status and outlook for shale gas and tight oil …. energy information administration independent...

TRANSCRIPT

www.eia.gov U.S. Energy Information Administration Independent Statistics & Analysis

Status and outlook for shale gas and tight oil development in the U.S.

for Energy Symposium, University of Oklahoma, Price College Energy Institute March 05, 2013 | Norman, OK by Adam Sieminski, Administrator

EIA’s mission and main functions

Adam Sieminski , Energy Symposium, March 05, 2013 2

Independent Statistical and Analytical agency within the U.S. Department of Energy

– EIA collects, analyzes, and disseminates independent and impartial energy information to promote sound policymaking, efficient markets, and public understanding of energy and its interaction with the economy and the environment.

– By law, its data, analyses, and forecasts are independent of approval by any other officer or employee of the U.S. Government

[EIA] …is the gold standard for energy data around the world, and the accessibility of it is so much greater than other places – Dan Yergin, Platts Inside Energy

Annual Energy Outlook 2013 projections to 2040

Adam Sieminski , Energy Symposium, March 05, 2013 3

• Growth in energy production outstrips consumption growth

• Crude oil production rises sharply over the next decade

• Motor gasoline consumption reflects more stringent fuel economy standards

• The U.S. becomes a net exporter of natural gas in the early 2020s

• U.S. energy-related carbon dioxide emissions remain below their 2005 level through 2040

U.S. energy use grows slowly over the projection reflecting improving energy efficiency and slow, extended economic recovery

4

0

20

40

60

80

100

120

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

U.S. primary energy consumption quadrillion Btu

Adam Sieminski , Energy Symposium, March 05, 2013

History Projections 2011

36%

20%

26%

8% 8%

1%

32%

28%

19%

11%

9% 2%

Shares of total U.S. energy

Nuclear

Oil and other liquids

Liquid biofuels

Natural gas

Coal

Renewables (excluding liquid biofuels)

2000

23%

39%

24%

6% 8%

Source: EIA, Annual Energy Outlook 2013 Early Release

U.S. Shale Gas

5 Adam Sieminski , Energy Symposium, March 05, 2013

Theory Experiment Practice

These three drivers impact resource estimation metrics differently over time in an iterative process

Adam Sieminski , Energy Symposium, March 05, 2013 6

Geology

Technology

Economics

Resources in Place

Technically Recoverable Resources (TRR)

Economically Recoverable Resources (ERR)

Well-level data, incl. estimated ultimate recovery (EUR)

Thermal maturity Pressure Formation depth

Drilling costs Recompletions

Price of gas

P

Q

Adam Sieminski , Energy Symposium, March 05, 2013 7

• average initial production (IP) rate per well

• average decline curve (can vary by region and vintage)

• IP & decline curve define the Estimated Ultimate Recovery (EUR) per well

Other parameters

• drilling and operating costs

• number of active rigs

• how many wells a rig can drill (rig efficiency)

• well spacing

EIA’s focus is on the timing of production; the modeling focuses on these parameters

Technically recoverable natural gas resources reflect new information, a combination of assessments and EIA updates

8

U.S. dry gas resources trillion cubic feet

Source: EIA, Annual Energy Outlook 2013 Early Release AEO Edition

0

500

1000

1500

2000

2500

3000

2000 2005 2006 2007 2008 2009 2010 2011 2012 2013

2,327

304

543

1,479

*Alaska resource estimates prior to AEO2009 reflect resources from the North Slope that were not included in previously published documentation.

Unproved shale gas Unproved other gas (including Alaska* and offshore) Proved reserves (all types and locations)

Benchmark to USGS

2011 Marcellus Assessment

Adam Sieminski , Energy Symposium, March 05, 2013

U.S. wet natural gas proved reserves, 1980-2010

Adam Sieminski , Energy Symposium, March 05, 2013 9

trillion cubic feet

Source: U.S. Energy Information Administration

0

50

100

150

200

250

300

350

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010

U.S. Total

Lower 48 Onshore

Federal Offshore

Alaska

Adam Sieminski , Energy Symposium, March 05, 2013 10

EIA fits well production data to hyperbolic decline curves to estimate EUR

1985 vertical well

EUR=1.41 bcf

2004 vertical well EUR=0.46 bcf

2011 horizontal well EUR=1.76 bcf

Classic hyperbolic decline curve (Arps 1945):

Source: HPDI data from horizontal wells in the Newark East field in the Barnett Shale; EIA analysis

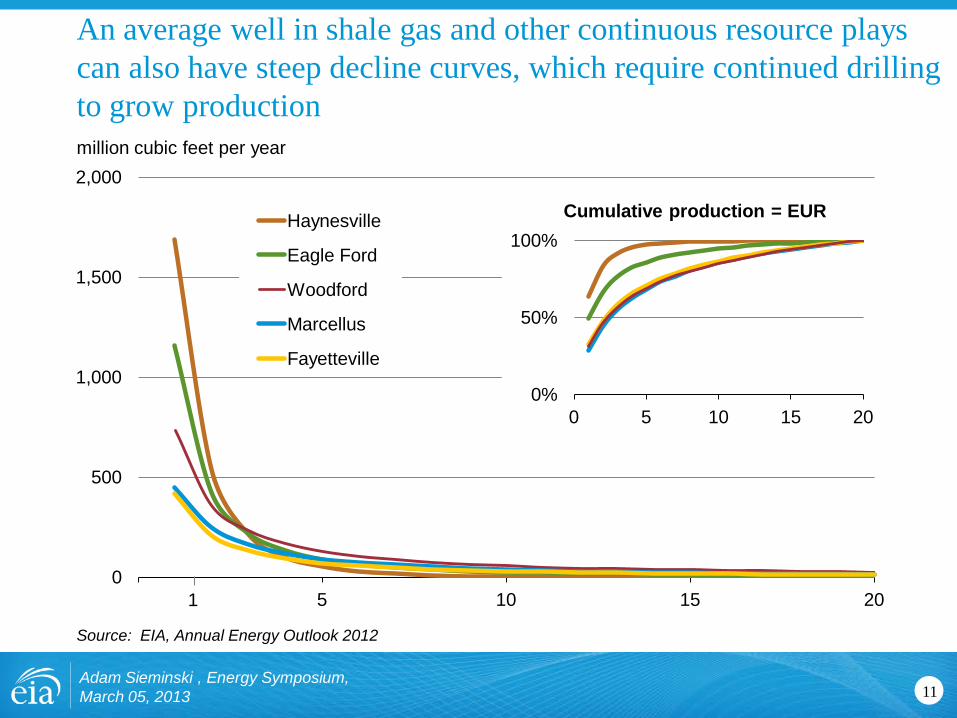

An average well in shale gas and other continuous resource plays can also have steep decline curves, which require continued drilling to grow production

11

0

500

1,000

1,500

2,000

0 5 10 15 20

Haynesville

Eagle Ford

Woodford

Marcellus

Fayetteville

million cubic feet per year

Source: EIA, Annual Energy Outlook 2012

1

0%

50%

100%

0 5 10 15 20

Cumulative production = EUR

Adam Sieminski , Energy Symposium, March 05, 2013

For example: Oil production by monthly vintage of wells in the Williston Basin

12

Source: DrillingInfo history through August 2012, EIA Short-Term Energy Outlook, February 2013 forecast

Adam Sieminski , Energy Symposium, March 05, 2013

Domestic production of shale gas has grown dramatically over the past few years

13

0

5

10

15

20

25

30

2000 2002 2004 2006 2008 2010 2012

Rest of US

Marcellus

Haynesville

Eagle Ford

Bakken

Woodford

Fayetteville

Barnett

Antrim

shale gas production (dry) billion cubic feet per day

Sources: LCI Energy Insight gross withdrawal estimates as of December 2012 and converted to dry production estimates with EIA-calculated average gross-to-dry shrinkage factors by state and/or shale play.

Adam Sieminski , Energy Symposium, March 05, 2013

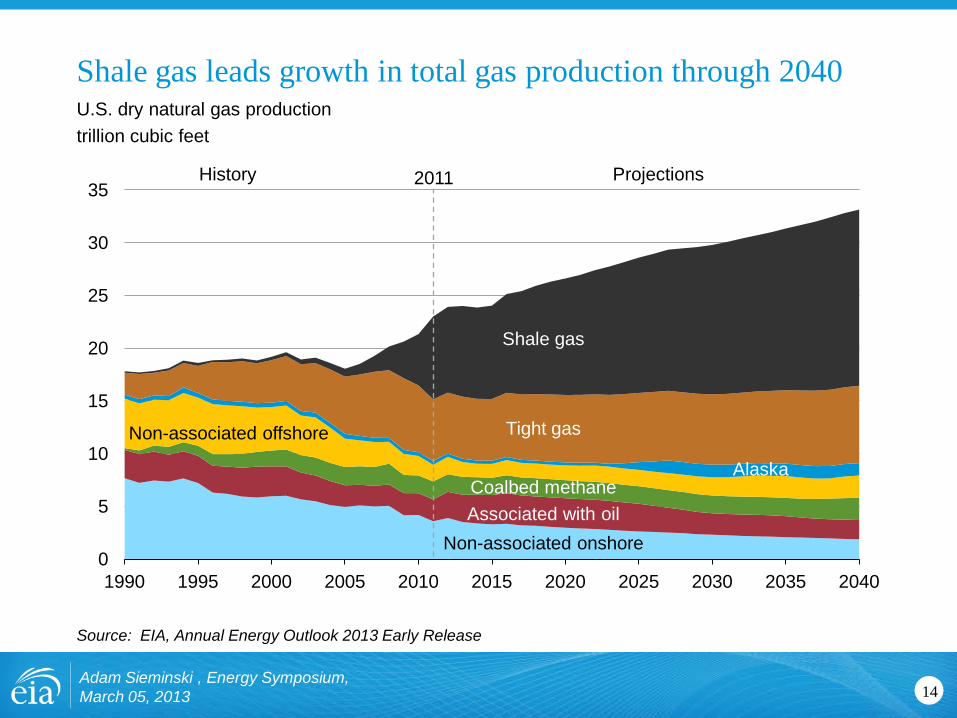

Shale gas leads growth in total gas production through 2040

14

U.S. dry natural gas production trillion cubic feet

Source: EIA, Annual Energy Outlook 2013 Early Release

0

5

10

15

20

25

30

35

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

Associated with oil Coalbed methane

Tight gas

Shale gas

Alaska

Non-associated onshore

Non-associated offshore

Projections History 2011

Adam Sieminski , Energy Symposium, March 05, 2013

15

0

5

10

15

20

25

30

35

2005 2011 2020 2025 2030 2035 2040

U.S. dry gas consumption trillion cubic feet

Source: EIA, Annual Energy Outlook 2013 Early Release

Projections History

Industrial*

Electric power

Commercial

Residential

Transportation**

33%

14%

6%

32%

12%

33%

19%

3%

31%

13%

*Includes combined heat-and-power and lease and plant fuel. **Includes pipeline fuel.

Gas to liquids 2%

Natural gas consumption is quite dispersed with electric power, industrial, and transportation use driving future demand growth

Adam Sieminski , Energy Symposium, March 05, 2013

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

Growth of natural gas in transportation led by heavy duty trucks (LNG) and gas to liquids (diesel)… marine and rail to come?

16

U.S. natural gas consumption quadrillion Btu

Pipeline fuel

Light-duty vehicles

2011 History Projections

95%

3%

1%

1%

28%

38%

3%

31%

1% Buses

Freight trucks

Gas to liquids

Note: Gas to liquids includes heat, power, and losses. Source: EIA, Annual Energy Outlook 2013 Early Release

Adam Sieminski , Energy Symposium, March 05, 2013

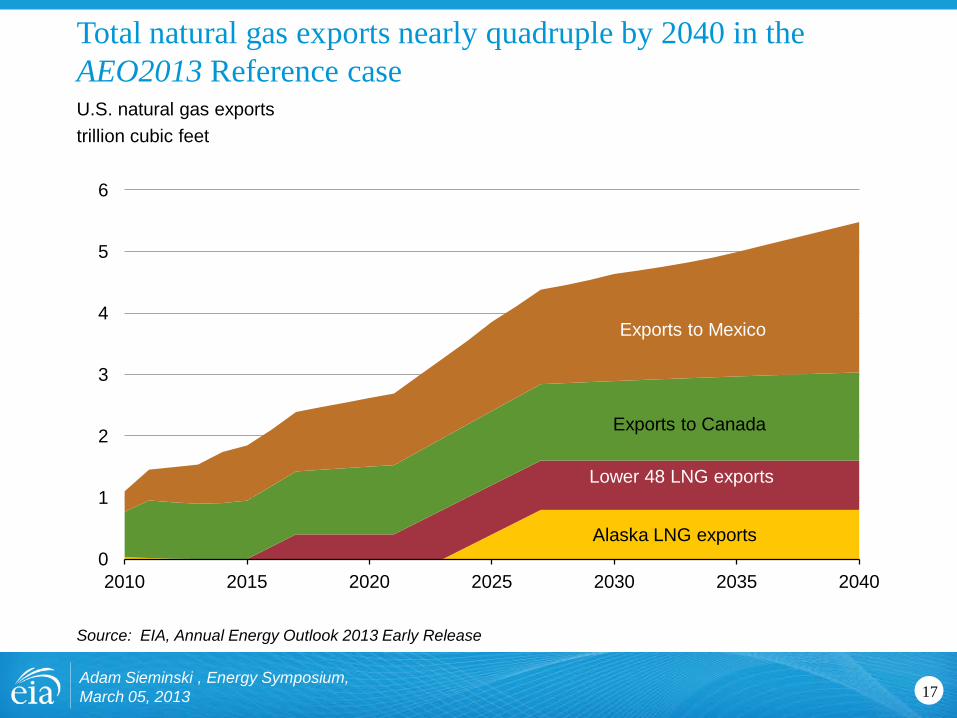

Total natural gas exports nearly quadruple by 2040 in the AEO2013 Reference case

17

U.S. natural gas exports trillion cubic feet

Source: EIA, Annual Energy Outlook 2013 Early Release

0

1

2

3

4

5

6

2010 2015 2020 2025 2030 2035 2040

Alaska LNG exports

Exports to Mexico

Exports to Canada

Lower 48 LNG exports

Adam Sieminski , Energy Symposium, March 05, 2013

Domestic natural gas production grows faster than consumption and the U.S. becomes a net exporter of natural gas around 2020

18

-5

0

5

10

15

20

25

30

35

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

U.S. dry gas trillion cubic feet

Source: EIA, Annual Energy Outlook 2013 Early Release

Projections History 2011

Consumption

Domestic supply

Net imports

Adam Sieminski , Energy Symposium, March 05, 2013

U.S. Tight Oil

19 Adam Sieminski , Energy Symposium, March 05, 2013

20

U.S. crude oil and lease condensate resources in non-prohibited areas billion barrels

(1) The USGS reduced NPR-A resource estimates, which is responsible for the lower AEO2013 Alaska resources. (2) Prior to AEO2009, resources in Pacific, Atlantic, and Eastern GOM OCS were under moratoria and not included. (3) Includes shale oil. Prior to AEO2011, tight oil is included in unproved other lower-48 onshore category.

Multiple factors have contributed to U.S. crude oil resource estimate increases over the years, with tight oil contributing recently

Source: EIA, Annual Energy Outlook 2013 Early Release

0

50

100

150

200

250

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Year of Annual Energy Outlook

Unproved Alaska (1) Unproved L48 Offshore (2) Unproved Tight Oil (3) Unproved Tight Oil (reclassified from onshore) Unproved Other L48 Onshore Proved Reserves

23.8

48.6

41.6

16.5

67.0

25.2

222.6

Adam Sieminski , Energy Symposium, March 05, 2013

U.S. crude oil plus condensate proved reserves, 1980-2010

Adam Sieminski , Energy Symposium, March 05, 2013 21

billion barrels

Source: U.S. Energy Information Administration

0

5

10

15

20

25

30

35

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010

U.S. Total

Lower 48 Onshore

Federal Offshore

Alaska

Domestic production of tight oil has grown dramatically over the past few years

22

tight oil production for select plays million barrels per day

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2000 2002 2004 2006 2008 2010 2012

Eagle Ford

Bakken

Granite Wash

Bonespring

Monterey

Woodford

Niobrara-Codell

Spraberry

Austin Chalk

Source: Drilling Info (formerly HPDI), Texas RRC, North Dakota department of mineral resources, and EIA, through August 2012

Adam Sieminski , Energy Symposium, March 05, 2013

U.S. tight oil production leads a growth in domestic production of 2.6 million barrels per day between 2008 and 2019

23

U.S. crude oil production million barrels per day

Source: EIA, Annual Energy Outlook 2013 Early Release and Short-Term Energy Outlook, February 2013

0

2

4

6

8

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

Projections History 2011

Alaska

Tight oil

Other lower 48 onshore

Lower 48 offshore

STEO Feb. 2013 U.S. crude oil projection

Adam Sieminski , Energy Symposium, March 05, 2013

U.S. petroleum product exports exceeded imports in 2011 for first time in over six decades

24

annual U.S. net exports of total petroleum products, 1949 – 2011 million barrels per day

Source: EIA, Petroleum Supply Monthly

-4

-3

-2

-1

0

1

2

3

4

1949 1955 1961 1967 1973 1979 1985 1991 1997 2003 2009

imports

exports

net exports

net product exporter

Adam Sieminski , Energy Symposium, March 05, 2013

U.S. dependence on imported liquids depends on both supply and demand

25

U.S. liquid fuel supply million barrels per day

Source: EIA, Annual Energy Outlook 2013 Early Release

0

5

10

15

20

25

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

Consumption

Domestic supply

Net imports 45%

37%

Projections History 2011

60%

2005

Adam Sieminski , Energy Symposium, March 05, 2013

Light-duty vehicle liquids consumption is lower primarily due to more stringent CAFE standards

Adam Sieminski , Energy Symposium, March 05, 2013 26

0

2

4

6

8

10

2010 2015 2020 2025 2030 2035 2040

light-duty vehicle liquids consumption million barrels per day

Source: EIA, Annual Energy Outlook 2013 Early Release

AEO2012

AEO2013

Reference case oil price initially drops and then rises steadily, but there is uncertainty about the future trajectory

27

0

50

100

150

200

250

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

Annual average spot price of Brent crude oil 2011 dollars per barrel

Projections History 2011

High Oil Price

Low Oil Price

Reference

Source: EIA, Annual Energy Outlook 2013 Early Release

Adam Sieminski , Energy Symposium, March 05, 2013

Global liquids supply increases 26 percent with regional market shares relatively stable

28

0

20

40

60

80

100

120

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

Global liquids supply million barrels per day

Source: EIA, Annual Energy Outlook 2013 Early Release

Projections History 2011

OPEC

Other non-OECD

OECD

44%

25%

31%

40%

26%

34%

Adam Sieminski , Energy Symposium, March 05, 2013

Global tight oil production comparisons

29

Source: Preliminary International Energy Outlook 2013, BP Energy Outlook 2030

0

2

4

6

8

10

12

2000 2010 2020 2030

Australia China Russia Argentina Mexico Canada United States

million barrels per day

BP Energy Outlook 2030 IEO2013 DRAFT

Adam Sieminski , Energy Symposium, March 05, 2013

Uncertainties that could slow global growth of shale gas and tight oil

Adam Sieminski , Energy Symposium, March 05, 2013 30

• Resource quantities and distribution

• Surface vs. mineral rights

• Risk appetite of industry participants

• Infrastructure and technology

• Environmental constraints

Changing electricity generation mix in AEO2012 reference case and carbon fee allowance side cases

31

0

1

2

3

4

5

1990 2005 2020 2035 0

1

2

3

4

5

1990 2005 2020 2035 0

1

2

3

4

5

1990 2005 2020 2035

U.S. electricity net generation trillion kilowatthours

Source: EIA, Annual Energy Outlook 2012

Natural gas

2012 Reference Case $15 Carbon Fee $25 Carbon Fee

Renewables

Nuclear

Coal

Natural gas Natural gas

Renewables

Renewables Nuclear

Nuclear Coal

Coal

2010

24%

10%

20%

45%

28%

15%

18%

38%

34%

22%

27%

16%

34%

23%

38%

4%

Adam Sieminski , Energy Symposium, March 05, 2013

Coal and Electricity

32 Adam Sieminski , Energy Symposium, March 05, 2013

Growth in electricity use slows, but still increases by 28% from 2012 to 2040

33

U.S. electricity use percent growth (3-year rolling average)

Source: EIA, Annual Energy Outlook 2013 Early Release

0

2

4

6

8

10

12

14

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040

Projections

History 2011

Period Annual Growth 1950s 9.8 1960s 7.3 1970s 4.7 1980s 2.9 1990s 2.4 2000-2011 0.9 2012-2040 0.9

Adam Sieminski , Energy Symposium, March 05, 2013

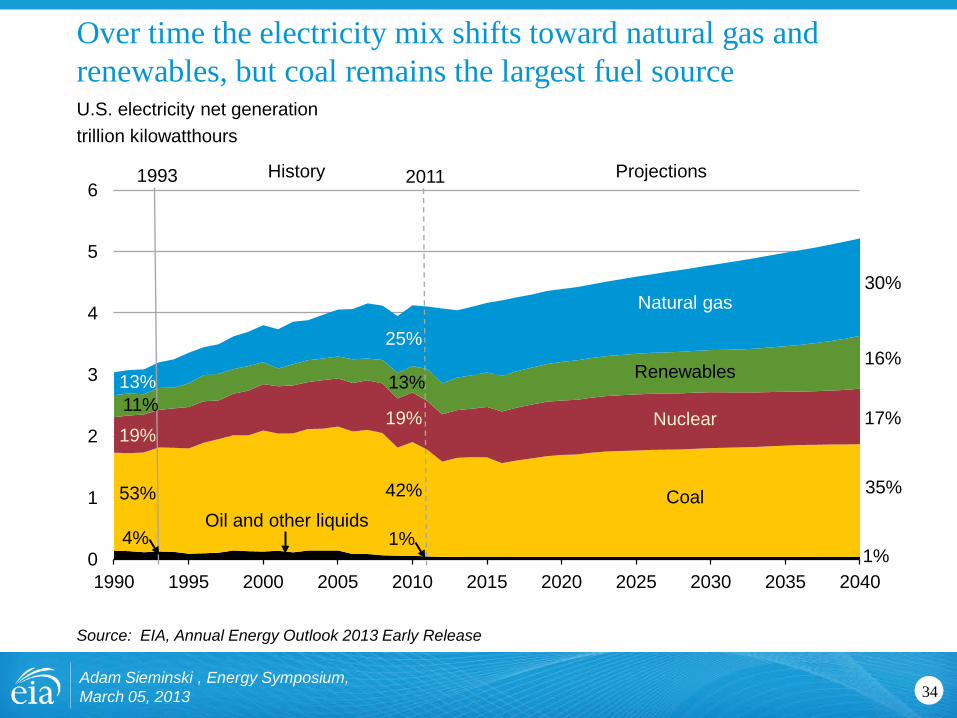

Over time the electricity mix shifts toward natural gas and renewables, but coal remains the largest fuel source

34

0

1

2

3

4

5

6

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

U.S. electricity net generation trillion kilowatthours

25%

19%

42%

13%

1%

Nuclear

Oil and other liquids

Natural gas

Coal

Renewables

2011 Projections History

17%

16%

35%

30%

1%

1993

53%

13%

19% 11%

4%

Source: EIA, Annual Energy Outlook 2013 Early Release

Adam Sieminski , Energy Symposium, March 05, 2013

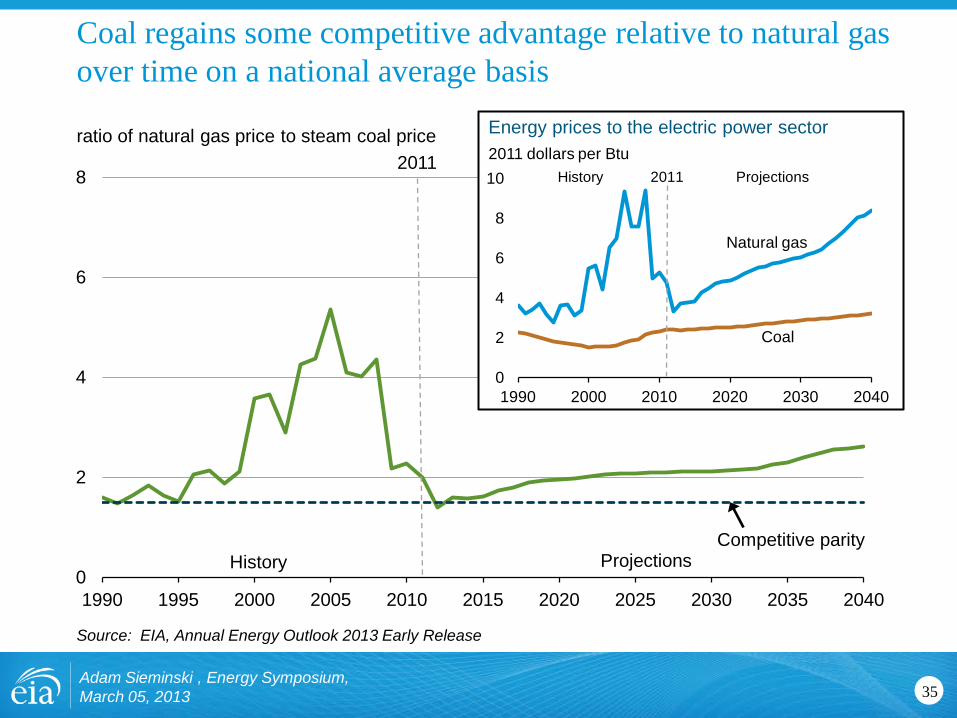

Coal regains some competitive advantage relative to natural gas over time on a national average basis

35

0

2

4

6

8

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

ratio of natural gas price to steam coal price

Source: EIA, Annual Energy Outlook 2013 Early Release

0

2

4

6

8

10

1990 2000 2010 2020 2030 2040

History Projections

2011 2011 dollars per Btu

History Projections 2011

Competitive parity

Energy prices to the electric power sector

Coal

Natural gas

Adam Sieminski , Energy Symposium, March 05, 2013

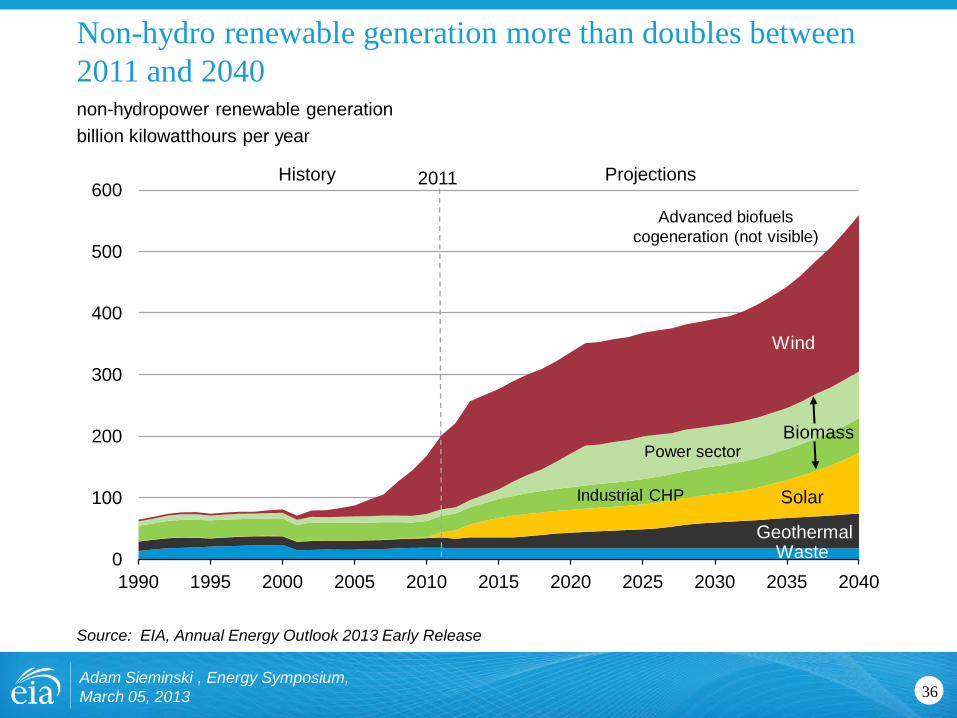

Non-hydro renewable generation more than doubles between 2011 and 2040

36

non-hydropower renewable generation billion kilowatthours per year

Source: EIA, Annual Energy Outlook 2013 Early Release

0

100

200

300

400

500

600

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

Wind

Solar

Geothermal Waste

Biomass

Industrial CHP

Power sector

Advanced biofuels cogeneration (not visible)

2011 Projections History

Adam Sieminski , Energy Symposium, March 05, 2013

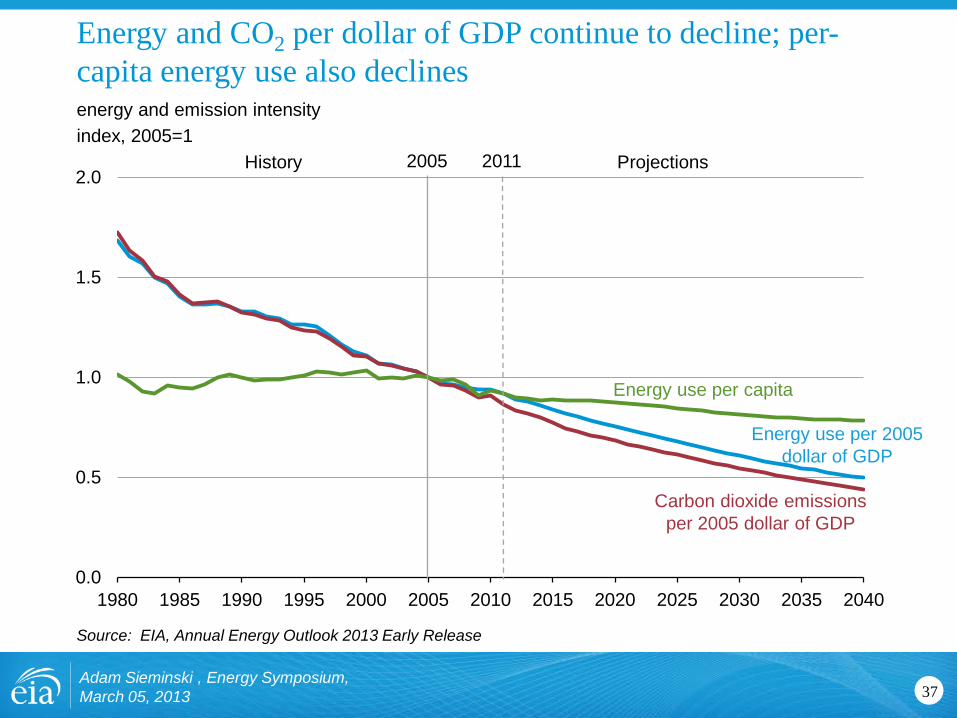

Energy and CO2 per dollar of GDP continue to decline; per-capita energy use also declines

Adam Sieminski , Energy Symposium, March 05, 2013 37

0.0

0.5

1.0

1.5

2.0

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

energy and emission intensity index, 2005=1

Source: EIA, Annual Energy Outlook 2013 Early Release

History Projections 2011

Carbon dioxide emissions per 2005 dollar of GDP

Energy use per 2005 dollar of GDP

Energy use per capita

2005

In the AEO2013 Reference case, energy-related CO2 emissions never get back to their 2005 level

38

carbon dioxide emissions billion metric tons

Source: EIA, Annual Energy Outlook 2013 Early Release

0

1

2

3

4

5

6

7

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

Projections History 2011 2005

2005 2020 2040 (billion metric tons)

6.00 5.45 5.69

- - -9.0% -5.1%

(percent change from 2005)

AEO2013

Adam Sieminski , Energy Symposium, March 05, 2013

For more information

39

U.S. Energy Information Administration home page | www.eia.gov

Annual Energy Outlook | www.eia.gov/forecasts/aeo

Short-Term Energy Outlook | www.eia.gov/forecasts/steo

International Energy Outlook | www.eia.gov/forecasts/ieo

Today In Energy | www.eia.gov/todayinenergy

Monthly Energy Review | www.eia.gov/totalenergy/data/monthly

Annual Energy Review | www.eia.gov/totalenergy/data/annual

Energy Kids | www.eia.gov/kids

Adam Sieminski , Energy Symposium, March 05, 2013