peter marshall - monash university - governance of controlled entities

TRANSCRIPT

Governance of Controlled Entities

Mr. Peter Marshall

Chief Operating Officer & Senior Vice-President

2

What is a Controlled Entity?

Definition of controlled entities

A controlled entity is one that satisfies the test of control in section 50AA of the Corporations Act 2001 and includes:

a. an entity which the University wholly owns (“wholly owned subsidiary”); or

b. an entity in which the University holds an interest of any kind (including a shareholding interest or membership interest) and the University has control of the entity.

3

Monash Controlled Entities

Monash University has 3 controlled entities, operating for a variety of reasons:

1. Monash College

2. Monash Foundation

3. Monash Accommodation Services

Significantly fewer than we had 15 years ago

4

Rationale for participation in Controlled Entities

The reasons for forming or participating in a Controlled Entity may include:

1. An area that is not core University business e.g. student accommodation

2. There are commercial reasons for operating under a controlled entity – i.e. it can operate under a “clean set of books”, e.g. Monash IVF, Monash College

3. Benefit in operating under different employment or regulatory environment – i.e. not under the University EBA, subject to different regulations etc.

(can be a combination of the above)

5

Ensuring the entity remains a CONTROLled entity

In theory exercised through governance (Council and VC)

Separation and clear roles for:– Shareholder

– Director

– University line accountability

But conflicts are inevitable

Clear delegations of authority – particularly financial

“Controlled” operating independence

6

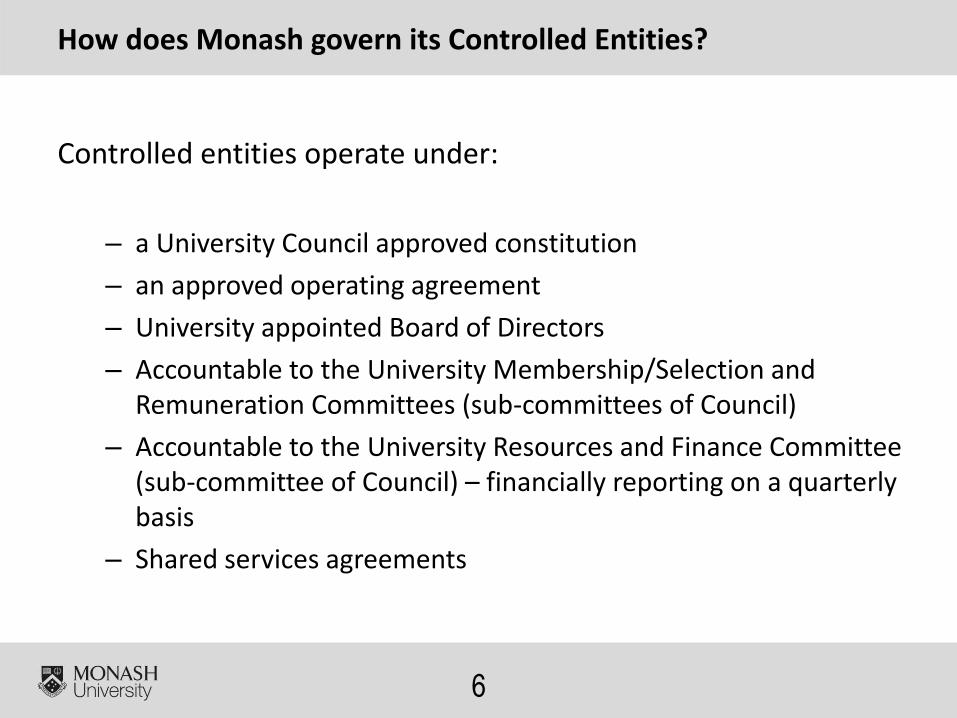

How does Monash govern its Controlled Entities?

Controlled entities operate under:

– a University Council approved constitution

– an approved operating agreement

– University appointed Board of Directors

– Accountable to the University Membership/Selection and Remuneration Committees (sub-committees of Council)

– Accountable to the University Resources and Finance Committee (sub-committee of Council) – financially reporting on a quarterly basis

– Shared services agreements

7

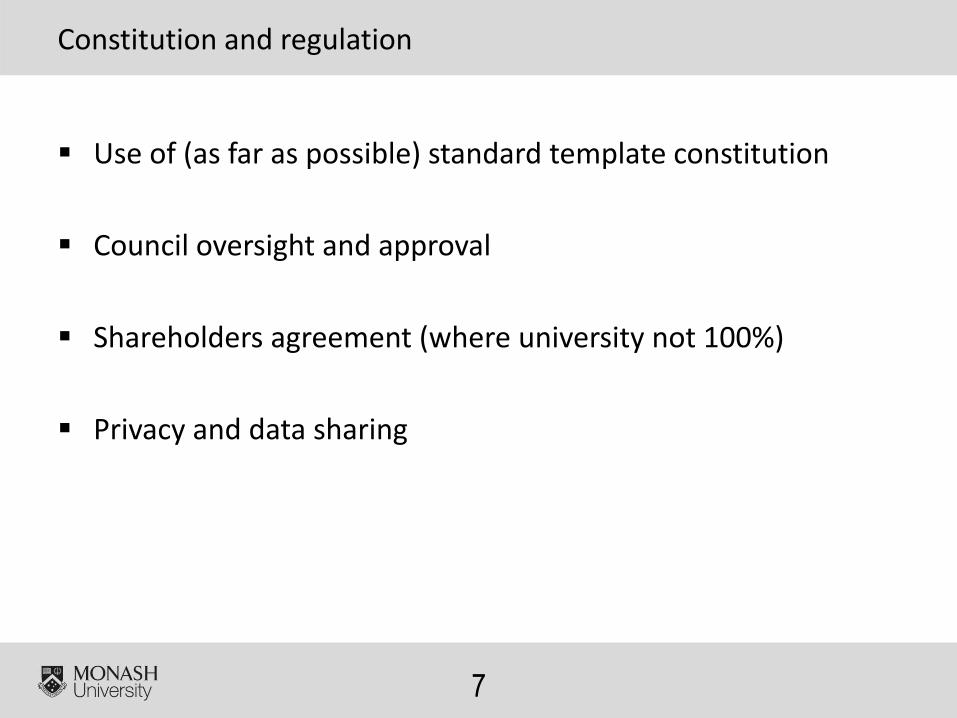

Constitution and regulation

Use of (as far as possible) standard template constitution

Council oversight and approval

Shareholders agreement (where university not 100%)

Privacy and data sharing

8

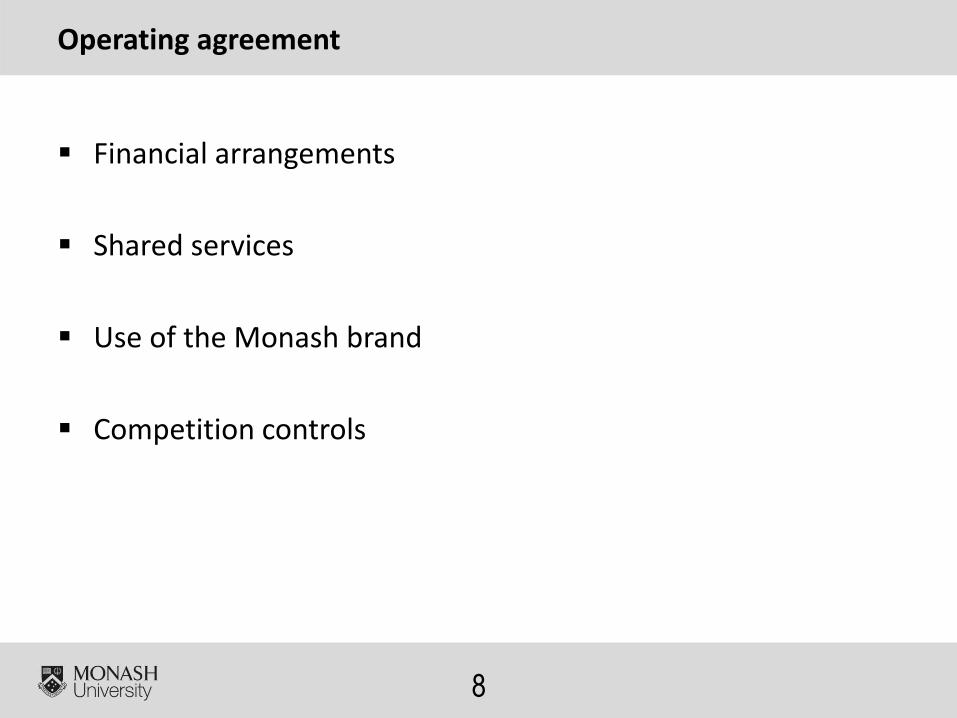

Operating agreement

Financial arrangements

Shared services

Use of the Monash brand

Competition controls

9

Board of Directors

Appointment arrangements– VC authority/approval

– Remuneration controlled at group level

– Remuneration only where required

– The Chair

Internal or external appointees

Term appointments

Clarity where appointments end/terminated

10

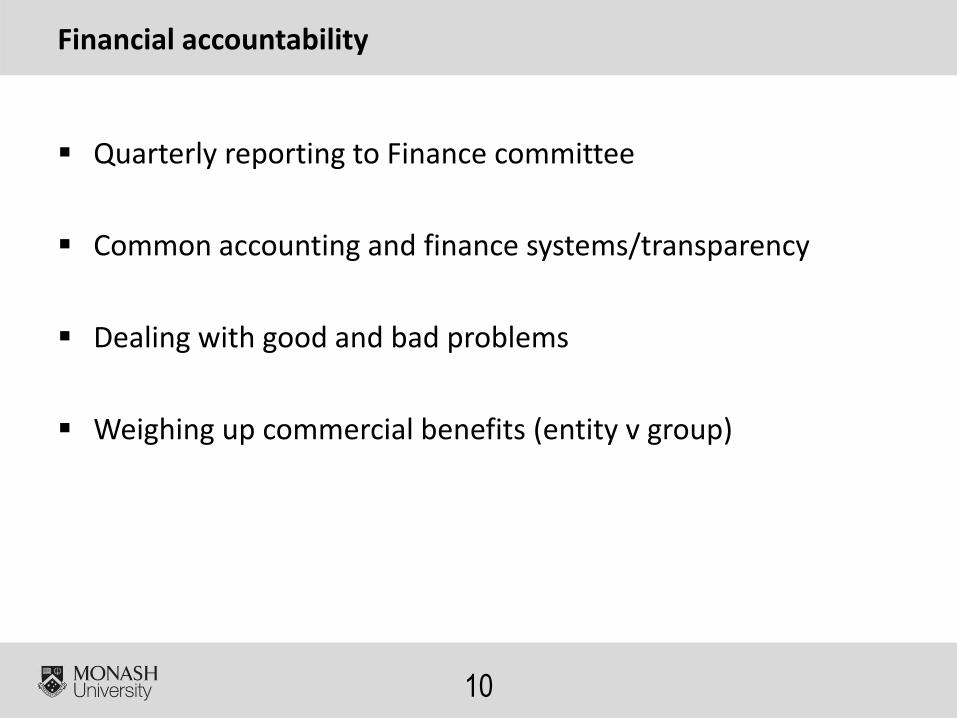

Financial accountability

Quarterly reporting to Finance committee

Common accounting and finance systems/transparency

Dealing with good and bad problems

Weighing up commercial benefits (entity v group)

11

Tension points

Insurance – who insures entity or group

Property – should the entity hold property or like assets, can the entity commit expose the group to liabilities or risk

Cash

Systems access and data

Internal Audit and Risk

12

Summary

Control needs to be operationalised as well as articulated

in regulation/policy/procedure

Alignment with the group vs alignment with AICD

guidelines

Independence vs Operating flexibility

Getting the people issues right