thought leadership - napa...

TRANSCRIPT

RETIREMENTCPII N S T I T U T E

FOR ADVISOR USE ONLY. NOt tO bE VIEwED OR DIStRIbUtED tO thE gENERAL pUbLIc.

People driven. Outcome focused.

Thought LeadershipDelivering the tools and resources to enhance your retirement plan business.

CPI Qualified Plan Consultants, Inc., a member of CUNA Mutual Group | Thought Leadership1

RETIREMENTCPII N S T I T U T E

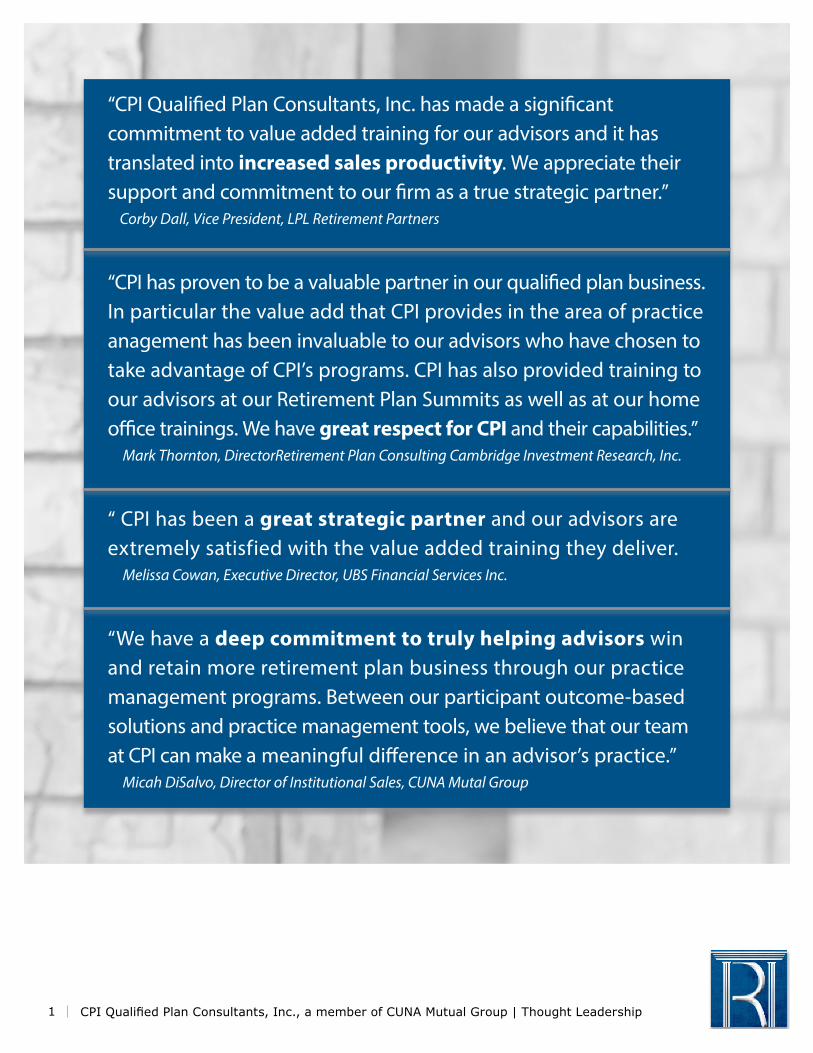

“CPI Qualified Plan Consultants, Inc. has made a significant commitment to value added training for our advisors and it has translated into increased sales productivity. We appreciate their support and commitment to our firm as a true strategic partner.”

Corby Dall, Vice President, LPL Retirement Partners

“CPI has proven to be a valuable partner in our qualified plan business. In particular the value add that CPI provides in the area of practice anagement has been invaluable to our advisors who have chosen to take advantage of CPI’s programs. CPI has also provided training to our advisors at our Retirement Plan Summits as well as at our home office trainings. We have great respect for CPI and their capabilities.”

Mark Thornton, DirectorRetirement Plan Consulting Cambridge Investment Research, Inc.

“ CPI has been a great strategic partner and our advisors are extremely satisfied with the value added training they deliver.

Melissa Cowan, Executive Director, UBS Financial Services Inc.

“We have a deep commitment to truly helping advisors win and retain more retirement plan business through our practice management programs. Between our participant outcome-based solutions and practice management tools, we believe that our team at CPI can make a meaningful difference in an advisor’s practice.”

Micah DiSalvo, Director of Institutional Sales, CUNA Mutal Group

For advisor use only. not to be viewed by or distributed to the general public.2

RETIREMENTCPII N S T I T U T E

3

Retirement Plan Advisors– Broker Dealer group– CPI Qualified Plan Consultants, Inc.

Department of Labor Agent ___________– Fiduciary responsibilities of a plan sponsor– Common fiduciary issues– Correcting issues– Questions… and their answers!

Seminar Agenda

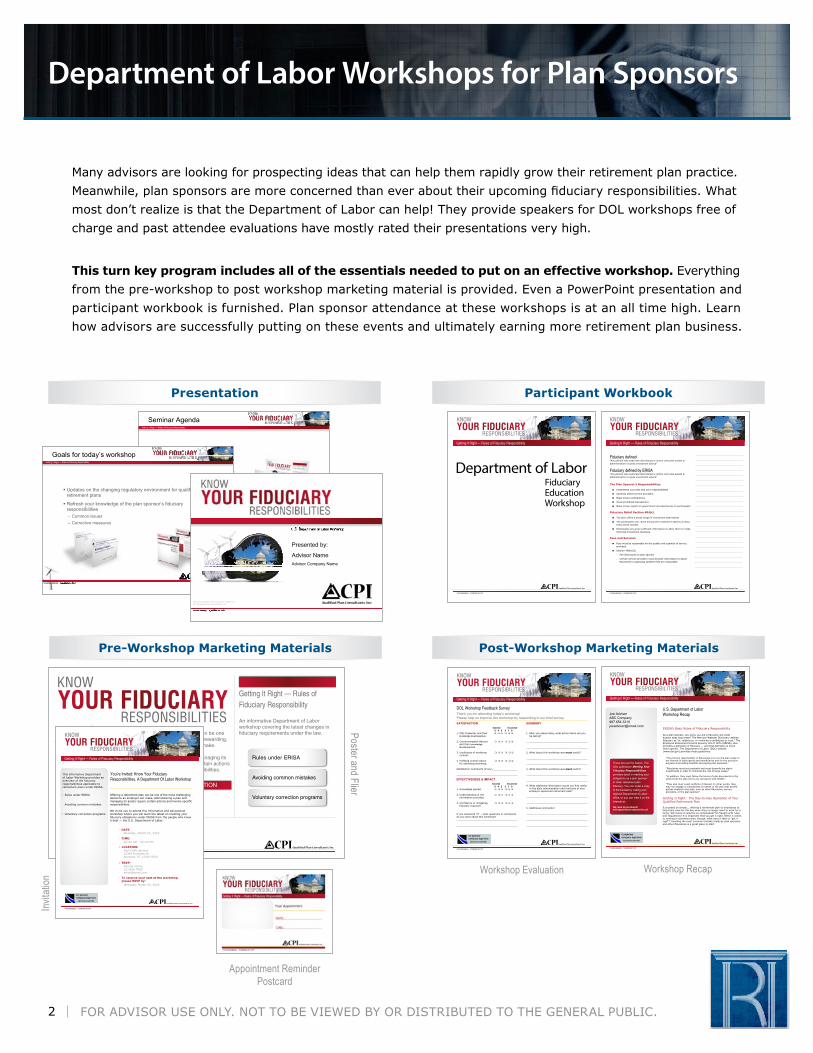

Many advisors are looking for prospecting ideas that can help them rapidly grow their retirement plan practice.

Meanwhile, plan sponsors are more concerned than ever about their upcoming fiduciary responsibilities. What

most don’t realize is that the Department of Labor can help! they provide speakers for DOL workshops free of

charge and past attendee evaluations have mostly rated their presentations very high.

This turn key program includes all of the essentials needed to put on an effective workshop. Everything

from the pre-workshop to post workshop marketing material is provided. Even a powerpoint presentation and

participant workbook is furnished. plan sponsor attendance at these workshops is at an all time high. Learn

how advisors are successfully putting on these events and ultimately earning more retirement plan business.

Department of Labor Workshops for Plan Sponsors

Rules under ERISA

Avoiding common mistakes

Voluntary correction programs

SPONSORSKEY NOTE SPEAKER

DATE TIME LOCATION

hOSTU.S. DEPARTMENT Of LAbOR REPRESENTATIVE

RESPONSIBILITIES

KNOW YOUR FIDUCIARY

Offering a retirement plan can be one of the most challenging, yet rewarding, decisions an employer can make.

Administering a plan and managing its assets, however, require certain actions and involve specific responsibilities.

An informative Department of Labor workshop covering the latest changes in fiduciary requirements under the law.

Getting It Right — Rules of Fiduciary Responsibility

RESPONSIBILITIES

KNOW YOUR FIDUCIARYGetting It Right — Rules of Fiduciary Responsibility

YOUR BUSINESS ... POWERED BY CPI®

SATISFACTION Satisfied Unsatisfied 5 4 3 2 1 01. DOL Presenter and their m m m m m m knowledge level/expertise. 2. Commonweatlth Advisor m m m m m m and their knowledge level/expertise.

3. Usefulness of workshop m m m m m m content.

4. Fulfilling overall reason m m m m m m for attending workshop. Satisfaction Comments (if any)

EFFECTIVENESS & IMPACT Satisfied Unsatisfied 5 4 3 2 1 01. Knowledge gained. m m m m m m 2. Understanding of the m m m m m m information provided.

3. Confidence in mitigating m m m m m m fiduciary exposure.

If you answered “0” – what questions or comments do you have about this workshop?

SUMMARY

1. After you leave today, what action items will you be taking?

2. What about this workshop was most useful?

3. What about this workshop was least useful?

4. What additional information would you find useful in the daily administration and functions of your employer sponsored retirement plan?

5. Additional comments?

Thank you for attending today’s workshop!Please help us improve this workshop by responding to our brief survey.

DOL Workshop Feedback Survey

RESPONSIBILITIES

KNOW YOUR FIDUCIARYGetting It Right — Rules of Fiduciary Responsibility

YOUR BUSINESS ... POWERED BY CPI®

U.S. Department of LaborWorkshop Recap

ERISA’s Basic Rules of Fiduciary Responsibility

As a plan sponsor, you know you are a fiduciary, but what exactly does that mean? The Merriam-Webster Dictionary defines fiduciary as “of, relating to, or involving a confidence or trust.” The Employee Retirement Income Security Act of 1974 (ERISA), also provides a definition of fiduciary ... and that definition is much more specific. The Department of Labor (DOL) website (www.dol.gov) provides these guidelines:

Getting It Right: The Day-to-Day Operation of Your Qualified Retirement Plan

It sounded so simple... offering a retirement plan to employees to help them save for the day when they no longer want to work for a living. Who knew it could be so complicated? So fraught with rules and regulations? It is important that you get it right. When it comes to running a retirement plan, though, what does it take to “get it right”? Avoiding the most common mistake made by plan sponsors and other fiduciaries is a great place to start.

“The primary responsibility of fiduciaries is to run the plan solely in the interest of participants and beneficiaries and for the exclusive purpose of providing benefits and paying plan expenses.”

“Fiduciaries must act prudently and must diversify the plan’s investments in order to minimize the risk of large losses.”

“In addition, they must follow the terms of plan documents to the extent that the plan terms are consistent with ERISA.”

“They also must avoid conflicts of interest. In other words, they may not engage in transactions on behalf of the plan that benefit parties related to the plan, such as other fiduciaries, service providers, or the plan sponsor.”

These are just the basics. The DOL publication Meeting Your Fiduciary Responsibilities provides detail in meeting your obligations as a plan sponsor or other retirement plan fiduciary. You can order a copy of the booklet by calling your regional Department of Labor office, or you can view it on the Internet at:

http://www.dol.gov/ebsa/pdf/meetingyourfiduciaryresponsibilities.pdf

Joe AdviserABC [email protected]

8

Updates on the changing regulatory environment for qualified retirement plans

Refresh your knowledge of the plan sponsor’s fiduciary responsibilities– Common issues– Corrective measures

Goals for today’s workshop

Welcome… Presented by:

Advisor NameAdvisor Company Name

This presentation is the exclusive property of CPI Qualified Plan Consultants, Inc.

Presentation Participant Workbook

Pre-Workshop Marketing Materials Post-Workshop Marketing Materials

RESPONSIBILITIES

KNOW YOUR FIDUCIARYGetting It Right — Rules of Fiduciary Responsibility

YOUR BUSINESS ... POWERED BY CPI®

Fiduciary defined“Any person who exercises discretionary control over plan assets or administration or gives investment advice”

Fiduciary defined by ERISA“Any person who exercises discretionary control over plan assets or administration or gives investment advice”

The Plan Sponsor’s Responsibilities

� Understand your plan and your responsibilities

� Carefully select service providers

� Make timely contributions

� Avoid prohibited transactions

� Make timely reports to government and disclosures to participants.

Fiduciary Relief Section 404(c)

� The plan offers a broad range of investment alternatives

� The participants can chose among the investment options at least every three months

� Participants are given sufficient information to allow them to make informed investment decisions

Fees and Services

� Fees must be reasonable for the quality and quantity of service provided

� Section 408(b)(2)

– Fee disclosures to plan sponsor

– Certain service providers must disclose information to assist fiduciaries in assessing whether fees are reasonable

RESPONSIBILITIES

KNOW YOUR FIDUCIARYGetting It Right — Rules of Fiduciary Responsibility

YOUR BUSINESS ... POWERED BY CPI®

Department of LaborFiduciaryEducationWorkshop

RESPONSIBILITIES

KNOW YOUR FIDUCIARYGetting It Right — Rules of Fiduciary Responsibility

YOUR BUSINESS ... POWERED BY CPI®

You’re Invited: Know Your Fiduciary Responsibilities, A Department Of Labor Workshop

Offering a retirement plan can be one of the most challenging decisions an employer can make. Administering a plan and managing its assets require certain actions and involve specific responsibilities.

We invite you to attend this informative and educational workshop where you will learn the latest on meeting your fiduciary obligations under ERISA from the people who know it best — the U.S. Department of Labor.

DATE:

TIME:

LOCATION:

RSVP:

To reserve your seat at the workshop, please RSVP by:

This informative Department of Labor Workshop provides an overview of the fiduciaryresponsibilities applicable to retirement plans under ERISA.

Rules under ERISA

Avoiding common mistakes

Voluntary correction programs

Weekday, Month XX, 20XX

XX:XX AM - XX:XX PM

Non-Profit sponsor 12345 Business St. Anytown, ST 12345-9876

Adviser Name 123.456.7890 [email protected]

Weekday, Month XX, 20XX

Appointment Reminder Postcard

Invita

tion

Poster and Flier

Workshop Evaluation Workshop Recap

CPI Qualified Plan Consultants, Inc., a member of CUNA Mutual Group | Thought Leadership3

RETIREMENTCPII N S T I T U T E

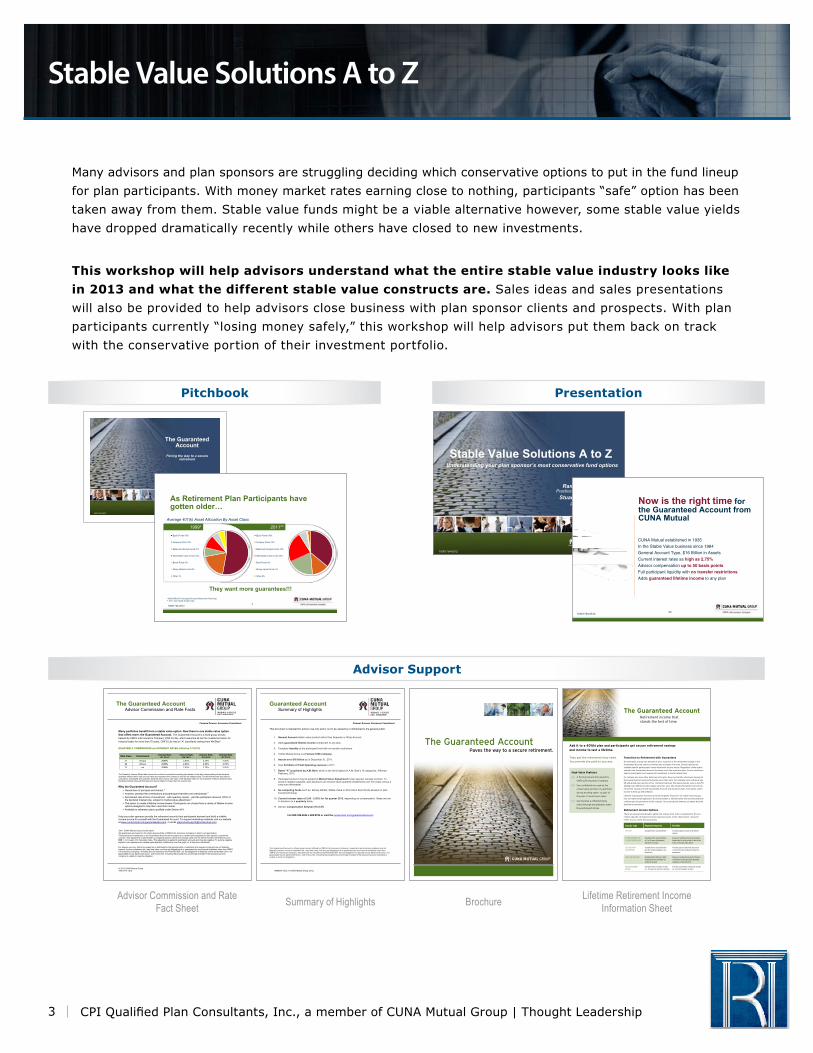

Many advisors and plan sponsors are struggling deciding which conservative options to put in the fund lineup

for plan participants. with money market rates earning close to nothing, participants “safe” option has been

taken away from them. Stable value funds might be a viable alternative however, some stable value yields

have dropped dramatically recently while others have closed to new investments.

This workshop will help advisors understand what the entire stable value industry looks like

in 2013 and what the different stable value constructs are. Sales ideas and sales presentations

will also be provided to help advisors close business with plan sponsor clients and prospects. with plan

participants currently “losing money safely,” this workshop will help advisors put them back on track

with the conservative portion of their investment portfolio.

Stable Value Solutions A to Z

The Guaranteed Account Paves the way to a secure retirement.

Transition to Retirement with Guarantees

At retirement, a lump sum amount of all or a portion of the retirement savings in the

Guaranteed Account can be converted into a stream of income. Several options are

available that fit participants’ varied retirement income needs. Regardless of the option

selected, the Guaranteed Account functions much like a pension plan. Income continues

and the participant is not exposed to investment or stock market risks.

For retirees who leave their balances in the plan, they can transfer retirement savings to

the Guaranteed Account and annuitize more than once. For example, Jane retires at age

65 and annuitizes a portion of her retirement savings. Five years pass by. Jane is now 70.

Adding more lifetime income makes sense for Jane. She decides to transfer more of her

retirement savings into the Guaranteed Account and annuitize again. This allows Jane’s

income to keep up with inflation.

Lifetime annuitization functions a bit like longevity insurance—no matter how long you

live, no matter what happens to the stock market or interest rates—the income payments

continue per the provisions of the contract. Once annuitized; however, be aware that the

decision is permanent.

Retirement Income Options

There are several annuitization options to choose from. Each is designed to fit your

clients’ specific retirement income planning needs. In the chart below, “insured”

refers to your client who annuitizes:

Annuity type Payment longevity Benefits

LIFE ONLY Guaranteed for insured lifetime Provides highest income of all lifetime options

5 YEAR CERTAIN & LIFE10 YEAR CERTAIN & LIFE

Guaranteed for insured lifetime or 5 or 10 years of payments, whichever is longer

Assures a continued income to insured’s beneficiary for a set period of time in the event of insured’s early death

LIFE ONLY WITH CASH REFUND

Guaranteed for insured lifetime plus the remaining balance to a beneficiary

Provides peace of mind that the return of insured’s full principal investment is guaranteed

JOINT AND SURVIVOR Guaranteed for lifetime of both insured and joint annuitant as named by insured

Assures a continued income for the lives of both the insured and joint annuitant, regardless of who dies first

FIXED INSTALLMENT METHOD

Guaranteed for a number of years (i.e., 20 years) of insured’s choosing

Provides insured with a maximum income for a selected number of years

High-Value Features

A fixed group annuity issued by

CMFG Life Insurance Company.

Can confidently be used as the

conservative portion of a portfolio

during working years— as part of

the plan, it never loses value.1

Can become a retirement pay

check through annuitization when

the participant retires.

The Guaranteed Account Retirement income that stands the test of time.

Add it to a 401(k) plan and participants get secure retirement savings

and income to last a lifetime.

They get the retirement they need.

You provide the path to success.

10001754-0512

The Guaranteed Account

Paving the way to a secure retirement

Pitchbook Presentation

Advisor Support

10001754-0512

Stable Value Solutions A to ZUnderstanding your plan sponsor’s most conservative fund options

Presented byRandy S. Fuss, CFP

Practice Management ConsultantStuart Rossmiller, CFA

Portfolio Strategist

2010001754-0512

CUNA Mutual established in 1935In the Stable Value business since 1984General Account Type, $16 Billion in AssetsCurrent interest rates as high as 2.75%Advisor compensation up to 50 basis pointsFull participant liquidity with no transfer restrictionsAdds guaranteed lifetime income to any plan

Now is the right time for the Guaranteed Account from CUNA Mutual

Common Purpose. Uncommon Commitment.

© 2012 CUNA Mutual Group 10001710-1212

The Guaranteed Account Advisor Commission and Rate Facts

Many portfolios benefit from a stable value option. Now there is one stable value option that offers more: the Guaranteed Account. The Guaranteed Account is a fixed group annuity backed by CMFG Life Insurance Company (CMFG Life), which assumes all risk for invested principal. An industry leader for more than 75 years, CMFG Life has an “A” (excellent) ranking from AM Best1. QUARTERLY COMMISSIONS and INTEREST RATES (effective 1/1/2013)

Rate Class Commission Interest Rate Q1 2013

Interest Rate Q4 2012

Interest Rate Q3 2012

Interest Rate Q2 2012

21 50 bps 2.00% 2.00% 2.25% 2.50% 22 25 bps 2.25% 2.25% 2.50% 2.75% 23 n/a 2.50% 2.50% 2.75% 3.00%

The Quarterly Interest Rates table shows the contract’s annualized crediting rate based on the daily compounding of the declared quarterly interest rate’s daily accrual value and assumes the contract is held for the stated period. Current interest rate and historic cumulative, annualized and quarterly declared rates vary by rate class. Past declared rates are not indicative of future declared rates. Declared interest rates will fluctuate and may be higher or lower than the current rate. Why the Guaranteed Account?

Guarantees of principal and interest.2 Anytime, penalty-free contributions and participant transfers and withdrawals.3 Set interest rate at time of investment - with quarterly resets – and the participant receives 100% of

the declared interest rate, subject to market value adjustment.3 The option to create a lifetime income stream. Participants can choose from a variety of lifetime income

options designed to help them meet their needs. Available to retirement plans qualified under Section 401.

Help your plan sponsors provide the retirement security their participants demand and build a reliable income source for yourself with the Guaranteed Account. To request marketing materials visit our website at www.cunamutual.com/guaranteedaccount, or email [email protected]. 12011 CUNA Mutual Group annual report. 2All guarantees are based on the claims paying ability of CMFG Life Insurance Company to honor such guarantees. 3Plan participant investments in the Guaranteed Account will be subject to a market value adjustment if plan sponsor cancels the contract. This adjustment is determined by comparing today’s yield to the average yield over the last 60 months of the Merrill Lynch BBB 7- to 10-year U.S. Corporate Index. The adjustment is applied to participant accounts and may be negative. To avoid a negative payback, plan sponsors can choose equal quarterly installments over five years vs. a lump sum withdrawal. For advisor use only. Not to be viewed by or distributed to the general public. Investment and insurance products are not federally insured, involve investment risk, may lose value, and are not obligations of or guaranteed by any financial institution other than CMFG Life Insurance Company. Annuities are not insured by the FDIC/NCUSIF, are not obligations or deposits of any bank/credit union, nor guaranteed by any bank/credit union, and involve risk, including the possible loss of principal invested if the issuing insurance company is unable to meet its obligation.

Common Purpose. Uncommon Commitment.

10002465-1212. © CUNA Mutual Group, 2012.

Guaranteed AccountSummary of Highlights

This document is intended for advisor use only and is not to be viewed by or distributed to the general public.

1. General Account stable value product rather than Separate or Wrap Account.

2. Adds guaranteed lifetime income component to any plan.

3. Complete liquidity at the participant level with no transfer restrictions.

4. CUNA Mutual Group is a Fortune 1000 company.

5. Assets over $16 billion as of December 31, 2011.

6. Over $3 billion of Total Operating revenue in 2011.

7. Rated “A” (excellent) by A.M. Best, which is the third-highest of A.M. Best’s 16 categories. Affirmed February, 2012.

8. Participant account may be subject to Market Value Adjustment if plan sponsor cancels contract. To avoid a negative payback, plan sponsors can choose equal quarterly installments over five years versus a lump sum withdrawal.

9. No competing funds such as Money Market, Stable Value or Short-term Bond funds allowed on plan investment lineup.

10. Current interest rates of 2.00 - 2.50% for 1st quarter 2013, depending on compensation. Rates are set in advance on a quarterly basis.

11. Advisor compensation between 0%-0.5%

Call 800-356-2644 x 665.8754 or visit the cunamutual.com/guaranteedaccount.

The Guaranteed Account is a fixed group annuity offered by CMFG Life Insurance Company. Investment and insurance products are not federally insured, involve investment risk, may lose value, and are not obligations of or guaranteed by any financial institution other thanCMFG Life Insurance Company. Annuities are not insured by the FDIC/NCUSIF, are not obligations or deposits of any bank/credit union, nor guaranteed by any bank/credit union, and involve risk, including the possible loss of principal invested if the issuing insurance company is unable to meet its obligations.

Advisor Commission and Rate Fact Sheet Summary of Highlights Brochure Lifetime Retirement Income

Information Sheet

210001754-0512

Equity Funds-36%

Company Stock-13%

Balanced/ Lifestyle Funds-19%

GICs/Stable Value Funds-23%

Bond Funds-6%

Money market Funds-1%

Other-2%

They want more guarantees!!!

As Retirement Plan Participants have gotten older…

Average 401(k) Asset Allocation By Asset Class

*1999 EBRI/ICI Participant-Directed Retirement Plan Data** 2011 Aon Hewitt 401(k) Index

2011**

Equity Funds-53%

Company Stock-19%

Balanced/ Lifestyle Funds-7%

GICs/Stable Value Funds-10%

Bonds Funds-5%

Money Market Funds-5%

Other-1%

1999*

For advisor use only. not to be viewed by or distributed to the general public.4

RETIREMENTCPII N S T I T U T E

RETIREMENTCPII N S T I T U T E

FOR ADVISOR USE ONLY. NOt tO bE VIEwED bY OR DIStRIbUtED tO thE gENERAL pUbLIc.1

DirectorThe Retirement Plan Advisor

Descriptors

Strengths

challenges

The Employer

Descriptors

cues and clues

Do

Don’t

WORKSHEET

MotivatorThe Retirement Plan Advisor

Descriptors

Strengths

challenges

The Employer

Descriptors

cues and clues

Do

Don’t

RETIREMENTCPII N S T I T U T E

For advisor use only. Not to be viewed by or distributed to the general public.1

Director

RelaterAnalyzer

You are talking to a Director when you hear the following verbal cues:

Fast-paced, loud voice with a lot of infl ection

Expresses opinions without hesitation

Makes statements more than asks questions

will ask whAt questions such as:

» What makes your retirement plan better than the one I have now?

» What is the #1 reason I should listen to your retirement plan pitch?

» What’s the cost of your retirement plan?

You are looking at a Director when you see physical clues:

Industry: attorneys, physicians, professional offi ces, etc.

position: owner, president, cEO

Offi ce space: Neat, conservative, expensive, high quality furnishings, big offi ce (if VIPs), power boardroom, bold artwork

greeting: Firm handshake with a cold hard stare

Attire: Dress is formal, conservative, power suits and ties, dark colors

Present the bottom line up front. present “all in” plan costs clearly and quickly. You think about all of the costs involved, such as plan level fees, participant level fees, fund fees and advisor compensation, but a Director wants just one number…fast. give it to them…fast. then explain the details, but be prepared for a Director to cut you off.

Highlight specifi c benefi ts to the Director. “this retirement plan design will let you make the maximum allowable contributions for your personal retirement account.” “this plan will save you $1,500 per year.”

Give up some control in your presentations by giving the Director choices, such as

» “what would you like to accomplish from this meeting?”

» “What would you like to discuss fi rst?”

» “How does your current plan control fi duciary risks and costs?”

Give a Director options throughout the sales process including offering more than one retirement plan solution. “You have several different choices: 1) You can do nothing; 2) You can seek lower pricing from your current plan provider; 3) You can change plans. Regardless of which choice you make, you also have the option to work with me so that you can tap into my superior service and expertise at a reasonable cost.”

Give Directors answers to the “What?” questions.

» “what will this plan cost me?” Respond immediately. “$1,500 per year and $25 per participant.”

» If possible, compare it to what they are paying now: “Right now you are paying $3,000 per year and $50 per participant.”

Now that you know the employer you are talking to is a Director ...

DO

Motivator

D

As a retirement plan advisor you need to master the ability to identify and adapt your selling style to the

four most common buying styles of your Retirement plan prospects and clients. For the average advisor

this is easy because they are dealing with one prospect / client at a time.

but for retirement plan advisors, the sales process not only involves more than one person, but it involves

multiple people (read: buying styles) over a longer period of time. This program shows retirement plan

advisors how to adapt their selling style so they win more retirement plans with less effort.

Adaptive Selling to Plan Sponsors

Workbook Presentation

CPI is a member of CUNA Mutual Group.

For advisor use only. Not to be viewed or distributed to the general public.

Presented by Randy Fuss, CFP©

Registered Corporate Coach™Practice Management Consultant

Adaptive Selling to Plan Sponsors

2011760.4-0310

4 | FOR ADVISOR USE ONLY. NOT TO BE VIEWED OR DISTRIBUTED TO THE GENERAL PUBLIC.

Four distinct selling and

buying behaviors

Analyzer

RelaterMotivator

Director

Social Styles 360

Meyers Briggs

DISCKolbe

What is Adaptive Selling?

RETIREMENTCPII N S T I T U T E

2

RelaterThe Retirement Plan Advisor

Descriptors

Strengths

challenges

The Employer

Descriptors

cues and clues

Do

Don’t

The Retirement Plan Advisor

Descriptors

Strengths

challenges

The Employer

Descriptors

cues and clues

Do

Don’t

Analyzer

Flashcard Tip Cards

People driven. Outcome focused.

RETIREMENTCPII N S T I T U T E

Adaptive Selling to Plan Sponsors

Presenting Retirement Plans to Directors

How do you know the employer you are talking to is a Director? Listen for cues. Look for clues. Follow the do points. Know the don’t list.

Don’t forget the Director wants to be in control, even when you are presenting. they will most likely dictate the agenda and the pace of the meeting. Be fl exible. Be prepared to pivot quickly and easily as the Director tries to take over the meeting.

Don’t come unprepared. Directors expect you to have invested a signifi cant amount of your time on their behalf and are coming to the table with viable solutions for their retirement plan. Directors will test your knowledge at certain points to make sure you really understand retirement plans, their needs and the retirement plan solution you are recommending. So be prepared.

Don’t get defensive about cost questions. Directors are fully willing to pay a higher price for a retirement plan solution if you can demonstrate that it delivers additional value. State the cost of your retirement plan solution plainly and clearly and then enumerate the ways it brings additional value: “This retirement plan costs $1,500 per year and $25 per participant while the underlying investments have annual expenses of 85 basis points. For this you receive:

1. a full scope fi duciary;

2. better performing fund choices;

3. more rigorous and regular monitoring;

4. more active participant education.

From a cost, risk and service perspective, how does this compare to what you have right now?”

Now that you know the employer you are talking to is an Director ...

DON’T

FOR ADVISOR USE ONLY. CPI Qualified Plan Consultants, Inc. is a member of CUNA Mutual Group, a leading insurance and financial services organization based in Madison, WI.

2011760.3-0313 © CPI, 2013 All Rights Reserved.

CPI Qualifi ed Plan Consultants, Inc. 1809 24th Street | PO Box 1167 Great Bend, KS 67530-1167www.cpiqpc.com

FOR ADVISOR USE ONLY. NOT TO BE VIEWED OR DISTRIBUTED TO THE GENERAL PUBLIC.

People driven. Outcome focused.

RETIREMENTCPII N S T I T U T E

Adaptive Selling to Plan Sponsors

Presenting Retirement Plans to Motivator

How do you know the employer you are talking to is a Motivator? Listen for cues. Look for clues. Follow the do points. Know the don’t list.

Don’t force the agenda. You may be prepared to give the fi nals presentation of your life, but they may want to socialize awhile and have the business agenda short and sweet.

Don’t focus on details or bring in detailed proposals and expect to present it cover to cover. the details should be in the proposal in case a non-Motivator on the team wants to see them, but when presenting to a Motivator focus more on the big picture.

Don’t expect them to meet deadlines or complete detailed tasks. Remember that Motivators tend to be disorganized so encourage them to bring detail-oriented coworkers into the process as needed.

Don’t fail to bring up plan costs because they might not bring it up. they are okay not going with a low cost leader if their peers are doing the same and they are sure they are not overpaying.

Don’t forget who likes to be recognized… they do. Everything is about the Motivator, not you. Once you have learned about them professionally and personally, their company and their retirement plan, fi nd things to compliment.

Don’t assume a “yes” is a yes forever! Motivators might make quick, impulsive decisions about even big decisions like deciding to say Yes to your retirement plan design recommendation. but don’t celebrate too early. Motivators can just as quickly change their mind. So if a Motivator says Yes to your recommendation be sure to maintain the momentum by following up on next steps diligently.

Now that you know the employer you are talking to is a Motivator ...

DON’T

FOR ADVISOR USE ONLY. CPI Qualified Plan Consultants, Inc. is a member of CUNA Mutual Group, a leading insurance and financial services organization based in Madison, WI.

CPI Qualifi ed Plan Consultants, Inc. 1809 24th Street | PO Box 1167 Great Bend, KS 67530-1167www.cpiqpc.com2011760.3-0313 © CPI, 2013 All Rights Reserved.

FOR ADVISOR USE ONLY. NOT TO BE VIEWED OR DISTRIBUTED TO THE GENERAL PUBLIC.

People driven. Outcome focused.

RETIREMENTCPII N S T I T U T E

Adaptive Selling to Plan Sponsors

Presenting Retirement Plans to Relater

How do you know the employer you are talking to is a Relater? Listen for cues. Look for clues. Follow the do points. Know the don’t list.

Don’t provide shallow answers to their concerns. put yourself in their shoes and employ feel-felt-found strategies. be sincere.

Don’t force the agenda or decision. Relaters may need to slow things down, express concerns and not make a decision today opting to “think about it.” Don’t let that discourage you. Stay in touch and share articles on how you are helping their peers or competitors.

Don’t forget how Relaters feel about change. they don’t like it. give thoughtful reasons for what is broken with their current plan and how your proposal will leave the company and the employees better off. talk about how the change is short-lived but the benefi ts of the new retirement plan will last a long time.

Don’t be too loud, energetic or impersonal. Abandon the audiovisuals, the overpromises and gimmicks in favor of sincerity, concern and how you can help them and their employees.

Don’t fail to justify your costs. Relaters are frugal by nature and generally look for lower cost plans, however they do want advisor expertise and customer service. If you can justify your costs, even if they are higher than other choices, Relaters may still say yes.

Now that you know the employer you are talking to is a Relater...

DON’T

FOR ADVISOR USE ONLY. CPI Qualified Plan Consultants, Inc. is a member of CUNA Mutual Group, a leading insurance and financial services organization based in Madison, WI.

CPI Qualifi ed Plan Consultants, Inc. 1809 24th Street | PO Box 1167 Great Bend, KS 67530-1167www.cpiqpc.com2011760.3-0313 © CPI, 2013 All Rights Reserved.

FOR ADVISOR USE ONLY. NOT TO BE VIEWED OR DISTRIBUTED TO THE GENERAL PUBLIC.

People driven. Outcome focused.

RETIREMENTCPII N S T I T U T E

Adaptive Selling to Plan Sponsors

Presenting Retirement Plans to Analyzers

How do you know the employer you are talking to is an Analyzer? Listen for cues. Look for clues. Follow the do points. Know the don’t list.

Don’t provide shallow answers to their concerns. put yourself in

their shoes and employ feel-felt-found strategies. be direct.

Don’t force an agenda or a decision. Analyzers may need to slow

things down, express concerns and not make a decision today opting

to “think about it”. Don’t get discouraged. continue to feed Analyzers

with regular doses of additional data, details and statistics.

Don’t forget who is always right … Analyzers are! Find out

who was responsible for choosing their current plan. If it wasn’t the

Analyzer, give objective reasons and pros and cons when comparing

their current plan to your proposed plan design. If it was the Analyzer,

make the same comparison but talk about how much plans have

changed since they installed their current plan. Never imply the

Analyzer made a bad decision.

Don’t fail to tie individual costs to individual services. Analyzers

are extremely frugal by nature and generally look for a “cafeteria”

style approach that will allow them to piece together a customized,

“smart” solution.

Don’t be too loud, energetic or emotional. Avoid diffi cult to prove

claims, approximations and gimmicks in favor of verifi able facts,

specifi c fi gures and exact data that can help an Analyzer make an

informed decision.

Don’t express opinions, share testimonials or provide any

other information that is of a subjective nature unless asked

directly by the Analyzer.

Now that you know the employer you are talking to is an Analyzer ...

DON’T

FOR ADVISOR USE ONLY. CPI Qualified Plan Consultants, Inc. is a member of CUNA Mutual Group, a leading insurance and financial services organization based in Madison, WI.

CPI Qualifi ed Plan Consultants, Inc. 1809 24th Street | PO Box 1167 Great Bend, KS 67530-1167www.cpiqpc.com2011760.3-0313 © CPI, 2013 All Rights Reserved.

FOR ADVISOR USE ONLY. NOT TO BE VIEWED OR DISTRIBUTED TO THE GENERAL PUBLIC.

People driven. Outcome focused.

Adaptive Selling to Plan Sponsors

RETIREMENTCPII N S T I T U T E

FOR ADVISOR USE ONLY. NOt tO bE VIEwED OR DIStRIbUtED tO thE gENERAL pUbLIc.

RETIREMENTCPII N S T I T U T E

Adaptive Selling: Identify Your Plan Sponsor Employees

More Aggressive and Authoritagive?

» closed posture

» Unexpressive/cool face

» Feelings unexpressed

» Formal

» Focuses on “what?”

» priority on goals and Results

Then you are talking to a

OUTGOING/DIRECT?

Faster paceMore tellingLouder speechMore inflection Director

More Talkative and Enthusiastic?

» Open posture

» Animated/warm face

» Feelings expressed

» casual

» Focuses on “who?”

» priority on people and Approval

Then you are talking to a

Motivator

RESERVED/INDIRECT?Slower paceMore askingSofter speechMore monotone

More Amiable and Accepting?

» Open posture

» Relaxed/warm face

» Feelings expressed

» casual

» Focuses on “why?”

» priority on cooperation and Stability

Then you are talking to a

Relator Analyzer

More Thinking and Methodical?

» closed posture

» Unexpressive/cold face

» Feelings unexpressed

» Formal

» Focuses on “how?”

» priority on procedures and Information

Then you are talking to an

People driven. Outcome focused.

2011760.2-0313 © CPI, 2013 All Rights Reserved. FOR ADVISOR USE ONLY. NOT TO BE VIEWED OR DISTRIBUTED TO THE GENERAL PUBLIC.

Understanding of:Priorities:

» Sincerity

» Relationships

» Dependability

Is bothered by: » pressure

» pushy people

» Uncertainty

» Unpredictability

» Sudden change

» Confl ict

Trusts: » Kindness

Relator AnalyzerSelling to:

Strategies: » Use a casual and low pressure approach

» Show warmth and sincerity

» present information in a step-by-step manner

» Allow them space and time to process information

» provide reassurance

Emphasize: » Ongoing support

» Examples from the past

» Stability and security

» warranties, service plans and guarantees

Understanding of:Priorities:

» Quality

» competency

» Dependability

Is bothered by: » Emotional or illogical people

» personal questions

» Overly enthusiastic presentations

» pressure

» Emotional Appeals

Trusts:Expertise

Selling to:Strategies:

» Use an objective approach

» go through details

» have evidence to back up your claims

» Use logic to connect your solutions to their problems

» give them a chance to show their knowledge

Emphasize: » Quality, high standards

» Your expertise

» Logical Reasons

» Evidence of Reliability

Understanding of:Priorities:

» Results

» Action

» competency

Is bothered by: » wasted time

» Small talk

» too many details

» Indecisiveness

» Lack of control

» challenges to their authority

Trusts: » Confi dence

Director MotivatorSelling to:

Strategies: » Use a confi dent and no nonsense approach

» get to the point

» give them options and a sense of control

» convey respect for their authority

» Show a desire to help them get immediate results

Emphasize: » Immediate Outcomes

» the bottom line

» Effi ciency, ease of use

» Profi ts, savings

Understanding of:Priorities:

» Enthusiasm

» Action

» Relationships

Is bothered by: » Dry or dull analysis

» too many details

» cold or detached people

» Loss of Approval

» Negativity or pessimism

Trusts: » Openness

Selling to:Strategies:

» Use an upbeat and lively approach

» give them a chance to tell their stories

» be open to discussing information about yourself

» Show empathy for their concerns

» Demonstrate how your offering helps other people

Emphasize: » testimonials

» Ease of use

» Exciting Opportunities

» how your offering makes them look good

RETIREMENTCPII N S T I T U T EFOR ADVISOR USE ONLY. NOT TO BE VIEWED OR DISTRIBUTED TO THE GENERAL PUBLIC.

CPI Qualified Plan Consultants, Inc., a member of CUNA Mutual Group | Thought Leadership5

RETIREMENTCPII N S T I T U T E

Presentation

CPI is a member of CUNA Mutual Group.

For advisor use only. Not to be viewed or distributed to the general public.

Leading Practices from Leading Advisors

Winning and Retaining Retirement Plan Business

Presented by Randy Fuss, CFP©

Registered Corporate Coach

2 | FOR ADVISOR USE ONLY. NOT TO BE VIEWED OR DISTRIBUTED TO THE GENERAL PUBLIC.

Today’s Agenda

▲ Six steps to building a successful retirement plan practice▲ Top ten prospecting and retention ideas▲ Social networking leading practices▲ Interactive session

Call today. 800.279.9916 ext. 765

cpI Qualified plan consultants, Inc. is a member of cUNA Mutual group, a leading insurance and fi nancial services organization based in Madison, wI.

1809 24th Street | PO Box 1167Great Bend, KS 67530-1167www.cpiqpc.com®

800.279.9916 ext. 765FOR ADVISOR USE ONLY. NOt tO bE VIEwED bY OR DIStRIbUtED tO thE gENERAL pUbLIc.

51. Get linked. Two things about LinkedIn (www.linkedin.com) can help your retirement plan prospecting efforts. First, spend two hours fi nding your clients, prospects, friend and family on LinkedIn and soon you will be surprised how many additional people you are “linked” to. Among these new “friends” will be more than a handful of business owners you can talk to about retirement plans. Secondly, since LinkedIn will tell you who is the connection between the business owner and you? You can ask that person to make a warm introduction. So with LinkedIn you not only fi ne more leads, you fi nd warm introductions.

52. Gateway to associations. Once you have found a niche you want to pursue, leverage the industry associations that bring all of those people in your niche together. And remember that people in your niche often belong to multiple industry associations. How do you fi nd which associations they belong to? First ask them. Secondly, here is a great place to fi nd all the associations you want to get to know better: http://www.asaecenter.org/Directories/AssociationSearch.cfm.

53. Small business PR. Invest in PR for your clients; Take out full page ad in local newspaper to tell their profile story; Sponsored by Epstein Financial; Picture with Advisor and Plan Sponsor; Be committed to this, the benefi t will be exponential (Retention & Prospecting).

54. Profi le your clients better than anyone else! Include a detailed profi ling process as part of the client transition; Find out who does their corporate P&C, Group Life and Health, Accounting, Legal Counsel, Payroll, etc.; Call to introduce yourself to the vendor and explain that you have a mutual client; Find opportunities for a joint partnership with that vendor.

55. Niche marketing. Forget prospecting letters, they don’t work! Send high value book to target prospects, it gets opened! Include hand written note to personalize the message.

LEADING PRACTICES FROM LEADING ADVISORS

2011730.4-0313 © CPI, 2013 All Rights Reserved.

the best ideas in the retirement plan business do not come from consultants, vendors or sales managers. they come from fellow advisors who are on the front lines of the qualified retirement plan business every day. CPI has formerly interviewed and collected some of those leading practices from some of the leading retirement plan advisors across the country.

these interactive workshops — Winning and Retaining Retirement Plan Business and Rethinking Your Profitability — will explore the concepts on the minds of most advisors. topics such as what is your true

ROI associated with the various functions of retirement plan advisors — serving as a co-fiduciary, providing support at the plan governance level versus plan participant level, investment reviews, etc. we also walk through common concepts of how to grow your practice using a smart strategy — expanding your team, how to structure compensation, roles and accountability, succession planning and ultimately how to position your brand for success.

These workshops are a true deep dive into optimizing your retirement plan practice unlocking the secrets of success from some of the top retirement plan advisors in the industry.

Leading Practices from Leading Advisors

Winning and Retaining Retirement Plan Business

Handouts

People driven. Outcome focused.

RETIREMENTCPII N S T I T U T E

1. Find a Niche Focus on one business segment or

industry

Be specifi c: Dentists, architects, dermatologists, engineering fi rms, etc.

Get smart about their specifi c industry issues

get known in that industry as “the Retirement plan guy for Dentists”

2. Small Business PR Invest in pR for your clients

take out full page ad in local newspaper to tell their profi le story

picture with Advisor and plan Sponsor

Be committed to this, the benefi t will be exponential (Retention & Prospecting)

3. Get Press Once you fi nd your niche, get known for it

in your community

be “the Financial guy” for your local tV station

write a retirement column for the local newspaper

Offer to speak at chamber of commerce, Local college for SbA class

4. News Hound Subscribe to magazines in 10-12 industries

For example, order It Service providers of Minnesota magazine

Read the pages that highlight high performers or major changes

Send laminated copies of articles to the individuals who are named

5. The Vendor Referral Ask current 401(k) clients for a referral to

their vendors

Vendor companies will take the referral very seriously

builds your expertise and contacts in a specifi c industry

6. Client Advisory Board Ask eight of your best clients to join your

“client Advisory board”

purpose: get candid answers to “what am I doing right? what can I do better?”

Answers help you refi ne your business model

Additional benefi t is that it generates high quality referrals

7. SHRM Society It’s where the human Resource decision

makers hang out

Find your local chapter and make friends

they are always looking for good speakers

And it won’t cost you a penny

8. Profi le Your Clients Include a detailed profi ling process as part

of the client transition

Find out who does their corporate P&C, Group Life & Health, Accounting, Legal counsel, payroll

call to introduce yourself to the vendor and explain that you have a mutual client

Find opportunities for a joint partnership with that vendor

9. 9. Niche Marketing Forget prospecting letters, they don’t

work!

Send high value book to target prospects, it gets opened!

Include hand written note to personalize the message

10. Bulletin Boards cork board posted in lunch room / break

room

Your name and company’s name at top

Update biweekly with plan updates and interesting articles

$200 investment that pays big dividends

FOR ADVISOR USE ONLY. NOt tO bE VIEwED OR DIStRIbUtED tO thE gENERAL pUbLIc.

Leading Practices from Leading Advisors

Top Ten Prospecting and Retention Ideas

2011730.3-0313 © CPI, 2013 All Rights Reserved.

People driven. Outcome focused.

RETIREMENTCPII N S T I T U T E

1. Referrals are key. Make friends with Advisors, Insurance Agents, Accountants and Lawyers who are not in the Retirement plan business.

2. Get smart. when I started, I paid out of my own pocket for a 2-week training on Retirement plans at a local University. It was the smartest thing I did. It helped me get smart fast.

3. Total immersion. If you are going to get in, get in all the way. You cannot tiptoe in the Retirement plan business because you are up against heavy competition.

4. Problem solver not product vendor. Do not hitch yourself to one plan provider because you be perceived as a product vendor. build partnerships with two or three quality plan providers. that’s enough to give your clients choice and small enough that you can be a good partner.

5. Bulletin Boards. buy an old-fashioned corkboard, put your name and the plan sponsor’s name at the top and place it in the company lunchroom. post updates and interesting articles every couple of weeks. Tack a few of your business cards on the bulletin board. Announce when you’ll next be in the offi ce for one-on-one meetings or a small group seminar. talk about investing ideas like how to save for college, current cD and bond yields or almost anything that you think will interest plan participants. A bulletin board costs about $200 and pays big dividends.

6. Do not be greedy. Some young Advisors load the plan up with too many expenses. Not only is it bad for the client, it makes it easy for the competition to replace you.

7. Move to an advisory relationship. Advisory relationships are more transparent and put you on the same side of the table as the client. You will represent your clients like attorneys represent their clients. This way the client feels as if their interests always come fi rst.

8. Join the Retirement Plan Advisory Group (RPAG). It can help dissect the internal aspects of a plan’s investment options. It is a very useful analytical tool. I also use Fi360 for the same purpose.

9. Be a good partner. If you are a loyal partner to a tpA or plan provider, you will often receive leads and referrals from these partners.

10. Annual communication plan. Develop your own Annual communication plan. Share it with your clients. get their input and make adjustments based on their preferences. Do not forget to follow through. this way there are rarely any miscommunications or misunderstanding about service levels.

11. “Have you done your due diligence on your plan?” clients often respond to this question by asking “What’s that?” That is your opening to talk about fi duciary liability. Now you can position yourself as the expert and a valuable resource they should listen to.

12. Enrollment protocols. Establish an Enrollment protocol that both you and the plan sponsor will follow when new employees are added or current employees leave. this ensures you receive a steady stream of new potential clients.

13. Annual review. Make an annual review with each of your plan sponsors a mandatory part of practice. talk about it as an automatic part of how you do business. It sets a high standard with your clients and it shows you are serious about your retirement plan business.

Leading Practices from Leading Advisors

Best Practices

FOR ADVISOR USE ONLY. NOt tO bE VIEwED OR DIStRIbUtED tO thE gENERAL pUbLIc.

Prospecting and Retention Ideas

Leading Practices

WORKSHEET

People driven. Outcome focused.

RETIREMENTCPII N S T I T U T E

RETIREMENTCPII N S T I T U T E

At the end of today’s workshop we will take a few minutes to exchange leading practices between you and your

fellow advisors. So as you hear ideas during today’s workshop that trigger leading practices you currently use in

your retirement plan business, write them down here. this way we can move more quickly into sharing leading

practices that everyone can profi t from.

My Leading Practices

123

As you learn new leading practices that you would like to implement into your retirement plan business, make

note of those ideas in the space below.

New Leading Practices

123

FOR ADVISOR USE ONLY. NOt tO bE VIEwED OR DIStRIbUtED tO thE gENERAL pUbLIc.

2011730.2-0313 © CPI, 2013 All Rights Reserved.

Workshop Worksheet

Worksheets

People driven. Outcome focused.

RETIREMENTCPII N S T I T U T E

Retirement Plan Advisor Profi le WORKSHEET

1. tell me about your business model and current structure?

2. how many plans and assets do you have under management?

3. how much of your business is retail wealth management vs. Retirement plans?

4. what is your prospecting strategy?

5. how do you prefer to communicate with product partners?

[ ] Face-to-face [ ] E-mail [ ] phone

how often? Etc.

6. what percentage of your business is bundled vs. open architecture?

% bundled

7. what is your value proposition that you communicate to plan sponsors?

8. where do you see your business growing three years from now?

9. what are you missing or need right now?

10. what is your focus?

[ ] plan governance at the plan sponsor level

[ ] participant education and service

[ ] both

FOR ADVISOR USE ONLY. NOt tO bE VIEwED OR DIStRIbUtED tO thE gENERAL pUbLIc.

2011730.1-0313 © CPI, 2013 All Rights Reserved.

Advisor Profile

RETIREMENTCPII N S T I T U T E

2

Leveraging your practice.5 Clients and community.

Centers of infl uence.

Industry.

Internal.

Complete sales process.6 Employer analysis.

Marketing.

Prospecting.

First meeting.

Second meeting.

Finals presentation.

Follow up.

Implementation.

Participant education.

Plan review and monitoring.

Client service.

Positives and challenges of your current practice.7 STRENGTHS

OPPORTUNITIES

WEAKNESSES

THREATS

People driven. Outcome focused.

RETIREMENTCPII N S T I T U T E

My Retirement Plan Business Strategies

Practice Development WORKSHEET

Define your current clients. Why do they do business with you?1$ Retirement plans $ wealth Management $ Other

Define your ideal client. In detail, defi ne your ideal future client and market.2$ Retirement plans $ wealth Management $ Other

What is the ROI?

Defi ne the Roles & Responsibilities of your current staff .3Defi ne the Roles & Responsibilities of your future staff .4What are your areas of specialization?

FOR ADVISOR USE ONLY. NOt tO bE VIEwED OR DIStRIbUtED tO thE gENERAL pUbLIc.

2011750.3-0313 © CPI, 2013 All Rights Reserved.

Practice Development Worksheet

For advisor use only. not to be viewed by or distributed to the general public.6

RETIREMENTCPII N S T I T U T E

Leading Practices from Leading Advisors

Rethinking Your Profitability

CPI is a member of CUNA Mutual Group.

For advisor use only. Not to be viewed or distributed to the general public.

Leading Practices from Leading Advisors

Rethinking Your Profitability

Presented by Randy Fuss, CFP©Registered Corporate Coach

30 | FOR ADVISOR USE ONLY. NOT TO BE VIEWED OR DISTRIBUTED TO THE GENERAL PUBLIC.

The 100 Client Rule

▲ If you have 100 Wealth clients, you are approaching maximum capacity.

▲ Of your top 20 Wealth clients, you should have at least 10 advocates … raving fans.

▲ Create a Board of Directors.

▲ Replicate your ideal client. Focus on finding clients who fit your practice rather than fitting your practice to fit clients.

People driven. Outcome focused.

RETIREMENTCPII N S T I T U T E

Bilingual Enrollment Specialist Department: Participant Enrollment Organization

POSITION SUMMARY the Retirement plan Specialist will provide dedicated, on-site support and educational services to a major

healthcare system. the incumbent is responsible for ensuring that the client’s overall communication

program objectives are met at the site level, including the delivery of quality educational meetings and one-

on-one counseling sessions. this position also acts as a primary relationship management contact with the

local human Resources representative. Minimal travel required.

PRINCIPAL RESPONSIBILITIES 1. Excellent written and verbal communications skills necessary for group presentations and daily contact

with client employee base.

2. conduct effective one on one counseling sessions and group educational meetings.

3. provide regular activity reports to team Leader, Manager, and hR contact as appropriate.

4. practice good time management skills to effectively balance high demand activities, such as one on one appointments, with higher effective efforts such as department meetings.

5. Must be proactive in resolving client issues and use appropriate diplomacy.

6. Self-starter who accepts challenges of exceeding goals.

7. Must be able to work independently and display a high level of initiative.

8. Maintain current and accurate records to document progress toward goals.

KNOWLEDGE/SKILLS 1. two to three years experience with pensions.

2. Strong investment knowledge.

3. Excellent presentation/communication skills.

4. Strong time/project management skills.

5. Must be bilingual English/Spanish – REQUIRED.

EDUCATIONAL / COURSE REQUIREMENTS 1. Bachelors degree in related fi eld

2. NASD Series 6 or 7 & 63

3. CEBS 3―Retirement Plans: Basic Features in Defi ned Contribution Approaches

4. CEBS 7―Investment Management

FOR ADVISOR USE ONLY. NOT TO BE VIEWED BY OR DISTRIBUTED TO THE GENERAL PUBLIC.

2011730.6-0313 © CPI, 2013 All Rights Reserved.

People driven. Outcome focused.

RETIREMENTCPII N S T I T U T E

Participant CounselorDepartment: Participant Counseling Organization

POSITION SUMMARY Responsible for plan promotion, participant education, and managing education campaigns for an assigned group of clients. the incumbent will conduct group educational meetings and one-on-one counseling sessions with participants on retirement and investment needs. Extensive travel throughout the U.S is required; frequent overnight and weekend travel is also required. Must be able to work closely with Service areas, client Management, Sales and Marketing to promote the participant counseling Organization. Also responsible for generating leads and managing projects.

PRINCIPAL RESPONSIBILITIES 1. Manage the education campaign for an assigned group of clients. consult with client on appropriate

strategies/approaches for their organization.

2. work directly with assigned clients for scheduling, promotion and execution of education meetings.

3. Responsible for group educational meetings by delivering workshops on investments and retirement goals.

4. Identify asset retention and gathering opportunities and initiate appropriate discussions with participants.

5. provide participants with insight into the funds offered under each clients plan with an understanding of fund objectives and fund performance.

6. provide regular activity reports to Manager, AE and others as required.

7. communicate effectively with team members, management and appropriate internal teams.

8. Manage projects designed for the expansion and enhancement of the participant counseling Organization as assigned.

9. Support client Management, Sales and Marketing by promoting the participant counseling Organization.

10. Maintain current and accurate records to document progress towards goals.

KNOWLEDGE/SKILLS 1. Strong investment knowledge for education meetings and one-on-one counseling sessions.

2. Knowledge of pension products required.

3. Strong presentation skills.

4. Excellent verbal and written skills necessary for contact with participants, sales personnel, service personnel and plan sponsors.

5. willingness to work in a team environment.

6. 6. team skills to contribute to the success of departmental goals and objectives.

7. 7. computer skills desirable. 8. Frequent overnight and weekend travel is required.

COURSE REQUIREMENTS 1. NASD Series 6 or 7 Registered Representative

2. NASD Series 63

3. CEBS 3―Retirement Plans: Basic Features in Defi ned Contribution Approaches and CEBS 7―Investment Management or cRpc designation or cFp designation

FOR ADVISOR USE ONLY. NOT TO BE VIEWED BY OR DISTRIBUTED TO THE GENERAL PUBLIC.

2011730.5-0313 © CPI, 2013 All Rights Reserved.

PresentationHandouts

People driven. Outcome focused.

RETIREMENTCPII N S T I T U T E

Leading Practices from Leading Advisors

Rethinking Your Profitability

FOR ADVISOR USE ONLY. NOt tO bE VIEwED OR DIStRIbUtED tO thE gENERAL pUbLIc.

RETIREMENTCPII N S T I T U T E

FOR ADVISOR USE ONLY. NOt tO bE VIEwED bY OR DIStRIbUtED tO thE gENERAL pUbLIc.1

Rethinking Your Profi tabilityThe Architect1. Multiple core offerings (retirement plans, employee benefi ts, wealth management)2. Long term plan to build staff and strategic partners3. well documented processes and job descriptions for everyone4. Large staff and overhead

5.

6.

7.

The Fixer1. Singular focus on qualifi ed retirement plans2. Most experienced, credentialed advisor to fi x employers’s current plan3. Focus is on consistency, high standards and fi nding employers who fi t their model4. Small staff and low overhead

5.

6.

7.

The Connector1. personal wealth Management is core offering2. All other services including retirement plans are secondary3. Focus is on meeting as many needs as possible for high net worth individuals

and connecting them with multiple professionals4. Medium staff and overhead, decisions to outsource and partner versus retaining

in house

5.

6.

7.

Advisors representing the following Broker-Dealers:

WORKSHEET

Workbook and Worksheets

RETIREMENTCPII N S T I T U T E

2

What is my billable hourly rate? Rethinking your profi tability starts with having a fi rm grasp on your desired and current hourly

billable rate. The fi rst step to increasing the profi tability of your retirement plan practice is to determine

your current billable hourly rate. Once you know your billable hourly rate, you can use it to make critical

decisions around hiring, partnering and outsourcing.

cALcULAtION

what is your desired billable hourly rate for your retirement plan efforts? . . $ per hour

what is your current billable hourly rate for your retirement plan efforts?

Annual revenue from retirement plans . . . . . . . . . . . . . . . . . . . . . . . . $

hours spent on your retirement plan practice each week . . . . . . . . . ÷ hours per week

x 50

hours spent on your retirement plan practice each year . . . . . . . . . . = hours per year

current billable hourly rate for retirement plan efforts . . . . . . . . . . . . . . . $ per hour

[annual revenue / annual hours]

how big is the gap between the desired and current billable hourly rate? . . . $ per plan

How do you increase your billable hourly rate?

there are several proven ways to close the gap. which of the following are most appealing?

Check all that apply.

Hire employees to complete tasks that cost less to deliver than your current billable hourly rate.

Hire 1099 independent contractors to complete tasks that cost less to deliver than your current billable hourly rate.

Outsource to a business that focuses on specifi c activities such as prospecting, marketing, etc.

Partner with a related business professional who can deliver quality services in a way that upholds your high levels of service and rewards you with direct compensation or referrals. (Examples of related businesses: Wealth Management or Employee Benefi ts.)

Partner with CPI—a full service retirement plan service provider—who can assist in completing certain activities such as employee education, fi duciary service support and fi nals presentations.

Now how much higher can you raise your billable hourly rate?

WORKSHEET RETIREMENTCPII N S T I T U T E

4

Retirement Plan Profitability Analysis Make sure you don’t get paid less than your desired billable hourly rate by completing this worksheet.

plan name: today’s date:

Now how do you want to spend that time?

Knowing that you only have X hours to devote to this plan each year, be proactive and plan exactly how you are going to spend those hours by entering the number of hours per activity until you have reached your maximum annual time commitment. For any activity left blank, the next worksheet can help identify to whom you will turn to fi ll the gap.

cAtEgORIES cORE ActIVItY hOURS

prospecting/pre-sale

plan data collection and aggregation

cold calling, Appointment scheduling

prospect meeting

Finals presentation

general plan governance

plan design and demographic review

IpS development and support

communication strategy

Fiduciary review quarterly and annually

Investment governance

Fund analysis

Model portfolios

Investment recommendations and implementation

Investment menu monitoring

3(21) and 3(38) investment co-fi duciary services

Employee education

Initial and new enrollment support

Ongoing education and support

One-on-one meetings; fi nancial planning

participant customer service

Outcome-based support; success measurement

Vendor management

tpA relationship management

Fund relationship management

Due diligence

Problem solving; communication

Employer relationship management

Fiduciary guidance/education (fi duciary fi le, documented process, etc.)

Fee education (sub-TA, 12b-1s, expense ratios, advisor comp, RKer fees, administration fees)

408(b)(2), 404a-5, 404(c) support and education

Quarterly meetings; annual due diligence

tracking federal regulations and legislation

tOtAL

cALcULAtION

Annual plan revenue (fl at fee or basis points) . . . . . . . . . . . . . . . . . . . . . . . $ $ plan assets x bps = per year or fl at fee per year

Desired billable hourly rate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ calculate using the “what’s is my billable hourly rate?” worksheet.

My maximum annual time commitment for this plan . . . . . . . . . . . . . . . . . . . hours

WORKSHEET

Job Descriptions

“Operating in the qualified retirement plan business is not for the faint of heart. As a registered corporate coach, my sole purpose is to help advisors succeed in this challenging industry. All of our resources are developed to assist the retirement plan advisor with the unique issues they face with a focus on growabiliity, sustainability and profitability.”

~ Randy Fuss, CFP©, Registered Corporate Coach™, Practice Management Consultant

RETIREMENTCPII N S T I T U T E

5 FOR tRAININg pURpOSES ONLY. Not to be viewed or distributed to the general public.

What are leading retirement plan advisors doing to increase their profitability? Rethink it. Below are a few ways leading advisors have assigned activities to increase their retirement plan practice profi tability. Think of the varying amount of revenue received from each retirement plan and start with the REtAIN column. will you be providing each core activity for ALL of your plans, MOSt of your plans, only SOME of your plans or NONE of your plans? Place an A=All, M=Most, S=Some, N=None. For each activity not marked with an A, in the hIRE StAFF, OUtSOURcE and pARtNER columns, write in the name of each source you can use i.e., Finals presentation under the PARTNER column, write CPI.

cAtEgORIES cORE ActIVItY REtAIN hIRE StAFF OUtSOURcE pARtNER

prospecting/pre-sale

plan data collection and aggregation

cold calling, Appointment scheduling

prospect meeting

Finals presentation

general plan governance

plan design and demographic review

IpS development and support

communication strategy

Fiduciary review quarterly and annually

Investment governance

Fund analysis

Model portfolios

Investment recommendations and implementation

Investment menu monitoring

3(21) and 3(38) investment co-fi duciary services

Employee education

Initial and new enrollment support

Ongoing education and support

One-on-one meetings; fi nancial planning

participant customer service

Outcome-based support; success measurement

Vendor management

tpA relationship management

Fund relationship management

Due diligence

Problem solving; communication

Employer relationship management

Fiduciary guidance/education (fi duciary fi le, documented process, etc.)

Fee education (sub-TA, 12b-1s, expense ratios, advisor comp, RKer fees, administration fees)

408(b)(2), 404a-5, 404(c) support and education

Quarterly meetings; annual due diligence

tracking federal regulations and legislation

WORKSHEET

Unsure which activities you should consider delegating to whom? contact your cpI Sales team to discuss which activities are essential to retain, and which activities you can offer a better solution. they can share ideas and resources that may help you rethink your retirement plan profi tability.

800.279.9916 ext. 765

CPI Qualified Plan Consultants, Inc., a member of CUNA Mutual Group | Thought Leadership7

RETIREMENTCPII N S T I T U T E

cpI Qualified plan consultants, Inc. is a member of cUNA Mutual group, a leading insurance and fi nancial services organization based in Madison, wI.

1809 24th Street | PO Box 1167Great Bend, KS 67530-1167www.cpiqpc.com®

800.279.9916 ext. 765

2011750.4-0313 © CPI, 2013 All Rights Reserved.

Did you know CPI Qualifi ed Plan Consultants, Inc., a member of CUNA Mutual, provides a complete suite of retirement plan solutions?

Learn more about how CPI can help you grow your retirement plan business.

Call today: 800.279.9916 ext. 765

Visible Branding

Understand the power of personal branding

Commit to the four disciplines of brand thinking

Build your brand equity account

Utilize brand audits to identify gaps

Map your personal brand to sales strategies

FOR ADVISOR USE ONLY. NOt tO bE VIEwED bY OR DIStRIbUtED tO thE gENERAL pUbLIc.

1. How do you reposition your current brand for success in the retirement plan business?

2. How does your brand need to change without abandoning what you are already known for?

3. How do you need to communicate your brand to new retirement plan prospects?

this program will teach advisors how to leverage their existing personal brand power so they can grow

their retirement plan business. Advisors will learn the principles of personal branding, how top

retirement plan advisors use personal branding to develop and grow their practice, and how

to execute a “Personal Brand Action Plan.”

Brand Yourself for Retirement Plan Sales Success

Handouts Presentation

Workbook

People driven. Outcome focused.

Brand.1-0113 CPI

RETIREMENTCPII N S T I T U T E

“Branding is all about discovering and staying consistent to a core value. Find your brand, hone it, and stay true to it.”

— Donny Deutsch in Success Magazine, December, 2008

Brand Yourself for Business Success

Visible vs. Invisible Branding

Invisible Branding

S Service standards

S Staff training

S Branch relationships

S Internal communication

S Business planning

S Personal education

S Technical proficiency

S Vendor selection

S Community involvement

Visible Branding

S Marketing collateral

S Point of sale material

S Awards and recognition

S Professional designations

S Personal appearance

S Advertising

S Communications

S Web presence

Visible Branding involves all

touchpoints relative to the client

experience and tangibly demonstrate

your personal brand attributes,

building brand equity.

Invisible Branding involves the

intangible aspects of the client

experience. These critical elements of

brand equity add up to what is often

described as professionalism.

1809 24th Street | PO Box 1167Great Bend, KS 67530-1167www.cpiqpc.com800.491.7859 or 800.279.9916 ext. 765

Getting Started1. Identify brand touchpoints.

2. Rate your brand experience from the client’s point of view: Positive, Neutral or Negative.

3. Identify gaps between your brand promise and the actual experience.

4. Prioritize the gaps and areas needing improvement.

5. Set improvement objectives and monitor progress.

Brand Experience AuditVisible Branding how would clients rate your brand experience?

1-positive | 2-Neutral | 3-Negative

forpriorityattention

Brand Look Brand Appearancepersonal appearance

Offi ce or meeting environment

Advertising

professional designations

web presence

communications

Marketing collateral

presentation material

point of purchase material

client appreciation

Service standards

Staff training

Center of Infl uence development

Internal communications

business planning

continuing education

Technical profi ciency

Vendor selection

community involvement

plan monitoring

FOR TRAINING PURPOSES ONLY. NOT TO BE VIEWED BY OR DISTRIBUTED TO THE GENERAL PUBLIC.

cpI Qualified plan consultants, Inc. is a member of CUNA Mutual Group, a leading insurance and fi nancial services organization based in Madison, wI.

Identify gaps between your brand promise and your brand experience

Regularly monitor and refocus your brand

brand audits benchmark the current position and show what your branding efforts must accomplish in the future

2011750.2-0313 © CPI, 2013 All Rights Reserved.

People driven. Outcome focused.

Brand.2-0113 CPI

RETIREMENTCPII N S T I T U T E

Strong Brands Evolve Over Time

S This evolution may result in the extension of your brand to additional market segments or specialized

markets.

S This evolution will impact the way you communicate your brand.

S This evolution may require refocusing or augmenting your brand attributes as you continue to grow

your career.

Brand Yourself for Business Success

Build a Strong Brand

A Brand Audit benchmarks a current position and shows you what your branding efforts must accomplish in the future.

A Personal Brand AuditAssessing your brand starts with an audit of your personal style. Your brand equity is like a bank account.

Everything you say or do either adds to or takes away from your brand equity bank account.

Scoring Options:

Think about how others view you. Their opinions will be positive, neutral or negative. Score each statement

with a (1) positive, (2) neutral, (3) negative.

Does your personal style create

desired expectations?

Smart

Trustworthy

Credible

Disciplined

Professional

Dedicated

Authentic

What impression do the following convey to others about you?

Your handshake

Your office

Your clothes

Your table manners

Your friends

Your listening skills

Your business card

Your voice

Your car

Your reading habits

Your articulation

Your hair

Your teeth

Your weight

People driven. Outcome focused.

Brand Yourself for Retirement Plan Sales Success

RETIREMENTCPII N S T I T U T E

FOR ADVISOR USE ONLY. NOt tO bE VIEwED OR DIStRIbUtED tO thE gENERAL pUbLIc.

WORKBOOK

For advisor use only. Not to be viewed or distributed to the general public.

CPI is a member of CUNA Mutual Group.

Brand Yourself for Retirement Plan Sales Success

Presented by Randy Fuss, CFP©

Registered Corporate Coach™Practice Management Consultant

5 | FOR ADVISOR USE ONLY. NOT TO BE VIEWED OR DISTRIBUTED TO THE GENERAL PUBLIC.

this is a product.

this is a logo.

this is a brand.

Harley DavidsonHarley Davidson’’s mission statement is:s mission statement is:““We Fulfill Dreams.We Fulfill Dreams.””

What is a Brand?

9 | FOR ADVISOR USE ONLY. NOT TO BE VIEWED OR DISTRIBUTED TO THE GENERAL PUBLIC.

Who are you?

What do you do?

YOURBRAND

Value Proposition-

Promise

Differentiation-Expectation

Execution-Relationship

How Are You

Different?

The Elements of a Personal Brand

FOR ADVISOR USE ONLY. NOt tO bE VIEwED bY OR DIStRIbUtED tO thE gENERAL pUbLIc.1

Branding 101A Brand Audit benchmarks a current position and shows you what your branding eff orts must accomplish in the future.

The Authentic Man: Dan Acedo10 Truth’s About Building Brand Equity

1. Really listen.

2. Gain trust fi rst.

3. the client is the really important person in the room.

4. take good care of people.

5. Do what you say you are going to do, then do a little more.

6. Answer your own phone and return calls within 24 hours.

7. try to see three people face to face every day.

8. You can’t be all things to all people.

9. Own the relationship.

10. be the best you you can be today.

4 | For training purposes only. Not to be viewed by or distributed to the general public.

Personal Branding ROI

Fame and fortune

Power and influence

The ability to drive positive change

Career security and stability

The power of pull*

* Tim O’Brien, The Power of Personal Branding, 2007

4 Disciplines of Personal Branding

Differentiate yourself

Leverage partnerships

Exercise creativity

Commit to your brand

For training purposes only. Not to be viewed by or distributed to the general public. | 5

Curtis Farrell: Become an Expert

Dan Acedo: The Authentic Man

10. Really listen.

9. Gain trust first.

8. The client is the really important person in the room.

7. Take good care of people.

6. Do what you say you are going to do, then do a little more.

5. Answer your own phone and return calls within 24 hours.

4. Try to see three people face to face everyday.

3. You can’t be all things to all people.

2. Own the relationship.

1. Be the best you, you can be today.

10 Truth’s About Building Brand Equity

Curtis Farrell “Become an expert.”

4 | For training purposes only. Not to be viewed by or distributed to the general public.

Personal Branding ROI

Fame and fortune

Power and influence

The ability to drive positive change

Career security and stability

The power of pull*

* Tim O’Brien, The Power of Personal Branding, 2007

4 Disciplines of Personal Branding

Differentiate yourself

Leverage partnerships

Exercise creativity

Commit to your brand