smart grid aspects of the winter package: facilitating a flexible retail market

Upload: funseam-fundacion-para-la-sostenibilidad-energetica-y-ambiental

Post on 07-Apr-2017

46 views

TRANSCRIPT

Energy ENER B3Energy

SMART GRID ASPECTS OF THE WINTER PACKAGE:

FACILITATING A FLEXIBLE RETAIL MARKET

Kostas STAMATIS

Directorate-General for Energy

European Commission

WORKSHOP

“DEFINING SMART GRIDS: CONDITIONS FOR SUCCESSFUL IMPLEMENTATION”

Session 1: Technical and regulatory aspects and recommendations for effective

smart grids deployment under the provisions of the winter package

Barcelona, 9th February 2017

European cooperation Network on Energy Transition in Electricity

Energy ENER B3

Recent policy drivers

Winter package

Electricity market and consumers

Renewables & bioenergy

sustainability

Energy Efficiency Directive

Energy efficiency of buildings

Ecodesign

Governance

....

Energy Union

Energy ENER B3

Market design not fit for VRES E generation

Energy ENER B3

Making demand side more flexible

Prosumers

Supplier

DSO TSO

Power exchange market

Supply&flexibility

Balancing Market /

Ancillary services

Commercial domain - Supply

Regulated domain

Generator

Flexibility purchase contract

Mutual exchange of operational and contractual data

Flexibilityprocurement

Grid access & Generation management

Commercial domain - Flexibility

Possible relations between market roles

Information exchange

Financial adjustment mechanism

BRP

BRP

Aggregator

Distribution network constraint

management

Smart metering and

data

DSOs to use flexibility and

DSO/TSO

Aggregators and access to

the market

Smart Grids Task Force (2015)

Energy ENER B3

Roll out of Electricity

smart metering by 2020:

22 CBAs, 17 MS: large-scale

roll-out

~ 72% EU consumers

195 million meters

€ 35 billion

Smart metering: the picture today

ref. COM(2014) 356; SWD(2014) 189

Energy ENER B3

Current situation and problem:

• Smart metering projects are going ahead…

roll out of smart meters according to Electricity Directive

(+CBA 80% 2020)

full roll out of smart meters only planned in 17 MS

(+2 selective roll-outs)

• …however problems still exist

not all fit for purpose (lack of functions & interoperability)

enabling technologies not widely accessible

Smart metering: problems identified

Energy ENER B3

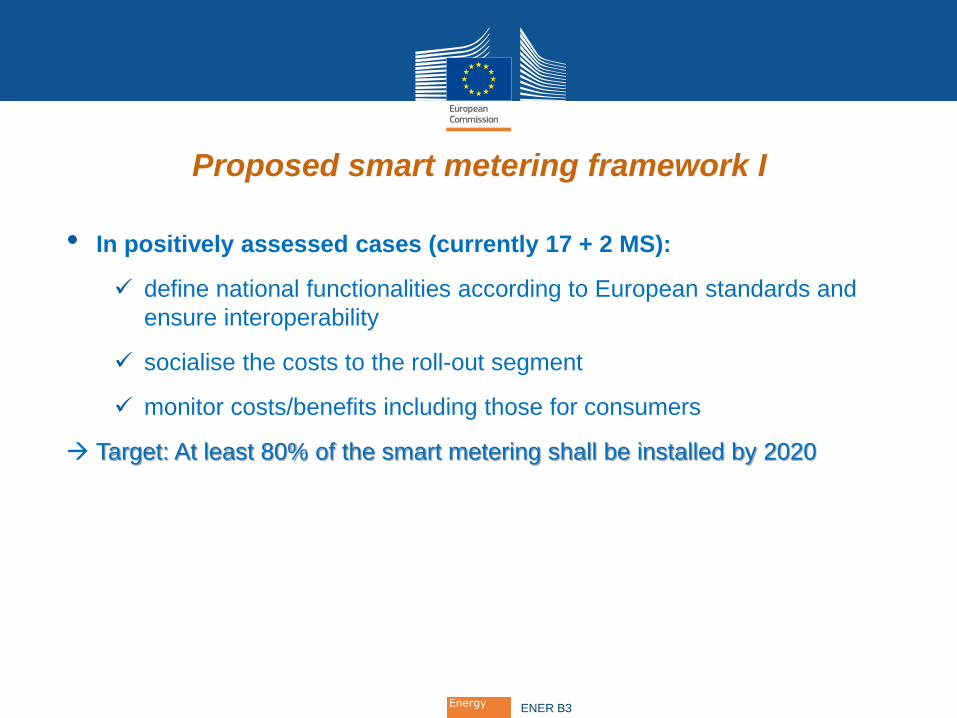

• In positively assessed cases (currently 17 + 2 MS):

define national functionalities according to European standards and

ensure interoperability

socialise the costs to the roll-out segment

monitor costs/benefits including those for consumers

Target: At least 80% of the smart metering shall be installed by 2020

Proposed smart metering framework I

Energy ENER B3

• In Member States which do not intend still to go ahead:

right to request a smart meter - to be installed within 3 months with a set

of minimum functionalities defined by Member State

cost should be supervised by Member States and borne by the end user

Member States shall periodically assess changes in technology and

assumptions of CBA

when CBA becomes positive, Member States to roll-out 80% within 8

years

Proposed smart metering framework II

Energy ENER B3

• Proposed smart metering functionalities:

provide near real time information to consumer on actual

consumption in order to support energy services

follow security and data protection EU requirements

fit for active consumers

provide data to be available to consumers or service

providers of their choice

enable measurement and settlement at the same time

intervals as the imbalance period in the national market

Appropriate advice and information to consumers on the

full potential of the smart meter and privacy issues

Proposed smart metering framework III

Functionalities

Interoperability

Connectivity

Fit-for-purpose

smart metering

Energy ENER B3

Current situation and problem:

• Fair market access for demand response according to EED…

General principles and rules to ensure participation of demand

response in all markets

• …but market barriers continue to exist

service providers (aggregators) are effectively banned in some MS

many markets remain effectively closed to DR

granular price signals are not passed onto consumers

consumers do not always have access to markets

Demand response: problems identified

Energy ENER B3

Enabling demand response:

Entitlement to a dynamic electricity price contract

Transfer Art 15.8 EED to electricity directive and

Remove market barriers for aggregators

Introduce additional rules for flexible markets (electricity regulation)

Enabling active consumers and energy communities:

Entitlement to all consumers to generate, self-consume, store or sell self-

generated electricity while ensuring non-discriminatory network tariffs

Proposed framework for DR and new services

Energy ENER B3

Currently activated demand response

15 GW activated through incentive based DR

6 GW activated through price based DR

Demand response activation 2030

Business as usual scenario

Activated: DR 35 GW

Net Benefit: 4.4 bn euro/annum

Policy scenario enabling price and incentive based DR

Activated: DR 52 GW

Net Benefit: 5.6 bn euro/annum

160 GWTheoretical demandresponse potential in 2030

100 GWTheoretical demand response potential today

21 GWDemand response activated today

Demand response potential and benefits

Energy ENER B3

Current situation:

• Smart metering systems, in 17 (+2) Member States more granular

consumption data and new services

• Existing provisions in Electricity Directive not fit for new developments

Proposed measures:

Define responsibilities for parties involved in data handling

Set principles on non-discriminatory and transparent access to data

Certification and compliance of the parties responsible for data handling,

including DSOs

Standardised data format

Creating a level playing field for access to data

Support active

consumer and new

services

Facilitate switching

and billing

Energy ENER B3

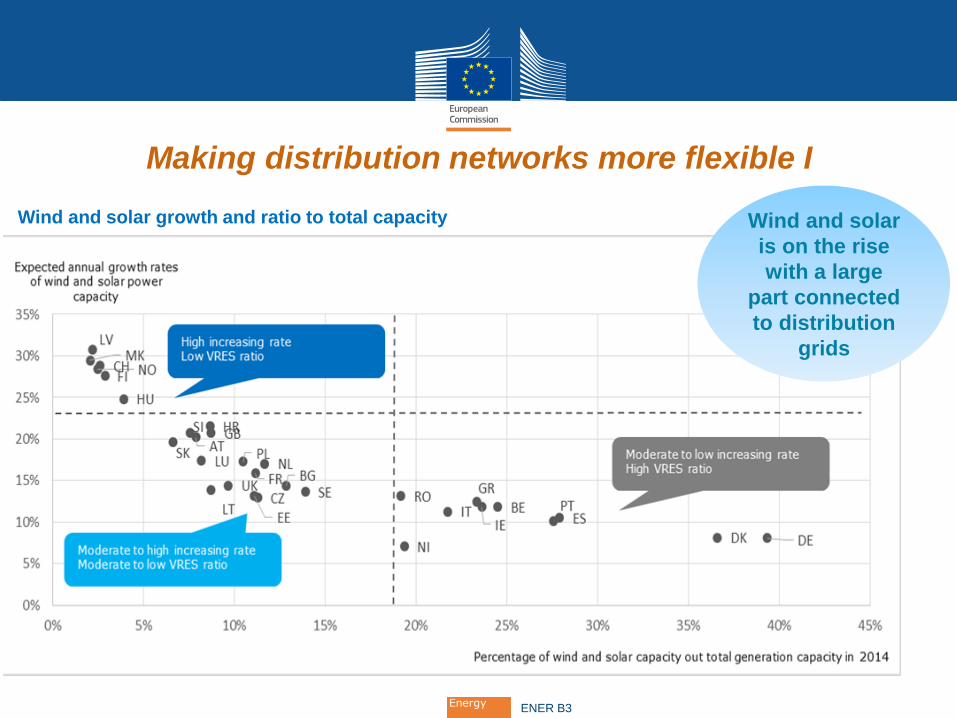

Wind and solar growth and ratio to total capacity

Making distribution networks more flexible I

Wind and solar

is on the rise

with a large

part connected

to distribution

grids

Energy ENER B3

Problems identified:

• Current framework at EU or national level does not:

... allow DSOs to be flexible and cope with variable RES and new loads

... clarify DSO role in specific tasks

Proposed measures:

Enabling framework for DSOs to procure and use flexibility

DSO tasks in storage, EVs infrastructure and data management

Cooperation between DSOs and TSOs alongside a EU DSO entity

Lower grid

costs and

tariffs

Neutrality of

DSOs in new

tasks

Making distribution networks more flexible II

Energy ENER B3

Current situation and problem:

− In most cases DSO remuneration favours network expansion solutions

− Diversity of distribution tariffs create different market conditions for distributed

resources across EU

Proposed measures:

EU-wide principles for distribution network tariffs

DSOs to prepare multiannual development plans

ACER recommendation and network code on network tariffs

Monitoring smart grid development and transparency of network tariffs

methodology and costs

Efficient grid

operation

and planning

Support

innovative

solutions

Facilitate the

integration of

distributed

resources

Distribution network tariffs and DSO remuneration

Energy ENER B3

https://ec.europa.eu/energy/

https://ec.europa.eu/energy/en/topics/markets-and-consumers/smart-grids-

and-meters

Energy ENER B3

European Commission

Technology Supply

ConsumersDSOsTSOsRegulators

ICT&Energy

•Ad-hoc expert working groups

High Level Steering Committee

30+ associations representing all stakeholders

350+ experts from national regulatory agencies and industrial market actors

9 DGs

European Smart Grids Task Force (SGTF)

https://ec.europa.eu/energy/en/topics/markets-and-consumers/smart-grids-and-meters/smart-grids-task-force

Energy ENER B3

Standards and interoperability

Data privacy, data protection

and cyber-security

Regulatory issues

Industrial policy and infrastructure

European Smart Grids Task Force is working on key challenges

Energy ENER B3

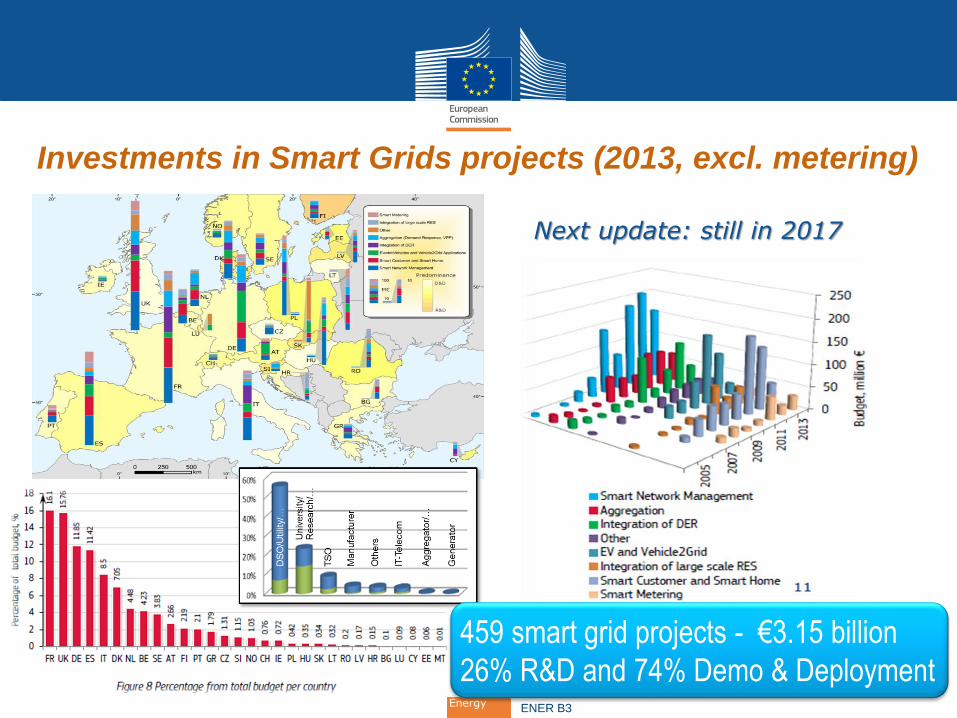

Investments in Smart Grids projects (2013, excl. metering)

459 smart grid projects - €3.15 billion

26% R&D and 74% Demo & Deployment

Next update: still in 2017