richard larkin, hj sims director of credit analysis october 2, 2014 smith’s research &...

DESCRIPTION

TOBACCO BONDS: for a sector thAT’S SUPPOSED TO BE STRUCTURED , IT’S BECOMING AN AMORPHOUS BLOB OF UNPREDICTABLE VARIABLES. Richard Larkin, HJ SIMS Director of Credit Analysis October 2, 2014 SMITH’S RESEARCH & GRADINGS HIGH YIELD MUNICIPAL BOND CONFERENCE. - PowerPoint PPT PresentationTRANSCRIPT

Richard Larkin, HJ SIMSDirector of Credit Analysis

October 2, 2014SMITH’S RESEARCH & GRADINGS

HIGH YIELD MUNICIPAL BOND CONFERENCE

The material presented here is for information purposes only and is not to be considered an offer

to buy or sell any security. This report was prepared from sources believed to be reliable but it is not

guaranteed as to accuracy and it is not a complete summary of statement of all available data.

Information and opinions are current up to the date of publication and are subject to change without

notice. The purchase and sale of securities should be conducted on an individual basis considering the

risk tolerance and investment objective of each investor and with the advice and counsel of a

professional advisor.

•Joined SIMS in 2008•26 Years at 2 Rating Agencies, 38 Years Total Experience•Former Chief Municipal Rating Officer at S&P•Chaired or Co-Chaired Rating Criteria Committees at Both S&P and Fitch

•Opinions are mine & mine alone, not necessarily shared by my employer, HJ SIMS, who has allowed me to speak on this subject

•Not a recommendation to buy, sell or hold securitized tobacco settlement bonds

Richard Larkin, Director of Credit Analysis

New projections for default are earlier than last year. Primarily because the Tobacco Companies are still withholding funds from all states, including those that signed the “side settlement” agreement in 2012-13

Cash flows for NY issuers should improve by likely arbitration wins that will earn them refunds of past NPM holdings

More variables keep entering the structures, making forecasts more difficult and with larger margins for future error

Richard Larkin, Director of Credit Analysis

NAAG is cutting back on information needed to analyze tobacco cash flows

The introduction of “losers” in the NPM arbitration has caused ripples in winning and settling states

Ohio Buckeyes will be an interesting battleground in the NPM arena—wins will dramatically improve cash flows, but the Buckeyes won the first arbitration by the “skin of their teeth”. Even so, default can’t be avoided.

Future average annual shipment declines: -4% or -5%??

Do you really understand the concept of extension risk

Richard Larkin, Director of Credit Analysis

MSAi % change TTB % change NAAG OPM % change1997 528.3 N/A 508.6 N/A N/A N/A1998 504.0 -4.60% 456.7 -10.22% N/A N/A1999 458.6 -9.00% 434.5 -4.86% 409.0 N/A2000 459.1 0.10% 422.5 -2.76% 402.7 -1.55%2001 444.4 -3.20% 412.1 -2.46% 384.2 -4.58%2002 427.9 -3.70% 395.2 -4.09% 365.2 -4.94%2003 406.1 -5.10% 376.7 -4.70% 344.7 -5.64%2004 398.8 -1.80% 375.6 -0.29% 339.1 -1.61%2005 385.2 -3.40% 363.0 -3.36% 332.1 -2.08%2006 376.0 -2.40% 364.6 0.44% 327.1 -1.49%2007 357.2 -5.00% 348.3 -4.46% 312.4 -4.50%2008 345.3 -3.33% 335.4 -3.71% 300.2 -3.92%2009 315.7 -8.57% 307.9 -8.19% 269.1 -10.35%2010 303.7 -3.80% 292.8 -4.93% 258.4 -3.96%2011 293.1 -3.49% 286.4 -2.19% 250.5 -3.09%2012 286.5 -2.25% 279.8 -2.27% 245.5 -1.99%2013 273.3 -4.61% 266.1 -4.91% 234.8 -4.34%

2013 YTD 128.6 -4.17% 126.2 -5.13% n/a n/a

-4.04% -3.97% -3.88%Compound Annual Rate of Decl ine 1997-2013

US Domestic Cigarette Shipments 1997-2014 YTD(billions of cigarettes)

Sources : MSAi information comes from Reynolds American 10K reports ; TTB data from Tobacco Tax Bureau; NAAG data from National Association of Attorneys General YTD REPRESENTS THROUGH JUNE 2014

Richard Larkin, Director of Credit Analysis

Issuer NJ OH VAState New Jersey Ohio Virginia

Original Par Issuance $3,436,225,000 $5,212,146,138 $1,052,185,000

Yr Issued 2007 2007 2007Final Maturity 2041 2047 2047Performance

2011 Default Forecast

22% of the 2029 maturity defaults; $1.176 bilion of

seniors and 1.281 million of subordinated debt remain

unpaid in 2041; debt reserves drawn starting 2023

30% of the 2024 maturity defaults; $2.768 billion of

seniors (representing 2037s, 2042s qnd 2047s) and $3.207

billion of subordinated debt unpaid by 2047; debt reserves drawn starting 2011 and 2016.

91% of the 2046 maturity defaults in 2046; %990 million unpaid by 2047 (representing

both 2046 and 2047 maturities.

2013 Forecast, After Settlements And Arbitration

Results through Sept. 12, 2013

Debt service reserves drawn in 2026 & 2029; 16% of 2034s default; $840.1 or

66%% of 2041s unpaid.

6.4% of 2030s in default; 26% of 2034s go unpaid;

each maturity sees larger defaults until 47s in default;

$891 or 64% unpaid………..not paid in

full until about 2052

Debt reserves drawn 2014-15-16-17; in 2047, 30% of 2046s and 100% of 2047s

2014 Forecast,

Debt service reserves drawn in 2014, 2023,

exhausted with default by 2026; & 2029; 89% of 2041s

go unpaid; may take 7 years to fully pay without

interest accruing after 2041 maturity

Debt service reserves drawn in 2016, 2017,

exhausted with default by 2024; & 2029; 2042s not

fully paid until 2047, & 100% of 2047s unpaid…could

take 8 years to fully repay.

Debt reserves drawn in 2014; by 2047, 53% of '46

maturity unpaid and 100% of '47 maturity unpaid;

could wait 12 years before all principal paid

Selected Tobacco Bond PerformancePost 2005 Issuance

Richard Larkin, Director of Credit Analysis

Issuer NJ at -4% Shipment Declines NJ at -5% Shipment DeclinesState New Jersey New Jersey

Original Par Issuance $3,436,225,000 $3,436,225,000

Yr Issued 2007 2007Final Maturity 2041 2041Performance

2014 Forecast,

Debt service reserves drawn in 2014, 2023, exhausted with default by 2026;

58% of 2034s default, and 89% of 2041s go unpaid; may take 7 years to fully pay without interest accruing after

2041 maturity

Debt service reserves drawn in 2014, 2023, exhausted with default by 2026; 2034s miss 100% of principal due; by

2047, 2% of 34s remain unpaid & 100% of 2041s unpaid

New Jersey Tobacco Bond PerformanceWorsening Credit Quality Comparing Shipment Declines at -4% & -5%

Richard Larkin, Director of Credit Analysis

IssuerOH Status Quo

Projections

OH Performance if it Wins Next 10 Years of

ArbitrationState Ohio Ohio

Original Par Issuance $5,212,146,138 $5,212,146,138

Yr Issued 2007 2007Final Maturity 2047 2047Performance

2014 Forecast

Debt service reserves drawn in 2016, 2017,

exhausted with default by 2024; & 2029; 2042s not

fully paid until 2047, & 100% of 2047s unpaid…could

take 8 years to fully repay.

Debt service reserves not drawn until 2024, defaults

not until 2030; by 2047, only 44% remain unpaid

OHIO BUCKEYE Tobacco Bond PerformanceImprovement Attributable to Winning NPM Cases

Richard Larkin, Director of Credit Analysis

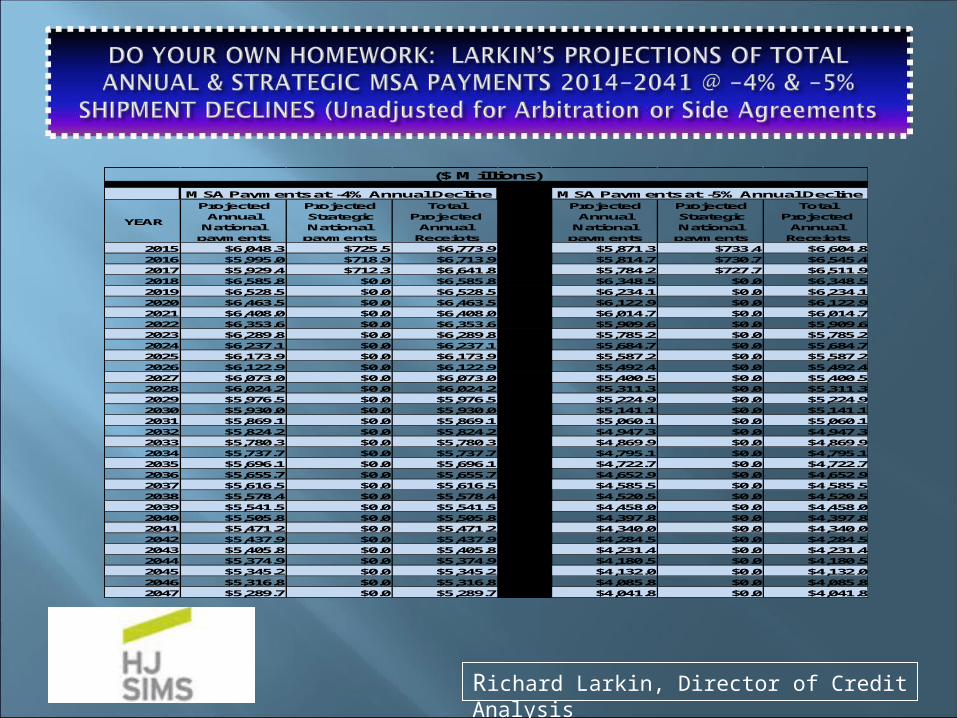

YEAR

Projected Annual

National payments

Projected Strategic National

payments

Total Projected

Annual Receipts

Projected Annual

National payments

Projected Strategic National

payments

Total Projected

Annual Receipts

2015 $6,048.3 $725.5 $6,773.9 $5,871.3 $733.4 $6,604.82016 $5,995.0 $718.9 $6,713.9 $5,814.7 $730.7 $6,545.42017 $5,929.4 $712.3 $6,641.8 $5,784.2 $727.7 $6,511.92018 $6,585.8 $0.0 $6,585.8 $6,348.5 $0.0 $6,348.52019 $6,528.5 $0.0 $6,528.5 $6,234.1 $0.0 $6,234.12020 $6,463.5 $0.0 $6,463.5 $6,122.9 $0.0 $6,122.92021 $6,408.0 $0.0 $6,408.0 $6,014.7 $0.0 $6,014.72022 $6,353.6 $0.0 $6,353.6 $5,909.6 $0.0 $5,909.62023 $6,289.8 $0.0 $6,289.8 $5,785.2 $0.0 $5,785.22024 $6,237.1 $0.0 $6,237.1 $5,684.7 $0.0 $5,684.72025 $6,173.9 $0.0 $6,173.9 $5,587.2 $0.0 $5,587.22026 $6,122.9 $0.0 $6,122.9 $5,492.4 $0.0 $5,492.42027 $6,073.0 $0.0 $6,073.0 $5,400.5 $0.0 $5,400.52028 $6,024.2 $0.0 $6,024.2 $5,311.3 $0.0 $5,311.32029 $5,976.5 $0.0 $5,976.5 $5,224.9 $0.0 $5,224.92030 $5,930.0 $0.0 $5,930.0 $5,141.1 $0.0 $5,141.12031 $5,869.1 $0.0 $5,869.1 $5,060.1 $0.0 $5,060.12032 $5,824.2 $0.0 $5,824.2 $4,947.3 $0.0 $4,947.32033 $5,780.3 $0.0 $5,780.3 $4,869.9 $0.0 $4,869.92034 $5,737.7 $0.0 $5,737.7 $4,795.1 $0.0 $4,795.12035 $5,696.1 $0.0 $5,696.1 $4,722.7 $0.0 $4,722.72036 $5,655.7 $0.0 $5,655.7 $4,652.9 $0.0 $4,652.92037 $5,616.5 $0.0 $5,616.5 $4,585.5 $0.0 $4,585.52038 $5,578.4 $0.0 $5,578.4 $4,520.5 $0.0 $4,520.52039 $5,541.5 $0.0 $5,541.5 $4,458.0 $0.0 $4,458.02040 $5,505.8 $0.0 $5,505.8 $4,397.8 $0.0 $4,397.82041 $5,471.2 $0.0 $5,471.2 $4,340.0 $0.0 $4,340.02042 $5,437.9 $0.0 $5,437.9 $4,284.5 $0.0 $4,284.52043 $5,405.8 $0.0 $5,405.8 $4,231.4 $0.0 $4,231.42044 $5,374.9 $0.0 $5,374.9 $4,180.5 $0.0 $4,180.52045 $5,345.2 $0.0 $5,345.2 $4,132.0 $0.0 $4,132.02046 $5,316.8 $0.0 $5,316.8 $4,085.8 $0.0 $4,085.82047 $5,289.7 $0.0 $5,289.7 $4,041.8 $0.0 $4,041.8

MSA Payments at -4% Annual Decline MSA Payments at -5% Annual Decline

($ Millions)

Richard Larkin, Director of Credit Analysis

StateShare Within the Side Agreement

Projected Annual 12 1/2% Refund Credits for 2014-

20171 AL 3.36% $7.122 AZ 3.62% $7.673 AR 1.81% $3.834 CA 26.33% $55.825 CT 4.43% $9.396 DC 1.37% $2.917 GA 5.05% $10.708 KS 2.07% $4.409 LA 5.05% $10.71

10 MI 9.17% $19.4411 NE 1.35% $2.8612 NV 1.44% $3.0613 NH 1.52% $3.2214 NJ 8.28% $17.5515 NC 5.04% $10.6916 OK 2.77% $5.8717 SC 2.63% $5.5718 TN 4.98% $10.5619 VA 4.20% $8.9120 WV 2.28% $4.8321 WY 0.67% $1.4122 Puerto Rico 2.59% $5.50

100.00% $212.00

Master Settlement Allocations Under 2012 Side Agreement

• Email Me at [email protected]

• Access all of Dick Larkin’s reports and commentaries on the HJ SIMS website under SIMS INSIGHTS: http://www.hjsims.com/news-and-views/sims-insights/