public disclosure authorized afil .p ll }0to be returned...

TRANSCRIPT

aFIL CIRCuLATIN~G COPY.P LL }0TO BE RETURNED TO REPORTS DESK

DOCUMENT OF INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

Not For Public Use

CIRCULATING COPY

TO BE RETURNED TO REPORTS DESK Report No. P-1672a-YU

REPORT AND RECOMMENDATION

OF THE

PRESIDENT

TO THE

EXECUTIVE DIRECTORS

ON A

PROPOSED LOAN

TO

JUGOSLAVENSKI NAFTOVOD PODUZECE

ZA TRANSPORT NAFTE U OSNIVANJU, RIJEKA

(YUGOSLAV OIL PIPELINE ENTERPRISE)

WITH THE GUARANTEE OF

THE SOCIALIST FEDERAL REPUBLIC OF YUGOSLAVIA

FOR AN

OIL PIPELINE PROJECT

October 22, 1975

This report was prepared for official use only by the Bank Group. It may not be published, quotedor cited without Bank Group authorization. The Bank Group does not accept responsibility for theaccuracy or completeness of the report.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

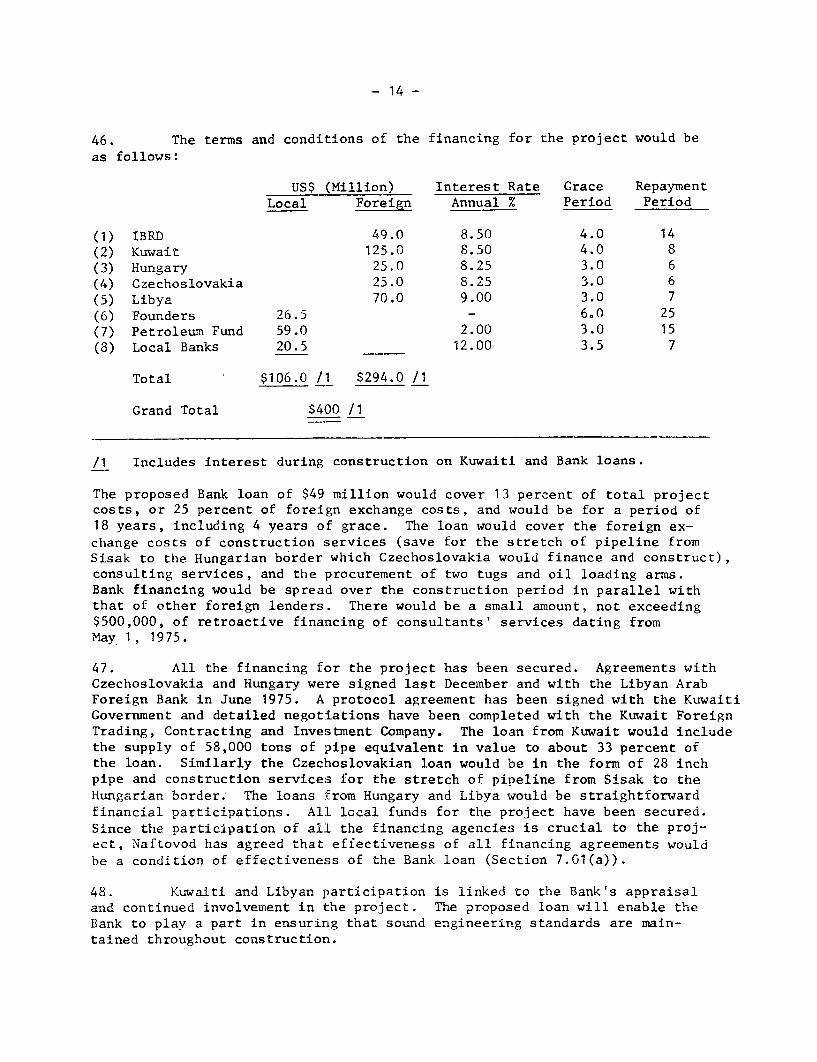

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRE1CY EQUIVALENTS *

Currency Unit Yucgoslav D:inar (Din.)

US$1 Din. 17 .CO

Din. 1 US$o0.o588

Din. 1,000 US$58 .82,.

Din'. 1,000-,000 US$58,823.53

* The Yugoslav Dinar has been floating since Julyr 13, 1973.The carrenCr eguivaleIits given abo ve are as of Mlay 30, 1975.

Fiscal Year January I - December 31

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

REPORT AND RECOMMENDATION OF THE PRESIDENTTO THE EXECUTIVE DIRECTORS ON A

PROPOSED LOAN TO JUGOSLAVENSKINAFTOVOD PODUZECE ZA TRANSPORT NAFTE U OSNIVANJU, RIJEKA

WITH THE GUARANTEE OFTHE SOCIALIST FEDERAL REPUBLIC OF YUGOSLAVIA

1. I submit the following report and recommendation on a proposed loanequivalent to US$49.0 million to Jugoslavenski Naftovod Poduzece Za TransportNafte U Osnivanju, Rijeka (Naftovod), with the guarantee of the SocialistFederal Republic of Yugoslavia, to help finance an oil pipeline project. Theloan would have a term of eighteen years including four years of grace. Inter-est would be at 8-1/2 percent per annum. Co-financing for the project is beingprovided by agencies in Czechoslovakia, Hungary, Kuwait and Libya.

PART I - THE ECONOMY

2. A basic economic mission visited Yugoslavia in November 1972; itsreport entitled "The Economic Development of Yugoslavia" (R74-1) was distri-buted to the Executive Directors on January 2, 1974. An updating EconomicMemorandum (662a-YU) was distributed to the Executive Directors on June 23,1975. Basic data on the economy are given in Annex I.

Economic Trends and Development Issues

3. The Yugoslav economy has experienced rapid growth during the lasttwo decades, with total GDP at constant prices having increased by an averagerate of 6.3 percent, and per capita GDP at 5.2 percent annually. In 1973,per capita GNP came to about US$900 (World Bank Atlas methodology). Thisimpressive record of growth was accompanied by some fundamental structuralchanges in the economy which has moved towards a modern industry/serviceoriented urban society. The share of agriculture in GDP declined from 38 to20 percent while the share of industry and mining increased from 16 to 37percent.

4. The population growth rate averaged 1 percent per year during thelast two decades, but with considerable regional variations ranging from 1.6percent in the less developed republics and provinces to 0.7 percent in thedeveloped ones. The structural changes in the economy permitted a sizeabletransfer of labor force from agriculture to industry and services. However,by 1974 nearly 42 percent of the active population was still engaged inagriculture and forestry, mostly on small private farms; industry (includingmining, construction and handicraft) accounted for 28 percent, services for20 percent, and the remainder was working abroad or unemployed.

5. The socio-political framework evolved through several constitutionalamendments which were consolidated in the new constitution of 1974. Itstrengthens three important features of the socio-political system ofYugoslavia. First, self-management, whereby the use and control of the

socially owned means of production is entrusted to the workers' collectives,is the fundamental right and obligation of every "basic organization ofassociated labor" (the smallest technologically identifiable unit of operation)in every sector and activity. Second, the responsibility for most importantsocial and policy decisions has been shifted from the Federation down to therepublics and provinces, and on to the communes. And third, the managementand financial responsibility for social activities (like health, education,welfare, etc.) is transferred from the realm of the state to "communities ofinterest" (decision-making bodies which comprise delegates of both suppliersand users of the specific se-rvices). Responsibility for certain economicactivities affecting large segments of the society (like communal services,power production, highways and water management) can be - and progressivelyis - similarly organized through communities of interest.

6. The social sector, which includes government, most enterprises andinstitutions such as libraries, hospitals, theatres and schools, has theleading role in economic and social devleopment; it accounts for 85 percentof GDP and employs over half of the total labor force. The private sectoris predominantly comprised of peasant farms (with a 10 hectare limit to landholdings) and small enterprises (with a 5 person limit on the number of non-family workers), mainly in handicrafts, construction, trade, transport andtourism. In the past the private sector has been relatively neglected bygovernment policy. However, lately more attention is being devoted to pri-vate farmers with a view to accelerating the growth of agricultural productionand reducing the rural/urban income disparity.

7. Regional income disparity - with a gradient of GDP per capita fallinggenerally from North to South - has emerged as one of the most important de-velopment issues of the country. Four distinct regions can be distinguishedby stage of development. The Republic of Slovenia is the high income regionwith almost double the national average. The Republics of Serbia, Croatiaand the Autonomous Province of Vojvodina - make up the middle income regions,ranging from 100 to 125 percent of the national average. The Republics ofBosnia-Herzegovina, Montenegro and Macedonia - with per capita GDP between 67to 75 percent constitute the upper group among the officially designated "lessdeveloped regions". The Autonomous Province of Kosovo, with an average in-come of only 33 percent of the national average, is at the bottom of thespread. These inter-regional disparities can be traced back further to intra-regional disparities. Within Republics and Provinces the spread betweencommunes can extend over the range of 10 to 1, and it is the prevalence ofstagnating poor rural communes within the less developed regions which largelydetermnines the disparity between the regions. The rate of economic growthof the less developed regions as a whole was only slightly below the averagefor Yugoslavia, but due to the faster population growth (1.6 percent peryear versus 0.7 percent in the more developed regions) the income disparityhad tended to widen significantly during the last two aecades. In order toreverse this trend and to accelerate economic growth anc social developmentin the less developed regions, mechanisms have been &nsituted for sizeabletransfers of financial resources. in i973. credits on highly fiavor al:e terms(containing a grant element of around 50 percuac) were maade available through

- 3 -

the "Federal Fund" to the less developed regions in the amount of almostUS$300 million, equivalent to more than 20 percent of their total investmentin the social sector. An additional US$120 million for social services weretransferred as budgetary grants.

8. Open unemployment has not been a serious problem and is estimatedto be only around 3-4 percent of the resident labor force in 1974. However,this low rate conceals three important aspects of the employment problem.First, an estimated 1 million out of a total labor force of around 9 million(in 1974) has assumed temporary employment abroad. Second, there is someevidence of growing regional and occupational imbalances, due to low inter-regional mobility of labor and to unmatched skill requirements in a fastchanging economy. And third, severe underemployment persists in the privateagricultural sector.

Recent Developments

9. In 1974, Yugoslavia recorded a rapid increase of GDP of 8 percentin real terms as compared to 5 percent and 4 percent in 1973 and 1972 respec-tively. Industry was the leading sector with an estimated growth rate of 11percent in 1974; however, the growth of agricultural production, enhanced byfavorable weather conditions, and of services (with the exception of tourism)also accelerated during the year. This rapid expansion of economic activitypermeated the whole economy. Investment outlays grew in nominal terms byalmost 50 percent and consumer incomes by close to 30 percent during the year.The resulting rapid increase in total demand for goods and services was re-flected both in the rise of employment and of imports - both in nominal andreal terms - and domestic prices. The gain in total employment amounted toabout 5 percent in 1974 and exceeded for the first time the natural increaseof the labor force. The industrial price index rose by almost 30 percentwhile the cost of living index rose less rapidly by some 21 percent. Sinceincome and fiscal policy leave, for institutional reasons, little room fordemand management, the major response to the inflationary pressures was interms of monetary policy. After an expansionary phase during 1972 and 1973,the money supply increased by only 24 percent as compared to a nominal in-crease of social product of about 36 percent. The shift to a large deficit inthe balance of payments materializing in 1974 also contributed to the increasedeffectiveness of the monetary policy.

10. The balance of trade deficit increased from US$1.7 billion in 1973to almost US$3.7 billion in 1974 both on account of an increase in the volumeand the rapid rise in the price of imports and the stagnation of real exports(the terms of trade for the country are estimated to have deteriorated byabout 10 percent). The traditionally large surplus for invisibles (mostlyfrom workers remittances and tourism receipts) failed to compensate for thelarge trade deficit and the country recorded a current account deficit in ex-cess of US$1 billion in 1974 as compared to a surplus of US$464 million in1973. To counteract the situation, the import regime was gradually tightenedsince August 1974, affecting a large variety of consumer goods and some capitaland intermediate goods. In addition, the National Bank raised the intervention

-4-

point in the foreign exchange market, in effect devaluing the dinar by about7 percent as against the currencies of Yugoslavia's major trading partners.The large current account deficit has led to some loss of foreign exchangereserves; after gains of US$632 million in 1973, the official reserves fellby US$345 million in 1974. In addition net foreign borrowing, which averagedUS$390 million during 1971-73, increased to around US$65n million in 1974.Coranercial import credits from suppliers and credits from financial institu-tions continued to be the major sources of foreign capital. Long-term fundsre'lated to financing of development are being made available mainly by theIBRD and some bilateral donors (particularly the Federal Republic of Germany).Yugoslavia has also been one of the beneficiaries of the IMF's Special OilFacility. Yugoslavia's medium- and long-term external debt outstanding as ofDecember 31, 1973 was US$4,319 million (disbursed onlv) and is expected tohave increased to about US$5.1 billion during 1974. Debt service paymentsamounted to about 14 percent of foreign exchange earnings (including workersremittances) in 1973 and about the same ratio is estimated for 1974.

Prospects for 1975

11. The economic program of Yugoslavia for 1975 envisages a slowdown ofoverall growth to about 6 percent in real terms. This, in combination witha reduced rise of import prices should ease the inflationary pressures. Thegood harvest in 1974 should affect favorably both food exports and imports.Measures have also been taken to encourage other exports, especially to oilexporting countries and to the non-convertible currency area where valuableraw materials can be obtained in exchange for Yugoslav manufactured goods.Workers' remittances and receipts from tourism are expected to increase mar-ginally. While these changes may lead to some improvement in the country'sbalance of payments, there is little hope that the current account deficitwill be significantly reduced during the current year. Yugoslavia will there-fore need to continue to raise foreign capital on a fairly large scale, mostlyfrom established channels such as the Euro-currency market, suppliers creditsand the W4orld Bank. In addition, greater use may be made of credit linesfrom COMECON countries, and efforts to open up new sources of capital in OPECcountries will be enlarged.

Medium- and Long-Term Objectives and Prospects

12. The aggravation of major economic problems during 1974, such asrapid inflation and balance of payments pressures, has led to a reappraisal ofdevelopnrent objectives. In the light of the recent shift of relative prices7 n favor of raw materials, ,nore emphasis will be given to the development ofYugoslavia's owr. natural resources, mainly at the expense of processing in-dustries. In this connection, the development of the energy sector is giventhe highest priority. It focuses on electric power, where the generatingcapacity is likely to fall critically short of the rapidly rising power re-quirements of the expanding economy. The development of the power sector williargely be based on the large unutilized hydropower potential and soft-coalreserves of: the country. Other -riority activities are ferrous metallurgy,so-u.e segrenr.s of nor-ferrous metallurgy (notably lead, zinc, copper, nickel and

- 5 -

bauxite/aluminum), technologically advanced production equipment, basicchemicals including petroleum refining, agriculture and food processing,interrepublic transportation, multipurpose works, and housing and basicconstruction material.

13. This emphasis on accelerated development of the raw material basisand the deepening of the economic infrastructure requires a more capital-intensive investment pattern, associated with longer time-lags between invest-ment and output. To sustain this development path, both continued high bor-rowing abroad and an increased savings rate will be essential. Therefore,the income policy - i.e. the guidelines governing the distribution of enter-prise income between workers' income and accumulation - will have a crucialrole.

14. The new Five Year Plan (1976-1980), presently under preparation,will focus on the implementation of these objectives. For growth, an averagerate of 7 percent per year is proposed as feasible, comparing with a targetgrowth rate of the present Plan of 7.5 percent and an expected realizedgrowth rate of 6.5 percent. For employment, the average planned growth ratewould come to about 3 percent with annual increments exceeding the naturalincrease of the labor force by growing margins. This would permit morevigorous pursuit of two major social objectives: the reduction of the numberof temporary migrants abroad, and an increased absorption of the rural under-employment into the social sector. The economy will continue to be open tothe world market although the compositon of foreign trade is expected tochange with a reduced share for raw material, semifinished products andconsumer goods on the import side, and an increased share for agriculturalproducts and manufactured goods on the export side. Workers' remittanceswill decline (relatively, and possibly in absolute terms), but rising tourismreceipts are expected to compensate for this loss in invisible exports.

15. The reduction of regional disparities is another priority objectiveof the new Five Year Plan. To that end, the transfer of financial resourcesto the less developed regions in the form of loans at concessionary terms foreconomic investment and budgetary grants for social development will be con-tinued and will increase at a rate of around 7 percent per year in real terms.Since most of the natural resources of the country, including hydropower, areto be found in the less-developed regions, they will, in additon to the trans-fers, benefit from the increased emphasis on the development of basic indus-tries and power which will to a considerable degree be financed through directfinancial contribution from the consuming regions.

16. The new Five Year Plan will be prepared according to the self-management principle as stipulated by the Constitution of 1974, i.e. largelyfrom the bottom up. Planning commences at the level of individual workingorganizations (economic enterprises or social institutions) and proceeds ina unifying process of converging consensus finding. Working organizationsset out their initial programs, coordinate them horizontally (within the sameactivity) at the level of the Republics or Provinces and - for the priority

- 6 -

sectors - at the level of the Federation, and they reconcile them verticallywith supplying and/or consuming activities, again on a regional and nationallevel. At an advanced stage of consultation and adjustment, the socio-political organizations (communes, Republics and Provinces, the Federation)will join the planning process in order to ensure the integration of overalleconomic and social objectives and constraints. The consolidated programsof action, which in their totality will constitute the operational portionof the Plan, will be codified in the form of "social contracts" or "self-management agreements" which are legally binding for the whole Plan periodunless renegotiated in the case of major deviations occuring in the course ofPlan implementation. The new Plan, thus, will differ from the previous Planin strengthening and formalizing the commitments for implementation by enter-prises, banks and government institutions.

Creditworthiness

17. In spite of the present unsettled conditions, the prospects forYugoslavia's continued economic growth during the next decade are good. Thecountry's endowment of natural and human resources, its relatively low de-pendence on imported primary energy, its pragmatic approach to economicproblems and its readiness to undertake institutional changes, combine togive grounds for a favorable assessment of future prospects. Due to thesize and structure of external borrowing during 1974 and the years to come,the debt service ratio is expected to gradually increase over the next fewyears, from 14.4 in 1974 to 14.8 in 1976. However, taking into accountYugoslavia's debt service record and the measures taken in the past to controlbalance of payments problems, as well as the prospective growth of productionand structural improvement of the balance of trade, Yugoslavia remains credit-worthy for a substantial amount of Bank lending.

18. Many of the high priority projects in Yugoslavia have a low foreignexchange component due to the relatively advanced state of Yugoslav industryand the competitiveness of Yugoslav contractors. Were the Bank to confineits lending to the foreign exchange costs of projects, an adequate contri-bution to Yugoslavia's external capital needs could be made only by spreadingthe lending over a large number of projects, including some of lesser priority.It is therefore appropriate to provide for some measure of local expenditurefinancing in the Bank's lending program, especially in the less-developedregions.

PART II - BANK GROUT OPERATIONS IN YUGOSL-VIA

19. The Bank has made 35 loans totalling about US$1,181 million toYugoslavia. Of this amount approximately 50 percent (US$571.4 million) hasbeen for 13 loans for the transportation sector - seven for highways totallingUS$220 million, four for railways totalling US$248 million, US$59.4 millionfor the Naftagas pipeline, and $44 mil_Lor, for the Port of Bar Pro4cz:. Banklending has generally concentrated on infrastructure i,ncluding, in additionto the transportation loans, power (four loans tota-1ing US$205 milLion),

- 7 -

telecommunications (one loan for US$40 million), three multipurpose projectstotalling US$103 million and US$6 million for the Dubrovnik Water Supply andWastewater project. Nine loans have also been made for industry and two eachfor tourism and agriculture. IFC has made investments in nine Yugoslav enter-prises totalling about US$130 million.

20. The Federal Government of Yugoslavia with Bank encouragement hasrecently streamlined the procedures for declaring loans effective. GuaranteeAgreements for all loans which formerly required approval from each republicand autonomous province can now be approved by a Federal Coordinating Committee.The average time required to declare loans effective is expected to be reducedfrom six to three months. Over $140 million were disbursed during FY75, com-pared with $59.4 million in FY74.

21. The major objectives of Bank lending to Yugoslavia are to acceleratedevelopment in the less-developed regions of the country; to promote agricul-tural development, particularly among the small private farmers by providingbasic infrastructure and credit for the financing of farm development, equip-ment and processing facilities; to promote structural reforms in major sectorsof the economy through improved coordination and the strengthening of institu-tions; and to provide Yugoslavia with long-term external capital and thusreduce the country's dependence on short-term external borrowings. Theseobjectives are basically the same as those which have guided Bank lending inprevious years, but efforts to give special support to the less-developedregions are being strengthened.

22. Over the next two years loans envisaged for less developed areasinclude the initial loan for a major multipurpose water development programdesigned to provide flood control, industrial and domestic water supply,irrigation, and sewerage; the second loans for agricultural and industrialcredit; and loans for irrigation. Highway, railway and power transmissionprojects during the same period will both assist the less-developed regionsand promote structural reforms in the transport and energy sectors. IFC iscurrently investigating several new investment opportunities to encouragejoint ventures which would provide technical, management and marketingexpertise as well as long-term capital.

23. In addition to substantial assistance given in identifying and pre-paring projects for Bank financing, the Bank is providing technical assistancein several areas. A series of regional studies of the four less-developedregions of Yugoslavia was initiated two years ago and two studies, coveringKosovo and Bosnia-Herzegovina, have been completed. This fall, the thirdstudy, of Macedonia, will be completed and the field work for the fourth(Montenegro) will begin. This series, when completed, will contribute tobetter assessment of development programs and will assist in formulatingdevelopment strategies for these regions. A Bank assisted study on theimprovement of the financial mechanism has been concluded and its recommenda-tions have been included in draft legislation for a new banking law. A Bank

- 8-

assisted training program for auditors of the Social Accounting Service, whichaudits all enterprises and Government activities, including Bank financedprojects, has progressed satisfactorily and further training is underway incooperation with an English accounting firm. Assistance from EDI, as well asBank operations, has been directed towards the improvement of project evaluation.

24. The level of Bank lending has risen substantially to an average ofabout US$200 million during the period FY74-76. Although this represents onlya small proportion of the country's need for external finance, it would beequivalent to almost one-third of the annual long-term official capital in-flow in convertible currencies. The outstanding debt to the Bank is expectedto remain at less than 10 percent of Yugoslavia's total external debt. Serv-ice on Bank loans as a proportion of total debt service would decrease from4.8 percent in 1973 to 4.5 percent in 1976.

PART III - THE ENERGY SECTOR

25. Traditionally Yugoslavia has covered a large part of its energyneeds from its own resources, but the degree of self-sufficiency has beenfalling. In 1965 domestic production accounted for 84 percent of consumptionon a calorific basis, but by 1973 the percentage had dropped to 67. Thistrend, coupled with the sharp increase in world energy prices nearly two yearsago, explains why Yugoslav national energy policy is now based on restrainingdependence on imported fuel through the development of indigenous energy re-sources.

Energy Resources

26. Yugoslavia's main domestic energy resources are lignite, coal andhydro-power. Lignite and coal account for 97 percent of the fossil fuel re-serves (hydrocarbons for the balance). Most of the lignite and coal is ofpoor quality and is located in Kosovo and Bosnia-Herzegovina. Since trans-portation over long distances is not economic, it is used mainly for powerand steam generation. Hydro-power resources amount to about 60,000 millionkWh/years, 70 percent of which are located in Croatia, Serbia and Bosnia-Herzegovina. About 2.5 percent of total Yugoslav energy resources are proven,recoverable natural gas and oil reserves. Most of the gas lies in Vojvodinaand the oil in Croatia and possibly off-shore in the Adriatic. Preliminarysurveys suggest that some 36,500 tons of uranium concentrate could be recoveredfrom an area of 170,000 km2 with suitable geological formations. The mostpromising deposits 1.ie in Slovenia.

Demand and Suplv

27. After a period of relative stagnation, overall energy consumption-increased rapidly from 1967 to 1973 at an average rate of 8.2 percent perannur.1 compared with a-n average GNP increase of 6.4 percent per annum. Duringthe same period the structure of demand changed considerably and coal, which

-9-

had been traditionally the predominant fuel, was surpassed by oil. This wasdue primarily to the development of a modern industrial sector and to therapid growth of road transportation. In 1973 oil consumption accounted forover 40 percent of the total demand compared with 28 percent in 1967. Theindustrial and transportation sectors account for 84 percent of total demandfor oil products. Oil and gas consumption in power generation has alwaysbeen and will remain marginal, as most of the projected increase in capacitywill be based on the use of domestic coal and hydro-power.

28. Domestic oil production which, in 1973 amounted to about 3.3 mil-lion tons, has not kept pace with demand and Yugoslavia has to rely in-creasingly on imports to supply its six domestic refineries (Rijeka, Sisak,Bosanski Brod, Novi Sad, Pancevo, and Lendava). In 1973 oil imports ac-counted for 70 percent of total internal demand for refined products. Hither-to, the USSR has been the main foreign supplier of oil. However, in recentyears, Yugoslavia has been importing increasingly from the Middle East (Iraq,Iran). Russian crude is imported through the Danube by barge, while MiddleEast crude is imported through Adriatic ports and transported by rail to therefineries of Sisak and Bosanski Brod.

29. Since Yugoslavia is a large importer of crude oil, it was seriouslyaffected by the oil crisis although the problem was more one of prices thanavailability. Because of the poor quality of domestic coal, the possibilityof substituting coal for oil is limited and only minor adjustments could bemade in the short-run to reduce the country's dependence on foreign oil. Themain steps taken were increases in the price of refined oil products and thecreation of an equalization fund to align the price of domestic crude withworld market prices; as a result, the increase in the consumption of oilslowed down to 6 percent per annum in 1974 compared to 7.7 percent in 1973.

30. Before the oil crisis it was expected that total energy demand wouldcontinue to grow rapidly and would increase 3.5 times between 1973 and 1990.Similarly it was expected that oil demand would continue to grow faster thanoverall demand and would be satisfied primarily by imports, since domesticoil production was not expected to meet more than 9 percent of the totalenergy demand. By 1990 it was confidently expected that hydrocarbons wouldaccount for more than 51 percent of total energy demand.

31. Following the oil crisis these projections were lowered. Prelim-inary studies show that total energy consumption will increase by only 3times over the next 15 years reaching about 83 million tons of oil equivalentby 1990. Hydrocarbon demand will grow at the same pace as total demand.However the volume of oil imports in 1990 will be almost identical to thatprojected previously because the previous projections were based on rapidgrowth in the use of natural gas which is not likely to materialize sincerecent evaluations of domestic fields have been disappointing. Furthermorethe previous projections for domestic oil production were over-optimistic.It is now estimated that domestic production will start declining after 1985reaching 5 million tons in 1990 instead of 8 million as previously projected.

- 10 -

32. Based on these projections it is now considered that imports ofcrude oil will increase from about 7.9 million tons in 1975 to 28 milliontons in 1990, at average rates per annum declining from 11 percent between1975 and 1980, to 8 percent and 7 percent between 1980 and 1985, and 1985and 1990, respectively. Most of this oil will be imported from the MiddleEast through Adriatic ports and transported overland to the inland refineries.

Sectoral Organization

33. The Yugoslav system of decentralized economic management does notfacilitate coordination between the various Republics and Provinces. Further-more it is not yet clear how the emergence of self-managing communities ofinterest in the power sub-sector, responsible for all aspects of the supplyand demand for power, will affect the situation. However there has been adetermined effort at closer coordination within the energy sector as a wholeover the last two years, encouraged by the Bank and by the changing interna-tional oil situation.

34. In 1974, following discussions with all the Republican and Provin-cial governments, the Federal Executive Council issued a document entitled"The Basis of Common Policy for Long-Term Development of Yugoslavia". AFederal Committee on Energy and Industry (FCEI) was set up with responsibilityfor coordinating the planning and implementation of energy programs. Thesedevelopments are evidence of the governments' desire to create a more rationalframework for development within the sector. Under the aegies of the FCEI,studies have been carried out which will form an integral part of the nextFive-Year Plan, currently in the final stages of preparation. The main ele-ments of energy policy over the next few years emerging from these studiesare that Yugoslavia should limit its dependence on imported fuels and developdomestic sources to the maximum extent possible, that coal should be used inpreference to hydrocarbons whenever feasible, and that national energy re-sources should be safeguarded in a manner consistent with maintaining thenation's overall economic growth. It is too early to assess how well thesepolicies will meet the country's needs. But the substantial reductions inthe level of demand projections already made through the elimination of dup-lication in individual enterprises' development plans, suggest that bettercoordination should prove beneficial. The proposed project, in which threeenterprises normally in competition are cooperating together, is a reflectionof this trend.

Pri,oes

35. Energy pricing policy is presently under review. The problem ofaligning domestic oil prices with those of imported oil has been solvedthrough the mechanism of the equalization fund and an increase in the priceof refined products. Gas producers are seeking comparable increases in gasprices. However, given the serious attempts to keep inflation under control,the authorities have been reluctant to increase the prices of other sourcesof energy.

36. In spite of Yugoslavia's relatively low dependence on imported oil,increases in the price of oil are bound to affect the government's effortsto improve the external payments position. In 1973 oil imports amounted toUS$259 million, or 6 percent of commodity imports. For 1974 oil import pay-ments were of the order of US$900 million, at an average c.i.f. price ofUS$100 per metric ton (US$13 per barrel), equivalent to about 13 percent ofimports of goods and services. The impact on the balance of payments hasbeen to contribute to a substantial current account deficit in 1974, whichwill continue in later years, instead of the surpluses Yugoslavia has recent-ly enjoyed.

37. The Bank's main involvement in the field of energy thus far has beenthe four loans made to the power sector, where the emphasis has been on highpriority generation projects and on extending the national grid. The Bank hasalso made one previous loan in the pipeline subsector, for the Naftagas project(Loan 916-YU of June 25, 1973), which provides for the facilities to transmitnatural gas from Vojvodina, and later from Hungary, to industrial consumers inVojvodina and Serbia (see Annex II). A Bank sector mission currently in thefield is reviewing with the Yugoslav authorities their proposals for thedevelopment of the energy sector.

PART IV - THE PROJECT

38. As their main source of crude oil has shifted from Russia to theMiddle East, Yugoslavia and some of her eastern neighbors have long been con-sidering the most suitable means of bringing Middle Eastern crude, presentlytransported by rail from various Yugoslav ports, to the refineries. It becameapparent that a pipeline system connecting an Adriatic port of entry withYugoslavia's five inland 1/ refineries, and those of her neighbors, would beeconomic. The Bank helped to determine the most favorable pipeline systemwithin the context of a transport sector survey in 1971. Subsequently, inJuly 1973, the three leading oil and gas enterprises in Yugoslavia - INA,Energoinvest and Naftagas - formed a consortium which later became known asJugoslavenski Naftovod, to carry out the project. The Yugoslav governmentasked the Bank to participate in the financing of the project in order tofacilitate the raising of other external finance on reasonable terms. Afeasibility study was carried out by INA Engineering, a Yugoslav concern, anda UK firm of consultants. The project was prepared in 1974 and appraised inJanuary, 1975. Negotiations were held in Washington in July, 1975. TheYugoslav Delegation, which was led by Mr. Juraj Kontent, Legal Advisor,Naftovod consisted of representatives from the Federal Government and Naftovod.

1/ The sixth, at Rijeka, is at seaboard and would not be served by thepipeline.

Project Description

39. The project, which is summarized in Annex III and described in

detail in the report "Appraisal of the Yugoslav Oil Pipeline" (Report No. 886-YU

dated October 7, 1975), would consist of the construction of an oil port at

Omisaij, just south of Rijeka, 736 'mi of pipeline, storage tanks, pump stations,

a control system,-, sundry equipment anrd engineering services. It would provide

overland oil transoortatior facjiAties -with a capacity to pump by 1979 20 mil-

lion tons of oil annually, ircluding 6.6 million tons in transit to refineries

in Huungary and Czechoslovakia. The project would be the main part of Naftovod's

invest.Tlent program! desigred to handle bulk oil transport through 1990. The

balance of the program would consist of increasing the port, storage and pump-

ing facilities sufficiently to enable the system to handle the ultimate capa-

city of 34 m-illion tons by 1990, including 10 rmiillion tons in transit. The

project would only cover construction within Yugoslavia. It would be carried

out in two stages. Stage I would comprise the facilities to transport 16 mil-

lion tons of petroleum per year and would be completed by 1978. Stage II would

bring the total capacity up to 20 million tons by 1979. The ultimate expansion

of the pipeline system, and terminal facilities to handle 34 million tons an-

nually by 1990 (Stage III) is not included in this project.

40. Naftovod used computer simulation models to optimize the size of the

pipeline and tanker terminal.. The methodology used was satisfactory and led

to reduction in the diameter of the Sisak-Slobodnica section of the line and

in tankage capacity. Naftovod, however, has decided to maintain the diameter

of the first section (Omisalj-Sisak) at 36" for which the study shows the

optimum size to be 34". The main reason behind this decision is that transit

traffic might increase in the future (discussions have taken place with

Austria), and that it would be difficult to increase the capacity of the first

section of the line to satisfy additional transit requirements, since it

crosses difficult mountainous terrain. In the light of the comparatively

small difference in initial :lnvestment costs (less than US$3 million, i.e.

0.75% of the total project cost) this decision is acceptable.

Implementation

41. The project would be implemented by Naftovod, a new enterprise set

up to construct and operate the pipeline, which would transport crude oil

from the ocean terminal to the off-takers. While still involved in construc-

tion Naftovod would, in accordance with Yugoslav practice, have its internal

affairs ruled by a governing body appointed by Naftovod and its founders.

14her. the pipelIne starts o?e.:at_.ng, the council would be replaced by the

no!rmal Wor er- .ouncil, e:ected by t;h. staf-f of the enterprise. From the

ouatset there wti` ne a business com-mittee made up of six founders' represen-

-at4ves plUs >>Naftovod"s gcerne-al -ange r, to advise .Naftovod's management on

policy matters. Nearly ha>: of Naftovod's p-resent establishment of about

.00 people has been recruited. There is an ample reservoir of experience in

p:peline constrcucttion an, cna a:TiOn and Naftovod should not encounter any par-

Zi cuar difILcuity ir bri`g- ±y S staff up o strength. However the project

wou,l` Drov`dtc -or train-n;. -a sreclal skills like instrumentation and oil dis-

v,atching, .o begin no later t:han May 31, /977. (Section 3.04).

- 13 -

42. Under agreements already signed Naftovod will incur penalties ifit fails to start deliveries to both domestic and foreign refineries by May 31,1978. The construction schedule for Stage I is geared to completion by thisdate. This schedule is very tight, and Naftovod has undertaken to make everyeffort to meet it. However, should any unforeseen development make this im-possible, Naftovod has agreed to seek the agreement of the five Yugoslavrefineries (owned by its Founders) to postpone the start of oil deliveries tothem, as well as take all measures within its powers to minimize constructiondelays, so as to meet its commitments to deliver to the foreign offtakers(Section 3.11). Acquisition of all land and access to land required for theproject has been approved in principle by the communes or other local authori-ties concerned, and Naftovod will complete arrangements for final purchase oraccess as required to permit construction to proceed on schedule (Section 3.09).Delays in finalizing land acquisition should not occur, since this project hasbeen formally designated a project of national importance by the Assembly ofthe Federal Republic, thereby giving Naftovod the right to expropriate any landthat it could not otherwise acquire on reasonable terms.

43. Overall engineering responsibility has been assigned to Industro-projekt, a local engineering consulting enterprise, assisted by French con-sultants, who would be responsible for designs, tender preparation, coordina-tion and supervision. (Section 3.02). Competent inspection agencies wouldbe employed to ensure that the pipe provided by Kuwaiti and Czechoslovakmills, meets acceptable standards (Section 3.03) (see para. 47 below).

44. The port facilities financed under the project would be operated bythe Rijeka Port Enterprise in accordance with an agreement to be entered intoby May, 1977 between Naftovod and the Port (Section 3.06). The refinerieswould arrange for the supplies of crude oil.

Project Costs and Financing

45. The project would cost US$377 million, including local taxes (US$15.7million) and contingencies amounting to nearly 40 percent of basic projectcosts. Price contingencies account for the major share (72 percent) of thecontingency allowances; physical contingencies account for the balance (28percent). Both allowances are in accordance with Bank Guidelines and areconsidered adequate. The foreign exchange component would be US$193.2 million,or 51 percent of total costs. Interest during construction on all loans butKuwait's and the Bank's proposed loan will accrue, but will not be payableuntil operations start; interest will be paid during construction on theKuwait and Bank loans, and US$23 million is included for this purpose in thefinancing plan.

- 14 -

46. The terms and conditions of the financing for the project would beas follows:

US$ (Million) Interest Rate Grace RepaymentLocal Foreign Annual % Period Period

(1) IBRD 49.0 8.50 4.0 14(2) Kuwait 125.0 8.50 4.0 8(3) Hungary 25.0 8.25 3.0 6(4) Czechoslovakia 25.0 8.25 3.0 6(5) Libya 70.0 9.00 3.0 7(6) Founders 26.5 - 6.0 25(7) Petroleum Fund 59.0 2.00 3.0 15(8) Local Banks 20.5 12.00 3.5 7

Total $106.0 /1 $294.0 /1

Grand Total $400 /1

/1 Includes interest during construction on Kuwaiti and Bank loans.

The proposed Bank loan of $49 million would cover 13 percent of total projectcosts, or 25 percent of foreign exchange costs, and would be for a period of18 years, including 4 years of grace. The loan would cover the foreign ex-

change costs of construction services (save for the stretch of pipeline fromSisak to the Hungarian border which Czechoslovakia would finance and construct),consulting services, and the procurement of two tugs and oil loading arms.Bank financing would be spread over the construction period in parallel withthat of other foreign lenders. There would be a small amount, not exceeding$500,000, of retroactive financing of consultants' services dating fromMay 1, 1975.

47. All the financing for the project has been secured. Agreements withCzechoslovakia and Hungary were signed last December and with the Libyan ArabForeign Bank in June 1975. A protocol agreement has been signed with the KuwaitiGovernment and detailed negotiations have been completed with the Kuwait ForeignTrading, Contracting and Investment Company. The loan from Kuwait would includethe supply of 58,000 tons of pipe equivalent in value to about 33 percent ofthe loan. Similarly the Czechoslovakian loan would be in the form of 28 inchpipe and construction services for the stretch of pipeline from Sisak to theHungarian border. The loans from Hungary and Libya would be straightforwardfinancial participations. All local funds for the project have been secured.Since the participation of all the financing agencies is crucial to the proj-ect, Naftovod has agreed that effectiveness of all financing agreements wouldbe a condition of effectiveness of the Bank loan (Section 7.01(a)).

48. Kuwaiti and Libyan participation is linked to the Bank's appraisaland continued involvement in the project. The proposed loan will enable theBank to play a part in ensuring that sound engineering standards are main-tained throughout construction.

49. The agreements between Naftovod and its founders, the owners of thefive refineries, provide for annual revisions of Naftovod's tariffs to takeaccount of operating costs plus a surplus equal to 25 percent of its grosssalaries. These measures should guarantee Naftovod substantial annual operat-ing surpluses rising from $0.13 million in 1978 to $12.6 million by 1988, afterall expenditures, including debt service, are met. Naftovod has agreed thatit would not amend the offtakers' contracts on matters relating to capacitiesand tariffs, without prior consultation with the Bank (Section 3.10). Theagreements with Czechoslovakia and Hungary provide for tariff charges indexedt o the price of steel, labor and electricity and should enable Naftovod tomake a net surplus on transit totalling $85 million over the period 1978-1988which would be transferred to the refineries.

50. Naftovod has entered into take-or-pay agreements with the futureofftakers which provide that the offtakers would pay 80 percent of the tarifff or any allocated capacity not utilized; likewise Naftovod would pay 80 percentof the tariff for any agreed amount of oil that it fails to deliver. The take-or-pay clauses are voided by events of "force majeure" qualified, in the caseo f the agreements with the Founders, as events lasting more than six months.Temporary shutdowns of the pipeline lasting a few days should pose no finan-cial threat to Naftovod, and a total shutdown for periods exceeding a few daysis extremely unlikely. However, to guard against the possibility that a majorhazard like a fire or landslide might close the pipeline for up to six months,or that project completion might be delayed, Naftovod has obtained guaranteesfrom the two local banks that are participating in the financing of the projectto meet these financial commitments in case of need, other than the debt serv-ice obligations on the Bank loan (Recital (R)(v)). The latter is of courseguaranteed by the Federal Republic.

51. Should cost overruns occur in the project, they will be covered intwo ways. First, the Founders have agreed to finance all cost over-runs,and appropriate amendment of the Founders' and the Founders-Naftovod Agreementsis a condition of effectiveness of the proposed loan (Section 7.01(b). Second,the local banks will provide for cost over-runs in proportion to their parti-cipation in the project. These two arrangements will ensure that cost over-runs, if any, will not aggravate the already tight implementation schedule.

52. The Federal authorities have agreed to finance on a grant basis theinitial supply of crude oil to fill the pipeline and storage tanks includedin the Project (Section 2.02, Guarantee Agreement).

Audit

53. Agreement has been reached that Naftovod's accounts for the year1979 onwards would be audited by the Social Accounting Service in accordancewith the procedures now common to most recent Bank projects (Section 5.02).

- 16 -

Procurement

54. Procurement under the loan would be by international competitivebidding in accordance with the Bank Group's `Guidelines for Procurement".Exceptions would be: (a) construction contracts not exceeding US$100,000 pro-

vided that in the aggregate they do not exceed US$1 million, would be letby local shopping, and (b) construction contracts over US$100,000, but not

exceeding US$500,000, provided that in the aggregate they do not exceed US$9million, would be let after local competitive bidding. These exceptions areappropriate because the works concerned are geographically dispersed and theamounts involved too small to interest foreign firms. The construction coststo be financed by the loan would exclude all construction materials andequipment and the'related transportation cost (if imported), since these areto be financed by other foreign loans. Yugoslavia has no preference treaties,and bids for the tugs and loading arms would be compared on a CIF basis netof customs duties; a preference of 15 percent of the CIF Price, or the actual

customs duties, whichever is lower, would be given to local manufacturers.

55. In view of the specialized nature of the work and the tight proj-

ect schedule Naftovod agreed to prequalify construction contractors under theBank's Guidelines for Procurement. The Bank would thus assist Naftovod in

screening contractors, particularly evaluating the capacity of local con-

tractors who might be fully occupied in other oil and gas pipeline projectsbeing undertaken in Yugoslavia and hence might require the cooperation of

international contractors. Local contractors are competent to construct the

port facilities, pump stations, tanks and some of the pipelines; the mostprobable outcome of the bidding would be a mix of local contractors and jointventures between foreign and local firms.

56. The Kuwaiti and Czechoslovak loans would together involve the supplyof some 73,000 tons of pipe. It is important that the pipe be made accordingto internationally-recognized standards and supplied in accordance with theproject schedule. Naftovod has provided the Bank with an engineering reportprepared by consultants establishing that the mills in question can supplygood quality pipe, but raising some question as to whether the mills can

supply the pipe in time to meet the construction schedule. Any delay in thedelivery schedule will, however, be detected in time for Naftovod to obtain

supplies from alternative sources. Naftovod has also agreed to select andhire competent inspection agencies to inspect the pipe at the mills (Section3.03).

Disbursements

57. Loar. d'isbursemTents would cover the foreign exchange costs of the

foreign consultants, the foreign exchange costs of construction contracts

with foreign firmis or 25 pe-rcent of the total cost of local construction

contractors, and the total .oreign exchange costs of two tugs and loading

arms for two berths if procuired abroad or 75 percent of their total cost if

procured locally. Disbursements are exDected to take place over a four-year

period frof,, the fourth quarter of 1975 to the fourth quarter of 1979.

Rate of Return

58. The comparison of the project cost and that of the next best alter-native, a combination of rail and inland waterways, shows that the rate ofdiscount which would equalize both cost streams over 20 years would be 50percent. This high rate of return indicates that the facilities should havebeen built sooner. If oil imports were lower than forecast so that the traf-fic in 1990 were only 35 percent of the projections (a conservative assump-tion), the pipeline would still be the least cost solution for the transportof oil, and the rate of discount which would equalize both cost streams over20 years would be in excess of 43 percent.

59. The benefits derived from the project would be savings in transpor-tation costs which are estimated at about 1 percent of the average salesprice of oil products. During construction, the pipeline would provide em-ployment to some 2,000 persons while during operations some 350 staff wouldbe employed. The increase in the transport of refined oil products and othercargo resulting from normal growth of the economy would, in a short time, makeup any temporary slack created by the pipeline in the railways and the fewlocal waterways carriers involved.

Environment

60. The land in which the pipe would be buried would be restored toits normal use. The pipe would be laid deeply enough to avoid interferencewith land cultivation, highway and railway crossings, natural drainage, andanimal migration. Under the aegis of a UNDP Study Group for "Protection ofHuman Environment in the Yugoslav Adriatic Region", environmental impactstudies are being carried out by various consultants. The Guarantor andNaftovod have separately agreed to implement the measures recommended to,inter alia, contain oil spills, receive slops from tankers and purify alleffluents from the installations (Section 3.05 (Loan Agreement) and Section3.03 (Guarantee Agreement)).

PART V - LEGAL INSTRUMENTS AND AUTHORITY

61. The draft Loan Agreement between the Bank and Jugoslavenski Naftovod,the draft Guarantee Agreement between the Socialist Federal Republic ofYugoslavia and the Bank, the Report of the Committee provided for in Arti-cle III, Section 4 (iii) of the Articles of Agreement and the text of a draftresolution approving the above loan, are being distributed to the ExecutiveDirectors separately.

62. Special conditions of effectiveness of the proposed loan were notedin Paragraphs 47 (effectiveness of all other financing agreements - Section7.01(a)), and 51 (provision for financing cost overruns - Section 7.01(b)).

- 18 -

63. I am satisfied that the proposed loan would comply with the Articlesof Agreement of the Bank.

PART VI - RECOMMENDATIONS

64. I recommend that the Executive Directors approve the proposed loan.

Robert S. McNamaraPresident

Attachments

Page I

CO0NTRT DATA - Th0ILGSAVIA

AXEA POPULATION =8ITT

255,01, kml 20.q6 s.ioe. (mid-1973) 22 N l b.lu

SOCIAL INDICATORSRfrncCotre

Off PBS CAPITA US$ (ATLA BASIS) /1 375 890 /a 89'0 1,210 3,390 b

DE2GRAP1ICr&Wthrate (Pe, thouand) 21 19 8 1.1 -19 / 10.,2

Crude death rate (per thou.and) ii 9 9.2 9 u 10.

I,fact mortality rate (par thounad lIte birth.) 28 3 . 38 ~ 1 ~ 20.1

Le ctoyat birth (years) 62 68 69d 71'L 71.3

Oros. anuiiort/ 1.31313 22

Fpoulatio gotrae 1.2 . 0 11 09

Population groth r-te - orbam z

Al.aruur (pmrosn)0-11 63 27~, 25 a 28 23.06

5odoor61 654 66 a 63 6360

Age dependency atio /1 0.6 0.5 0. : 6 o3.6Econonc d.peod-oy ;M. A 1. 0.9 0.7 kO 1.1 0.9

Urban popalation os pre,o.t of total 208~ 39 LL.". 12 Zb- 69/1.1 38.1 0.

Family ple-itg. No. of acceptors uolte (thou.. No. of u..ers (1 of narriad ae

X~rIb r force (thousands) 8,300 8,900 10.110 200 ~ 27,100

Peroentap employed in ogrioltoes 57 45Li 28 , 7.2 sPeroonnttge unemplyed 7/ 3. L 0 1 1.1

DIren of ocinlincome -soj-d by highest 5% 17 /1.. 15 L.

Par oant of notional I---.w romived by bighest 20% Li Is.. 12

Poroent of natiol .. oom. ro-i-od by loosst 20% 7 .. 7 23.0 /.

oroent of .. ti ...l in-ne roc-i-d by Ioussi 40% 19 1

t 2 9

DISTNRXUTION OF LAND OWN~ERSHIP

% ownd by wrallest 10% of 0aner,

Poplatonperpholojan.. 180 3 . 30 Z.i 720 53. 60/.

Populatio pen nu,sing P.rson 5 03 l 380 /i 20 950/ 330 7

Population pen bospital bed 19o 170 120 MI 0 90~

Per capita calorie supply a3 % of rsquirace,nt. 115 121 111 107 121

Per napita protisi supply, total (gr- Per doy) g 9 / 92 971 81 88

Of ha,hl,b,anol and poNo 27 2~29 2 O5

Death rate 1-L ye.ar /7 i.7 2.5 2 09 56

Ad3etd a8 priosry schol .oru.1esnt ratio 91 91 109 83 132

Adjusted e=o00day school enrollment ratio 31- h5 62 19 61

Ysar, of shooling provided, first and second level 12 12 12-IL 13 12-15

Vo..ational -nr1le-t as 8 of -a, -chol .. r..l1sont 72 7 50 IR. 0 18

Adult literacy rote % 77 is 5~L/ Va 99 X,n,,ba

"'7iiia No. of Per.ons pun room (urban) ad 3 0.7 /0

Porosnt of occupied onts aithat piped water 6 08 .o .34"

Acrass t elsoinnitll(m % of total P,pulation) - I. 9 7 J 0P.,an of -Io poplti connected to .s.a..tnilaity2 ad of

CONSRGIGTIONp~~eie rpu 1000 pupultion 81 171 4b 150 /b 210 / 329b

P.ssungr oars. per 1000 pupl.tit 3 Li ~ .957 253

Electric power cos-ption (kwh p-c.) 529 LI 1570 rb 1.931 Zb 191 161

Newsprint -nwnption P.c. kg pun year 2.3 L.2/b 2.8 Tb 6.0 1.

Notes: Figures refer either to the leteni periode or to nooio a rmoet.1 teeas'roitre, body -eights, wae

ths oIet.:tynar. Latest period. refer in principle to distribution by age ad ae" of natiOal POPu11imtoA.

ths years 1956-60 or 1966-70; ihe li.t.i yearn i, pl. L.6 Protein standards (reqirm nte) for all nontrias a estab-

dipI. to 1960 nod 1970. Itched by USDA F-nwel teeRob. Sernio provide for a 010150.

A The Per Copito GNP F.ti-tai ie at moket prior for ellowano of 60 gron of total protein par day, ad DO woe of

-ar oth-r thn 1960,.cal-ulted by tin 00- con-rion anma and pulse protein, of which 10 grams ehold be animl

teohniq.e as thn 1972 World Bunk Atlla. protein. The.se tadard. are enmasht lseen than tho of 75

/. Averag. runber of daughters per uonn of reprrduotle groom of total protein an 23 groo of anleal protein an an

oge. anerage for the word, prnposed by PAO In the Third World Food

Pcpulation grothb rtor or for inn docodr ending in Sorry.

1960 and 1970. /7 S-n studies baresmuggested that orude death ratee of children

P atin of PnPulotion under 15 and 65 and over to popolo- age. 1 throogi 4 na be osod as a firot opproatoatino intda of

tion of agos 15-61 for age depoodeny ratio and to labor na-n-tritino.

fnrce of ogeo 15-6h for oco.omic dependency ratio. L/. Percntage enrolld of morreepondilog population of school gag

d PAO reference tand.rds roprnt phy.Ii.ogi-l in- as defi,,ed for each cootryn.

qior.xnnts for corra .. tiinty nod health, taking

A 1973; A~ 1972; /c 190-71-,; Ld 1970-72; /- 1970-75; /f I1960-72; & For the definition of urban oee

bUasorPin Yearbook 197 p. 129; A Citie., t-n and 183 other 1-naltiem haring urban nocin-econ,alo

cbaroinnio;on; L-71 itie o3 f 10,000 or cors inhbitants; Z,j 1971; Ratio of Populntinn under 15 and 65

and or to total labor foc-e; LIEsimate; I. efitnno avIlable I 1969; /o 1971; ~ eimp

hoe nthereotoo s-Rg-.c lh Yr fntn e1963e uoe. H.- 192;h. RatIo of Meg stred Job seekere to activePOPulato; foltrdol; e~~16 ~ ~ buooo; l.1968;- / Percent of eslarled wkrier mannig

less than 1,300 Lei; /. Percent of salarIed onrkers morog =mo than 2,500 Le; zz Nb.nero the register not all

-crInig to tin coutry; Lz 1961;; an_ Palti-io oducatio only; ~a 15 Yearn andi ... r; Urban only;

/ad 1966; /me Tntal, urban ad rural ,A Percetage of dwelling.; ~jWater pipd in -e h nldigodree

.assitant nidvees nod midwifery nod nurng oumliarles.ed i. 7 Ilig dv,,

1970

Agriol.ct-e land hold by ...clnl rector- clur 15.1

Agric-ltre lu-d bold by pri-cat -nol-hoid.rs 81.9

nollolcof Fed,rn1 intPublic or lemot,Y an an bjection countrY in bared onthe lcln --oonl Lies naiclaind by the

too c-trie-, or cell or c- tn foot 1181, tin grecier port of fcclo around -c million norbrs teoporarily

abroadl boo found -npicy-et i. tic Federal hncclllc of Cor__cy.

11 July 18, 1975

ANNEX IPage 2

IMPORT DETAIT,(million US$)

Av.A. Constant (1972) Prices 1967-69 1972 1973 197421/ 1975-?/ 1976?-/

1. Food 131 207 228 243 225 2252. Other consumer goods 309 296 296 353 370 3883. Petroleum 83 161 208 185 220 2304. Other intermediate goods 1,262 1,875 2,194 2,651 2,888 3,0775. Capital goods 547 689 833 902 960 1,0226. Total goods c.i.f 2,332 3,227 3,759 4,334 4,663 4,9427. Non-factor services 299 594 532 529 550 575

8. Total goods and NFS 2,631 3,821 4,291 4,863 5,213 5,517

B. Price Indices (1972 = 100)

1. Food 83.9 100 150 189 190 2002. Other conslmer goods 78.9 100 121 145 170 1953. Petroleum 81.1 100 143 451 450 5004. Other intermediate goods 81.4 100 115 167 173 1815. Cavital goods 78.9 100 121 145 165 1826. Non-factor services 78.9 100 124 155 170 178

C. Current Prices

1. Food 110 207 341 459 428 4502. Other consumer goods 244 296 357 512 629 7063. Petroleum 68 161 297 843 990 1,1504. Other intermediate goods 1,027 1,875 2,512 4,423 4,996 5,5695. Capital goods 432 689 1,004 1,305 1,584 1,8606. Total goods 1,880 3,227 4,511 7,542 8,627 9,7357. Non-factor services 236 594 657 820 935 1,023

8. Total goods and NFS 2,116 3,821 5,168 8,362 9,562 10,758

1/ Estimates.

2/ Projections

July 18, 1975

ANNEX IPage 3

EXPORT DETAIT(million US$)

A. Constant (1972) Prices Av. 19 1973 1974/ 19752/ 1976

1. Meat 245 247 182 75 75 1252. Other agricultural products 54 21 50 55 75 863. Wood 69 83 107 80 90 954. Steel 65 51 88 93 102 1085. Copper 37 53 46 38 40 4L6. Other primary metals 71 82 100 125 135 1487. Machinery and equipment 375 544 621 664 730 8038. Fabrics and clothing 203 274 259 260 265 2709. All other goods 597 1,019 944 1,130 1,366 1,43710. Total goods 1,714 2,237 2,397 2,520 2,878 3,11611. Non-factor services 743 1,188 1,288 1,347 1,414 1,484

12. Total goods and NFS 2,457 3,425 3,685 3,867 4,292 4,600

B. Price Indices (1972 = 100)

1. Meat 62.9 100 136 172 170 1782. Other agricultural products 83.5 100 104 185 185 1953. Wood 77.9 100 130 195 205 2204. Steel 51.3 100 111 156 156 1605. Copper 120.5 100 122 171 170 1806. Other primary metals 103.6 100 115 140 140 1557. Machinery and equipment 78.9 100 117 142 161 1778. Fabrics and clothing 78.9 100 121 135 142 1519. All other goods 78.9 100 117 154 164 18410. Non-factor services 78.9 100 120 150 163 181

C. Current Prices

1. Meat 154 247 247 129 128 2232. Other agricultural commodities 45 21 52 102 139 1683. Wood 53 83 139 156 185 2094. Steel 33 51 98 145 159 1735. Copper 44 53 56 65 68 796. Other primary metals 74 82 115 175 189 2297. Machinery and equipment 296 544 727 943 1,175 1,4218. Fabrics and clothing 160 274 313 351 376 4089. All other goods 471 1,019 1,107 1,739 2,237 2,63710. Total goods 1,330 2,237 2,853 3,805 4,656 5,54711. Non-factor services 586 1,188 1,546 2,021 2,339 2,687

12. Total goods and NFS 1,916 3,425 4,399 5,826 6,995 8,234

1/ Estimates.2/ Projections.

July 18, 1975

Page c

SUMMRY BATANCE OF PAYNTS(million US,t)

1967-69 1972 1973 197)4V 1975_' 197f5

1. Imnorts (inc.NFS) 2,116 3,821 5,163 8,362 9,562 10,7582. Pxports (inc. NFS) 1,916 3,)425 )4,399 5,826 6,995 8,23)43. Balance of goods and NFS -200 -396 -769 -2,536 -2,567 -2,524L. Tnterest (net) -62 -1148 -17)4 -185 -271 -3965. WTorkers' remittances 139 889 1,310 1,512 1,693 1,8)456. Other -factor services (net) -17 - 10 - - -7. Current transfers (net) 38 74 87 109 125 1258. Balance of current accounts -101 419 46L -1,100 -1,020 -9509. M & iTT loans 1/

a. Disbursemnents 419 838 1,020 1,235 1,867 1,9)46b. Repayments -210 -507 -616 -870 -997 -1,096c. Net disbursements 209 331 )404 365 870 850

10. IMF drawings -7 22 - - - -11. Other short term 2/ -69 -97 -205 297 150 10012. Use of reserves -33 -675 -663 438 - -

Memo Items

13. Reserves (net), end period -120 145 689 481 481 )4811L. Debt service ratio 3/ 13.2 15.1 13.8 1l.)4 1)4.6 1L.815. External debt outstanding

and disbursed, end period:Total 1,785 3,552 4,319 5,100IBRD 212 317 352 465 597 701

16. IBRM service as percentageof total debt service 6.4 4.9 4.8 3.9 -.1 4.5

1/ Net of export credits; including private direct investment.

2/ Includes errors and omissions, IMF account, National Bank andcommercial bank credits.

3/ On exports (incl. MFS) nlus workers' remittances.

Ii/ Estimates.

5/ Projectitons.

July 18, 1975

ANNEX I

Page 5

SELECTED ECONOMIC DEVELOPMENT DATA

Av. Actuals ,Projections Growth Rates As % of GDY1967-69 1972 1973 1974 - 1975 1976 1965-70 1970-73 1973-76 1972 1974 1976

National Accounts(average 1967-69 prices; million US$)

GDP 10,542 13,491 14,177 15,311 16,230 17,204 4.7 5.8 6.6 99.8 102.3 101.7Gains from terms of trade 1 26 -5 -350 -380 -293 0.2 -2.3 -1.7GDY 10,543 13,517 14,172 14,961 15,850 16,911 4.7 5.8 6.1 100.0 100.0 100.0

Imports (incl. NFS) 2,116 3,074 3,455 3,913 4,196 4,440 11.5 7.5 8.7 22.7 26.2 26.3Exports (import capacity, incl.NFS) 1,918 2,755 2,941 2,726 3,069 3,398 7.7 9.4 4.9 20.4 18.2 20.1Resource gap 198 319 514 1,187 1,127 1,042 2.3 7.9 6.2

Consumption 7,628 9,763 10,259 11,285 11,962 12,680 6.2 5.6 7.3 72.2 75.4 75.0Investment (incl. stocks) 3,113 4,073 4,427 4,863 5,015 5,273 4.0 7.4 6.0 30.1 32.5 31.2

National Savings 3,013 4,350 4,672 4,297 4,512 4,829 3.0 10.9 1.1 38.2 38.7 28.6Domestic Savings 2,914 3,754 3,913 3,676 3,888 4,231 1.1 6.5 2.6 27.8 24.6 25.0

Price Indices (1967-69 = 100)Import price index 99.9 124.3 149.6 213.7 227.9 242.3 2.8 9.7 17.0Export price index 99.9 125.5 149.3 189.4 202.8 223.1 2.8 14.8 14.3Terms of trade index 100.0 101.0 99.8 88.6 89.0 92.1 0.0 0.1 -2.6

Public Finance(current prices; million US$)

Current receipts 2,951 3,421 4,139

Current expenditures 2,938 3,493 4,160Budgetary savings 13 -72 -21Public sector investment 241 276 329

1/ Estimates.

July 18, 1975

Page I

TIIE STATUS OF BANK GROUP OPERATIONS IN YUGOSLAVIA

A. STATEMENT OF BANK LOANS (as at August 31, 1975)US$ millionAmount (lesscancellations)

Number Year Borrower Purpose Bank Undisbursed

Thirteen Loans fully disbursed 326.2

531 1968 Yugoslav Investment Bank Railways 50.0 0.7657 1970 Yugoslav Investment Bank Telecommuni- 40.0 0.4

cations678 1970 SFRY Roads 40.0 1.9751 1971 SFRY Roads 35.0 4.1752 1971 Hotel "Bernardin", Piran Tourism 10.0 5.2777 1971 SFRY Multi-purpose 45.0 37.2

water782 1971 "Babin Kuk' Hotelsko

Turisticki Centar,Dubrovnik Tourism 20.0 14.5

836 1972 Twelve Electric PowerEnterprises in Yugoslavia Power 75.0 36.8

894 1973 Stopanska Banka, Skopje AgriculturalIndustries 31.0 17.9

916 1973 Naftagas Gas Pipeline 59.4 34.8947 1973 Kikinda Iron Foundry 14.5 7.4965 1974 IMT Tractor Factory 18.5 10.8966 1974 FOB Iron Foundry 15.0 12.4990 1974 Bosnia-Herzegovina Road Fund Roads 30.0 10.81012 1974 Stopanska Banka, Skopje Industrial

Credit 28.0 26.41013 1974 Privredna Banka Sarajevo Industrial

Credit 22.0 20.91026 1974 Community of Yugoslav

Railways Railways 93.0 86.71060 1974 Port of Bar Harbor Expansion 44.0 44.01066 1974 Vodovod Dubrovnik Water Supply

and Wastewater 6.0 6.01129* 1975 Vojvodjanska Banka Agricultural

Credit 50.0 50.01136* 1975 Elektroprivreda Sarajevo Power

Bosne i Hercegovine 70.0 70.01143* 1975 Republic Road Organization Roads

in Slovenia, Montenegroand Serbia 40.0 40.0Total (less cancellation) 1181.1 539.0of which has been repaid 122.3

Total now outstanding 1058.8Amount sold 7.7of which: Amount repaid 6.1 1.6

Total now held by Bank 1057.2Total undisbursed 539.0

* Not yet effective.

AiNNEX IIPage 2

B. STATEMENT OF IFC INVESTMFNTS (as at August 31, 1975)

Type of Amount in US$ millionYear Obligor Business Loan Equitv Total

1970 International Investment Corpora- Investment - 2.0 2.0tion for Yugoslavia Corporation

1970 Zavodi Crvena Zastava Fiat S.P.A. Automotive 5.0 8.0 13.0Industry

1971 Tovarna Automobilov in Motorjev Automotive 7.5 2.3 9.8Maribor (TAM) /Klockner- IndustryHumboldt Deutz A.G. (KiD)

1972 FAP-FATMOS Belgrade/Daimler Automotive 13.0 3.0 16.0Benzz A.G. Industry

1972 Sava/Semperit Tires 4.0 1.5 5.51973 Belisce/Bell Pulp and Paper 13.4 - 13.41974 Zelezarna Jesenice/ARNMCO Special Steel 10.0 - 10.01974 Salonit Anhovo Cement Plant 10.0 - 10.01975 Rudarsko Melaturski Steel 50.0 - 50.0

Total Gross Commitments 112.9 - 129.7less cancellations, terminationsrepayment and sales 54.8 2.4 57.2

Total Commitments held by IFC 58.1 14.4 _72.5

Total Undisbursed 67.8 6.3 74.1

C. PROJECTS IN EXECUTION 1/

Loan 531 Belgrade-Bar Railway: US$50.0 million Loan of March 22, 1968;Closing Date: December 31, 1975.

Tlhe completion of this project was originally scheduled for 1973but geo-technical and other construction difficulties in mountainous terrainare expected to delay operation of the line at least until 1976. The ClosingDate will be adjusted when the final completion date is known. As a resultof inflation and cost overruns, the total project cost has increased from$225.5 million to $350.0 million. Supplementary finance has been made avail-able from Yugoslav sources.

1/ These notes are designed to inform the Executive Directors regarding theprogress of projects in execution, and in particular to report anyproblems which are being encountered, and the action being taken toremedy them. They should be read in this sense, and with understandingthat they do not purport to present a balanced evaluation of strengthsand weaknesses in project execution.

ANNEX IIPage 3

Loan 657 Telecommunications: US$40.0 million Loan of February 20, 1970;Closing Date: December 31 1975

After initial delays the Bank-financed part of the project is pro-ceedirg satisfactorily and is now nearing completion. The installation oftrunk exchanges which are not financed by the Bank, has been delayed andwill be fully completed by 1976. At that time the full benefit of the proj-ect will be realized. The loan amount is likely to be fully disbursed at theclosing date. The finances of the Telecommunications Branches of the YPTTEsare sound.

Loan 678 Fourth HIighway: USS40.0 million Loan of May 28, 1970;Closing Date: December 31, 1975.

After an initial delav of about one year in starting work on theSarajevo-Zenica section because of difficulties in acquiring the right-of-wav,and delays due to inclement weather in 1974, work on this section has beenproceeding satisfactorily and it is expected to be completed by November 1975.All other road sections are open for traffic. The Closing Date has been post-poned from June 30, 1974 to December 31, 1975.

Loan 751 Fifth Highway: USS35.0 million Loan of June 18, 1971;Closing Date: September 1, 1976.

After an initial delav of about eight months in fulfilling theconditions for effectiveness of the loan, construction work on all sectionshas progressed well. All road sections but one are open for traffic. Com-pletion of the remaining section has been delayed due to lack of funds.While costs have increased, future earmarked revenues from fuel taxes, par-ticularly on purchases of fuel by Italian motorists crossing the border tobuy cheaper fuel in Yugoslavia, have decreased. The final section is nowexpected to be completed by September, 1977.

Loan 752 Bernardin Tourism: US$10.0 million Loan of June 18, 1971;Closing Date; June_30, 1976.

There have been delays in implementation. of the project due todelays in making the loan effective, appointing consultants, providing thenecessarv infrastructure and approvals by local authorities. As a resultdisbursements are behind schedule. Bids received in July 1974 indicated thatthe project, if it were to he implemented as originally envisaged (2,50() beds)would cost- approximatelv 100 percent above the originally estimated cost ofUS$25.6 mlion. This increa.se was mainly (lue to rapi(d inflatlon in constrtic-tion costs. ihe 3ank and the project sponsors have agreedI to finance a ro-ducecl complex ccntaining somc@ 1,616 beds (Amendment to Loan 752-YU, December16, 1974, R74-258). The total cost would be US$39.9 million requiring addi-tional financing of about US$14 million. Financing for the revised projecthas been agreed upon and formal commitments are expected to be entered intoin due course. Construction has begun and the execution of the port hoteland vacation village is progressing satisfactorily; however, serious construc-tion problems with regard to the foundations have been encountered in the caseof the cliff hotel, the complecion of which has been delayed for at least afurther sLx months.

A"NNEX IIPage 4

Loan 777 Ibar Multipurpose Water: US$45.0 million Loan of June 30, 1971;Closing Date: December 31, 1976.

The start of project work was delayed for one year. However, con-struction is now underway with the main dam scheduled for completion by late1976 and the irrigation networks in 1977. Project costs are currently esti-mated to be about 19 percent above the appraisal estimate. Additional fundsare being provided by the Province of Kosovo. Disbursements are proceedingin line with the revised schedule. Arrangements for land consolidation andagricultural extension services have been delayed although discussions areunderway with consultants to carry out necessary studies.

Loan 782 Babin Kuk Tour4sm: US$20.0 million Loan of July 21, 1971;Closing Date: July 31, 1976.

There have been delays in the implementation of the project due todelays in making the loan effective and in mobilizing consultants. According-ly disbursements are behind schedule. Although these problems have now beenlargely resolved, the project is almost two years behind schedule. Bids forcivil works and estimates for other components indicated that the projectwould cost at least twice as much as originally estimated (US$49.9 million).This increase is largely due to rapid inflation in construction costs. TheBank and the project sponsors have agreed to finance a reduced complex con-taining some 2,034 beds. The total cost would be US$51.5 million requiringadditional financing of about US$1.6 million. This additional financing forthe revised project has been arranged but in light of the increased financialcommitments necessary from the local banks and a re-evaluation of the finan-cial capabilities of the sponsor necessary to implement a project of this size,the local banks and the Borrower have proposed and are discussing with theBank a change in sponsorship. This proposed change in sponsorship will besubmitted to the Executive Directors for their consideration after being fullyreviewed by the Bank. Meanwhile, construction has begun and is proceedingwell with tenders for fixed and moveable equipment and furniture having beeninvited.

Loan 836 Power Transmission: US$75.0 million Loan of June 23, 1972;Closing Date: June 30, 1977.

Project execution began about one year behind schedule mainlybecause of coordination difficulties and inherent delays in reaching agree-ment among 12 borrowers. (This is the first attempt at countrywide coordina-tion In the sector). All main contracts have been awarded and constructionis proceeding satisfactorily; however, the cost of the project has increased84 percent from $225 million to $415 million chiefly due to escalation inoverall costs, including both civil works and equipment. The cost overrun isexpected to be financed from funds from the Federal Republic of Germany andthe borrowers' own resources. Action on appointment of Management consultantsto help improve planning operation and management of the inter-connected powersystem is still pending. To ensure a more even distribution of disbursementsover the construction period, the Bank as of July 1975 has been only disbursingon foreign expenditures. Early difficulties with reporting, changes in theorganization of the sector, and determination of the financial performance ofindividual borrowers have largely been resolved.

ATNNEX IIPage 5

Loan 894 Agricultural Industries (Macedonia): US$31 million Loan of May 25,1973; Closing Date: December 31, 1978.

Forty-two of the expected 43 social sector subloans, and 41 privatesector subloans (81 percent of the amount allocated) have been approved by thelending institution. Private sector demand for subloans already exceeds fi-nancing available under the project. Eight social sector sub-projects havebeen completed and twentv-nine are under construction. Progress is beingmade on the three studies encompassed by the project.

Loan 916 Naftagas Pipeline: USS59.4 million Loan of June 25, 1973;Closing Date: June 30 1977.

This loan became effective on March 22, 1974, after about fourmonths' delay. Bids received on pines and equipment exceeded appraisal es-timates and civil works costs have increased so that project costs are nowabout 93 percent above the appraisal estimate. Accordingly the project hasbeen redefined. Phase I is a reduced version of the original plan. PhaseII would provide for a pipeline extension to link up with the pipeline tobe constructed under the proposed Sarajevo Air Pollution Control Project, forwhich supplementary Bank financing will be proposed. Naftagas will obtainadditional local currency financing required for Phase I and II. Finalagreement on the revised project is expected shortly.

Loan 947 Kikinda Iron Foundry: US$14.5 million Loan of November 30, 1973;Closing Date: March 31, 1978.

This loan was declared effective on Mav 28, 1974 after four monthsdelay, which was primarily due to the extra time required for the ratificationof the Guarantee Agreement bv the Federal Assembly. Project implementationis about four months ahead of schedule. Total project costs now are about13 percent (Din. 79.0 million, about US$4.6 million equivalent) above appraisalestimates due to large increases in local costs. Financing of this cost over-run has been arranged with a local bank.

Loan 966 FOB Iron Foundry: US$15.0 million Loan of February 22, 1974;Closing Date: December 31, 1977.

This loan became effective on May 28, 1974. Project implementationis proceeding on schedule. Local costs are about 50 percent (Din. 173 million,about US$10.0 million equivalent) above appraisal estimates due to designchanges and domestic inflation. Financing of this local cost overrun has beenarranged with a local bank.

Loan 965 IMIT Tractor Factor Expansion: US$18.5 million Loan of February 22,1974; Closing Date: December 31 1 977.

This loan became effective on June 11, 1974. Project irmplementationis proceeding satisfactorily and disbursements are underway. Due to delays

ANN EX I-LPage 6

in obtaining import permits, the project is now expected to be completed twomonths behind schedule. Local costs are about 7 percent (Din. 97 million,about US$5.6 million equivalent) above appraisal estimates due to domesticinflation. Financing of this local cost overrun has been arranged with alocal bank.

Loan 990 Sixth Highway: USS30.0 million Loan of Mav 31, 1974;Closing Date: December 31, 1977.

This loan was declared effective on December 10, 1974. Two out ofsix road sections are nearly complete and work on other sections has progressedconsiderably. One of the road sections is being executed on an alignmentdifferent from that agreed with the Bank and the borrower has submitted arequest for inclusion of the alignment in the project. This request is beingreviewed.