idea of what you expect to pay your investor. The only reason someone is going to lend you money is if they can see decent profits in exchange for lending it to you. Your market research had best substantiate that your plan is viable and will provide them with sufficient return on investment to justify their involvement.

Before you begin your search for investors, it’s a good idea to have an attorney and/or accountant take a look at your plan. A good professional may sug-gest specific points that you may have overlooked.

Once your paperwork is in order, it’s time to start looking for investors. One place to begin your search might be friends or family. You might approach them singularly or in a group. Whatever method, you need to have a complete copy of your proposal carefully outlining your research and what they can expect in return for their assistance.

Read the classified pages of your local newspaper. Venture capitalists often advertise this way. Their rates are usually pretty high because they have a tendency to take on “risky” investments. A twist on this method might be to run your own ad either locally or nationally. If you select this method, explain the particulars and emphasize how much they can expect to receive for the load of their funds.

Use local business directories to find companies that specialize in “investment services.” You can approach a local bank, but try and find a bank that spe-cializes in industrial or business type loans.

You might consider incorporating and selling stock in the company.

Another option might be a “money broker.” This can be risky. There are some legitimate brokers and others who operate on the shady side.

Be creative. If you believe in your idea, don’t be afraid to do what ever it takes to launch. There are plenty of ways to come up with the capital you need. Think outside the box. Whether you are looking for $300 or $300,000 the money is there you just need to dig for it.

16 Version 1, Issue 1

It can sometimes be a little bit daunting if you are either thinking of starting a new business or possibly expanding your present business; you realize that you need some sort of a small business loan but until you have a good idea of what the various loans are called and what they can be used for, how do

you know who to approach for that loan and what to ask for? Here are some of the terms explained:

A business expansion loan

If a business is doing well and the owner is feeling restricted because the premises are too small or they need to take on more employees in order to get a bigger share of the business available, then the owner might well consider taking out a business expansion loan. This loan will probably be easier to get than a business start-up loan, providing the business is already profitable, as the lending company will have the company accounts to check over and give them confidence that the business owner will be able to repay the loan.

A bridging loan

A bridging loan is probably the least stable of all the loans that a small business owner might consider. This is where the business owner needs to sell something in order to release some finance and has perhaps a property for sale. Usually for a high APR %, the business owner will be able to arrange a bridging loan on a property but many things can go wrong in the house selling market and there is a distinct risk that the property will not sell and then the business owner would have the burden of the bridging loan on his shoulders, as well as the problems of starting up and running a business.

Bad credit business financing

If you have gotten stuck in a low-paying job and you’ve ended up racking up your credit card, you may find that you are being sucked into a bad credit black hole, where your committed outgoings exceed your income and the increased credit card charges are beginning to swamp you. Your credit rating will start to deteriorate and it will become more and more difficult to get credit.

If you are prepared to do all the work that is necessary to start a new business and you have a good business in mind, it is possible that you could get some sort of business financing; this is known as bad credit business financing and it will probably come with some helpful conditions which allow lesser initial payments while you get back on your feet but then the payments will increase significantly after perhaps 6 months or a year.

Business line of credit

Unlike most loans which make the agreed finance available straight away, a business line of credit is an agreed amount of credit that the borrower can draw on at any time up to the agreed limit; interest is only charged on money that has actually been drawn from the loan account, so this tends to be very convenient for a small business starting out and you are not having to pay interest on money that is just sitting in your account waiting for you to use it. The interest rate is less than the interest rate charged by credit cards but higher than a normal business loan; in addition there will be a fee involved in setting up the line of credit.

Some Small Business Loans Explained

Authored by Mike Horley

Business Expansion Loan

Bridge Loan Companies

17Version 1, Issue 1

Listen in to Candid Conversations as We Grill These Experts… • We ask the questions you don’t normally hear on their PUBLIC interviews • We get beyond the standard answers and get to the deeper level where they reveal how to work with Lenders as well as the “Good, Bad, and Ugly” about investing smart.

Every month you can get a short list of high-leverage, barrier-busting, profit-boosting strategies that you can put to work in your financial life right away- and jump-start your success using the best minds in the business to build your business!

http://meetmybanker.com/specialoffer2.html