trim company focus - trimegah · trim company focus - jul 10, 2012 2 the operator of high quality...

TRANSCRIPT

-

100

200

300

400

500

600

09/0

4/20

12

09/0

6/20

12

-

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

Volume Price

Muhamad Makky [email protected]

Richardo Putra [email protected]

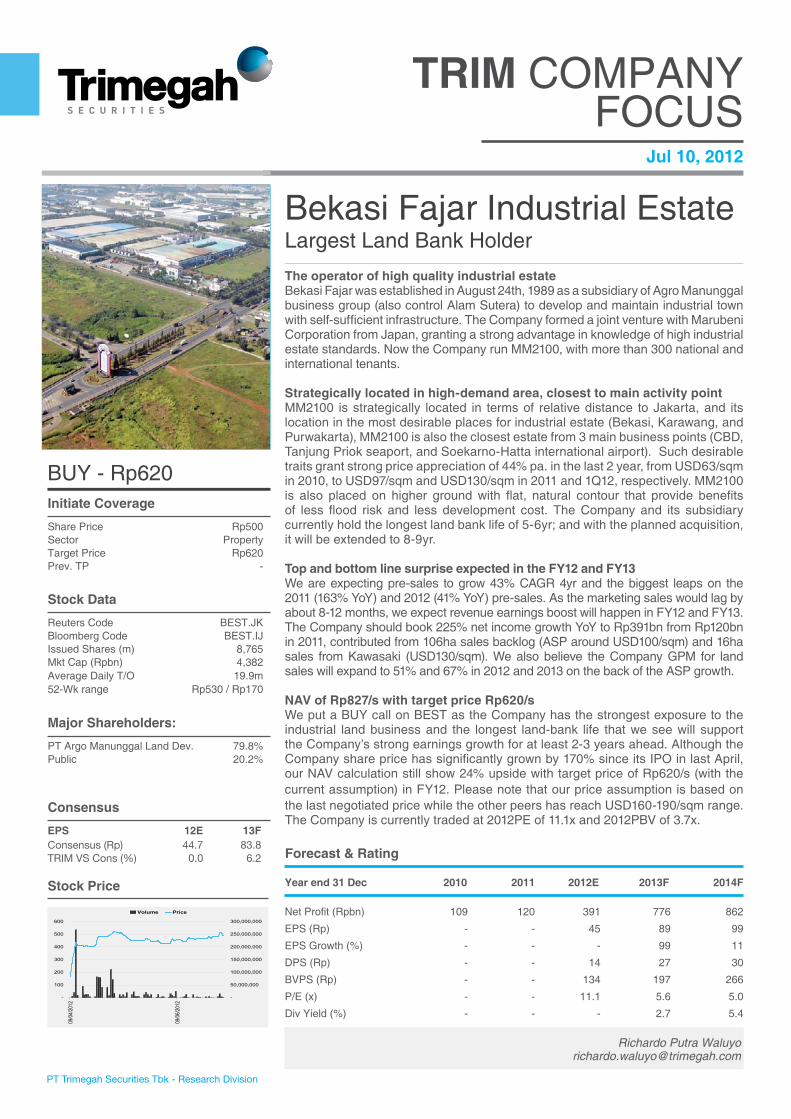

Bekasi Fajar Industrial EstateLargest Land Bank Holder

Net Profit (Rpbn) 109 120 391 776 862

EPS (Rp) - - 45 89 99

EPS Growth (%) - - - 99 11

DPS (Rp) - - 14 27 30

BVPS (Rp) - - 134 197 266

P/E (x) - - 11.1 5.6 5.0

Div Yield (%) - - - 2.7 5.4

The operator of high quality industrial estateBekasi Fajar was established in August 24th, 1989 as a subsidiary of Agro Manunggal business group (also control Alam Sutera) to develop and maintain industrial town with self-sufficient infrastructure. The Company formed a joint venture with Marubeni Corporation from Japan, granting a strong advantage in knowledge of high industrial estate standards. Now the Company run MM2100, with more than 300 national and international tenants.

Strategically located in high-demand area, closest to main activity pointMM2100 is strategically located in terms of relative distance to Jakarta, and its location in the most desirable places for industrial estate (Bekasi, Karawang, and Purwakarta), MM2100 is also the closest estate from 3 main business points (CBD, Tanjung Priok seaport, and Soekarno-Hatta international airport). Such desirable traits grant strong price appreciation of 44% pa. in the last 2 year, from USD63/sqm in 2010, to USD97/sqm and USD130/sqm in 2011 and 1Q12, respectively. MM2100 is also placed on higher ground with flat, natural contour that provide benefits of less flood risk and less development cost. The Company and its subsidiary currently hold the longest land bank life of 5-6yr; and with the planned acquisition, it will be extended to 8-9yr.

Top and bottom line surprise expected in the FY12 and FY13 We are expecting pre-sales to grow 43% CAGR 4yr and the biggest leaps on the 2011 (163% YoY) and 2012 (41% YoY) pre-sales. As the marketing sales would lag by about 8-12 months, we expect revenue earnings boost will happen in FY12 and FY13. The Company should book 225% net income growth YoY to Rp391bn from Rp120bn in 2011, contributed from 106ha sales backlog (ASP around USD100/sqm) and 16ha sales from Kawasaki (USD130/sqm). We also believe the Company GPM for land sales will expand to 51% and 67% in 2012 and 2013 on the back of the ASP growth.

NAV of Rp827/s with target price Rp620/s We put a BUY call on BEST as the Company has the strongest exposure to the industrial land business and the longest land-bank life that we see will support the Company’s strong earnings growth for at least 2-3 years ahead. Although the Company share price has significantly grown by 170% since its IPO in last April, our NAV calculation still show 24% upside with target price of Rp620/s (with the current assumption) in FY12. Please note that our price assumption is based on the last negotiated price while the other peers has reach USD160-190/sqm range. The Company is currently traded at 2012PE of 11.1x and 2012PBV of 3.7x.

BUY - Rp620

Stock Price

Jul 10, 2012

TRIM COMPANYFOCUS

Year end 31 Dec 2010 2011 2012E 2013F 2014F

Forecast & Rating

Reuters Code BEST.JKBloomberg Code BEST.IJIssued Shares (m) 8,765Mkt Cap (Rpbn) 4,382Average Daily T/O 19.9m52-Wk range Rp530 / Rp170

Stock Data

PT Argo Manunggal Land Dev. 79.8%Public 20.2%

Major Shareholders:

EPS 12E 13FConsensus (Rp) 44.7 83.8TRIM VS Cons (%) 0.0 6.2

Consensus

Share Price Rp500Sector PropertyTarget Price Rp620Prev. TP -

Initiate Coverage

XXX

TRIM Company Focus - Jul 10, 2012

2

The operator of high quality industrial estate

Bekasi Fajar was established in August 24th, 1989 as one of the Agro Manunggal business group (also control Alam Sutera) subsidiaries. The Company’s main activity is developing and managing industrial town with self-sufficient infrastructure. The Company formed a joint venture with Marubeni Corporation from Japan, under one company named PT Megalopolis Manunggal Industrial Development (MMID). Together, the Company pioneered the industrial estate in the west of Cikarang and developed around 2500ha master plan of industrial townships. Alas, when Asian Financial Crisis striked Indonesia in 1998, Marubeni decided to cease any further expansion. Bekasi Fajar then sold its stake in MMID to PT Jatiwangi Utama in 2011, afterwards it expanded organically to MM2100 industrial town, which still has strong demand.

Director and management backgroundThe Company is known for having more than 20 years of experience in developing and managing big-scale industrial estates. The management now led by:

Hungkang Sutedja: also a son of the Nin King family. As a CEO he earned his Finance BoS degree from University of Missouri and has been in the industrial estate business since 1996. He was also appointed as the CEO of PT Daya Sakti, PT Manunggal Prime Development, PT Daya Manunggal, PT Delta Mega Persada, PT Putra Manunggal Energy, and BMIE up until current date.

Hendra Kurniawan: was appointed as Director in charge of marketing, estate, and development in 2011, and also serves as the Corporate Secretary of Alam Sutera He earned his Accounting Bachelor degree from University of Indonesia. Past positions held were the associate director of RSM AAJ Batavia and a member of theAudit Comitee of PT Krakatau Steel.

Wilson Effendy: was appointed as Director in charge of finance, operations, and supports in 2011. He earned his Accounting Bachelor degree in University of Tarumanegara and Master of Business Administration from California State University. His past experiencea were Finance Director in Uresources Group, Head of Banking in Asia Pulp Paper, Deputy GM in Asia Pulp Paper, and Senior Business Financial Analyst of Barclays Global Investors.

Source: TRIM Research, Company

Company shareholder

BEST

BMIE

AMLD*

The Ning King & Family

Hungkang Sutedja

Public

100%

79.78% 0.08% 20.14%

99.98% 0.02%

TRIM Company Focus - Jul 10, 2012

3

Complete infrastructure to efficiently support its tenant productivityJV with Marubeni in developing MMID unwittingly granted the Company a strong advantage because the Company can adopted Japanese high quality and standards of industrial estate. Marubeni Corporation, a well-known Japanese company established since 1858 with expertise in industrial estate, infrastructure, and construction has designed MMID (and the rest MM2100) under 2500ha master plan. The Company prioritized on upfront investment initially to build main infrastructures, facilities, and management of their industrial town, before starting to market commercially.

From the infrastructure perspective, MM2100 has decent facilities that supports its tenant. Highway access has provided the Company for easier entry to MM2100. Electricity is directly supplied by PLN and private electricity company, Cikarang Listrindo. MM2100 is also passed by PGN gas line that makes it easier for the tenants to receive gas supply in a efficient way. Standardized water is easily acquired from Citarum and Cikarang River, which are located arround the area. While for the waste management, MM2011 benefits from Sadang and Cikedon River that are directly flowing to the waste water treatment area. The other examples of the Japanese high standards are shown from the easy access from toll-road, first-class main road (with width around 41-50m), and 7 man—made lakes spread in the estate to control flood and waste. All of this advantages have enabled the Company to operate the estate efficiently, with around 80% gross margin in maintenance fee.

Source: Company

Highway access

Highway access . MM2100 Entrance

MM2100 entrance

Source: Company

Electricity

Water waste treatment

TRIM Company Focus - Jul 10, 2012

4

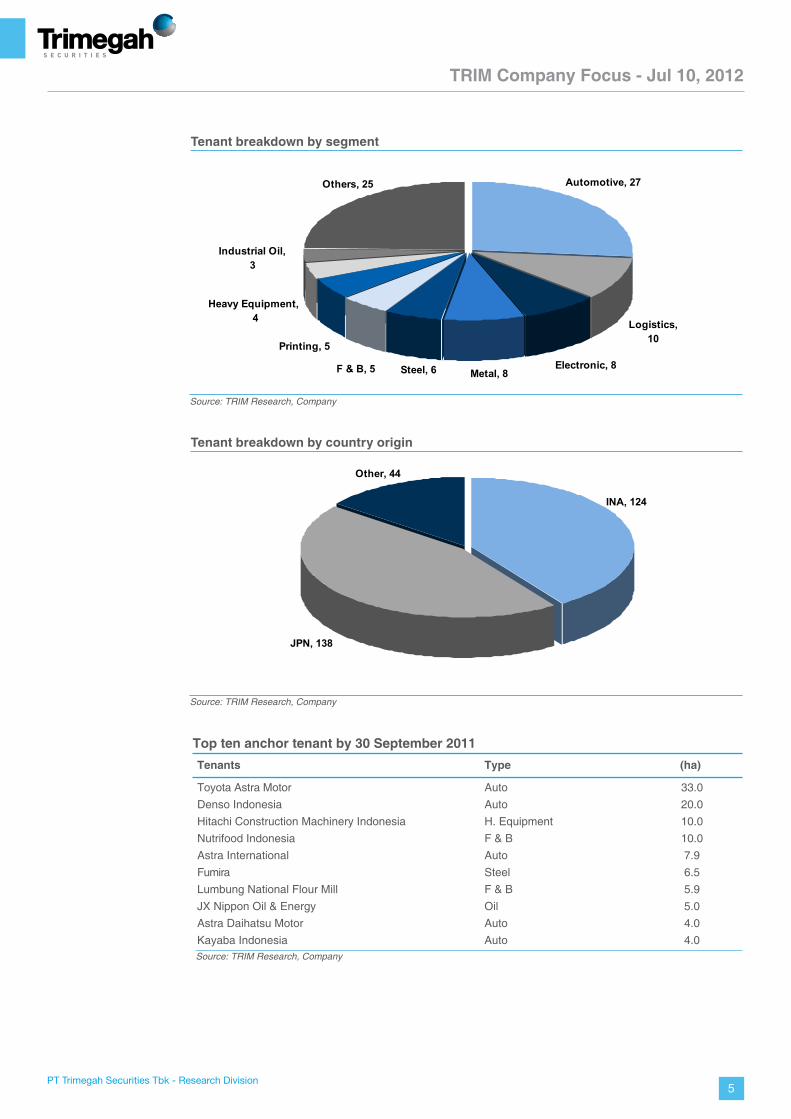

Diversified tenant segmentMM2100 emphasized their focus on middle-upper level manufacturers and has been occupied by more than 300 national and international tenants such as Marubeni Chemicals Group, Yamaha Music Manufacturing, Astra Honda Motor, Denso, and Hitachi. With the current market, where industrial land business is a landlord market, the Company has the power to select its tenants. Tenants with reputable name and tenants that has the ability to drive demand on the estate are prioritized. MM2100 is mostly occupied by light industry thus not emitting high pollution, so that F&B industries may open new factories or expand in MM2100. We also notice that most tenants are coming from Japan (45%) and then followed by Indonesia (40%).

Source: TRIM Research, Company

MM2100 master plan map

This 30-40ha area is preserved for commercial area. The location is near the entrance and currently occupied by a Japanese restaurant, golf and driving range, and retail shops.The Company is planning to develop several budget hotels, a serviced apartment, and other supporting facilities.

The pink area is showing MMID area with around 800ha that is already sold out. Although the Company is not managing this area anymore, certain benefits like: further expansions from tenants in this area are potential buyers for MM2100.

The blue and white areas are managed by the Company (BFIE) and through its subsidiary (BMIE), with 1,100ha licensed area for development.

Source: TRIM Research, Company

Japanese restaurant Golf and driving range

TRIM Company Focus - Jul 10, 2012

5

Source: TRIM Research, Company

Tenant breakdown by segment

Tenants Type (ha)

Toyota Astra Motor Auto 33.0 Denso Indonesia Auto 20.0 Hitachi Construction Machinery Indonesia H. Equipment 10.0 Nutrifood Indonesia F & B 10.0 Astra International Auto 7.9 Fumira Steel 6.5 Lumbung National Flour Mill F & B 5.9 JX Nippon Oil & Energy Oil 5.0 Astra Daihatsu Motor Auto 4.0 Kayaba Indonesia Auto 4.0

Top ten anchor tenant by 30 September 2011

Source: TRIM Research, Company

Source: TRIM Research, Company

Tenant breakdown by country origin

INA, 124

JPN, 138

Other, 44

Steel, 6F & B, 5

Printing, 5

Industrial Oil, 3

Heavy Equipment, 4

Metal, 8 Electronic, 8

Logistics, 10

Automotive, 27Others, 25

TRIM Company Focus - Jul 10, 2012

6

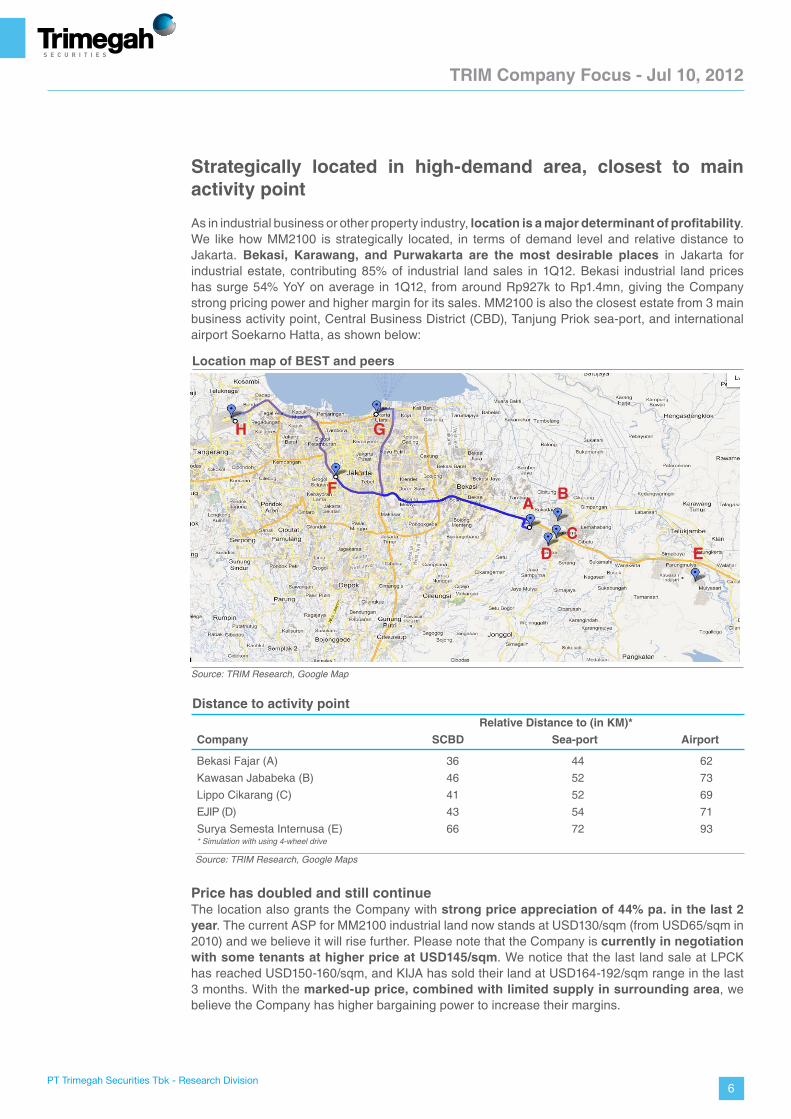

Strategically located in high-demand area, closest to main activity point

As in industrial business or other property industry, location is a major determinant of profitability. We like how MM2100 is strategically located, in terms of demand level and relative distance to Jakarta. Bekasi, Karawang, and Purwakarta are the most desirable places in Jakarta for industrial estate, contributing 85% of industrial land sales in 1Q12. Bekasi industrial land prices has surge 54% YoY on average in 1Q12, from around Rp927k to Rp1.4mn, giving the Company strong pricing power and higher margin for its sales. MM2100 is also the closest estate from 3 main business activity point, Central Business District (CBD), Tanjung Priok sea-port, and international airport Soekarno Hatta, as shown below:

Price has doubled and still continueThe location also grants the Company with strong price appreciation of 44% pa. in the last 2 year. The current ASP for MM2100 industrial land now stands at USD130/sqm (from USD65/sqm in 2010) and we believe it will rise further. Please note that the Company is currently in negotiation with some tenants at higher price at USD145/sqm. We notice that the last land sale at LPCK has reached USD150-160/sqm, and KIJA has sold their land at USD164-192/sqm range in the last 3 months. With the marked-up price, combined with limited supply in surrounding area, we believe the Company has higher bargaining power to increase their margins.

Relative Distance to (in KM)*Company SCBD Sea-port Airport

Bekasi Fajar (A) 36 44 62 Kawasan Jababeka (B) 46 52 73 Lippo Cikarang (C) 41 52 69 EJIP (D) 43 54 71 Surya Semesta Internusa (E) 66 72 93 * Simulation with using 4-wheel drive

Distance to activity point

Source: TRIM Research, Google Maps

Source: TRIM Research, Google Map

Location map of BEST and peers

A B

G

DC

E

F

H

TRIM Company Focus - Jul 10, 2012

7

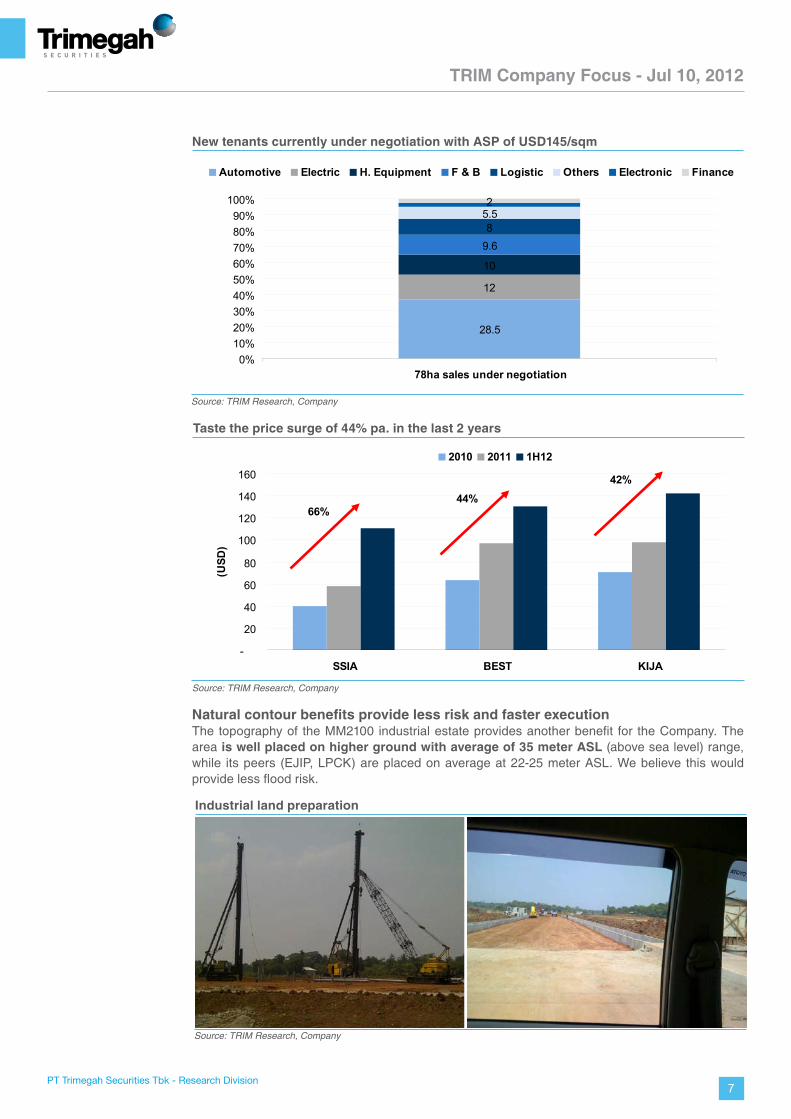

Natural contour benefits provide less risk and faster executionThe topography of the MM2100 industrial estate provides another benefit for the Company. The area is well placed on higher ground with average of 35 meter ASL (above sea level) range, while its peers (EJIP, LPCK) are placed on average at 22-25 meter ASL. We believe this would provide less flood risk.

Source: TRIM Research, Company

New tenants currently under negotiation with ASP of USD145/sqm

28.5

12

10

9.68

5.52

0%10%20%30%40%50%60%70%80%90%

100%

78ha sales under negotiation

Automotive Electric H. Equipment F & B Logistic Others Electronic Finance

Source: TRIM Research, Company

Taste the price surge of 44% pa. in the last 2 years

-

20

40

60

80

100

120

140

160

SSIA BEST KIJA

(USD

)

2010 2011 1H12

66%44%

42%

Source: TRIM Research, Company

Industrial land preparation

TRIM Company Focus - Jul 10, 2012

8

Another benefit is coming from the flat contour of the MM2100 land. One of the issues faced by industrial land player is land processing, where land is flattened to be ready for the plant construction. With flat contour, the Company can finish land preparation faster (ranging for 8-12 months), with less cost (around USD13-15, vs peers reaching USD20/sqm) hence recognized revenue and receiving full cash payment faster. In contrast, other areas such as Karawang, has uneven contour that could extend land processing to 2 years.

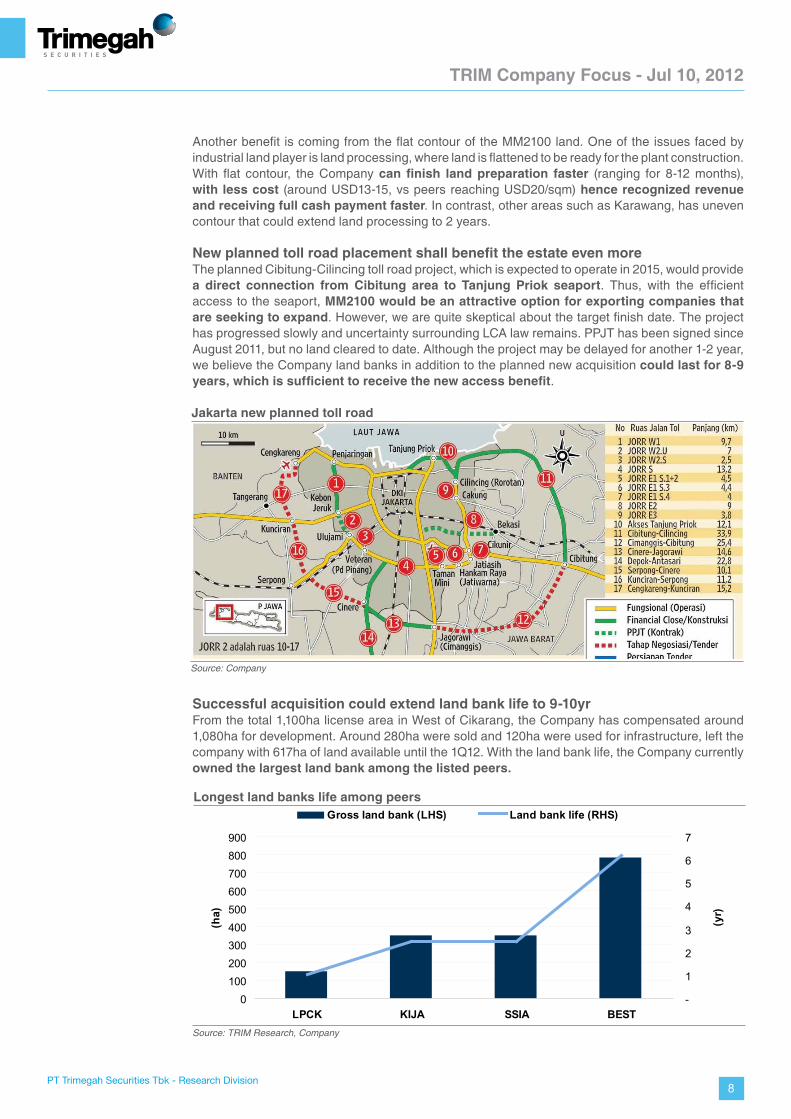

New planned toll road placement shall benefit the estate even more The planned Cibitung-Cilincing toll road project, which is expected to operate in 2015, would provide a direct connection from Cibitung area to Tanjung Priok seaport. Thus, with the efficient access to the seaport, MM2100 would be an attractive option for exporting companies that are seeking to expand. However, we are quite skeptical about the target finish date. The project has progressed slowly and uncertainty surrounding LCA law remains. PPJT has been signed since August 2011, but no land cleared to date. Although the project may be delayed for another 1-2 year, we believe the Company land banks in addition to the planned new acquisition could last for 8-9 years, which is sufficient to receive the new access benefit.

Successful acquisition could extend land bank life to 9-10yr From the total 1,100ha license area in West of Cikarang, the Company has compensated around 1,080ha for development. Around 280ha were sold and 120ha were used for infrastructure, left the company with 617ha of land available until the 1Q12. With the land bank life, the Company currently owned the largest land bank among the listed peers.

Source: TRIM Research, Company

Longest land banks life among peers

0100200300400500600700800900

LPCK KIJA SSIA BEST

(ha)

-

1

2

3

4

5

6

7

(yr)

Gross land bank (LHS) Land bank life (RHS)

Source: Company

Jakarta new planned toll road

TRIM Company Focus - Jul 10, 2012

9

To keep up with the strong demand for industrial lands, the Company is on the way to acquire 400ha license (gross) on the area south of MM2100. The acquisition price is expected to range around Rp220-250k and targeted to replenish the same amount of land bank that were sold, or around 100ha pa.

Escalating acquisition price and land bank monetization riskThe strategic location of the Company in the other hand could bring risk to the acquisition process. MM2100 (KM24) is located close to Grand Wisata (KM21) and Summarecon Bekasi development (KM15), where this proximity to those prominent residential developers might bring domino effect to the land price in the area of BEST’s acquisition target. Summarecon Bekasi and Grand Wisata priced their land at around Rp2.5-3.5mn. This might encourage landowners whose land around MM2100 to sell at higher price to the Company.

We also notice MM2100 is facing the challenge to monetize their huge land bank, with a few amount of anchor tenants that could bring tens of hectares demand to the estate. But we believe the supply of industrial area is scarce and left the investor with little option. MM2100 strategic location and facilities, with its huge amount of space is surely encourage investment to the estate.

Source: TRIM Research, Company

Proximity to prominent developers might escalate the land price around

Summarecon Bekasi

Grand Wisata

MM 2100

TRIM Company Focus - Jul 10, 2012

10

Source: TRIM Research, Company

Earnings boost in FY12 and FY13 as huge amount of sales backlog recognized

165155145

97

6362

-

200

400

600

800

1,000

1,200

1,400

1,600

2007 2008 2009 2010 2011 2012F 2013F 2014F

(Rpb

n)

-20406080100120140160180

(in U

SD)

Revenue Gross Profit EBITDA Net Income ASP USD/sqm

Expected top and bottom line surprises in the FY12 and FY13

We are expecting pre-sales to grow 43% 4yr CAGR 2010-14 and the biggest scale is in 2011 (163% YoY) and 2012 (41% YoY) pre-sales. As marketing sales would lag about 8-12 months, we expect revenue boost would happen in FY12 and FY13. We assumed slow growth on our price assumption in 2013 and 2014 to address uncertainty effect from the coming presidential election, and in turn, to the investment climate.

We expect the Company to book Rp391bn net income this year, 225% YoY growth compared to 2011 of Rp120bn. This earnings jump is contributed by 106ha sales backlog (ASP around USD100/sqm) and 16ha sales from Kawasaki (USD130/sqm) to be booked this year.

Source: TRIM Research, Company

Massive pre-sales growth on 2011 and 2012 inline with the growing pricing power

165155

145

97

63

-

200

400

600

800

1,000

1,200

1,400

1,600

2010 2011 2012F 2013F 2014F

(Rpb

n)

-

20

40

60

80

100

120

140

160

180

Marketing sales Revenue ASP USD/sqm

TRIM Company Focus - Jul 10, 2012

11

Profitability is expected to peak in 2013We expect the Company to post significant increase in FY12 and FY13 ROAE and ROAA, as pre-sales with higher price increase in FY11 and FY12 are booked. The profitability ratios decrease in FY2014 as we use slow price growth assumption in that year.

Major GPM expansion for land sales, while others segment stabilizedLower gross profit margin (GPM) for land sales in 2010 and 2011 of 59% and 40.7% respectively, occured due to: 1) the Company sold around 20ha at book value cost to MMID, for their requirement in green area space. 2) giving discount price to some anchor tenants. But we believe the Company GPM for land sales will expand to 51% and 67% in 2012 and 2013 on the back of the ASP growth. No significant expansion in maintenance and service since this segment already has high margin and relatively stable recurring income.

Source: TRIM Research, Company

ROAE and ROAA

-

10.0

20.0

30.0

40.0

50.0

60.0

2007 2008 2009 2010 2011 2012 2013 2014

(%)

ROAE ROAA

Source: TRIM Research, Company

GPM breakdown by segment Blended profitability margins

0

10

20

30

40

50

60

70

80

2010 2011 2012 2013 2014

(%)

Gross Margins EBITDA MarginsNet Margins

-10.020.030.040.050.060.070.080.090.0

100.0

2010 2011 2012 2013 2014

(%)

Sales of land MaintananceService

TRIM Company Focus - Jul 10, 2012

12

Further funding would not be an issue until 2014We assume the Company will acquire 100ha of new land with acquisition price of Rp250k/sqm and increasing 15% pa, taking into account the escalating price for the Bekasi region. Cash needed for land processing is expected at Rp125k/sqm and increase inline with expected inflation rate. Opex is estimated to grow by 25% pa on average, driven by salary and commission growth. Capex totaling Rp50bn will be spent in 2012 and 2013 to build extra capacity for waste treatment to cope up with increasing number of tenants.

Expected dividend yield of 3% with the FY12 earningsThe Company dividend policy is to distribute 20% of its earnings if net income only reach below Rp200bn, or 30% if earnings reach above Rp200bn. With expected earnings of Rp391bn in FY12, the Company would distribute dividend of Rp13/s for FY12, reflecting 2.7% yield from the current price.

Source: TRIM Research, Company

Dividend yield for FY12, FY13 and FY14

-

50

100

150

200

250

300

2012 2013 2014

(Rp)

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

(%)

Dividend in Rpbn (LHS) DVPD (LHS) Yield (RHS)

Source: TRIM Research, Company

Net operating cash flow is sufficient for funding expansion and development

-100200300400500

600700800900

1,000

2012 2013 2014

Land acquisition Development Cost OPEX Capex Free Cash

(Rpb

n)

TRIM Company Focus - Jul 10, 2012

13

NAV of Rp827/s with target price Rp620/s

We put a BUY call on BEST as the Company has the strongest exposure to the industrial land business and the longest land bank life that we see will support the Company’s strong earning growth for at least 2-3 years ahead. Despite its risk on monetizing a large industrial land bank, we believe the current investment climate will support the sales, noting FDI and business expansion in Indonesia has reached USD40bn and not even a half of it has been realized, combined with limited supply from big listed industrial land player (<1000ha land supply in East Jakarta areas). We believe the industrial estate in Bekasi area will be the first pick for investor looking for expansion in Jakarta, considering the area currently holds the best infrastructure and facilities.

Although the Company share price has significantly grew by 170% since its IPO in last April, our NAV calculation still shows 24% upside with target price of Rp620/s (with the current assumption) in FY12. Please note that our price assumption is based on the last negotiated price (USD145/sqm) while BEST’s peers land prices in the vicinity has reach USD160-190/sqm range. The Company currently traded at 2012PE of 11.1x and 2012PBV of 3.7x.

NAV Calculation 2012

Land in the end year (net) MM2100 543ha

New area 70ha Price/sqm assumption USD145 / Rp1.33mn Development cost 819 NAV after tax 6.991 (+) Cash 451 (-) Debt 251 Shares 8.7bn RNAV/shares 827 Discount 25%Target Price 620

Show 24% upside in FY12 with current assumption

Source: TRIM Research

TRIM Company Focus - Jul 10, 2012

14

Balance Sheet (Rpbn)

Key Ratio Analysis

Interim Result (Rpbn)

1Q11 2Q11 3Q11 4Q11 1Q12

Sales - - - - -

Gross Profit - - - - -

Operating Profit - - - - -

Net Profit - - - - -

Gross Margins (%) - - - - -

Opr Margins (%) - - - - -

Net Margins (%) - - - - -

Income Statement (Rpbn)

Year end 31 Dec 2010 2011 2012E 2013F 2014F

Revenue 232 476 970 1,360 1,453

% growth 10.3 105.0 103.8 40.2 6.9

Gross Profit 137 194 503 919 1,012

Opr Profit 97 158 450 854 943

EBITDA 101 161 454 857 947

% growth (18.1) 59.5 181.6 88.8 10.5

Net Int Inc/(Exp) (22) (29) (28) (27) (27)

Gain/(loss) Forex 9 - - - -

Other Inc/(Exp) 48 14 14 14 14

Pre-tax Profit 123 143 437 840 931

Tax (14) (22) (46) (64) (68)

Minority Int. - - - - -

Extra. Items - - - - -

Net Profit 109 120 391 776 862

% growth 2.7 9.7 225.4 98.6 11.1

Year end 31 Dec 2010 2011 2012E 2013F 2014F

Profitability

Gross Margins (%) 59.0 40.7 51.8 67.6 69.6

Op Margins (%) 41.9 33.1 46.4 62.8 64.9

EBITDA Margins (%) 43.5 33.9 46.8 63.0 65.1

Net Margins (%) 47.1 25.2 40.3 57.1 59.3

ROE (%) 12.9 13.9 37.9 53.9 42.8

ROA (%) 9.4 8.5 20.7 32.0 28.4

Stability

Current Ratio (x) 21.2 19.5 15.7 18.9 24.1

Net Debt/Equity (x) 0.2 0.2 (0.2) (0.4) (0.5)

Int Coverage (x) 6.9 5.4 15.8 30.4 34.3

Efficiency

A/P days 56 74 64 64 64

A/R days 12 7 7 7 7

Inventory Days 3,290 1,876 1,187 1,345 1,468

Capital History

Date

10-Apr-12 IPO @ Rp170

Cash Flow (Rpbn)

Year end 31 Dec 2010 2011 2012E 2013F 2014F

Net Profit 107 109 120 391 776

Depr/Amort - 4 3 3 3

Others 2 3 4 5 6

Chg in Opr Ass&Liab (115) 217 523 184 26

CF's from Oprs (8) 330 647 579 805

Capex (4) 195 (3) (0) 0

Others 2 3 4 5 6

CF's from Investing 50 (334) (594) (69) (107)

Net Change in Debt (13) 120 48 - -

Others 2 3 4 5 6

CF's from Financing (20) (7) (17) (118) (233)

Net Cash Flow 22 (11) 36 391 466

Cash at BoY 13 36 24 60 451

Cash at EoY 35 24 60 451 917

Free Cashflow 42 (4) 52 510 699

Year end 31 Dec 2010 2011 2012E 2013F 2014F

Cash and Deposits 24 60 451 917 1,404

Inventory 859 1,450 1,519 1,625 1,775

Other Current Assets 13 30 58 80 86

Undevelopment Land - - - - -

Net Fixed Assets 75 74 71 67 64

Investment Properties - - - - -

Other Noncurrent Assets 217 30 30 30 30

Total Assets 1,187 1,644 2,129 2,720 3,359

ST Debt - - - - -

Other Current Liabilities 42 79 129 138 135

LT Debt 203 251 251 251 251

Other LT Liabs 103 419 581 620 658

Minority Interest 0 - - - -

Total Liabilities 348 749 961 1,009 1,045

Shareholder's Equity 840 895 1,168 1,711 2,314

Net Debt/(Cash) 179 191 (200) (666) (1,154)

Net Working capital 853 1,460 1,899 2,484 3,130

PT Trimegah Securities Tbk18th Fl, Artha Graha BuildingJl. Jend. Sudirman Kav. 52-53Jakarta 12190, INDONESIA

Tel : (6221) 2924 9088 Fax : (6221) 2924 9163

DISCLAIMER

This report has been prepared by PT Trimegah Securities Tbk on behalf of itself and its affiliated companies and is provided for information purposes only. Under no circumstances is it to be used or considered as an offer to sell, or a solicitation of any offer to buy. This report has been produced independently and the forecasts, opinions and expectations contained herein are entirely those of Trimegah Securities. While all reasonable care has been taken to ensure that information contained herein is not untrue or misleading at the time of publication, Trimegah Securities makes no representation as to its accuracy or completeness and it should not be relied upon as such. This report is provided solely for the information of clients of Trimegah Securities who are expected to make their own investment decisions without reliance on this report. Neither Trimegah Securities nor any officer or employee of Trimegah Securities accept any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents. Trimegah Securities and/or persons connected with it may have acted upon or used the information herein contained, or the research or analysis on which it is based, before publication. Trimegah Securities may in future participate in an offering of the

company’s equity securities.