singapore property weekly issue 153.pdf

TRANSCRIPT

ContributeDo you have articles and insights and articles that you’d like to share with thousands of readers interested in the Singapore property market? Send them to us at [email protected], and if they’re good enough, we’ll publish them here, on our blog and even on Yahoo! News.

AdvertiseWant to get your brand, product, service or property listing out to thousands of Singapore property investors at a very reasonable cost? Head over to www.propwise.sg/advertise/ to find out more.

CONTENTS

p2 The “Resurrection” of Property Prices

p6 Singapore Property News This Week

p12 Resale Property Transactions

(April 7 – April 15)

Welcome to the 153th edition of the Singapore Property Weekly.

Hope you like it!

Mr. Propwise

FROM THE

EDITOR

SINGAPORE PROPERTY WEEKLY Issue 153

Page | 2Back to Contents

By Property Soul (guest contributor)

The Easter holiday celebrates the

resurrection of Jesus Christ from death on the

third day, a critical belief in Christianity. By

coincidence, this past Easter also marked the

“resurrection” of the purchase price for a

private property bought in the mid-1990s by a

friend of my father-in-law, i.e. the current

market prices have finally recovered to the

level that he bought it at.

I am not surprised that it took him almost 20

years to break-even. I just wonder how many

people are comfortable telling others how

long it took for their overpriced property to

“return to life” again.

The “Resurrection” of Property Prices

SINGAPORE PROPERTY WEEKLY Issue 153

Page | 3Back to Contents

Why the Property Price Index can be

deceiving

The URA‟s Property Price Index (PPI) shows

that the property price peak in the second

quarter of 1996 was surpassed by a new high

sometime in the middle of 2010. However, the

PPI is an index that only shows the average

price of all caveats lodged when buyers

exercise their Option to Purchase. It monitors

the general price movement of all private

residential properties, but hides all the

deviations from the average PPI.

PPI includes all the transacted units from

property new launches sold at „future prices‟

by the developers. It also encompasses

resale units from relatively new projects that

are able to sell at higher prices. There are

relatively few transactions from projects that

are 15, 20 years or even older. After all, with

so many new launches coming up every

quarter, who cares about such old

developments?

What goes up must come down

It is naïve to believe that prices can rise

indefinitely. The market never goes up or

down forever. It is destined to change course

at a certain point of time.

Nothing can defy the law of gravity: If you

drop a ball from a height, it will bounce back

from the ground and reach for the sky again.

And the higher it bounces, the nearer to the

point where you will see the ball falling again.

Forget the sales talk about how property

prices can only go up, how property investors

always prosper in the long-term, and how this

time is going to be different.

SINGAPORE PROPERTY WEEKLY Issue 153

Page | 4Back to Contents

The Japanese property bubble that burst in

the late 1980s started two lost decades (and

still counting). The question is: How long are

you prepared to wait to see the resurrection

of your purchase price?

How history repeats itself

Many people are asking: What will happen to

the Singapore property market?

If you want to understand the financial

markets and how it will turn out, don‟t study

economics or finance. You should delve into

history. For history doesn't only show you how

to read the present, it also tells you the future

from the past.

Don't just look at the name and date of a

historical event. Read the details. You will find

that there are many lessons to be learnt

because there are so many up and downs in

the history of the property industry.

If the history of Singapore is not long enough,

look outside the country. Look at what has

happened in the property markets in any

country in Asia, US or Europe.

If the property market has not given you too

many hints, you can look outside of real

estate to study the history of different market

bubbles. We have experienced many booms

in our history: the railway industry in the

1840s, the commodity market in the early

1970s, technology stocks in the late 1990s,

and the US housing market in the 2000s.

These booms all developed into speculative

manias, before they finally collapsed and

caused an economic upheaval.

SINGAPORE PROPERTY WEEKLY Issue 153

Page | 5Back to Contents

Technology evolves over time. Things change

in the long run. But the ignorance and greed

of human nature remain the same.

Once you understand the past, you can

explain why things are where they are now.

Once you know what is going on at present, it

is not difficult to tell what will happen in the

near future.

Stay calm, be intact

I am not a doomsayer. But please keep in

mind that:

When the market is hot, there is no need

to be too excited. Likewise, when the

market is gloomy, it is not necessary to

be too pessimistic.

Buy new launch projects before prices go up

again?

All overseas properties promise handsome

profit?

Any time is a good time to buy property?

Property prices will always go up?

Property is a safe investment for the long-

term?

Whenever you hear people making these

statements, you don't even bother to argue.

You can just keep quiet and smile.

By guest contributor Property Soul, a

successful property investor, blogger, and

author of the newly released No B.S. Guide to

Property Investment.

SINGAPORE PROPERTY WEEKLY Issue 153

Singapore Property This Week

Page | 6Back to Contents

Residential

100 of 131 units in The Sorrento sold

100 of the 131 units have been sold in The

Sorrento – a five-storey freehold

condominium on West Coast Road which

offers one-to three-bedroom units from 441 to

1,808 sq ft and is expected to be granted the

temporary occupation permit (TOP) in

1Q2015. The rapid sales were the result of

attractive prices ($1,380 to $1,600 psf) and

the sense of exclusivity offered through the

condo‟s small scale and freehold status.

Other developments such as Icon@Pasir

Panjang, Seasuites, Village@Pasir Panjang

and Whitehaven have also achieved

transacted prices of $1,600-1,700 psf.

(Source: Business Times)

11,000 Singaporean families purchased

exec condos from 4Q2010 to 4Q2013

According to Minister for National

Development Khaw Boon Wan, 11,000

Singaporean households purchased

executive condominiums (EC) from Q4 2010

to Q4 2013. Approximately 86 percent of the

buyers are HDB residents and 55 percent are

second-timer families. Due to the increase of

the income ceiling for ECs in 2011 – from

$10,000 to $12,000, there have been

changes in terms of EC buyers‟ profile over

SINGAPORE PROPERTY WEEKLY Issue 153

Page | 7Back to Contents

that one-year period, where the share of

second-timers increased from 43 percent to

57 percent and those aged from 35 to 44

increased from 35 percent to 43 percent.

(Source: Business Times)

HDB resale prices dropped 1.6% in Q1

2014

Resale prices of HDB flats have decreased

by 1.6 percent in Q1, with the number of

transactions falling 5 percent to 3,781,

making it the third consecutive quarter where

prices slid. According to ERA Realty,

government measures of reducing the

mortgage servicing ratio from 35 percent to

30 percent limited buyers from owning more

expensive flats. Furthermore, the minimum

three-year waiting period for newly minted

permanent residents before they can

purchase resale flats, the availability of two-

room build-to-order (BTO) flats for singles

and the cessation of reporting cash-over-

valuation (COV) held back market activities.

Due to the slowdown in resale activities, the

sub-letting market has seen improvement

where subletting transactions rose 17 percent

quarter-on-quarter in Q1 to 8,485.

(Source: Business Times)

Increase in foreigners’ proportion of home

purchases

Transactions of private home purchases in

Q1 dropped to 2,076 units, seeing

Singaporeans‟ share falling to 70 percent

from 73 percent in Q1 2013, PRs‟ share rising

to 19 percent from 16 percent in Q4 2013 and

foreigners‟ share – mainly coming from

mainland Chinese, Malaysians, Indonesians

and Indians – climbing up to 10 percent from

9 percent in Q4 2013.

SINGAPORE PROPERTY WEEKLY Issue 153

Page | 8Back to Contents

Due to the additional buyer‟s stamp duty and

the high home ownership rate, purchasing

activities among Singaporeans have slowed

down, while with the regulation that new PRs

must wait for three years before being

allowed to purchase public flats, those who

are in urgent need of accommodation started

setting their eyes on the private housing

market.

(Source: Business Times)

51 percent of units purchased by HDB

owners were below 800 sq ft

A total of 892 non-landed private homes were

purchased by HDB owners in Q1 2014, 453

units or 51 percent of which were of areas of

up to 800 sq ft, showing an increase from 44

percent in 2013. On the contrary, in terms of

the equivalent area, merely 29 percent of the

1,014 non-landed private homes were

acquired by private home owners. Smaller

units are preferable among those with HDB

addresses as the required investment sum is

more affordable and they can benefit from the

progressive payment scheme if they buy in

the primary market, where 581 units or 65

percent of the total 892 private homes were

purchased from developers in Q1.

(Source: Business Times)

0.7 percent drop in private residential

rentals quarter-on-quarter in 1Q2014

On a quarter-on-quarter basis, private

housing rentals fell 0.7 percent for the second

consecutive quarter, as a consequence of the

growth in completed private homes, more

restriction on foreign tenants in Singapore

and a stricter property tax system. Private

residential completions are estimated to

reach 17,138 units in 2014, higher than the

SINGAPORE PROPERTY WEEKLY Issue 153

Page | 9Back to Contents

13,150 units in 2013, whereas demand will

not match this supply due to tighter

regulations on hiring foreign executives.

Additionally, a stricter property tax policy took

effect from Jan 1, 2014, stating that landlords

can no longer claim vacancy refunds on

property tax. Overall, consultants estimate a

5-10 percent dip in private housing rentals for

the full year.

(Source: Business Times)

Commercial

Lian Beng purchases 70,000 sq ft at 24

Leng Kee Road for $46.2m

A site of approximately 70,000 sq ft at 24

Leng Kee Road has been purchased by Lian

Beng Group for $46.2m. It is expected that

the area will be developed to prepare for the

entry to the automotive business of Wealth

Assets Pte Ltd – a joint venture company

between Lian Beng Group and parallel

importer Vincar. The tender attracted around

a dozen bidders as the Leng Kee

Road/Alexandra Road area is regarded as

Singapore‟s key auto belt.

(Source: Business Times)

15% increase in Singapore’s office rents

this year

Office rents in Singapore are anticipated to

increase to 15 percent this year owing to the

rise in demand, where international

companies such as Cargill Inc and Bordier &

Cie are having their offices in the central

business district. Additionally, landlords are

getting more bargaining power due to the lack

of completed developments in 2015 and the

increase in office occupancy rates – which,

SINGAPORE PROPERTY WEEKLY Issue 153

Page | 10Back to Contents

according to DTZ, rose to 95.1 percent from

the last quarter. Compared to the previous

quarter, rents in Marina Bay area rose by 4.5

percent, while compared to the same period

in 2012, rents in the central business district

increased by 8.4 percent in 4Q2013.

(Source: Business Times)

Two units in Orchard Towers and one unit

in Marine Parade for sale

Two commercial units in Orchard Towers and

one in Marine Parade Central are open for

sale, with no advanced indicative prices but

guiding prices from sales of shops nearby.

The freehold units in Orchard Towers occupy

a strata area of approximately 8,105 sq ft,

covering the ground floor and the basement.

A third-floor unit in Orchard Towers was sold

for $6,636 psf last year. With 62 years

remaining on the lease, the unit in Marine

Parade Central occupies a strata area of

about 25,833 sq ft over the ground and

second floors of Block 87. Sales of ground

floor and basement shops in nearby The Flow

ranged from $4,008 to $5,789 psf during the

past nine months.

(Source: Business Times)

Retail rentals in Central Region showed

0.3 percent drop: URA

According to the Urban Redevelopment

Authority (URA)‟s data, there was a decline of

0.3 percent in rentals at retail malls in the

Central Region, covering retailers and non-

shop space such as food and beverage,

entertainment, and health and fitness in the

downtown area and city fringe.

SINGAPORE PROPERTY WEEKLY Issue 153

Page | 11Back to Contents

However, skepticism about the index‟s

reliability was raised as according to several

retailers, rentals have significantly increased

in the past three years. URA‟s data set may

not have captured the full scene as it does

not look at suburban malls in Jurong East,

Tampines and Bedok.

(Source: Business Times)

Annual supply of 2.1m sq m of industrial

space over the next three years

According to JTC Corp‟s data, there is an

average annual supply of industrial space of

2.1 million square metres (sq m) coming on-

stream over the next three years, of which 28

percent is multiple-user factory space, 37

percent is single-user factory space, 25

percent is warehouse space, and the rest

business park space. This is double of the

annual average demand. Concerns have

been raised as there is no dearth in industrial

space and the appropriate use of industrial

space needs to be restructured, in order to

capture more manufacturing companies.

(Source: Business Times)

SINGAPORE PROPERTY WEEKLY Issue 153

Page | 12Back to Contents

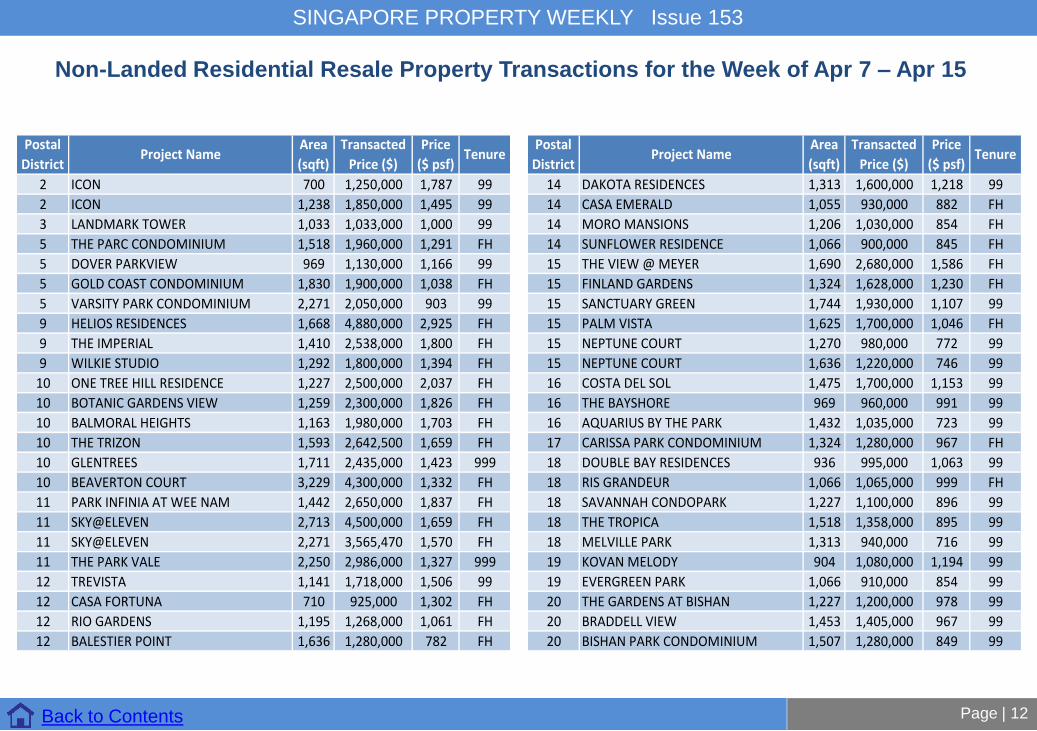

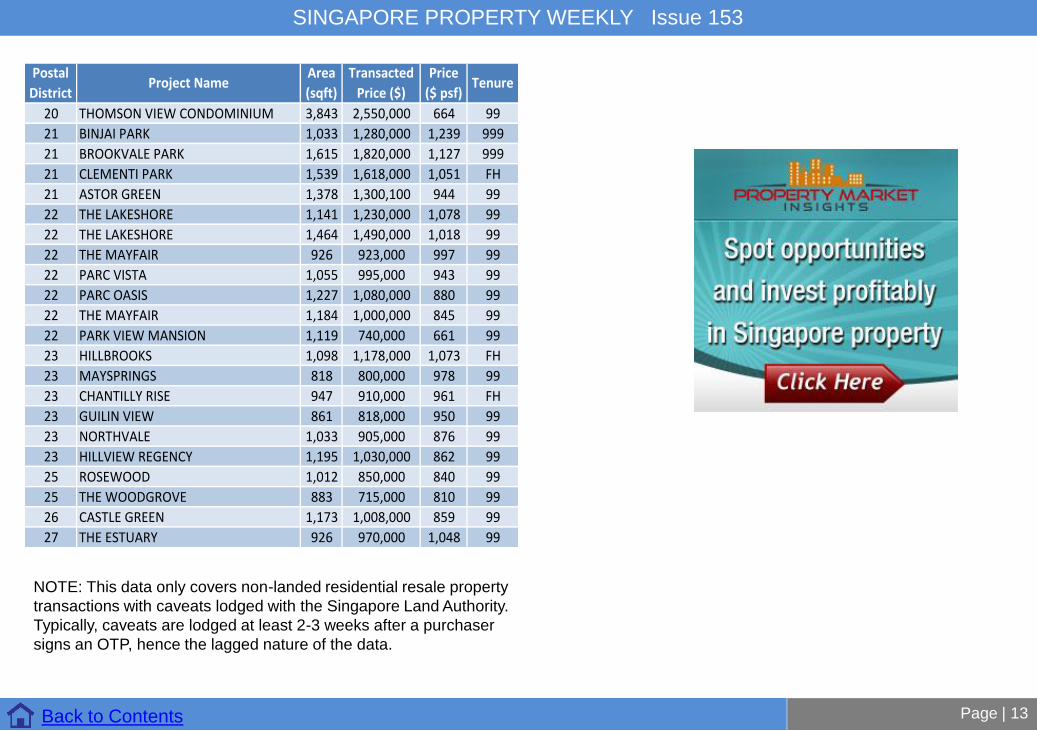

Non-Landed Residential Resale Property Transactions for the Week of Apr 7 – Apr 15

Postal

DistrictProject Name

Area

(sqft)

Transacted

Price ($)

Price

($ psf)Tenure

2 ICON 700 1,250,000 1,787 99

2 ICON 1,238 1,850,000 1,495 99

3 LANDMARK TOWER 1,033 1,033,000 1,000 99

5 THE PARC CONDOMINIUM 1,518 1,960,000 1,291 FH

5 DOVER PARKVIEW 969 1,130,000 1,166 99

5 GOLD COAST CONDOMINIUM 1,830 1,900,000 1,038 FH

5 VARSITY PARK CONDOMINIUM 2,271 2,050,000 903 99

9 HELIOS RESIDENCES 1,668 4,880,000 2,925 FH

9 THE IMPERIAL 1,410 2,538,000 1,800 FH

9 WILKIE STUDIO 1,292 1,800,000 1,394 FH

10 ONE TREE HILL RESIDENCE 1,227 2,500,000 2,037 FH

10 BOTANIC GARDENS VIEW 1,259 2,300,000 1,826 FH

10 BALMORAL HEIGHTS 1,163 1,980,000 1,703 FH

10 THE TRIZON 1,593 2,642,500 1,659 FH

10 GLENTREES 1,711 2,435,000 1,423 999

10 BEAVERTON COURT 3,229 4,300,000 1,332 FH

11 PARK INFINIA AT WEE NAM 1,442 2,650,000 1,837 FH

11 SKY@ELEVEN 2,713 4,500,000 1,659 FH

11 SKY@ELEVEN 2,271 3,565,470 1,570 FH

11 THE PARK VALE 2,250 2,986,000 1,327 999

12 TREVISTA 1,141 1,718,000 1,506 99

12 CASA FORTUNA 710 925,000 1,302 FH

12 RIO GARDENS 1,195 1,268,000 1,061 FH

12 BALESTIER POINT 1,636 1,280,000 782 FH

Postal

DistrictProject Name

Area

(sqft)

Transacted

Price ($)

Price

($ psf)Tenure

14 DAKOTA RESIDENCES 1,313 1,600,000 1,218 99

14 CASA EMERALD 1,055 930,000 882 FH

14 MORO MANSIONS 1,206 1,030,000 854 FH

14 SUNFLOWER RESIDENCE 1,066 900,000 845 FH

15 THE VIEW @ MEYER 1,690 2,680,000 1,586 FH

15 FINLAND GARDENS 1,324 1,628,000 1,230 FH

15 SANCTUARY GREEN 1,744 1,930,000 1,107 99

15 PALM VISTA 1,625 1,700,000 1,046 FH

15 NEPTUNE COURT 1,270 980,000 772 99

15 NEPTUNE COURT 1,636 1,220,000 746 99

16 COSTA DEL SOL 1,475 1,700,000 1,153 99

16 THE BAYSHORE 969 960,000 991 99

16 AQUARIUS BY THE PARK 1,432 1,035,000 723 99

17 CARISSA PARK CONDOMINIUM 1,324 1,280,000 967 FH

18 DOUBLE BAY RESIDENCES 936 995,000 1,063 99

18 RIS GRANDEUR 1,066 1,065,000 999 FH

18 SAVANNAH CONDOPARK 1,227 1,100,000 896 99

18 THE TROPICA 1,518 1,358,000 895 99

18 MELVILLE PARK 1,313 940,000 716 99

19 KOVAN MELODY 904 1,080,000 1,194 99

19 EVERGREEN PARK 1,066 910,000 854 99

20 THE GARDENS AT BISHAN 1,227 1,200,000 978 99

20 BRADDELL VIEW 1,453 1,405,000 967 99

20 BISHAN PARK CONDOMINIUM 1,507 1,280,000 849 99

SINGAPORE PROPERTY WEEKLY Issue 153

Page | 13Back to Contents

NOTE: This data only covers non-landed residential resale property

transactions with caveats lodged with the Singapore Land Authority.

Typically, caveats are lodged at least 2-3 weeks after a purchaser

signs an OTP, hence the lagged nature of the data.

Postal

DistrictProject Name

Area

(sqft)

Transacted

Price ($)

Price

($ psf)Tenure

20 THOMSON VIEW CONDOMINIUM 3,843 2,550,000 664 99

21 BINJAI PARK 1,033 1,280,000 1,239 999

21 BROOKVALE PARK 1,615 1,820,000 1,127 999

21 CLEMENTI PARK 1,539 1,618,000 1,051 FH

21 ASTOR GREEN 1,378 1,300,100 944 99

22 THE LAKESHORE 1,141 1,230,000 1,078 99

22 THE LAKESHORE 1,464 1,490,000 1,018 99

22 THE MAYFAIR 926 923,000 997 99

22 PARC VISTA 1,055 995,000 943 99

22 PARC OASIS 1,227 1,080,000 880 99

22 THE MAYFAIR 1,184 1,000,000 845 99

22 PARK VIEW MANSION 1,119 740,000 661 99

23 HILLBROOKS 1,098 1,178,000 1,073 FH

23 MAYSPRINGS 818 800,000 978 99

23 CHANTILLY RISE 947 910,000 961 FH

23 GUILIN VIEW 861 818,000 950 99

23 NORTHVALE 1,033 905,000 876 99

23 HILLVIEW REGENCY 1,195 1,030,000 862 99

25 ROSEWOOD 1,012 850,000 840 99

25 THE WOODGROVE 883 715,000 810 99

26 CASTLE GREEN 1,173 1,008,000 859 99

27 THE ESTUARY 926 970,000 1,048 99