session01 doviak - introduction to the shipping industry

TRANSCRIPT

1

IFLOS SUMMER ACADEMY - HAMBURG

Session 1 – Week 3Introduction to the Shipping Industry

5 August 2019

Presented byDr John M DoviakManaging Director

Cambridge Academy of Transport

CambridgeAcademy ofTransport

2

Content

• Perspective on World Trade

• Perspective on Shipping

• Tonnage Definitions

• Limiting Factors to Trading

• Who Owns the Major Fleets of the World

• The Big Picture: Historical Growth of Merchant Fleet

• Conclusion

1

CambridgeAcademy ofTransport

3

Perspective on World Trade

Demand for Ships

CambridgeAcademy ofTransport

4

PERSPECTIVE ON WORLD TRADE(2015)

• World GDP is approximately $74,689bn – down 5.4% from 2014 ($78,832bn) †

• The first fall in GDP since 2009

• Most of this drop can be put down to the method of measurement: GDP Constant Prices , US$

• In 2015, on this basis, 128 countries showed a negative growth and only 60 were positive

• Included in the negative group are almost all oil or commodity exporting countries including:

– All Middle East exporters

– Nigeria

– Norway

– Australia

– South Africa

• In the positive group were many countries that rely on aid including most of Africa, Latin America and Caribbean

• NOTE:

– USA growth was 3.6% to $18,000bn

– China growth was 9.9% to $11,400bn

† All GDP figures from Interna onal Monetary Fund (IMF)

2

CambridgeAcademy ofTransport

5

PERSPECTIVE ON WORLD TRADE(2016)

• World GDP is approximately $75,735bn (1.4% over 2015)

• Of this, World (International) Trade is about $15,500bn (Down ~8% as value of goods fell).

• Of this, the major part is carried by ships (approx $10,000bn by value and 90-95% by volume)

– GACAG (Global Air Cargo Advisory Group) estimates air cargo value at 30% of World Trade value

• Total freight bill between $300-$400bn (~3%) but operators gained benefit of lower fuel costs

World GDP

World Trade

Seaborne Trade

$75,653bn

$16,058bn

$10,000bn (Estimate)

Shipping services this part

CambridgeAcademy ofTransport

6

PERSPECTIVE ON WORLD TRADE(2017)

• World GDP is approximately $80,144bn (5.8% over 2016)

• Of this, World (International) Trade grew by 10.9% as the value of goods recovered.

• Of this, the major part is carried by ships (approx $11,000bn by value and 90-95% by volume)

– GACAG (Global Air Cargo Advisory Group) estimates air cargo value at 30% of World Trade value

• Total freight bill between $300-$400bn (~3%) but gained benefit of lower fuel costs

World GDP

World Trade

Seaborne Trade

$80,144bn

$17,810bn

$11,000bn (Estimate)

Shipping services this part

3

CambridgeAcademy ofTransport

7

PERSPECTIVE ON WORLD TRADE(2018)

• World GDP is approximately $84,740bn (5.7% over 2017)

• Of this, World (International) Trade grew by 10.6% as the value of goods continued to recover.

• Of this, the major part is carried by ships (approx $11,000bn by value and 90-95% by volume)

– GACAG (Global Air Cargo Advisory Group) estimates air cargo value at 30% of World Trade value

• Total freight bill between $300-$400bn (~3%) but gained benefit of lower fuel costs

World GDP

World Trade

Seaborne Trade

$84,740bn

$19,690bn (Exceeded previous peak in 2014of $18,891bn for imports

$11,500bn (Estimate)

Shipping services this partFreight > $350bn

CambridgeAcademy ofTransport

Global Picture GDP 2017

8

2018 GDPUSA $20,494China $13,407Japan 4,972Germany 4,000UK 2,829

Source: World Economic Forum

4

CambridgeAcademy ofTransport

9

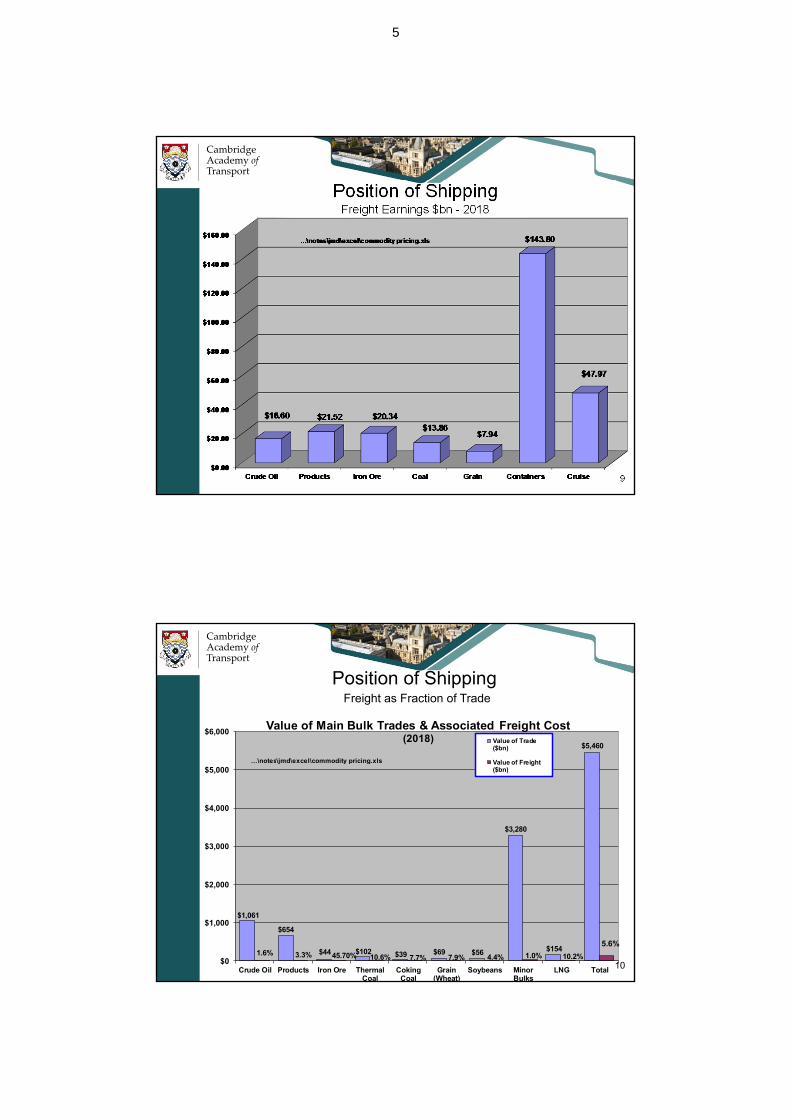

Position of ShippingFreight Earnings $bn - 2018

CambridgeAcademy ofTransport

$1,061

$654

$44 $102 $39 $69 $56

$3,280

$154

$5,460

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

Crude Oil Products Iron Ore ThermalCoal

CokingCoal

Grain(Wheat)

Soybeans MinorBulks

LNG Total

Value of Main Bulk Trades & Associated Freight Cost(2018) Value of Trade

($bn)

Value of Freight($bn)

1.6% 3.3% 45.70% 10.6% 7.7% 4.4%

…\notes\jmd\excel\commodity pricing.xls

1.0% 10.2%

5.6%

7.9%10

Position of ShippingFreight as Fraction of Trade

5

CambridgeAcademy ofTransport

11Source:Clarksons

Stable Markets

Low Commodity Prices

CommodityPricesRecovering

CambridgeAcademy ofTransport

12

Dry Cargoes, 8,068

Liquid Cargoes, 3,878

(Total 11,946 million tonnes)

Dry Cargo accounts for approximately 68% of World Trade

NB: Dry cargo includes all cargoes including containerised

World Seaborne Trade 2018 (Est)

Source:Clarksons

6

CambridgeAcademy ofTransport

13

Crude Oil2,036

Products1,104

LNG325

Chemical319

LPG94

(Total 3,878 million Tonnes)

Crude Oil accounts for approximately 53% of Liquid Cargo Tradewhich has fallen as a percentage over several years

(Chemicals include organic, inorganic, molasses, veg oil, lubes & ethanol)

Liquids Seaborne Trade 2018 (Est)

Source:Clarksons

CambridgeAcademy ofTransport

14

Container1,926

Other Dry918

Dry Bulk5,224

(Total 8,068 million Tonnes)

Dry Bulk Cargo accounts for approximately 65% of the Dry Trade

Dry Cargo Seaborne Trade 2018 (Est)

Source:Clarksons

7

CambridgeAcademy ofTransport

15

Major Bulks accounts for approximately 62% of the Dry Bulk Trade

Minor Bulks1,995

Major Bulks3,229

(Total 5,224 million Tonnes)

Agribulks & SoftsMetals & MineralsManufactures

Iron OreCoalGrainSoybean

Dry Bulk Trade 2018 (Est)

Source:Clarksons

CambridgeAcademy ofTransport

16

The Steel Industry accounts for approximately 55% of the Major Bulk Trade

NB: Iron Ore and Coking Coal are basic ingredients for steel

Coking Coal267

Grain335

Soybeans148

Iron Ore1498

Steam Coal981

Major (Dry) Bulk Trade 2018 (Est)(Total 3,229 million Tonnes)

Source:Clarksons

8

CambridgeAcademy ofTransport

17

The Steel Industry accounts for approximately 32% of the Minor Bulk Trade

NB: Production of steel products makes use of scrap, coke and some petcoke

Other277 Bauxite & Alumina

145Phosphate Rock

28

Steel Products391

Scrap119

Coke21

Petcoke74

Sugar55

Agribulks175

Fertilizer145

Nichel Ore48

Anthracite33

Cement110

Forest Products374

(Total 1,995 million Tonnes)

AgribulksSoymealOilseed/mealRiceGrapeseed extractGroundnut kernelsCorn Gluten CakesGuarmealCotton seed extractLinseed extractOther extracts

Minor Bulk Trade 2018 (est)

Source:Clarksons

CambridgeAcademy ofTransport

18

% Dry Bulk Trade

Steel Industry

- Iron Ore & Coking (metallurgical) Coal

- Steel Products

- Scrap

- Pig Iron Est (13m mt) & Coke (& 25% petcoke)

34.1%

7.8%

2.1%

0.6%

Total 44.6%

Energy

Steaming coal 18.4%

Agriculture

Grain, Soybeans, Ferts, Sugar & Agribulks 17.7%

What Trades Drive Dry-Cargo Freight Rates?2018

9

CambridgeAcademy ofTransport

19

Perspective on Shipping

Definition of ShippingCharacteristics of Shipping

Ship typesStructure of the fleet

CambridgeAcademy ofTransport

20

Shipping Is…

…a Derived Demand industry

• If there were no seaborne trade, we wouldn’t need ships.

• The growth of seaborne trade increases the demand for shipping services

• Matching trade growth with ship fleet growth is a tricky business

• Trade growth cannot be accurately predicted

• BUT ships must be ordered 3-4 years ahead

• If trade grows faster than the fleet: SHIPPING BOOM

• If the fleet grows faster than trade: SHIPPING RECESSION

These mismatches in growth rates lead to fluctuations in the “freight market” – where the charges for using ships are negotiated between shipowner and cargo owner.

10

CambridgeAcademy ofTransport

21

Shipping

“Shipping is a complex industry and the conditions which govern its operations in one sector do not necessarily apply in another; it might even, for some purposes, be better regarded as a group of related industries. Its main assets, the ships themselves, vary widely in size and type; they provide the whole range of services which are needed to transport passengers and a great variety of goods, whether over shorter or longer distances. Although one can, for analytical purposes, usefully isolate sectors of the industry providing particular types of service, there is usually some interchange at the margin which cannot be ignored.”

(UK Parliament Rochdale Report 1967)

What does all this mean?

CambridgeAcademy ofTransport

22

• “... a group of related (but distinct) industries.”

Liner - Tanker

Gas - ReeferFerries - Dry-Bulk

• “...ships vary widely in size and type.”Small to very BIG: 10 tonnes to 440,000 tones

How big was the biggest?mid 50s - 50,000 dwtmid 60s - 100,000 dwtmid 70s - 555,000 dwtmid 80s - “mid 90s - “2000 - 440,000 dwt

• “...interchange at the margin.”finance classificationshipbuilding ports & terminalsskilled crew fuels & lubricantsinsurance ship management

Characteristics of Shipping

11

CambridgeAcademy ofTransport

23

Ship Types

Fishing Offshore Cable ResearchVessels

Anchor handlingDredgers Survey Tugs Icebreakers

Supply Boats Ships

Floating storage

Production

Pipe Laying

Passenger General Cargo Combination Bulk

CruiseUnit Load Ro/Ro Break Bulk Tanker Dry Bulk Timber Specialist

FerryContainer Car/PCC Tweendecker Crude Grain Wood chip Chemical

Ro/RoLash Reefer Products Coal Pulp Gases

HovercraftSeabee LPG Open Self Wine and

Hydrofoil Hatch Unloading SpiritsPallet Ethylene Log Carrier

Jetfoil O/O Iron BeerHeavy Lift LNG

Cat OBO Sugar Orange JuiceBacat CNG

Hotel/Prison Probo Cement Sulphuric AcidATB Asphalt

Auto/Reefer Lakers NuclearITB Molten

Conbulker Sulphur BIBO Sugar

FPSO Livestock(TO/TO)

FSO

Ships which carry things

Ships which keepthe sea lanes open

Rescue/Standby

CambridgeAcademy ofTransport

24

Passenger General Cargo Combination Bulk

CruiseUnit Load Ro/Ro Break Bulk Tanker Dry Bulk Timber Specialist

FerryContainer Car/PCC Tweendecker Crude Grain Wood chip Chemical

Ro/RoLash Reefer Products Coal Pulp Gases

HovercraftSeabee LPG Open Self Wine and

Hydrofoil Hatch Unloading SpiritsPallet Ethylene Log Carrier

Jetfoil O/O Iron BeerHeavy Lift LNG

Cat OBO Sugar Orange JuiceBacat CNG

Hotel/Prison Probo Cement Sulphuric AcidATB Asphalt

Auto/Reefer Lakers NuclearITB Molten

Conbulker Sulphur BIBO Sugar

FPSO Livestock(TO/TO)

FSO

Ships which carry things

CambridgeAcademy ofTransport

12

CambridgeAcademy ofTransport

25

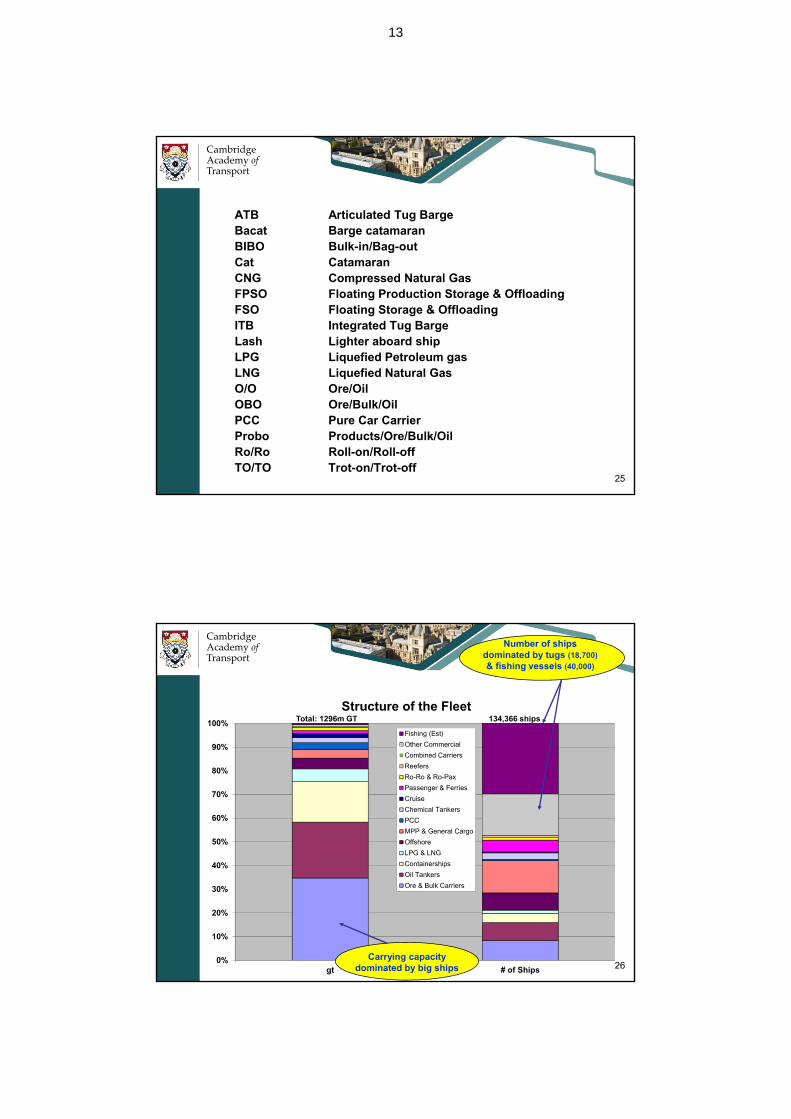

ATB Articulated Tug BargeBacat Barge catamaranBIBO Bulk-in/Bag-outCat CatamaranCNG Compressed Natural GasFPSO Floating Production Storage & OffloadingFSO Floating Storage & OffloadingITB Integrated Tug BargeLash Lighter aboard shipLPG Liquefied Petroleum gasLNG Liquefied Natural GasO/O Ore/OilOBO Ore/Bulk/OilPCC Pure Car CarrierProbo Products/Ore/Bulk/OilRo/Ro Roll-on/Roll-offTO/TO Trot-on/Trot-off

CambridgeAcademy ofTransport

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

gt # of Ships

Structure of the Fleet

Fishing (Est)

Other Commercial

Combined Carriers

Reefers

Ro-Ro & Ro-Pax

Passenger & Ferries

Cruise

Chemical Tankers

PCC

MPP & General Cargo

Offshore

LPG & LNG

Containerships

Oil Tankers

Ore & Bulk Carriers

Carrying capacitydominated by big ships

Number of shipsdominated by tugs (18,700)

& fishing vessels (40,000)

26

Total: 1296m GT 134,366 ships

13

CambridgeAcademy ofTransport

27

Physical Characteristics of Ships

Tonnage Explained

CambridgeAcademy ofTransport

28

• Displacement - The actual weight of the ship at any given time (corresponds to the weight of the water which the vessel displaces).

NB: Varies depending on how much weight the vessel is carrying

• Light Weight - the weight of the empty ship (no cargo, crew, stores, fuel, water and ballast).

NB: Displacement = Light Weight when the ship is completely empty

• Deadweight - Total weight of cargo, crew, stores, fuel, water and ballast.Displacement – Deadweight = Light weight

The above weights are today conventionally measured in metric tonnes (=1000kg)

Tonnage Definitions

14

CambridgeAcademy ofTransport

29

• Gross Ton – A volume measure of the internal capacity of a vessel. Until early 1990s, 1 grt (gross registered ton) was defined as 100 cubic feet. The International Tonnage Convention 1969 which came into force in the 1990s redefined the Gross Ton as 1 gt ≈ 3 cubic metres.

NB: Although called a “ton” it is actually a volume

• Net Ton – defined in the same way as the Gross Ton but some of the internal carrying capacity of the vessel is excluded. The object is to arrive at a volume of space which can be used to carry passengers or goods: the revenue earning space. Therefore such spaces as crew quarters, engine room, ballast tanks and the like are excluded.

NB: Taxes and port dues are usually levied on the Net Tonnage

Tonnage definitions - continued

CambridgeAcademy ofTransport

30

Ship size measurement

Tankers Bulk Carriers LinersLiners

(containers) Gas Cruise

Unit dwt(deadweight)

dwt gt(gross ton)

TEU(twenty foot

equivalent unit

cubic metres Lower Berths

Measure metric tonnecapacity

metric tonnecapacity

volume measure

1 gt~100 cu ft

volume measure

1 TEU=8'x8'x20'

volumemeasure

passengers

All vessels have a maximum weight that they can carry as determined by the weight which causes the vessel to sink to its "load line".

Different groups of vessels use different units for their size measurement

15

CambridgeAcademy ofTransport

31

Limiting Factors

How much can vessels carryWhere can vessels trade

CambridgeAcademy ofTransport

32

How much may a Vessel Carry

Loadline Marks (Plimsoll Line)Deck Edge

L R

TF

FT

S

W

WNA

(Tropical Fresh)

(Fresh)(Tropical)

(Summer)

(Winter)

(Winter North Atlantic)

FWA (Fresh WaterAllowance)

Freeboard

Rules:

1. FWA = D/(40T) where D is Displacement weight at Summer Draft and T is TPC

2. Gap between (T - S), (S - W) and (TF - F) = Draft/48

3. WNA applies only to vessels of 100m length or less.

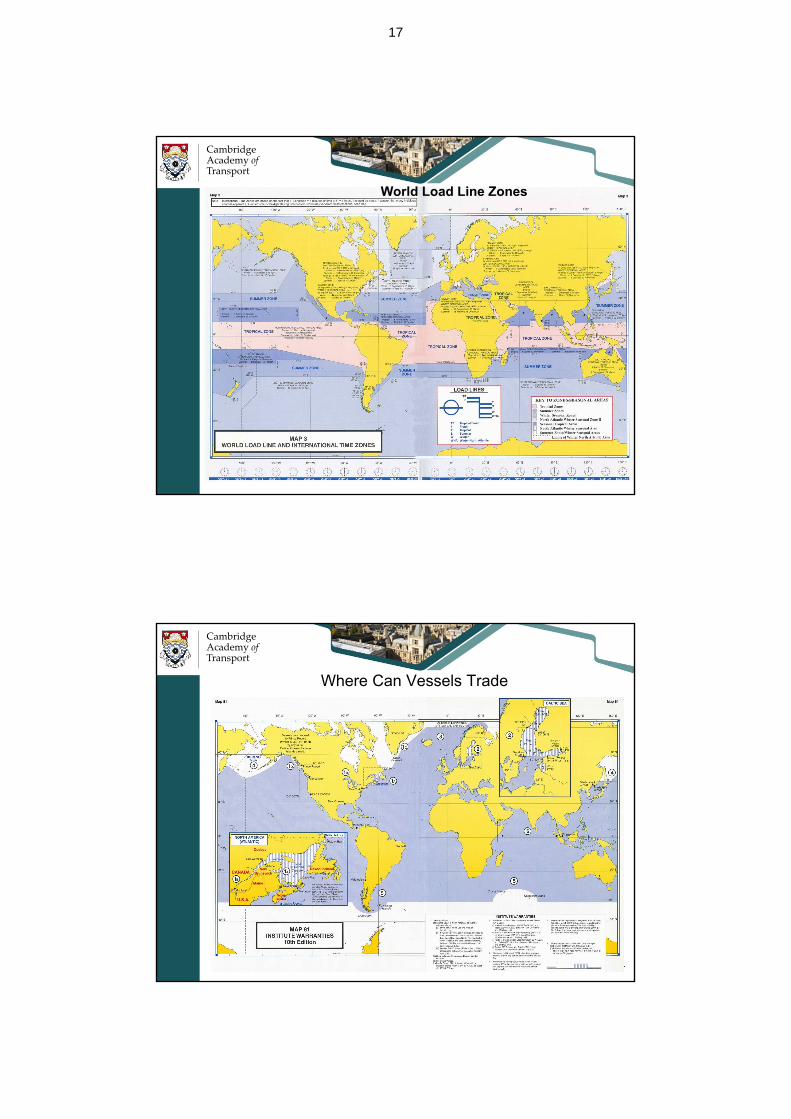

16

CambridgeAcademy ofTransport

3333

World Load Line Zones

CambridgeAcademy ofTransport

3434

Where Can Vessels Trade

17

CambridgeAcademy ofTransport

35

• IWL – Institute Warranties LimitsA separate clause dating from 1/7/76 which was added to hull insurance contracts. It restricted where the vessel could trade. No Arctic, Antarctic, Baltic in winter etc.(Institute = Institute of London Underwriters)

• INL – International Navigation LimitsThe modern form of wording used to restrict the operation of ships geographically. It is expressly included in the new International Hull Clauses dating from 2003. Largely the same as IWL with an clarification of the restricted areas

IWL versus INL

CambridgeAcademy ofTransport

3636

Stowage factor Principles

WaterLine

If holds are completely filled with cargo of stowage factor 40, vessel will sink down to “her marks” - in other words the Plimsoll Mark line will align with the surface of the water when in salt water. Example Calcium Nitrate: 32-40 cu ft/tonne

With a cargo of higher stowage factor (ie a cargo that is less dense), the vessel will not sink as deeply as her Plimsoll Mark even with the hold completely full. Example Soyabean meal in bulk: 58-60 cu ft/tonne

With a more dense cargo (lower stowage factor), the vessel will have sunk to her Plimsoll Mark before the hold is completely full. Example iron ore concentrate: 11-20 cu ft/tonne

Relationship between Stowage Factor (Cubic Feet per Ton) and Hold occupancy.

PlimsollMark

Vessel design for cargo of stowage factor 40.

With a cargo of stowage factor 60.

With a cargo of stowage factor 20.

18

CambridgeAcademy ofTransport

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

gt # of Ships

Structure of the Fleet

Fishing (Est)

Other Commercial

Combined Carriers

Reefers

Ro-Ro & Ro-Pax

Passenger & Ferries

Cruise

Chemical Tankers

PCC

MPP & General Cargo

Offshore

LPG & LNG

Containerships

Oil Tankers

Ore & Bulk Carriers

Let’s take a closer look atthe three biggest sectors:Bulker, Tanker & Container

Recall…

37

CambridgeAcademy ofTransport

38Source: Clarksons March 2017

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Fleet Development (million dwt)at 1st January

Other

Containerships

General Cargo

Combination

Bulkers

Tankers

= Tramp, Liner, Multi-purpose & Ro/Roships

= LPG, LNG, PCC, Reefer, Offshore (AHTS & PSV), & Other Cargo

19

CambridgeAcademy ofTransport

39

Vessel Terminology

Dry-BulkTanker

Container

CambridgeAcademy ofTransport

40

Dry-bulk Shipping

20

CambridgeAcademy ofTransport

4141

Bulk-Cargo Vessel Terminology

Source: Clarksons December 2018

Note: Kamsarmax vessels are those of length 229m, but of “old” Panamax beamExcludes Lakes Only vessels (78 no.) & Combination Carriers (47 no.)Specials include Aggregate, Deck Cargo Only, Heavy Lift, Landing Craft, Livestock and Pallet

Generic Name Typical SizeNo.

OwnersNo.

Ships Dwt

General Cargo General Cargo / Tweendecker <43,000 dwt 6,066 11,984 29.1m

Specials <47,000 dwt 970 1,763 2.3m

Multi-Purpose (MPP) 1,000-55,000 dwt 968 3,174 29.2m

Small Bulkers Small Bulkers <10,000 dwt 729 1,190 3.0m

Dry Bulk Handysize 10 – 39,999 dwt 1,120 3,378 96.6m

Handymax 40 – 49,999 dwt 310 703 32.4mSupramax 50 – 59,999 dwt 604 2,076 115.3mUltramax (Note overlap with Panam 60 – 69,999 dwt 236 801 50.1mPanamax 65 – 79,999 dwt 422 1,173 91.8mKamsarmax 80 – 82,999 dwt 277 848 69.3mPost-Panamax 83 – 99,999 dwt 159 499 45.3mCapesize 100 – 404,000 dwt 256 1,703 326.6m…of which VLBC (or VLOC) >200,000 dwt 84 488 119.8m

TOTAL (>10,000 dwt) 1,938 11,182 823.8m

Bulk Cargo Vessel Terminology

CambridgeAcademy ofTransport

4242Source: Clarksons October 2018

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

800.00

900.00

mil

lio

n d

wt

Bulk Carrier Fleet Development(@ year end except 2018 which is at 1/10/2018)

Capesize

Panamax

Handymax

Handysize

21

CambridgeAcademy ofTransport

Source: Clarkson, October 201843

Pacific Basin Shpg2,646,224

Fednav1,623,649

Wisdom Marine Group1,508,910

Polish Steamship Co1,393,658

John Swire & Sons1,179,463

China COSCO Shipping1,145,283

Shih Wei Navigation1,013,186

Canadian Forest Nav.984,420

Interlink Ltd961,223

Hartmann AG838,650

Top 10 Owners ‐ Handysize(13.8% of Handysize Fleet)

Total Handy Fleet:1120 Owners3378 Vessels / 30.2% Fleet96.6 dwt / 11.7% FleetAverage Age: 12.1Average Size: 28,592 dwt

CambridgeAcademy ofTransport

Handysize Bulk Carrier

44m.v. Mount Owen 28,333 dwt - owned by Pacific Basin

22

CambridgeAcademy ofTransport

Source: Clarkson, October 201845

China COSCO Shipping16,270,716

Berge Bulk9,930,665

Angelicoussis Group9,168,375

Fredriksen Group8,692,082

Nippon Yusen Kaisha8,567,905

K-Line8,237,992

Polaris Shipping Co7,855,751

Mitsui O.S.K. Lines7,575,356

Pan Ocean6,387,748

NS United KK6,294,688

Top 10 Owners ‐ Capesize(26.9% of Capesize Fleet)

Total Capesize Fleet:256 Owners1703 Vessels / 15.2% Fleet326.6 dwt / 39.6% FleetAverage Age: 9.2Average Size: 191,771 dwt

CambridgeAcademy ofTransport

Largest Dry-Bulk Carrier

46mv Sea Beijing 403,818 dwt 7 Holds - owned by Pan Ocean Shipping

Note: One hold equivalent to Panamax size ship!

23

CambridgeAcademy ofTransport

47

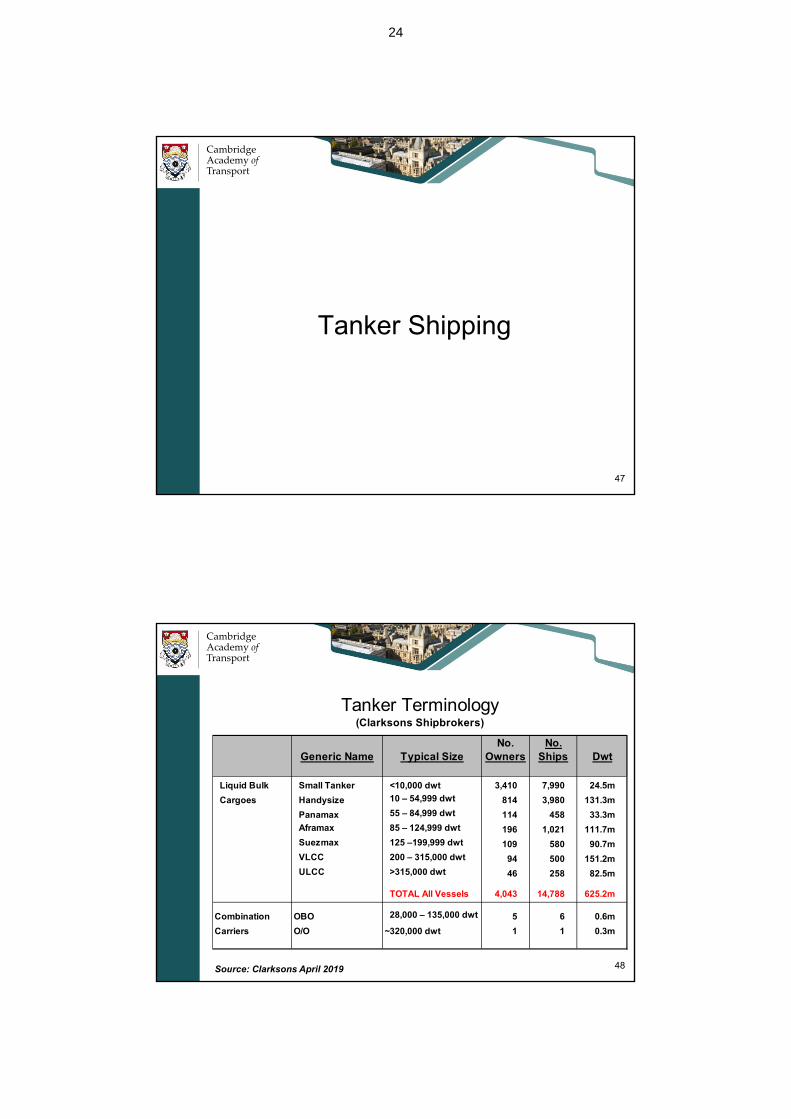

Tanker Shipping

CambridgeAcademy ofTransport

48

Tanker Terminology(Clarkson Shipbrokers)

Source: Clarksons April 2019

Generic Name Typical SizeNo.

OwnersNo.

Ships Dwt

Liquid Bulk Small Tanker <10,000 dwt 3,410 7,990 24.5m

Cargoes Handysize 10 – 54,999 dwt 814 3,980 131.3m

Panamax 55 – 84,999 dwt 114 458 33.3m

Aframax 85 – 124,999 dwt 196 1,021 111.7m

Suezmax 125 –199,999 dwt 109 580 90.7m

VLCC 200 – 315,000 dwt 94 500 151.2m

ULCC >315,000 dwt 46 258 82.5m

TOTAL All Vessels 4,043 14,788 625.2m

Combination OBO 28,000 – 135,000 dwt 5 6 0.6m

Carriers O/O ~320,000 dwt 1 1 0.3m

Tanker Terminology(Clarksons Shipbrokers)

24

CambridgeAcademy ofTransport

4949Source: Clarksons April 2018

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00m

illio

n d

wt

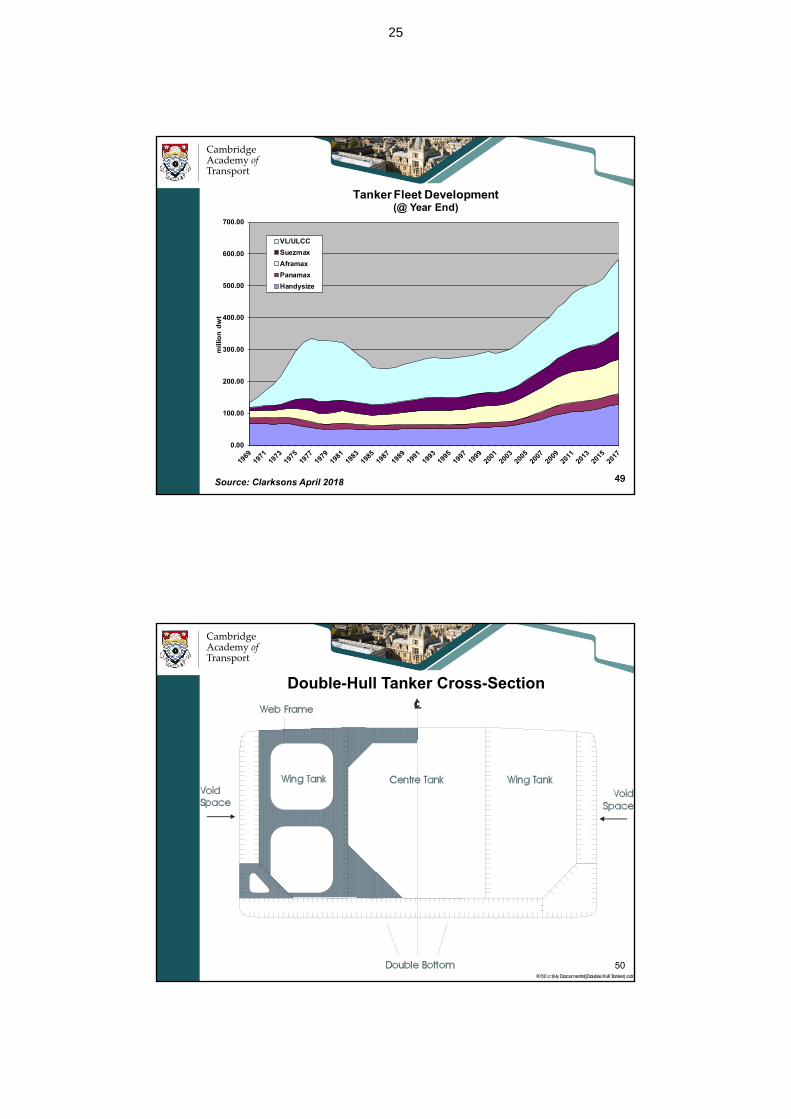

Tanker Fleet Development(@ Year End)

VL/ULCC

Suezmax

Aframax

Panamax

Handysize

CambridgeAcademy ofTransport

50

Double-Hull Tanker Cross-Section

25

CambridgeAcademy ofTransport

51Source: October 2018

51

China Merchants14,488,548

Euronav NV14,029,096

Bahri13,995,145

China COSCO Shipping

12,799,690

Nat Iranian Tanker11,763,127

Angelicoussis Group11,048,841

Mitsui O.S.K. Lines8,600,303

DHT Holdings8,054,148

SK Holdings5,644,945

Nippon Yusen Kaisha5,165,428

Top 10 Owners (dwt) ‐ UL/VLCC(47.0% of UL/VLCC Fleet)

Total UL/VLCC Fleet:107 Owners729 Vessels / 5.0% Fleet224.65m dwt / 36.8% FleetAverage Age: 9.4Average Size: 308,160dwt

CambridgeAcademy ofTransport

Largest Tanker Afloat

52Euronav TI Europe 441,561 dwt, 380.0m length

26

CambridgeAcademy ofTransport

53Source: October 2018

53

Scorpio Group3,214,408

TORM A/S2,781,856

Mitsui O.S.K. Lines2,576,549

Stolt-Nielsen2,252,145

A.P. Moller Holding2,140,149

Sinokor Merchant2,032,030

China Merchants2,008,290

Diamond S Shipping1,657,324

China COSCO Shipping1,596,302

SCF Group1,573,711

Top 10 Owners (dwt) ‐ Handysize(16.6% of Handysize Fleet)

Total Handy Fleet:814 Owners3,980 Vessels / 26.9% Fleet131.33m dwt / 21.0% FleetAverage Age: 11.1Average Size: 32,997dwt

CambridgeAcademy ofTransport

Chemical Carrier

54Fairfield “Fairchem Friesian” 21,209 dwt, LOA 146m

27

CambridgeAcademy ofTransport

55

Container Shipping

CambridgeAcademy ofTransport

56

Key Features of Container Shipping – 1

A Liner Business

• It is “Liner” shipping, not “Tramp” shipping

– Liner Shipping are ships plying a fixed route or routes, sailing according to pre-determined schedules which offer cargo and/or passengers space at fixed rates to those who wish to have goods transported or make journeys

– Tramps are vessels that trade anywhere in the world without a fixed itinerary and which offer their services to the highest bidder

– Not all vessels and trades fall into these two neat categories: for example, industrial shipping such as the regular supply of iron ore to a steel mill, which service may be agreed many years ahead.

28

CambridgeAcademy ofTransport

57

• For many years, the container business was under the dominant influence of the “Conference System”

– A “Conference” is a group of two or more vessel operating carriers which provides international liner services for the carriage of cargo on a particular route or routes within specified geographical limits and which has an agreement or arrangements, whatever it’s nature, within the framework of which they operate under uniform or common freight rates and any other agreed conditions with respect to the provision of liner services.

Key Features of Container Shipping – 2

The Conference System

CambridgeAcademy ofTransport

58

Key Features of Container Shipping – 3

Consortia

• Today, Container Shipping companies group together in what are known as “Consortia”

– ‘Consortium’ means an agreement between two or more vessel-operating carriers which provide international liner shipping services exclusively for the carriage of cargo, chiefly by container, relating to a particular trade

– the object of a consortium is to bring about co-operation in the joint operation of maritime transport services, which improves the service which would otherwise be offered individually by each of its members in the absence of the consortium

– Members of the consortium rationalize their services by means of technical, operational and/or commercial arrangements, with the exception of price fixing.

29

CambridgeAcademy ofTransport

Container Terminology(Clarkson Shipbrokers)

59Source: Clarksons August 2018

No. No.

Owners Ships

Feeder <3000 TEU 567 2,907 3,930,160 53.42 Large Feeder 3,000 –5,999 TEU 133 1,089 4,972,506 62.75 Intermediate 6,000 – 7,999 TEU 44 270 1,865,063 23.09 Neo Panamax 8,000 – 11,999 TEU 54 607 5,339,472 64.16 Large Neo Panamax 12,000 – 14,999 TEU 22 223 2,931,890 32.00 Post Panamax >15,000 TEU 13 104 1,629,407 16.90

TOTAL 631 5,200 21,193,470 256.83

TEU dwtGeneric Name Typical Size

CambridgeAcademy ofTransport

60Source: Clarksons as at April 2018

0

5,000

10,000

15,000

20,000

25,000

'000

TE

U

Containership Fleet Development('000 TEU as at 1 January)

Post-Panamax (>15,000TEU)

Large Neo-Panamax (12-15,000TEU)

Small Neo-Panamax (8-12,000TEU)

Large Intermediate (6-8,000TEU)

Small Intermediate (3-6,000TEU)

Large Feeder (2-3,000TEU)

Intermediate Feeder (1-2,000TEU)

Feeder (<1000TEU)

…\my documents\notes\clarkson data\container fleet.xls

30

CambridgeAcademy ofTransport

61Source: Clarksons April 2018

A.P. Moller2,327,892

MSC1,258,197

China COSCO Shipping1,151,234CMA CGM

1,082,654

Hapag-Lloyd1,031,575

Seaspan Corporation869,500

Evergreen Marine558,991

Orient Overseas Intl543,547

Reederei C-P Offen499,860

Costamare Shipping459,547

Top 10 Owners ‐ Containerships(46.2% of Total Fleet)

CambridgeAcademy ofTransport

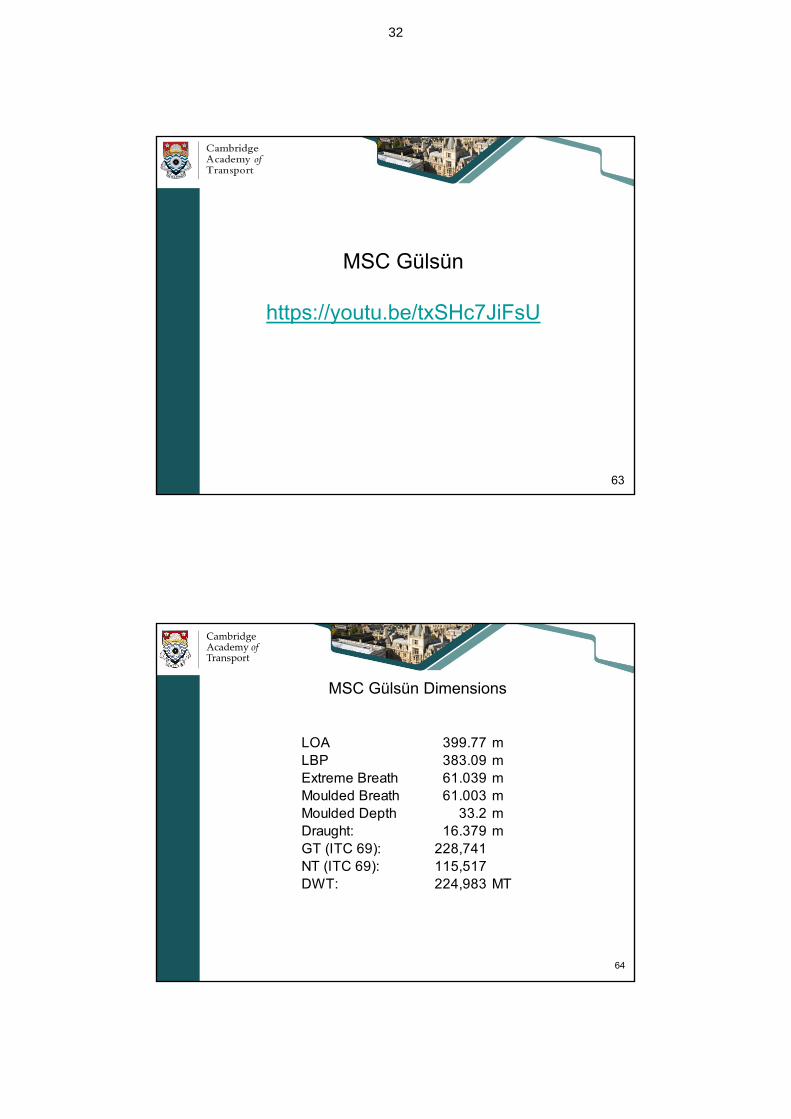

Largest Container Ship…for now!

62“MSC Gülsün” Launched July 2019 224,983 dwt LOA400m

31

MSC Gülsün

https://youtu.be/txSHc7JiFsU

63

CambridgeAcademy ofTransport

MSC Gülsün Dimensions

64

LOA 399.77 mLBP 383.09 mExtreme Breath 61.039 mMoulded Breath 61.003 mMoulded Depth 33.2 mDraught: 16.379 mGT (ITC 69): 228,741NT (ITC 69): 115,517DWT: 224,983 MT

32

CambridgeAcademy ofTransport

65

Top 20 Operator-Owner Container Fleets – 2017No. Ships TEUs

Maersk 259 1,730,630MSC 201 1,248,061Hapag-Lloyd 122 1,058,186China COSCO Shipping 152 1,053,506CMA-CGM 133 1,027,721Evergreen 105 543,705OOCL 56 436,482NYK 52 338,694Hamburg-Sud 46 308,334PIL 117 299,024Mitsui OSK 32 252,419Yang Ming 47 224,319K-Line 30 222,540HMM 25 186,193Wan Hai 73 172,871Zim 18 110,839China Merchants Grp 29 105,264SM Line 18 102,452Sinokor 36 101,986Arkas 50 93,263

Source: Clarksons SIN September 2017

• 52.5% of Top 20 Operator-Owner TEUs in the control of European Companies

• 41.5% of TEUs in the control of Asia/Far East Companies

• Top 20 control 46.1% of the World Fleet

• Until 2012, European Operators owned more capacity than Asian Operators

• By 2013, Asian Operator-Owners controlled more than 50%.

• As of mid-2015, European Owner-Operators have reversed the trend

CambridgeAcademy ofTransport

66

Top 20 Operator-Owner Container Fleets - 2018

Source: Clarksons SIN September 2018

• 55.5% of Top 20 Operator-Owner TEUs in the control of European Companies

• 44.5% of TEUs in the control of Asia/Far East Companies

• Top 20 control 51.9% of the World Fleet

• Until 2012, European Operators owned more capacity than Asian Operators

• By 2013, Asian Operator-Owners controlled more than 50%.

• European Owner-Operators have reversed the trend since mid-2015 but gap closed in 2018.

No. teuMaersk 328 2,394,312China COSCO Shipping 231 1,871,922MSC 209 1,278,354CMA CGM 145 1,119,254Hapag-Lloyd 112 1,031,575ONE* 121 938,357Evergreen 115 575,078PIL 124 392,571Yang Ming 47 224,319HMM 25 196,791Wan Hai 77 180,879China Merchants 31 129,544Zim 18 110,839Sinokor 50 107,931Arkas 50 93,263IRISL 24 85,872Quanzhou Ansheng 28 78,068KMTC 36 68,315SITC 49 67,369Zhonggu Shipping 20 62,639

33

CambridgeAcademy ofTransport

Top 20 Charterer-Owner Container Fleets

67Source: Clarksons SIN September 2018

• 41.3% of Top 20 Charterer-Owners TEUs are in control of 8 KG Funds based in Germany (down from 62.1% & 11 in 2016 and 53.8% and 9 in 2017)

• These 8 companies fleets are about 13.4% of the World total, down ~1% from previous year

• The Top 20 Charterer-Owners control about 27.3% of the World Fleet, upa bit

• KG Companies and Charterer-Owners share of the World total have been declining in recent years.

No. teu KGSeaspan 112 909,900 3

C-P Offen 63 487,532 3

Costamare 73 477,544Peter Dohle 98 408,145 3

Danaos Shipping 58 347,180Zodiac Maritime 42 338,751Shoei Kisen Kaisha 45 327,345BoCom Leasing 28 317,882Rickmers 36 230,849 3

E.R. Schiffahrt 37 221,835 3

Norddeutsche 44 221,061 3

Fredriksen Group 25 202,046Schulte Group 45 190,802 3

Eastern Pacific Shipping 26 185,851Navios Maritime 42 183,823MPC Group 80 176,096 3

Technomar 35 164,261Minsheng Bank 10 142,920SinOceanic Shipping 13 133,665Lomar Kaiun 18 123,361

CambridgeAcademy ofTransport

Container Operators Deployed Fleets (1/9/2018)

68

No. teu No. teu No. teuMaersk 328 2,394,312 389 1,585,753 717 3,980,065 7 77,034MSC 209 1,278,354 278 1,907,118 487 3,185,472 11 242,000China COSCO Shippin 231 1,871,922 206 895,883 437 2,767,805 17 261,020CMA CGM 145 1,119,254 343 1,514,238 488 2,633,492 17 238,400Hapag-Lloyd 112 1,031,575 111 535,558 223 1,567,133ONE* 121 938,357 110 614,575 231 1,552,932 13 181,870Evergreen 115 575,078 86 580,800 201 1,155,878 16 111,280Yang Ming 47 224,319 60 423,034 107 647,353 10 28,000PIL 124 392,571 8 42,776 132 435,347 5 47,800HMM 25 196,791 47 223,731 72 420,522Zim 18 110,839 64 284,272 82 395,111Wan Hai 77 180,879 33 94,366 110 275,245 8 22,400KMTC 36 68,315 38 90,343 74 158,658X-Press Feeders 31 51,708 49 82,444 80 134,152SITC 49 67,369 27 36,595 76 103,964 12 20,466SM Line 21 116,711 21 116,711IRISL 24 85,872 - 24 85,872 4 57,904Quanzhou Ansheng 28 78,068 -1 -698 27 77,370 25 38,880Arkas 50 93,263 -4 -16,078 46 77,185Zhonggu Shipping 20 62,639 2 8,074 22 70,713 10 18,728

TOTAL 3,657 19,840,980

Owned Chartered Total Deployed On Order

Source: Clarkson SIN 94% of World fleet

34

CambridgeAcademy ofTransport

69

Key Features of Container Shipping – 5

NVOCC

• Non-Vessel Operating Common Carriers are companies which do not own nor operate vessels but none-the-less offer container space to shippers.

– NVOCCs lease space from existing “carriers” on a wholesale basis

– To the customer, they behave like a carrier as they will issue bills of lading in their own name.

CambridgeAcademy ofTransport

70

The Big Picture

Historical Supply/Demand

35

CambridgeAcademy ofTransport

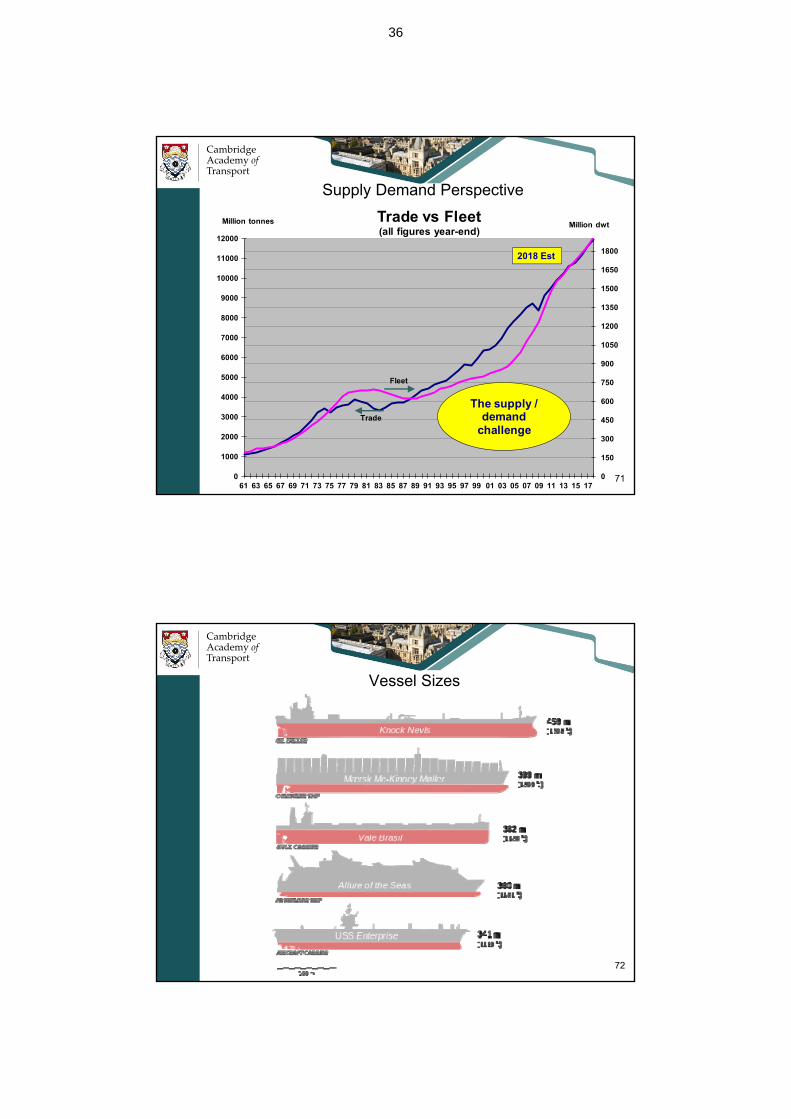

Supply Demand Perspective

0

150

300

450

600

750

900

1050

1200

1350

1500

1650

1800

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

11000

12000

61 63 65 67 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17

Trade vs Fleet(all figures year-end)

Trade

Fleet

The supply / demand

challenge

Million tonnes Million dwt

71

2018 Est

CambridgeAcademy ofTransport

Vessel Sizes

72

36

CambridgeAcademy ofTransport

73

Conclusion

What you should know about ShippingWhat is Shipping

What is Shipowning

CambridgeAcademy ofTransport

74

What You Should Know About Shipping

• Shipping is one of the most international of industries– shrouded in mystique– dominated by private companies– many small players– many rules govern safety and pollution, but few rules govern its

commercial practice• The World is a shrinking market place

– can’t work without reliance upon shipping– container shipping has done more to achieve “globalisation” than

even the microchip

• The industry is going through a period of change

– a decade of relentless growth has tracked World trade

– the Credit Crisis of 2008/9 has stalled demand

– a potential gap between supply and demand will influence revenues

37

CambridgeAcademy ofTransport

75

Seaborne Trade

Shipping

Finance

Insurance

Shipbuilding

Crew

Ports

• Debt• Equity• Lease• ….

• H & M• P & I• War• …. • Steel

• Engines• Cargo Gear• ….

• Training• Employment• Certification• ….

• Tugs• Pilots• Dreding• Customs• Terminals• Containers• ….

Shipping is all of this and more…

OperationsChartering

HULL & MACHINERYPROTECTION & INDEMNITY

What is Shipping?

CambridgeAcademy ofTransport

76

The ShipActual Owner

Seller

Sell the ship

S&PMarket

Buyer

Sales Contract

Lease/Bareboat

CapitalMarkets

Bareboat Charter

Lessee

Lessor

Time charter

PeriodMarket

Time Charter

Owner

Charterer

Carry Cargo

FreightMarket

Voyage Charter

Owner

Charterer

NewbuildingMarket

ShipYard

Buy NewShip Newbuilding

Contract

Scrap theShip

ScrapMarket

DemolitionContract

ScrapYard

OPERATIONS

FINANCIAL

What Is Shipowning?

38