retail research talbros automotive components limited

TRANSCRIPT

RETAIL RESEARCH Stock Note 18 Sep 2017

Talbros Automotive Components Limited

RETAIL RESEARCH P a g e | 1

Industry CMP Recommendation Add on dips to Sequential Targets Time Horizon

Auto Parts & Equipment Rs. 197.50 Buy at CMP and add on declines Rs.179 - 183 Rs.234.5 & Rs.264 2-3 quarters

Company Description: Talbros Automotive Components Ltd (TACL) is the flagship manufacturing company of the Talbros group established in 1956 as a gasket supplier. Promoted by Talwar Family in 1956, the company supplies to OEMs across 2Ws, 3Ws, PVs, CVs and Farm Equipments. The product portfolio for the company along with its 3 JVs include gaskets, forgings, suspension systems, anti-vibration products & hoses. TACL has three JVs - Nippon Leakless – producing automotive gasket, Magneti Marelli - producing suspension system and Marugo Rubber Industries - producing anti vibration parts. It is a market leader in gaskets with a 38% market share. TACL has a diversified clientele spread across OEMs, exports and after market and its top 5 clients account for 40% of its revenue.

Investment Rationale:

New products like heat shields and post coated gaskets under technical collaborations to boost company’s revenue growth.

Large export orders and company’s attempt to foray in the foreign OEM market of gaskets increases visibility.

Strategic measures like transfer of materials business & reducing employee count will lead to cost efficiencies.

GST to help company increase its aftermarket business and help it improve its working capital position.

Hedged business profile, strong clientele and business partnerships with strong JV partners have helped the company stay in green over years.

Concerns:

Adverse fluctuation in RM prices may impact company’s margins.

High current utilization levels requires capex to be incurred by the company to grow further.

With increase in OEM business share, company may face stretched working capital.

Slowdown in the user auto industry could affect growth prospects.

Rising popularity of Electric cars may impact company’s business.

View and Valuation: TACL is the leader in the domestic gaskets market (38%) and has been in this business for 7 decades. It has set up three JVs with world leaders, all of which support the auto sector. With its business catering to the auto sector, TACL is expected to grow with the growing auto sector in the forthcoming fiscals. TACL has entered into technical collaborations with foreign players from Japan and USA to increase its product portfolio without cannibalization and also has adopted a number of cost reduction measures which are expected to help company not only increase its revenues but also expand its margin profile. With strong clientele in the OEM market and increasing share in the aftermarket due to introduction of GST, company’s core standalone business is set to grow in the near future. With increased revenue prospects and better margin profile, company is expected to increase its profit at a CAGR of ~23.9% over next two years which would help it attain better valuations going forward.

HDFC Scrip Code TALAUTEQNR

BSE Code 505160

NSE Code TALBROAUTO

Bloomberg TALB IN

CMP Rs.197.50

Equity Capital (Rs crs) 12.4

Face Value (Rs) 10.0

Equity Share O/S (crs) 1.24

Market Cap (Rs crs) 243.9

Book Value (Rs) 27.4

Avg. 52 Wk Volumes 13951

52 Week High 226.0

52 Week Low 116.2

Shareholding Pattern % (Jun 30, 2017)

Promoters 56.6

Institutions 2.4

Non Institutions 41.0

Total 100.0

Fundamental Research Analyst CA Arpit Bhatt [email protected]

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 2

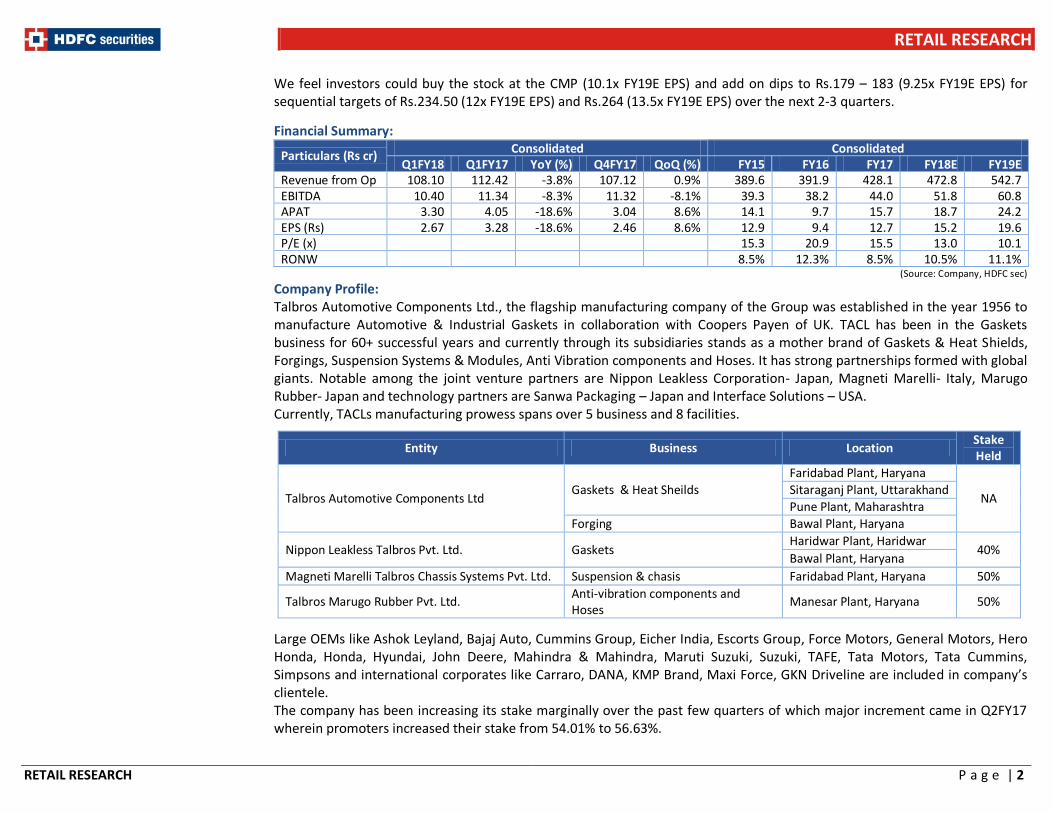

We feel investors could buy the stock at the CMP (10.1x FY19E EPS) and add on dips to Rs.179 – 183 (9.25x FY19E EPS) for sequential targets of Rs.234.50 (12x FY19E EPS) and Rs.264 (13.5x FY19E EPS) over the next 2-3 quarters.

Financial Summary:

Particulars (Rs cr) Consolidated Consolidated

Q1FY18 Q1FY17 YoY (%) Q4FY17 QoQ (%) FY15 FY16 FY17 FY18E FY19E Revenue from Op 108.10 112.42 -3.8% 107.12 0.9% 389.6 391.9 428.1 472.8 542.7 EBITDA 10.40 11.34 -8.3% 11.32 -8.1% 39.3 38.2 44.0 51.8 60.8 APAT 3.30 4.05 -18.6% 3.04 8.6% 14.1 9.7 15.7 18.7 24.2 EPS (Rs) 2.67 3.28 -18.6% 2.46 8.6% 12.9 9.4 12.7 15.2 19.6 P/E (x) 15.3 20.9 15.5 13.0 10.1 RONW 8.5% 12.3% 8.5% 10.5% 11.1%

(Source: Company, HDFC sec) Company Profile: Talbros Automotive Components Ltd., the flagship manufacturing company of the Group was established in the year 1956 to manufacture Automotive & Industrial Gaskets in collaboration with Coopers Payen of UK. TACL has been in the Gaskets business for 60+ successful years and currently through its subsidiaries stands as a mother brand of Gaskets & Heat Shields, Forgings, Suspension Systems & Modules, Anti Vibration components and Hoses. It has strong partnerships formed with global giants. Notable among the joint venture partners are Nippon Leakless Corporation- Japan, Magneti Marelli- Italy, Marugo Rubber- Japan and technology partners are Sanwa Packaging – Japan and Interface Solutions – USA. Currently, TACLs manufacturing prowess spans over 5 business and 8 facilities.

Entity Business Location Stake Held

Talbros Automotive Components Ltd Gaskets & Heat Sheilds

Faridabad Plant, Haryana

NA Sitaraganj Plant, Uttarakhand

Pune Plant, Maharashtra

Forging Bawal Plant, Haryana

Nippon Leakless Talbros Pvt. Ltd. Gaskets Haridwar Plant, Haridwar

40% Bawal Plant, Haryana

Magneti Marelli Talbros Chassis Systems Pvt. Ltd. Suspension & chasis Faridabad Plant, Haryana 50%

Talbros Marugo Rubber Pvt. Ltd. Anti-vibration components and Hoses

Manesar Plant, Haryana 50%

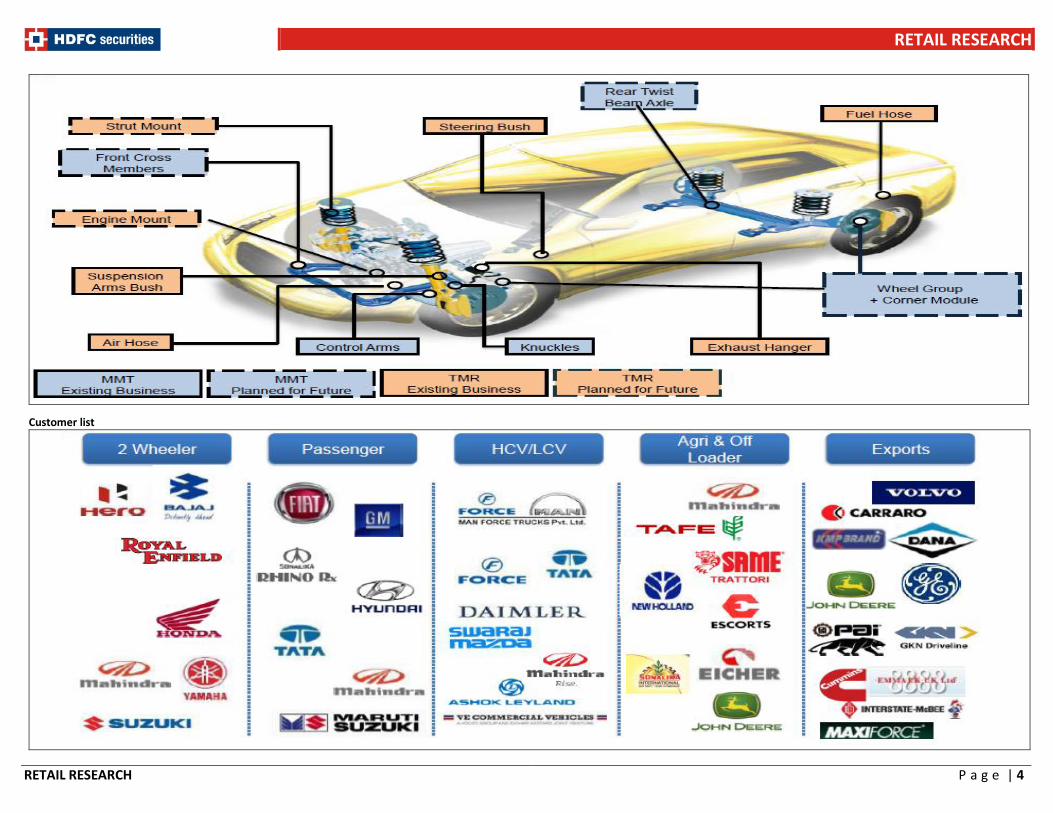

Large OEMs like Ashok Leyland, Bajaj Auto, Cummins Group, Eicher India, Escorts Group, Force Motors, General Motors, Hero Honda, Honda, Hyundai, John Deere, Mahindra & Mahindra, Maruti Suzuki, Suzuki, TAFE, Tata Motors, Tata Cummins, Simpsons and international corporates like Carraro, DANA, KMP Brand, Maxi Force, GKN Driveline are included in company’s clientele. The company has been increasing its stake marginally over the past few quarters of which major increment came in Q2FY17 wherein promoters increased their stake from 54.01% to 56.63%.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 3

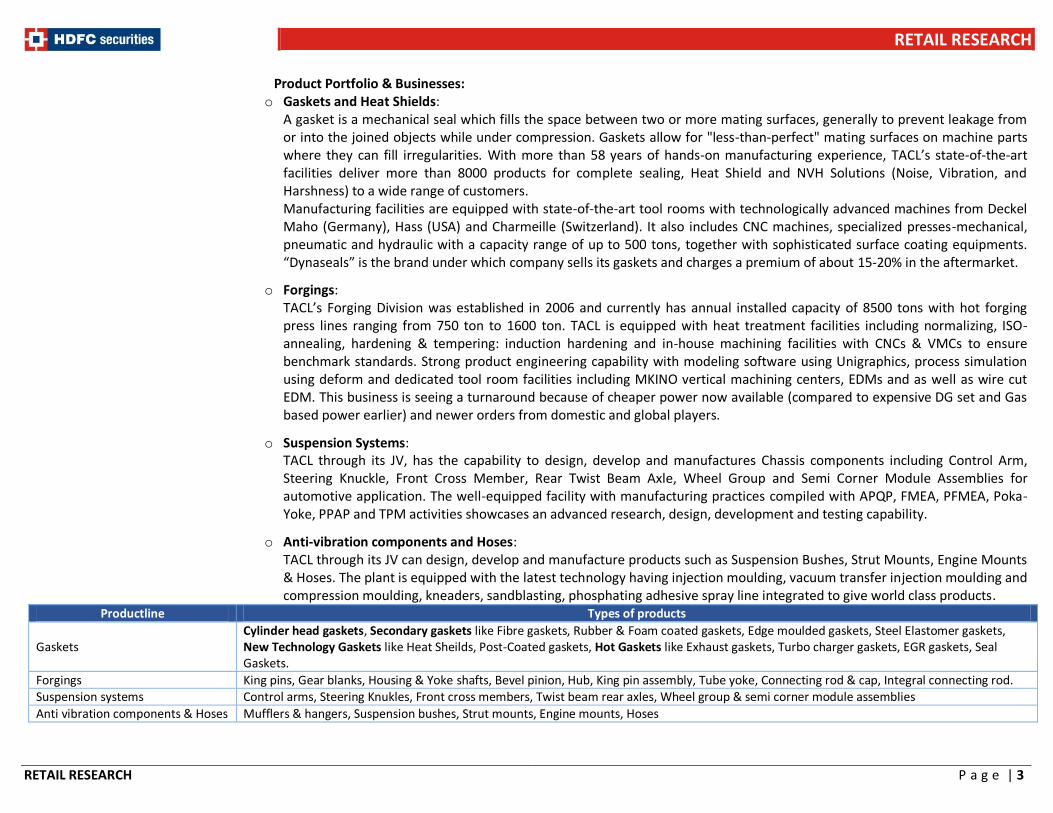

Product Portfolio & Businesses: o Gaskets and Heat Shields:

A gasket is a mechanical seal which fills the space between two or more mating surfaces, generally to prevent leakage from or into the joined objects while under compression. Gaskets allow for "less-than-perfect" mating surfaces on machine parts where they can fill irregularities. With more than 58 years of hands-on manufacturing experience, TACL’s state-of-the-art facilities deliver more than 8000 products for complete sealing, Heat Shield and NVH Solutions (Noise, Vibration, and Harshness) to a wide range of customers. Manufacturing facilities are equipped with state-of-the-art tool rooms with technologically advanced machines from Deckel Maho (Germany), Hass (USA) and Charmeille (Switzerland). It also includes CNC machines, specialized presses-mechanical, pneumatic and hydraulic with a capacity range of up to 500 tons, together with sophisticated surface coating equipments. “Dynaseals” is the brand under which company sells its gaskets and charges a premium of about 15-20% in the aftermarket.

o Forgings: TACL’s Forging Division was established in 2006 and currently has annual installed capacity of 8500 tons with hot forging press lines ranging from 750 ton to 1600 ton. TACL is equipped with heat treatment facilities including normalizing, ISO-annealing, hardening & tempering: induction hardening and in-house machining facilities with CNCs & VMCs to ensure benchmark standards. Strong product engineering capability with modeling software using Unigraphics, process simulation using deform and dedicated tool room facilities including MKINO vertical machining centers, EDMs and as well as wire cut EDM. This business is seeing a turnaround because of cheaper power now available (compared to expensive DG set and Gas based power earlier) and newer orders from domestic and global players.

o Suspension Systems: TACL through its JV, has the capability to design, develop and manufactures Chassis components including Control Arm, Steering Knuckle, Front Cross Member, Rear Twist Beam Axle, Wheel Group and Semi Corner Module Assemblies for automotive application. The well-equipped facility with manufacturing practices compiled with APQP, FMEA, PFMEA, Poka-Yoke, PPAP and TPM activities showcases an advanced research, design, development and testing capability.

o Anti-vibration components and Hoses: TACL through its JV can design, develop and manufacture products such as Suspension Bushes, Strut Mounts, Engine Mounts & Hoses. The plant is equipped with the latest technology having injection moulding, vacuum transfer injection moulding and compression moulding, kneaders, sandblasting, phosphating adhesive spray line integrated to give world class products.

Productline Types of products

Gaskets Cylinder head gaskets, Secondary gaskets like Fibre gaskets, Rubber & Foam coated gaskets, Edge moulded gaskets, Steel Elastomer gaskets, New Technology Gaskets like Heat Sheilds, Post-Coated gaskets, Hot Gaskets like Exhaust gaskets, Turbo charger gaskets, EGR gaskets, Seal Gaskets.

Forgings King pins, Gear blanks, Housing & Yoke shafts, Bevel pinion, Hub, King pin assembly, Tube yoke, Connecting rod & cap, Integral connecting rod. Suspension systems Control arms, Steering Knukles, Front cross members, Twist beam rear axles, Wheel group & semi corner module assemblies

Anti vibration components & Hoses Mufflers & hangers, Suspension bushes, Strut mounts, Engine mounts, Hoses

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 4

Customer list

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 5

Joint Ventures: Apart from its standalone business, company has entered into joint ventures with 3 internationally renowned corporate entities to foray in similar business lines in India in which said companies have excelled globally. The said JVs include:

o Nippon Leakless Talbros Pvt. Ltd. - Nippon Leakless Talbros Private Limited (NLTL) a joint venture company between Nippon Leakless Corporation (NLK) Japan and Talbros Automotive Components Ltd. (TACL) India – was established in the year 2005 to manufacture Gaskets for passenger cars, motorcycles, scooters, power equipment products and industrial applications. NLK group supplies gaskets to leading OE vehicle and motorcycle manufacturers such as Honda, Suzuki and Yamaha Worldwide. This JV was initially set up to meet the requirements of Honda. The JV has State–of-the-art facilities to manufacture diversified range of Cylinder Head Gaskets in composite, Multi Layered Steel (MLS), Single Layered Steel (SLS), and Secondary Gaskets made from metallic and nonmetallic jointing sheet materials. NLTPL has strong research & development support from Nippon Leakless, Japan and TACL, India not only for product design, but also for engine testing with computerized engine test bed and deep thermal shock testing facility. The plant is equipped with in-house tool room with modern manufacturing equipment having high level of automation. Nippon Leakless Talbros can design, develop and manufacture products as per customer requirements competitively. In FY17 said JV contributed roughly 16% of consolidated revenue of the company at Rs.71 Crs (TACL’s share of JV revenues). It earns a very high margin on account of its close relations with various OEMs.

o Magneti Marelli Talbros Chassis Systems Pvt. Ltd. - Magneti Marelli Talbros Chassis Systems Pvt. Ltd. (MMT) is a joint venture between Sistemi Sospensioni S.p.A., Italy and Talbros Automotive Components Limited, India (TACL). The Joint Venture can design, develop and manufacture Chassis components including Control Arm, Steering Knuckle, Front Cross Member, Rear Twist Beam Axle, Wheel Group and Semi Corner Module Assemblies for automotive applications. Magneti Marelli has high prowess in design, technology and know-how for full spectrum of suspension components and modules thereby bringing in the most advanced light-weight solutions for the Indian automobile industry. The well-equipped facility with manufacturing practices is in line with World Class Manufacturing processes. In addition it has state-of-the-art in-house tool room with sophisticated machines, like mechanical presses ranging from 30 tons to 400 tons, automatic feeders, robotic welding with turn table and 5-Axis Multi Spindle machine facility for single set up machining of Steering Knuckles. Maruti Suzuki is the dominant customer for this JV wherein company supplies the auto components to the new class of cars introduced by Maruti in the market including Vitara Brezza, Baleno etc. Company has recently procured an order from JLR. This JV contributed approx. 10% of company’s consolidated revenues at Rs.43 Crs (TACL’s share) in FY17.

o Talbros Marugo Rubber Pvt. Ltd. - Talbros Maurgo Rubber Pvt. Ltd (MRT) is a joint venture company between Marugo Rubber Industries, Japan and Talbros, set up in 2012. Marugo Rubber Industries, is a leading OEM supplier of Anti Vibration products and Hoses to worldwide OEMs like Mitsubishi, Fuso (Daimler), Suzuki, Isuzu, Daihatsu, Hino, Subaru, Kawasaki, Nissan & UD Trucks (Volvo). The new JV Company can design, develop and manufacture products such as Suspension Bushes, Strut Mounts, and Engine Mounts & Hoses. MRT is equipped with the latest technology having injection moulding, vacuum transfer injection moulding and compression moulding, kneaders, sandblasting, phosphating adhesive spray line integrated to give world class products. MRT is comparatively smaller in scale in comparison with other

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 6

JVs of company and it contributed roughly 3.5% of consolidated turnover at Rs.15.4 Crs in FY17 (TACL’s share). High rubber prices and revision of wages in Haryana have led to subdued profitability.

(Source: Company, HDFC sec – FY17 numbers)

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 7

Business Development over the years:

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 8

Q1FY18 Result Update: In Q1FY18, company has on a consolidated basis witnessed degrowth in revenues of 3.8% QoQ and a growth of 0.9% YoY. The EBITDA margins have contracted during the quarter falling to 9.6% witnessing a contraction of 50/100 bps QoQ/YoY. However, on PAT margin front, company has experienced an expansion on a YoY basis with the PAT margin settling at 3.1% for the quarter. Results of this quarter were impacted majorly due to the destocking of goods carried out all across the industry majorly impacting the aftermarket sales in the Gaskets business. However, company’s OEM sales of gaskets remained stable and it experienced good growth YoY in its other 4 major business lines which include the Forgings on standalone basis and 3 JVs. With the aftermarket sales being impacted, company witnessed a contraction in the margins as the aftermarket sales fetch higher margins. The company has stated that of the sales lost due to the negative impact of GST, 80% would be recovered over the remaining portion of FY18. Further, company has intimated about its vision to achieve turnover of close to Rs. 700 Crs and generate EBITDA and PAT margins of 14% and 5% respectively by effectively earning a ROCE of >20% over next 3 years (vs sales of Rs.428 cr , EBITDA and PAT margins of 10.3% and 3.7% and RoCE of 14.4% in FY17).

Investment Rationale: Technical collaborations enabling company to bring in newer products and assure revenue growth: TACL has recently entered into technical collaboration with Sanwa Packing from Japan, a company which has been engaged in the business of gaskets since 1945 i.e. more than 7 decades. Further, company has also entered into a technical collaboration with Interface, USA. Through these technical knowhow flows into the company, the company is developing newer products to tap new markets.

TACL has developed a product called Heat shields which is expected to gain traction with the stricter emission norms coming in. With the requirement of BS VI norms, entire auto industry would require this product to meet the new requirements. Heat shields are said to have overall domestic market size of about Rs.~125 - 150 Crs and the company intends to sell and capture about 18-20% of said market in a span of 3 years. Management of the company is confident to increase its revenues from this product by Rs.25 Crs by end of FY20. More importantly this product is not a replacement of gaskets and hence does not entail any cannibalization impact on company’s existing sales.

TACL has also developed another product called post coated gaskets which is well received by the OEMs. TACL’s management guided that they will start marketing this new product from October 2017 and expect an additional revenues of Rs.5-6 Crs in FY18 itself. Thus with these new products to offer, the revenues of the company are expected to post steady growth.

Large orders and Foreign OEM market attempt to help company’s standalone business: TACL is already a supplier of gaskets to a rich customer base including names like Ashok Leyland, Bajaj Auto, Cummins Group, Eicher, Escorts Group, Force Motors, General Motors, Hero Honda, Honda, Hyundai, John Deere, Mahindra & Mahindra, Maruti Suzuki, Suzuki, TAFE, Tata Motors, Tata Cummins, Simpsons and international corporates like Carraro, DANA, KMP Brand, Maxi Force and GKN Driveline. TACL is now attempting to increase its presence in the OEMs business outside of India. This will help it generate long term high value contracts and increase its exports exponentially. Company has on account of said efforts won an order of Rs.175 Crs

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 9

from BMW in the forgings business over a period of 7 years the shipment for which is to start from September 2017 accruing an incremental income of Rs.2 Cr per month. TACL has also received another order from Jaguar Land Rover in the MMT business which is expected to increase the revenue from this segment to the tune of 14% of FY17 revenues and double this amount in FY19. On the back of these orders, company will not only grow its revenues but also increase its visibility in foreign markets which may open an opportunity for it to serve in the aftermarket. These attempts by the company to look beyond India as a market is seen as a proactive measure which may yield good results in the years to come due to higher utilizations of its capacities in India.

Strategic cost reduction measures to help company expand its margins: Company has thoroughly studied the costs it incurs and where a cut can be implemented for better margin ratios. TACL has realized that one of the major components in its cost structure is the employee costs which is about ~13.2% which it intends to bring down to 12.5% over the next few years. This it shall achieve by not replacing the excess labor retiring each year. This would add to the EBITDA numbers for the company.

Further, company has recently sold an underutilized non-core materials business assets to Indian affiliate of Interface Performance Materials, USA. This would help company bring down its cost in two ways. First being the savings in the fixed costs attached to the non-core materials business assets. Second would be from the materials sourcing agreement it has signed with the buyer of said materials business assets. TACL will also save on the costs due to lower working capital requirements and also due to lesser forex exposure. This sale is itself expected to benefit company to the extent of Rs.0.7 to 1 Crs annually. These reduction of costs in the standalone business will help it achieve better margins going forward.

GST to be advantageous for organized player: A large number of unorganized players vie for revenues in the aftermarket of various products offered by the company along with its JVs. However, with the advent of GST the cost efficiencies to be experienced by the organized players would help them price their products better as compared to the unorganized players in the industry. This may help a company like TACL to increase its revenue share at the cost of sales lost by the unorganized players. The management has said that initially it has not achieved the kind of growth it expected in the aftermarket due the stock clearance spree prior to implementation of GST. However, going forward company expects annual growth of 18% from its aftermarket business. Further, company said that due to the availability of input credit, it shall be able to improve its working capital situation. Hence, GST is a positive change for the company and the company is ready to grab this opportunity to its advantage.

Hedged business with positively contributing JVs to help company maximize shareholder wealth: TACL’s started its operations 5 decades ago entering into the Gaskets market. Today, however, company has managed to diversify its business resulting in low level operational/concentration risk. Company has forayed and stabilized in newer businesses with help of partnerships with globally recognized players like Magneti Marelli, Marugo Rubber and Nippon Leakless. The JVs entered by company have already reached levels where it generates sales not only to reach breakeven but also to generate profits for the company. Also, company has been able to attract some big names in the auto industry, as their OEM customers. Some of the customers to whose needs company caters to include the following, Ashok Leyland, Bajaj Auto, Cummins Group, Eicher India, Escorts

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 10

Group, Force Motors, General Motors, Hero Honda, Honda, Hyundai, John Deere, Mahindra & Mahindra, Maruti Suzuki, Suzuki, TAFE, Tata Motors, Tata Cummins, Simpsons and international corporates like Carraro, DANA, KMP Brand, Maxi Force & GKN Driveline. Due to such strong clientele, their repeat orders, growing businesses of the JVs that company has, company has been able to stay in the green over previous 8 fiscals. Same level of low operational risk is expected to continue for the company.

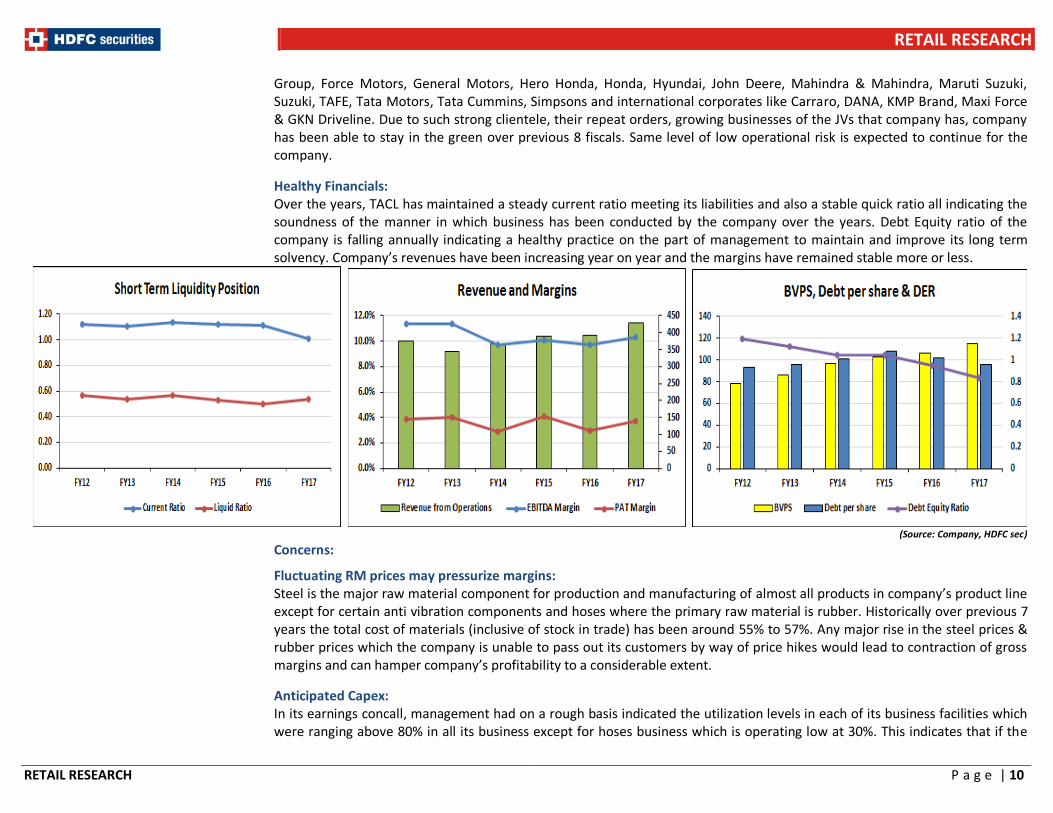

Healthy Financials: Over the years, TACL has maintained a steady current ratio meeting its liabilities and also a stable quick ratio all indicating the soundness of the manner in which business has been conducted by the company over the years. Debt Equity ratio of the company is falling annually indicating a healthy practice on the part of management to maintain and improve its long term solvency. Company’s revenues have been increasing year on year and the margins have remained stable more or less.

(Source: Company, HDFC sec)

Concerns:

Fluctuating RM prices may pressurize margins: Steel is the major raw material component for production and manufacturing of almost all products in company’s product line except for certain anti vibration components and hoses where the primary raw material is rubber. Historically over previous 7 years the total cost of materials (inclusive of stock in trade) has been around 55% to 57%. Any major rise in the steel prices & rubber prices which the company is unable to pass out its customers by way of price hikes would lead to contraction of gross margins and can hamper company’s profitability to a considerable extent.

Anticipated Capex: In its earnings concall, management had on a rough basis indicated the utilization levels in each of its business facilities which were ranging above 80% in all its business except for hoses business which is operating low at 30%. This indicates that if the

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 11

company is desirous to attain higher growth levels and scale of operations, it will be required to incur capex. This may entail higher depreciation and finance cost if the funds are not used from internal accruals.

Stretched Working Capital Cycle: TACL already faces the problem of stretched working capital cycle which may worsen if the company is able to expand its clientele by adding more OEMs from the foreign markets. Currently company’s operating cycle is as long as 172 days and cash conversion cycle of 74 days. With increasing working capital requirements company’s short term borrowings goes up and consequently the finance cost also would rise.

Economic Slowdown: Economic slowdown, though not very likely, but may bring down the level of activity in the automotive sector and the industrial and construction industry. In this case, since company majorly derives its income from a demand in these segments, the company’s sales may be negatively impacted.

Electric Cars – a potent threat to current business: Advent and popularity of electric cars may and the impact of same on the auto sector requiring shift from conventional engines to electric cars may dramatically bring down company’s level of operations. The company believes that it shall foray in non-automotive segment by then in such a manner that the electric car popularity would have negligible impact on its revenues. View and Valuation: TACL is the leader in the domestic gaskets market (38%) and has been in this business for 7 decades. It has set up three JVs with world leaders, all of which support the auto sector. With its business catering to the auto sector, TACL is expected to grow with the growing auto sector in the forthcoming fiscals.

TACL has entered into technical collaborations with foreign players from Japan and USA to increase its product portfolio without cannibalization and also has adopted a number of cost reduction measures which are expected to help company not only increase its revenues but also expand its margin profile.

With strong clientele in the OEM market and increasing share in the aftermarket due to introduction of GST, company’s core standalone business is set to grow in the near future. With increased revenue prospects and better margin profile, company is expected to increase its profit at a CAGR of ~23.9% over next two years which would help it attain better valuations going forward.

We feel investors could buy the stock at the CMP (10.1x FY19E EPS) and add on dips to Rs.179 – 183 (9.25x FY19E EPS) for sequential targets of Rs.234.50 (12x FY19E EPS) and Rs.264 (13.5x FY19E EPS) over the next 2-3 quarters.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 12

Quarterly Financials (Consolidated) - Rs in Cr Q1FY18 Q1FY17 YoY (%) Q4FY17 QoQ (%) FY17 FY16 YoY (%)

Total Income from Operation 108.1 112.4 3.8% 107.1 0.9% 428.1 391.9 9.3%

COGS 60.0 65.3 0.0% 60.8 1.4% 242.7 218.5 0.0%

Employee Expenses 15.0 13.5 10.9% 14.3 4.9% 56.2 51.6 8.8%

Other Expenses 22.7 22.2 2.2% 20.7 9.8% 85.3 83.6 2.0%

Total Expenditure 97.7 101.1 3.3% 95.8 2.0% 384.1 353.7 8.6%

EBITDA 10.4 11.3 8.3% 11.3 8.1% 44.0 38.2 15.3%

Depreciation 4.1 4.0 3.3% 3.9 4.6% 15.3 10.4 47.2%

EBIT 6.3 7.4 14.5% 7.4 14.9% 28.7 27.8 3.4%

Interest 3.5 4.2 16.3% 4.4 20.5% 16.7 17.7 5.8%

Other Income 2.0 2.9 31.3% 1.3 50.4% 8.6 6.0 42.6%

Profit before Tax 4.8 6.1 21.3% 4.3 10.9% 20.7 16.1 28.2%

Tax Expenses 1.5 2.1 26.8% 1.3 16.3% 4.9 4.5 10.3%

Reported Profit After Tax 3.3 4.1 18.6% 3.0 8.6% 15.7 11.7 35.1%

EPS 2.67 3.28 18.6% 2.46 8.6% 12.75 9.44 35.1%

Financials (Consolidated) - Profit & Loss – Cash Flow Statement –

Particulars, Rs in Cr FY15 FY16 FY17 FY18E FY19E

Particulars, Rs in Cr FY15 FY16 FY17 FY18E FY19E Revenue from Operations 389.6 391.9 428.1 472.8 542.7

EBT 21.1 16.1 20.7 26.0 33.6

Cost of Materials Consumed 214.7 220.3 233.8 256.1 292.7

Depreciation and Amortization 10.0 10.4 15.3 17.5 18.6 Stock Adjustment -14.2 -10.4 1.7 1.9 2.2

Interest /Dividend paid 18.7 17.7 16.7 15.5 15.7

Purchase of finished goods 18.2 8.5 7.2 7.9 9.0

Other Adjustment -2.5 -2.1 -2.8 -2.2 -3.9 Employee Benefits Expense 48.0 51.6 56.2 61.9 67.8

(Inc)/Dec in working Capital -8.7 -3.9 31.1 -5.4 -14.3

Other Expenses 83.6 83.6 85.3 93.1 110.2

Tax Paid -5.6 -4.8 -4.9 -7.3 -9.4 Total Expenses 350.3 353.7 384.1 421.0 481.9

CF from Operating Activities 33.0 33.3 76.0 44.2 40.3

EBITDA 39.3 38.2 44.0 51.8 60.8

Capital expenditure -16.7 -8.8 -35.0 -18.4 -28.4 Depreciation 10.0 10.4 15.3 17.5 18.6

Proceeds from sale of fixed assets 0.6 1.3 1.7 4.0 1.3

EBIT 29.3 27.8 28.7 34.2 42.1

(Purchase)/Sale of Investment -1.5 -1.5 -3.2 -1.5 -1.8 Interest 18.7 17.7 16.7 15.5 15.7

Others 3.4 2.0 2.3 2.9 3.2

Other Income 10.4 6.0 8.6 7.3 7.1

CF from Investing Activities -14.2 -7.1 -34.2 -13.0 -25.7 Profit before Tax 21.1 16.1 20.7 26.0 33.6

Inc/(Dec) in Share capital 0.0 0.0 0.0 0.0 0.0

Tax Expenses 5.1 4.5 4.9 7.3 9.4

Inc/(Dec) in Debt 8.4 -7.2 -10.6 -8.0 10.4 PAT 16.0 11.7 15.7 18.7 24.2

Dividend and Interest Paid -25.2 -21.1 -18.5 -17.7 -18.2

EPS 12.9 9.4 12.7 15.2 19.6

Others -2.9 2.5 -4.3 -2.7 -4.4

CF from Financing Activities -19.7 -25.8 -33.4 -28.4 -12.2

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 13

Net Cash Flow -0.8 0.5 8.4 2.7 2.4

Opening Balance 4.4 3.6 4.1 12.5 15.2

Closing Balance 3.6 4.1 12.5 15.2 17.6

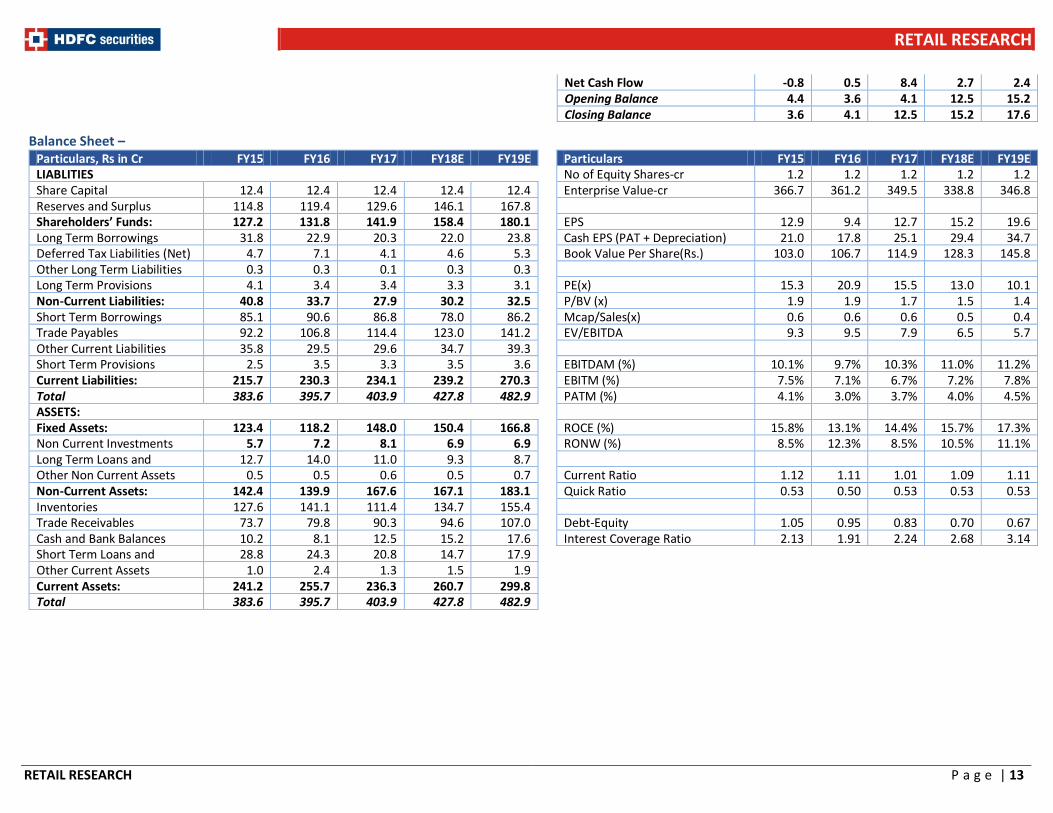

Balance Sheet – Particulars, Rs in Cr FY15 FY16 FY17 FY18E FY19E

Particulars FY15 FY16 FY17 FY18E FY19E

LIABLITIES

No of Equity Shares-cr 1.2 1.2 1.2 1.2 1.2 Share Capital 12.4 12.4 12.4 12.4 12.4

Enterprise Value-cr 366.7 361.2 349.5 338.8 346.8

Reserves and Surplus 114.8 119.4 129.6 146.1 167.8

Shareholders’ Funds: 127.2 131.8 141.9 158.4 180.1

EPS 12.9 9.4 12.7 15.2 19.6

Long Term Borrowings 31.8 22.9 20.3 22.0 23.8

Cash EPS (PAT + Depreciation) 21.0 17.8 25.1 29.4 34.7 Deferred Tax Liabilities (Net) 4.7 7.1 4.1 4.6 5.3

Book Value Per Share(Rs.) 103.0 106.7 114.9 128.3 145.8

Other Long Term Liabilities 0.3 0.3 0.1 0.3 0.3

Long Term Provisions 4.1 3.4 3.4 3.3 3.1

PE(x) 15.3 20.9 15.5 13.0 10.1

Non-Current Liabilities: 40.8 33.7 27.9 30.2 32.5

P/BV (x) 1.9 1.9 1.7 1.5 1.4 Short Term Borrowings 85.1 90.6 86.8 78.0 86.2

Mcap/Sales(x) 0.6 0.6 0.6 0.5 0.4

Trade Payables 92.2 106.8 114.4 123.0 141.2

EV/EBITDA 9.3 9.5 7.9 6.5 5.7 Other Current Liabilities 35.8 29.5 29.6 34.7 39.3

Short Term Provisions 2.5 3.5 3.3 3.5 3.6

EBITDAM (%) 10.1% 9.7% 10.3% 11.0% 11.2% Current Liabilities: 215.7 230.3 234.1 239.2 270.3

EBITM (%) 7.5% 7.1% 6.7% 7.2% 7.8%

Total 383.6 395.7 403.9 427.8 482.9

PATM (%) 4.1% 3.0% 3.7% 4.0% 4.5% ASSETS:

Fixed Assets: 123.4 118.2 148.0 150.4 166.8

ROCE (%) 15.8% 13.1% 14.4% 15.7% 17.3% Non Current Investments 5.7 7.2 8.1 6.9 6.9

RONW (%) 8.5% 12.3% 8.5% 10.5% 11.1%

Long Term Loans and Advances

12.7 14.0 11.0 9.3 8.7

Other Non Current Assets 0.5 0.5 0.6 0.5 0.7

Current Ratio 1.12 1.11 1.01 1.09 1.11

Non-Current Assets: 142.4 139.9 167.6 167.1 183.1

Quick Ratio 0.53 0.50 0.53 0.53 0.53 Inventories 127.6 141.1 111.4 134.7 155.4

Trade Receivables 73.7 79.8 90.3 94.6 107.0

Debt-Equity 1.05 0.95 0.83 0.70 0.67 Cash and Bank Balances 10.2 8.1 12.5 15.2 17.6

Interest Coverage Ratio 2.13 1.91 2.24 2.68 3.14

Short Term Loans and Advances

28.8 24.3 20.8 14.7 17.9 Other Current Assets 1.0 2.4 1.3 1.5 1.9 Current Assets: 241.2 255.7 236.3 260.7 299.8 Total 383.6 395.7 403.9 427.8 482.9

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 14

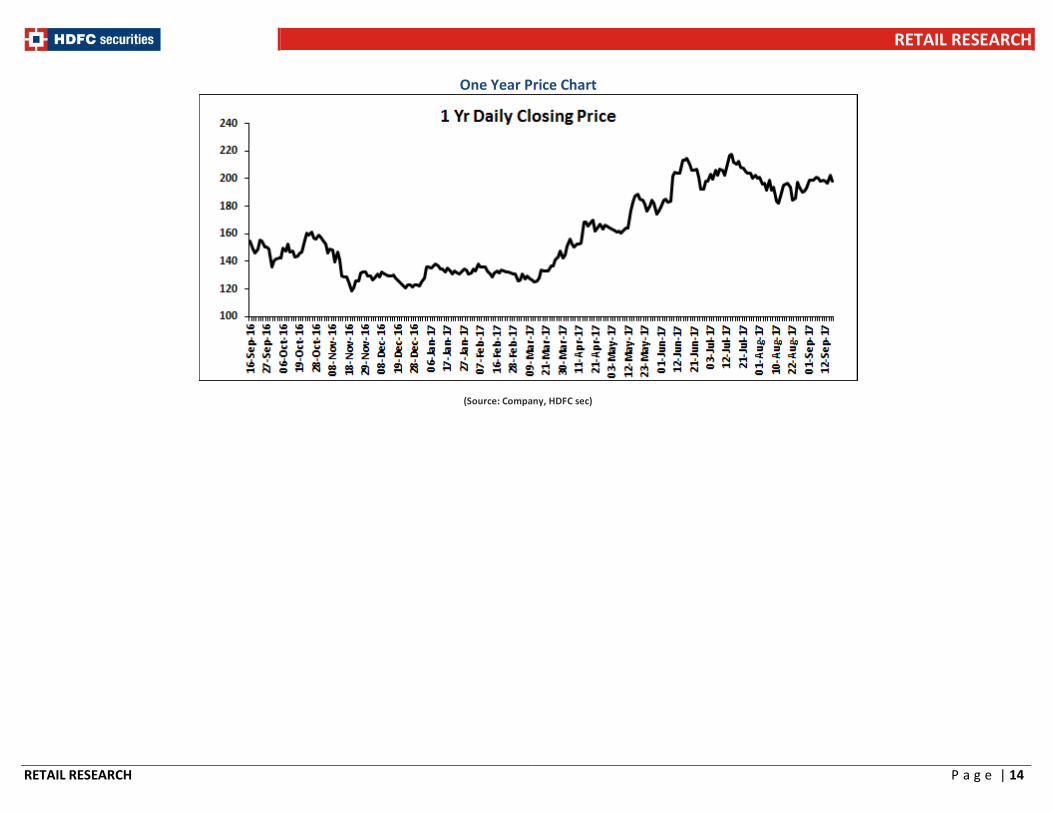

One Year Price Chart

(Source: Company, HDFC sec)

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 15

Fundamental Research Analyst: CA Arpit Bhatt ([email protected])

HDFC securities Limited, I Think Techno Campus, Building - B, "Alpha", Office Floor 8, Near Kanjurmarg Station, Opp. Crompton Greaves, Kanjurmarg (East), Mumbai 400 042 Phone: (022) 3075 3400 Fax: (022) 2496 5066Website: www.hdfcsec.com Email: [email protected].

Compliance Officer: Binkle R. Oza Email: [email protected] Phone: (022) 3045 3600 __________________________________________________________________________________________________________________________________________________________________________________________ Disclosure: I, (Arpit Bhatt, CA), authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. HSL has no material adverse disciplinary history as on the date of publication of this report. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. Research Analyst or his/her relative or HDFC Securities Ltd. does not have any financial interest in the subject company. Also Research Analyst or his relative or HDFC Securities Ltd. or its Associate does not have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Research Report. Further Research Analyst or his relative or HDFC Securities Ltd. or its associate does not have any material conflict of interest. Any holding in stock – No HDFC Securities Limited (HSL) is a SEBI Registered Research Analyst having registration no. INH000002475. Disclaimer: This report has been prepared by HDFC Securities Ltd and is meant for sole use by the recipient and not for circulation. The information and opinions contained herein have been compiled or arrived at, based upon information obtained in good faith from sources believed to be reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. This document is for information purposes only. Descriptions of any company or companies or their securities mentioned herein are not intended to be complete and this document is not, and should not be construed as an offer or solicitation of an offer, to buy or sell any securities or other financial instruments. This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any person or entity who is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be contrary to law or regulation or what would subject HSL or its affiliates to any registration or licensing requirement within such jurisdiction. If this report is inadvertently send or has reached any individual in such country, especially, USA, the same may be ignored and brought to the attention of the sender. This document may not be reproduced, distributed or published for any purposes without prior written approval of HSL. Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate fluctuations, which could have an adverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively assume currency risk. It should not be considered to be taken as an offer to sell or a solicitation to buy any security. HSL may from time to time solicit from, or perform broking, or other services for, any company mentioned in this mail and/or its attachments. HSL and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions. HSL, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates, diminution in the NAVs, reduction in the dividend or income, etc. HSL and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities and financial instruments dealt in the report, or may make sell or purchase or other deals in these securities from time to time or may deal in other securities of the companies / organizations described in this report.

HSL or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months. HSL or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from t date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction in the normal course of business. HSL or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither HSL nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. HSL may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the subject company or third party in connection with the Research Report.

This report is intended for non-Institutional Clients only. The views and opinions expressed in this report may at times be contrary to or not in consonance with those of Institutional Research or PCG Research teams of HDFC Securities Ltd. and/or may have different time horizons

HDFC Securities Limited, SEBI Reg. No.: NSE-INB/F/E 231109431, BSE-INB/F 011109437, AMFI Reg. No. ARN: 13549, PFRDA Reg. No. POP: 04102015, IRDA Corporate Agent License No.: HDF 2806925/HDF C000222657, SEBI Research Analyst Reg. No.: INH000002475, CIN - U67120MH2000PLC152193

Mutual Funds Investments are subject to market risk. Please read the offer and scheme related documents carefully before investing.