partnership debt allocations and new irs regulations

TRANSCRIPT

WHO TO CONTACT DURING THE LIVE EVENT

For Additional Registrations:

-Call Strafford Customer Service 1-800-926-7926 x10 (or 404-881-1141 x10)

For Assistance During the Live Program:

-On the web, use the chat box at the bottom left of the screen

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register

additional people, please call customer service at 1-800-926-7926 x10 (or 404-881-1141 x10). Strafford

accepts American Express, Visa, MasterCard, Discover.

• Listen on-line via your computer speakers.

• Respond to five prompts during the program plus a single verification code.

• To earn full credit, you must remain connected for the entire program.

Partnership Debt Allocations and New IRS

Regulations: Minimizing Tax Consequences

THURSDAY, DECEMBER 7, 2017, 1:00-2:50 pm Eastern

FOR LIVE PROGRAM ONLY

Tips for Optimal Quality

Sound Quality

When listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, please e-mail [email protected]

immediately so we can address the problem.

FOR LIVE PROGRAM ONLY

Dec. 7, 2017

Partnership Debt Allocations and New IRS Regulations

Nickolas Gianou

Skadden Arps Slate Meagher & Flom, Chicago

Brian Krause, Partner

Skadden Arps Slate Meagher & Flom, New York

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

5 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Beijing / Boston / Brussels / Chicago / Frankfurt / Hong Kong / Houston / London

Los Angeles / Moscow / Munich / New York / Palo Alto / Paris / São Paulo / Seoul

Shanghai / Singapore / Tokyo / Toronto / Washington, D.C. / Wilmington

Partnership Debt Allocations and New IRS Regulations

December 7, 2017

Brian Krause & Nickolas Gianou

6 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Background on Sections 707 and 752

7 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Partnership

Assets w/ basis of

$100 and FMV of

$1000

• Section 721: Exchange of

Assets for an interest in

Partnership is generally tax-

free both to Partnership and

Contributing Partner (but see

Section 721(b)).

• Section 722: Contributing

Partner takes a “substituted

basis” in the partnership

interest it receives (i.e., its

basis in the partnership

interest equals its basis in the

property contributed).

• Section 723: Partnership

takes a “carryover basis” in

the asset contributed (i.e., the

same basis in the asset as

Contributing Partner’s basis in

the asset prior to the

contribution).

Partnership

Interest

Contributing Partner

Other

Partners

Overview of Partnership Provisions—Contributions

8 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Overview of Partnership Provisions—Distributions

Partnership

• Section 731: Recipient

Partner does not recognize

gain on a distribution of cash,

except to the extent that the

amount of money (or FMV of

“marketable securities”)

distributed exceeds Recipient

Partner’s basis in his

Partnership interest.

• Section 733: For non-

liquidating distributions,

Recipient Partner’s basis in its

interest in Partnership is

reduced by the amount of

money and the basis of other

property distributed to

Recipient Partner.

Recipient Partner Other

Partners

Cash

9 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Disguised Sales – Key Exception to Nonrecognition

• As a consequence of the foregoing rules, absent an exception, a

partner would generally be able to contribute appreciated property to a

partnership and receive cash distributions from that partnership up to

the partner’s basis in the property, all without recognizing any gain.

E.g.:

− Partner A contributes Appreciated Property with a basis of $100

and FMV of $1000 to Partnership, and Partner B Contributes

$1000 dollars. Under the general rules, Partnership could

distribute up to $100 of cash to Partner A (or more if Partnership

has liabilities that are allocated to Partner A; see discussion of

Section 752 below) before Partner A recognizes any gain.

• The disguised sale rules of Sections 707(a)(2)(B) and the regulations

thereunder are an important exception. These rules treat certain

contributions and related distributions as together being part of taxable

sale of property.

10 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Disguised Sales Generally

• Section 707(a)(2)(B) – If

− (i) there is a direct or indirect transfer of money or other

property by a partner to a partnership,

− (ii) there is a related direct or indirect transfer of money or

other property by the partnership to such partner (or

another partner), and

− (iii) the transfers described in (i) and (ii), when viewed

together, are properly characterized as a sale or exchange

of property,

then the transactions will be treated as occurring between

the parties (either the partner and the partnership or two or

more partners) acting other than in their capacity as

members of the partnership.

11 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Disguised Sales – Regulatory Landscape

• Treas. Reg. § 1.707-2 – Disguised payments for services [Reserved]

• Treas. Reg. § 1.707-3 – General rules related to disguised sales of

property by partners to partnerships

• Treas. Reg. § 1.707-4 – Rules related to guaranteed payments;

preferred returns, operating cash flow distributions, and

reimbursements of preformation expenditures

• Treas. Reg. § 1.707-5 – Rules related to liabilities

• Treas. Reg. § 1.707-6 – General rules related to disguised sales of

property by partnerships to partners

• Treas. Reg. § 1.707-7 – Disguised sales of partnership interests

[Reserved]

• Treas. Reg. § 1.707-8 – Disclosure rules

12 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Disguised Sales – Tests for Identifying a Sale

• Facts and circumstances test – Treas. Reg. § 1.707-3(b)

− Must show

» (1) that the transfer of money or other consideration would not have

been made but for the transfer of property; and

» (2) In cases in which the transfers are not made simultaneously, the

subsequent transfer is not dependent on the entrepreneurial risks of

partnership operations.

− Regulations outline ten “facts and circumstances that may tend to

prove the existence of a sale”

• Two-year presumption – Treas. Reg. § 1.707-3(c)

− Transfers made within two years are presumed to be a sale unless the

facts and circumstances “clearly establish” otherwise

» Triggers disclosure requirement under Treas. Reg. § 1.707-8

− Transfers outside of two years are presumed not to be part of a sale

unless the facts and circumstances clearly establish otherwise

13 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Disguised Sales – Key Safe Harbors (1.707-4)

• Certain distributions are exempt from disguised-

sale treatment even if made within the two-year

presumption period

• A distribution will generally not be treated as

disguised sale proceeds for a related contribution

to the extent the distribution:

− Represents a reasonable guaranteed payment or

preferred return;

− Consists of operating cash flow; or

− Represents reimbursement for preformation capital

expenditures (capex made on the contributed property

in the two years preceding the contribution)

14 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Disguised Sales – General Rules for Liabilities (1.707-5)

• Assumption of “qualified liabilities” generally does not give rise

to disguised sale proceeds.

• Assumption of “nonqualified liabilities” does give rise to

disguised sale proceeds in the amount of the liability that is

allocable to other partners under Section 752 (discussed below)

• If the partner receives even a dollar of disguised sale

consideration (either actual consideration, e.g., cash or

property, or through an assumption and shift of non-qualified

liabilities), a portion of any assumed and shifted qualified

liabilities are “tainted” and treated as disguised sale proceeds

15 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Disguised Sales – Debt-Financed Distributions (1.707-5(b))

• Treas. Reg. 1.707-5(b): One of the provisions that makes

(or made) leveraged partnership transactions possible.

− Under the rule, cash proceeds traceable to a liability incurred by the

partnership and distributed to a partner within 90 days of the

incurrence can be treated as disguised sale proceeds only to the

extent they exceed the partner’s share of the liability

• Prior to the 2016 Final Treasury Regulations:

− a partner’s share of a recourse liability of the partnership was

determined in accordance with the allocation of recourse liabilities

under Section 752 (discussed below), and

− a partner’s share of a nonrecourse liability of the partnership was

determined in accordance with the allocation of excess

nonrecourse deductions (i.e., the third tier of allocations of

nonrecourse deductions under Section 752).

16 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Overview of Partnership Provisions—Liabilities

Partnership

• Section 752: A partner whose

“allocable share” of partnership

liabilities increases is treated as

having contributed money to the

partnership, and a partner whose

“allocable share” of partnership

liabilities decreases is treated as

receiving a distribution from the

partnership.

• Treas. Reg. 1.752-1, 2: Where a

single partner or a related person

bears the economic risk of loss for a

partnership liability, the partner’s

allocable share of that liability (for

purposes of Section 752) is 100%.

• Sections 722 and 733: A partner’s

basis in its partnership interest is

increased by any money contributed

(including money deemed contributed

pursuant to Section 752), and its basis

is reduced by any money distributed

(including money deemed distributed

under Section 752).

Guarantor Partner Other

Partners

Bank

Existing Loan of

$1500, otherwise

non-recourse to all

partners.

Guarantor Partner

guarantees*

Partnership’s loan

from Bank

Deemed

Contribution of Cash

*Subject to various

anti-abuse rules that

will be discussed

Deemed Distribution

of Cash

17 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Allocation of Partnership Liabilities—Section 752

• As noted above, the allocation of liabilities can be relevant both to:

− determining whether there is a disguised sale in connection with a

contribution of property, and

− even if there is no disguised sale issue (e.g., no contribution or no

distribution that is treated as part of a sale), determining the

consequences of the deemed contributions and distributions that

result from liability shifts.

• The allocation of a partnership liability among the partners depends on

whether the liability is a “recourse” or “nonrecourse” liability under Section

752.

• A liability is a recourse liability to the extent that any partner (or a related

person) bears the “economic risk of loss” for such liability.

• A liability is a nonrecourse liability to the extent that NO partner (or related

person) bears the “economic risk of loss”.

18 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Allocation of Partnership Liabilities—Section 752 (cont’d)

• “Economic risk of loss” is a term of art:

− Generally, a partner bears the economic risk of loss for a

partnership liability if the partner or related person would

be obligated to make a payment to any person (or a

contribution to the partnership), and would not be entitled

to reimbursement from another partner or person related

to another partner, assuming a deemed liquidation of the

partnership in which the assets of the partnership become

worthless and all debt of the partnership was required to

be repaid in full

− Risk of loss can be created by, among other things, deficit

restoration obligations, guarantees, and pledges of the

partner’s assets, and also exists where the partner is the

lender

19 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Allocation of Recourse and Nonrecourse Liabilities

• Generally, recourse liabilities are allocated to the partner or partners that bear the

economic risk of loss for such liability, to the extent the partner or partners bear

the economic risk of loss.

• Nonrecourse liabilities, for general liability allocation purposes (but, as described

below, not for disguised sale purposes), are allocated according to a 3-tier

waterfall:

• First tier: an amount equal to a partner’s share of the “partnership minimum gain”

attributable to that liability is allocated to the partner (very generally, the amount by which

a nonrecourse liability exceeds the book basis of an encumbered property).

• Second tier: then, an amount equal to the partner’s share of the pre-contribution built in

gain that would be allocated to such partner under Section 704(c) if the property subject

to the nonrecourse liability were sold in full satisfaction of the liability and for no other

consideration.

• Third tier: any remaining “excess nonrecourse liabilities” are allocated in accordance with

the partner’s share of partnership profits.

− As an alternative to allocating in accordance with share of partnership profits, the Section

752 regulations permit alternative (and generally more flexible ) methods of allocation. For

example, allocations can be made in accordance with the partner’s share of a “significant

item.” As described below, however, the new temporary Section 707 regulations do not

permit the use of the alternative methods for disguised sale purposes.

20 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Guarantees Generally

• As the rules described above suggest, a partner will ordinarily be incentivized to cause itself

be allocated as much partnership debt as possible, which both:

− minimizes the likelihood of having (or minimizes the consequences of having) a disguised sale;

and

− minimizes the likelihood of otherwise receiving taxable deemed or actual distributions.

• Traditionally, the most common way for a partner to maximize its debt allocation was to

guarantee the debt

• The rules generally assume that the partner will make good on its guarantee

• Pre-Existing Anti-Abuse Rules

− Treas. Reg. § 1.752-2(j)(1)): “An obligation of a partner or related person to make a

payment may be disregarded or treated as an obligation of another person for

purposes of this section if facts and circumstances indicate that a principal purpose of

the arrangement is to eliminate the partner’s economic risk of loss with respect to that

obligation or create the appearance of the partner or related person bearing the

economic risk of loss when, in fact, the substance of the arrangement is otherwise.

− Treasury Reg. § 1.752-2(j)(3): “An obligation of a partner to make a payment is not

recognized if the facts and circumstances evidence a plan to circumvent or avoid the

obligation.”

− The IRS has sought to apply this anti-abuse rule with some success.

» See, e.g., Canal Corp. v. Comm’r.

21 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Generic Leveraged Partnership Structure

Partnership

Bank

Owner Investor

Assets w/ basis of

$0 and FMV $2000

Asset w/ basis of

$1500 and FMV of

$2000

Loan of $1800

$1800 of loan

proceeds

Owner

Guarantees

Loan 1 1

2

2

3

1. Owner contributes

appreciated property and

Investor contributes other

property to Partnership in

exchange for interests in

Partnership.

2. Partnership borrows cash

from unrelated Bank.

− Owner guarantees

Partnership’s borrowing.

3. Partnership distributes

$1800 of loan proceeds to

Owner.

Result under prior law: Owner

does not recognize any gain.

22 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Brief Introduction to the “Bottom Dollar Guarantee”

• A “Bottom Dollar Guarantee” is a guarantee of debt only to the extent that a

certain minimum amount is not received from the primary obligor.

• Consider the following example:

• Guarantor executes a Bottom Dollar Guarantee of $200 of an Obligor’s $2000 loan.

• If the Obligor repays $200 or more of the $2000 it owes, the Guarantor has no liability.

• If the Obligor repays $150 of the $2000 it owes, the Guarantor has an obligation to pay

$50.

• If the Obligor repays $0 of the $2000 it owes, the Guarantor has an obligation to pay

$200.

• Bottom Dollar Guarantees were commonly used to make a partner bear the economic

risk of loss for a partnership liability under the Section 752 rules, while limiting the

partner’s actual economic risk with respect to the guarantee.

• Contrast the Bottom Dollar Guarantee with:

• First dollar guarantees: lender may go after guarantor if any amount of the liability is

unrecovered from the obligor

• Vertical slice guarantees: a percentage of each unrecovered dollar is guaranteed

23 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

(Over) Simplified Bottom-Dollar Guarantee Structure

UP-REIT

Partnership

REIT Real Estate with $0

basis, FMV of

$2000 subject to

nonrecourse liability

of $1,800

PRIOR LAW

Historic Owners have held real

estate for several years. The real

estate has a zero basis and is

subject to an $1,800 nonrecourse

qualified liability.

1. Historic Owners contribute

property to UP-REIT

Partnership, a large

partnership with a diversified

real-estate portfolio in

exchange for a small interest

in UP-REIT Partnership and

UP-REIT Partnership pays off

the liability.

2. To prevent gain on the liability

shift, under prior law, Historic

Owners enter into a “Bottom-

Dollar Guarantee” of UP-REIT

Partnership’s other liabilities.

Historic Owners Guarantee

Bank Loan to UP-REIT

Partnership, to the extent

Bank collects less than

$1,800 on the loan.

Historic

Owners

1

Bank

Outstanding unsecured

loan of $50,000.

2

*Bottom Dollar Guarantees or the opportunity to

enter into such guarantees in the future may also

be desirable when property is contributed but

remains subject to a pre-contribution liability, if

there is a later liability shift because of changes in

the contributing partner’s 704(c) amount

24 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Brief Overview of the 2014 Proposed Regulations

• “Payment Obligation Standards” of Proposed Treasury Reg. § 1.752-2(b)(3): In order for a liability

to be treated as a recourse liability of a partner, all of the following must be true:

− The partner’s obligation to repay must require partner to maintain “commercially reasonable” net worth

throughout period of payment obligation.

− The obligation must subject the partner to “commercially reasonable” restrictions on transfers for low or

no consideration.

− The obligor partner must provide “commercially reasonable” documentation regarding financial

condition on a periodic basis.

− The term of payment obligation must not end prior to the term of the partnership liability.

− The partner’s payment obligation must not require any other primary obligor or other obligor with

respect to partnership liability to hold money or other liquid assets in an amount that exceeds the

reasonable needs of such obligor. AND

− The partner must receive arm’s length consideration for entering into the payment obligation.

• Importantly, the Payment Obligation Standards would have applied for all purposes, not just for

purposes of exceptions to disguised sale treatment.

• Each Payment Obligation Standard was a necessary prerequisite for qualification as a recourse

liability. In other words, if any one of the Payment Obligation Standards was not met to any extent,

then a liability would be treated as fully nonrecourse.

• In contrast, although the Tax Court in Canal Corp. referenced many facts similar to the Payment

Obligation Standards, it was the sum total of these facts that the Tax Court found dispositive under

the -2(j) anti-abuse regulation.

25 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Brief Overview of the 2014 Proposed Regulations (cont’d)

• In addition to the Payment Obligation Standards, the Proposed

Regulations specifically targeted “Bottom Dollar Guarantees.” Prop.

Reg. § 1.752-2(b)(3)(ii)(F) would have required that a partner must be

liable up to the full amount of the partner’s payment obligation, if and

to the extent that any partnership liability is not satisfied in order for

the obligation to be respected.

• In addition, a “Net Value Requirement” would have recognized

payment obligations of a partner or related person “only to the extent

of the net value of the partner or related person as of the allocation

date”. Former Prop. Reg. § 1.752-2(k).

• Certain changes were made to permissible methods of allocating

excess nonrecourse liabilities, including the removal of allocation in

accordance with a significant item of income.

• These portions of the 2014 Proposed Regulations received a

relatively negative reception from many tax practitioners.

26 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Brief Overview of New Regulations

• On October 4, 2016, the Treasury released a sweeping package of proposed,

temporary, and final regulations that drastically change the rules described above.

• Key Provisions of the Regulations:

− Final Regulations:

» Section 707:

> Capex amendments (20% imitation applied property-by-property; contributions of partnership interests;

overlap with qualified liabilities)

> De minimis exception to taint of qualified liabilities

> Step-into-shoes rules for capex and qualified liabilities

> New category of qualified liability

> Alternative methods of allocating nonrecourse liabilities not available for disguised sale purposes

− Temporary Regulations:

» Section 707:

> All liabilities allocated as tier 3 nonrecourse

» Section 752:

> Bottom Dollar Guarantees disregarded

− Proposed Regulations:

» Section 752: New anti-abuse rule for disregarded guarantees and other payment obligations

28 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Overview of New Section 752

Regulations

29 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

New Temporary 752 Regs—Bottom Dollar Guarantees

• For all purposes of Section 752 (not just for disguised sale purposes), “bottom

dollar payment obligations” (“BDPOs”) will not taken into account for

determining whether a liability is recourse to a partner, subject to certain

exceptions.

− Reasoning: IRS generally views such arrangements as lacking significant non-tax

commercial business purpose

• BDPO defined: “[A]ny payment obligation other than one in which the partner or

related person is or would be liable up to the full amount of such partner’s or

related person’s payment obligation if, and to the extent that, any amount of the

partnership liability is not otherwise satisfied”.

− Includes tiered partnerships, intermediaries, senior and subordinate liabilities and

other obligations involving multiple liabilities if the liabilities were incurred as part of a

common plan to avoid having at least one of the liabilities be treated as a bottom-

dollar payment obligation

• Disclosure is required of all BDPOs that are incurred or modified (including

obligations that are recognized under the 90% rule on the following slide)

30 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

New Temporary 752 Regs—Exceptions

• Exceptions: An obligation is not treated as a BDPO merely because:

− Capped Obligations: a maximum amount is placed on the obligation

− Vertical Slice Guarantees: the obligation is stated as a fixed percentage of every dollar of

the partnership liability to which such obligation relates

− Certain Rights of Contribution: there is a right of proportionate contribution running

between co-obligors with respect to a payment obligation for which each of them is jointly

and severally liable

• 90% risk retention exception: Additionally, a BDPO is nevertheless recognized if:

− The payment obligation would otherwise be recognized, but for the effect of an indemnity,

reimbursement agreement, or similar arrangement, AND

− Taking into account the indemnity or reimbursement agreement, the partner or related

person remains liable for at least 90% of the partner’s or a related person’s initial payment

obligation (i.e., the amount of the payment obligation determined without regard to the

indemnity or reimbursement obligation).

• Anti-Abuse Rule:

− Finally, an anti-abuse rule allows the IRS to respect certain payment obligations that

otherwise would be disregarded under the new rules, if the obligation was structured

purposefully to allow the related liability to be treated as nonrecourse (e.g., where a

principal purpose to have other partners include the debt in their basis)

31 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

New Temporary 752 Regs—Effective Dates and Expiration

• Immediate effectiveness for new obligations:

− The new bottom dollar guarantee rules became effective immediately for all liabilities

incurred/assumed by a partnership, and payment obligations undertaken by partner,

after Oct. 4, 2016

• Grandfathering of preexisting liabilities/obligations and those under contract:

− The new rules do not apply to liabilities incurred/assumed and payment obligations

undertaken prior to Oct. 5, 2016, nor do they apply to liabilities/obligations incurred

pursuant to a written binding contract in effect prior to Oct. 5, 2016

» Note, however, that post-Oct. 4 modifications or refinancings of existing

debts/payment obligations are generally not grandfathered

• Seven-year transitional relief: The regulations contain a seven-year transition rule for

partners with negative tax capital accounts:

− To the extent a partner’s negative tax capital account (i.e., the excess of its allocable

share of partnership liabilities over its adjusted basis in its partnership interest) as of

Oct. 5, 2016, a partner may continue to apply prior law to debts and payment

obligations incurred even after Oct. 4, 2016, but only for seven years thereafter

− The amount for which this transitional rule is available is reduced as a partner’s

negative tax capital is reduced following Oct. 4, 2016

• Expiration if not finalized sooner: Oct. 4, 2019

32 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

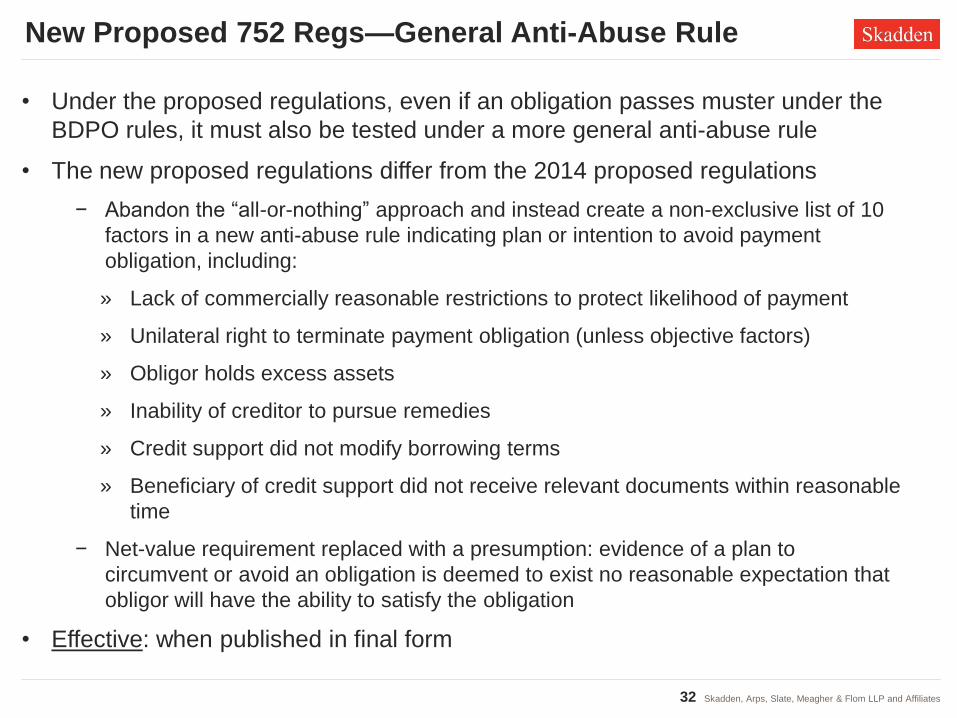

New Proposed 752 Regs—General Anti-Abuse Rule

• Under the proposed regulations, even if an obligation passes muster under the

BDPO rules, it must also be tested under a more general anti-abuse rule

• The new proposed regulations differ from the 2014 proposed regulations

− Abandon the “all-or-nothing” approach and instead create a non-exclusive list of 10

factors in a new anti-abuse rule indicating plan or intention to avoid payment

obligation, including:

» Lack of commercially reasonable restrictions to protect likelihood of payment

» Unilateral right to terminate payment obligation (unless objective factors)

» Obligor holds excess assets

» Inability of creditor to pursue remedies

» Credit support did not modify borrowing terms

» Beneficiary of credit support did not receive relevant documents within reasonable

time

− Net-value requirement replaced with a presumption: evidence of a plan to

circumvent or avoid an obligation is deemed to exist no reasonable expectation that

obligor will have the ability to satisfy the obligation

• Effective: when published in final form

33 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Overview of New Section 707

Regulations

34 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

New Temporary 707 Regs—All Liabilities

Nonrecourse

• The most significant change in the new Section 707 regulations

(contained in the temporary portion of the reg package) is that for

disguised sale purposes, all liabilities are treated as nonrecourse

• Guarantees, even guarantees fully recognized under the new final and

proposed 752 regulations, no longer can prevent a shift in liabilities for

disguised sale purposes

• This means that an assumption of any nonqualified liability will

always cause the related contribution to be treated in part as a

taxable disguised sale

• Similarly, a debt-financed distribution in excess of the partner’s pro

rata share of the liability (based on share of profits) will trigger a

partial sale if not otherwise exempt under the disguised sale rules

35 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

New Temporary 707 Regs—Allocation of Liabilities

• All liabilities are generally treated as Section 752 “excess

nonrecourse liabilities”—i.e., allocated under “tier 3”

− Under new final regulations, Treas. Reg. 1.752-3 has

been amended so that the alternative methods for

allocating excess nonrecourse liabilities in tier 3 (e.g.,

“significant item” method) do not apply for disguised

sale purposes

• A contributing partner’s share of liabilities is reduced,

however, by any amount with respect to which any other

partner has the risk of loss

• In other words, a contributing partner’s guarantee cannot

help, but guarantees by other partners can hurt

36 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Result of attempted leveraged partnership structure (same

example as above) under new Temporary 707 Regulations

Partnership

Bank

Owner Investor

Assets w/ basis of

$0 and FMV $2000

Asset w/ basis of

$1500 and FMV of

$2000

Loan of $1800

$1800 of loan

proceeds

1. Notwithstanding Owner’s

guarantee of the loan, for

purposes of applying the

disguised sale rules, the

$1800 liability is treated as

nonrecourse.

2. The nonrecourse liability, for

disguised sale purposes is

allocated according to “tier 3”

of the nonrecourse liability

allocation under Section 752.

3. Assuming Owner owns 1/11 of

the Partnership, Owner is

allocated $163 of the Bank

Loan.

4. Owner is treated as receiving

a distribution of $1637 ($1800

- $163) that is part of a

disguised sale. Owner

recognizes gain as if it sold

81.85% (1637/2000) of the

property.

Owner

Guarantees

Loan

37 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

New Temporary 707 Regs—Effective Dates and

Expiration

• The new temporary regulations have a 90-day delayed effective date

− The regulations are effective for “any transaction with respect to which all transfers

occur on or after January 3, 2017”

• Because “all transfers” are required to occur on or after January 3, 2017 in order to be

subject to the new regulations, certain transactions are grandfathered even where a part

of the transaction takes place after the January 3, 2017 effective date

− E.g., contribution made before Jan. 3, but debt-financed distribution and related

guarantee not made until after Jan. 3.

• But because the 752 temporary regulations are immediately effective, any guarantee

would need to pass muster under those regulations even if the transaction can be

grandfathered for 707 purposes

• Expiration if not finalized sooner: Oct. 4, 2019

• Possible Repeal: According to a report issued by the Secretary of the Treasury on October

2, 2017, Treasury is “considering whether the proposed and temporary [707] regulations

should be revoked and the prior regulations reinstated”

• By contract, although Treasury will continue to study the temporary 752 regulations on

BDPOs, it does not expect to propose substantial changes to those regulations

38 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Final 707 Regulations—Ancillary Disguised Sale

Issues

• In addition to the significant changes in the temporary

regulations, Treasury issued final Section 707 regulations

that address a number of ancillary issues, many (but not all)

of which were resolved in a taxpayer-favorable manner:

− Capex amendments (20% imitation applied property-by-

property; contributions of partnership interests; overlap

with qualified liabilities)

− De minimis exception to taint of qualified liabilities

− Step-into-shoes rules for capex and qualified liabilities

− New category of qualified liability

39 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Final 707 Regulations—Capex Rules (Background)

• An important exception to the disguised sale rules is the

“preformation capital expenditure” exception

• This exception permits a contributing partner to receive

distributions from the partnership as reimbursement for

capital expenditures made by the partner within two years of

the contribution

− In general, the exception is available for expenditures only

up to 20% of the value of the contributed property

− However, the 20% limitation does not apply if the

property’s FMV is less than 120% of its basis

• The final regulations address a number of issues with the

“capex” exception

40 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Final 707 Regulations—Capex Rules (20%

Limitation)

• 20% Limitation Tested Property-by-Property

− Under the final regulations, when multiple properties are

contributed in a single transaction, the 20% capex

limitation is generally tested on a property-by-property

basis, not in the aggregate

− Depending on the facts, this rule may be taxpayer-

favorable or taxpayer-unfavorable (see examples

below)

− No guidance as to what constitutes a “property”

41 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Final 707 Regulations—Capex Rules (20% Limitation

Examples)

• EXAMPLE 1

• Facts: X owns two assets. Asset 1 (FMV $200, basis $170) and Asset 2

(FMV $200, basis $150). X bought each asset for $200 each within the last

two years.

• Property-by-Property Result:

− Asset 1 is not substantially appreciated (120% of $170 = $204).

» Result: Entire $200 may be reimbursed.

− Asset 2 is substantially appreciated (120% of $150 = $180).

» Result: Only 20% of $200 or $40 may be reimbursed.

− Total amount qualifying under Treas. Reg. § 1.707-4(d): $240

• Aggregation Result:

− Total FMV would be $400 and total basis would be $320. The properties, in the

aggregate, are substantially appreciated (120% of $320 = $384).

− Result: Only 20% of $400 or $80 would qualify under Treas. Reg. § 1.707-4(d).

42 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Final 707 Regulations—Capex Rules (20% Limitation

Examples)

• EXAMPLE 2

• Facts: Same facts as Example 1 except basis of Asset 2 is $165, not $150.

• Property-by-Property Results:

− Asset 1 is not substantially appreciated (120% of $170 = $204).

» Result: Entire $200 may be reimbursed.

− Asset 2 is substantially appreciated (120% of $165 = $198).

» Result: Only 20% of $200 or $40 may be reimbursed.

− Total amount qualifying under Treas. Reg. § 1.707-4(d): $240

• Aggregation Results:

− Total FMV would be $400 and total basis would be $335. The properties, in the

aggregate, are not substantially appreciated (120% of $335 = $402).

− Result: Entire $400 would qualify under Treas. Reg. § 1.707-4(d).

43 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

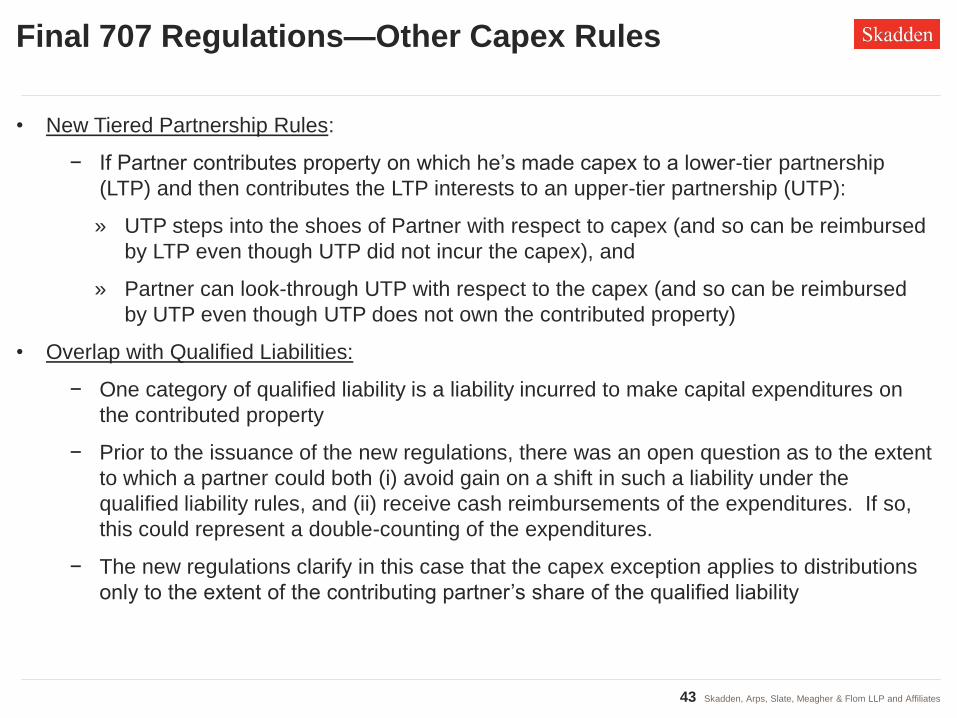

Final 707 Regulations—Other Capex Rules

• New Tiered Partnership Rules:

− If Partner contributes property on which he’s made capex to a lower-tier partnership

(LTP) and then contributes the LTP interests to an upper-tier partnership (UTP):

» UTP steps into the shoes of Partner with respect to capex (and so can be reimbursed

by LTP even though UTP did not incur the capex), and

» Partner can look-through UTP with respect to the capex (and so can be reimbursed

by UTP even though UTP does not own the contributed property)

• Overlap with Qualified Liabilities:

− One category of qualified liability is a liability incurred to make capital expenditures on

the contributed property

− Prior to the issuance of the new regulations, there was an open question as to the extent

to which a partner could both (i) avoid gain on a shift in such a liability under the

qualified liability rules, and (ii) receive cash reimbursements of the expenditures. If so,

this could represent a double-counting of the expenditures.

− The new regulations clarify in this case that the capex exception applies to distributions

only to the extent of the contributing partner’s share of the qualified liability

44 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Final 707 Regulations—De Minimis Exception to

Qualified Liability Taint

• As noted above, if a contributing partner receives even a dollar

of disguised sale consideration (including through a shift in

nonqualified liabilities), a portion of any assumed qualified

liabilities are tainted

• The new regulations contain a de minimis exception to this

rule:

− Qualified liabilities will not be tainted if the total amount of

nonqualified liabilities assumed by the partnership is the

lesser of 10% of all qualified liabilities assumed by the

partnership or $1 million.

• Because of the $1 million threshold, many transactions will

not benefit from this rule

45 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Final 707 Regulations—Step-into-Shoes Rule

• Prior to the new regulations, it was generally unclear when and to

what extent a transferee of property would step into the transferor’s

shoes with respect to preformation capex made by the transferor

• Similarly unclear was whether a qualified liability retained its status

as qualified when assumed by a transferee

• Previous guidance on both points was generally limited to 381

transactions (e.g., 368 reorganizations, 332 liquidations) and certain

other limited situations addressed in the prior regulations

− For example, unclear what happened in other nonrecognition

transactions, such as a 721 or 351 contribution or a 731

partnership distribution

• The new regulations clarify that a transferee steps into the

transferor’s shoes, both with respect to preform capex and qualified

liabilities, to the extent the property/liability was acquired/assumed in

a nonrecognition transaction under 721, 731, 351, and 381.

46 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Final 707 Regulations—New Qualified Liability

• The regulations create a new class of qualified liabilities:

− “A liability that was not incurred in anticipation of the transfer of the

property to a partnership, but that was incurred in connection with a

trade or business in which property transferred to the partnership was

used or held but only if all the assets related to that trade or business are

transferred other than assets that are not material to a continuation of the

trade or business”

• Key requirements

− “not in anticipation of the transfer of the property to a partnership”

− “in connection with”

48 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Practical Implications and Planning

Techniques

49 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Immediate To-Dos for Existing Partnerships

• Partners and partnerships that have debt in their structures should undertake an evaluation of

the effects of the new Section 752 rules on those structures

− This is especially true for partnerships, including many UPREITs, that have debt-

maintenance guarantee-opportunity obligations with their partners. For these

partnerships, the stakes may be covenant breaches.

• Given that currently outstanding debt and payment obligations are grandfathered, the main

pressure points for existing partnerships will be modifications and refinancings; these are not

grandfathered and could trigger immediate application of the new rules (or application at the

end of the seven-year transition period; see next slide).

− Example: Partner X owns 10% of Partnership and has a basis in his partnership interest

of $40. Partnership has one nonrecourse liability of $1000, $200 of which is allocated to

Partner X because Partner X has undertaken a BDPO. Assume Partnership refinances

the debt with $1000 of new debt (to which same BDPO applies), and assume that the

seven-year transition rule discussed above does not apply (e.g., because the refinancing

took place more than seven years after the promulgation of the regulations).

− Result: Partner X’s BDPO is disregarded, meaning that Partner X’s share of the new

liability is only $100 (10% of $100). This causes Partner X to receive a $100 deemed

distribution, triggering $60 of gain.

50 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Immediate To-Dos for Existing Partnerships (cont’d)

• Any partners that expect that they may want or need to rely on the seven-year

transitional relief will need to determine negative tax capital accounts as of Oct. 4,

2016, and will need to diligently track changes in those accounts and partnership

allocations that can reduce the maximum amount of guarantee that is available for

the benefit of the transitional rule

• Partners and partnerships should also begin planning for the expiration of the

seven-year period—what will the effect be for your partners at the end of the period

when the new rules immediately take effect, and how can that be mitigated?

− Example: Same facts as above, except assume the seven-year transition rule

initially applies to the refinanced debt and BDPO. If the debt remains

outstanding at the end of the seven-year period, the new rules will take effect

at that point, triggering the $50 of gain then, unless the BDPO is restructured

to comply with the new regulations.

− Restructuring of the payment obligation to satisfy the new rules, or maintaining

more partnership-level debt in order to provide sufficient debt allocations for

partners whose payment obligations do not satisfy the new rules, may be

required

51 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Strategies for Dealing with the New 707 Rules—

Post-Effective Planning

• For non-grandfathered transactions, the new regulations largely

shut down the opportunity for tax-deferral through (i)

contributions of property subject to nonqualified liabilities, and

(ii) traditional debt-financed distributions occurring in

connection with a contribution of property.

• There are, however, some alternatives that could be considered

52 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Leveraged Partnership Alternatives—Delayed Debt-

Financed Distribution

• Steps:

− Step 1: Partner contributes Property (free of nonqualified liabilities) to

Partnership

− Step 2: More than two years later, Partnership makes a debt-financed

distribution. Partner guarantees enough of the debt to give it sufficient basis to

absorb the distribution without recognizing gain.

• Considerations:

− Guarantee cannot be a BDPO or other guarantee that is disregarded under the

new Section 752 regulations.

− Even though the distribution is presumed not to be part of a sale (because it

occurs more than two years after the contribution), this presumption could be

rebutted if there is not sufficient entrepreneurial risk with respect to the

occurrence of the subsequent distribution.

» This means that the parties would have to take material business risk of the

later distribution not occurring or occurring on terms not initially anticipated.

53 Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates

Leveraged Partnership Alternatives—Debt

Structured as Qualified Liability

• Steps:

− Step 1: Partner borrows against property. Borrowing is secured by

Property.

− Step 2: More than two years later, Partner contributes Property to

Partnership, subject to the debt. Because the debt was incurred

more than two years earlier and secured the contributed Property,

the debt is a qualified liability.

• Considerations:

− Again, the contribution should not be so certain that there is not

significant entrepreneurial risk due to change in circumstances.